Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.23 Billion |

| Market Size (2026) | USD 3.83 Billion |

| Market Size (2031) | USD 4.51 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Major Home Appliances Market Analysis by Mordor Intelligence

The GCC Major Home Appliances market size reached USD 3.23 billion in 2025, is at USD 3.83 billion in 2026, and is projected to reach USD 4.51 billion by 2031 at a 3.32% CAGR. The GCC major home appliances market is benefiting from ongoing energy-efficiency mandates that steer households and commercial buyers toward inverter platforms and high-ambient designs aligned with T3 climate conditions, thereby raising specification thresholds and supporting premium pricing. Uptake of smart-connected features is expanding into mid-tier product lines as manufacturers embed predictive maintenance, remote diagnostics, and demand-response interfaces, positioning these as service value rather than just gadget features. Logistics and last-mile improvements in Saudi Arabia and the United Arab Emirates are shortening the path from online order to installation, which supports the durability of e-commerce growth even in bulky categories like refrigerators and air conditioners in the GCC major home appliances market. Refrigerant phase-down schedules under the Kigali Amendment and new technical regulations in Saudi Arabia and the UAE continue to reshape product roadmaps and refresh cycles, favoring efficient compressors and lower-GWP refrigerants.

Key Report Takeaways

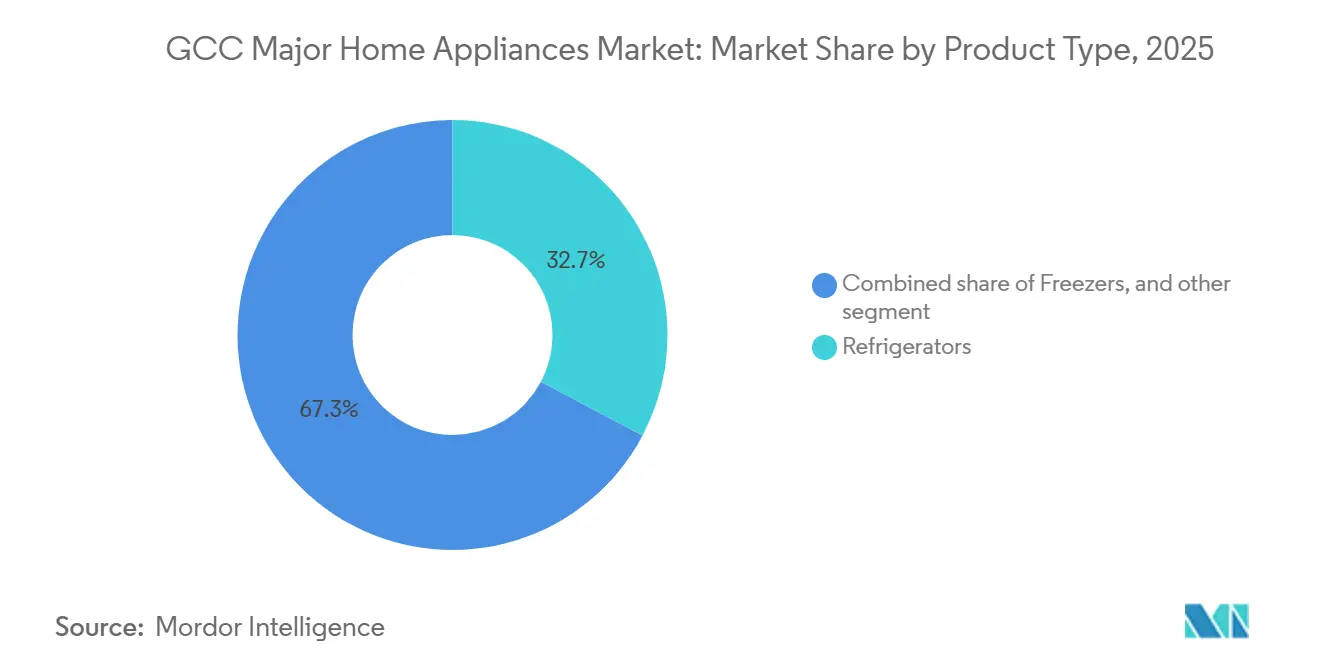

- By product type, refrigerators led with 32.74% revenue share in 2025, while air conditioners are forecast to expand at a 3.72% CAGR through 2031.

- By distribution channel, multi-brand stores held 48.62% in 2025, while online outlets are projected to grow at a 4.31% CAGR through 2031.

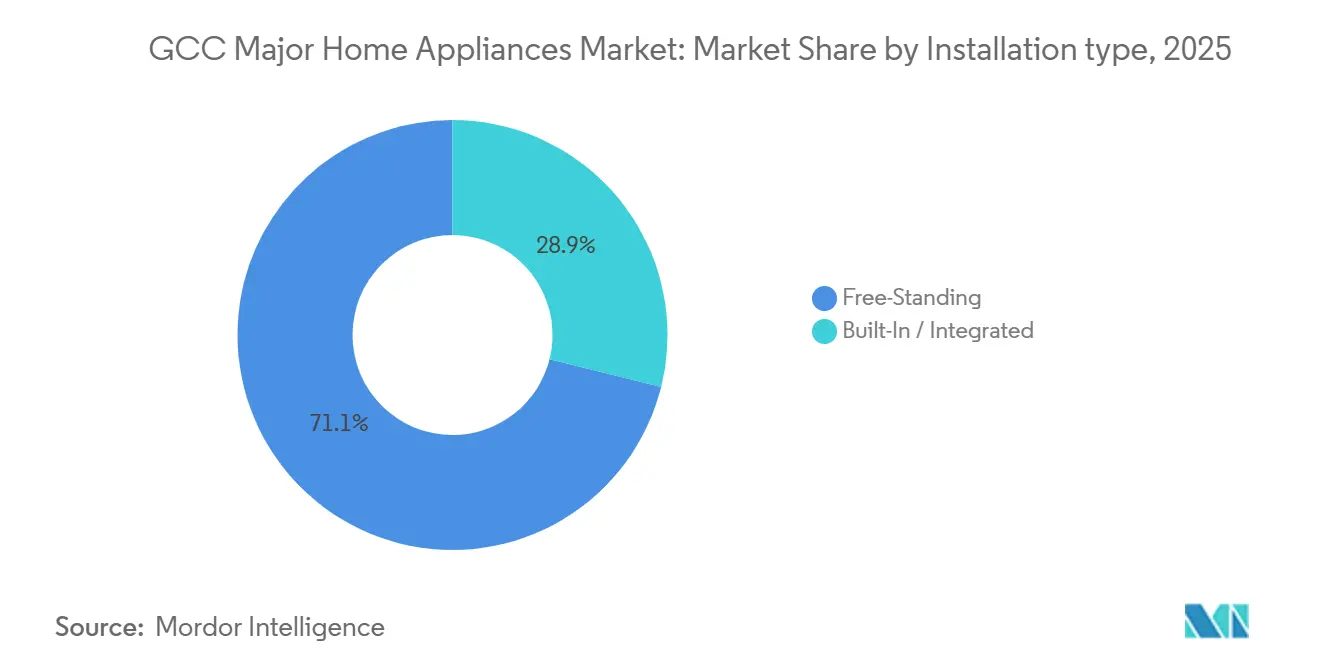

- By installation type, free-standing units commanded a 71.12% share in 2025, while built-in appliances are set to grow at a 4.12% CAGR.

- By technology, conventional appliances captured 84.45% in 2025, while smart-connected models are advancing at a 4.65% CAGR to 2031.

- By geography, the United Arab Emirates held 36.78% in 2025, while Saudi Arabia is set to post a 3.98% CAGR through 2031.

- By competitive landscape, LG, Samsung, Whirlpool, BSH, Haier, and Midea collectively held 55–65% combined share across major categories in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Major Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing And Hospitality Build-Out | +0.8% | Saudi Arabia, UAE, Qatar (mega-project zones) | Medium term (2-4 years) |

| Tightening Energy-Efficiency Standards | +1.1% | GCC-wide, strongest in the UAE and Saudi Arabia | Short term (≤ 2 years) |

| Omnichannel And Last-Mile Expansion | +0.5% | UAE leading, expanding to Saudi Arabia and Qatar | Medium term (2-4 years) |

| Rising Incomes and Urban Household Formation | +0.7% | Global, spill-over to GCC urban centers | Long term (≥ 4 years) |

| Refrigerant Transitions Under Kigali | +0.6% | GCC-wide, Article 5 Group 2 countries | Short term (≤ 2 years) |

| High-Ambient T3 And Inverter Designs | +0.5% | Saudi Arabia, Kuwait, UAE coastal areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Housing and Hospitality Build-out Propels Turnkey Demand

Saudi Arabia’s Vision 2030 housing pipeline delivered more than 800,000 Sakani contracts by 2024 and targets 115,000 residential starts annually through the decade, while NEOM, Qiddiya, and the Red Sea Project are slated to add 320,000 hotel rooms by 2030 that each require coordinated procurement across refrigeration, laundry, and climate control. In the UAE, developers in Expo City and on Abu Dhabi’s Yas Island specify built-in suites for luxury villas, which supports a 4.12% CAGR for integrated installations relative to a dominant 71.12% free-standing share in 2025. Hospitality operators lock multi-year service agreements that compress per-unit lifecycle costs, nudging suppliers to expand B2B coverage and then convert project-led placements into B2C brand pull. Preparations for the 2030 Asian Games and World Cup legacy projects in Qatar sustain a steady pipeline of mid-market apartments, prompting demand for efficient washers and French-door refrigerators that balance utility pricing with comfort needs. Air-conditioning vendors report growth tied to mega-project participation and exports, reinforcing how construction cycles translate into appliance volumes across the GCC Major Home Appliances Market.

Tightening Energy-Efficiency Standards Accelerates Replacements

Saudi Arabia’s SASO 2663 introduced seasonal energy-efficiency ratio labeling and disqualified fixed-speed ACs effective April 2022, which pushed retailers to clear legacy inventory and spurred manufacturers to shift new stock into inverter systems that reached 70% of new models by late 2024[1]Saudi Standards, Metrology and Quality Organization, “SASO Energy Efficiency and SEER Framework,” SASO, saso.gov.sa. The Saudi Energy Efficiency Center’s Estbdal program adds a SAR 1,000 rebate with free delivery for compliant split ACs and has pulled more than 50,000 non-compliant window units from shelves, reinforcing the replacement pace that lifts value over volume. The UAE’s Cabinet Resolution No. 157 of 2025, effective November 4, 2025, enforces UAE.S 5010-1:2025 and UAE.S 5010-5:2025 for low and large-capacity ACs with a 365-day compliance window, which shortens product-refresh cycles while aligning refrigerant choices with R-32 and R-600a. Five-star refrigerator labels in the UAE consume far less electricity than one-star units, which translates into measurable household savings and strengthens the case for upgrades in price-sensitive segments. Regional guidance from Eurovent Middle East and product showcases from leading HVAC firms add technical clarity, helping the GCC Major Home Appliances Market transition to low-GWP and high-efficiency SKUs without sacrificing high-ambient performance.

Omnichannel Expansion with E-commerce Scaling Last-Mile

Saudi Arabia’s logistics corridor and private investments in delivery hubs have reduced the time from order confirmation to installation, enabling online platforms to grow at a 4.31% CAGR while multi-brand stores continue to dominate share at 48.62% in 2025. Direct-to-site installation, integrated financing, and Arabic interfaces underpin rising online acceptance for large-ticket ACs, as seen with Zamil AC’s national e-commerce model. In the UAE, digital adoption and voice-assisted product discovery redirect search and purchase journeys onto mobile apps, aided by re-export logistics that shorten sea-freight windows and support duty-free regional distribution. Hybrid retail models that combine showrooms with click-and-collect strengthen household decision-making in categories like large-capacity washers and premium refrigerators. Trade-in programs and certified recycling for new AI-enabled models further accelerate digital conversion in the GCC Major Home Appliances Market as consumers capture both environmental and financial benefits[2]Samsung Newsroom, “Bespoke AI Appliances and SmartThings Updates,” Samsung, news.samsung.com.

Rising Disposable Incomes and Urban Household Formation

Non-oil growth in Saudi Arabia and rising female labor participation are expanding dual-income households that allocate more budget to premium home systems with lower total cost of ownership. The UAE’s expatriate-majority population searches for global brands with Arabic-language support and localized features, which strengthen premium categories across built-in kitchen and smart climate products. Qatar’s high per-capita income and expanding distributed solar encourage smart-thermostat and energy-management adoption that integrates appliances into home energy dashboards. Localization policies in Saudi Arabia are also driving domestic manufacturing capacity that reduces tariff exposure while compressing lead times for high-ambient SKUs. Retail partnerships and prioritized shelf placement for fast-growing brands signal a competitive channel mix that broadens consumer choice within the GCC Major Home Appliances Market.

Restraints Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VAT And Policy-Driven Cost Pass-Through | -0.4% | GCC-wide, particularly affecting mid-tier segments | Short term (≤ 2 years) |

| Brand Fragmentation and Private Labels | -0.3% | GCC-wide, the strongest impact is in the UAE and Saudi Arabia | Medium term (2-4 years) |

| Water Stress and Total Cost of Use | -0.3% | Qatar and UAE primarily, secondary impact on Oman, Bahrain | Long term (≥ 4 years) |

| Compliance Costs Under Updated MEPS/Labels/Testing | -0.2% | GCC-wide, elevated for smaller brands/importers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

VAT and Policy-Driven Cost Pass-Through to Retail Prices

VAT regimes in the UAE and Saudi Arabia, along with customs and tariff policies, raise landed costs and flow through to appliance retail prices that are most sensitive in mid-tier segments[3]Federal Tax Authority, “Value Added Tax (VAT) in the UAE,” FTA, tax.gov.ae. Duty-related changes in electrical items and local-assembly incentives are shifting sourcing patterns as manufacturers weigh deeper in-country partnerships to stabilize margins[4]Zakat, Tax and Customs Authority, “Tax and Customs Framework in Saudi Arabia,” ZATCA, zatca.gov.sa. Although higher prices can defer purchases, government housing programs, employer allowances, and zero-interest installment plans help moderate the net impact on replacement cycles. Region-wide regulatory updates also influence certification timelines and stocking strategies, which can add complexity to assortment planning. The result is a manageable drag on near-term growth in the GCC Major Home Appliances Market that is partly offset by financing innovation and developer-led bulk procurement.

Highly Fragmented Brand Landscape and Retailer Private Labels

The GCC retail environment carries a wide field of global, regional, and private-label brands that intensify price competition and compress margins in core categories like refrigerators, washers, and ACs. Regional electronics groups use GCC-wide dealer networks and value engineering to undercut imported MSRPs while meeting GSO and national energy-label thresholds. Private-label penetration is expanding through online platforms that test own-brand SKUs at lower marketing cost, which shifts promotional bargaining power toward retailers. Consolidation in large chains improves national coverage but can further tilt be negotiating leverage away from manufacturers on co-op budgets and shelf priority. This dynamic restrains pricing power for premium brands in the GCC Major Home Appliances Market even as top-tier SKUs defend value through warranties, energy ratings, and connectivity features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Air Conditioners Outpace Traditional Leaders

Refrigerators captured 32.74% of the GCC Major Home Appliances market share in 2025, anchored by universal need across households and hospitality, while vendors pursue compliant designs aligned with updated energy standards to stabilize unit economics. Air conditioners are projected to expand at a 3.72% CAGR to 2031 as the GCC Major Home Appliances Market aligns with SEER labeling, T3 performance specs, and low-GWP refrigerant transitions that favor inverter compressors. Washing machines hold the second-largest subsegment but face slower penetration in water-stressed cities, which pushes makers to add water-saving programs and sensors that optimize each cycle. Dishwashers are gaining traction in premium homes under Saudi labeling mandates that steer buyers toward efficient SKUs despite continued hand-wash habits in some households. Built-in cooking solutions move with luxury spec packages across new towers and villas, which lifts average selling prices even when unit volumes hold flat.

Freezers and niche cooking devices round out the product mix and serve hotel kitchens and villa upgrades that require specific footprints and energy labels now harmonized under GSO frameworks. Air-conditioning innovation continues to cluster around inverter control, AI-assisted optimization, and R-32 or R-600a refrigerants, all tuned for high-ambient reliability. Expanded local testing capacity for chillers and performance labs narrows certification cycles and reduces overseas dependency for high-capacity equipment. Regulatory tightening across the region penalizes legacy stocks and rewards manufacturers with pre-certified lineups ready for immediate listing, which channels growth toward ACs and smart refrigerators in the GCC Major Home Appliances Market. The overall shift keeps refrigerators as anchors for volume while ACs provide incremental growth that reshapes category balance across 2026–2031.

By Distribution Channel: Multi-Brand Dominance Meets Digital Acceleration

Multi-brand stores held 48.62% of sales in 2025 on the strength of tactile demos, bundled installation, and omnichannel pickup, which remains central to category decisions like AC tonnage and washer capacity in the GCC Major Home Appliances Market. Flagship alliances in malls and national chains pair co-op advertising with exclusive SKUs to drive footfall and cross-sell warranties or smart-home packages. Hypermarkets focus on entry-tier SKUs and seasonal promotions, while premium European brands continue to rely on specialist outlets and direct-to-consumer storefronts. Online channels are projected to grow at a 4.31% CAGR to 2031 as end-to-end installation, financing, and faster logistics remove friction from large-ticket e-commerce. Trade-in programs for AI-enabled appliances, together with regional re-export hubs, are improving inventory pooling and regional shipping efficiency on scale.

Direct-to-consumer and subscription service bundles are emerging in select categories, offering convenience and predictable maintenance for mobile tenants and project buyers. Historical channel growth was steady through 2025, with recent momentum tilting online as last-mile networks mature and tax structures reshape pricing strategies. Manufacturers calibrate presence by country, with ACs still skewed to store-based consultative sales in Saudi Arabia and refrigerators or washers increasingly purchased online in the UAE. Regional brands leverage GSO certifications and localized features to secure shelf slots and online placement at competitive MSRPs, which sustains choice across the GCC Major Home Appliances Market. As omnichannel adoption rises, last-mile readiness and post-purchase services become the decisive differentiators for repeat purchases.

By Installation Type: Free-Standing Prevails, Built-In Gains Premium Ground

Free-standing appliances accounted for 71.12% of sales in 2025 and remain standard for furnished rentals and villa retrofits that prioritize flexibility and quick tenant readiness in the GCC Major Home Appliances Market. Built-in formats held 28.88% in 2025 and are set to grow at a 4.12% CAGR as premium projects specify integrated kitchens with panel-ready units that deliver seamless aesthetics. Premium built-in ovens, induction hobs, and coffee systems bring higher installation and fit-out costs but signal quality and design alignment in luxury towers and villas. Hospitality programs often standardize built-in formats to simplify maintenance and replacement, which aligns with bulk procurement structures. These choices push a steady premium mix without displacing the free-standing baseline that anchors volume.

From 2026 to 2031, growing construction quality and green-building codes support the integrated shift, while updated label schemes apply equally to both types to focus competition on features and energy. Manufacturers emphasize compact footprints, dual-fuel flexibility, and connectivity parity with free-standing units to protect value in built-in lines. Modular built-in options and panel-ready laundry broaden use cases in villas where cabinetry can conceal appliances without sacrificing performance. The GCC Major Home Appliances Market will likely keep a free-standing majority while integrated solutions expand in projects and premium renovations. This balance preserves affordability for mass segments and elevates margins where integrated design is a priority.

By Technology: Conventional Base, Smart Surge Reshapes Mix

Conventional appliances held 84.45% of shipments in 2025, given lower MSRPs, hypermarket reach, and buyer familiarity across Tier 2 cities and rural districts in the GCC Major Home Appliances Market. Smart-connected models are projected to grow at a 4.65% CAGR through 2031 as Samsung’s Bespoke AI lineup and LG’s Copilot integration normalize predictive maintenance, remote diagnostics, and energy optimization among mid-tier SKUs. High internet coverage and strong 5G availability help appliance connectivity scale beyond early adopters, especially in Saudi Arabia and the UAE. Interoperability through open alliances allows cross-brand control and enables utility demand-response incentives to reach more households. These features complement updated labels and support higher star ratings that reinforce the upgrade rationale.

Across 2026–2031, manufacturers are migrating mid-tier lines to baseline connectivity without large price premiums, which narrows the gap between conventional and smart. Smart refrigerators add inventory cameras and energy dashboards while washers improve dosing and cycle personalization, which increases perceived value at similar footprints. ACs deploy occupancy sensors and adaptive inverter logic that syncs with building or utility programs for peak-load control. Label frameworks do not mandate connectivity, yet connected devices often exceed minimum efficiency thresholds through real-time optimization. The GCC Major Home Appliances Market is on track to shift toward a 75% conventional and 25% smart mix by decade-end as connectivity becomes standard in upper entry and mid-range lines.

Geography Analysis

The United Arab Emirates held 36.78% of the GCC Major Home Appliances market share in 2025, supported by duty-free re-export zones, rapid logistics, and high adoption of connected devices. Cabinet Resolution No. 157 of 2025 took effect on November 4, 2025, and grants a 365-day compliance window for AC technical regulations, which accelerates refrigerant transitions and inverter penetration. The GCC Major Home Appliances Market benefits from the UAE’s regional distribution strength, with new logistics infrastructure in Egypt further shortening freight windows into Gulf warehouses. Premium built-in adoption remains concentrated in new developments around Dubai and Abu Dhabi, where integrated kitchens are standard in upper-tier units. The mix continues to skew toward higher efficiency across 2026 as enforcement timelines and developer specs reward compliant inventories.

Saudi Arabia is set to grow at a 3.98% CAGR through 2031 as housing starts under Vision 2030, and mega-projects add sustained demand for refrigeration, laundry, and climate control. The Estbdal rebate of SAR 1,000 for efficient split ACs has removed tens of thousands of non-compliant window units, which shortens replacement cycles and increases inverter shares. Western regions tied to large tourism and hospitality projects are pacing growth, while domestic manufacturing and testing capacity strengthen local supply and certification timelines. Refrigerators and ACs dominate replacement volume in Saudi Arabia as MEPS and SEER labeling displace legacy fixed-speed models. The GCC Major Home Appliances Market tracks these policies and project effects into 2031 with steady share gains for compliant, premiumized SKUs.

Qatar’s deliveries are supported by Asian Games preparations and World Cup legacy housing that favor efficient washers and premium refrigeration despite lower dishwasher uptake under water-stress considerations. Kuwait’s dynamics reflect labor-nationalization headwinds that limit mid-range growth, while premium built-in and smart appliances sustain margins among affluent buyers. Oman prioritizes energy-efficient imports and targeted localization, including AC lines designed for high-ambient performance with advanced filtration. Bahrain benefits from UAE logistics spillover and early pilots of T3 inverter SKUs that scale region-wide post-validation. These country-level patterns keep the GCC Major Home Appliances Market on a steady path where Saudi Arabia leads growth and the UAE anchors distribution and premium adoption.

Regulatory Landscape

Major home appliances sold across the GCC are governed by Gulf Standardization Organization (GSO) technical regulations for low-voltage electrical equipment and appliances (BD-142004-01). These require the Gulf Conformity Mark (G-Mark) for market access in member states, alongside safety requirements commonly mapped to the IEC 60335 series. On top of this regional baseline, national conformity pathways add country-specific documentation and clearance steps that affect lead times, portfolio planning, and importer compliance costs.

Saudi Arabia layers SABER-based registration and certification for regulated appliances through SASO programs, tightening gatekeeping for shipments and raising the value of pre-certified lineups. In the UAE, the Ministry of Industry and Advanced Technology (MoIAT) administers conformity certification routes (ECAS/EQM) and country-level technical regulations that shape market access for high-volume categories such as air conditioners. For example, Cabinet Resolution No. 157 of 2025 took effect on November 4, 2025, with a 365-day compliance window for updated AC requirements, accelerating product refresh and documentation cycles for importers and brands.

Value Chain Analysis

The GCC major home appliances value chain is anchored by offshore component and finished-goods manufacturing, followed by importation into regional consolidation hubs where warehousing, compliance documentation, and redistribution are managed before retail and installation. The UAE functions as a key re-export and distribution node through its free-zone logistics ecosystem, while Saudi Arabia combines import flows with growing local assembly and testing capacity for climate-relevant categories, particularly air conditioning, to shorten certification and delivery timelines.

Downstream, multi-brand retailers and national distributors translate manufacturer assortments into country-ready listings by bundling delivery, installation, warranty, and after-sales service, which is especially important for bulky categories. Partnerships illustrate how brands use established route-to-market capabilities, for example Panasonic Marketing Middle East & Africa appointing Al Essa Industries as a distributor for large home appliances in Saudi Arabia (May 2025). Localized manufacturing and JV models in air conditioning also integrate upstream and downstream economics, with players such as Shaker Group combining manufacturing and distribution capabilities in Saudi Arabia. In this setup, national compliance workflows (G-Mark plus SABER/MoIAT pathways) influence SKU selection and inventory positioning.

Competitive Landscape

The GCC Major Home Appliances Market is moderately concentrated, with LG, Samsung, Whirlpool, BSH, Haier, and Midea together holding an estimated 55–65% across major categories in 2025, while regional brands, AC specialists, and private labels maintain a long tail. Samsung’s 2025 Bespoke AI portfolio and LG’s Copilot-enabled appliances reinforce premium positions and extend AI features into mid-tier ranges to defend share. Chinese brands scale through GCC retail alliances and regional manufacturing footprints that lower landed cost and speed listings. Three strategic levers stand out across leaders: local production or assembly alignment, open-ecosystem connectivity, and pre-compliance with new efficiency and refrigerant standards. Water-smart laundry, D2C maintenance bundles, and built-in packages for developer projects are notable white-space plays through 2031.

Technology differentiation is clear in AI diagnostics, energy optimization, and interoperability that support building and utility programs in high-ambient markets. BSH extends Matter-ready appliances and advanced efficiency features that sync with GCC sustainability goals and premium kitchen designs. Strategic acquisitions and distribution consolidation continue to reshape coverage and service footprints in the region. Standards engagement by industry groups provides technical inputs that inform national enforcement guidance and market education. Warranty tenure, label star ratings, and connectivity stack often tilt category decisions when prices converge.

Competitive intensity peaks in Saudi Arabia’s replacement window under Estbdal and in the UAE’s retrofit cycle for integrated kitchens, where European brands maintain a significant premium. Volume remains rooted in free-standing conventional appliances sold via multi-brand stores, while margins concentrate in smart and built-in niches supported by omnichannel services. Localized features such as Arabic interfaces and anti-corrosion treatments support warranty performance in saline and desert conditions. As testing infrastructure localizes and policies converge, product-refresh speed and channel execution will define outperformance in the GCC Major Home Appliances Market.

GCC Major Home Appliances Industry Leaders

LG Electronics Inc.

Samsung Electronics Co. Ltd.

BSH Hausgeräte GmbH

Haier Smart Home

Midea Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Built-in and smart bundles are gaining practical whitespace in GCC premium apartments, villas, and developer-led communities where integrated kitchens and connected living systems are specified upfront, rather than being sold as standalone appliances. One demand catalyst is the Sheikh Zayed Housing Programme partnership with e& (announced in July 2026), which aims to integrate smart home automation and connected devices, including the Hassantuk fire detection system, into residential communities in the UAE, creating an entry channel for appliance brands that can interoperate with broader home platforms.

Energy- and compliance-driven product refresh is also creating room for differentiated SKUs that pair high-ambient performance with measurable efficiency improvements and lower standby consumption. On the standards side, GSO issued updated standards for core white-goods categories, including GSO 2769:2024 for household refrigerators and freezers (up to 1,500 liters) and GSO 2738:2024 for electric clothes washing machines (up to 25 kg), which supports a more harmonized baseline for scale across GCC markets. In Saudi Arabia, SASO updates around smart products introduce additional technical hurdles that can act as differentiators for larger vendors with embedded-software and compliance teams, including a revised SASO IEC 62301:2026 focused on standby power and labeling, and a SASO Digital ID requirement tied to SABER workflows for smart products. These requirements push suppliers toward tighter firmware-level traceability and more formalized smart-appliance certification readiness.

Recent Industry Developments

- June 2026: LG Electronics launched the DUALCOOL AI air conditioner across the UAE, Oman, and selected nearby markets, emphasizing ThinQ-based energy management and smart comfort controls tailored for high-ambient usage. The rollout reinforces the premium, inverter-led replacement cycle that is being shaped by tightening efficiency rules and retailer focus on higher-spec SKUs.

- May 2026: LG Electronics partnered with Al Yousuf Electronics to open an LG AI Home showroom on Sheikh Zayed Road in Dubai, featuring a dedicated AI Home experience zone developed with Schneider Electric. The partnership lifts experiential retail for major appliances and supports conversion of connected features from a specification into a demo-led selling point in a market where multi-brand stores still dominate volume.

- August 2025: Panasonic Marketing Middle East & Africa expanded its route-to-market in Oman with OMASCO through the launch of the EU-Series air conditioner tailored for local conditions, combining Adaptive Inverter Technology with nanoe X air purification. The product localization reinforces how GCC demand increasingly rewards high-ambient performance alongside air-quality features, particularly in categories where installation and after-sales capability influence brand selection.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market is defined as the value of major home appliances sold for household use across GCC countries, counted at the point of sale and reported in USD for the study period.

Scope exclusions: We exclude small home appliances, spare parts, and stand-alone repair and maintenance services from the market totals.

Segmentation Overview

- By Product Type

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Cooktops & Ranges

- Microwave Ovens

- Air Conditioners

- Others (Electric Hobs)

- By Distribution Channel

- Multi-Brand and Exclusive Brand Stores (EBOs)

- Hypermarkets & Supermarkets

- Online / E-commerce Platforms

- Direct-to-Consumer (D2C) & Subscription Models

- By Installation Type

- Free-Standing

- Built-In / Integrated

- By Technology

- Conventional Appliances

- Smart / Connected Appliances

- By Geography

- Saudi Arabia

- United Arab Emirates

- Kuwait

- Qatar

- Oman

- Bahrain

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the starting structure for the model and align it with commonly tracked GCC appliance categories and channels. We referred to public sources such as national statistics offices and customs authorities in GCC countries, UN Comtrade for trade direction, and International Energy Agency releases to understand electricity-use patterns that affect appliance replacement. For product and efficiency context, we also used resources such as SASO and ESMA program pages and published policy notes linked to refrigerants and minimum energy performance standards.

To keep inputs practical, we combined these public signals with company annual reports, investor presentations, retailer disclosures, and reputable regional business news for pricing and channel shifts. Where needed, we used paid subscriptions for company financials and intelligence, and we performed shipment-level import and export checks to sanity-test volumes by product family. These sources supported sizing, validation, and assumption setting, and the list here is illustrative rather than exhaustive.

Primary Interviews and Surveys

Primary work was used to validate what is actually selling across GCC and how pricing and promotions are moving by appliance type and channel. We spoke with manufacturers, distributors, large-format retailers, online-led sellers, and service ecosystem participants, then cross-checked inputs across Saudi Arabia, the UAE, and the smaller GCC markets to avoid one-country bias. These discussions clarified adoption assumptions for smart-connected models, helped split offline versus online mix, and pressure-tested replacement demand versus new household formation.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 19% | |

| Mid tier: 41% | Functional/Unit leaders: 23% | |

| Smaller Players: 20% | Managers: 58% |

Market-Sizing & Forecasting

Sizing started with a top-down build where GCC demand was reconstructed by combining appliance category splits with country-level consumption signals and trade availability, then mapped to the main distribution channels. The totals were corroborated with selective bottom-up checks, such as sampled average selling prices multiplied by implied unit volumes for key categories, and channel checks on online share and promotion depth.

Inputs that mattered most included replacement cycles for air conditioners and washing machines, housing completions and household formation indicators, efficiency regulation milestones that trigger upgrade buying, seasonality tied to summer cooling demand, and country-level import patterns that signal product availability. Pricing was modeled using observed price bands from retailers and distributor feedback, then normalized for mix shifts toward smart or inverter-based products.

For forecasting, we used scenario analysis supported by simple trend smoothing on category growth, and we adjusted assumptions using expert consensus on housing momentum, regulation timing, and expected channel mix changes. When gaps appeared in bottom-up approximations, we filled them with conservative ranges derived from adjacent GCC countries with similar appliance penetration, then re-validated through follow-up calls.

Data Validation & Update Cycle

Totals were checked through triangulation across category splits, country rollups, and channel shares so that the final value is consistent with multiple independent signals. Outliers, sudden jumps, or unusual price movements were flagged, reviewed by a second analyst, and then re-checked with an additional primary contact when the variance stayed material. Before sign-off, we also compared model outputs with practical markers such as import surges, reported retailer expansion, and major policy changes affecting refrigerants or efficiency.

Reports are refreshed on an annual cycle, and interim updates are made when major events materially change demand, pricing, or trade flows. Right before delivery, we run a final update pass so clients receive the most current view that can be traced back to clear inputs and review steps.

Mordor Intelligence's Gcc Major Home Appliances Market Size Versus Other Published Estimates

Published market values for GCC major home appliances can look far apart because analysts do not always count the same products, the same sales channels, or the same point in the value chain. Differences also show up when one estimate leans more on imports, while another leans more on consumer spending proxies, and the two do not reconcile cleanly.

Small appliances such as microwaves and irons are often bundled into broader household appliance totals, and that item sits outside Mordor Intelligence's scope for this report, which is limited to major home appliance categories in the GCC. Some published figures also apply aggressive price growth across all categories, even though price movement in air conditioners and large refrigeration can be moderated by promotions, efficiency standards, and mix shifts. Finally, refresh cadence matters because a model that is not re-checked against recent channel mix and currency timing can drift away from what retailers and distributors are seeing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.23 B (2025) | |

| Regional Consultancy A | USD 5.80 B (2024) | Uses a wider basket that likely blends major and small home appliances, and it appears to use a different base year and inflation assumptions, which can lift the total when converted to USD. |

| Industry Report Publisher B | USD 3.90 B (2025) | Likely includes adjacent categories and uses a higher growth path into the forecast period, with less transparent checks on channel mix and category-level pricing in GCC markets. |

Across the three figures, the spread is best explained by product scope and how pricing and category mix are treated year to year, rather than by a single demand driver. By keeping the counted categories specific, and then cross-checking totals using trade signals, channel feedback, and practical price bands, the final value stays easier to replicate and explain when assumptions need to be updated.

Key Questions Answered in the Report

What is the current size and outlook for the GCC Major Home Appliances market?

The GCC Major Home Appliances market size is USD 3.83 billion in 2026 and is projected to reach USD 4.51 billion by 2031 at a 3.32% CAGR.

Which product categories lead growth in the GCC Major Home Appliances market?

Refrigerators led with 32.74% share in 2025, while air conditioners are the fastest-growing category with a 3.72% CAGR through 2031.

How are regulations shaping the GCC Major Home Appliances market through 2031?

Saudi SEER rules, UAE’s Cabinet Resolution No. 157 of 2025, and Kigali refrigerant timelines are accelerating inverter adoption and R-32 or R-600a transitions.

Which sales channels are expanding fastest for GCC appliances?

Online channels are scaling at a 4.31% CAGR as logistics, trade-in programs, and installation services remove friction from large-ticket e-commerce.

What are the top country markets within the GCC for major appliances?

The UAE held a 36.78% share in 2025, and Saudi Arabia is projected to post a 3.98% CAGR through 2031 on housing and mega-project demand.

Which technologies are differentiating premium appliances in the GCC?

AI-enabled diagnostics, inverter compressors, and open-ecosystem connectivity are key differentiators, with smart models growing at a 4.65% CAGR to 2031.

Page last updated on: