Varicose Veins Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.78 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

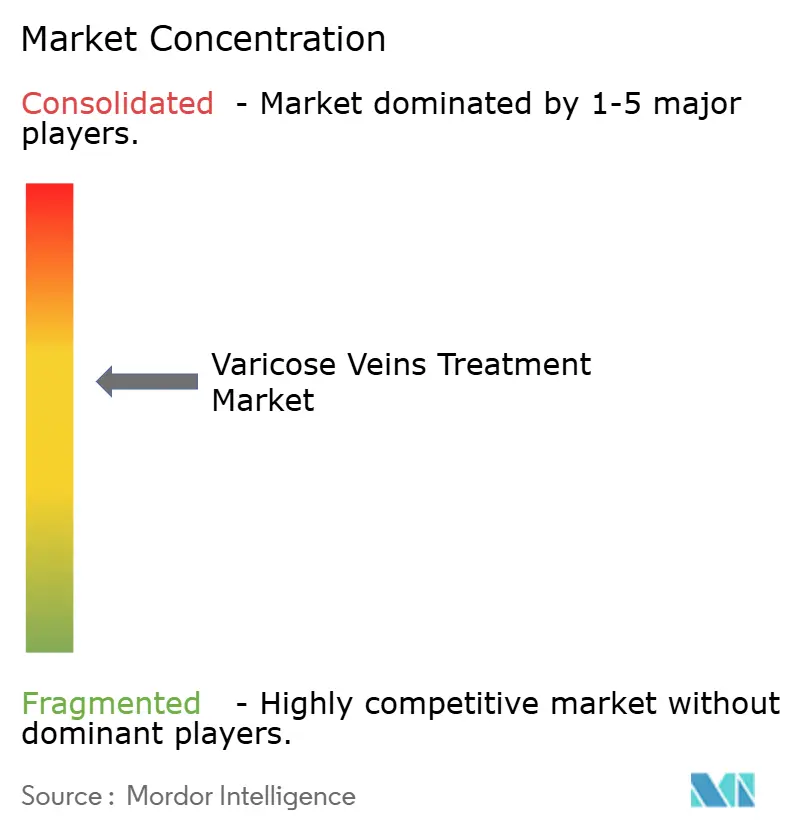

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Varicose Veins Treatment Market Analysis by Mordor Intelligence

The global varicose veins treatment market size in 2026 is estimated at USD 1.39 billion, growing from 2025 value of USD 1.32 billion with 2031 projections showing USD 1.78 billion, growing at 5.12% CAGR over 2026-2031. Expansion is driven by the accelerated adoption of minimally invasive therapies, the rising prevalence of obesity-linked venous disease, and expanding insurance coverage, which collectively reinforce patient demand. North America remains the most significant regional contributor, while aggressive capacity additions in Asia-Pacific point to a rising procedural volume that will reshape global revenue distribution. Portfolio diversification among medical-technology leaders is intensifying, exemplified by Boston Scientific’s 2024 acquisition of Silk Road Medical, which underscores a shift toward comprehensive vascular solutions. The growing preference among physicians for endovenous techniques continues to displace traditional surgery, and specialty vein clinics are leveraging telehealth triage to capture an expanding outpatient clientele.

Key Report Takeaways

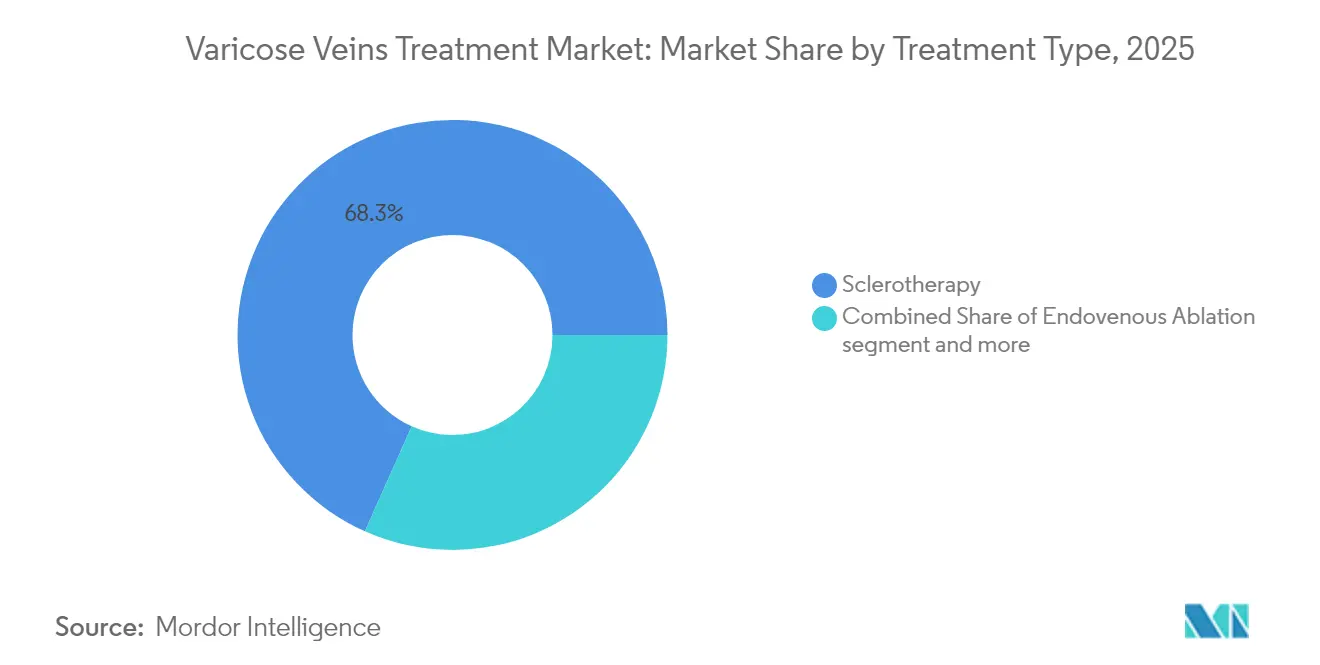

- By treatment type, sclerotherapy accounted for 68.32% of the varicose vein treatment market share in 2025, while endovenous ablation is projected to expand at a 6.87% CAGR through 2031.

- By product, ablation devices led with a 46.45% revenue share in 2025; support devices are expected to post the fastest growth of 6.31% CAGR through 2031.

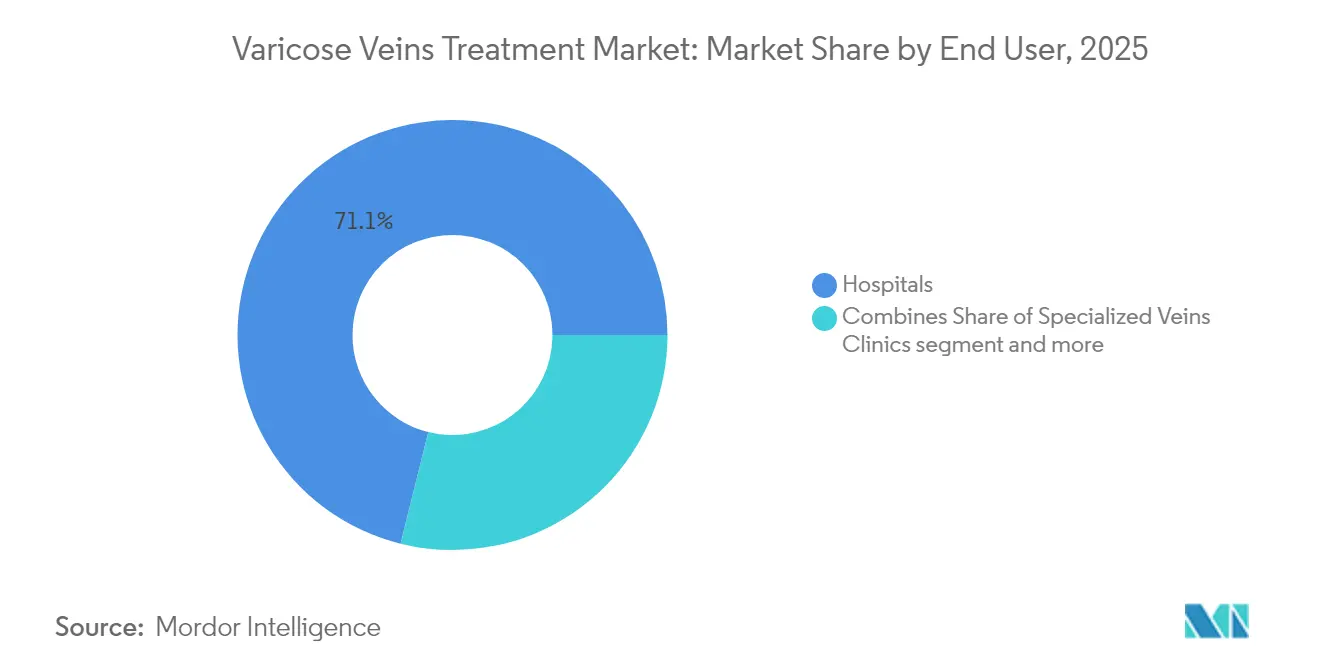

- By end user, hospitals accounted for 71.12% of the varicose vein treatment market size in 2025, whereas specialty vein clinics are expected to advance at a 6.78% CAGR between 2026 and 2031.

- By vein type, significant saphenous vein interventions accounted for 63.05% of the varicose vein treatment market share in 2025. Perforator and accessory veins represent the fastest-growing segment, with a 7.22% CAGR from 2025 to 2031.

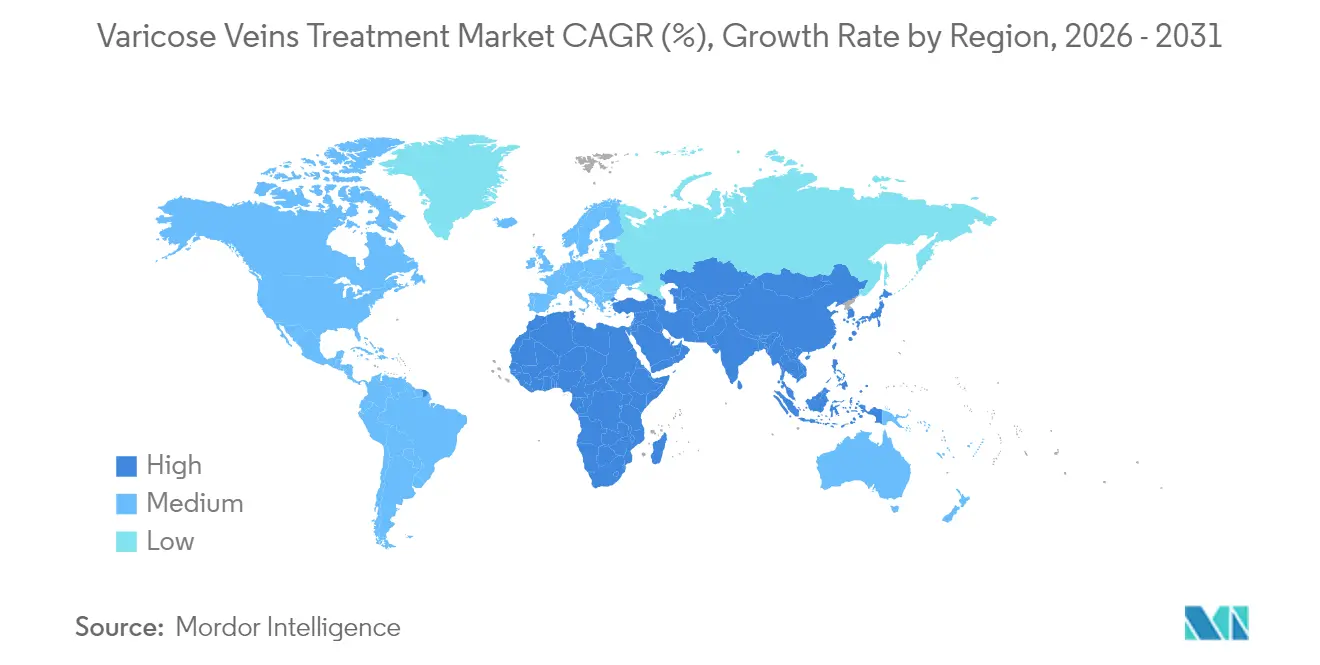

- By geography, North America dominated the market with a 42.85% revenue share in 2025; however, the Asia-Pacific region is poised to grow at a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Varicose Veins Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for minimally invasive surgeries | 1.80% | Global (early adoption in North America & Europe) | Short term (≤ 2 years) |

| Obesity-driven chronic venous insufficiency | 1.20% | Global, notably North America and emerging Asia-Pacific | Medium term (2–4 years) |

| Medicare reimbursement expansion for endovenous thermal ablation | 1.50% | United States with spillover to other developed markets | Short term (≤ 2 years) |

| Tele-consult triaging boosting early referrals | 0.90% | North America, Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Surge in office-based vein clinics adopting NTNT technologies across Europe | 0.70% | Europe (Germany, UK, France) | Medium term (2–4 years) |

| Rapid uptake of cyanoacrylate adhesive closure systems in Middle-Eastern private hospitals | 0.40% | Middle East (GCC countries) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Minimally Invasive Surgeries

Patients are increasingly opting for outpatient solutions that shorten recovery time and minimize scarring. Endovenous ablation, cyanoacrylate closure, and foam sclerotherapy now dominate the varicose vein treatment market, offering clinical efficacy comparable to open surgery with fewer complications. VenaSeal achieves a 94.6% five-year closure rate, allowing for an immediate return to activity and illustrating the competitive edge of catheter-based systems. The shift is accelerating the retirement of vein stripping, redirecting capital toward radiofrequency generators, endolaser consoles, and NTNT technologies that fit office-based workflows. As device portfolios broaden, technology leaders differentiate through lower recurrence rates and simplified anesthesia requirements. Product positioning centered on patient convenience has become a central marketing pillar that resonates across both self-pay and reimbursed channels.

Obesity-Driven Chronic Venous Insufficiency

Escalating obesity prevalence correlates with heightened venous hypertension, propelling demand for interventional care. Overweight individuals experience a 1.5-fold greater risk of varicose pathology because excess weight impairs venous valve competence. Women with elevated BMI report lower quality-of-life scores and higher pain indices, pushing providers to recommend definitive procedures earlier in the disease course. This demographic trend expands the varicose vein treatment market by amplifying the need for compression therapy, ablative devices, and follow-up diagnostics. Device makers respond with larger-diameter catheters and enhanced delivery systems to accommodate diverse vein calibers. Public health initiatives that encourage weight reduction indirectly support procedure volume by improving caregiver awareness and referral patterns.

Medicare Reimbursement Expansion for Endovenous Thermal Ablation

Regulatory support in the United States now classifies endovenous ablation and related therapies as medically necessary when conservative measures fail, shifting a substantial senior cohort into the insured addressable base. Coverage of USD 1,814 per procedure in ambulatory centers, minus a USD 362 patient responsibility, has catalyzed a shift from hospital to office settings. Specialty vein clinics capitalize on favorable economics to scale geographically, investing in ultrasound suites and disposable-light devices that optimize throughput. The reimbursement expansion lifts utilization rates, enabling manufacturers to forecast more predictable stocking, and reinforces physician confidence in investing in new generator platforms. Secondary effects include faster technology iteration cycles and heightened demand for adjunct accessories such as disposable sheaths and closure catheters.

Tele-consult Triaging Boosting Early Referrals

Standardized remote algorithms, such as VELTAS, segment patients by urgency, allowing primary care teams to route complex venous cases to specialists in days rather than months. Earlier referral stalls disease progression, reduces ulcer development, and enlarges the varicose vein treatment market size by capturing cases that historically lingered untreated. Telehealth monitoring also drives compliance, with reminder systems prompting the use of stocking and follow-up visits. Rural patients gain access to metropolitan expertise, expanding geographical penetration without bricks-and-mortar investment. Digital engagement metrics further help clinics refine marketing spend and identify underserved micro-regions. Device makers now bundle tele-monitoring applications with procedure kits, embedding themselves throughout the care pathway.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket cost | −1.2% | Global, particularly emerging markets with limited insurance coverage | Medium term (2–4 years) |

| Safety concerns | −0.8% | Global | Short term (≤ 2 years) |

| Stock-outs of sclerosant drugs in sub-Saharan public hospitals | −0.3% | Sub-Saharan Africa | Medium term (2–4 years) |

| Rigid laser-ablation credentialing rules slowing adoption in Japan | −0.2% | Japan | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost

Procedures deemed purely cosmetic often fall outside insurance coverage, requiring patients to self-fund multiple sessions and ancillary imaging. Emerging markets feel the pinch more acutely where payer networks remain nascent, dampening penetration of premium catheters and specialty adhesives. Providers respond by offering flexible payment plans and batching bilateral treatments to reduce per-leg cost, yet price sensitivity persists. The constraint steers some patients toward compression-only management, slowing adoption curves in lower-income segments. Equipment makers are therefore engineering simplified RF consoles with modular pricing to address clinics in cost-constrained geographies.

Safety Concerns

Skin burns, nerve injury, and thromboembolic events associated with thermal ablation temper physician enthusiasm, especially in outpatient centers lacking immediate surgical backup. Non-thermal alternatives pose allergy risks, necessitating the implementation of patch testing protocols that add logistical complexity. Variability in operator technique magnifies complication rates, thereby raising credentialing thresholds in markets such as Japan. Manufacturers mitigate perceptions through long-term registries, dual-heating-length catheters, and disposable fiberoptic tips that safeguard surrounding tissue. Robust safety data become critical in tender evaluations, and companies with superior profiles win hospital formularies more readily. The restraint nudges research toward next-generation pulsed-field or mechanochemical systems promising minimal collateral damage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Endovenous Ablation Leads Shift From Surgery

Sclerotherapy accounted for 68.32% of 2025 revenue, reflecting its versatility in treating small-diameter vessels and spider veins. Endovenous ablation, however, is registering a 6.87% CAGR that lifts its contribution to the varicose vein treatment market over the forecast horizon. The technique’s success rides on devices such as ClosureFast, which posts 91.9% closure and 94.9% reflux-free outcomes five years after intervention. With each clinical update, payers become increasingly comfortable funding ablation as a first-line option, thereby displacing ligation and stripping.

Technological momentum now centers on non-thermal, non-tumescent systems, such as ClariVein MOCA, which combines mechanical agitation with sclerosant delivery. Cyanoacrylate adhesive closure further enhances patient satisfaction by eliminating post-procedure stocking requirements, which are critical for compliance in warmer climates. These innovations reduce anesthesia time and enable same-room turnover, advantages that specialty clinics leverage to achieve higher daily procedure volumes. As a result, segment analysts expect a continued reweighting toward catheter-based interventions within the varicose vein treatment market.

By Product: Support Devices Gain Momentum

Ablation platforms generated 46.45% of 2025 sales, underscoring the primacy of RF and laser consoles. Yet, accessories and compression products are growing at a rate of 6.31% per year, as they underpin peri-procedural success. Graduated stockings remain the mainstay of conservative therapy and post-ablation prophylaxis, endorsed by the American Venous Forum for symptom relief and ulcer prevention.

Foam-injection kits, epitomized by Varithena with its patented Microfoam UDSS technology, reinforce the segment with a ready-to-use formulation that bypasses the need for manual mixing steps. Ultrasound probes, disposable introducers, and fiberoptic light guides round out accessory demand by ensuring accurate vein access and thermal control. The procedural stack, therefore, widens the varicose vein treatment market size through ancillary revenue streams even as console margins compress. Manufacturing roadmaps emphasize ergonomic handles, single-use locking syringes, and color-coded catheter sets to streamline training and inventory tracking.

By End User: Specialty Clinics Challenge Hospital Dominance

In 2025, hospitals dominated the treatment landscape, securing a 71.12% market share, bolstered by established reimbursement flows and robust imaging resources. However, specialty clinics are on the rise, expanding at an annual rate of 6.78%. These clinics are increasingly attracting patients who prioritize swift scheduling and reduced copays. A testament to this trend is the Center for Vein Restoration, which boasts over 200,000 patient interactions annually across its more than 100 facilities.

Clinic operators benefit from compact RF generators and plug-and-play laser modules that fit standard exam rooms, obviating operating-theater overhead. Tele-consult platforms funnel triaged patients directly into same-week appointments, reducing leakage to competing hospitals. This shift redistributes revenue within the varicose vein treatment market, stimulating device OEMs to develop clinic-friendly leasing models and service contracts. Hospitals respond by opening dedicated vein suites and partnering with outpatient chains to preserve referral streams.

By Vein Type: Perforator Veins Present Technical Opportunity

Intervention on the great saphenous vein represented 63.05% of 2025 procedures, driven by its dominance in reflux pathology. Yet perforator and accessory veins are growing at a 7.22% CAGR, as clinical guidelines recommend addressing incompetent perforators larger than 3.5 mm with a duration of more than 500 ms of reflux.

Endovenous laser ablation using 1,320-nm Nd:YAG fibers has proven effective for these anatomically challenging channels, expanding physician comfort. Industry R&D focuses on angled-tip catheters and echo-radiopaque sheaths that navigate tortuous tracks. As knowledge spreads, comprehensive treatment plans are increasingly covering both axial and perforator segments, thereby enlarging the varicose vein treatment market share for specialty devices that address multi-segment disease. Vascular software now maps reflux pathways, guiding staged interventions that improve ulcer healing times and reduce the recurrence of ulcers.

Geography Analysis

North America retained a 42.85% revenue share in 2025, underpinned by advanced imaging infrastructure, high awareness, and favorable Medicare policies that reimburse endovenous ablation after failed conservative care. Hospital chains have expanded their outpatient suites, and payer bundles reward efficiency, allowing clinicians to schedule bilateral procedures in a single visit. Boston Scientific’s launch of the FARAPULSE Pulsed Field Ablation System drove regional sales growth of 13.8% year over year, underscoring a robust appetite for technology.

Europe follows, buoyed by strong public systems in Germany, the United Kingdom, and France that swiftly incorporate evidence-backed devices. The region has adopted NTNT approaches, and regulatory clarity supports rapid rollouts once post-market surveillance confirms safety. Reimbursement parity between RF and laser methods levels the playing field and sparks iterative upgrades, such as dual-heating catheters from BD. Southern European nations mirror adoption patterns with a lag tied to fiscal budgets, yet patient demand remains stable due to high cosmetic expectations. The Asia-Pacific region posts the fastest growth rate of 6.12%, driven by capacity expansion in Japan, China, and India. Japan’s strict credentialing standards slow the adoption of lasers but stimulate innovation in training simulators and e-credential platforms. China’s 2024 approval of FARAPULSE unlocked a population base that can swell the varicose vein treatment market size once urban outpatient chains scale rapid private-insurance growth in India, coupled with rising middle-class incomes, to fuel device imports. Australia and South Korea maintain steady upgrade cycles as clinics retire older diode lasers in favor of RF generators. The Middle East, led by GCC states, adopts premium cyanoacrylate systems as affluent patients prefer compression-free recovery. Sub-Saharan Africa grows from a smaller base; supply chain volatility around sclerosant drugs curtails volume in public hospitals, but private centers in South Africa sustain modest uptake. South America, spearheaded by Brazil and Argentina, experiences rising procedural counts aligned with expanded private coverage.

Regulatory Landscape

In the United States, minimally invasive varicose-vein treatment devices (including endovenous laser and other catheter-based systems) are commonly regulated as medical devices under FDA oversight and often follow the 510(k) pathway, where manufacturers must demonstrate substantial equivalence to a predicate device. A notable compliance change occurred on February 2, 2026, when the FDA transitioned from the Quality System Inspection Technique (QSIT) to a new inspection approach. This has prompted manufacturers and contract manufacturers supplying ablation platforms, catheters, and accessories to update audit readiness and quality-system evidence packages.

In Europe, varicose-vein treatment devices are governed by Regulation (EU) 2017/745 (MDR), with ongoing implementation updates through 2026 and additional support mechanisms such as EMA expert-panel scientific advice for clinical investigation and development strategies for higher-risk devices (notably Class III and some Class IIb). In 2026, Commission Implementing Decision (EU) 2026/1231 updated the list of harmonized standards, reinforcing requirements around areas such as biological evaluation (EN ISO 10993 series) and labeling symbols (EN ISO 15223-1), alongside broader manufacturer information requirements reflected in ISO 20417:2026. These updates increase the documentation and labeling burden for companies commercializing thermal, non-thermal, and sclerotherapy-related device portfolios across EU markets.

Competitive Landscape

The varicose vein treatment market comprises diversified conglomerates and focused vascular specialists competing across RF, laser, sclerotherapy, and adhesive treatment niches. Boston Scientific’s 2024 purchase of Silk Road Medical for USD 1.26 billion and Bolt Medical for up to USD 664 million signals a multi-platform expansion strategy aimed at end-to-end vascular portfolios. Medtronic leverages a decade of ClosureFast and VenaSeal data, touting five-year closure rates above 90% that fortify brand loyalty.

AngioDynamics positions its VenaCure EVLT laser system as a cost-efficient alternative, appealing to budget-conscious clinics. BD’s Venclose catheter features dual heating lengths, allowing physicians to treat a range of vein diameters without switching disposables, thereby simplifying inventory management. Philips’ Duo venous stent, cleared by the FDA in 2024, broadens adjunct device options for patients with concomitant outflow obstruction.

Competitive playbooks center on generating clinical evidence, office-friendly design, and forming global distribution alliances. Firms court outpatient chains with lease-to-own console packages and bundled service agreements that offload maintenance risk. Emerging-market entry strategies feature value-tier RF kits and localized training hubs. Intellectual-property barriers persist in proprietary foam formulations and catheter tip geometries, while service differentiation includes tele-monitoring apps that reinforce postoperative compliance.

Varicose Veins Treatment Industry Leaders

Medtronic Plc

AngioDynamics, Inc.

Lumenis

Teleflex Incorporated

Quanta System (El.en.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clinical shift toward non-thermal, non-tumescent (NTNT) approaches creates room for device and kit suppliers that simplify outpatient workflows and reduce tumescent anesthesia dependence, especially in specialty vein clinics and office-based settings. In April 2026, InVera Medical received FDA 510(k) clearance for the InVera Infusion Device, positioning a non-thermal catheter focused on enhanced sclerosant infusion. The company also communicated 12-month pilot results reporting 90% vein closure with statistically significant quality-of-life improvements. Alongside established catheter-based closure systems, this kind of cleared, procedure-enabling platform expands the innovation surface area around standardized infusion, disposables, and ultrasound-guided technique optimization.

Guideline maturation also supports broader standardization and training, which can widen adoption beyond early adopters into more routine care pathways. The 2025 SCAI Clinical Practice Guidelines for chronic venous disease, endorsed by the Society for Vascular Medicine, provide evidence-based recommendations spanning patient selection, compression therapy, and ablation methods, and explicitly recognize NTNT options as comparable to thermal ablation in appropriate patients. A persistent access gap underpins the opportunity set, with only about 1% of an estimated 120 million people with venous disease in the United States and Europe receiving treatment annually, suggesting potential expansion through earlier referral pathways, clinic network buildouts, and technology that addresses harder anatomies such as perforator and accessory veins through improved deliverability and durable occlusion outcomes.

Recent Industry Developments

- April 2026: InVera Medical received FDA 510(k) clearance for the InVera Infusion Device, a non-thermal catheter designed to enhance sclerosant infusion in chronic venous disease. The clearance adds a new competitive pathway focused on infusion consistency and catheter-enabled delivery rather than thermal energy, supporting broader product differentiation within sclerotherapy-adjacent workflows.

- November 2025: Medtronic announced 12-month clinical results from the VenaSeal Spectrum Program at The VEINS symposium, reporting effectiveness of cyanoacrylate closure and comparative outcomes versus endothermal ablation. The update strengthens long-term evidence for a non-tumescent option and supports physician confidence and payer discussions around minimally invasive alternatives to thermal procedures.

- July 2024: Boston Scientific reported Chinese regulatory approval for the FARAPULSE Pulsed Field Ablation System, expanding the company’s regional reach with an additional high-profile electrophysiology platform. While FARAPULSE is not a varicose-vein therapy, the approval reinforces Boston Scientific’s broader vascular and catheter-based footprint in Asia-Pacific, shaping channel leverage and capital allocation across adjacent endovascular categories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from diagnosing and treating varicose veins using in-clinic and hospital-based procedures and the procedure-linked devices and consumables used to close or remove affected superficial veins, mainly in the lower limbs.

Scope exclusions: Cosmetic topical products, over-the-counter compression stockings sold without a procedure, and standalone teleconsultation fees are excluded.

Segmentation Overview

- By Treatment Type

- Endovenous Ablation

- Radiofrequency (RFA)

- Laser (EVLA)

- Mechanochemical (MOCA)

- Cyanoacrylate Closure

- Sclerotherapy

- Liquid

- Foam

- Surgical Ligation & Stripping

- Others

- Endovenous Ablation

- By Product

- Ablation Devices

- RFA Generators & Catheters

- Laser Consoles & Fibers

- Non-thermal Closure Systems

- Sclerotherapy Injection Kits

- Support Devices & Accessories

- Ablation Devices

- By End User

- Hospitals

- Specialized Vein Centers

- Others

- By Vein Type

- Great Saphenous Vein

- Small Saphenous Vein

- Perforator & Accessory Veins

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia- Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the clinical and utilization backbone before we sized revenues. We relied on reputable public sources such as the Centers for Disease Control and Prevention (CDC), the National Institutes of Health (NIH) and PubMed-indexed journals, the World Health Organization (WHO), and the OECD for healthcare system indicators and population aging context.

To translate disease burden into a treated pool, we reviewed sources such as national health ministry portals, procedure coding and reimbursement references made available by public payers, and peer-reviewed studies that report treatment patterns for ablation, sclerotherapy, and surgical options. We also screened company annual reports, investor presentations, and trusted press coverage, and we used paid subscriptions for company financials and patent databases to cross-check product pipelines and revenue exposure. These sources are illustrative, and many other public and paid references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on validating the treated patient funnel and the real-world mix of settings where procedures are performed, since pricing and volumes can vary between hospitals, ambulatory centers, and vein clinics. We spoke with a balanced set of stakeholders across manufacturers, distributors, vascular clinicians, and procurement or reimbursement-focused roles. We then rechecked assumptions across APAC, EMEA, and the Americas to avoid over-weighting one care pathway.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 42% |

| Mid tier: 56% | Functional/Unit leaders: 39% | EMEA: 31% |

| Smaller Players: 16% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts from a top-down patient and procedure build, where prevalence and diagnosis rates are converted into a treated cohort, which is then split by therapy choice and care setting before revenue is calculated. The model uses practical inputs such as the share of symptomatic patients seeking care, procedure volumes by setting, average devices and consumables used per case (for example catheters, fibers, closure kits, and sclerosant usage), and typical price ranges by region after currency normalization.

Once the demand pool is built, revenues are derived using sampled ASPs and procedure-linked consumption assumptions. The results are cross-checked using selective bottom-up approximations such as supplier revenue exposure, channel feedback on unit shipments, and clinic utilization checks. Forecasting relies mainly on scenario analysis anchored to how clinicians see adoption shifting toward minimally invasive modalities, along with changes in reimbursement support, aging population trends, and elective procedure recovery patterns. When country-level procedure statistics are missing, we bridge gaps using comparable markets with similar demographics and healthcare access, followed by expert confirmation and sensitivity testing.

Data Validation & Update Cycle

Outputs are validated through multiple checks so that one noisy input does not drive the final number. We compare implied procedure counts, device intensity per case, and regional pricing against independent signals, and outliers are reviewed again before sign-off, including a second-pass recalculation by another analyst.

If a large variance shows up, such as an unexpected shift in the procedure mix or a pricing step-change, we re-contact sources and adjust the assumptions with written rationale. Reports are refreshed annually, and interim updates are made when material events occur such as reimbursement revisions, major regulatory clearances, or notable changes in clinical practice patterns. Before delivery, one last update pass is completed so the view reflects the latest available data.

Mordor Intelligence's Varicose Veins Treatment Market Sizing Compared With Other Published Estimates

Published market sizes for varicose veins treatment can differ even when they sound like they cover the same topic, because the counted revenue can shift based on what is treated as a procedure-linked sale versus an adjacent consumer product. Differences also come from the year used for the "current" estimate, the currency conversion timing, and whether the model assumes faster adoption of newer closure techniques.

The main gap comes from whether over-the-counter compression stocking sales and other non-procedural spend are included, where Mordor Intelligence counts only procedure-tied devices and consumables and keeps retail compression and cosmetic topicals out of the market total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.39 B (2026) | |

| Industry Publisher A | USD 1.42 B (2024) | Uses an earlier base year and presents a broader treatment umbrella, which can pull in non-procedural revenue lines, and then applies a longer forecast window that lifts the implied growth path. |

| Healthcare Advisory B | USD 1.11 B (2024) | Anchors to a narrower near-term demand view and applies a more aggressive growth rate, and the mix and pricing assumptions by setting are less clearly tied back to procedure volumes. |

Looking across the three figures, most of the spread is explained by scope choices and timing, rather than a disagreement that patients exist. By keeping the model traceable to treated cohorts, procedure volumes, and per-procedure device and consumable use, the estimate stays easier to reproduce and to update when utilization or pricing shifts.

Key Questions Answered in the Report

What is the projected value of the varicose vein treatment market in 2031?

The market is forecast to reach USD 1.78 billion by 2031.

Which treatment type is growing fastest?

Endovenous ablation is expanding at a 6.87% CAGR through 2031, outpacing other modalities.

How large is North America’s share of global revenue?

North America accounts for 42.85% of worldwide sales in 2025.

Why are specialty vein clinics gaining traction?

Outpatient clinics offer shorter wait times, tele-consult triage, and lower procedural costs, driving a 6.78% CAGR in this end-user segment.

What technology trend is reshaping European practice?

Non-thermal, non-tumescent (NTNT) systems such as mechanochemical ablation and cyanoacrylate closure are seeing rapid adoption across European offices.

Page last updated on: