Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

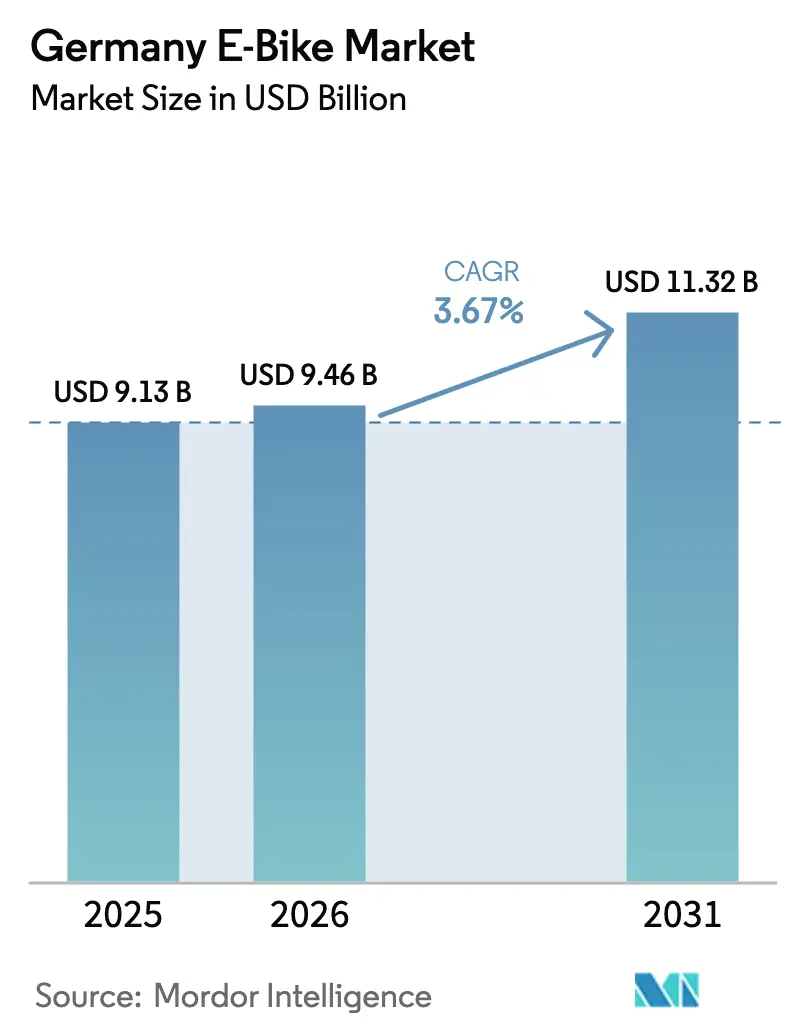

| Base Year Market Size (2025) | USD 9.13 Billion |

| Market Size (2026) | USD 9.46 Billion |

| Market Size (2031) | USD 11.32 Billion |

| Growth Rate (2026 - 2031) | 3.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany E-Bike Market Analysis by Mordor Intelligence

The German E-Bike market size is expected to grow from USD 9.13 billion in 2025 to USD 9.46 billion in 2026 and is forecast to reach USD 11.32 billion by 2031 at 3.67% CAGR over 2026-2031. Demand normalization after the pandemic surge now pivots growth toward steady replacement cycles, commercial fleet expansions, and incremental first-time adoption. Battery regulation, corporate mobility budgets, and improving infrastructure sustain forward momentum even as average selling prices stabilize. Competitive dynamics reflect consolidation, inventory rebalancing, and a decisive shift from volume chasing to profitability, yet the German E-Bike market continues to capture a notable share of total bicycle sales as of 2024.

Key Report Takeaways

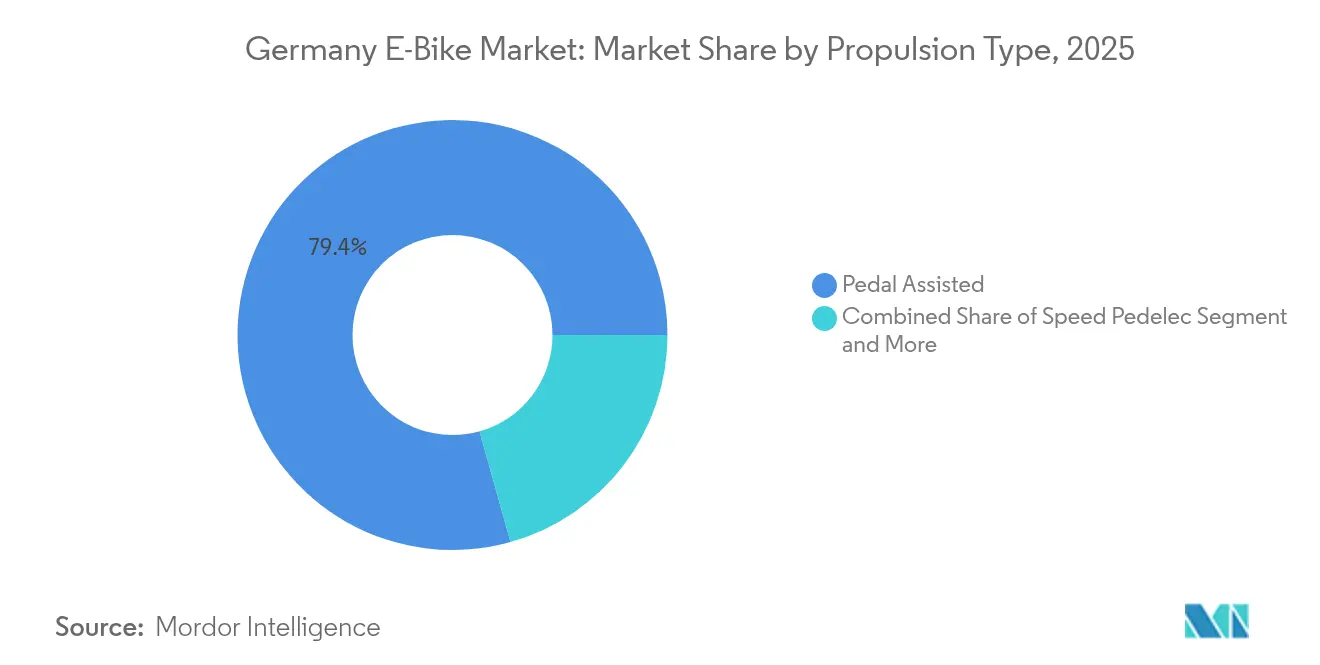

- By propulsion type, pedal-assisted systems led with 79.35% of the German E-Bike market share in 2025, while speed pedelecs are advancing at a 3.76% CAGR through 2031.

- By application type, city/urban riding held 70.92% of the German E-Bike market share in 2025, while cargo/utility records the highest projected 3.74% CAGR to 2031.

- By battery type, lithium-ion accounted for a 99.82% of the German E-Bike market share in 2025 and is projected to rise alongside a 3.67% CAGR to 2031.

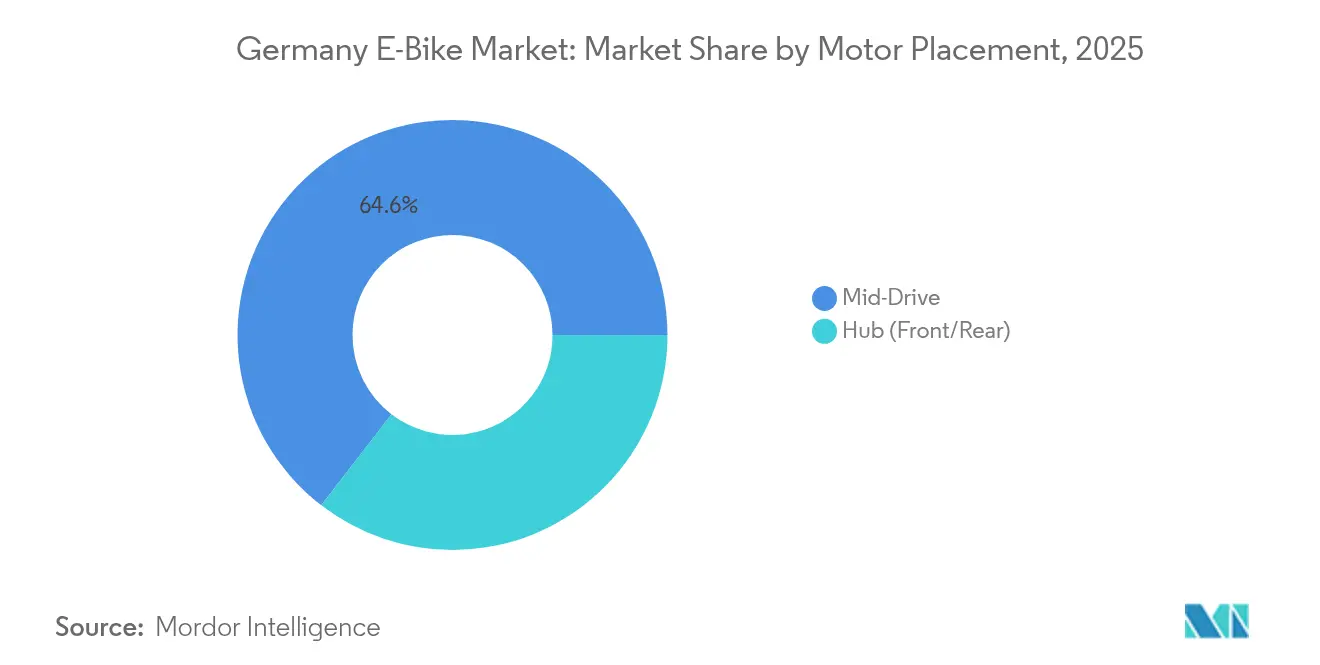

- By motor placement, mid-drive units secured a 64.55% of the German E-Bike market share in 2025 and are set for a 4.05% CAGR through 2031.

- By drive systems, the chain drive held 71.30% of the German E-Bike market share in 2025, whereas the belt drive systems are set for a 5.02% CAGR through 2031.

- By motor power, the below 250 W segment held 55.40% of the German E-Bike market share in 2025, WHILE 351-500 W are set to expand with a 4.78% CAGR.

- By price band, the USD 1,500–2,499 models range remains the volume leader accounting 27.95% of the German E-Bike market share in 2025, whereas priced at USD 3,500–5,999 command the fastest 4.42% CAGR.

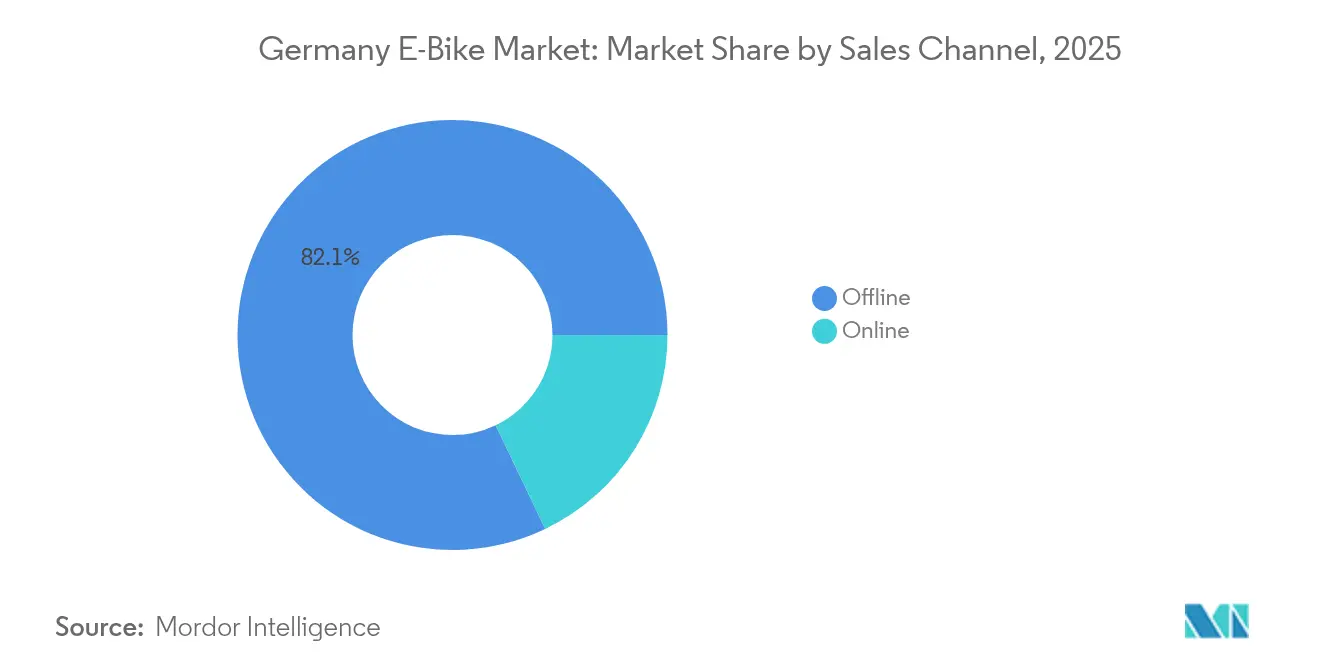

- By sales channel, offline retail retained an 82.10% of the German E-Bike market share in 2025; online direct-to-consumer revenue is growing at a 6.02% CAGR.

- By end use, e-bikes for personal and family use accounted for 61.20% of the German E-Bike market share in 2025, while commercial delivery fleets are projected to expand at a CAGR of 5.28% by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany E-Bike Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Congestion and Modal Shift | +1.2% | Berlin, Munich, Hamburg, Cologne | Long term (≥ 4 years) |

| Corporate Mobility and Budget Leasing | +1.1% | Corporate clusters nationwide | Short term (≤ 2 years) |

| Battery and Motor Technology | +0.9% | National R&D hubs in Bavaria, Baden-Württemberg | Medium term (2-4 years) |

| Government Purchase Incentives | +0.8% | NRW, Baden-Württemberg, Bavaria | Medium term (2-4 years) |

| Awareness for Environmental Targets | +0.6% | National, urban centers | Long term (≥ 4 years) |

| Tourism-Driven Trail Expansion | +0.4% | Alpine regions, Rhine Valley, Baltic coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urban Congestion-Driven Modal Shift

Germany's Federal Government has unveiled the National Cycling Plan (NCP) 3.0, a strategic initiative aimed at promoting cycling across the nation, with a vision extending to 2030. NCP 3.0's primary objective is to enhance the appeal and safety of cycling in Germany, thereby aiming for a substantial uptick in the distance covered by cyclists [1]“Nationaler Radverkehrsplan 3.0,” Bundesministerium für Digitales und Verkehr, bmvi.de. E-bikes, although forming a smaller portion of the total fleet, play a disproportionately significant role in overall bicycle usage. Protected lanes in Munich are set to reach 1,200 km by 2025, enabling commutes once considered car-only. Longer range, hill-flattening assistance, and lower weather sensitivity explain why urban residents substitute cars with e-bikes more often than with acoustic bikes.

Corporate Mobility-Budget Leasing

Germany's corporate bike-leasing boom is largely driven by fiscal policy. A 2019 amendment to the Income Tax Act, which allows employees leasing bicycles or e-bikes through salary sacrifice to treat only a small portion of the manufacturer's list price as a monthly taxable benefit. The National Cycling Plan 3.0 highlights company-bike leasing as a “key action” to shift work-related travel from cars. They estimate a substantial annual CO₂ saving if a significant portion of short commutes transitions to bicycles or e-bikes. Through gross-salary leasing, employees enjoy significant savings on bike models. Employers value the predictability of monthly deductions, while suppliers appreciate the stability of bulk contracts, which are less vulnerable to retail fluctuations.

Battery and Motor Technology Advances

Prototype solid-state cells from QuantumScape and PowerCo deliver 844 Wh/L energy density and can charge to 80% in 12 minutes. Commercial mid-drive motors reach 85 Nm at 2.8 kg, improving hill performance without breaching Germany’s 250 W nominal cap. DJI’s Avinox unit offers 105 Nm at 2.5 kg plus 12 A fast-charging inlets, proving that consumer-electronics engineering is permeating the drivetrain.

Government Purchase Incentives

Localized subsidies cushion demand against the lack of federal aid. Stuttgart grants up to EUR 1,100 (~USD 1,278) per cargo e-bike, while North Rhine-Westphalia covers 25% of the purchase value up to EUR 3,500 (~USD 4,067) [2]“Förderprogramm Lastenräder,” Stadt Stuttgart, stuttgart.de. Cargo e-bikes benefit most because percentage-based help offsets higher sticker prices. Subsidized municipalities exhibit adoption rates above the national mean. Baden-Württemberg’s Bike+Ride program funds secure parking projects, closing last-mile gaps that often limit daily use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Post-Subsidy | -0.7% | Lower-income regions nationwide | Short term (≤ 2 years) |

| Domestic Battery-Cell Supply Risk | -0.5% | National, concentrated supply chains | Medium term (2-4 years) |

| After-Sales Workshop Bottlenecks | -0.4% | Rural and suburban areas | Short term (≤ 2 years) |

| Rising Theft-Insurance Premiums | -0.3% | Berlin, Hamburg, Cologne, Frankfurt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Post-Subsidy

In 2024, consumers became increasingly price-conscious, with many opting to delay significant discretionary purchases, according to surveys. In 2024, average retail prices declined, but many mainstream buyers still perceive a specific price point as a psychological ceiling. Without nationwide incentives, Germany ranks below neighboring France on net purchase support, encouraging cross-border shopping in border towns.

Domestic Battery-Cell Supply Risk

Manufacturers face geopolitical and freight disruptions as a significant portion of e-bike cells are sourced from China. EU Battery Regulation 2023/1542 will require CO₂ footprint declarations and digital passports from 2027, potentially favoring suppliers already collecting granular provenance data. Domestic initiatives such as Northvolt’s Heide plant remain several years from mass output, leaving a near-term security gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Speed Pedelecs Drive Premium Growth

Pedal-assisted systems generated 79.35% of the Germany E-Bike market in 2025, benefiting from a bicycle-equivalent legal status that avoids insurance and license requirements. Speed Pedelecs post a 3.76% CAGR as commuters seek 45 km/h cruising on longer routes. This segment will contribute disproportionately to the expansion of the German e-bike market between 2026 and 2031.

Regulatory debate on EPAC definitions adds forecast volatility. ZIV’s proposal to cap peak power at 750 W and maintain a 1:4 assist ratio aims to preserve the non-motor-vehicle classification. Advocacy group LEVA-EU counters that tighter rules would restrain cargo innovation. A decision expected in 2026 could widen or narrow the addressable market for high-assist bicycles, directly influencing Germany's E-Bike market share trajectories.

By Application Type: Commercial Delivery Transforms Urban Logistics

City/Urban riding held 70.92% of 2025 revenue, but the cargo/utility segment is on track for a 3.74% CAGR to 2031, the top growth lane within the German E-Bike market. Cargo/Utility usage follows closely as parcel companies and grocery platforms electrify last-mile fleets to meet city emission zones.

In 2024, the industry experienced significant growth in cargo units, reflecting a notable year-on-year increase, with many fleets now spec 1,000 Wh batteries to secure a full shift without midday recharging. Combined with diesel vehicle bans in Berlin, fleet orders promise steady demand inflows that stabilize quarterly shipment cycles previously driven by consumer seasonality.

By Battery Type: Lithium-Ion Achieves Near-Universal Adoption

Lithium-ion packs represented 99.82% of 2025 shipments and will chart a parallel 3.67% CAGR through 2031, underpinning most gains in the German E-Bike market size. Alternative chemistries remain relegated to sub-USD 1,000 entry bikes or experimental solid-state pilots.

The EU Battery Regulation introduces mandatory digital passports from February 2027 and collection targets of 51% by 2028. These measures institutionalize circular-economy practices, reinforcing lithium-ion incumbency while encouraging European cell production to cut embedded scope-3 emissions and lower transport risk.

By Motor Placement: Mid-Drive Systems Dominate Performance Applications

Mid-drive units commanded a 64.55% share in 2025, buoyed by superior balance and native gearbox integration. The anticipated mid-drive CAGR of 4.05% exceeds the overall Germany E-Bike market growth, advancing the Germany E-Bike market share of mid-drive platforms by 2031.

Pinion’s integrated MGU motor-gearbox has already been adopted by Riese & Müller’s 2025 Delite 5, replacing chains with a sealed unit that cuts maintenance intervals in half. Yamaha’s planned acquisition of Brose’s e-Kit business further concentrates expertise and may accelerate mid-drive torque density innovations after 2025 regulatory clearance.

By Drive System: Belt Drive Innovation Challenges Chain Dominance

Chain transmissions still held 71.30% of unit shipments in 2025. Belt drive, however, is tracking a 5.02% CAGR, double the overall Germany E-Bike market rate, as commuters demand grease-free drivetrains.

Fleet operators report lower downtime with belt-equipped cargo bikes, citing reduced chain stretch under heavy loads. As manufacturing scale lowers cost premiums, belt systems could claim a visible Germany E-Bike market share leap within premium urban segments by 2031.

By Motor Power: Mid-Range Power Gains Traction

Below-250 W motors account for 55.40% of today’s installed base, aligning with legal limits for bicycle classification. Yet the 351-500 W class posts the swiftest 4.78% CAGR, driven by cargo applications that value sustained torque.

If ZIV’s 750 W peak allowance is adopted, manufacturers can unlock extra performance without vehicle registration, potentially shifting the power segmentation mix and lifting the German E-Bike market size for high-capacity batteries.

By Price Band: Premium Segment Drives Value Migration

Models priced at USD 1,500–2,499 retain 27.95% volume leadership, but the USD 3,500–5,999 tier shows the quickest 4.42% CAGR, propelled by leasing plans that dilute upfront cost shock. Corporate salary-sacrifice programs increase transaction value even as retail channels aim for affordability through component optimization.

Corporate customers typically spend significantly more per unit compared to retail channels. This divergence underscores bifurcation: mainstream consumers hunt sub-EUR 2,000 (~USD 2,325) deals, while employees in large firms gravitate toward high-spec connectivity, integrated lighting, and premium suspension.

By Sales Channel: Online Growth Accelerates Digital Transformation

Brick-and-mortar (offline) stores maintained an 82.10% share in 2025, reflecting the importance of test rides and local servicing. Yet online direct-to-consumer revenue is scaling at 6.02% CAGR. Canyon’s EUR 792 million (~USD 921 million) turnover, delivered without a traditional dealer network, demonstrates digital potential despite slim margins.

Surveys reveal that most Germans favor online shopping for big-ticket items, provided a 30-day return window exists, while a few still want in-store consultation. Consequently, leading brands deploy hybrid models online configuration paired with local service partners to capture both consumer segments.

By End Use: Commercial Applications Reshape Market Dynamics

Personal and family riding constitutes 61.20% of the present volume, yet Commercial Delivery’s 5.28% CAGR will steadily lift its weight in the German E-Bike market. Service providers and municipal institutions also bolster B2B demand, valuing the total cost of ownership over initial price.

Berlin-based CYCLE’s July 2024 purchase of Ebike4Delivery consolidates rental and fleet management know-how, illustrating how integrated services, not just hardware, differentiate suppliers in commercial channels.

Geography Analysis

Southern powerhouse states Bavaria and Baden-Württemberg comprise a notable share of total unit sales, aided by dense cycling networks and corporate headquarters that underwrite mobility budgets. North Rhine-Westphalia follows with strong municipal subsidies targeting commuter congestion mitigation. Berlin shows the highest per-capita ridership but moderates in raw volume because of its smaller population base.

Regional incentives produce patchy demand. In 2024, Stuttgart experienced a notable increase in local sales due to financial incentives, while neighboring regions without similar support observed relatively slower growth during the same timeframe. Vendors tailor marketing and stock allocation to these pockets, with premium mid-drive cargo models concentrated in subsidy-heavy districts.

Tourism accelerates adoption along the Rhine Valley and Baltic coast, where rental operators upgrade fleets every 18 months to maintain battery health. Alpine resorts report that e-MTB rentals extend average visitor stays by 1.3 nights, driving hospitality revenue synergies. Eastern rural areas lag owing to sparse dealer networks; federal infrastructure funds allocated under the Sonderprogramm “Stadt und Land” aim to close this gap by 2028.

Competitive Landscape

Domestic champions CUBE, Riese & Müller, and Bulls retain brand equity through dealer intimacy and made-in-Germany craftsmanship. Bosch supplies drive units to a notable share of all locally assembled e-bikes, making its firmware updates and warranty programs pivotal to brand differentiation. Canyon leverages factory-to-door logistics to undercut retail markups, though its EUR 38 million (~USD 44 million) operating loss in 2024 signaled the thin margin reality of pure-play e-commerce.

Strategic moves trend toward vertical integration. Yamaha’s acquisition of Brose’s e-Kit subsidiary, announced in 2025, consolidates electric motor IP and ramps up R&D scale [3]“Brose e-Kit Acquisition Press Release,” Yamaha Motor, yamaha-motor.eu. Meanwhile, JobRad Loop’s certified refurbishment program channels used bikes into secondary markets, extending product life cycles and introducing price entry points for budget buyers.

Digitalization is an emerging battleground. Industry consortium DiBike adopted the Veloconnect interface to harmonize inventory and after-sales data flow, positioning brands that integrate seamlessly with dealer point-of-sale systems for quicker service turnaround and warranty claim resolution. EU battery-passport mandates also reward manufacturers equipped with track-and-trace infrastructure, raising compliance costs for low-price importers and nudging market share toward established players.

Germany E-Bike Industry Leaders

Riese & Müller GmbH

Canyon Bicycles GmbH

Pon Holdings B.V.

Accell Group

Prophete In Moving GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Fafrees unveiled its first EU-type-approved high-speed e-bikes during Eurobike 2025 at Messe Frankfurt.

- March 2025: Yamaha Motor signed to acquire Brose’s e-Kit subsidiary and launched Yamaha eBike Systems in Germany, targeting full operational rollout by June 2025.

- July 2024: Berlin-based CYCLE acquired Ebike4Delivery, strengthening its share in Europe’s delivery-bike leasing segment.

Germany E-Bike Market Report Scope

Pedal Assisted, Speed Pedelec, Throttle Assisted are covered as segments by Propulsion Type. Cargo/Utility, City/Urban, Trekking are covered as segments by Application Type. Lead Acid Battery, Lithium-ion Battery, Others are covered as segments by Battery Type.By Propulsion Type

| Pedal Assisted |

| Speed Pedelec |

| Throttle Assisted |

By Application Type

| Cargo/Utility |

| City/Urban |

| Trekking/Mountain |

By Battery Type

| Lead Acid Battery |

| Lithium-ion Battery |

| Others |

By Motor Placement

| Hub (Front/Rear) |

| Mid-Drive |

By Drive Systems

| Chain Drive |

| Belt Drive |

By Motor Power

| Below 250 W |

| 251-350 W |

| 351-500 W |

| 501-600 W |

| Above 600 W |

By Price Band

| Up to USD 1,000 |

| USD 1,000-1,499 |

| USD 1,500-2,499 |

| USD 2,500-3,499 |

| USD 3,500-5,999 |

| Above USD 6,000 |

By Sales Channel

| Online |

| Offline |

By End Use

| Commercial Delivery | Retail and Goods Delivery |

| Food and Beverage Delivery | |

| Service Providers | |

| Personal and Family Use | |

| Institutional | |

| Others |

| By Propulsion Type | Pedal Assisted | |

| Speed Pedelec | ||

| Throttle Assisted | ||

| By Application Type | Cargo/Utility | |

| City/Urban | ||

| Trekking/Mountain | ||

| By Battery Type | Lead Acid Battery | |

| Lithium-ion Battery | ||

| Others | ||

| By Motor Placement | Hub (Front/Rear) | |

| Mid-Drive | ||

| By Drive Systems | Chain Drive | |

| Belt Drive | ||

| By Motor Power | Below 250 W | |

| 251-350 W | ||

| 351-500 W | ||

| 501-600 W | ||

| Above 600 W | ||

| By Price Band | Up to USD 1,000 | |

| USD 1,000-1,499 | ||

| USD 1,500-2,499 | ||

| USD 2,500-3,499 | ||

| USD 3,500-5,999 | ||

| Above USD 6,000 | ||

| By Sales Channel | Online | |

| Offline | ||

| By End Use | Commercial Delivery | Retail and Goods Delivery |

| Food and Beverage Delivery | ||

| Service Providers | ||

| Personal and Family Use | ||

| Institutional | ||

| Others | ||

Market Definition

- By Application Type - E-bikes considered under this segment include city/urban, trekking, and cargo/utility e-bikes. The common types of e-bikes under these three categories include off-road/hybrid, kids, ladies/gents, cross, MTB, folding, fat tire, and sports e-bike.

- By Battery Type - This segment includes lithium-ion batteries, lead-acid batteries, and other battery types. The other battery type category includes nickel-metal hydroxide (NiMH), silicon, and lithium-polymer batteries.

- By Propulsion Type - E-bikes considered under this segment include pedal-assisted e-bikes, throttle-assisted e-bikes, and speed pedelec. While the speed limit of pedal and throttle-assisted e-bikes is usually 25 km/h, the speed limit of speed pedelec is generally 45 km/h (28 mph).

| Keyword | Definition |

|---|---|

| Pedal Assisted | Pedal-assist or pedelec category refers to the electric bikes that provide limited power assistance through torque-assist system and do not have throttle for varying the speed. The power from the motor gets activated upon pedaling in these bikes and reduces human efforts. |

| Throttle Assisted | Throttle-based e-bikes are equipped with the throttle assistance grip, installed on the handlebar, similarly to motorbikes. The speed can be controlled by twisting the throttle directly without the need to pedal. The throttle response directly provides power to the motor installed in the bicycles and speeds up the vehicle without paddling. |

| Speed Pedelec | Speed pedelec is e-bikes similar to pedal-assist e-bikes as they do not have throttle functionality. However, these e-bikes are integrated with an electric motor which delivers power of approximately 500 W and more. The speed limit of such e-bikes is generally 45 km/h (28 mph) in most of the countries. |

| City/Urban | The city or urban e-bikes are designed with daily commuting standards and functions to be operated within the city and urban areas. The bicycles include various features and specifications such as comfortable seats, sit upright riding posture, tires for easy grip and comfortable ride, etc. |

| Trekking | Trekking and mountain bikes are special types of e-bikes that are designed for special purposes considering the robust and rough usage of the vehicles. These bicycles include a strong frame, and wide tires for better and advanced grip and are also equipped with various gear mechanisms which can be used while riding in different terrains, rough grounded, and tough mountainous roads. |

| Cargo/Utility | The e-cargo or utility e-bikes are designed to carry various types of cargo and packages for shorter distances such as within urban areas. These bikes are usually owned by local businesses and delivery partners to deliver packages and parcels at very low operational costs. |

| Lithium-ion Battery | A Li-ion battery is a rechargeable battery, which uses lithium and carbon as its constituent materials. The Li-Ion batteries have a higher density and lesser weight than sealed lead acid batteries and provide the rider with more range per charge than other types of batteries. |

| Lead Acid Battery | A lead acid battery refers to sealed lead acid battery having a very low energy-to-weight and energy-to-volume ratio. The battery can produce high surge currents, owing to its relatively high power-to-weight ratio as compared to other rechargeable batteries. |

| Other Batteries | This includes electric bikes using nickel–metal hydroxide (NiMH), silicon, and lithium-polymer batteries. |

| Business-to-Business (B2B) | The sales of e-bikes to business customers such as urban fleet and logistics company, rental/sharing operators, last-mile fleet operators, and corporate fleet operators are considered under this category. |

| Business-to-Customers (B2C) | The sales of electric scooters and motorcycles to direct consumers is considered under this category. The consumers acquire these vehicles either directly from manufacturers or from other distributers and dealers through online and offline channel. |

| Unorganized Local OEMs | These players are small local manufacturers and assemblers of e-bikes. Most of these manufacturers import the components from China and Taiwan and assemble them locally. They offer the product at low cost in this price sensitive market which give them advantage over organized manufacturers. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Dockless e-Bikes | Electric bikes that have self-locking mechanisms and a GPS tracking facility with an average top speed of around 15mph. These are mainly used by bike-sharing companies such as Bird, Lime, and Spin. |

| Electric Vehicle | A vehicle which uses one or more electric motors for propulsion. Includes cars, scooters, buses, trucks, motorcycles, and boats. This term includes all-electric vehicles and hybrid electric vehicles |

| Plug-in EV | An electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. In this report we use the term for all-electric vehicles to differentiate them from plug-in hybrid electric vehicles. |

| Lithium-Sulphur Battery | A rechargeable battery that replaces the liquid or polymer electrolyte found in current lithium-ion batteries with sulfur. They have more capacity than Li-ion batteries. |

| Micromobility | Micromobility is one of the many modes of transport involving very-light-duty vehicles to travel short distances. These means of transportation include bikes, e-scooters, e-bikes, mopeds, and scooters. Such vehicles are used on a sharing basis for covering short distances, usually five miles or less. |

| Low Speed Electric Vehicls (LSEVs) | They are low speed (usually less than 25 kmph) light vehicles that do not have an internal combustion engine, and solely use electric energy for propulsion. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms