GCC Luxury Goods Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.02 Billion |

| Market Size (2026) | USD 16.53 Billion |

| Market Size (2031) | USD 26.66 Billion |

| Growth Rate (2026 - 2031) | 10.03% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC Luxury Goods Market Analysis by Mordor Intelligence

The GCC luxury goods market size is expected to increase from USD 15.02 billion in 2025 to USD 16.53 billion in 2026 and reach USD 26.66 billion by 2031, growing at a CAGR of 10.03% over 2026-2031. Accelerated sovereign-wealth allocations to European maisons are giving brands leverage to negotiate exclusive capsules, while government-funded cultural festivals are turning tourism peaks into predictable retail windfalls. Women represented 65.21% of demand in 2025, yet the men’s segment is expanding swiftly as grooming and tailoring collections gain traction. Swiss watchmakers are capitalizing on Ramadan and Eid gifting cycles, and e-commerce is allowing labels to bypass wholesale margins while gathering first-party data. Although the United Arab Emirates supplied nearly half of 2025 revenue, Saudi Arabia’s pipeline of mixed-use malls and flagship openings points to a two-speed growth dynamic that brands must balance.

Key Report Takeaways

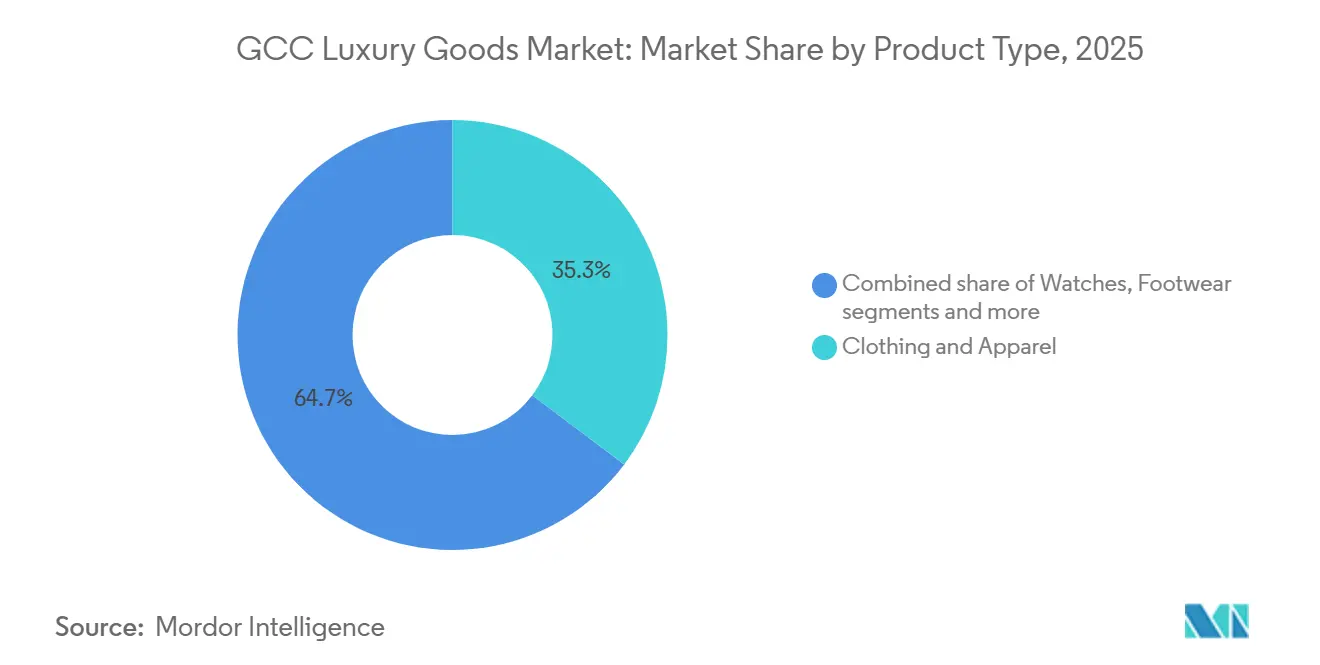

- By product type, clothing and apparel led with 35.28% of GCC luxury goods market share in 2025, while watches are poised for a 10.50% CAGR through 2031.

- By end user, women captured 65.21% of 2025 revenue; men’s purchases are forecast to surge at 10.76% annually to 2031.

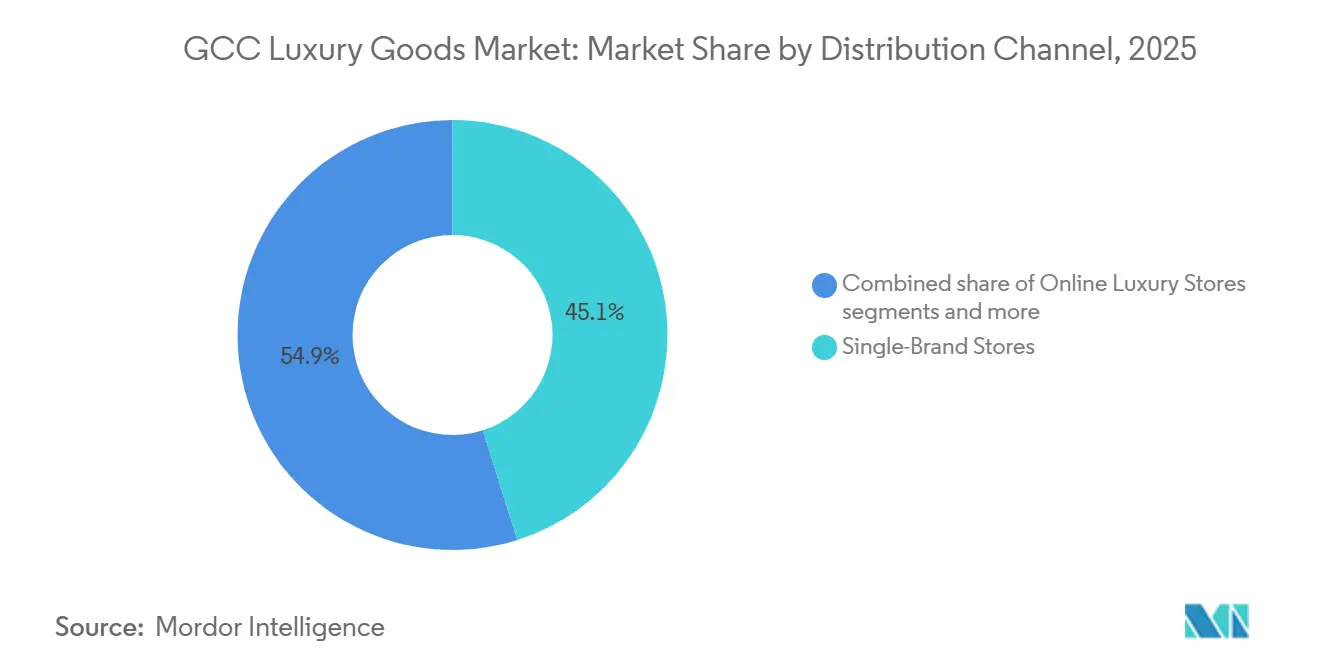

- By distribution channel, single-brand stores held 45.12% of the GCC luxury goods market size in 2025, yet online luxury platforms are accelerating at 12.30% CAGR between 2026-2031.

- By country, the United Arab Emirates commanded 48.15% of revenue in 2025; Saudi Arabia is projected to register a 10.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Middle east representing one of the more structurally developed among them. The global report on luxury goods market by Mordor Intelligence reflects how these regional layers combine into a single system.

GCC Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased consumer demand for limited edition offerings | +1.8% | GCC-wide, strongest in United Arab Emirates and Saudi Arabia | Medium term (2-4 years) |

| Role of social media and celebrity endorsements in influencing purchases | +1.5% | GCC-wide, particularly United Arab Emirates, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Heritage festivals supported by governments driving consumer spending | +1.2% | Saudi Arabia, United Arab Emirates, Qatar, Kuwait | Medium term (2-4 years) |

| Strategic investments by the Gulf Cooperation Council in European luxury brands | +1.0% | GCC-wide, with direct benefits to the United Arab Emirates and Saudi Arabia | Long term (≥ 4 years) |

| Growing market for sustainable and eco-certified luxury products | +0.8% | GCC-wide, early adoption in United Arab Emirates | Long term (≥ 4 years) |

| Expansion of luxury retail spaces and shopping malls | +1.5% | Saudi Arabia, United Arab Emirates, Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased consumer demand for limited edition offerings

Increased consumer demand for limited edition luxury goods in the GCC is driven by affluent shoppers seeking exclusivity, personalization, and emotional value beyond standard product offerings. This trend is underpinned by rising disposable incomes and wealth concentration, which enhance the willingness to pay premiums for scarcity-driven collections. The growing number of high-net-worth individuals further supports this dynamic, with the UAE recording a net increase of 6,700 high-net-worth individuals in 2024, the highest globally, according to the World Economic Forum [1]Source: World Economic Forum, "Bahrain Economic Development Board: Private Wealth is Coming to the Gulf. Here’s why," weforum.org. This expansion directly broadens the target audience for limited edition releases. Brands are increasingly adopting strategies such as capsule collections and regional exclusives to create urgency and reinforce brand prestige. For example, Louis Vuitton’s Middle East-exclusive handbag launches have generated significant waitlists in Dubai and Riyadh boutiques, often tied to cultural events to enhance emotional relevance. Limited editions also boost perceptions of resale value, strengthening their investment appeal. Social media amplifies demand by transforming scarcity into visibility-driven desirability, ensuring sustained interest in limited edition luxury offerings in the GCC.

Heritage festivals supported by governments driving consumer spending

Government-supported heritage festivals are increasingly influencing consumer spending in the luxury goods market by integrating cultural pride with premium retail experiences. Saudi Arabia’s Riyadh Season 2024 featured the “Christian Dior: Designer of Dreams” exhibition and the “1001 Seasons of Elie Saab” fashion show, aligning global luxury brands with national cultural themes and transforming luxury consumption into immersive lifestyle experiences. Similarly, Layali Diriyah 2025 attracted over 110,000 visitors near the Diriyah UNESCO site, combining designer pop-ups with heritage-focused entertainment formats to encourage longer visitor engagement and higher discretionary spending within curated retail spaces. Luxury brands benefit from increased foot traffic and stronger emotional connections through destination-driven luxury experiences. For example, Elie Saab leveraged its fashion show to enhance brand loyalty among affluent regional consumers. Furthermore, government-backed festivals lower market entry barriers for luxury brands by offering infrastructure and visibility support. Collectively, cultural programming, tourism initiatives, and brand storytelling are driving sustained growth in luxury spending across the GCC.

Growing market for sustainable and eco-certified luxury products

The demand for sustainable and eco-certified products in the luxury goods market is rising, driven by regulatory developments and changing consumer preferences. Policies such as the UAE’s ban on single-use plastic bags, effective January 1, 2024, and Saudi Arabia’s upcoming carbon labeling requirements are embedding sustainability into standard consumption practices. These regulations are encouraging luxury brands to adopt eco-certified materials, responsible sourcing, and sustainable packaging solutions. Among affluent consumers in the GCC, sustainability has shifted from being a premium feature to a baseline expectation. This trend is further reinforced by the Saudi Green Initiative, which attracted over SAR 705 billion in green investments by 2024, reflecting institutional commitment to sustainable growth, according to the Saudi and Middle East Green Initiatives [2]Source: Saudi and Middle East Green Initiatives, "SGI: Steering Saudi Arabia Towards a Green Future," sgi.gov.sa. To remain relevant and compliant, luxury brands are aligning with these frameworks. For example, Cartier’s certified responsible gold collections resonate with sustainability-conscious buyers in the region. The combined influence of regulatory momentum and evolving consumer values is reshaping product development and retail narratives, positioning eco-certified luxury as a critical element of brand equity across the GCC.

Expansion of luxury retail spaces and shopping malls

The expansion of luxury retail spaces and shopping malls in the GCC is reshaping consumer engagement with premium brands, moving beyond transactional purchases to immersive experiences. This development emphasizes creating environments where customers connect with brand heritage through private salons, bespoke tailoring services, and exclusive previews of upcoming collections, fostering deeper emotional engagement and brand loyalty among high-spending consumers. Physical flagship stores act as cultural landmarks within premium malls, reinforcing destination-led luxury retail while complementing digital channels to establish a hybrid model that appeals to both convenience-driven and experience-seeking shoppers. For example, Burberry’s experiential store formats in Dubai integrate customization lounges with digital styling tools, showcasing craftsmanship while personalizing the customer journey. Mall developers are capitalizing on this trend by positioning luxury as a lifestyle ecosystem rather than a retail cluster. The combination of experiential retail and omnichannel strategies is accelerating the growth of luxury mall developments across the GCC.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.5% | GCC-wide, particularly United Arab Emirates and Saudi Arabia | Short term (≤ 2 years) |

| Impact of cultural sensitivities and norms | -0.3% | Saudi Arabia, Kuwait, conservative segments across GCC | Long term (≥ 4 years) |

| Compliance costs due to regulatory frameworks | -0.2% | GCC-wide, administrative burden highest in Saudi Arabia | Medium term (2-4 years) |

| Increased import duties on personal luxury goods in Saudi Arabia (2024) | -0.3% | Saudi Arabia, spillover to cross-border shopping in United Arab Emirates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

The proliferation of counterfeit products poses a significant challenge in the luxury goods market across the GCC, eroding brand equity, consumer trust, and legitimate sales volumes. Enforcement data highlights the scale of this issue, with Dubai Customs reporting 285 intellectual property seizures in 2024 valued at approximately AED 92.695 million. These seizures encompassed watches, eyewear, clothing, bags, and shoes, directly impacting core luxury segments. Despite the registration of 439 trademarks, 205 commercial agencies, and 6 intellectual property assets reflecting intensified brand protection efforts, counterfeiting risks persist [3]Source: Dubai Customs, "Dubai Customs Celebrates World Intellectual Property Day with Focus on Creativity and Protection," dubaicustoms.gov.ae . The circulation of fake goods undermines pricing power and premium positioning, while consumer confusion between authentic and counterfeit products delays purchase decisions. For example, Gucci continues to invest heavily in authentication technologies and regional legal enforcement to combat counterfeit handbags in the GCC. This environment increases compliance and monitoring costs for luxury brands, ultimately constraining market growth by diluting exclusivity and damaging long-term brand credibility in the region.

Increased import duties on personal luxury goods in Saudi Arabia (2024)

The increase in import duties on personal luxury goods in Saudi Arabia in 2024 is altering consumer purchasing patterns and brand strategies. Saudi consumers are increasingly timing their purchases during travel to Dubai or through United Arab Emirates-based e-commerce platforms, which has led to a decline in domestic store traffic. This shift in cross-border shopping behavior reduces the intended impact of tariff increases and redirects demand to neighboring retail hubs. As a result, brands are encountering challenges in demand forecasting and inventory planning across the Saudi Arabia and United Arab Emirates markets. To address these issues, some luxury brands are exploring local assembly or finishing operations in Saudi Arabia to qualify for reduced duties, though this approach requires achieving sufficient scale to justify the associated costs. These adjustments add operational complexity and increase investment risks. For example, Hermès is evaluating localized finishing options for leather goods to protect margins in the Saudi market, though such strategies may not be viable for all product categories or volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Watches Accelerate as Gifting Staples

Clothing and apparel are expected to maintain the largest share of the market, accounting for 35.28% of the product-type segment in 2025. This category's dominance is attributed to its broad scope, encompassing ready-to-wear, haute couture, and modest fashion. However, growth in this segment is moderating as brands face inventory challenges in aligning seasonal collections with both Western fashion calendars and Islamic holidays. Watches, on the other hand, are forecast to grow at an annual rate of 10.50% from 2026 to 2031, outpacing the overall market. Swiss manufacturers are leveraging cultural occasions such as Ramadan and Eid by introducing limited-edition timepieces, exemplified by Audemars Piguet's 2025 novelties, including the Caliber 7138 perpetual calendar and Royal Oak variants, which sold out shortly after launch.

Jewelry, footwear, leather goods, and eyewear collectively represent the remaining market share. Jewelry benefits from the cultural significance of gold in the region, while leather goods are gaining traction through personalized monogramming services offered by brands like Louis Vuitton and Hermès. Eyewear and footwear are emerging as underdeveloped categories, with opportunities for growth through standalone boutiques and collaborations with regional retailers. Additionally, the watch segment is bolstered by the pre-owned and vintage markets, where platforms like The Luxury Closet in Dubai are attracting younger buyers, fostering a progression from entry-level purchases to new-watch acquisitions as incomes and brand familiarity increase.

By End User: Men's Segment Gains Momentum

Women's luxury purchases accounted for the largest share of the market in 2025, with 65.21% of the total demand. These purchases remain concentrated in categories such as apparel, handbags, and jewelry, where brands have developed extensive product assortments and strong customer loyalty programs. In contrast, the men's segment, while smaller, is projected to grow at an annual rate of 10.76% through 2031, the fastest among all end-user categories. This growth is driven by expanding grooming and tailoring offerings, with brands like Tom Ford Beauty and Dior Men introducing region-specific product lines tailored to Middle Eastern preferences, such as oud-based fragrances and bespoke suiting. Additionally, Ermenegildo Zegna and Brioni are opening dedicated men's boutiques in Riyadh and Dubai, offering made-to-measure services that cater to professionals seeking differentiation in business settings.

The unisex segment, though currently smaller, is also gaining traction as brands introduce gender-neutral fragrances, accessories, and ready-to-wear collections that appeal to younger, cosmopolitan consumers in urban centers. The men's segment benefits from lower baseline penetration, creating significant growth potential as disposable incomes rise and cultural norms around male grooming evolve. Saudi Arabia's Vision 2030 initiative, emphasizing entertainment and lifestyle sectors, is further normalizing luxury consumption among men, who are increasingly engaging with fashion events and brand activations at heritage festivals. The unisex category represents a strategic opportunity for brands to test inclusive marketing and product designs before scaling globally.

By Distribution Channel: Online Platforms Disrupt Traditional Retail

Single-brand stores accounted for the largest share of revenue in 2025, contributing 45.12%, while online luxury stores are projected to grow at an annual rate of 12.30% from 2026 to 2031, the fastest among distribution channels. Single-brand stores retain a competitive edge in experiential retail, offering services such as private salons, bespoke tailoring, and exclusive previews that cannot be replicated online. For example, Dolce & Gabbana's 16,000-square-foot flagship store in Saudi Arabia and its 1,500-square-meter Diriyah brand center, both launched in December 2024, highlight how physical retail spaces are transforming into brand museums that emphasize heritage and craftsmanship. However, rising rents in prime locations like Dubai Mall and The Avenues Riyadh, increasing by 10 to 15% annually, are pressuring brands to justify occupancy costs through higher transaction values and improved conversion rates.

Online luxury stores are gaining momentum as brands increasingly adopt direct-to-consumer e-commerce platforms to bypass traditional retail intermediaries, capture detailed customer insights, and deliver personalized recommendations powered by artificial intelligence. Chalhoub Group's Level Shoes platform, operating in the United Arab Emirates, Saudi Arabia, and Kuwait, exemplifies this trend by combining curated selections with same-day delivery in major cities. Meanwhile, multi-brand stores and other channels, such as department stores and duty-free outlets, are experiencing slower growth as consumer foot traffic shifts online and brands prioritize flagship locations over wholesale partnerships. Consolidation among regional retailers and a shift toward franchise models further reflect the evolving dynamics of the luxury retail market.

Geography Analysis

The United Arab Emirates held the largest share of GCC luxury goods revenue in 2025, accounting for 48.15%. This dominance is supported by Dubai's advanced infrastructure, strong tourism appeal, and extensive luxury brand presence, which surpasses any other city in the region. Events such as the Dubai Shopping Festival and Dubai Summer Surprises consistently drive demand, with luxury categories experiencing higher transaction values during these periods. However, as the market matures, growth is slowing, and brands are increasingly shifting investments toward Saudi Arabia. Despite this, the UAE benefits from a favorable regulatory environment with no personal income tax and streamlined customs processes that facilitate cross-border trade. Rising commercial rents in prime locations, however, are pressuring retailer margins, requiring brands to focus on higher conversion rates and increased average transaction values to sustain profitability.

Saudi Arabia is forecast to grow at an annual rate of 10.05% from 2026 to 2031, the fastest among GCC countries. This growth is driven by infrastructure investments, cultural festivals, and a young, digitally native population. Riyadh Season attracted over 15.1 million visitors by the end of Q3 2025, generating SAR 33 billion (USD 8.8 billion) in spending, according to the Ministry of Tourism of Saudi Arabia. The luxury market in Riyadh in 2025 offers significant opportunities for new entrants and flagship store expansions. However, import duty increases in October 2024 and tariff adjustments in November 2025 are complicating pricing strategies and encouraging cross-border shopping in the UAE. Female workforce participation under Vision 2030 is expanding the market for women's luxury goods, while cultural shifts are driving growth in male grooming and tailoring categorie

Qatar, Kuwait, Oman, and Bahrain collectively represent smaller shares of the GCC luxury market but are experiencing growth due to tourism diversification and retail modernization. Qatar's luxury market benefits from sustained post-FIFA World Cup tourism, with Doha achieving significant brand coverage in 2025 and attracting visitors through cultural institutions like the National Museum of Qatar and the Museum of Islamic Art. Kuwait's affluent population and compact geography make it an efficient market for single-brand store rollouts, with brands leveraging high per-capita income to test premium SKUs before scaling to larger markets. Oman and Bahrain remain niche markets where brands can pilot concepts such as modest-fashion lines and Arabic-language customer service. However, lower population densities and GDP per capita limit their near-term revenue potential compared to the UAE and Saudi Arabia.

Mordor Intelligence provides coverage of the luxury goods market across other key regional markets. Detailed country-level analysis extends to Russia incorporating local coverage and market participation, as required.

Regulatory Landscape

Luxury goods trade and retail in the GCC operate under the Common Customs Law for GCC States, with customs process harmonization such as the 2025 Unified Guide for Customs Procedures at First Points of Entry issued in the UAE. Alongside these regional customs baselines, brands also have to manage country-specific import and labeling and tariff actions that can affect pricing and assortment decisions, including Saudi Arabia's increased import duties on personal luxury goods introduced in 2024.

Regulatory attention is also rising around provenance, precious metals, and anti-counterfeit enforcement. In the UAE, Ministerial Decree No. (68) of 2024 established a Due Diligence Policy for responsible sourcing of gold, tightening expectations for refineries and supply-chain stakeholders relevant to luxury jewelry. In Saudi Arabia, the Ministry of Commerce ran an August 2025 public consultation on the Draft Implementing Regulations of the Precious Metals and Gemstones Law, and an October 2025 announcement covered amendments that shift supervision to the Ministry of Industry and Mineral Resources, pointing to more structured oversight for high-value categories sold through boutiques and malls.

Competitive Landscape

Global conglomerates such as LVMH, Kering, and Richemont hold the largest share in the GCC luxury market, coexisting with regional specialists like the Chalhoub Group. The Chalhoub Group operates retail outlets across the Gulf and holds exclusive distribution rights for brands such as Chanel, Dior, and Louis Vuitton. This hybrid structure enables international brands to achieve rapid market penetration while leveraging local retail expertise. At the same time, it creates opportunities for niche players, including independent watchmakers, sustainable fashion labels, and pre-owned luxury platforms. These emerging players benefit from partnerships that maintain brand exclusivity while accessing premium mall networks. For example, independent watch brands have expanded their visibility through curated placements at Ahmed Seddiqi & Sons boutiques. This combination of global scale and regional specialization fosters a structurally diversified luxury ecosystem.

Localization and digital innovation are becoming critical competitive strategies. Brands are introducing Ramadan and Eid capsule collections, offering Arabic-language customer service, and implementing VIP client programs that provide early access to limited editions and private shopping appointments. These efforts strengthen emotional connections with high-spending GCC consumers and enhance client lifetime value. Concurrently, technology is playing a pivotal role in differentiation. LVMH’s Aura blockchain platform ensures tamper-proof provenance records, while Kering’s environmental profit-and-loss methodology increases supply chain transparency. Bulgari’s adoption of blockchain-backed gemstone traceability further enhances consumer confidence in ethical sourcing. Together, these initiatives reinforce trust, traceability, and responsible luxury positioning, making cultural relevance and technological assurance central to brand competitiveness.

Smaller players are disrupting the market by targeting underserved segments such as modest fashion, pre-owned luxury, and men’s grooming, where established brands often have limited offerings. Regional retailers like Majid Al Futtaim and Etoile Group are consolidating their store networks to achieve economies of scale in procurement and marketing. Meanwhile, brands are reclaiming distribution control by opening direct-operated stores and launching e-commerce platforms, compressing wholesale margins for multi-brand retailers. This shift compels retailers to differentiate through exclusive collaborations and experiential retail formats. For instance, Farfetch’s expansion into the Middle East luxury resale highlights the growing traction of pre-owned luxury channels. These dynamics are driving a bifurcation between conglomerate-led scale and specialist-led personalization, intensifying competition across the GCC luxury market.

GCC Luxury Goods Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton

-

Kering SA

-

Compagnie Financière Richemont SA

-

Chanel SA

-

Chalhoub Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Institutional investment into premium retail infrastructure is creating clearer space for luxury brands to secure long-duration, high-visibility locations and build experience-led concepts. A specific signal came in February 2026, when Aldar and Mubadala completed an AED 10 billion retail platform joint venture, consolidating assets including Yas Mall and The Galleria Luxury Collection under Aldar management in Abu Dhabi. This strengthens the landlord-side capability for luxury tenant mix, services, and events, and it fits with the report emphasis on government-supported festivals and destination-led retail.

Cross-border trade policy and compliance-led product differentiation also support tactical opportunities. The UK-GCC trade agreement concluded in May 2026 includes removal of a 5% tariff on industrial and agricultural goods and liberalisation across tariff lines, improving landed-cost dynamics for UK-origin categories such as skincare, toiletries, and perfumes in GCC channels. At the same time, tighter governance in high-value materials, including the UAE gold due-diligence framework under Ministerial Decree No. 68 of 2024, and Saudi rulemaking activity around precious metals and gemstones during 2025, increases the payoff from verified sourcing, traceability tooling, and authenticated resale models. Brands can use these capabilities in-store and online to reduce counterfeiting exposure and support premium pricing narratives.

Recent Industry Developments

- June 2026: RAK Ceramics signed an exclusive multiyear licensing agreement with Roberto Cavalli to develop, manufacture, and distribute Roberto Cavalli-branded ceramic tiles, sanitaryware, and faucets across the GCC and other regional markets. The deal extends luxury branding into the home category, supporting premium lifestyle positioning and creating new cross-category collaboration and merchandising avenues in Gulf luxury retail.

- October 2025: Saudi Arabia's Ministry of Commerce announced amendments to the Precious Metals and Gemstones Law via Cabinet Resolution No. 269, shifting industry supervision to the Ministry of Industry and Mineral Resources. The change tightens the operating environment for jewelry and watch retailers by increasing the importance of compliant sourcing, documentation, and category-specific governance across supply chains.

- December 2024: Dolce & Gabbana opened a 1,500-square-meter luxury center in Diriyah (The City of Earth), combining a boutique with DG Caffe and an exclusive Abaya section. This reinforced Saudi Arabia's role as a flagship-led growth market and demonstrated how brands are embedding localized assortments and experience formats into destination developments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of luxury goods sold across GCC countries, counted at the consumer-facing sales value in USD. It includes premium-priced apparel, footwear, leather goods, watches, jewelry, eyewear, and related luxury items purchased through physical and online retail.

Scope exclusions: We exclude non-luxury mass premium products, second-hand resale value, and non-product luxury services such as travel and hospitality.

Segmentation Overview

-

By Product Type

- Clothing and Apparel

- Footwear

- Leather Goods

- Watches

- Jewellery

- Eyewear

- Other Product Types

-

By End User

- Men

- Women

- Unisex

-

By Distribution Channel

- Single-Brand Stores

- Multi-Brand Stores

- Online Luxury Stores

- Other Distribution Channels

-

By Country

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the economic and retail context for the GCC demand pool and to confirm category definitions for luxury goods. We referenced public sources such as national statistics offices in GCC countries, central bank and government economic releases, customs and trade statistics portals, and tourism authority dashboards that track inbound visitor flows and spend patterns.

To ground the model inputs, we also reviewed company annual reports and investor presentations for leading luxury groups and regional retail operators, along with reputable business press and major mall operator updates on store openings. In parallel, we used paid subscriptions for company financials and news intelligence, and for shipment-level import and export checks where relevant to validate directionally the flow of high-value goods. The sources mentioned here are illustrative only, and many other public documents and datasets were reviewed to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with brand-side leaders, regional distributors, luxury retail managers, mall leasing teams, and selected industry advisors across the GCC. These inputs were used to confirm what sells as luxury within each category, how typical price bands move across the year, and how the mix shifts between single-brand stores, multi-brand stores, and online luxury channels, then to sense-check the final totals for each country.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | |

| Mid tier: 49% | Functional/Unit leaders: 32% | |

| Smaller Players: 20% | Managers: 55% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where national retail and consumer spend signals are reconstructed into a luxury-addressable pool, then refined using category shares supported by interviews. Since tourism can swing demand in the GCC, we treat resident demand and visitor-driven spend as separate checks before totals are finalized.

The model uses practical inputs such as inbound tourist arrivals, luxury mall space additions and occupancy trends, online luxury penetration, category-level price inflation in key items (watches, jewelry, leather goods), and the pace of store openings and closures. Where a public data series is missing for a smaller GCC market, we use proxy indicators like population income brackets and retail density, and later re-check outputs with local expert feedback.

Forecasts are developed using scenario analysis. The base case is shaped by expected tourism momentum, retail expansion plans, and category mix shifts, then adjusted using primary guidance on pricing and promotion intensity. The results are corroborated with selective bottom-up approximations, such as sampled average selling price ranges multiplied by unit-volume proxies for a few anchor categories, alongside channel checks from retailers to avoid double-counting online and offline sales.

Data Validation & Update Cycle

Validation is done through multiple comparison steps so the final number stays consistent with what the market can realistically absorb. We run variance checks across countries and categories, test whether growth aligns with known demand drivers like tourism and retail space expansion, and then review outliers through follow-up expert calls when something appears unusually high or low.

Before sign-off, the model and assumptions go through an internal analyst review so calculation logic, currency handling, and category mapping are consistent across the GCC. Reports are refreshed annually, and interim updates are triggered when material events occur, such as a sharp change in visitor flows, major tax or duty changes, or large-scale retail developments. Right before delivery, a fresh update pass is completed so clients receive the latest view available at that time.

Mordor Intelligence's Gcc Luxury Goods Market Sizing Compared With Other Published Estimates

Published market sizes for GCC luxury goods can look far apart because the word luxury is not applied the same way by every publisher. Differences usually come from what product buckets get counted, whether values are measured at retail sales or closer to trade value, and how the GCC country mix is treated when data is thin.

A common gap driver in this market is scope creep into adjacent luxury spending such as premium travel, luxury cars, or real estate, which can lift totals quickly even if the core luxury goods basket stays unchanged. Other spreads come from how online sales are handled, especially when cross-border ecommerce is blended with in-country retail, and from currency timing and inflation assumptions that move average selling prices year to year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.02 B (2025) | |

| Industry Publisher A | USD 19.60 B (2024) | This estimate appears to include broader luxury spend categories beyond goods, with coverage extending into high-end automobiles and real estate. It also uses a different base year, which makes direct comparison harder. |

| Research House B | USD 10.30 B (2024) | This figure is framed as personal luxury goods, which is typically a narrower basket than total luxury goods. Coverage gaps can also occur through channel and category scope, such as excluding parts of eyewear or other smaller luxury categories. |

The table shows that the spread is mostly explained by what gets counted as luxury and how wide the product basket becomes once adjacent spending is included or removed. By keeping the scope anchored to luxury goods categories across the six GCC countries and cross-checking tourism-driven demand and channel overlap, the total stays more traceable to clear inputs, a choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the GCC luxury goods market?

The GCC luxury goods market size reached USD 15.02 billion in 2025 and is forecast to hit USD 26.66 billion by 2031.

Which segment is growing fastest within Gulf luxury retail?

Watches are forecast to expand at a 10.50% CAGR through 2031, outpacing apparel and other categories.

How fast is men’s luxury spending rising in the Gulf?

Men’s purchases are projected to grow at 10.76% per year between 2026-2031, the highest rate among end-user groups.

What role do cultural festivals play in sales?

Events such as Riyadh Season and Dubai Shopping Festival boost luxury transaction values by up to 30% during their runs, making them pivotal launch windows.

Page last updated on: