Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.10 Billion |

| Market Size (2026) | USD 17.07 Billion |

| Market Size (2031) | USD 23.61 Billion |

| Growth Rate (2026 - 2031) | 6.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Textile Market Analysis by Mordor Intelligence

The GCC textile market size is expected to increase from USD 16.10 billion in 2025 to USD 17.07 billion in 2026 and reach USD 23.61 billion by 2031, growing at a CAGR of 6.7% over 2026-2031. Sustained demand from a digitally connected youth population, accelerating e-commerce adoption, and industrial-diversification programs under Vision 2030 and Vision 2040 are strengthening the growth trajectory. Capacity additions in petrochemical feedstocks are trimming synthetic-fiber costs, while near-shoring by European and Middle-Eastern brands is shifting sourcing flows toward the region. Investments in circular-economy infrastructure and advanced nonwoven technologies are widening the product mix and lifting value capture. At the same time, volatile cotton prices and aggressive Asian imports keep pricing pressure elevated and reward vertically integrated, technology-driven players that can respond quickly to demand swings.

Key Report Takeaways

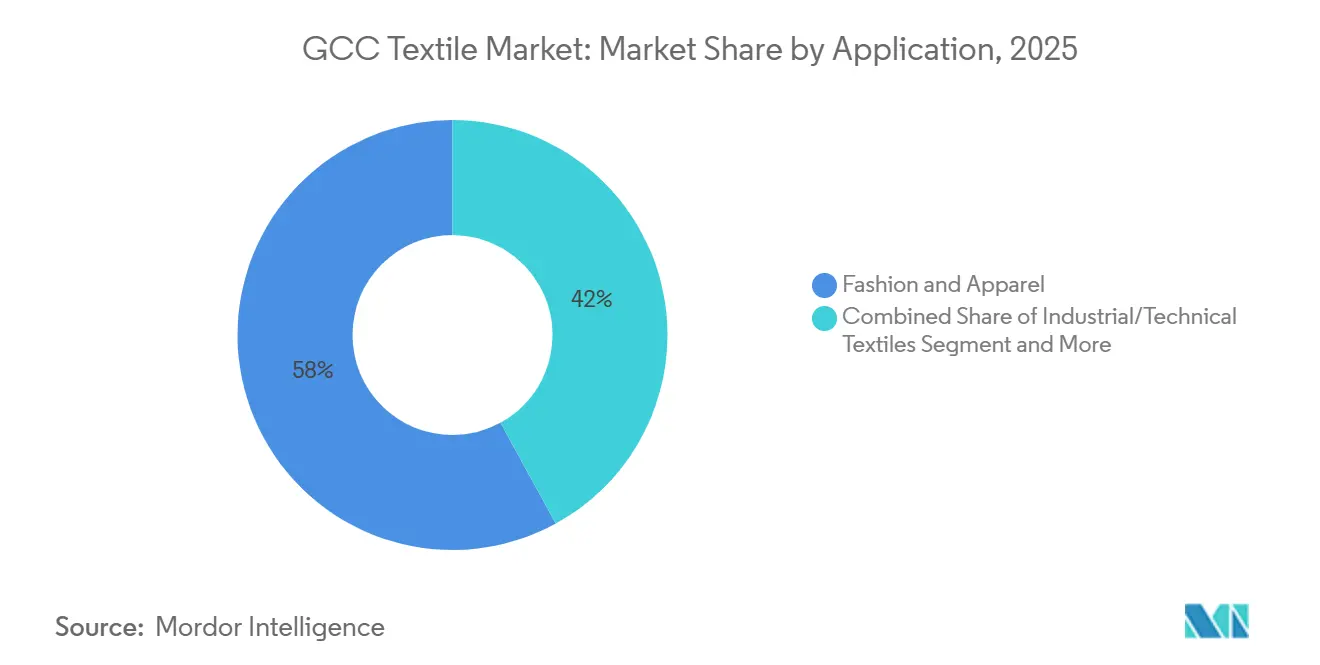

- By application, fashion & apparel held 57.97% of the GCC textile market share in 2025, while industrial/technical textiles are projected to expand at a 7.94% CAGR through 2031.

- By raw material, synthetic fibers commanded 48.87% of the GCC textile market size in 2025. Polyester is forecast to grow at an 8.35% CAGR to 2031 as new polyolefin capacity comes onstream.

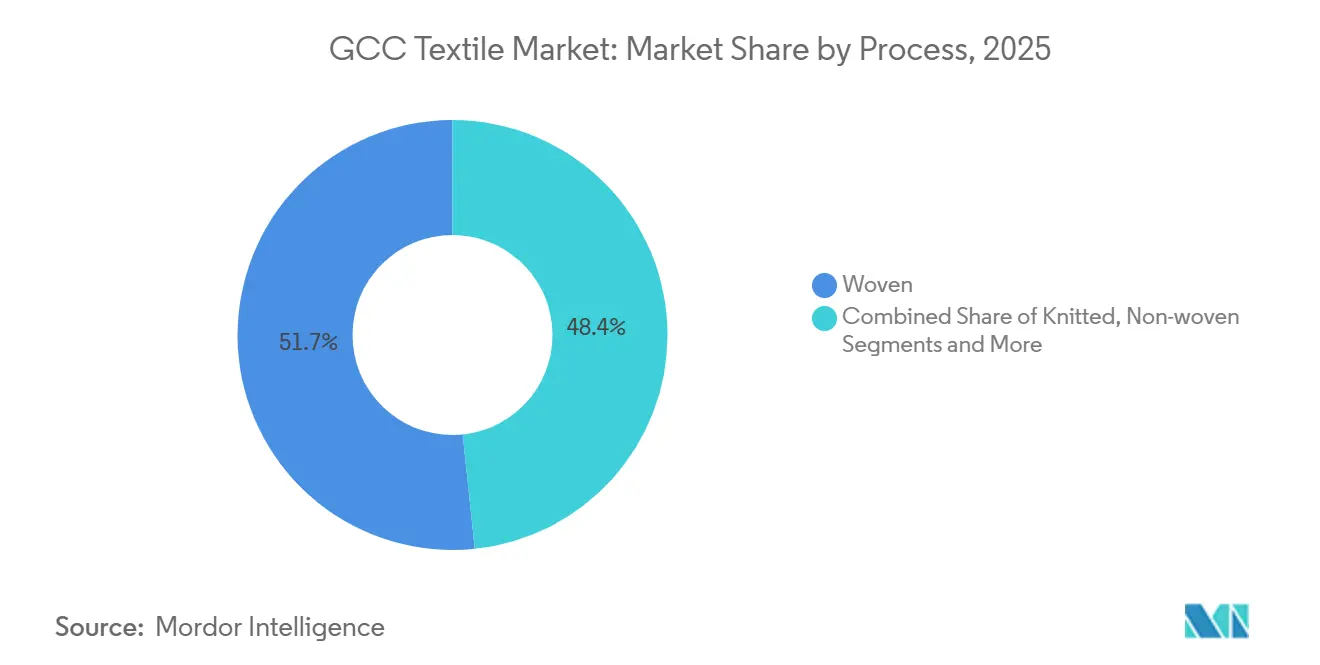

- By process, woven textiles accounted for 51.65% of production in 2025, yet nonwoven textiles are the fastest-growing process at a 7.84% CAGR due to rising hygiene and medical consumption.

- Saudi Arabia led geographically with 38.5% of 2025 revenue, whereas Oman is expected to register the quickest expansion at a 7.59% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Textile Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030/2040 industrial-diversification incentives & subsidies | +1.8% | Saudi Arabia, United Arab Emirates (national programs); spillover to Bahrain, Oman | Long term (≥ 4 years) |

| E-commerce-enabled fast-fashion adoption surge | +1.2% | United Arab Emirates, Saudi Arabia, Qatar (high digital penetration); Kuwait, Bahrain | Medium term (2-4 years) |

| Near-shoring pivot by EU & MENA brands to mitigate supply-chain shocks | +1.0% | Bahrain, United Arab Emirates (re-export hubs); Saudi Arabia (vertically integrated capacity) | Medium term (2-4 years) |

| Fashion-conscious youth cohort expansion | +0.9% | Saudi Arabia, United Arab Emirates, Qatar (60% population under 30); Kuwait | Medium term (2-4 years) |

| Circular economy and textile recycling mandates | +0.7% | Saudi Arabia (Sustainable Ihram Initiative); United Arab Emirates (Tadweer program); regional policy adoption | Long term (≥ 4 years) |

| AI-driven on-demand micro-factory models reducing lead-times & waste | +0.6% | United Arab Emirates, Saudi Arabia (technology hubs); gradual adoption across the GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030/2040 Industrial-Diversification Incentives & Subsidies

Robust policy support is drawing capital into spinning, nonwoven, and technical-textile projects, helping the GCC textile market localize inputs and upgrade technology. Saudi Arabia’s August 2025 regulatory framework synchronizes industrial licensing, environmental compliance, and fire-safety approvals, thereby professionalizing factory operations. Concurrently, targeted financing such as the USD 55 million credit line that funded Al Shair Group’s new staple-fiber plant in Yanbu underlines lender confidence. Oman’s Ladayn Polymer Programme, backed by USD 104 million, replicates this model by bundling feedstock supply with offtake agreements. These initiatives are extending the regional value chain, but long gestation periods mean the full output uplift will arrive after 2028.

E-Commerce-Enabled Fast-Fashion Adoption Surge

Mobile penetration above 95% in the UAE and Saudi Arabia is accelerating direct-to-consumer sales and putting a premium on speed-to-market. Omnichannel revenue expanded 21% between 2019 and 2023, with click-and-collect now accounting for a quarter of sales for leading retailers. The result is compressed production cycles that favor local mills capable of replenishing inventories within days rather than weeks. Rising female labor-force participation widens the addressable consumer pool, and seasonal peaks tied to Ramadan and national holidays further stress supply chains. Manufacturers adopting agile production, real-time inventory tools, and augmented-reality selling are pulling ahead of peers confined to long import lead times.

Near-Shoring Pivot by EU & MENA Brands

Red Sea congestion, tariff volatility, and sustainability audits are persuading brands to split sourcing between Asia and the GCC. WestPoint Home’s total outlay of USD 165 million in Bahrain, plus a new 4 million-unit towel line, showcases confidence in the region’s logistics and trade treaties. The launch of KAST W.L.L. in Bahrain, with a USD 5 million spend to supply reinforcement fabrics, further validates the appeal of shorter transit windows for construction and infrastructure clients.[1]BNA, “KAST JV to Produce Technical Textiles in Bahrain,” bna.bh Pending GCC-UK and India-GCC agreements could unlock additional tariff savings, cementing the Gulf as a complementary hub rather than a replacement for Asian capacity.

Circular-Economy and Textile-Recycling Mandates

Public-private partnerships are scaling organized collection and localized processing of post-consumer waste, tightening environmental compliance, and opening a recycled-fiber niche within the GCC textile market. Saudi Arabia’s Sustainable Ihram Initiative recycled 95% of 5 tons of garments during the last Hajj season and retails the regenerated products at a competitive USD 26 price point. In the UAE, Tadweer’s COP28-era program targets diversion of 210,000 tonnes of textiles from landfills each year. Although collection momentum is strong, the lack of large-scale regional re-spinning facilities keeps costs elevated, meaning policy support and consumer education remain critical levers for scale.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cotton and synthetic feedstock prices | -1.1% | Saudi Arabia, Oman (yarn/spinning); UAE, Bahrain (converters/garments) | Short term (≤ 2 years) |

| Margin pressure from low-cost Asian import influx | -0.9% | UAE, Saudi Arabia, Qatar (apparel/fashion segments); Kuwait, Bahrain | Medium term (2-4 years) |

| Rising water-tariffs and carbon-pricing costs in dyeing/finishing | -0.6% | Saudi Arabia, UAE (water-scarce regions with dyeing/finishing operations) | Medium term (2-4 years) |

| Absence of unified GCC textile-safety standards inflating compliance costs | -0.5% | All GCC states (fragmented regulatory landscape) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Cotton and Synthetic Feedstock Prices

The USDA’s December 2025 WASDE report projected global ending stocks at 76.0 million bales as production of 119.8 million bales narrowly tops mill use of 118.6 million bales, signaling continued price volatility.[2]USDA, “World Agricultural Supply and Demand Estimates, December 2025,” usda.gov Cotton futures climbed past 64.5 cents /lb in December 2025 as weaker global demand intersected with dollar softness, boosting spot costs for regional spinners. Polyester tracks oil, so Brent fluctuations feed directly into PET fiber quotes. Counter-measures are emerging: Borouge 4’s 1.4 million-tpa polyolefin line promises to temper synthetic-fiber prices once fully operational, while OQ’s polymer project in Oman adds localized PP supply. Even so, dual exposure to agricultural commodities and crude keeps near-term margin visibility low, forcing mills to hedge or alter blend ratios quickly.

Margin Pressure from Low-Cost Asian Import Influx

Vietnam, Bangladesh, India, and Pakistan collectively exported more than USD 100 billion in textiles in 2025, flooding GCC retail channels with competitively priced apparel. Faster sailing times from Ho Chi Minh City to U.S. West Coast ports relative to Bangladesh have sharpened price competition even for GCC exporters chasing American buyers. Regional producers lacking cost scale must differentiate through sustainability certifications, rapid replenishment, and niche technical offerings. Energy subsidies and proximity to Middle-Eastern consumers help, but the price gap remains a persistent headwind, particularly for commodity knitwear and fashion basics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Technical Textiles Capture Infrastructure Spend

Technical textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles and Others (Protective, Sports Textiles, etc.) are accounted for 42.03% of the GCC textile market size for non-fashion uses in 2025, trailing only fashion & apparel but expanding more quickly at a 7.94% CAGR through 2031. Major construction programs such as NEOM and Diriyah are specifying geotextiles, geocomposites, and reinforcement fabrics to meet stringent engineering codes, lifting large orders for domestic producers. Alyaf Industrial added capacity above 20,000 tpa to service landfill, drainage, and green-roof projects, while KAST W.L.L. is targeting USD 6 million in revenue within three years by localizing fiberglass reinforcements for concrete structures.

Fashion & apparel still led consumption with 57.97% GCC textile market share in 2025, reflecting high discretionary income and luxury retail clusters in Dubai and Riyadh. Yet, rising import substitution in uniforms, automotive fabrics, and medical disposables is tilting capital spending toward technical lines. Nonwoven suppliers such as Saudi German Nonwovens, now operating five Reicofil lines, are capturing hygiene and drape contracts from global majors like Mölnlycke. Over 2026-2031, product development that blends performance with Islamic modest-fashion cues is set to widen margins and smooth demand seasonality.

By Raw Material: Polyester Gains on Regional Capacity Additions

Synthetic fibers held 48.87% of feedstock demand in 2025, and polyester alone is projected to register an 8.35% CAGR to 2031 as fresh polymer output reduces import dependency. Borouge 4 lifts UAE polyolefin capacity to 6.4 million tpa, the world’s largest single-site complex, underpinning cost-competitive staple and filament yarn lines. OQ’s OMR 40 million (USD 104 million) Ladayn cluster extends the benefit to Oman with nine downstream plants producing PP-based fibers and packaging.

Cotton remains strategic for premium shirting and home linens, supported by SV Pittie Sohar’s USD 300 million spinning complex exporting compact yarn worldwide. Still, volatile global harvests and high freight costs push converters to widen polyester blends for stability. Recycled fibers are emerging, yet limited domestic re-spinning capacity and higher conversion costs keep penetration low. Maintaining a balanced raw-material basket shields mills from price shocks and meets varied buyer specifications.

By Process: Nonwoven Expands on Hygiene and Medical Demand

Woven fabrics commanded 51.65% of the GCC textile market size in 2025, anchored in apparel, furnishings, and traditional applications. Nonwoven, however, is forecast to log a 7.84% CAGR through 2031, riding demographic growth in baby diapers, feminine care, and adult incontinence products. Saudi German Nonwovens’ fifth Reicofil 5 line raised total nonwoven output and introduced the premium Sofina series, while Al Shair Group’s new Yanbu plant adds 30,000 tpa of hygiene staples, with expansion to 50,000 tpa planned.

Knitted goods capture the surge in activewear and athleisure, segmenting toward higher-margin stretch and performance fabrics. Spacer and 3-D weaves remain niche but benefit from local demand in automotive seating and footwear components. Investments in melt-blown filtration media for HVAC and industrial dust control show promise as governments tighten air-quality regulations. Process selection is increasingly dictated by end-use compliance standards, reinforcing the shift toward engineered, high-spec nonwoven lines.

Geography Analysis

Saudi Arabia generated 38.5% of GCC textile market revenue in 2025, helped by Vision 2030 incentives, a unified factory-licensing regime, and QR-code traceability rules that elevate compliance and consumer confidence. Capacity expansions in hygiene nonwovens and the Sustainable Ihram recycling pilot illustrate the kingdom’s twin focus on advanced manufacturing and circularity. The planned Sukuk issuance by Takween Advanced Industries underscores active capital-market support for sector growth.

The United Arab Emirates benefits from world-scale feedstock at Borouge 4 and sophisticated logistics that funnel raw materials to converters and finished goods to export lanes. The Emirates also leverages the India-UAE CEPA to position itself as a re-export hub, reinforcing its second-place standing within the GCC textile market.

Oman, while smaller, is the fastest-growing geography at a 7.59% CAGR through 2031, propelled by SV Pittie Sohar’s spinning expansion and the Ladayn Polymer Programme’s downstream cluster. Export-oriented yarn output and favorable free-zone incentives are drawing ancillary investments in fabrics and home textiles. Bahrain and Qatar round out the regional landscape; Bahrain’s liberal trade regime attracted WestPoint Home’s USD 165 million cumulative commitment and the KAST joint venture, underlining how boutique technical-textile capacity can thrive in smaller Gulf economies.

Competitive Landscape

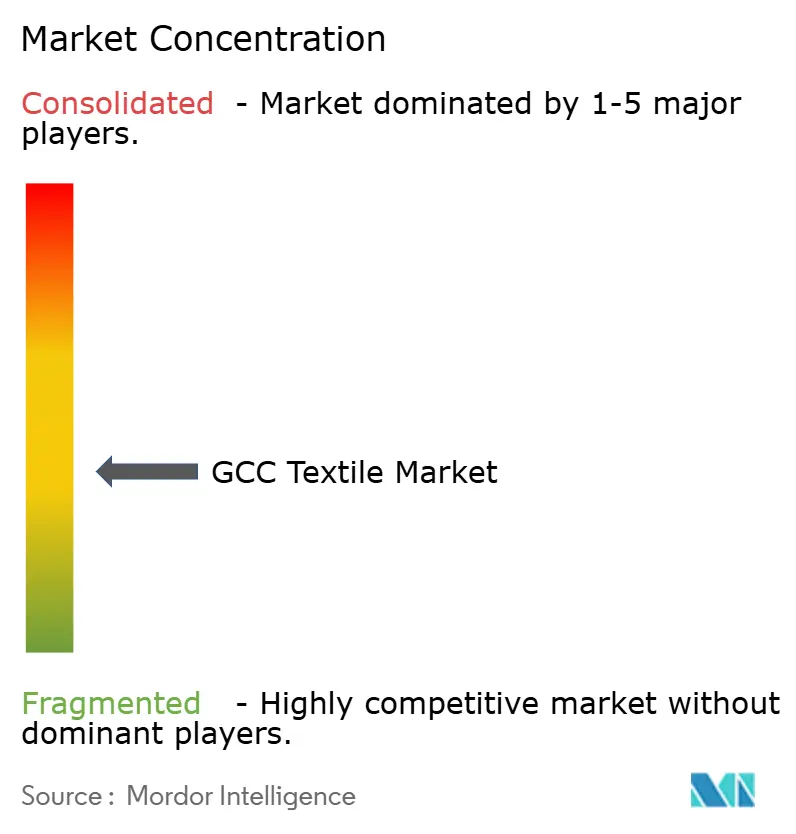

Moderate fragmentation defines the GCC textile market, with regional champions coexisting alongside foreign entrants. Saudi German Nonwovens differentiates through state-of-the-art Reicofil 5 lines and branded offerings that meet European hygiene specifications, securing USD 140 million in 2024 sales. Alyaf Industrial leverages ISO-accredited geosynthetics to win infrastructure contracts from energy majors and global engineering consultants.

Strategic finance is reshaping ownership structures. Takween Advanced Industries’ memorandum to absorb JOFO’s 70% stake in SAAF would consolidate nonwoven capacity under a single Saudi-listed entity, backed by a planned SAR 650 million Sukuk program. Ruya Partners’ USD 55 million credit investment demonstrates increasing appetite for private credit as a tool to accelerate greenfield builds aligned with national diversification goals.[3]Argaam, “Takween Eyes Full Ownership of SAAF,” argaam.com

Technology partnerships and ESG credentials are emerging as competitive moats. KAST W.L.L. couples German process know-how with Gulf proximity to construction end-users, while digital-twin dyeing trials that cut energy use by 12.1% symbolize the cost and compliance gains awaiting early adopters. Suppliers that internalize global buyer protocols such as Inditex’s stricter pH and VOC thresholds secure access to premium channels and mitigate reputational risk.

GCC Textile Industry Leaders

Alyaf Industrial Co. Ltd.

SV Pittie Sohar Textiles

Takween Advanced Industries

Aratex Group

Avgol Middle East

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: OQ commissioned the Ladayn Polymer Programme in Oman, adding nine plants and USD 104 million in investment to supply polypropylene-based textiles and packaging.

- December 2025: Takween Advanced Industries signed an MoU to acquire JOFO’s 70% stake in SAAF, potentially making the unit wholly owned.

- November 2025: KAST W.L.L. launched in Bahrain with USD 5 million to produce fiberglass-reinforced technical textiles.

- September 2025: The Sakhaa Program unveiled plans for a textile-recycling facility in Riyadh to process post-consumer garments.

GCC Textile Market Report Scope

The GCC Textile Market Report is Segmented by Application (Fashion & Apparel, Industrial/Technical Textiles, and More), by Raw Material (Natural Fibers, Synthetic Fibers, and More), by Process/Technology (Woven, Knitted, Non-Woven, and More), and by Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman and Bahrain). Market Forecasts are Provided in Terms of Value (USD).

By Application

| Fashion & Apparel |

| Industrial/Technical Textiles |

| Household & Home Textiles |

| Medical & Healthcare Textiles |

| Automotive & Transport Textiles |

| Others (Protective, Sports Textiles, etc.) |

By Raw Material

| Natural Fibers | Cotton |

| Wool | |

| Silk | |

| Synthetic Fibers | Polyester |

| Nylon | |

| Rayon / Viscose | |

| Acrylic | |

| Polypropylene | |

| Recycled Fibers | |

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) |

By Process / Technology

| Woven | |

| Knitted | |

| Non-woven | Spunlaid (Spunbond / Melt-blown) |

| Dry-laid Hydro-entangled | |

| Wet-Laid | |

| Needle-punched | |

| 3-D Weaving & Spacer Fabrics |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Application | Fashion & Apparel | |

| Industrial/Technical Textiles | ||

| Household & Home Textiles | ||

| Medical & Healthcare Textiles | ||

| Automotive & Transport Textiles | ||

| Others (Protective, Sports Textiles, etc.) | ||

| By Raw Material | Natural Fibers | Cotton |

| Wool | ||

| Silk | ||

| Synthetic Fibers | Polyester | |

| Nylon | ||

| Rayon / Viscose | ||

| Acrylic | ||

| Polypropylene | ||

| Recycled Fibers | ||

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) | ||

| By Process / Technology | Woven | |

| Knitted | ||

| Non-woven | Spunlaid (Spunbond / Melt-blown) | |

| Dry-laid Hydro-entangled | ||

| Wet-Laid | ||

| Needle-punched | ||

| 3-D Weaving & Spacer Fabrics | ||

| By Geography | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

Key Questions Answered in the Report

What is the current value of the GCC textile market?

It was valued at USD 16.10 billion in 2025 and is projected to reach USD 23.61 billion by 2031.

Which segment is expanding fastest within GCC textiles?

Industrial/technical textiles are forecast to grow at a 7.94% CAGR through 2031, outpacing all other applications.

Why is polyester demand rising in the Gulf?

New polyolefin capacity at Borouge 4 and Oman’s Ladayn cluster is lowering feedstock costs, supporting an 8.35% CAGR for polyester fibers.

Which country is the largest market inside the GCC?

Saudi Arabia led with 38.5% of regional textile revenue in 2025.

How are Gulf producers responding to circular-economy pressures?

Initiatives such as Saudi Arabia’s Sustainable Ihram project and the UAE’s Tadweer circularity program are scaling collection and recycling of post-consumer textiles.

What level of competition exists among GCC textile manufacturers?

The landscape is moderately concentrated, with the top five firms controlling roughly 60-65% of revenue, giving mid-sized players room to differentiate through technology and sustainability.

Page last updated on: