Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

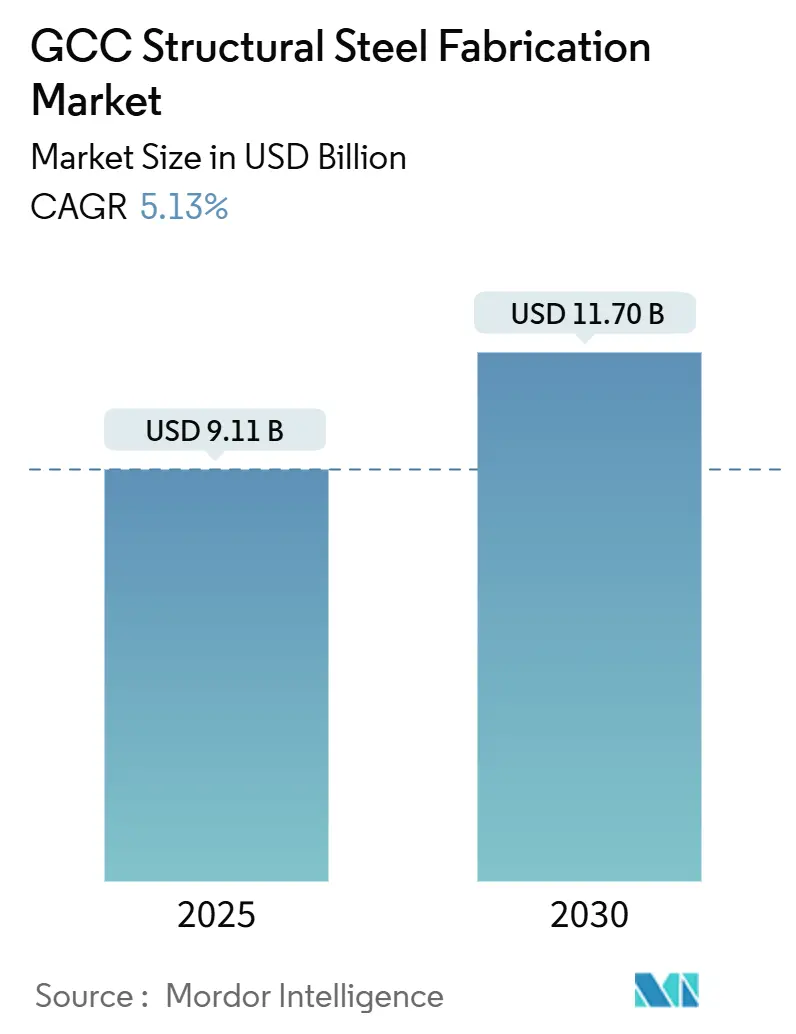

| Market Size (2025) | USD 9.11 Billion |

| Market Size (2030) | USD 11.70 Billion |

| Growth Rate (2025 - 2030) | 5.13% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Structural Steel Fabrication Market Analysis by Mordor Intelligence

The GCC Structural Steel Fabrication Market size is valued at USD 9.11 billion in 2025 and is forecast to reach USD 11.70 billion by 2030, translating into a 5.13% CAGR over the period. The market benefits from Saudi Arabia’s giga-project pipeline, stringent local-content policies, and rapid adoption of modular construction, all of which sustain order books for fabricators even when crude prices fluctuate. Renewable-energy mega-parks, data-center rollouts, and defense stockpiling further diversify demand, while digitization and automation allow leading players to meet tighter delivery windows and ESG requirements. Competitive intensity is moderate, with integrated champions such as Zamil Steel, Emirates Steel, Arkan, and Hadeed defending share through scale, technology upgrades, and low-carbon credentials. Their investments in advanced cutting, welding, and surface-treatment lines create a cost and quality gap that traditional shops struggle to close.

Key Report Takeaways

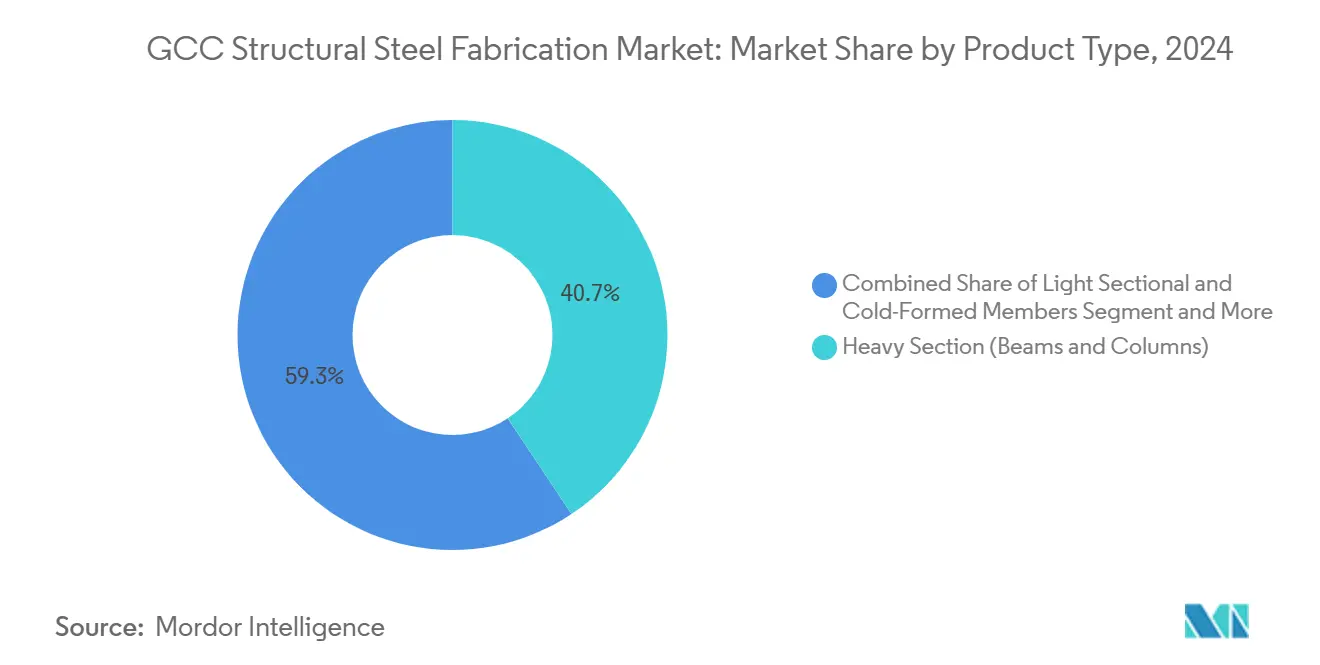

- By product type, heavy sections accounted for 40.67% of the GCC structural steel fabrication market size in 2024; plate-worked girders and custom modules are advancing at a 6.92% CAGR to 2030.

- By end-user industry, construction retained 46.89% of the GCC structural steel fabrication market share in 2024, while infrastructure transport is projected to expand at a 7.17% CAGR through 2030.

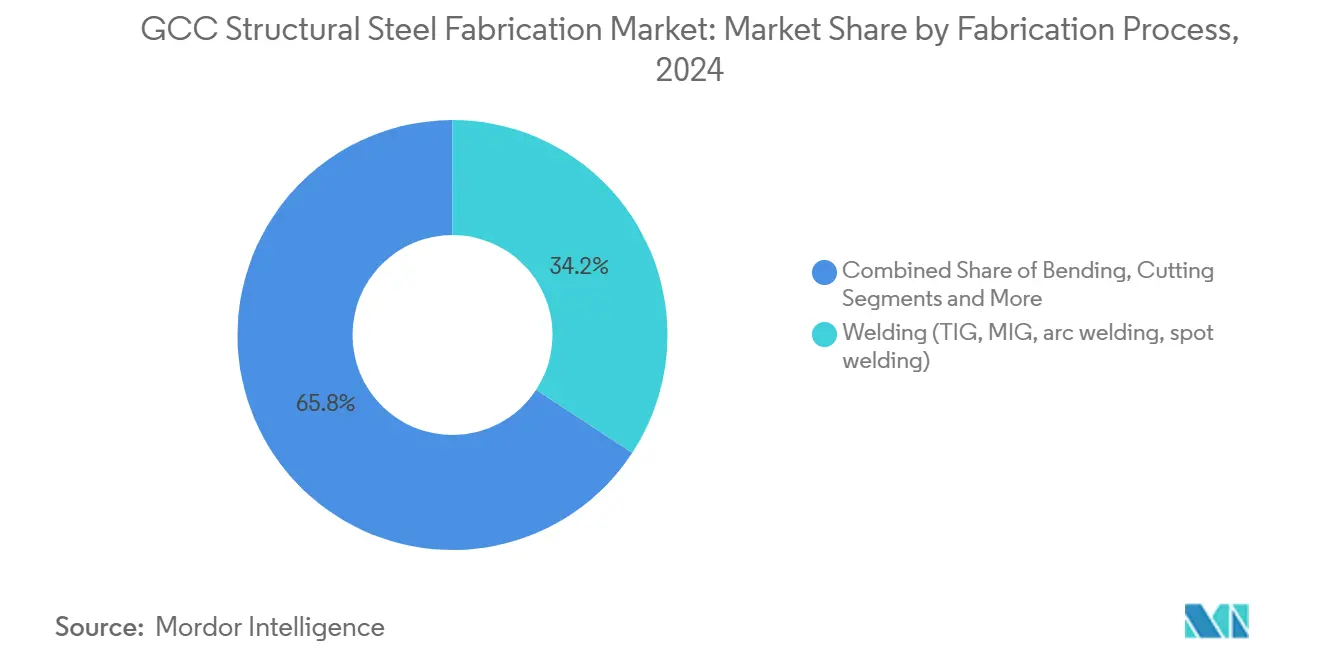

- By fabrication process, welding delivered 34.23% of 2024 revenue; cutting technologies are forecast to grow at a 6.56% CAGR through 2030.

- By geography, Saudi Arabia led with 30.24% revenue share in 2024; Qatar records the fastest forecast CAGR at 6.43% through 2030.

GCC Structural Steel Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated giga-project pipeline | +1.8% | Saudi Arabia's core; spill-over to UAE, Qatar | Long term (≥ 4 years) |

| Mandatory local-content policies | +1.2% | GCC-wide; strongest in Saudi Arabia, UAE | Medium term (2-4 years) |

| Rapid switch to modular construction | +0.9% | Early adoption in Saudi Arabia, UAE | Medium term (2-4 years) |

| Renewable-energy mega-parks | +0.7% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Strategic stockpiling by the defense sector | +0.5% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Growth of data-center colocation hubs | +0.4% | UAE, Saudi Arabia, expanding to Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Giga-Project Pipeline Drives Structural Transformation

The pipeline of record-setting projects such as NEOM, Diriyah, and Red Sea tourism zones is reshaping procurement norms. NEOM alone targets 90% off-site assembly, translating to persistent demand for precision-fabricated beams, trusses, and volumetric modules. Emirates Steel’s supply contract for the Trojena ski village demonstrates how giga-projects pull premium steel grades and traceable low-carbon material into the specification mix. Beyond volume, these projects enforce new digital-twin and sustainability benchmarks that spread to everyday builds, rewarding fabricators that have automated lines and third-party certified EPDs. As schedules stretch over a decade, the pipeline offers unrivaled visibility that underpins multi-year capex decisions.

Mandatory Local-Content Policies Reshape Supply Chains

Saudi Arabia’s target of 75% local value add in oil and gas by 2030, mirrored by In-Country Value programs across the UAE and Oman, is forcing global OEMs to shift sourcing to domestic yards. The Baosteel-Saudi Aramco-PIF plate mill joint venture illustrates how localization requirements attract technology inflows and capital partners that expand regional rolling and fabrication depth. Compliance covers headcount, R&D, and supplier development, so fabricators that invest early lock in framework agreements and preferred status advantages that outlive the policy window[1]Aramco, “Baosteel–Aramco–PIF Plate Mill JV Press Release,” aramco.com.

Modular Construction Revolution Accelerates Market Evolution

Off-site manufacturing cuts GCC job-site labor by up to 60% and shortens project schedules, benefits that resonate in extreme-climate locations. Demand is therefore pivoting from commodity H-beams toward shop-finished volumetric pods and plate-worked skids. Fabricators with BIM-integrated detailing, automated cutting, and robotic welding enjoy higher margins and lower repair rates, positioning them as indispensable partners to design-build contractors. Early movers already report order backlogs exceeding 18 months, validating the strategic shift.

Renewable-Energy Infrastructure Creates Specialized Demand

Utility-scale solar and emerging wind projects require corrosion-resistant pile foundations, single-axis trackers, and inverter platforms that differ materially from building steel. Qatar’s 4 GW renewable target by 2030 underscores the opportunity, with each gigawatt of tracker-based solar needing roughly 40,000 tons of galvanized structural steel. These contracts favor fabricators certified to ISO 1461 hot-dip galvanizing and equipped to batch-produce repetitive components at tight tolerances, expanding the industry’s product palette.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Project-award cyclicality linked to oil | -0.8% | GCC-wide; most pronounced in Saudi Arabia, UAE | Short term (≤ 2 years) |

| Shortage of certified welding inspectors | -0.6% | Global issue; acute in GCC | Medium term (2-4 years) |

| Stringent ESG / embodied-carbon disclosure | -0.4% | GCC-wide; aligned with global standards | Long term (≥ 4 years) |

| Volatile plate-steel import tariffs | -0.3% | Affects GCC exporters to the U.S.; regional flows | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Project Cyclicality Creates Demand Volatility

Fiscal revenues in Saudi Arabia and the UAE still move with Brent prices, so ministries sometimes defer tender awards when receipts dip. The stop-start pattern inflates contractor financing costs and complicates capacity planning for fabricators. Diversified customer portfolios and framework agreements with utility clients help cushion the impact, but smaller shops tied to single contractors face order-book whiplash whenever budgets tighten.

Skilled-Labor Shortages Constrain Capacity Expansion

Only around 6,000 AWS-certified welding inspectors currently work in the GCC, a figure far below the 2026 requirement forecast by the Saudi Council of Engineers. Fabricators must therefore recruit internationally, driving wage inflation and visa processing delays. Remote-inspection technology and up-skilling academies launched by Emirates Steel ease the pain, yet the human-capital gap remains a drag on ramp-up schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heavy Sections Anchor Revenue while Engineered Modules Outpace Growth

Heavy sections such as beams and columns captured 40.67% of 2024 revenue, proving indispensable to stadiums, terminals, and industrial sheds that dominate GCC skylines. Their sheer tonnage keeps most mills running full shifts, and surface-treatment upgrades like robotic blasting position them for long-term relevance. However, engineered products, plate-worked girders, modular skids, and prefabricated pods are growing at a 6.92% CAGR, outstripping commodity profiles. The GCC structural steel fabrication market size tied to specialized components benefits from higher margin potential because each order adds design, machining, and QA services. Zamil Steel’s decision to allocate a third of its 30,000 t/month capacity to modular units illustrates how incumbents pivot toward this premium lane.

Demand for light cold-formed members persists in villa construction, while tubular sections thrive in pipe racks and canopy structures favored by renewable plants. Yet complexity, not tonnage, is now the key profit driver. Fabricators equipped with five-axis CNC drilling lines and automated welding gantries can shave 12% off cycle times, a decisive edge when giga-project lots hinge on time-certain delivery. Consequently, the GCC structural steel fabrication market continues to witness investment in simulation software, laser-cutting cells, and automated plate lines that convert design intent into shop drawings and nesting programs in hours rather than days.

By End-User Industry: Construction Dominates; Transport Infrastructure Accelerates

Construction demanded 46.89% of output in 2024, spanning high-rise towers, malls, and industrial estates that populate Saudi Vision 2030 and Dubai’s Industrial Strategy 2031. Civil contractors rely on mill-certified H-columns and trusses to compress timelines, underpinning stable base-load demand for commodity shapes. Yet transport infrastructure, rail, metro, airport expansions, and port quay walls will post a 7.17% CAGR to 2030, giving it the fastest growth trajectory in the GCC structural steel fabrication market. Rail projects such as Etihad Rail’s Stage 2 and Saudi Arabia’s Land Bridge need long welded box girders and plate-cut diaphragms that few regional players currently master.

Power-and-energy builds, including 400 kV substations and solar tracker parks, add diversification. For example, Masdar’s 2 GW Al Dhafra solar complex required more than 65,000 t of galvanized tracker columns, all sourced domestically. Oil and gas remains steady on the back of brownfield debottlenecking, while defense and data-center segments inject specialist demand for blast-rated or vibration-isolated frames. Fabricators holding ISO 3834 Part 2 and EN 1090 EXC4 certifications capture these regulated niches, expanding margins and extending their project pipelines.

By Fabrication Process: Welding Retains Volume Leadership; Cutting Delivers Technology Upside

Welding processes, TIG, MIG, and submerged-arc, accounted for 34.23% of 2024 revenue, underpinning everything from box columns to pipe racks. Skilled welders and flux-cored equipment remain the backbone of the GCC structural steel fabrication market, but productivity gaps emerge where manual gouging and re-work grow excessive. In contrast, advanced cutting methods, fiber-laser, high-definition plasma, and water-jet are scaling at a 6.56% CAGR as projects demand tighter fit-up and minimal heat-affected zones.

The GCC structural steel fabrication market size linked to digital cutting also benefits from software-driven nesting that lifts material utilization above 90% and shortens move-to-weld timeframes. EMSTEEL’s 2024 commissioning of a 20 kW fiber-laser line with robotic loading illustrates the pivot. Bending, roll-forming, and machining provide value-added steps for curved façades, wind-tower flanges, and high-precision skid frames. Forward-looking plants embed these processes in single-piece-flow cells, reducing WIP and allowing traceable barcode tracking from plate receipt to dispatch.

Geography Analysis

Saudi Arabia held 30.24% of 2024 revenue thanks to a USD 2.7 trillion public-sector pipeline covering NEOM’s 170 km linear city, Diriyah Gate, and 59 industrial clusters slated for completion by 2030. These projects require domestic fabricators to double output by mid-decade, a task eased by Hadeed’s 3.8 million t long-product capacity and new PIF-backed investments in plate mills. Consolidation, seen in Hadeed’s acquisition of AlRajhi Steel, pairs with workforce localization programs to ensure supply security and technology diffusion. Fabricators with in-Kingdom Total Value Add (IKTVA) ratings above 50 already enjoy bid-list priority in Aramco and Ma’aden tenders.

Qatar, although smaller, will grow fastest at a 6.43% CAGR through 2030 as LNG expansion, Sharq Crossing, and 4 GW of renewables extend the post-World Cup building boom. Local yards pivot from stadium roofs to offshore jackets, exemplified by the six-platform EPC contract QatarEnergy awarded in 2024, which allocated over 120,000 t of steel fabrication to regional vendors. Complementary government programs, such as mandatory carbon footprints for state projects, further stimulate upgrades in galvanizing and blasting capacity[2]QatarEnergy, “North Field Expansion Factsheet,” qatareenergy.qa.

The UAE balances diversified demand across tourism, logistics, and industrial segments. Emirates Steel Arkan reported USD 1.08 billion revenue in H1 2024, buoyed by domestic orders that offset weak export margins as global prices softened. Abu Dhabi’s “Make it in the Emirates” initiative offers subsidized loans for digital retrofits and green hydrogen pilots, positioning the federation as the region’s low-carbon steel trailblazer. Kuwait, Oman, and Bahrain provide niche volumes tied to petrochemical revamps and port developments, and common GCC tariff shields against low-priced imports cement a regional production bloc that shares capacity during peaks and troughs.

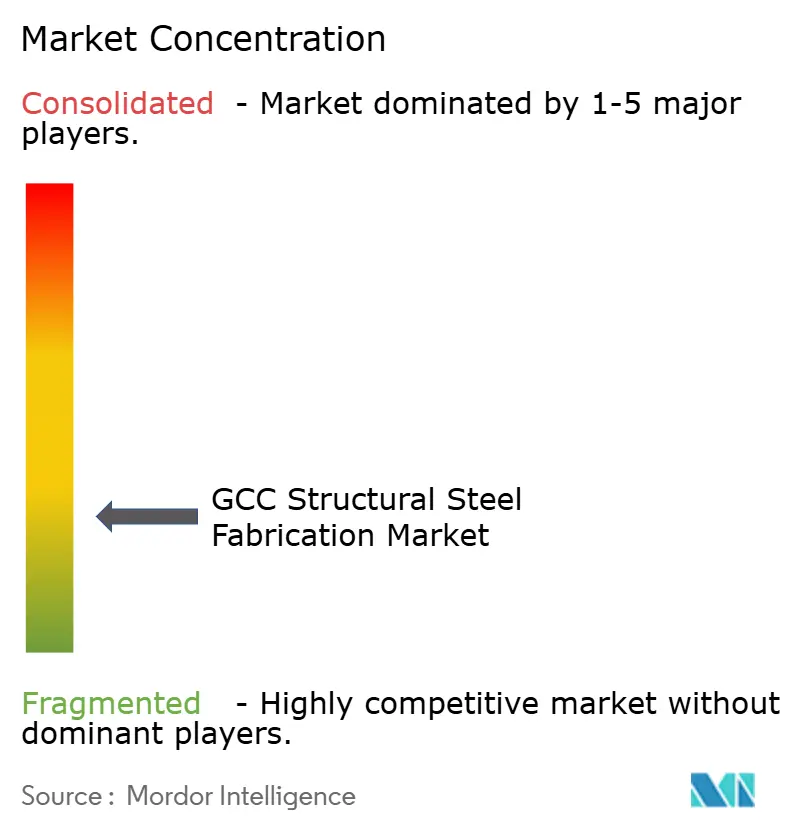

Competitive Landscape

Competition centers on the ability to combine scale, technology, and ESG credentials. Zamil Steel leverages nine factories across Saudi Arabia, the UAE, Vietnam, and India to buffer demand swings and shift overflow capacity between regions. Its digital design toolkit links Tekla Structures with shop-floor CNC codes, cutting detailing time by 20%. Emirates Steel Arkan counters with a growing portfolio of LEED-compliant plate, securing anchor orders for NEOM’s low-carbon mandates. Hadeed, under PIF ownership, fast-tracks a modernization plan that adds a 1 million t electric arc furnace powered by solar energy, lowering Scope 1 emissions.

Strategic moves emphasize partnerships. Emirates Steel’s tie-up with Eversendai grants access to European welding protocols for Trojena’s extreme-climate nodes, while Itochu’s DRI joint venture indicates Japanese buyers’ appetite for green sponge iron billets. Smaller specialists carve out niches in precision cutting, marine fabrication, and high-chromium alloy work, often subcontracted by EPC giants looking to derisk schedules. Across the GCC structural steel fabrication market, superior QC metrics, rework rates below 1% and on-time delivery above 95% increasingly determine preferred-supplier status[3]Itochu Corporation, “Abu Dhabi DRI JV Details,” itochu.co.jp.

Sustainability has become a prime differentiator. EMSTEEL’s green-hydrogen pilot, validated by Bureau Veritas, demonstrated a 95% CO₂ reduction potential, earning it a seat on Abu Dhabi’s Operation 300bn council. Zamil Steel is trialing scrap-based micro-mills to reduce logistics emissions, while Hadeed installs AI-enabled flue-gas analytics to optimize energy use. As developers embed embodied-carbon clauses, these initiatives influence bid scoring and long-term framework awards.

GCC Structural Steel Fabrication Industry Leaders

Hidada Ltd Co.

Arabian International Co. for Steel Structures

Al Yamamah Steel Industries Co.

Mabani Steel LLC

Al Shahin Co. for Metal Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EMSTEEL selected as Metals and Fabrications sector partner for Make it in the Emirates 2025, positioning the company to showcase UAE manufacturing capabilities and drive industrial innovation aligned with Operation 300 billion national initiatives.

- October 2024: Masdar and EMSTEEL announced successful completion of green hydrogen steel pilot project in Abu Dhabi, the first such demonstration in MENA region, with renewable hydrogen certified by Avance Labs and third-party assurance by Bureau Veritas Masdar.

- July 2024: Emirates Steel and Eversendai formalized partnership to supply premium steel beams for NEOM Trojena Ski Village, emphasizing sustainable, low-carbon-emission steel and global quality standards.

- June 2024: Itochu and Emirates Steel Arkan announced 2.5 million tonnes per year direct reduced iron production facility in Abu Dhabi, delayed from April 2025 target to post-2027 timeline, with low-carbon DRI supply to Japan's JFE Steel.

- June 2024: Itochu and Emirates Steel Arkan announced 2.5 million tonnes per year direct reduced iron production facility in Abu Dhabi, delayed from April 2025 target to post-2027 timeline, with low-carbon DRI supply to Japan's JFE Steel.

GCC Structural Steel Fabrication Market Report Scope

By Product Type

| Heavy Section (Beams & Columns) |

| Light Sectional & Cold-Formed Members |

| Tubular & Hollow Structural Sections (HSS) |

| Other Product Types (Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) |

By End-user Industry

| Construction | Commercial |

| Residential | |

| Industrial Buildings | |

| Infrastructure (Transport) | |

| Power & Energy (include utilities and renewable energy) | |

| Manufacturing & Industrial Equipment | |

| Oil and Gas | |

| Automotive & Transportation (railways systems, metro components, etc.) | |

| Other End User Industries (Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) |

By Fabrication Process

| Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) |

| Bending (Press brakes, roll bending, rotary bending) |

| Welding (TIG, MIG, arc welding, spot welding) |

| Machining (Milling, turning, drilling, grinding, CNC machining) |

| Forming (Stamping, forging, rolling, hydroforming) |

| Casting (Sand casting, die casting, investment casting) |

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Product Type | Heavy Section (Beams & Columns) | |

| Light Sectional & Cold-Formed Members | ||

| Tubular & Hollow Structural Sections (HSS) | ||

| Other Product Types (Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) | ||

| By End-user Industry | Construction | Commercial |

| Residential | ||

| Industrial Buildings | ||

| Infrastructure (Transport) | ||

| Power & Energy (include utilities and renewable energy) | ||

| Manufacturing & Industrial Equipment | ||

| Oil and Gas | ||

| Automotive & Transportation (railways systems, metro components, etc.) | ||

| Other End User Industries (Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) | ||

| By Fabrication Process | Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) | |

| Bending (Press brakes, roll bending, rotary bending) | ||

| Welding (TIG, MIG, arc welding, spot welding) | ||

| Machining (Milling, turning, drilling, grinding, CNC machining) | ||

| Forming (Stamping, forging, rolling, hydroforming) | ||

| Casting (Sand casting, die casting, investment casting) | ||

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) | ||

| By Geography | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

Key Questions Answered in the Report

How large is the GCC structural steel fabrication market in 2025?

The market stands at USD 9.11 billion and is projected to reach USD 11.70 billion by 2030, growing at a 5.13% CAGR.

Which end-user segment buys the most structural steel in the GCC?

Construction accounts for 46.89% of 2024 revenue, spanning commercial, residential, and industrial buildings.

What drives the fastest growth in this market?

Transport infrastructure projects such as rail and airport expansions are set to post a 7.17% CAGR through 2030.

Why are local-content rules important for fabricators?

GCC mandates reward firms that source, hire, and invest locally, ensuring preferred status on mega-projects and sustained order pipelines.

How are fabricators addressing carbon-reduction goals?

Leading players adopt electric-arc furnaces, green hydrogen pilots, and EPD certification to meet embodied-carbon requirements on flagship projects.

Page last updated on: