GCC Gaming Headsets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

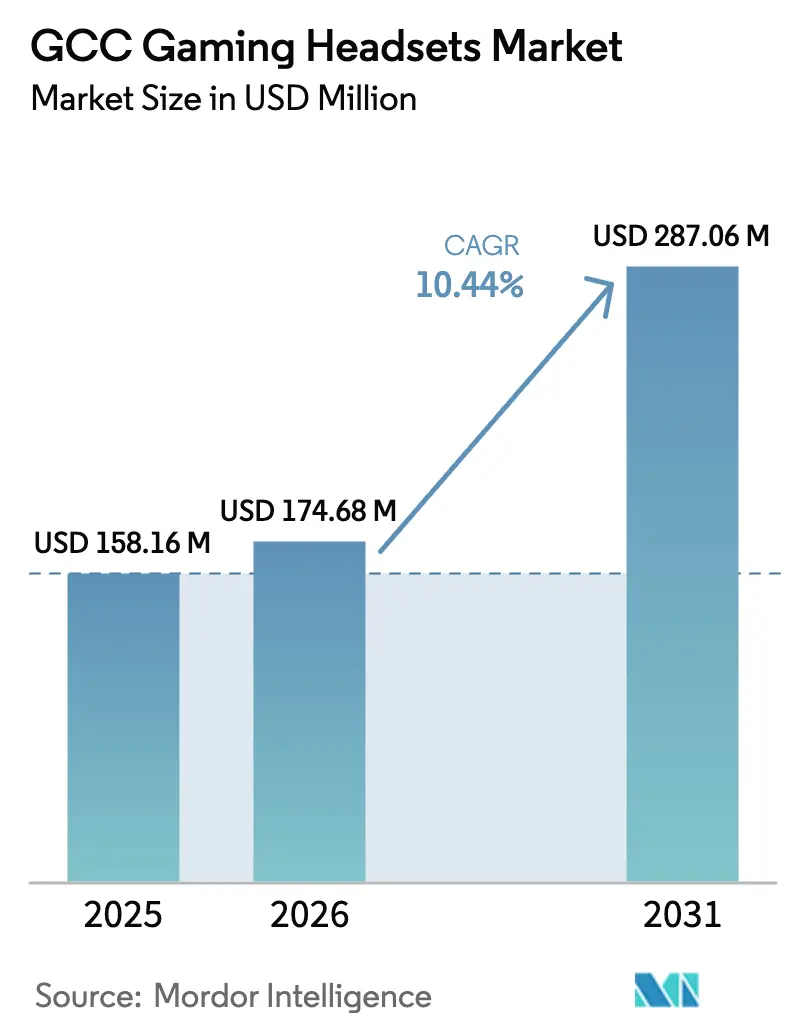

| Base Year Market Size (2025) | USD 158.16 Million |

| Market Size (2026) | USD 174.68 Million |

| Market Size (2031) | USD 287.06 Million |

| Growth Rate (2026 - 2031) | 10.44% CAGR |

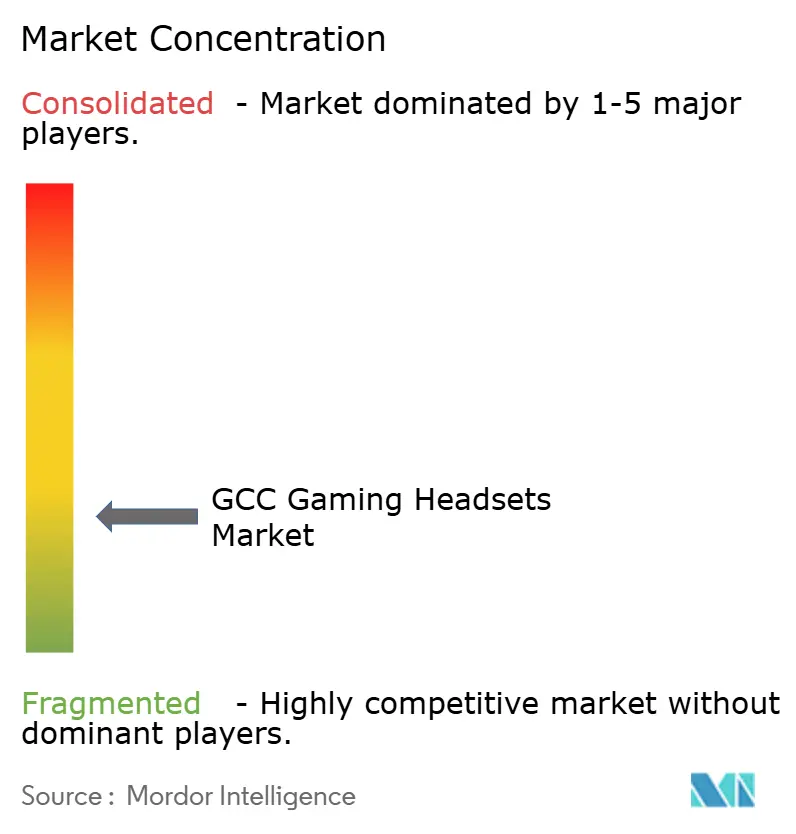

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Gaming Headsets Market Analysis by Mordor Intelligence

The GCC Gaming Headsets Market size was valued at USD 158.16 million in 2025 and estimated to grow from USD 174.68 million in 2026 to reach USD 287.06 million by 2031, at a CAGR of 10.44% during the forecast period (2026-2031). Growth reflects Gulf governments’ decision to use gaming as an industrial diversification lever, with Saudi Arabia allocating USD 38 billion to build a domestic games ecosystem that directly increases demand for performance headsets across the region.[1]Frank Kane, “Video Game Industry Helping to Reshape Saudi Economy, Experts Say,” Arab News, arabnews.com Improved GPU supply, a rebound in enthusiast spending, and the launch of large-scale esports venues underpin higher unit volumes for premium models, while tariff-driven price inflation encourages brands to reposition mid-tier wired models to protect value-conscious buyers. E-commerce platforms benefit from upgraded logistics corridors through Jebel Ali and King Abdullah Ports, translating rising internet penetration above 95% in the UAE into double-digit online sales growth for headsets that combine low-latency wireless codecs with Arabic firmware menus. Manufacturers focus on heat-resistant plastics, extended battery life, and dustproof mic booms to cope with the Gulf’s desert environment, thereby lowering product returns and sustaining retail margins across Saudi Arabia, UAE, and Qatar.

Key Report Takeaways

- By compatibility type, console headsets held 46.45% of GCC gaming headset market share in 2025; mobile/VR devices are set to grow at a 17.47% CAGR through 2031.

- By connectivity, wired models captured 56.85% of GCC gaming headset market size in 2025, while wireless solutions advance at a 13.78% CAGR.

- By sales channel, retail outlets commanded 64.05% of GCC gaming headset market share in 2025; online platforms record the fastest 12.74% CAGR to 2031.

- By gamer type, casual gamers represented 55.12% of GCC gaming headset market share in 2025; streamers and content creators rise at an 17.95% CAGR.

- By audio technology, stereo units controlled 51.05% of GCC gaming headset market size in 2025, whereas spatial/3D audio models post a 19.40% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Figures recorded within Middle east and africa feed into a worldwide estimate while studying the global industry. Mordor Intelligence's gaming headsets market size captures this aggregation.

GCC Gaming Headsets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising internet penetration & cloud gaming | +2.8% | GCC-wide with UAE, Saudi Arabia strongest | Medium term (2-4 years) |

| Expansion of esports arenas & tournaments | +3.2% | Saudi Arabia, UAE core; spillover to Qatar, Kuwait | Long term (≥ 4 years) |

| Youth disposable income growth | +2.1% | GCC-wide, highest in oil-rich states | Short term (≤ 2 years) |

| Government mega-investments in gaming | +4.5% | Primarily Saudi Arabia, secondary UAE | Long term (≥ 4 years) |

| Surge in Arabic-localized multiplayer titles | +1.9% | GCC-wide | Medium term (2-4 years) |

| Expansion of female gamer segment | +1.4% | UAE and Saudi Arabia lead | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Internet Penetration & Cloud Gaming Adoption

Gulf telcos completed multi-gig fibre roll-outs and early 5G Stand-Alone cores in 2024, enabling seamless cloud-gaming sessions that shift audio latency demands from the console to the headset DSP.[2]Monsha’at Economic Division, “SME Monitor Q4 2023,” Monsha’at, monshaat.gov.sa Brands such as Logitech and Sony now include low-latency LE Audio codecs and automatic network jitter mitigation in mid-tier wireless models, making cable-free play viable for e-football cafés in Dubai and Riyadh. Because cloud platforms remove the need for high-spec PCs, consumers redirect savings toward peripherals that improve competitive performance, driving up ASPs for noise-cancelling microphones and spatial audio drivers. Regional internet penetration above 95% in UAE and Qatar accelerates this shift from entry-level stereo headsets toward premium multi-platform SKUs. Consequently, the GCC gaming headset market registers sustained double-digit revenue growth in wireless SKUs even as unit volumes stay flat in wired categories.

Proliferation of E-Sports Arenas & Tournaments

Institutional investment reshapes buyer archetypes by adding bulk orders from venue operators to traditional retail purchases. True Gamers is rolling out 150 Saudi esports centres stocked with tournament-grade audio peripherals that meet latency regulations mandated by event partners. Riyadh’s Esports World Cup, with its USD 60 million prize pool, normalised broadcast-quality audio among casual viewers, sparking an aspirational uptick in sales of 40 mm neodymium driver headsets that emulate pro gear. Abu Dhabi’s USD 280 million Esports Island adds further institutional demand, compelling manufacturers to guarantee replacement-cycle contracts that lock in multi-year revenues.[3]Esports Insider Team, “True Gamers Announces $280m Esports Island in Abu Dhabi,” Esports Insider, esportsinsider.com As venue operators standardise product SKUs, distributors gain negotiating power, pressuring OEMs to offer climate-proof housings and Arabic UI updates to win tenders.

Growing Youth Disposable Income

Oil-funded public salaries place GCC youth purchasing power above global peers, allowing premium headset penetration levels uncommon in emerging markets. With 60% of the population under 30, headset upgrades follow console refresh cycles rather than wage cycles, creating predictability in quarterly demand curves. Young consumers who view esports streaming as an income source justify headset prices near USD 350 when features include replaceable ear-cushion kits and dual-mode wireless protocols. Government-run talent incubators provide subsidies for equipment purchases that effectively lower retail price points without compressing OEM gross margins.

Government Mega-Investments in Gaming

The Public Investment Fund’s USD 38 billion program commits to 250 new gaming companies and 39,000 jobs by 2030, translating to professional headsets in every training lab and on every esports stage. Savvy Games Group spends USD 37.7 billion on studio acquisitions, importing global audio standards that elevate SKU specifications across retail shelves. State-backed esports curricula include headset-hygiene protocols, boosting demand for removable microphone filters and antimicrobial ear pads that lengthen product replacement cycles while raising unit prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Piracy, regulatory uncertainty & fraud | −1.8% | Region-wide, with the sharpest drag on online sales | Short term (≤ 2 years) |

| High import tariffs & rising logistics bills | −2.3% | All GCC markets, but especially the smaller states | Medium term (2-4 years) |

| Fragmented retail networks in smaller Gulf economies | −1.2% | Bahrain, Oman and Kuwait | Medium term (2-4 years) |

| Headset durability issues in desert heat and humidity | −0.9% | Across the GCC, most acute in Saudi Arabia and the UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Piracy, Regulatory Uncertainty and Fraud

Counterfeit peripherals flow into Bahrain and Oman’s free-zones, undermining consumer trust, while fragmented e-commerce return rules deter high-ticket wireless purchases.[4]Brendan Sinclair, “Trump's Tariffs: Video Games Braced for Job Losses, Higher Prices and Falling Investment,” The Game Business, thegamebusiness.com Payment fraud rate spikes during major shopping festivals raise dispute costs for platforms, adding friction to headset adoption. Large retailers now embed NFC chips for on-shelf authentication, but smaller vendors cannot absorb the extra BOM costs, widening the credibility gap between channels.

High Import Tariffs and Logistics Costs

Average headset wholesale prices rose 8.7% YoY in Q1 2025 as US-China trade tensions rerouted supply chains through costlier Southeast Asian assembly plants. GCC customs duties vary from 5% to 15%, prompting cross-border price arbitrage that erodes authorised dealer margins. Extreme summer heat requires refrigerated warehouse space, lifting per-unit handling costs above global averages. Together, these factors shave 2.3 percentage points off forecast CAGR yet do not derail the upward trajectory of the GCC gaming headset market due to offsetting demand drivers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compatibility Type: Console Dominance Faces Mobile Disruption

Console models generated the largest GCC gaming headset market size within the category, anchored by a 46.45% share in 2025, reflecting entrenched PlayStation and Xbox user bases across Saudi Arabia and Kuwait. Mobile and VR options, however, are scaling faster at an 17.47% CAGR as telecom operators bundle cloud-gaming subscriptions with 5G plans. The arrival of lightweight hybrid designs that support USB-C, 3.5 mm, and low-latency Bluetooth modes lets players shift from living-room consoles to smartphones without changing headsets, blurring segment boundaries inside the GCC gaming headset market.

Demand for smartphone-ready cans is reinforced by an average 8.7-hour weekly mobile playtime among Gulf users. Sony’s regional INZONE launch added a 40-hour battery headset tuned for mobile shooters, signalling legacy console vendors’ pivot toward cross-platform ecosystems. Retailers now allocate equal shelf space to console and multipurpose headsets, while VR arcades in Dubai Mall buy commercial-grade ear-cups with antimicrobial coatings, further diversifying revenue streams for the GCC gaming headset market.

By Connectivity: Wireless Acceleration Despite Wired Leadership

Wired units still hold 56.85% of GCC gaming headset market share because tournament regulations often force players to use cabled gear for latency parity. Yet wireless shipments are climbing 13.78% CAGR, propelled by new LE Audio-enabled chipsets that cut lag below 20 ms and by the Gulf’s cultural preference for cable-free living-room setups. Gaming cafés in Riyadh now rent dual-mode headsets so amateurs can practice on wired lines and compete on wireless rigs, gradually normalising cordless play.

Dustproof USB-C charging ports feature prominently on premium SKUs to prevent sand ingress during daily commutes, addressing a chronic failure point cited by retailers. Battery lifetimes surpassing 40 hours let creators finish multi-day streaming events without mid-match charging, removing a key psychological barrier to wireless adoption in the GCC gaming headset market.

By Sales Channel: Online Momentum Challenges Retail Dominance

Retail shops accounted for 64.05% of GCC gaming headset market share in 2025 as consumers valued hands-on trials and immediate returns. However, online sales race ahead at a 12.74% CAGR, aided by same-day delivery in Dubai and Riyadh urban cores. Platforms like Noon integrate Arabic chatbots that offer fit-test advice, lowering return rates and boosting conversion.

Brick-and-mortar chains evolve into experience centres where shoppers benchmark frequency curves through in-store demo rigs before purchasing online via QR code. Click-and-collect models shorten last-mile costs, merging channel advantages while sustaining the overall health of the GCC gaming headset market.

By Gamer Type: Creator Economy Drives Premium Demand

Casual players make up 55.12% of GCC gaming headset market share, but streamers and content creators deliver the fastest 17.95% CAGR. Riyadh-based content houses under Savvy Games Group sponsor creator collectives, increasing the visibility of boom-arm mics with cardioid pick-up patterns that eliminate AC hum in Gulf homes.

Professional esports athletes procure multiple headsets per year to match team branding changes and sponsorship deals, inflating replacement cycles. Meanwhile, female creators emphasise comfort and aesthetics, nudging OEMs toward lighter frames and colour variants, trends that cascade into mainstream SKUs within the GCC gaming headset market.

By Audio Technology: Spatial Audio Revolution Accelerates

Stereo formats still command 51.05% of GCC gaming headset market size as price-sensitive buyers in Bahrain and Oman favour entry-level gear. Yet spatial/3D audio units climb at a 19.40% CAGR because Arabic-localized shooters encode vertical sound cues that require HRTF processing. Logitech’s recent DTS Headphone:X integration proves wireless models can now match wired localisation accuracy.

Virtual 7.1 acts as a mid-step, appealing to upgraders reluctant to pay top-tier premiums yet eager for immersion. VR adoption in education brings headsets into classrooms, broadening the user base and thrusting spatial audio into everyday academic life, thereby cementing future demand for advanced technologies across the GCC gaming headset market.

Geography Analysis

Saudi Arabia contributed more than half of GCC gaming headset market revenue in 2025 thanks to its USD 38 billion gaming stimulus package that underwrites 250 incubation studios and 150 esports centres. The kingdom’s 58% gamer penetration ensures deep consumer pools, while institutional procurement plugs in predictable baseline volumes for wired tournament rigs, lifting the GCC gaming headset market size within the country well ahead of peers. Price floors remain stable because PIF subsidies cushion tariff effects, preserving brand margins.

The United Arab Emirates secures second position through a unique blend of affluent expatriates and proactive state-backed tech clusters, exemplified by Abu Dhabi’s USD 280 million Esports Island that stipulates pro-grade headsets for its academy rooms. Dubai’s cross-docking hubs slash lead-times to 48 hours, making it the default re-export node for Oman, Bahrain, and beyond. Higher internet penetration and digital-wallet adoption spur online volumes, particularly for wireless SKUs suited to on-the-go gaming lifestyles that dominate UAE commuter culture.

Qatar, Kuwait, Oman, and Bahrain collectively form the emerging tier. Qatar’s high per-capita GDP encourages luxury headset purchases bundled with limited-edition FIFA esports packages. Kuwait remains a console stronghold where retail chains anchor promotions around Sony exclusives tied to local membership clubs. Oman and Bahrain offset small population scales with aggressive e-commerce plays that allow cross-border shoppers to access the full spread of the GCC gaming headset market catalog. All four states benefit from pan-Gulf promotional calendars such as White Friday that synchronise demand spikes and create logistical economies of scale.

Mordor Intelligence evaluates the gaming headsets market across all key regional markets, including Europe, Middle East and Africa, and North America, with deeper country-level insights covering United Kingdom, Germany, United States, Canada, Japan, and China.

Competitive Landscape

The GCC gaming headset market shows moderate fragmentation as the top five vendors command 32% collective revenue, leaving meaningful share for challenger brands. Turtle Beach retains core leadership through a 14-year console lineage and distributor tie-ups with Jarir and Virgin Megastore that cover 180 brick-and-mortar points. Corsair recorded Q1 2025 revenue of USD 369.75 million, up from USD 337.26 million a year earlier, driven by strong headset pull-through linked to an expanded Fanatec racing ecosystem.

Logitech positions G-series headsets around software-driven audio personalisation, giving it leverage to upsell creators who need voice filters for Arabic dialects. Sony’s INZONE line differentiates via 360 Spatial Sound, attracting PS5 owners in Saudi Arabia who prize first-party ecosystem integration. Razer underscores thermal durability, releasing ear-cups rated to 50 °C that meet Gulf climate norms.

Strategic moves centre on regional assembly, tariff-free warehousing, and female-gamer outreach. Turtle Beach signed a memorandum with Dubai Silicon Oasis to evaluate screwdriver assembly that would bypass import duties, while Corsair co-sponsors the Riyadh Creator League to tap influencer-led conversions. Logitech bundles Blue-branded microphones with mid-tier headsets, targeting the fast-growing streamer demographic that pushes the GCC gaming headset market toward premium price bands.

GCC Gaming Headsets Industry Leaders

Razer Inc.

SteelSeries

Corsair Gaming, Inc.

Logitech International S.A.

Cooler Master Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Corsair Gaming reported Q1 2025 revenue of USD 369.75 million, up from USD 337.26 million in Q1 2024, crediting headset demand for its peripherals segment growth.

- March 2025: True Gamers detailed a USD 280 million Esports Island in Abu Dhabi featuring training venues equipped with tournament-grade headsets.

- February 2025: DTS renewed collaboration with Logitech G to embed DTS Headphone:X across upcoming wireless lines, bringing spatial audio to mid-priced GCC SKUs.

- January 2025: Saudi Arabia confirmed the gaming sector’s target GDP contribution of USD 13 billion by 2030, reinforcing public procurement of esports peripherals.

GCC Gaming Headsets Market Report Scope

Gaming headsets, specialized headphones tailored for video games, feature superior sound quality built-in microphones for in-game communication and often include extras like surround sound, noise cancellation, and wireless connectivity. They enhance the gaming immersion, providing clear audio and facilitating smooth communication, especially in multiplayer and competitive gaming scenarios.

The GCC gaming headsets market is segmented by compatibility type (console headset and PC headset), by connectivity type (wired and wireless), by sales channel (retail and online), and by country (Saudi Arabia, UAE, Qatar, and other GCC countries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Console Headset |

| PC Headset |

| Mobile/VR Headset |

| Wired |

| Wireless |

| Retail |

| Online |

| Casual Gamers |

| Professional / E-sports Gamers |

| Streamers and Content Creators |

| Stereo |

| Virtual Surround 7.1 |

| Spatial / 3D Audio |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Rest of GCC |

| By Compatibility Type | Console Headset |

| PC Headset | |

| Mobile/VR Headset | |

| By Connectivity | Wired |

| Wireless | |

| By Sales Channel | Retail |

| Online | |

| By Gamer Type | Casual Gamers |

| Professional / E-sports Gamers | |

| Streamers and Content Creators | |

| By Audio Technology | Stereo |

| Virtual Surround 7.1 | |

| Spatial / 3D Audio | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Rest of GCC |

Key Questions Answered in the Report

How large is the GCC gaming headset market in 2026?

The market stands at USD 174.68 million in 2026 and is projected to hit USD 287.06 million by 2031 at a 10.44% CAGR.

Which compatibility type leads sales?

Console headsets hold the lead with 46.45% market share in 2025, although mobile and VR headsets are expanding fastest at an 17.47% CAGR.

Are wired or wireless headsets more popular in the Gulf?

Wired units still dominate with 56.85% share due to tournament rules, but wireless shipments are growing 13.78% annually as latency falls and battery life improves.

What role does government spending play?

Saudi Arabia’s USD 38 billion gaming initiative and similar UAE programs finance esports venues and training centres, directly stimulating institutional headset purchases.

How big is the opportunity in online sales?

Online channels currently represent 35.95% of sales but are advancing at a 12.74% CAGR thanks to same-day delivery services and Arabic-language customer support.

Which technology segment is growing fastest?

Spatial and 3D audio headsets are rising at a 19.40% CAGR as localized multiplayer games demand positional accuracy and immersive soundscapes

Page last updated on: