Market Overview

| Study Period | 2021 - 2031 |

|---|---|

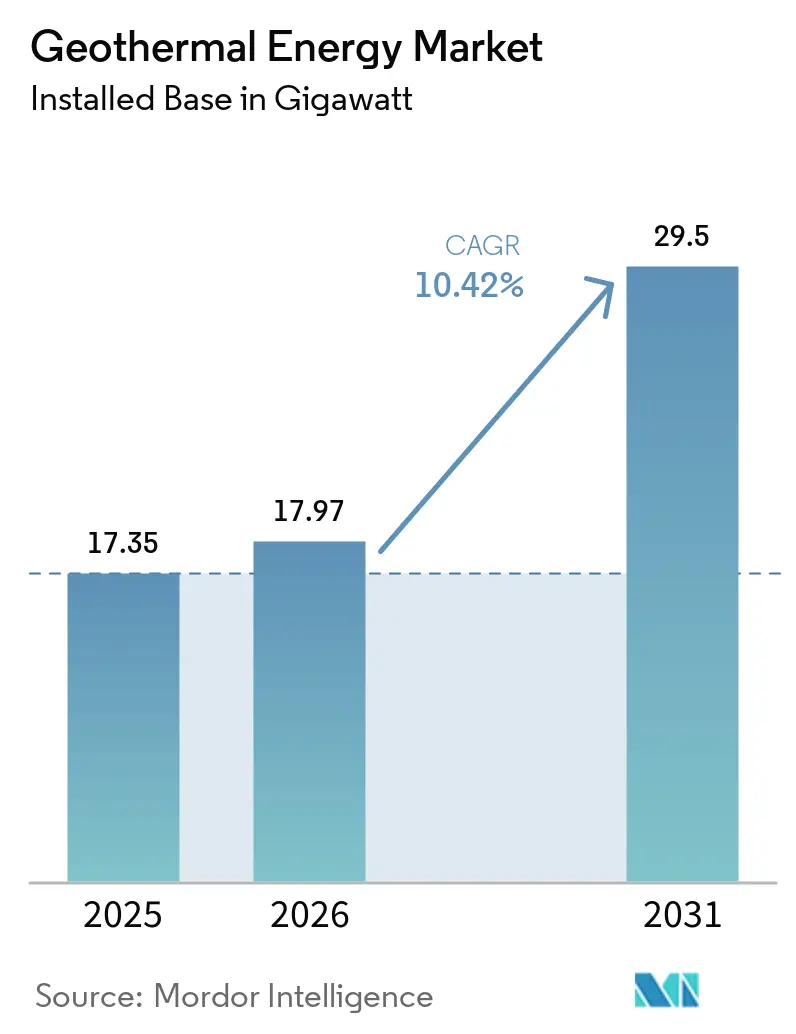

| Market Volume (2026) | 17.97 gigawatt |

| Market Volume (2031) | 29.5 gigawatt |

| Growth Rate (2026 - 2031) | 10.42% CAGR |

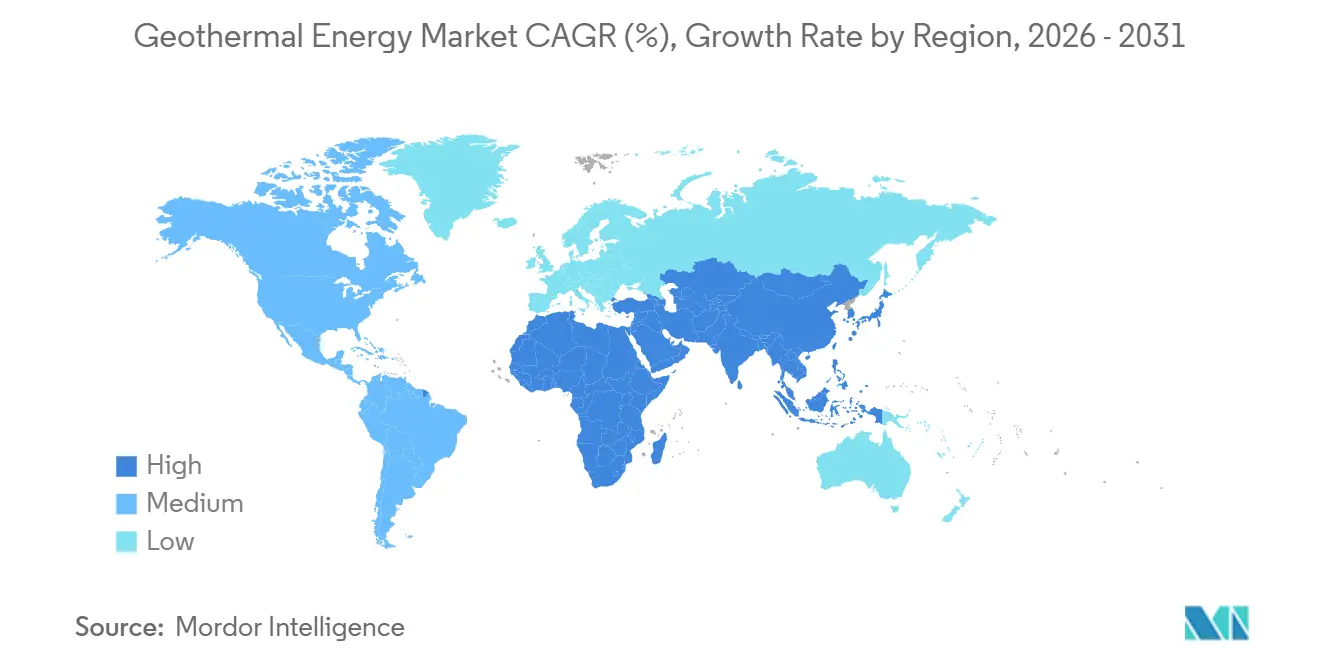

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

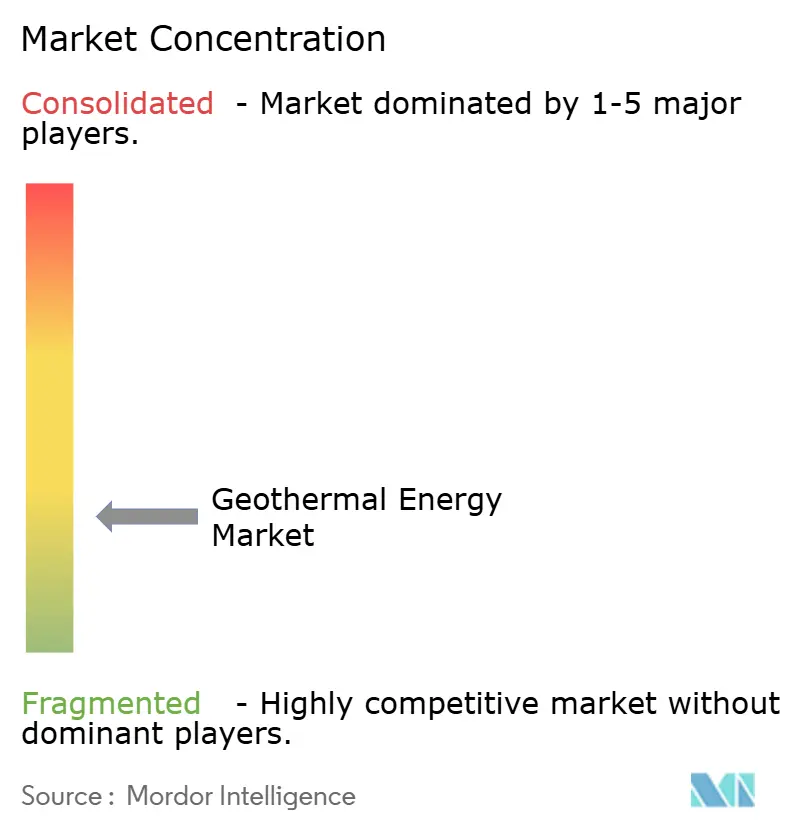

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Geothermal Energy Market Analysis by Mordor Intelligence

The Geothermal Energy Market size in terms of installed base is projected to expand from 17.35 gigawatt in 2025 and 17.97 gigawatt in 2026 to 29.5 gigawatt by 2031, registering a CAGR of 10.42% between 2026 to 2031.

Grid operators are turning to the technology because geothermal delivers continuous renewable power that minimizes balancing costs tied to solar and wind variability. Capacity additions are accelerating in Asia-Pacific as Indonesia and the Philippines monetize volcanogenic reservoirs under new feed-in tariff regimes. Flash-steam plants still dominate installed capacity, yet Enhanced Geothermal Systems (EGS) are scaling quickly as horizontal drilling and hydraulic stimulation adapted from shale operations unlock hot-rock resources. District heating networks in Europe are expanding demand beyond electricity, while recent U.S. federal grants cut exploration risk and draw private capital into pilot projects. Competitive intensity is moderate, with the top developers and state utilities controlling about one-half of installed capacity.

Key Report Takeaways

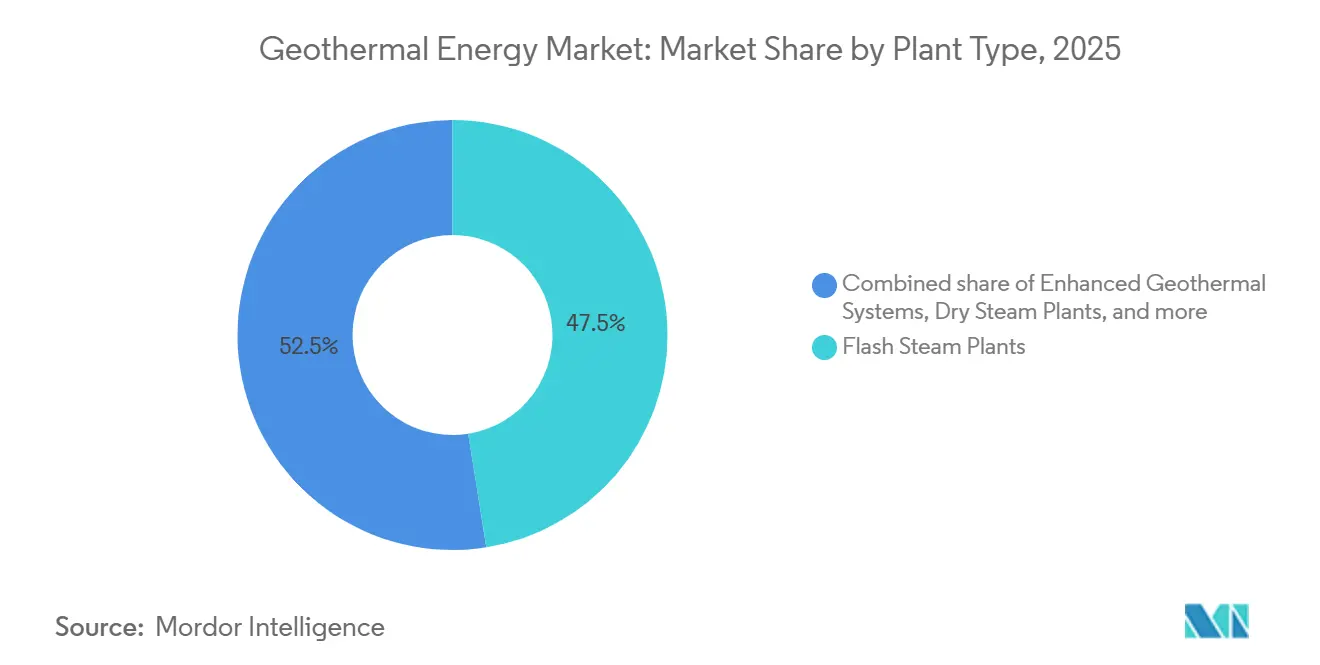

- By plant type, flash steam led with 47.50% of the global geothermal energy market share in 2025, while Enhanced Geothermal Systems posted the fastest growth at an 18.80% CAGR through 2031.

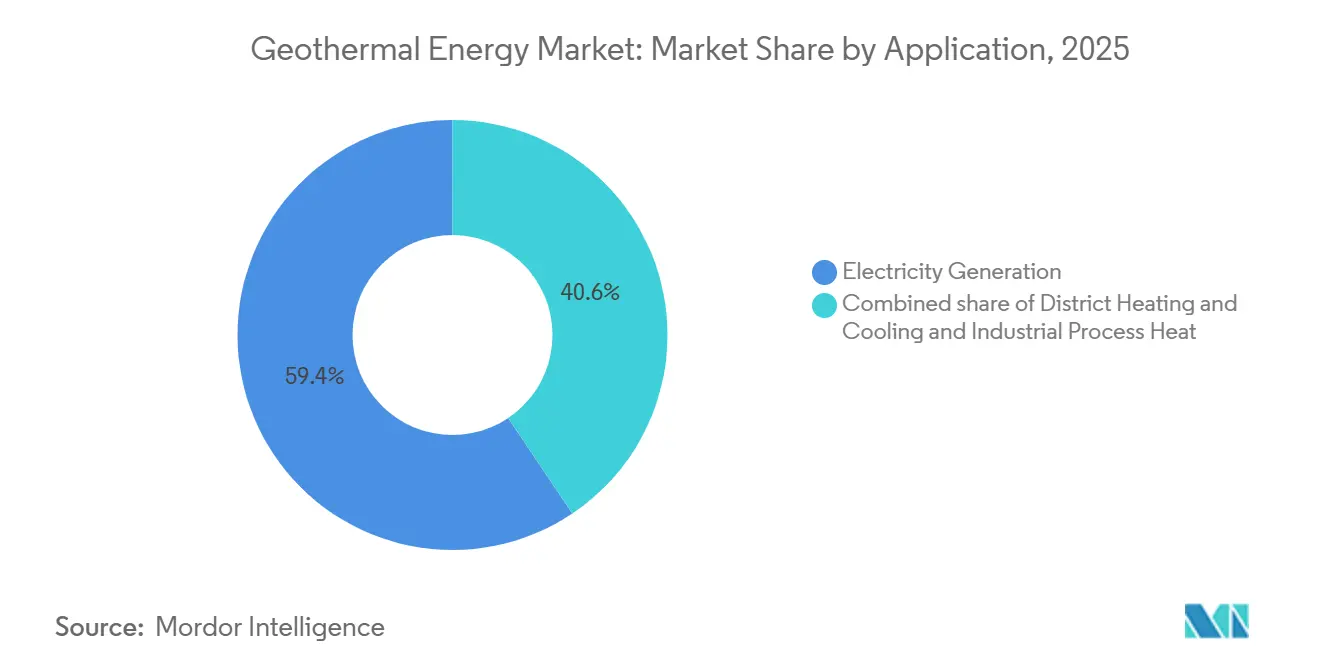

- By application, electricity generation commanded 59.4% of the global geothermal energy market size in 2025 and district heating and cooling is expanding at a 14.5% CAGR to 2031.

- By geography, Asia-Pacific geothermal industry accounted for 44.27% of installed capacity in 2025, and the region is projected to advance at an 11.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Geothermal Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising government incentives & FiTs for baseload renewables | 2.80% | Indonesia, Philippines, Kenya, Turkey, Iceland | Medium term (2-4 years) |

| Growing deployment of geothermal heat pumps | 1.90% | North America, Germany, France, Nordics | Long term (≥ 4 years) |

| Heightened energy-security needs for 24/7 green power | 2.30% | Europe, Japan, South Korea | Short term (≤ 2 years) |

| Repurposing idle oil & gas wells for closed-loop geothermal | 1.50% | United States, UAE, Saudi Arabia | Medium term (2-4 years) |

| Emerging geothermal-to-hydrogen production hubs | 0.90% | Iceland, New Zealand, Utah, Nevada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Government Incentives & FiTs for Baseload Renewables

Feed-in tariffs and capacity payments are reshaping project economics by locking in revenue streams that neutralize exploration risk in the geothermal industry. Indonesia lifted its geothermal tariff to IDR 1,450 per kWh in 2025, a 12% premium that accelerated well-field work in Sumatra and Sulawesi. Turkey extended its tariff guarantee to 2030, triggering eight new binary-cycle plants totaling 320 MW. Kenya introduced sovereign drilling insurance that now covers up to 70% of well losses, directly addressing the single largest barrier to private finance. The European Union shortened geothermal permitting to below 18 months, improving project lead times and bankability. These moves convert speculative acreage into investable assets in markets where solar and wind curtailment already exceeds 15%.

Growing Deployment of Geothermal Heat Pumps

Ground-source heat-pump installations are creating a parallel demand channel for the geothermal industry that is independent of electricity generation. A 30% U.S. federal tax credit drove a 41% year-on-year jump in residential systems during 2025 in cold-climate states. Germany issued 87,000 new permits as gas boilers are phased out under the Building Energy Act. Sweden retrofitted district-heating plants with large-scale pumps that cut operating costs by 35% and improved seasonal performance ratios. Japan earmarked JPY 18 billion in subsidies for commercial retrofits, pursuing a 20% fossil-fuel reduction in buildings by 2028. Contractors see this segment as high margin and low risk because shallow drilling avoids deep subsurface uncertainty.

Heightened Energy-Security Needs for 24/7 Green Power

Geopolitical disruptions have pushed regulators to mandate firm renewable capacity, creating new opportunities for the geothermal industry. The European Union now requires at least 15% of electricity from dispatchable renewables by 2030, explicitly including geothermal. Japan allocated JPY 50 billion for exploration subsidies in regions hit by blackouts during the 2024 winter peak. South Korea’s utility signed a 20-year PPA paying a 22% premium for a 50 MW project that will supply semiconductor plants. The Philippines now requires at least 30% firm capacity in new renewable contracts, effectively mandating geothermal or storage pairing. These policies elevate geothermal from a niche option to a grid-stability necessity.

Repurposing Idle Oil & Gas Wells for Closed-Loop Geothermal

Closed-loop systems lower exploration risk by using known well paths, creating new opportunities across the geothermal industry. Chevron and Baker Hughes began retrofitting 12 depleted wells at California’s Salton Sea in 2025, targeting 5 MW online by Q4 2026 at capital costs 40% below greenfield geothermal. Eavor Technologies achieved an LCOE of EUR 72 per MWh in a German demonstration without induced seismicity concerns. The U.S. Wells of Opportunity program is cataloging 2.3 million orphaned wells, with 18,000 already flagged for temperatures above 150 °C. Saudi Aramco is assessing closed-loop systems to displace oil used for steam injection, highlighting oil-field expertise migration into geothermal. Development cycles in proven basins are dropping from seven years to under three.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront drilling risk & capex | −2.1% | East Africa, South America, Southeast Asia | Short term (≤ 2 years) |

| Cost-competitive pressure from solar & wind | −1.6% | Middle East, Australia, Southern Europe | Medium term (2-4 years) |

| Global shortage of specialised geothermal drill crews | −0.8% | Indonesia, Kenya, Turkey | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Drilling Risk & Capex

Exploration wells succeed only 55%-65% of the time in frontier basins, with dry-hole costs up to USD 8 million, making financing difficult. Drilling consumes 40%-50% of total capex, and one failed well can sink a 20 MW project if permeability is poor. Kenya’s Menengai field saw only a 38% success rate, causing USD 47 million in write-offs and 18-month delays. Indonesia’s Sarulla project ended 23% over budget due to unexpected reservoir compartmentalization. Risk-mitigation funds cover part of the loss, but developers remain exposed to reservoir performance uncertainty, steering capital toward retrofits with known subsurface data in the geothermal industry.

Cost-Competitive Pressure from Solar & Wind

Weighted-average LCOE for utility-scale solar fell to USD 36 per MWh and onshore wind to USD 38 per MWh in 2025, while geothermal averaged USD 68 per MWh. Record-low solar bids under USD 17 per MWh in the Middle East widen the gap further. Auctions in Spain and Australia favored solar paired with batteries over geothermal despite rising curtailment rates. Developers respond by bundling ancillary grid services and targeting industrial offtakers that need an uninterruptible supply, creating new challenges for the geothermal industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plant Type: Flash Dominates but EGS Gains Pace

Flash-steam plants represented 47.50% of capacity in 2025, reflecting their long track record in high-enthalpy zones across Indonesia and the Philippines. The segment benefits from established supply chains and proven reservoir management practices, keeping drilling risk moderate. However, the global geothermal energy market size for Enhanced Geothermal Systems is projected to expand at an 18.80% CAGR to 2031 as shale-style stimulation creates reservoirs in previously uneconomic hot-dry-rock formations. Pilot successes in Nevada and Utah validated cost benchmarks near USD 4.2 million per MW, on par with binary plants in lower-temperature fields. Dry-steam configurations persist at legacy sites like The Geysers but face a gradual decline as vapor-dominated fields deplete. Binary-cycle technology continues to serve low-enthalpy markets in Europe, where organic Rankine turbines cut water use by 85%, strengthening the global geothermal energy industry mix.

EGS momentum is altering supply-chain dynamics. Service companies with horizontal-drilling expertise are entering the market, increasing competition for casing, proppant, and stimulation crews. Equipment vendors respond with modular surface plants that shorten construction timelines. Combined-cycle hybrids that co-locate solar collectors with geothermal wells are emerging in regions with strong isolation, adding daytime output without new turbines and nudging the global geothermal energy market trends toward integrated renewable hubs.

By Application: District Heating Moves into the Spotlight

Electricity generation held 59.4% of 2025 capacity, supported by baseload PPAs in emerging economies. Yet, the global geothermal energy market share for district heating and cooling is set to grow rapidly, with the segment advancing at a 14.5% CAGR through 2031. Paris drilled six new doublets in the Dogger aquifer, and Reykjavik Energy already supplies 95% of buildings with geothermal heat at costs 40% below natural gas. Industrial process heat in food and chemical plants is also expanding, although from a smaller base, thanks to corporate decarbonization targets.

Revenue diversification is improving project economics. Heat-only projects avoid turbine costs and reach breakeven sooner, enticing municipal utilities with limited capital budgets. The global geothermal energy market size for heat applications benefits from year-round load factors and local demand elasticity. Developers increasingly co-locate heat and power facilities to maximize reservoir utilization and lengthen field life. Direct-use clusters in China’s North China Plain illustrate this integrated model, where shallow aquifers supply both residential heating and greenhouse agriculture at one-third the cost of coal boilers.

Geography Analysis

Asia-Pacific held a 44.27% global geothermal energy market share in 2025 and is projected to grow at an 11.9% CAGR through 2031, supported by Indonesia’s plan to commission 3.3 GW of new capacity and the Philippines’ streamlined permitting framework.[1]Ministry of Energy and Mineral Resources, “Geothermal Policy Update 2025,” Government of Indonesia, esdm.go.id Indonesia’s Pertamina Geothermal Energy added 165 MW across three Sumatra fields in 2025, and Star Energy completed a 110 MW expansion at Salak to prolong reservoir life by 18 years. Japan removed drilling limits near onsen resorts, opening 420 km² for exploration and prompting Mitsubishi Power to propose a 30 MW plant in Beppu slated for 2027. China continues to focus on direct-use heating; shallow aquifers in the North China Plain now supply residential heat at one-third the cost of coal boilers.

North America is experiencing a resurgence as the U.S. Bureau of Land Management issued 47 leases covering 78 000 acres in 2025, attracting USD 142 million in bonus bids, the highest since 2008.[2] Ormat Technologies expanded the Steamboat complex by 18 MW using binary cycles that tap 155 °C fluids formerly deemed sub-economic.[3] Canada’s CAD 50 million exploration fund targets retrofits in depleted gas wells, while Mexico’s Comisión Federal de Electricidad maintains 963 MW but lacks fresh projects after 2015 budget cuts in the geothermal industry.

Europe, the Middle East, and Africa reveal contrasting trajectories. Turkey reached 1.7 GW after adding 95 MW of binary-cycle capacity in 2025 under a 10-year tariff guarantee. Iceland’s installed base is steady at 755 MW, with developers now exporting renewable hydrogen from geothermal electrolysis.[4] Kenya lifted its capacity to 985 MW after completing two 35 MW units at Olkaria V, and a further 140 MW is planned at Olkaria I by 2027. Ethiopia’s Tulu Moye project secured a USD 800 million package to target 520 MW by 2029, while Chile’s only operating plant remains Cerro Pabellón at 48 MW amid high Andean transmission costs in the geothermal industry.

Competitive Landscape

The top 10 firms controlled roughly 55% of installed capacity in 2025, indicating moderate concentration that still leaves room for regional specialists. Ormat Technologies, Enel Green Power, and Calpine dominate North America and parts of Europe through vertically integrated exploration-to-operations models. State-owned utilities, Pertamina Geothermal Energy in Indonesia, KenGen in Kenya, and Contact Energy in New Zealand, retain home-market advantages via sovereign risk guarantees and preferred access to high-enthalpy concessions.

Disruptive entrants center on Enhanced Geothermal Systems. Fervo Energy raised USD 244 million in Series C funding in 2024 and signed a 20-year PPA for 320 MW with Southern California Edison in January 2026, the largest U.S. geothermal deal since 2018. Baker Hughes and Chevron formed a joint venture in 2025 to retrofit 12 Salton Sea wells for closed-loop production, cutting capital costs 38% below greenfield benchmarks.

Equipment rivalry is intensifying. Mitsubishi Power, Toshiba Energy Systems, and Fuji Electric compete on turbine efficiency, while Turboden filed 14 organic Rankine patents in 2024-2025 to target low-temperature district-heating retrofits. Service firms with shale-drilling expertise are entering EGS work scopes, increasing demand for high-temperature casing and stimulation crews. This competition, combined with rising hybrid-plant interest, is poised to reshape supply chains and accelerate project timelines across the global geothermal energy market.

Geothermal Energy Industry Leaders

Ormat Technologies Inc.

Enel Green Power

Calpine Corporation

KenGen

Star Energy Geothermal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ormat Technologies entered into a long-term agreement with NV Energy to provide 150 MW of geothermal power to support Google's operations in Nevada. The projects are anticipated to commence operations between 2028 and 2030.

- October 2025: Jindal Power acquires Jhajjar thermal power plant – Jindal Power has agreed to acquire Apraava Energy’s 1,350 MW Jhajjar thermal power plant in Haryana, valued at approximately INR 4,000 crore. This acquisition strengthens its base-load capacity and aligns with its broader energy strategy.

- September 2025: Approval of geothermal projects in India – The Indian government has approved five geothermal energy projects under its new national geothermal policy. These initiatives focus on pilot projects and resource assessment, with potential subsidy support and international collaborations to advance geothermal power, heating, and cooling solutions.

- August 2025: CBRE Investment Management expands geothermal platform – CBRE Investment Management has expanded its Geonova geothermal platform by acquiring Aitoenergia in Finland. This acquisition nearly triples its long-term energy-as-a-service (EaaS) contracts and broadens its sustainable heating solutions in the region.

- June 2025: Ormat Technologies acquires Blue Mountain geothermal plant – Ormat Technologies has completed the acquisition of the 20 MW Blue Mountain geothermal power plant in Nevada from Cyrq Energy for USD 88 million. This purchase adds capacity, includes plans for upgrades, and strengthens Ormat’s clean energy portfolio.

Global Geothermal Energy Market Report Scope

Geothermal energy refers to the heat derived from the Earth's subsurface. It is harnessed by tapping into geothermal reservoirs in regions with high volcanic activity. This renewable energy source can be used for various applications, including electricity generation, direct heating, and industrial processes. Geothermal energy is considered sustainable and environmentally friendly, as it produces minimal greenhouse gas emissions compared to fossil fuels.

The geothermal energy market is segmented by plant type, application, and geography. The market is segmented by plant type into dry steam plants, flash steam plants, binary cycle plants, combined cycle/hybrid plants, and enhanced geothermal systems (EGS). By application, the market is segmented into electricity generation, district heating and cooling, and industrial process heat. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report also covers the market size and forecasts for the geothermal energy market across each region. The market sizing and forecasts for each segment were made based on installed capacity.

By Plant Type

| Dry Steam Plants |

| Flash Steam Plants |

| Binary Cycle Plants |

| Combined Cycle/Hybrid Plants |

| Enhanced Geothermal Systems (EGS) |

By Application

| Electricity Generation |

| District Heating and Cooling |

| Industrial Process Heat |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Philippines | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Kenya | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Plant Type | Dry Steam Plants | |

| Flash Steam Plants | ||

| Binary Cycle Plants | ||

| Combined Cycle/Hybrid Plants | ||

| Enhanced Geothermal Systems (EGS) | ||

| By Application | Electricity Generation | |

| District Heating and Cooling | ||

| Industrial Process Heat | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Philippines | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Kenya | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the geothermal energy market in 2026?

The geothermal energy installed capacity in 17.97 GW in 2026 and is forecast to grow to 29.50 GW by 2031.

What makes Enhanced Geothermal Systems attractive to investors?

EGS projects apply shale-style drilling to create artificial reservoirs, demonstrating costs near USD 4.2 million per MW and 18.80% forecast CAGR through 2031.

Which application segment in geothermal industry shows the highest growth outlook?

District heating and cooling is advancing at a 14.5% CAGR to 2031 as European cities decarbonize legacy heat networks.

How are oil companies participating in geothermal development?

Firms such as Chevron and Baker Hughes retrofit idle wells for closed-loop systems, cutting capital costs by about 40% versus greenfield drilling.

What policy tools are driving new geothermal projects?

Feed-in tariffs, drilling-risk insurance, and accelerated permitting especially in Indonesia, Turkey, Kenya, and the European Union are converting exploration acreage into bankable projects.

Why does geothermal still face cost pressure from solar and wind?

Solar and onshore wind LCOE fell below USD 40 per MWh in 2025, versus geothermal at USD 68 per MWh, forcing developers to monetize geothermal's 24/7 reliability and ancillary services.

Page last updated on: