Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Middle East and Africa Gaming Headsets Market Report is Segmented by Compatibility Type (Console, PC, Multi-Platform/Mobile/VR), Connectivity (Wired, Wireless), Sales Channel (Offline Retail, Online), Form Factor (Over-Ear, On-Ear, In-Ear), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, South Africa, Egypt, Nigeria, Rest of MEA). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

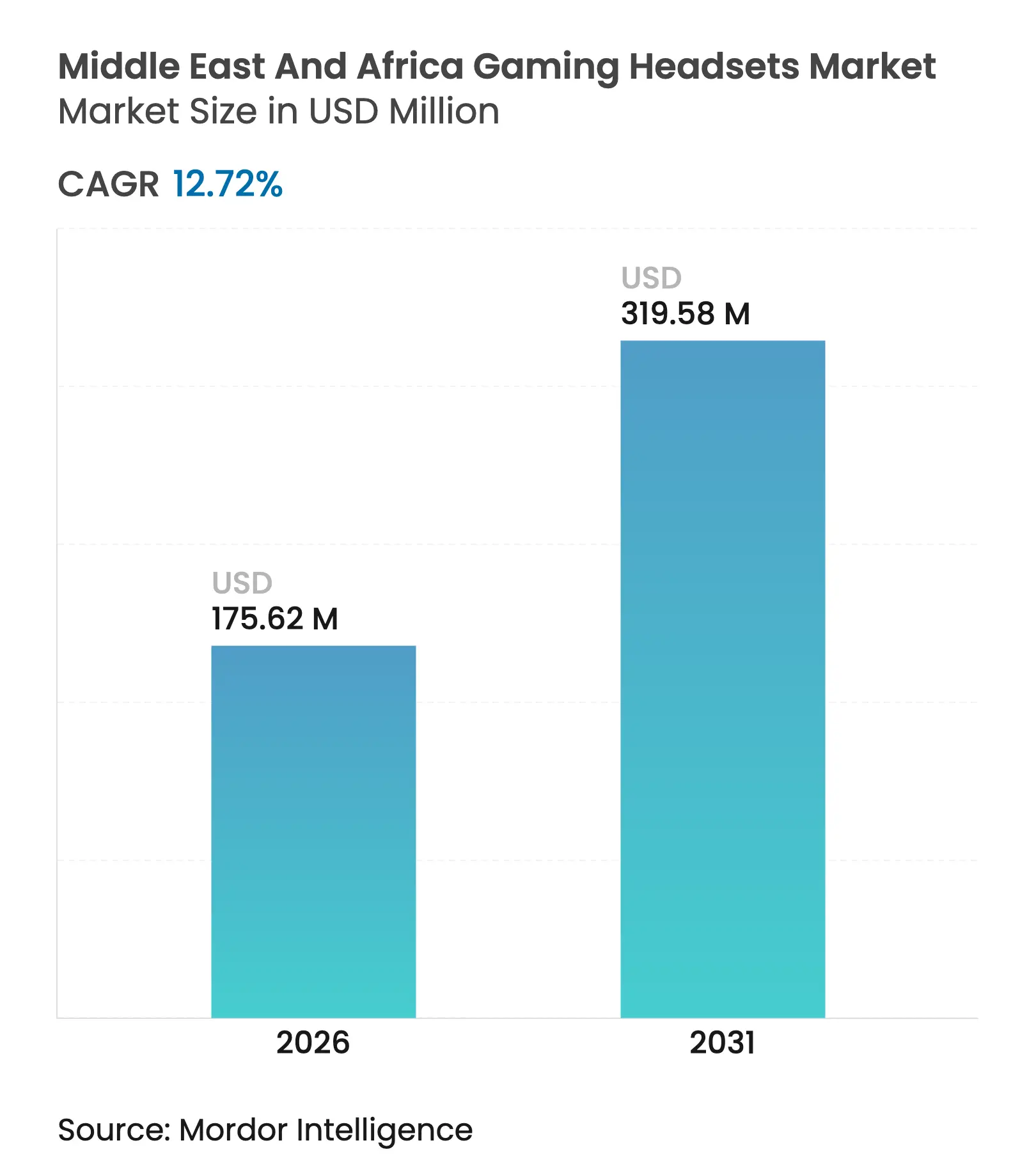

| Market Size (2026) | USD 175.62 Million |

| Market Size (2031) | USD 319.58 Million |

| Growth Rate (2026 - 2031) | 12.72 % CAGR |

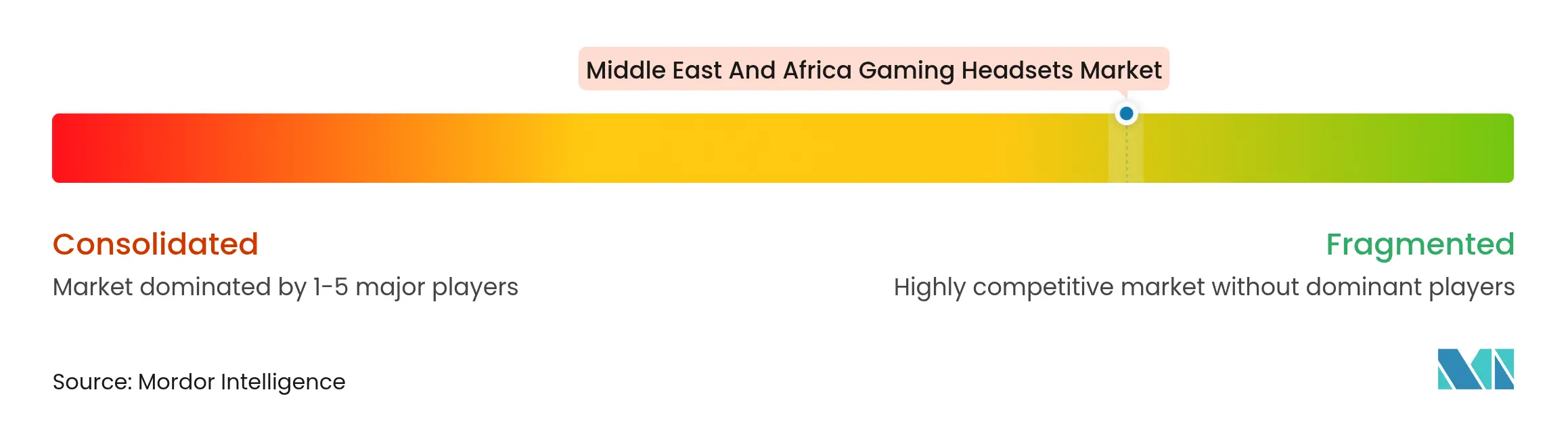

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Middle East and Africa gaming headsets market size in 2026 is estimated at USD 175.62 million, growing from 2025 value of USD 155.80 million with 2031 projections showing USD 319.58 million, growing at 12.72% CAGR over 2026-2031. Enhanced fiber-optic coverage, 5G roll-outs, and state-sponsored esports investments are broadening broadband access and stimulating high-performance audio demand. Console ecosystem strength, particularly around PlayStation 5, continues to anchor premium headset spending, while mobile-first gamers accelerate multi-platform headset uptake. Hybrid wireless advances are compressing latency gaps between wired and wireless devices, encouraging technology upgrades across all price bands. E-commerce penetration is reshaping retail dynamics by giving consumers wider model choice and transparent pricing. On the supply side, easing chip shortages and new AI-driven acoustics platforms are enabling quicker model refresh cycles and differentiated audio features.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising

internet penetration and affordable fiber roll-outs Rising

internet penetration and affordable fiber roll-outs | +2.8% | Saudi Arabia, UAE, South Africa | Medium term (2-4 years) |

(~)

% Impact on CAGR Forecast

:

+2.8%

|

Geographic

Relevance

:

Saudi

Arabia, UAE, South Africa

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Government-funded

e-sports arenas (Gamers8, etc.)

Government-funded

e-sports arenas (Gamers8, etc.)

| +2.1% | Saudi Arabia, UAE, Qatar | Short term (≤2 years) | |||

“Tempest-class”

3D-audio requirements of Gen-9 consoles

“Tempest-class”

3D-audio requirements of Gen-9 consoles

| +1.9% | Saudi Arabia, UAE | Medium term (2-4 years) | |||

Growth

of female-gamer headset spend

Growth

of female-gamer headset spend

| +1.4% | Nigeria, South Africa | Long term (≥4 years) | |||

Arabic

voice-chat moderation AI

Arabic

voice-chat moderation AI

| +0.8% | GCC markets | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Internet Penetration and Affordable Fiber Rollouts

Rapid fiber build-outs have lifted urban broadband penetration beyond 85% in Saudi Arabia and near universal coverage in the UAE, cutting latency and supporting cloud gaming sessions that reward premium headsets.[1]Panasonic Marketing Middle East & Africa, “Panasonic Announces FY24 Business Strategy For Sustained Growth in Middle East and Africa,” panasonic.com Nigerian cities report latency drops of 40%, translating into higher competitive play participation and headset upgrades. South Africa and Egypt combine 5G with fiber backhaul, pushing demand for multi-platform wireless models. These infrastructure improvements extend battery life by off-loading processing to the cloud and justify premium price points as gamers perceive tangible audio advantages.

Government-Funded E-Sports Arenas

Saudi Arabia’s USD 45 million rollout of 150 esports centers sets professional audio baselines that cascade into consumer expectations.[2]Arab News, “Video game industry helping to reshape Saudi economy, experts say,” arabnews.com Bulk procurement lowers OEM costs, encouraging wider retail availability of certified headsets. Dubai’s X-Stadium and Qatar’s federation-backed facilities echo this trend, stimulating demand for headsets with tournament-grade microphones and spatial-audio compliance. As amateur gamers replicate arena standards at home, average selling prices for console and PC headsets trend upward, boosting revenue per unit.

“Tempest-Class” 3D-Audio Requirements of Gen-9 Consoles

Sony’s Tempest 3D AudioTech processes hundreds of simultaneous sound sources, forcing users to replace legacy stereo gear with compliant headsets capable of elevated frequency response.[3]Headliner Hub, “Sony's PS5 To Launch With Tempest 3D Audio,” headlinerhub.com Patent filings around ambisonic soundfields and personalized HRTF push manufacturers toward AI-assisted driver tuning. Competitive offerings from Microsoft and Meta intensify a technology cycle that underpins premium segment growth and accelerates platform convergence across console, PC, and XR devices.

Growth of Female-Gamer Headset Spend

Female gamers increasingly demand lightweight, aesthetically appealing headsets with enhanced microphones for streaming and social play, creating a new addressable segment in Nigeria and South Africa. Manufacturers respond with color-variant SKUs, narrower headbands, and plush ear-cushion options. Multi-platform compatibility is critical, reflecting gaming patterns that span mobile, console, and PC. The segment’s sustained double-digit expansion supports product-line extensions and targeted marketing campaigns.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Grey-market

inflow and parallel imports Grey-market

inflow and parallel imports | -1.7% | Nigeria, Egypt, South Africa | Short term (≤2 years) |

(~)

% Impact on CAGR Forecast

:

-1.7%

|

Geographic

Relevance

:

Nigeria,

Egypt, South Africa

|

Impact

Timeline

:

Short

term (≤2 years)

|

Cyber-fraud

and payment-regulation frictions Cyber-fraud

and payment-regulation frictions | -1.2% | Pan-African markets | Medium term (2-4 years) | |||

Shortage

of service/repair centres

Shortage

of service/repair centres

| -0.9% | Rural and secondary urban centers across MEA | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Grey-Market Inflow and Parallel Imports

Unauthorized channels price headsets 20-30% below official listings, eroding brand equity and warranty confidence. Customs loopholes and tariff disparities create arbitrage that weakens authorized dealers, especially in Nigeria and South Africa.[4]World Bank, “Middle East & North Africa Trade Summary 2022,” wits.worldbank.org While Section 337 actions offer legal remedies, practical enforcement remains limited, dampening official volume growth in the near term.

Cyber-Fraud and Payment-Regulation Frictions

Fragmented cross-border payment rules and high fraud risk curb big-ticket e-commerce purchases. Although the UAE’s new gaming regulator signals progress, many African shoppers still favor cash-on-delivery or local kiosks, restricting online headset assortment and slowing digital channel penetration.

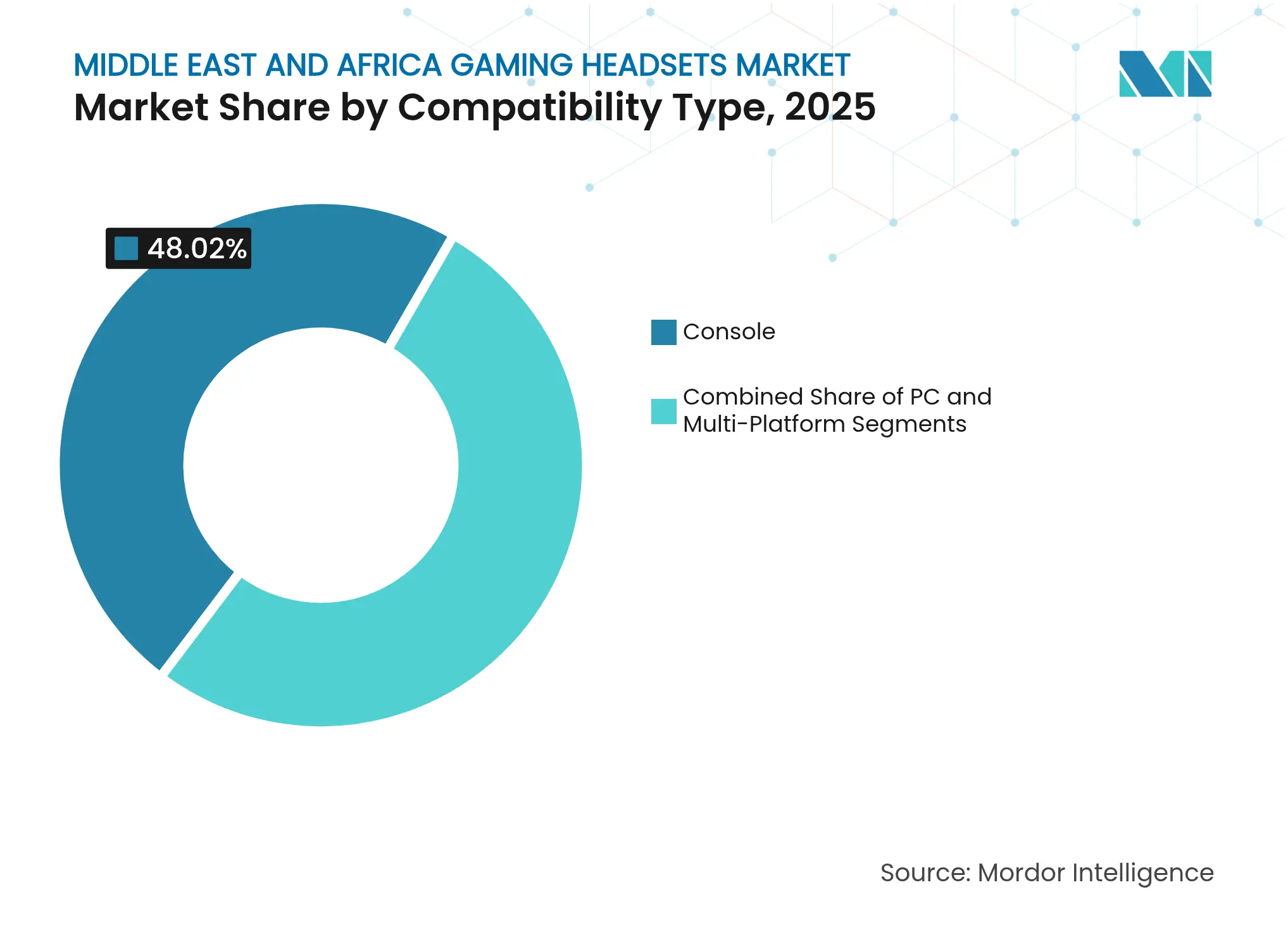

By Compatibility Type: Console Dominance Drives Premium Adoption

Console models secured a 48.02% share of the Middle East and Africa gaming headsets market in 2025, reflecting deep PlayStation and Xbox penetration. Multi-platform headsets, however, are rising fastest at a 14.05% CAGR as gamers juggle mobile, console, and PC play styles. In GCC countries, premium console headsets priced above USD 150 gain traction, while budgets under USD 60 prevail in sub-Saharan Africa. Cross-platform designs eliminate device-specific purchases, expanding addressable spend and lifting average selling price.

Second-generation mobile gamers are graduating to console esports, supporting a steady replacement cycle. VR is nascent but signals future demand, with Meta’s spatial-audio patents hinting at ecosystem convergence. Manufacturers embedding USB-C, Bluetooth LE-Audio, and 2.4 GHz dongles in one SKU capture the broadest use cases, mitigating platform risk and sustaining brand loyalty.

Note: Segment shares of all individual segments available upon report purchase

By Connectivity: Wired Reliability Meets Wireless Innovation

Wired units held 53.22% of the Middle East and Africa gaming headsets market share in 2025, favored for esports latency performance. Hybrid dual-radio devices, however, clock an 18.30% CAGR as Bluetooth LE-Audio narrows delay to near-wired levels. USB digital links dominate tournament play, while 3.5 mm analog jacks retreat. AI-based channel-hopping and wideband noise control widen the wireless addressable base, encouraging PC and console players to adopt untethered designs.

Open-ear ANC technology unveiled by NTT Corporation demonstrates that comfort and situational awareness need not compromise immersion. Battery density gains and USB-C fast-charging minimize downtime, underscoring wireless practicality for everyday gaming and live streaming. As chip supply improves, average wireless ASPs drift lower, fostering price-tier migration from analog wired sets.

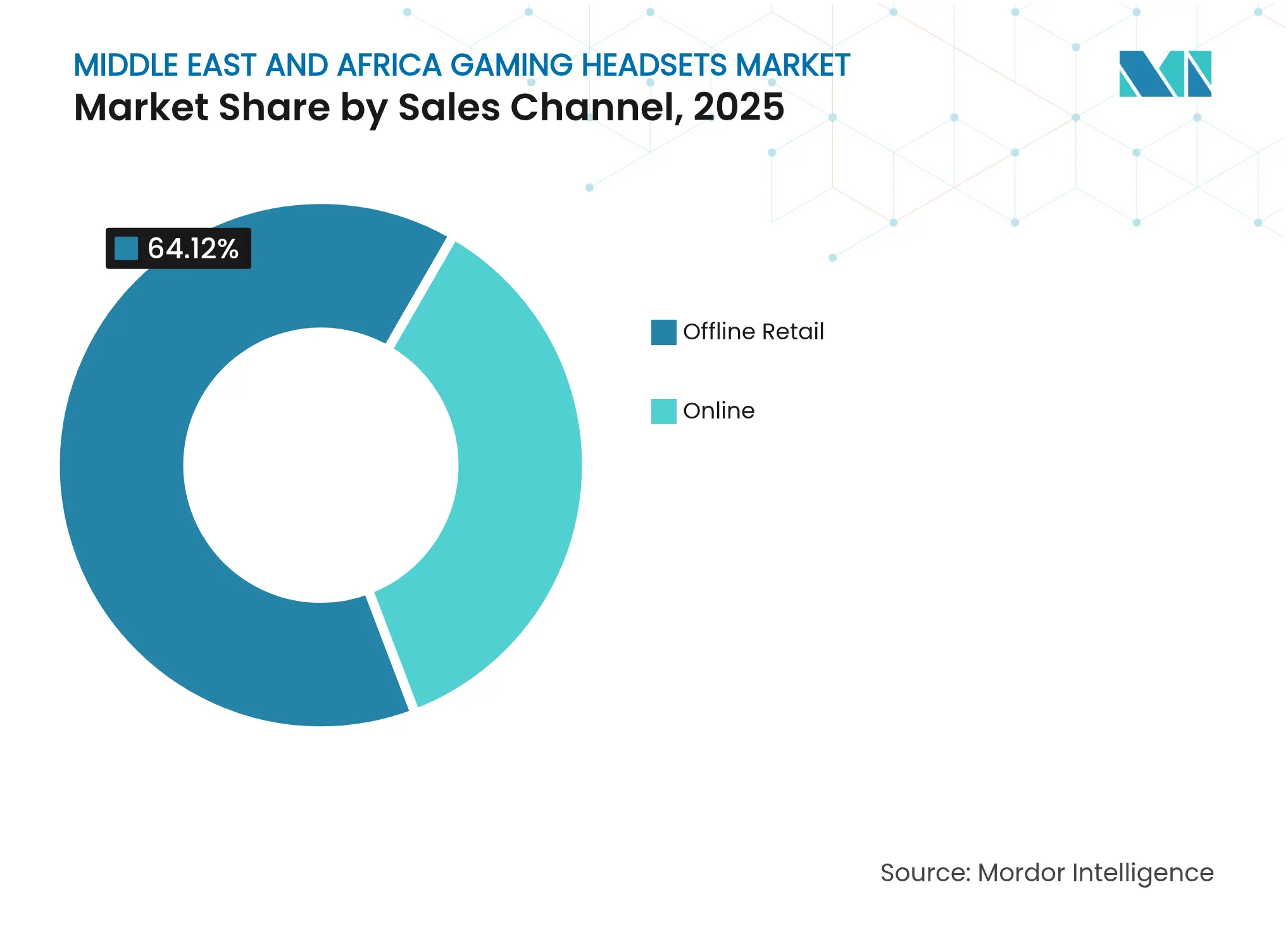

By Sales Channel: Digital Transformation Reshapes Distribution

Offline retail captured 64.12% revenue in 2025 due to experiential selling and immediate product availability. Electronics specialists and hypermarkets exploit display demos that let consumers test microphone pickup and ear-cup comfort. Toy chains increasingly stock entry-level gaming headsets as gaming crosses into family entertainment.

Online platforms, though smaller, are forecast to outpace all channels at a 21.20% CAGR. Broader assortment, rapid price discovery, and influencer-led marketing drive digital traffic, particularly among Gen Z shoppers. Brand webstores enable direct firmware updates and loyalty programs, enhancing lifecycle value. Payment gateways integrating local wallets and fraud screening are shrinking cart abandonment, nudging higher ASP units through virtual try-ons and AR fit guides.

Note: Segment shares of all individual segments available upon report purchase

By Form Factor: Comfort Evolution Drives Innovation

Over-ear designs dominated 62.54% of the Middle East and Africa gaming headsets market size in 2025, prized for spatial-audio and passive isolation. Closed-back versions excel in competitive settings that call for noise suppression, while open-back models court audiophiles who favor natural soundstage. Memory-foam cushions and lightweight metals extend comfortable wear beyond three-hour sessions.

In-ear gaming earbuds are on a 19.60% CAGR trajectory, propelled by smartphone esports leagues and streaming culture. Latency-reduced Bluetooth profiles and miniaturized drivers bring console-grade acoustics to pocket-sized devices. Biosignal-sensing patents hint at adaptive EQ that tunes output to user fatigue, promising future product differentiation. On-ear models, although niche, carve a following among commuters needing compact yet immersive audio.

Saudi Arabia claimed 26.63% of 2025 revenue, buoyed by Vision 2030 and a USD 37.7 billion gaming investment plan through Savvy Games Group. The Kingdom’s 150 esports centers institutionalize audio standards that ripple into home-use purchasing. Disposable income and a tech-savvy youth skew sales toward premium wireless headsets with surround capability.

The UAE leverages Dubai’s X-Stadium and a newly formed gaming regulator to attract global publishers, reinforcing demand for headsets that meet international tournament specifications. Qatar’s event-driven economy and esports federation certifications foster a quality-conscious consumer base. Kuwait’s youthful demographics translate into sustained hardware refresh cycles, while Bahrain benefits from regional cross-border retail flows.

Nigeria exhibits the fastest 15.05% CAGR, fuelled by an expanding gaming population shifting from mobile to console/PC ecosystems. Improved submarine cable landings and 5G pilots slash latency, encouraging headset upgrades. Despite grey-market interference, localized e-commerce platforms are scaling refurbished and entry-level offerings, broadening accessibility.

South Africa remains Africa’s gaming capital with 24 million gamers and mature retail logistics. Strong telecom backbone supports cloud gaming, driving demand for low-latency wireless headsets. Egypt’s large youth cohort underpins volume potential, though currency swings constrain premium imports. Across Africa, a rise from 77 million to 186 million gamers between 2015 and 2021 illustrates headroom for headset penetration.

Arabic language preference shapes hardware specs: 41% of GCC gamers want localized games, and 74% value Arabic representation. OEMs integrating beamforming mics tuned for Arabic phonetics and on-device NLP stand to capture loyalty. As localization evolves into an expected baseline, headset firms are differentiating through cultural motifs and voice-assistant integration that recognize regional dialects.

Market Concentration

Global incumbents anchor the Middle East and Africa gaming headsets market through R&D scale and multi-platform partnerships. Sony, Logitech, and Turtle Beach continuously refresh line-ups with AI-driven noise suppression, 3D audio engines, and console-certified wireless protocols. Sony’s gaming segment posted a 37% profit rise on PlayStation 5 momentum, underlining tight hardware-software coupling. Logitech delivered 18% gaming sales growth by releasing 11 new peripherals and streamlining gamer-centric SKUs.

Component suppliers signal recovery: TSMC’s 17% revenue uptick suggests easing chip shortages that have constrained headset output. GN Store Nord’s SteelSeries recorded 7% organic growth, aided by continued brand investment. Corsair expanded into sim racing gear and AI-enhanced tuning, leveraging cross-category synergies.

White-space entrants concentrate on female-focused styling, Arabic language optimization, and direct-to-consumer logistics. Patents on contextual audio and health sensing offer differentiation pathways before becoming table stakes. Regional distributors use price localization and installment plans to fend off grey-market competition, while gaming cafés serve as influential demo venues for premium surround models.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Gaming headsets, specialized headphones tailored for video games, feature superior sound quality built-in microphones for in-game communication and often include extras like surround sound, noise cancellation, and wireless connectivity. They enhance the gaming immersion, providing clear audio and facilitating smooth communication, especially in multiplayer and competitive gaming scenarios.

The Middle East and African gaming headsets market is segmented by compatibility type (console headset and PC headset), by connectivity type (wired and wireless), by sales channel (retail and online), by country (Saudi Arabia, UAE, Qatar, Kuwait, South Africa, Egypt, Nigeria, and rest of MEA). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.