Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.35 Billion |

| Market Size (2026) | USD 5.63 Billion |

| Market Size (2031) | USD 7.28 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Luxury Goods Market Analysis by Mordor Intelligence

The Brazil luxury goods market size is expected to grow from USD 5.35 billion in 2025 to USD 5.63 billion in 2026 and is forecast to reach USD 7.28 billion by 2031 at 5.28% CAGR over 2026-2031. Resilient domestic demand, concentrated wealth among 16 million affluent consumers, and rising disposable incomes in upper-middle-class households drive the expansion of the market size. While real GDP growth is set to moderate to 2.4% in 2025, gains in formal employment and wages bolster spending on premium products [1]Source: The Institute of Applied Economic Research," Ipea maintains GDP growth projection of 2.4% for 2025 and projects 2% for 2026", ipea.gov.br. Millennials and Gen Z buyers add an ESG lens to buying decisions, prompting brands to launch lab-grown diamonds and traceable leather lines that align with sustainability preferences. Multinational houses are enlarging flagships in São Paulo and Rio to capture spending that might otherwise flow to Miami or Paris, while Brazilian groups are consolidating to defend share and strengthen omnichannel capability.

Key Report Takeaways

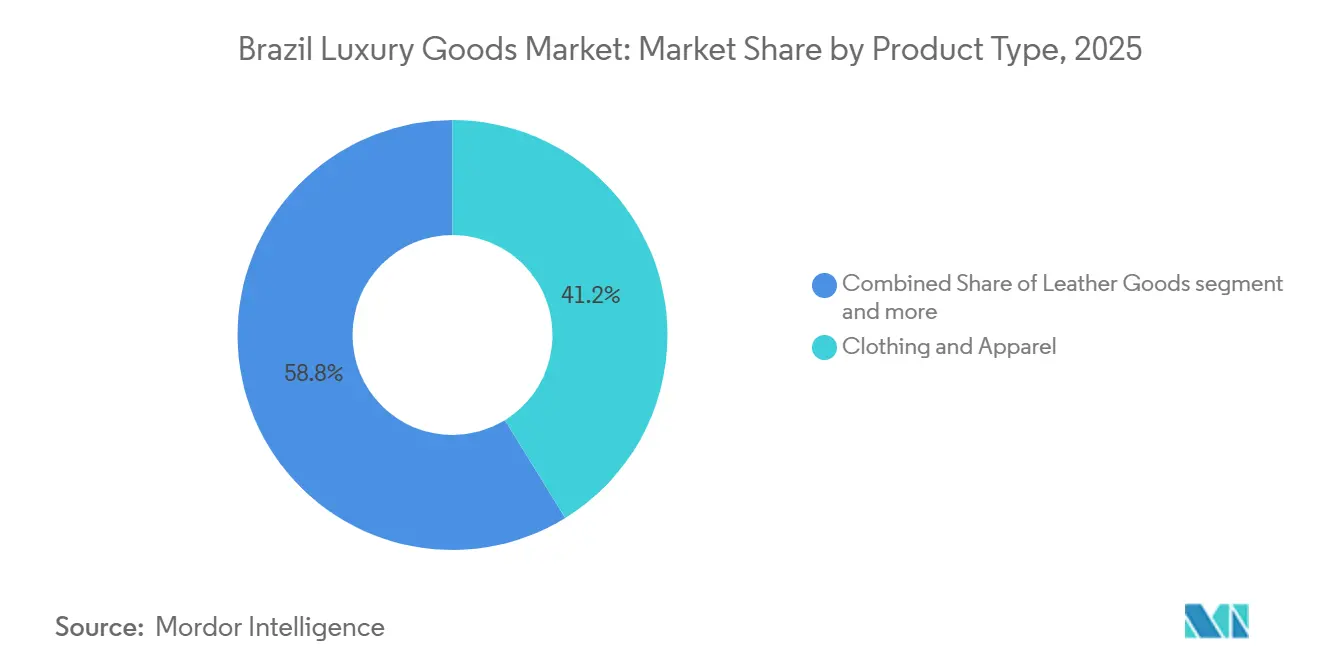

- By product type, clothing and apparel led with 41.22% revenue share in 2025, while leather goods are projected to expand at a 5.79% CAGR to 2031.

- By end user, women commanded 56.72% share in 2025; the men’s segment is advancing at a 7.02% CAGR over 2026-2031.

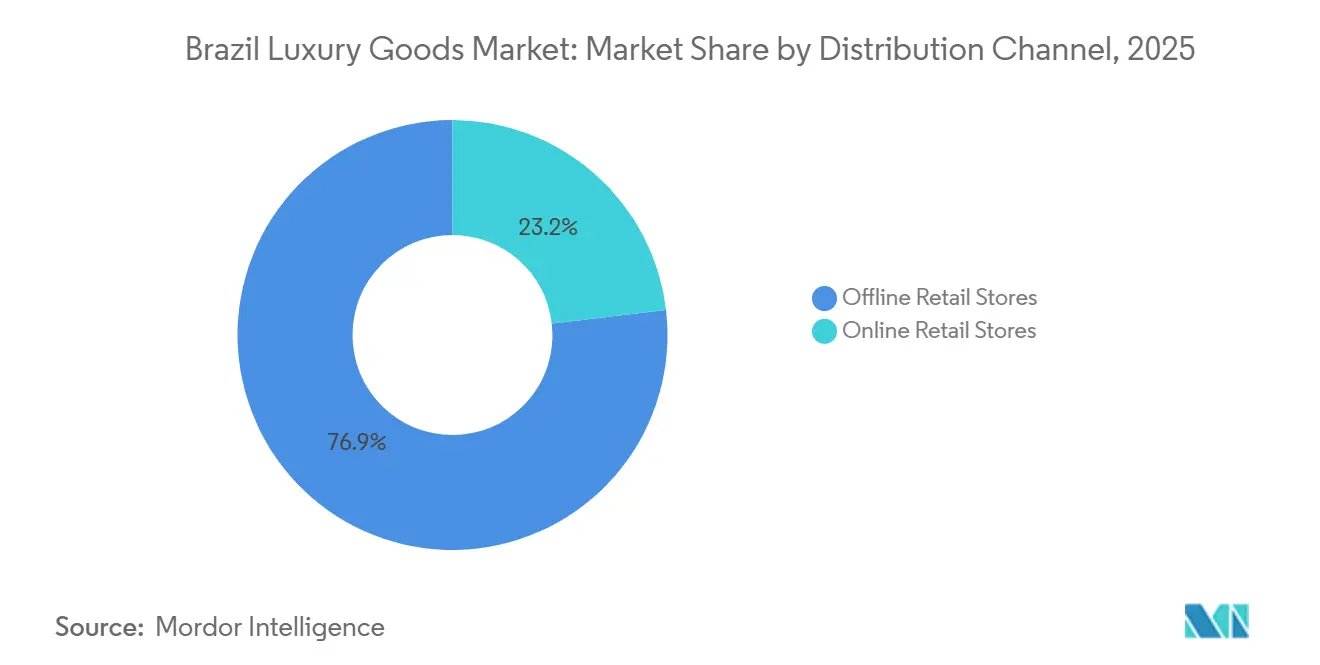

- By distribution channel, offline retail stores held 76.85% share in 2025, whereas online retail stores are expanding at a 6.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brazil's upper-middle class surge in disposable income | +1.2% | National, concentrated in São Paulo, Rio de Janeiro, Brasília | Medium term (2-4 years) |

| Global luxury brands broaden retail presence in Brazil | +1.0% | São Paulo, Rio de Janeiro, with spillover to Curitiba, Goiânia | Short term (≤ 2 years) |

| Millennials and Gen Z sustainability preferences wield growing influence | +0.8% | Urban centers (São Paulo, Rio, Belo Horizonte), coastal regions | Long term (≥ 4 years) |

| Tourism spending surges in São Paulo and Rio de Janeiro | +0.9% | São Paulo, Rio de Janeiro, extending to Florianópolis, Salvador | Short term (≤ 2 years) |

| Increasing influence of celebrity and influencer endorsements | +0.6% | National, amplified via digital platforms | Medium term (2-4 years) |

| Brand heritage reinforcing premium perception | +0.7% | National, stronger in established luxury hubs (São Paulo, Rio) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Brazil's Upper-Middle Class Surge in Disposable Income

Formal employment gains and real wage growth are recalibrating purchasing power among Brazil's upper-middle class, a cohort that expanded as unemployment fell to 6.8% in February 2025, according to the Brazilian Institute of Geography and Statistics. Household consumption expenditure rose despite inflation running at 5.7% in 2025, suggesting that income growth in the top two quintiles is outpacing headline price pressures, according to the Central Bank of Brazil. This dynamic is particularly pronounced in São Paulo and Brasília, where professional services and technology sectors are driving salary premiums. The shift matters because luxury brands rely on repeat purchases from affluent households; an increase in disposable income among the top section of earners can translate to a significant uplift in luxury spending due to high income elasticity of demand. Brazil's tax reform under Complementary Law 214/2025 is expected to simplify the consumption tax structure by 2027, potentially reducing cascading effects that currently inflate luxury goods prices, according to the Ministry of Finance.

Global Luxury Brands Broaden Retail Presence in Brazil

Multinational luxury houses are treating Brazil as a priority market for physical expansion, reversing a decade of cautious store rationalization. Tiffany opened a 408-square-meter flagship at Iguatemi São Paulo in January 2025, its largest Latin American footprint, signalling confidence in sustained demand for high-ticket jewelry and watches. Hermès is relocating its Rio de Janeiro boutique to a larger 233.1-square-meter space at Rio Village Mall, while Louis Vuitton operates 8 stores across São Paulo, Rio, Goiânia, Curitiba, and Brasília. The strategic calculus hinges on capturing tourists and domestic elites before they travel abroad; Brazil's currency depreciation makes international shopping trips less attractive, creating a window for brands to lock in local sales. LVMH reported strong performance in Brazil during Q3 2024, with selective distribution and price increases offsetting currency headwinds. This retail buildout also reflects brands' desire to control the customer experience and combat counterfeits through direct channels.

Millennials and Gen Z Sustainability Preferences Wield Growing Influence

Younger Brazilian consumers are demanding verifiable sustainability credentials from luxury brands, a shift that is reshaping product development and supply chain transparency. Pandora's introduction of lab-grown diamonds across 35 Brazilian stores in 2024 exemplifies this trend; the brand positioned the move as both an ethical and aesthetic choice, resonating with Gen Z buyers who prioritize traceability. L'Occitane au Brésil, a local subsidiary of the French beauty group, grew in 2024 by emphasizing Brazilian biodiversity and fair-trade sourcing of ingredients like açaí and cupuaçu. This cohort's influence extends beyond product attributes to brand activism; luxury houses that fail to articulate clear ESG commitments risk losing share to competitors with stronger sustainability narratives. The trend is amplified by digital platforms where influencers scrutinize brands' environmental and social governance practices, creating reputational risks for laggards.

Tourism Spending Surges in São Paulo and Rio de Janeiro

In 2025, the Ministry of Tourism aims for 8 million international arrivals, bolstered by new long-haul routes and a favorable exchange rate [2]Source: Presidency of the Republic," Brazil welcomed 6.6 million international tourists in 2024, its best historical mark", gov.br. Foreign tourist expenditure in Brazil reached USD 7.3 billion in 2024, a 15-year high, with São Paulo and Rio de Janeiro capturing the majority of luxury-related spending, according to Ministério do Turismo. The federal government's Tax-Free program, launched in January 2025, allows international visitors to reclaim VAT on purchases exceeding BRL 500, removing a longstanding barrier to high-value transactions. São Paulo's tourism sector is approaching 10% of state GDP, driven by business travel, cultural events, and gastronomy, all of which create touchpoints for luxury brand engagement. The influx of affluent travellers from the United States, Europe, and Asia provides luxury retailers with a diversified revenue base less vulnerable to domestic economic cycles. Brands are responding by staffing multilingual sales associates and curating product assortments that appeal to international tastes, such as limited-edition leather goods and locally inspired jewelry designs.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import taxes and duties burden luxury goods | -1.3% | National, most acute for imported finished goods | Short term (≤ 2 years) |

| Strict regulations on sourcing and materials | -0.5% | National, with heightened scrutiny in São Paulo, Rio de Janeiro | Medium term (2-4 years) |

| Counterfeit products diluting brand value | -0.8% | National, concentrated in e-commerce and informal retail | Medium term (2-4 years) |

| Supply chain complexity for premium materials | -0.6% | National, affecting import-dependent categories (watches, leather goods) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Taxes and Duties Burden Luxury Goods

Brazil's luxury goods market faces mounting challenges as tariffs on watches and jewelry, combined with an impending IBS/CBS VAT, significantly inflate shelf prices. This price surge is prompting affluent Brazilians to increasingly turn to international shopping destinations for their luxury purchases. Furthermore, the elimination of duty exemption for e-commerce now subjects even certified platforms to a hefty 20% charge, further inflating online shopping baskets and discouraging domestic online purchases [3]Source: Ministry of Finance," Novas Regras 01/08/2024", gov.br. The Remessa Conforme program, which offers reduced rates for e-commerce imports under USD 50, has inadvertently fuelled a grey market where luxury accessories are mislabelled to exploit the threshold, according to SECEX. Complementary Law 214/2025 aims to unify consumption taxes by 2027, but the transition period introduces uncertainty as brands navigate overlapping federal and state rules. The tax burden also disadvantages Brazil-based retailers against duty-free shopping in Miami or Paris, where Brazilian tourists can purchase the same items at 30-40% lower prices.

Counterfeit Products Diluting Brand Value

Counterfeit luxury goods represent a persistent threat to brand equity and revenue, with Brazil ranking among the top global markets for fake products. Operation Natal 2024, conducted by Receita Federal, seized BRL 1.5 billion worth of counterfeit luxury items, including handbags, watches, and apparel, underscoring the scale of illicit trade. Counterfeits circulate through e-commerce platforms, street markets, and social media, where sellers exploit lax enforcement and consumer price sensitivity. The proliferation of high-quality fakes, some nearly indistinguishable from authentic products, erodes the exclusivity that underpins luxury pricing. Brands invest heavily in authentication technologies (RFID tags, blockchain provenance) and legal enforcement, but the decentralized nature of counterfeit networks makes eradication difficult. The issue is compounded by cultural attitudes; some Brazilian consumers view counterfeits as acceptable alternatives when genuine articles are prohibitively expensive due to import taxes. This dynamic forces brands to balance aggressive anti-counterfeiting measures with the risk of alienating potential customers who may eventually trade up to authentic goods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Leather Goods Outpace Apparel's Dominance

Leather Goods is set to expand at 5.79% CAGR from 2026 to 2031, the fastest rate among product categories, even as Clothing and Apparel held 41.22% market share in 2025. The divergence reflects shifting consumer priorities: handbags, wallets, and belts offer higher perceived value per transaction and benefit from brands' emphasis on artisanal craftsmanship and heritage storytelling, which resonate with Brazil's affluent buyers. Hermès and Louis Vuitton have capitalized on this trend by launching Brazil-exclusive leather colorways and limited-edition collections that tap into local cultural motifs. Clothing and Apparel, while dominant, faces margin pressure from Brazil's high import duties on finished textiles and competition from domestic luxury brands like Osklen.

Footwear, Eyewear, Jewelry, and Watches collectively account for the remaining share, with each segment exhibiting distinct dynamics. Jewelry growth is anchored by H.Stern, which operates approximately 280 stores across 32 countries and emphasizes Brazilian gemstones like aquamarine and imperial topaz to differentiate from European rivals. Watches face headwinds from gray-market imports and counterfeit infiltration, though Rolex and Richemont brands maintain pricing power through authorized dealer networks and after-sales service. Eyewear and other product types (including fragrances and accessories) are expanding as brands extend product lines to capture lower-ticket aspirational buyers. INMETRO's conformity requirements for eyewear and cosmetics add regulatory complexity but also serve as a barrier to entry for unbranded competitors.

By End User: Female Dominance, Male Momentum

Men's luxury consumption is projected to grow at 7.02% CAGR from 2026 to 2031, outpacing the overall market and signaling a structural shift in gender-based spending patterns, even as Women commanded 56.72% share in 2025. The acceleration reflects younger male cohorts' willingness to allocate discretionary income to premium watches, footwear, grooming products, and tailored apparel, categories historically underserved in Brazil's luxury landscape. Nike's expansion in Brazil, though primarily in sportswear, elevated men's footwear expectations, creating spillover demand for luxury sneakers and hybrid dress-casual styles. Rolex and Richemont brands are benefiting from men's preference for investment-grade timepieces that signal professional success and can be worn daily, contrasting with women's jewelry, which is often reserved for special occasions.

Women remain the core demographic, driven by higher purchase frequency across apparel, handbags, jewelry, and cosmetics. Chanel, Prada, and Burberry have tailored assortments to Brazilian women's preferences for bold colors, tropical prints, and versatile pieces that transition from business to social settings. The Unisex segment, while smaller, is gaining traction as brands launch gender-neutral fragrances, eyewear, and accessories that appeal to Gen Z's fluid approach to fashion. Pandora's lab-grown diamond collections, introduced across 35 Brazilian stores in 2024, are marketed as unisex, reflecting the brand's strategy to broaden its customer base beyond traditional female jewelry buyers.

By Distribution Channel: Offline Dominance Persists as Digital Gains Momentum

Offline Retail Stores accounted for 76.85% of the distribution share in 2025, underscoring the enduring importance of tactile and experiential luxury shopping, yet Online Retail Stores are expanding at 6.33% CAGR through 2031 as brands deploy omnichannel strategies that blur physical and digital boundaries. The offline advantage stems from consumers' desire to inspect craftsmanship, try on products, and receive personalized service, elements that are difficult to replicate online, especially for high-ticket items like jewelry and watches. Tiffany's January 2025 opening of a 408-square-meter flagship at Iguatemi São Paulo exemplifies the continued investment in physical retail, with the store featuring private consultation rooms and bespoke design services.

Online channels are gaining share through innovations that address luxury buyers' concerns about authenticity and presentation. Brands are responding with augmented-reality try-on tools, virtual styling consultations, and premium delivery services that include white-glove unboxing and same-day fulfillment in São Paulo and Rio. L'Occitane's e-commerce platform grew in 2024, driven by subscription models and exclusive online product launches. Fragrance e-commerce surged in H1 2024, suggesting that lower-ticket luxury categories are more amenable to digital purchasing. DHL's luxury logistics whitepaper emphasizes the need for omnichannel processing centers that can handle both store replenishment and direct-to-consumer orders, a capability that separates leaders from laggards in customer satisfaction.

Geography Analysis

Brazil's luxury goods market is heavily concentrated in São Paulo and Rio de Janeiro, driven by higher per-capita income, international tourism, and the presence of flagship stores from global brands. São Paulo, as Latin America's financial hub, attracts business travelers and hosts corporate executives who constitute a core luxury customer segment. Rio de Janeiro benefits from leisure tourism and cultural cachet, with foreign tourist spending reaching USD 7.3 billion nationally in 2024, a 15-year record, according to the Ministério do Turismo. Secondary cities like Curitiba, Goiânia, and Brasília are emerging as growth frontiers; Louis Vuitton operates stores in all three, signaling that luxury demand is diffusing beyond coastal metros as regional economies mature.

Brazil's regulatory environment shapes geographic strategy through state-level ICMS (VAT) variations, which range from 7% to 18% in São Paulo depending on product category, creating pricing disparities that brands must navigate, according to the Brazilian Federal Revenue Service. Complementary Law 214/2025 aims to unify consumption taxes by 2027, but the transition period introduces uncertainty as federal and state authorities negotiate revenue-sharing arrangements, according to the Ministry of Finance. SECEX and SISCOMEX, Brazil's foreign trade secretariat and electronic trade system, mandate detailed documentation and RADAR licensing for importers, creating barriers to entry for smaller luxury brands but also professionalizing the market by weeding out gray-market operators.

SENACON, the National Consumer Secretariat, enforces the Consumer Protection Code (Law 8.078/1990), which mandates Portuguese-language labeling, 90-day warranties, and 24-hour recall notification, with fines up to BRL 12 million for non-compliance. These regulations, while protecting consumers, impose operational complexity that favors established brands with local legal and compliance teams. The geographic concentration of luxury retail also reflects infrastructure realities; DHL's premium delivery services and omnichannel processing centers are most developed in São Paulo and Rio, limiting e-commerce penetration in interior regions where logistics costs and delivery times remain prohibitive.

Competitive Landscape

The Brazil luxury goods market exhibits moderate concentration, indicating that while LVMH, Kering, and Richemont dominate high-margin categories such as jewelry, watches, and leather goods, local players Arezzo and H.Stern retain significant share through vertical integration and proximity to domestic supply chains. LVMH's portfolio, spanning Louis Vuitton, Dior, and Tiffany, reported strong performance in Brazil during Q3 2024, driven by selective distribution and price increases that offset currency headwinds. Kering, by contrast, faced challenges as Gucci's brand repositioning struggled to resonate with Brazilian consumers, who favor bold aesthetics over minimalist design.

Richemont's ERP implementation in Brazil during FY24 signals a long-term commitment to operational efficiency and omnichannel integration, a strategic imperative as online channels expand at 6.33% CAGR. The February 2024 Arezzo-Soma merger, creating a BRL 12 billion entity with 34 brands and 2,056 stores, represents a defensive consolidation by Brazilian firms seeking scale to compete against multinational entrants. Pandora's introduction of lab-grown diamonds across 35 Brazilian stores in 2024 exemplifies how technology can disrupt traditional jewelry economics while appealing to younger buyers' sustainability preferences.

L'Occitane au Brésil's growth in 2024, driven by Brazilian biodiversity ingredients and fair-trade sourcing, demonstrates that localized narratives can compete against global prestige. Emerging disruptors include digital-native brands that bypass traditional retail to offer luxury goods at discounts through direct-to-consumer models, though they face authenticity concerns and lack the brand heritage that justifies premium pricing. Brands are leveraging augmented-reality try-on tools, GenAI-enabled personalization, and omnichannel fulfillment to win share, capabilities that require significant IT investment and favor larger players with global scale.

Brazil Luxury Goods Industry Leaders

-

Kering Group

-

LVMH Moët Hennessy Louis Vuitton

-

Compagnie Financière Richemont SA

-

PUIG

-

Prada Holding S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The iconic jeweler Tiffany & Co. opened its first flagship store in Brazil in 2025, located inside the Iguatemi São Paulo mall. This two-floor location is one of Tiffany’s largest in the region and includes dedicated spaces for watches and high-jewelry offerings unique to the Brazilian market.

- April 2025: Tiffany launched its Blue Book 2025 collection, a high-end jewelry collection titled Sea of Wonder, in 2025. While this was a global launch (not Brazil-exclusive), the collection’s presence is relevant given Tiffany’s new flagship and market focus.

- June 2024: Tommy Hilfiger made a multi-year partnership with the United States SailGP Team as its Official Lifestyle Apparel Partner. Sharing an ethos of disruption and innovation, Tommy Hilfiger and the US SailGP Team use the partnership to push the boundaries of performance, design, and culture.

Brazil Luxury Goods Market Report Scope

Luxury goods are premium products that command higher prices than their counterparts in the market. The Brazil Luxury Goods Market is Segmented by Product Type (Clothing and Apparel, Footwear, Jewelry, Watches, Leather Goods, and More), End User (Male, Female, and More), and Distribution Channel (Offline Retail Stores and Online Retail Stores). The Market Forecasts are Provided in Terms of Value (USD).

Product Type

| Clothing and Apparel |

| Footwear |

| Eyewear |

| Leather Goods |

| Jewelry |

| Watches |

| Other Product Types |

End-User

| Men |

| Women |

| Unisex |

Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

| Product Type | Clothing and Apparel |

| Footwear | |

| Eyewear | |

| Leather Goods | |

| Jewelry | |

| Watches | |

| Other Product Types | |

| End-User | Men |

| Women | |

| Unisex | |

| Distribution Channel | Offline Retail Stores |

| Online Retail Stores |

Key Questions Answered in the Report

How big is the Brazil luxury goods market in 2026?

The market is forecast to reach USD 7.28 billion by 2031.

Which product category is expected to grow fastest through 2031?

Leather Goods is projected to expand at a 5.79% CAGR between 2026 and 2031.

Why is the men’s segment gaining momentum?

Younger male consumers are allocating more discretionary income to premium sneakers, watches, and grooming, driving a 7.02% CAGR for men’s luxury consumption.

How will the Tax-Free program influence luxury sales?

By allowing VAT refunds to tourists, the program improves price competitiveness and is expected to lift tourist-driven sales in São Paulo and Rio.

Page last updated on: