Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 33.79 Billion |

| Market Size (2031) | USD 49.23 Billion |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

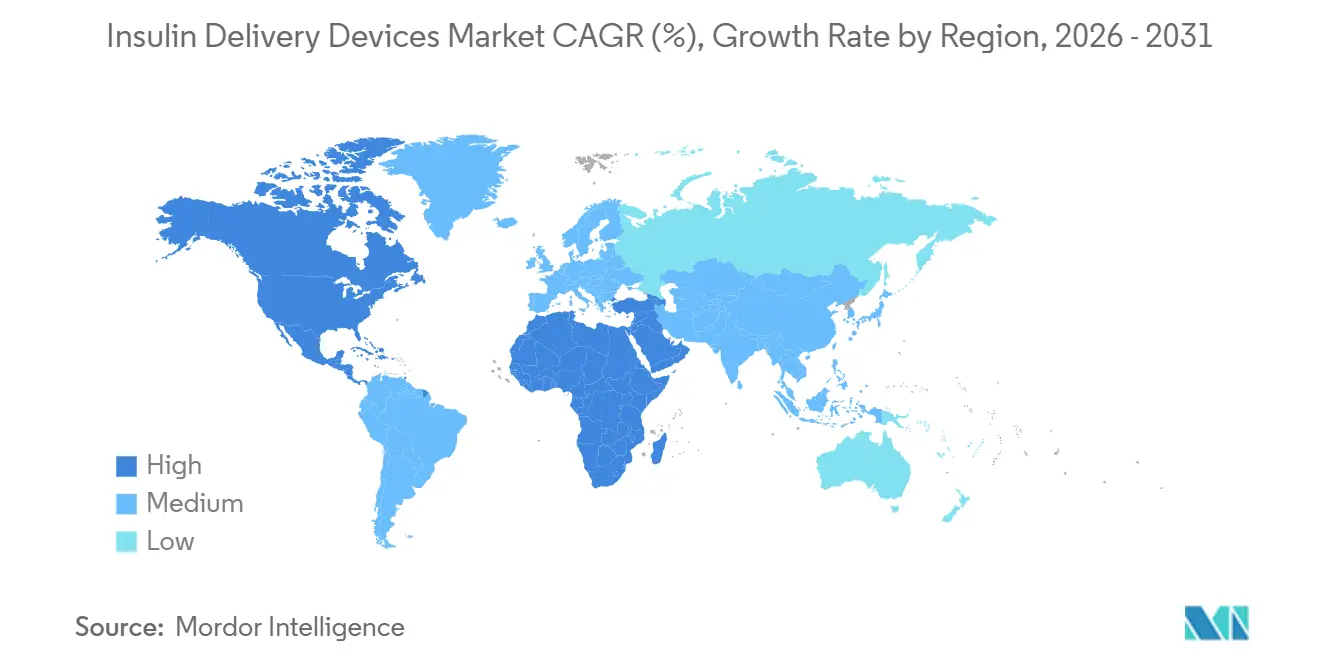

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulin Delivery Devices Market Analysis by Mordor Intelligence

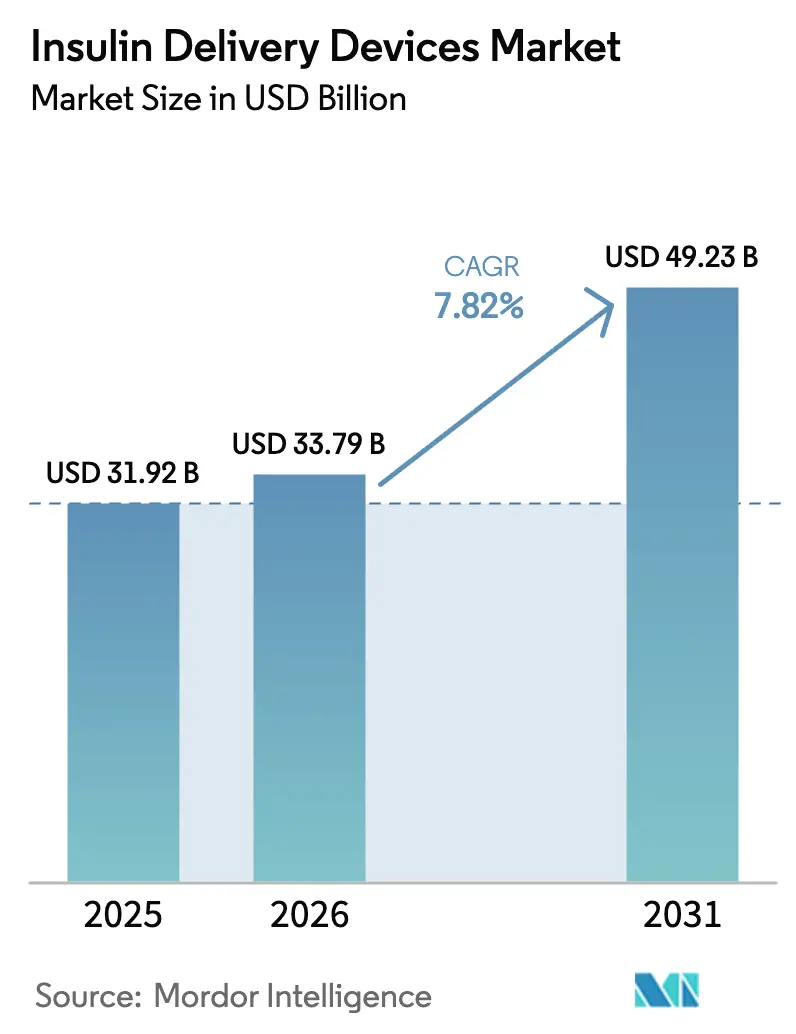

The Insulin Delivery Devices Market size is expected to increase from USD 31.92 billion in 2025 to USD 33.79 billion in 2026 and reach USD 49.23 billion by 2031, growing at a CAGR of 7.82% over 2026-2031.

Demand is shifting from vial-and-syringe routines toward automated, connected platforms that lower dosing errors, improve time-in-range, and lighten daily disease burden. Hybrid closed-loop approvals, wider reimbursement for patch pumps and smart pens, and national insurance rollouts in China and India are accelerating unit volumes. Middle-income economies are adopting low-cost wearable pumps at roughly half the price of Western incumbents, while payers in high-income regions favor devices that transmit real-time data. Cybersecurity, encryption, and algorithm depth now separate market leaders more than pure hardware design.

Key Report Takeaways

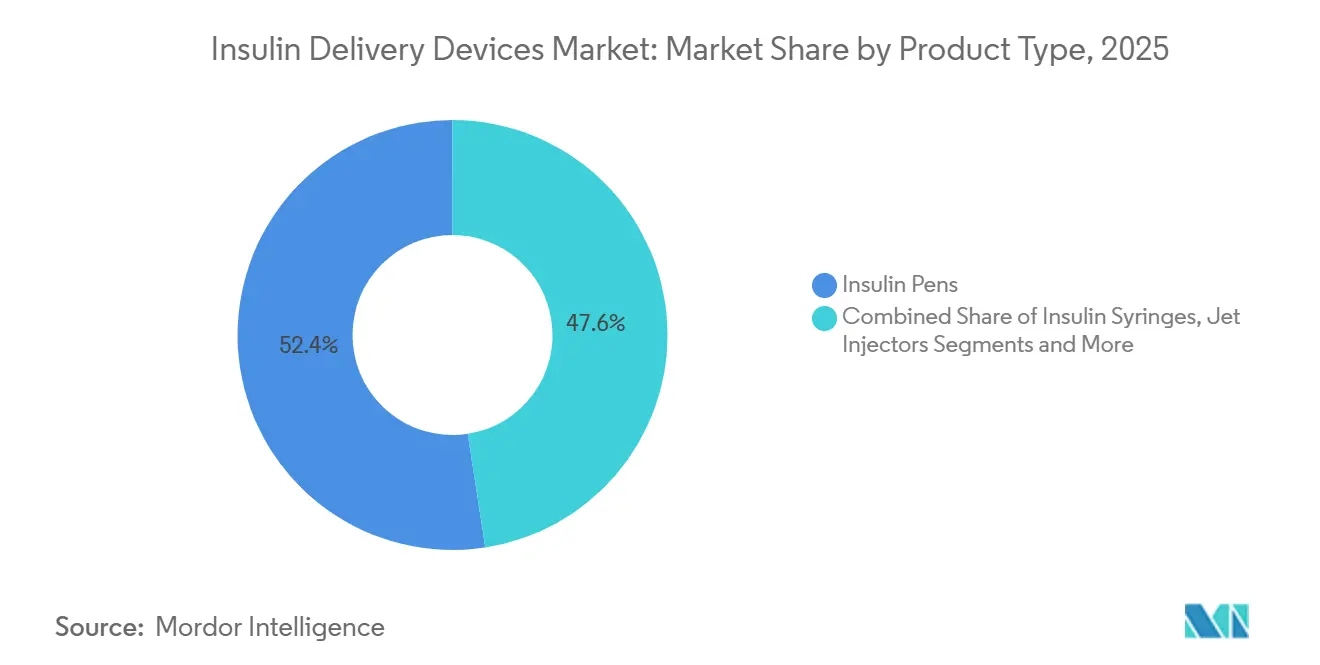

- By product type, insulin pens led with 52.44% of the insulin delivery devices market share in 2025, while insulin pumps are projected to grow at an 11.33% CAGR through 2031.

- By technology, non-connected hardware accounted for 71.45% of 2025 revenue, whereas connected devices are forecast to expand at a 12.77% CAGR over the same period.

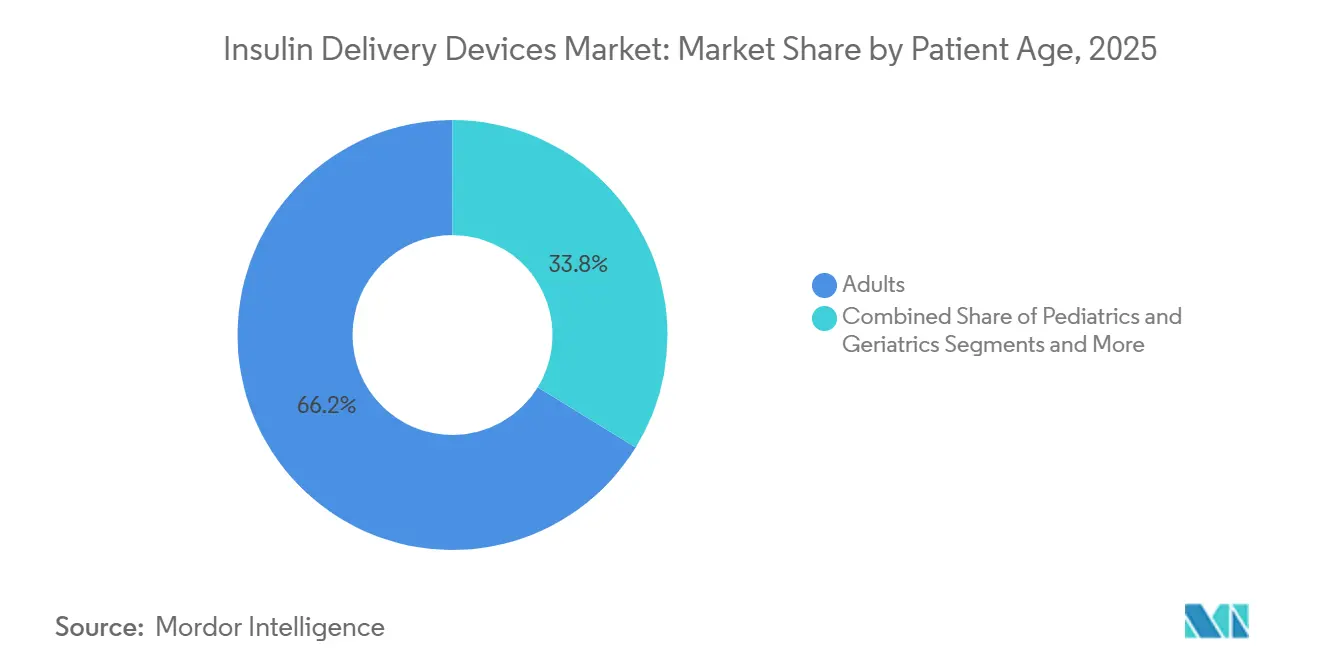

- By patient age group, adults held 66.24% of 2025 sales, but the pediatric cohort is advancing at a 9.34% CAGR to 2031.

- By distribution channel, retail pharmacies captured 44.73% of 2025 turnover, yet online pharmacies are on track for a 12.53% CAGR through 2031.

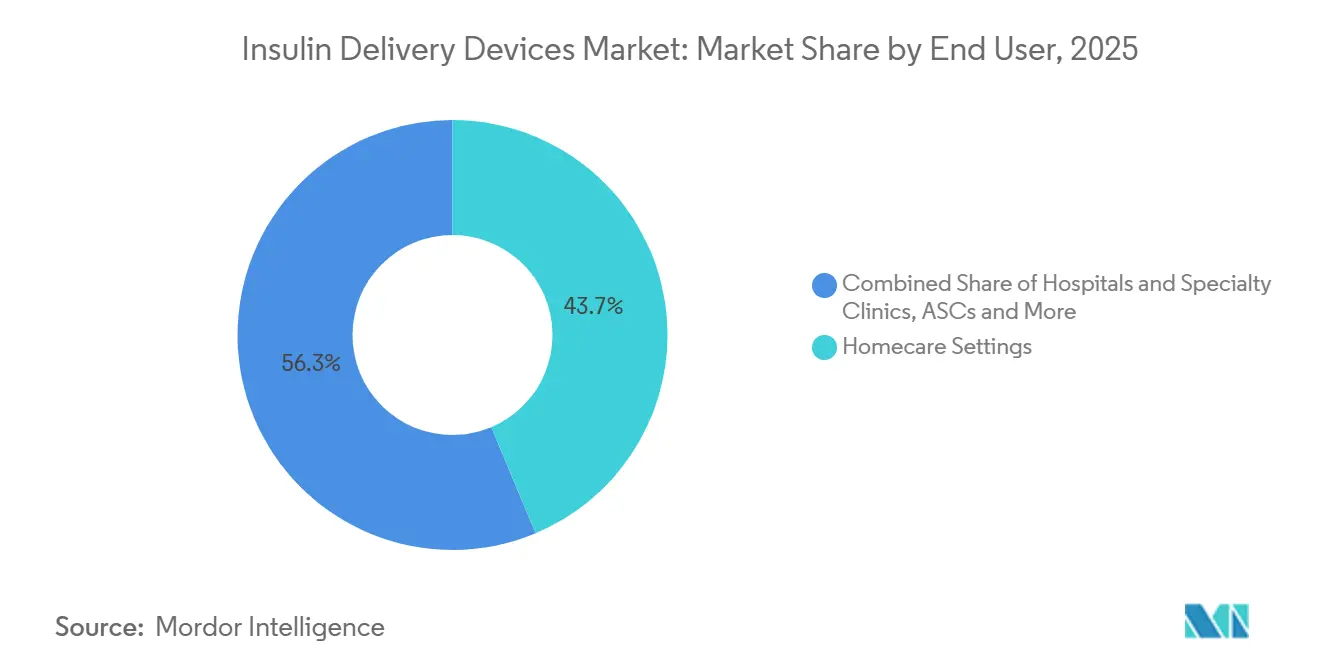

- By end user, homecare settings accounted for 43.67% of 2025 revenue and are also the fastest-growing slice of the market, rising at a 10.45% CAGR over the forecast horizon.

- By geography, North America commanded 38.55% of 2025 revenue, while Asia-Pacific is expected to record the highest regional growth at a 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Insulin Delivery Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Diabetes and Earlier Diagnosis | +1.5% | Global, highest absolute growth in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Shift Toward Convenient, Minimally Invasive Self-Administration | +1.2% | North America and Europe lead; Asia-Pacific accelerating | Medium term (2-4 years) |

| Reimbursement Expansion for Pen Cartridges and Patch Pumps | +1.0% | North America, Europe, select Asia-Pacific | Short term (≤ 2 years) |

| Rapid Uptake of Connected “Smart” Pens and Add-On Caps | +1.3% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Surge in GLP-1 / Insulin Co-Formulations Requiring Device Redesign | +0.8% | Global, early traction in United States and European Union | Long term (≥ 4 years) |

| Emergence of Low-Cost Chinese Patch Pumps | +0.7% | China, India, Southeast Asia; spill-over to Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes and Earlier Diagnosis

Global diabetes prevalence continues to climb, yet the more telling shift is the shorter interval between symptom onset and confirmed diagnosis.[1] International Diabetes Federation, “IDF Diabetes Atlas, 10th Edition,” International Diabetes Federation, idf.org The United States now recommends HbA1c screening for every adult over 35, enlarging the pool for basal-bolus regimens that need purpose-built devices.[2] National Health Commission of China, “Workplace Diabetes Screening Policy Notice, January 2025,” National Health Commission, nhc.gov.cn China mandated workplace screening for employees over 40 in January 2025, identifying millions of previously undiagnosed adults and boosting first-time device purchases. Europe recorded a 3.4% rise in pediatric type 1 incidence during 2024, lifting demand for simplified pumps with smaller reservoirs. Manufacturers are answering with color-coded pen caps and pre-set basal profiles that reduce the learning curve for new users. Earlier diagnosis therefore widens the installed base and pushes patients toward connected tools that guide dose titration.

Rapid Uptake of Connected “Smart” Pens and Add-On Caps

Smart pens that log dose data through Bluetooth or near-field communication are displacing conventional pens faster than forecast two years ago. Companion Medical’s InPen counted 180,000 active U.S. users in December 2025, up from 95,000 a year earlier.[3]Companion Medical, “InPen Active‐User Metrics, December 2025,” Companion Medical, companionmedical.com The Centers for Medicare & Medicaid Services reclassified smart pens as durable medical equipment in January 2025, cutting out-of-pocket spending for Medicare Part B users. Novo Nordisk shipped 1.2 million NovoPen 6 and Echo Plus units worldwide in 2025, securing 18% of reusable-pen sales. Bigfoot Biomedical began shipping its Unity smart cap in March 2025, creating a lower-cost entry point for patients hesitant to adopt pumps. Updated IEEE 11073 standards, released in June 2025, now require end-to-end encryption, easing privacy concerns among hospital IT teams.

Reimbursement Expansion for Pen Cartridges and Patch Pumps

Payer support broadened in 2024 and 2025. Medicare removed prior-authorization barriers for patch pumps in April 2024, opening full coverage for Omnipod 5 and similar systems. Germany added connected pens to its statutory benefit catalog in January 2025 at EUR 120 per device, payable every four years. France followed in March 2025, funding smart pens when paired with continuous glucose monitors. These moves shrink out-of-pocket costs, speed adoption, and shorten payback periods for device makers. Commercial insurers in the United States are mirroring Medicare to stay competitive, lifting coverage ceilings and embracing connected hardware that may cut long-term complication costs.

Surge in GLP-1 / Insulin Co-Formulations Requiring Device Redesign

Drug pipelines now blend GLP-1 agonists with basal insulin, prompting cartridge and reservoir redesigns. Lilly’s tirzepatide-insulin glargine combo demands a larger 3 mL cartridge to handle higher viscosity. Novo Nordisk’s icodec-semaglutide pen will likely need a wider-gauge needle, a trade-off that could temper uptake among needle-averse adults. Sanofi is engineering a dual-chamber SoloStar that mixes compounds only at injection to preserve stability. Pump makers face similar tasks: Medtronic is coating reservoirs to stop protein aggregation over a three-day wear cycle. These projects delay launches by roughly one year yet remain essential because combination therapy is moving toward first-line status.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Average Selling Prices Versus Injections | -0.9% | Asia-Pacific (excluding Japan), Middle East and Africa, South America | Medium term (2-4 years) |

| Needle-Phobia and User-Error Concerns | -0.5% | Global, higher incidence in pediatric and geriatric groups | Long term (≥ 4 years) |

| Cybersecurity and Data-Privacy Risks in Connected Pumps | -0.4% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Supply-Chain Pressure on Medical-Grade Plastics and Cannulas | -0.3% | Global, acute in Asian resin hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and Data-Privacy Risks in Connected Pumps

Connected pumps move dose data over Bluetooth Low Energy and cellular links, creating entry points for malicious actors. The U.S. Food and Drug Administration warned in April 2024 that certain MiniMed pumps could be accessed wirelessly if older firmware remained unpatched. Insulet fixed a man-in-the-middle vulnerability in Omnipod 5 within 72 hours of discovery in June 2025, underscoring strong incident response but highlighting ongoing exposure. The European Union Medical Device Regulation now mandates a full cybersecurity risk file in conformity assessments, adding up to nine months to approval timelines. Hospitals demand ISO 27001 compliance before including connected pumps on formularies, a hurdle for smaller entrants without dedicated security teams. Persistent headline risk can slow adoption among risk-averse clinics and older patients.

Global Supply-Chain Pressure on Medical-Grade Plastics and Cannulas

Pump manufacturers rely on medical-grade polycarbonate and cyclic olefin copolymers. A 2024 fire at a Mitsubishi Chemical plant in Japan removed 22% of global cyclic olefin copolymer output, delaying new pump rollouts by up to six months. BD faced a 12-week back-order for steel cannulas in late-2024 after a labor strike in Tijuana. Polycarbonate prices rose 14% year-over-year in 2024, eroding gross margins by 150 to 200 basis points for pump makers. Insulet reduced exposure by dual-sourcing cannulas from Japan and the Philippines. Ypsomed is shifting reservoir molding to Malaysia to cut per-unit cost by 20% by mid-2026. Supply-chain diversification helps, yet material shocks remain a near-term brake on volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pumps Outpace Pens Despite Smaller Base

Insulin pens commanded 52.44% of 2025 revenue, yet pumps are set to grow faster, with an 11.33% CAGR through 2031 as payers reward automated dosing that lowers hypoglycemia rates. Reusable pens represented 60% of pen sales, favored in regions with cartridge recycling mandates, while disposable pens held the remaining 40% thanks to convenience in markets with limited cold-chain capacity. Within pumps, tethered models still delivered 55% of 2025 pump turnover, but patch designs are advancing quickly because they avoid tubing snags and support discreet wear. Insulet shipped 1.8 million Omnipod 5 pods in 2025, up 38% year-on-year. Automated hybrid closed-loop pumps accounted for 22% of 2025 revenue share and are projected to reach 45% by 2031. Syringes continue to decline at 3% per year and now sit mainly in hospital wards and low-income regions. Needle-free jet injectors remain niche, under 2% of 2025 revenue, limited by high start-up cost and unfamiliar operation. Tandem’s Mobi pump, 50% smaller than the t:slim X2, entered the market in late-2024 and targets discretion-minded adolescents.

The U.S. Food and Drug Administration cleared the iLet Bionic Pancreas in May 2024, signaling confidence in algorithms that require minimal user input. Medtronic’s MiniMed 780G, approved in August 2024, adjusts basal rates up to 288 times per day and removes much of the carb-count burden. Chinese suppliers such as Medtrum now price starter kits at half Western levels, broadening access in middle-income economies. Reusable pens benefit from NFC-based dose logging, while disposable pens remain the default for basal-only regimens in type 2 patients who value simplicity over sustainability. Jet injectors appeal to needle-phobic adults but need stronger payer support to scale.

By Technology / Connectivity: Bluetooth-Enabled Devices Reshape Adherence Monitoring

Conventional hardware still held 71.45% of 2025 revenue, yet connected devices will grow at a 12.77% CAGR to 2031, bolstered by payer policy that classifies smart pens as durable equipment. InPen almost doubled its active user base within a year, confirming demand for dose-memory that links to CGM trends. Tandem’s t:slim X2 and Insulet’s Omnipod 5 send basal and bolus data to cloud dashboards, enabling remote care and expanding pediatric adoption. After IEEE 11073 added encryption mandates in June 2025, hospital IT teams warmed to connected pumps.

Cost-sensitive markets still favor non-connected pens, yet add-on caps such as Bigfoot Unity provide a bridge at lower price points. Novo Nordisk’s connected pens recorded 1.2 million global shipments in 2025, equal to 18% of reusable-pen volume. As smartphone penetration widens among seniors, connected uptake should further erode the gap. However, privacy concerns and the need to update firmware will keep a role for conventional devices through the decade.

By Patient Age Group: Pediatric Segment Accelerates on Closed-Loop Approvals

Adults drove 66.24% of 2025 revenue, reflecting the scale of type 2 diabetes, yet pediatric sales are rising faster at a 9.34% CAGR. The insulin delivery devices market size for pediatrics will surge as regulators clear closed-loop pumps for younger ages. Omnipod 5 reached children as young as two years in March 2025, answering long-held parental concerns over tubing and nighttime hypoglycemia. Tandem extended Control-IQ labeling to ages six and up in June 2024, reducing HbA1c by 1.1 percentage points without adding hypoglycemia risk.

The geriatric group held 18% of 2025 turnover and is advancing at 6.8% annually, slowed by lower tech confidence and fixed incomes. Medtronic’s simplified bolus mode reduces numeracy demands, aiding older patients. T1D Exchange data show that 42% of newly diagnosed U.S. children started on a pump in 2025 versus 28% two years earlier. Adult uptake remains moderate because entrenched injection habits and lower digital engagement persist.

By Distribution Channel: Online Pharmacies Disrupt Retail Incumbents

Retail pharmacies still supplied 44.73% of devices in 2025, yet online channels are set to grow faster at a 12.53% CAGR as Amazon and CVS expand digital fulfillment. Amazon launched a diabetes storefront in March 2024 with next-day delivery on pen needles and infusion sets. CVS added same-day delivery for pump consumables in 47 metropolitan areas by mid-2025. Hospital pharmacies remain important in acute care and accounted for 28% of 2025 volume. Diabetes clinics combined sales with education but fell to 12% of revenue as virtual onboarding gained traction.

Walgreens announced 150 store closures in April 2025 after device footfall shifted online. Retail outlets still offer immediate counseling, but telehealth plus fast shipping is narrowing that edge. Online players benefit from bulk procurement and lower overhead, translating into lower copays. Hospitals are under pressure to prescribe take-home devices that align with patients’ home routines, further channeling sales toward retail and online platforms.

By End User: Homecare Settings Dominate as Self-Administration Becomes Standard

Homecare generated 43.67% of 2025 turnover and will expand at a 10.45% CAGR through 2031 as patients prefer managing therapy at home. A 2024 survey found 78% of U.S. pump users favor self-care without routine clinic visits. Hospitals and specialty clinics supplied 38% of 2025 revenue, anchored in complex cases like pediatric initiations. Ambulatory surgery centers added 12% of revenue and are rising as diabetes-related procedures move outpatient.

Medicare introduced CPT codes 99457 and 99458 in January 2024, paying doctors for remote review of device data, which incentivizes connected pump prescriptions. Hospitals aim to discharge patients on the same device they will use at home, promoting pen or patch pump adoption. Surgical centers now rely on continuous glucose monitors and automated pumps to maintain safe glucose during procedures, cutting infection rates by 18%. Homecare uptake will continue as telehealth visits replace in-person check-ups.

Geography Analysis

North America is expected to record the highest regional growth at a 9.05% CAGR through 2031 on the back of high pump penetration and broad reimbursement. Medicare’s 2024 decision to cover tubeless pumps removed historic delays in the 65-plus cohort. Canada added connected pens to provincial formularies in 2025, lifting smart-pen prescriptions by 52%. Mexico’s social-security system started funding patch pumps in February 2025, though supply constraints limited early uptake. U.S. pump penetration in type 1 diabetes reached 63% in 2025; growth now leans on type 2 patients.

Europe held roughly 28% of 2025 turnover. Germany funded connected pens at EUR 120 per unit starting January 2025. France reimburses smart pens when paired with CGM, lowering hypoglycemia events by 28%. The United Kingdom signed a GBP 180 million framework with Medtronic and Insulet in June 2024 to deploy 100,000 hybrid closed-loop pumps by 2026. Southern Europe trails due to mixed reimbursement, while Eastern Europe still favors disposable pens. Ypsomed’s alliance with Biocon is beginning to change that dynamic.

Asia-Pacific accounted for 38.55% of 2025 revenue, supported by expanding reimbursement and rapid uptake of lower-cost patch pumps. China now reimburses up to 70% of pump cost for urban employees, driving 200,000 Medtrum shipments in 2025. India’s Ayushman Bharat pilot covers pumps in five states but faces clinician shortages. Japan approved Terumo’s dose-memory pen in April 2024 to serve 11 million diabetics who mainly use pens. South Korea added hybrid closed-loop systems to its insurance catalog in August 2024, spurring 41% pump growth. Southeast Asia remains syringe-heavy, yet online pharmacies are improving pen access in urban areas.

Middle East and Africa plus South America combined for about 10% of 2025 turnover. Gulf states now fund patch pumps for citizens, with Saudi Arabia approving reimbursement in March 2025. South Africa’s private plans cover pumps, but public patients rely on syringes. Brazil began a pen pilot in two major cities in mid-2025 that could reach 16 million users by 2028. Argentina’s currency devaluation lifted import prices, forcing many patients back to syringes. Sub-Saharan Africa faces cold-chain gaps that restrict cartridge distribution.

Competitive Landscape

Key companies include Novo Nordisk, Eli Lilly, Medtronic, Insulet, and others. The market is moderately concentrated. Novo Nordisk and Lilly dominate the pen segment through vertical integration of drug and device, bundling to secure formulary status. Medtronic’s MiniMed 780G and Insulet’s Omnipod 5 anchor the pump segment, each differentiating through algorithms and form factor. Tandem is gaining pump share with its Control-IQ system, which raised time-in-range by 14% versus older devices in a 2024 trial.

Chinese entrants, including Medtrum and Jiangsu Delfu, undercut on price by up to 50%. Bigfoot Biomedical won FDA clearance in November 2024 for its Unity smart cap and secured Medicare reimbursement in April 2025, creating a bridge between pens and pumps. Patent activity signals focus on software: Medtronic filed 14 applications in 2024 for predictive low-glucose algorithms, while Insulet filed nine patents for longer-wear adhesives.

Regulation is tightening. The European Union Medical Device Regulation, now fully enforced, adds cybersecurity files to conformity assessment and lengthens market entry by six to nine months for smaller companies. Manufacturers also face supply-chain risk; diversification strategies such as Ypsomed’s Malaysia plant aim to lower resin cost and ensure supply continuity. Despite higher entry barriers, white-space remains in geriatric-friendly screens, jet injectors, and hybrid pumps that accept third-party insulin cartridges.

Insulin Delivery Devices Industry Leaders

Novo Nordisk A/S

Ypsomed Holding Ag

Sanofi S.A.

Tandem Diabetes Care, Inc.

Insulet Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Diabeloop received 510(k) clearance for its DBLG2 interoperable automated glycemic controller, opening the U.S. market.

- January 2026: iCentia raised USD 13 million to advance commercialization of the Kaleido patch pump, bringing the Series D total to USD 98 million.

- December 2025: Cipla launched Afrezza, an orally inhaled, rapid-acting insulin powder in India, offering a needle-free alternative.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the insulin delivery devices market as all mechanical or electronic tools that store and administer therapeutic insulin, including reusable and disposable pens, patch or tethered pumps, smart wearables, standard syringes, jet injectors, and their proprietary reservoirs or cartridges, sold to health-care providers or end users. According to Mordor Intelligence, global revenue from these devices is valued at USD 40.98 billion in 2025.

Scope exclusion: glucose monitors, insulin formulations, and any non-insulin infusion hardware sit outside our coverage.

Segmentation Overview

- By Product Type

- Insulin Pens

- Reusable Pens

- Disposable Pens

- Insulin Pumps

- Tethered Pumps

- Patch / Wearable Pumps

- Automated Hybrid Closed-Loop Systems

- Insulin Syringes

- Needle-Free Injectors

- Jet Injectors

- Others

- Insulin Pens

- By Technology / Connectivity

- Connected (Bluetooth / NFC)

- Non-Connected / Conventional

- By Patient Age Group

- Pediatrics (Less Than 18 yrs)

- Adults (Equal to, More Than 18 yrs)

- Geriatrics (≥65 years+)

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Diabetes Clinics & Centers

- By End User

- Homecare Settings

- Hospitals & Specialty Clinics

- Ambulatory Surgical Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview endocrinologists, pump trainers, procurement officers at hospital chains, and regional distributors across North America, Europe, Asia-Pacific, and GCC states. These conversations validate shipment flows, replacement cycles, and near-term ASP movements that public sources rarely capture.

Desk Research

We start by extracting diabetic prevalence baselines, insulin treatment ratios, customs codes, and published device price filings from tier-1 sources such as the WHO Global Health Observatory, the IDF Diabetes Atlas, U.S. FDA 510(k) and CE mark registries, Eurostat trade databases, and diabetes technology association white papers. Company 10-Ks, investor decks, and patent families gathered through D&B Hoovers and Questel backstop competitive and pricing cues. This list is illustrative; many other open datasets were reviewed to cross-check signals and patch gaps.

Market-Sizing & Forecasting

We rebuild global demand with a top-down prevalence model: treated diabetic population × penetration of each device class × average annual units × ASPs, informed by variables such as insulin-treated share of diabetics, device wear-out intervals, reimbursement thresholds, and regional price corridors. Targeted bottom-up checks, sampled pump shipments, pen needle imports, and retail audits are then overlaid to fine-tune totals. Multivariate regression links forecast drivers, including obesity trend, income per capita, reimbursement expansion, and smart-device uptake, to project values through 2030. ARIMA smoothing handles short-term volatility where primary consensus is thin.

Data Validation & Update Cycle

Outputs face anomaly screens, peer review, and a senior analyst sign-off. Reports refresh annually, while material events, such as major product recalls and reimbursement changes, trigger interim updates so clients receive a live baseline before delivery.

Why Mordor's Insulin Delivery Devices Baseline Inspires Confidence

Published estimates often diverge because firms delimit products differently, apply distinct price erosion curves, or refresh data at varied cadences.

Key gap drivers for this market include whether consumables are bundled, how aggressively ASP declines are modeled, and if developing regions are fully captured before 2030 currency adjustment.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 40.98 B (2025) | Mordor Intelligence | - |

| USD 35.30 B (2025) | Global Consultancy A | Leaves out reservoirs and needles; static pen pricing; uses 2023 prevalence base |

| USD 25.20 B (2025) | Trade Journal B | Tracks only pumps and pens; applies steep 8% annual price erosion; excludes Africa and LATAM |

These comparisons show that when scope breadth, variable selection, and update cadence differ, headline numbers can swing widely. Our disciplined prevalence model, reconciled with real-world shipment checks, delivers a balanced, transparent baseline that decision-makers can retrace and replicate easily.

Key Questions Answered in the Report

How large will the insulin delivery devices market be in 2031?

It is projected to reach USD 49.23 billion by 2031, reflecting a 7.82% CAGR from 2026.

Which product type is growing fastest?

Insulin pumps are growing at 11.33% CAGR through 2031 on the strength of hybrid closed-loop approvals.

Why are connected devices gaining share?

Reimbursement policies now classify smart pens and pumps as durable equipment, and cloud links enable remote monitoring that clinicians value.

What is the biggest restraint in emerging markets?

High average selling prices versus multiple daily injections reduce uptake, trimming CAGR prospects by 0.9%.

Page last updated on: