China Gaming Headsets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

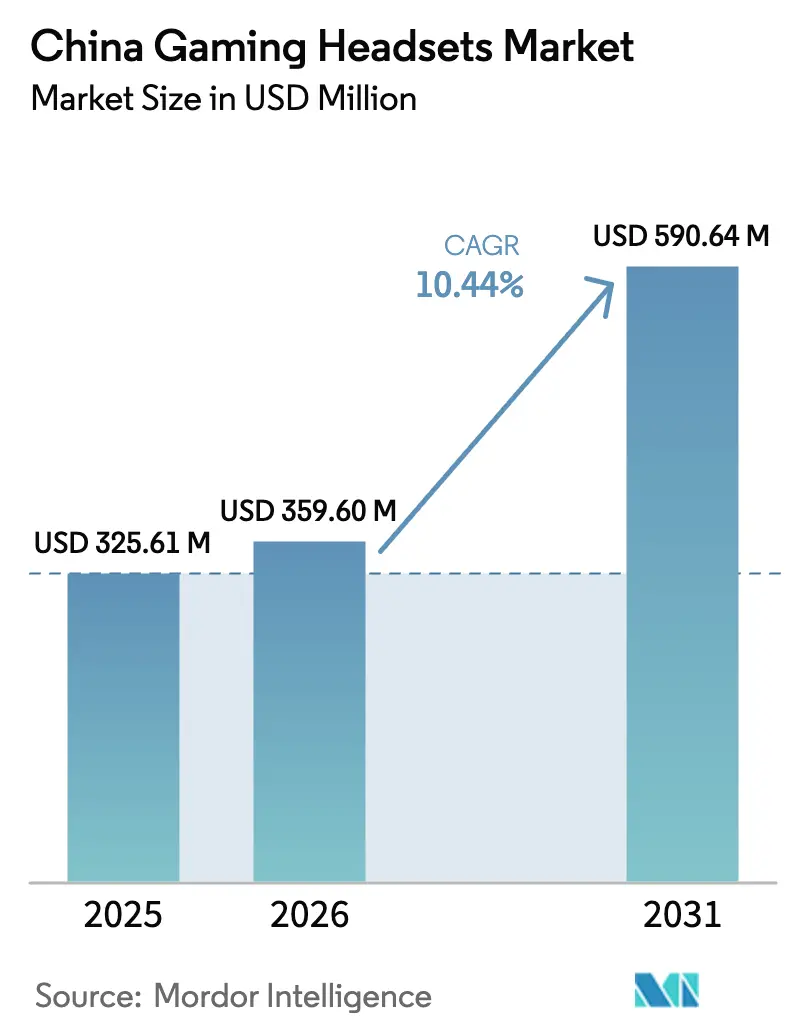

| Base Year Market Size (2025) | USD 325.61 Million |

| Market Size (2026) | USD 359.6 Million |

| Market Size (2031) | USD 590.64 Million |

| Growth Rate (2026 - 2031) | 10.44% CAGR |

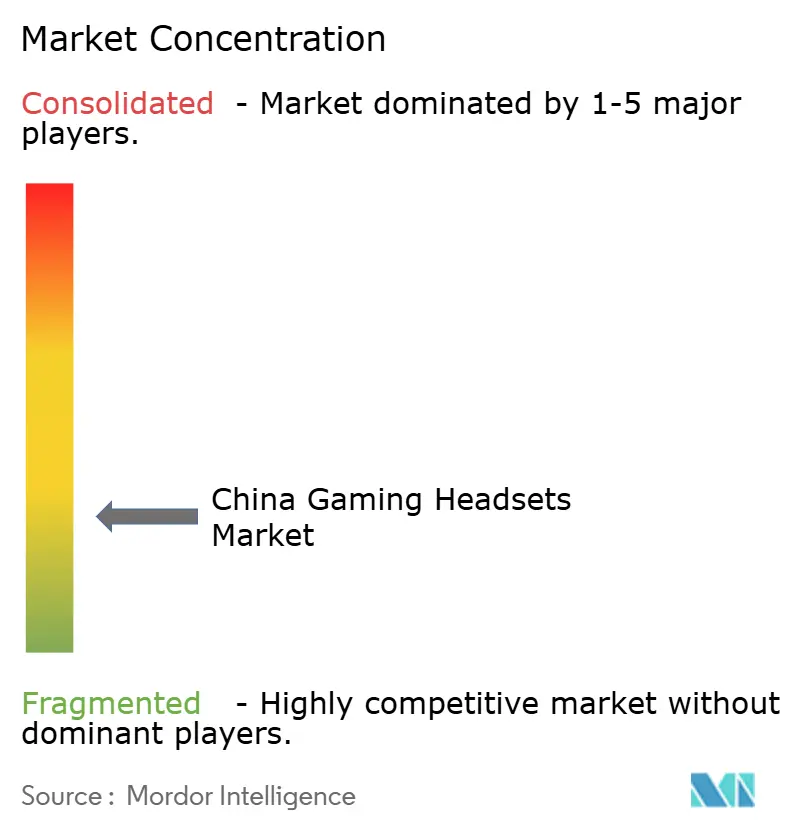

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Gaming Headsets Market Analysis by Mordor Intelligence

China Gaming Headsets Market size in 2026 is estimated at USD 359.6 million, growing from 2025 value of USD 325.61 million with 2031 projections showing USD 590.64 million, growing at 10.44% CAGR over 2026-2031. Government subsidies for digital products and large‐scale semiconductor investments nourish a self-sustaining hardware ecosystem, while the world’s largest gamer base generates consistent peripheral demand. Rapid adoption of virtual-reality (VR) titles, the professionalisation of esports, and influencer-driven livestream commerce collectively widen the addressable customer pool. Manufacturers respond with AI-enabled noise suppression, low-latency wireless chipsets, and platform-agnostic designs that encourage multi-device use. Supply-chain volatility linked to chip shortages and intensifying online price competition remain near-term hurdles, yet policy incentives for domestic audio-IC fabrication continuously ease hardware constraints.[1]中国政府网, “实施手机等数码产品购新补贴、增加发行超长期特别国债……国家发改委最新发布!,” gov.cn

Key Report Takeaways

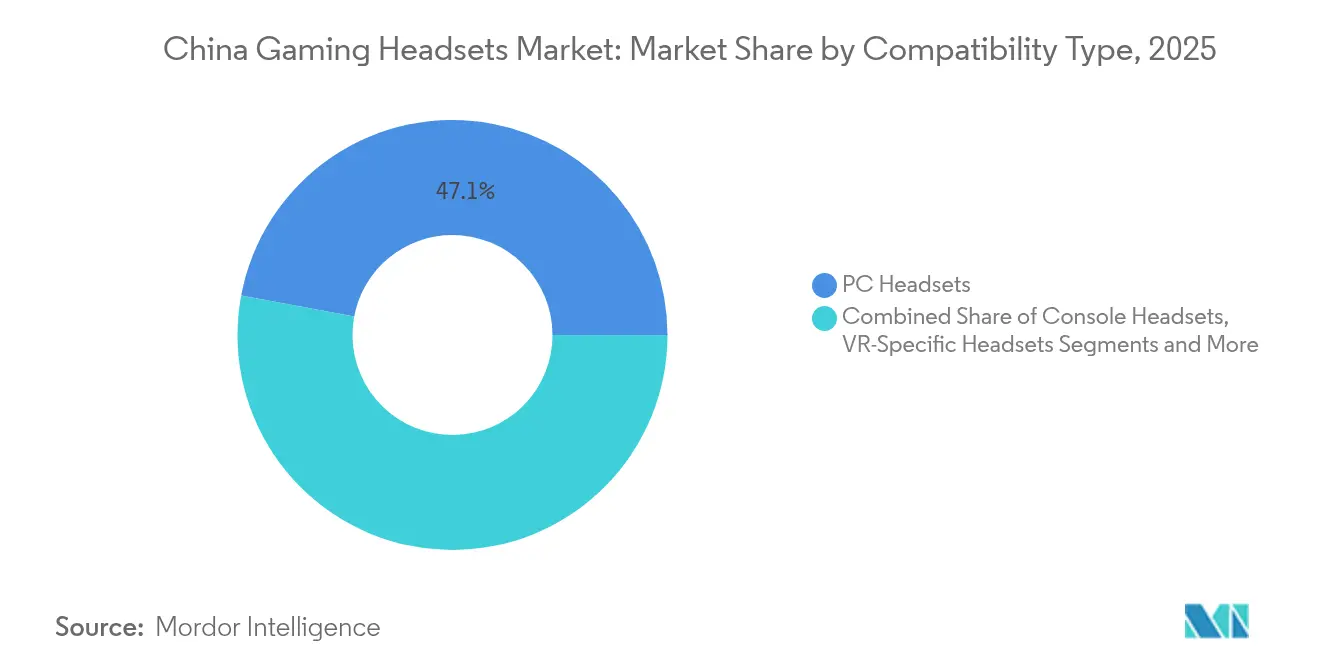

- By compatibility type, PC headsets led with 47.05% of gaming headsets market share in 2025, whereas VR-specific headsets are set to expand at a 18.53% CAGR through 2031.

- By connectivity type, wired solutions retained 63.15% revenue share in 2025; wireless products are on track for a 17.28% CAGR over 2026-2031.

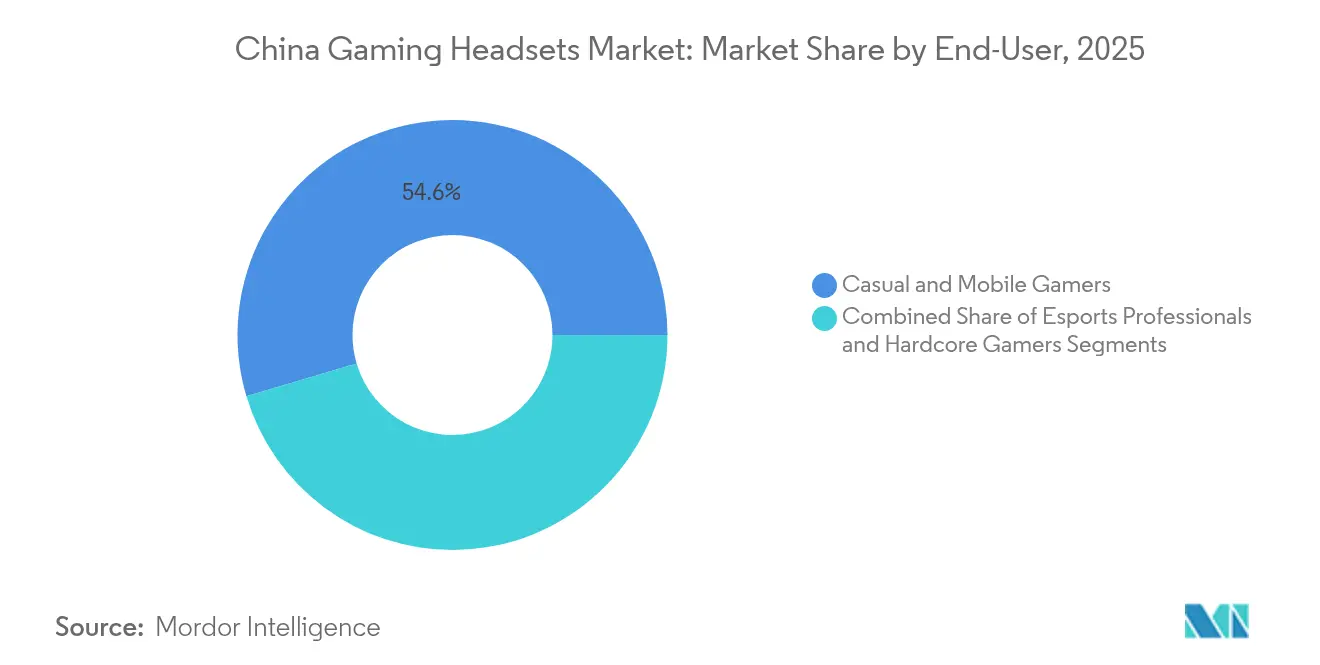

- By end-user, casual and mobile gamers accounted for 54.60% of the gaming headsets market size in 2025, while esports professionals will record the highest 15.85% CAGR to 2031.

- By sales channel, online marketplaces and brand websites captured 68.45% share of the gaming headsets market in 2025 and should advance at a 13.39% CAGR through 2031.

- By geography, East China commanded 31.05% revenue share in 2025, yet Central and West China will register the fastest 13.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with China representing one among them. The global report on gaming headsets market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

China Gaming Headsets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Esports boom elevates demand for tournament-grade audio | +2.1% | National, concentrated in East and South China | Medium term (2-4 years) |

| Rapid adoption of VR titles among urban gamers | +1.8% | East China, South China, major urban centers | Medium term (2-4 years) |

| Rising disposable income of Gen-Z & Gen-Alpha cohorts | +1.5% | National, strongest in East and South China | Long term (≥ 4 years) |

| Expansion of livestream commerce driving influencer-led upgrades | +1.3% | National, led by East China e-commerce hubs | Short term (≤ 2 years) |

| Government incentives for domestic audio-IC fabrication | +0.9% | National, focused on semiconductor manufacturing regions | Long term (≥ 4 years) |

| AI-enabled noise-suppression chips tailored to Chinese social apps | +0.7% | National, with early adoption in tech-forward cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Esports Boom Elevates Demand for Tournament-Grade Audio

Professional tournaments push audio precision to the foreground as match integrity depends on directional sound cues and flawless voice chat. The USD 1 million Counter-Strike 2 championship in Hong Kong, endorsed under the local “M-mark” sporting scheme, exemplifies institutional backing that legitimises esports as mainstream entertainment.[2]Ecns.cn, “Hong Kong to host the world's top Counter-Strike 2 teams at major esports gala,” ecns.cn Organisers stipulate certified headsets, which quickly influence amateur purchase behaviour and raise the technical baseline for retail products. Esports venues expanding in Shanghai, Shenzhen, and Chengdu amplify regional demand, while prize pools, sponsorship deals, and media rights reinforce a virtuous cycle that benefits premium peripheral suppliers. Component vendors consequently prioritise low-latency drivers, broadcast-quality microphones, and passive noise isolation for tournament compliance. Brands with official league partnerships secure repeat visibility, helping them out-perform general consumer electronics competitors within the gaming headsets market.

Rapid Adoption of VR Titles Among Urban Gamers

Government rebates of up to CNY 2,000 per headset have lowered entry barriers for immersive content, igniting renewed hardware interest despite a shipment dip in 2024. Industry trackers expect China’s AR/VR unit volumes to rebound 114.7% in 2025 as new all-in-one devices, AI-enhanced optics, and lighter form factors reach retail shelves.[3]映维网资讯, “XR日报:Quest Store营收20亿美元,国补PICO 4 Ultra降价千元,” news.nweon.com Spatial audio that matches head-tracked visuals is critical for presence, prompting headset makers to adopt high-resolution drivers and advanced head-related transfer function (HRTF) algorithms. Urban early adopters living in Beijing, Shanghai, and Guangzhou influence purchasing behaviour across lower-tier cities through social media content, creating trickle-down upgrade cycles. Accessory bundles, instalment financing, and premium limited editions further accelerate VR-specific revenue streams inside the gaming headsets market.

Rising Disposable Income of Gen-Z & Gen-Alpha Cohorts

Young gamers are earning earlier through creator economies and part-time e-sports engagement. NetEase recorded CNY 24 billion in Q1 2025 game revenue, up 12.1% year over year, underscoring the willingness of younger cohorts to spend on entertainment ecosystems that include peripherals.[4]NetEase, “NetEase Announces First Quarter 2025 Unaudited Financial Results,” ir.netease.com These consumers treat headsets as fashion accessories and status symbols, demanding RGB lighting, interchangeable ear-cup plates, and minimalist industrial design. Social validation on platforms such as Bilibili and Xiaohongshu positions premium SKUs as identity markers, making brand storytelling as important as technical specifications. Subscription-based software features, such as AI voice modulation and background soundscapes, open recurring revenue opportunities beyond the initial hardware sale.

Expansion of Livestream Commerce Driving Influencer-Led Upgrades

Livestream shopping links entertainment to transaction in one interface, shrinking the decision window from consideration to purchase. HUYA’s game-related services revenue rose 52.1% year over year in Q1 2025, signalling consumers’ growing comfort with buying peripherals during broadcast content. Influencers demonstrate microphone pick-up patterns, comfort over multi-hour streams, and noise isolation in real-time, effectively substituting for in-store trials. Flash discounts, limited-run colours, and bundled game codes create urgency. While smaller brands gain initial traction through aggressive price-cutting, sustained share growth requires differentiated acoustics and reliable after-sales service, steering viewers toward reputable vendors and tightening loyalty within the gaming headsets market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor supply-chain volatility | -1.4% | National, affecting all manufacturing regions | Short term (≤2 years) |

| Intensifying price wars compressing vendor margins | -1.1% | National, most severe in online channels | Short term (≤2 years) |

| Stringent CCC/GB compliance delaying product launches | -0.8% | National, regulatory compliance requirement | Medium term (2-4 years) |

| Shift toward lightweight gaming earbuds cannibalising over-ear demand | -0.6% | National, led by mobile gaming growth | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-Chain Volatility

Audio processing chips and wireless modules share fabrication lines with smartphones and automotive components, increasing competition for limited foundry space. Although Beijing committed CNY 344 billion to boost domestic chip output, near-term bottlenecks persist because mature-node capacity remains scarce for mixed-signal audio ICs. Factory shutdowns in key provinces and logistics disruptions extend lead times, forcing brands to carry higher inventory or redesign around alternative components. Some headset makers move to multi-sourcing but still face cost spikes that squeeze promotional budgets during high-sales events such as 11.11 and 6.18. Production delays ripple through the gaming headsets market, risking stock-outs of flagship models and pushing consumers toward substitute products.

Intensifying Price Wars Compressing Vendor Margins

Domestic upstarts reverse-engineer established acoustics, undermining premiums once justified by proprietary tuning. SteelSeries reported 7% organic gear growth in 2024 yet acknowledged mounting pressure on gross margins because price-match algorithms in e-commerce marketplaces react within hours to promotional changes. Brands increasingly bundle headsets with software licences or extended warranties to preserve revenue per user, but discount fatigue remains visible in Tier-2 city outlets. High churn among low-price entrants clouds brand equity across the category, nudging consumers to delay purchase until headline sales events or influencer coupons emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compatibility Type: VR Drives Next-Generation Audio Innovation

PC headsets contributed 47.05% of overall revenue in 2025, securing the largest gaming headsets market share due to entrenched esports ecosystems in internet cafés and home setups. Even so, VR-specific models will post a 18.53% CAGR through 2031, the highest within the compatibility spectrum, powered by subsidies that shave up to CNY 2,000 off eligible devices. Console headsets hold steady demand around major title releases, while mobile gaming headsets ride the region’s 70-million-plus cloud-gaming user base.

PC headsets keep leadership through modular upgrades such as swappable cables, dedicated DACs, and software equalisation suites. Yet cross-platform headsets that auto-detect console, PC, and mobile inputs dilute single-platform dominance, pooling R&D budgets and shortening payback periods. VR-oriented models emphasise weight distribution and 3D spatial audio, leveraging Sony-filed patents that improve HRTF rendering for frontal imaging accuracy. Component suppliers must address higher impedance drivers and low-profile battery packs, re-shaping supply-chain needs inside the gaming headsets market.

By Connectivity Type: Wireless Technology Accelerates Despite Wired Dominance

Wired designs generated 63.15% of 2025 revenue and remain the default for tournament hosts that prohibit wireless to avoid frequency congestion. Nevertheless, wireless units will advance at a 17.28% CAGR from 2026 as 2.4 GHz adaptive radios and Bluetooth LE-Audio reduce latency to sub-20 ms levels. Efficiency gains from 6 nm audio SoCs developed by Hengxuan, Zhongke Lanyun, and Juchip extend battery life beyond 40 hours between charges.

Hybrid headsets that switch between wired and wireless modes build resilience against venue interference while appealing to everyday convenience. Magnetic charging cradles, quick-swap batteries, and wireless dongles with console compatibility further erode resistance to premium price points. Conversely, wired models protect market share by offering broadcast-quality inline DACs at aggressive entry prices, ensuring their relevance among budget-focused gamers within the gaming headsets market.

By End-User: Esports Professionals Drive Premium Segment Expansion

Casual and mobile gamers represented 54.60% of 2025 demand, yet esports professionals will clock a 15.85% CAGR as national leagues proliferate and collegiate circuits formalise talent pipelines. Professional-grade headsets integrate isolated voice channels, memory-foam clamping, and league-approved branding. The gaming headsets market size for esports professionals is projected to reach USD 89.1 million by 2031, equating to roughly 15.08% of the total pool.

Influence extends beyond direct purchases, as amateur spectators mimic pro setups, triggering “listener envy” that nudges volume growth across mid-range SKUs. Tier-1 broadcasters now annotate matches with on-screen headset specifications, giving brands free advertising that cements mindshare. Patents filed by Meta reveal contextual-awareness subsystems that adjust equaliser curves when background noise exceeds threshold, an innovation first aimed at professional LAN environments but later cascaded into mainstream firmware updates.

By Sales Channel: Online Dominance Reflects E-Commerce Maturity

Digital storefronts and brand.com platforms generated 68.45% of 2025 sales, a lead reinforced by same-day fulfilment, AI customer service, and algorithmic personalisation. Livestream integration lets influencers pin product links during matches or unboxing sessions, compressing the purchase funnel to seconds. Offline specialty chains still command premium buyers who insist on fit-testing, especially for heavier surround-sound models.

The gaming headsets market size attributed to online channels is forecast to reach USD 439.2 million by 2031, delivering the bulk of incremental gains. Omnichannel strategies now let customers reserve units online and collect at partnered convenience stores, bridging trust gaps among new buyers in smaller cities. Retailers respond by expanding experience zones that showcase microphone pickup and ANC demos, justifying price differentials against pure-play online discounters.

Geography Analysis

East China delivered 31.05% of national revenue in 2025, reflecting Shanghai’s dense esports venue cluster and Hangzhou’s live-streaming production studios. Supply-chain vertical integration around the Yangtze River Delta speeds prototype iterations, letting brands compress launch cycles. High disposable incomes support multi-headset ownership, with separate units for work, console, and VR gameplay, lifting average selling prices across the gaming headsets market.

Central and West China, though historically under-penetrated, will register a 13.12% CAGR to 2031, outperforming other regions. Government-led “Digital Silk Road” investments are extending 5 G base stations and cloud gaming nodes to Chengdu, Chongqing, and Xi’an. As internet cafés upgrade to esports lounges, headset bulk orders flow to regional distributors, diversifying demand away from coastal provinces. The gaming headsets market size for Central and West China is expected to cross USD 117.4 million by 2031.

South China benefits from Shenzhen’s manufacturing corridor, which hosts ODM factories supplying global and domestic brands alike. Local component proximity shortens feedback loops between design and volume production, underpinning competitive pricing strategies. North and Northeast China maintain steady, albeit slower, growth anchored by university esports leagues in Harbin and Shenyang. Cold winters extend indoor gaming sessions, slightly lifting replacement cycles for over-ear units that double as general-purpose headphones.

Regional cultural nuances shape marketing tactics. East China campaigns stress creator studios and RGB aesthetics, whereas West China emphasises durability on dusty LAN floors. Retailers in North China run trade-in programmes timed around university enrolment seasons, capturing students upgrading from entry-level earbuds to full headset setups. Collectively, geographic diversification cushions cyclicality and distributes risk across China’s vast gaming headsets market.

Mordor Intelligence provides coverage of the gaming headsets market across other key regional markets, including Europe, Middle East and Africa, and Middle East and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India, Japan, Germany, United Kingdom, United States, and Canada incorporating local coverage and market participation, as required.

Competitive Landscape

The competitive field is characterised by moderate fragmentation. Top international brands such as Logitech, Razer, HyperX, Corsair, SteelSeries, Sony, and Sennheiser compete alongside domestic champions Edifier, ONIKUMA, EKSA, and Havit. No manufacturer holds dominant control, with the top five accounting for roughly 34% of revenue in 2024. Brands concentrate on three levers: acoustic engineering, wireless protocol optimisation, and design customisation for influencer branding.

Technology remains the decisive differentiator. Edifier leverages a partnership with Chinese AI chipset vendors to embed real-time noise suppression that adapts to WeChat and QQ voice call codecs, offering localisation advantages against global rivals. Logitech’s “Play All” ecosystem links headset equaliser profiles to mouse and keyboard configurations through a single application, creating stickiness across peripheral categories. HyperX expands its Cloud series into bronze-level esports leagues through sponsorship packages that bundle headsets with in-ear coach communicators.

Strategic moves in 2024–2025 illustrate varied playbooks. SteelSeries raised production at a Malaysian facility to de-risk China-centric assembly while simultaneously extending its Arctis Nova line with AI mic algorithms tailored for Mandarin consonant clarity. Razer co-developed a limited green-trim Kraken headset with NetEase’s Marvel Rivals, leveraging co-branding to tap dedicated fanbases. Edifier debuted a HECATE sub-brand flagship featuring graphene diaphragms and 40-hour battery life, aiming at Gen-Z streamers. These initiatives showcase relentless feature racing that keeps pricing and innovation fluid across the gaming headsets market.

China Gaming Headsets Industry Leaders

Razer Inc.

Logitech International SA

SteelSeries

Audio-Technica Ltd.

Sony Interactive Entertainment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NetEase reported Q1 2025 gaming revenue of CNY 24 billion (USD 3.3 billion), a 12.1% year-on-year increase that lifts demand for complementary hardware such as headsets.

- May 2025: HUYA Inc. posted 52.1% year-on-year growth in game-related services revenue to CNY 370.4 million (USD 51 million), signalling strong livestream-powered peripheral sales.

- March 2025: Chinese authorities rolled out AR/VR subsidies of up to CNY 2,000 per unit, immediately reducing retail prices for devices such as PICO 4 Ultra.

- February 2025: GN Store Nord’s SteelSeries division confirmed 7% organic growth in 2024 and signalled 7–12% expected growth for 2025, citing innovation in cross-platform audio.

China Gaming Headsets Market Report Scope

A gaming headset is a specialized audio device designed to enhance the gaming experience for users. It integrates headphones and a microphone, enabling gamers to hear in-game audio clearly and communicate effectively with teammates or opponents during multiplayer gaming sessions.

The Chinese gaming headset market is segmented by compatibility type (console headset and PC headset), connectivity type (wired and wireless), and sales channel (retail and online). The report offers the market size in value terms in USD for all the abovementioned segments.

| Console Headsets |

| PC Headsets |

| Mobile Gaming Headsets |

| VR-Specific Headsets |

| Wired |

| Wireless (2.4 GHz / Bluetooth) |

| Esports Professionals |

| Core / Hardcore Gamers |

| Casual and Mobile Gamers |

| Online Marketplaces |

| Offline Retail (Electronics Chains, Specialty) |

| By Compatibility Type | Console Headsets |

| PC Headsets | |

| Mobile Gaming Headsets | |

| VR-Specific Headsets | |

| By Connectivity Type | Wired |

| Wireless (2.4 GHz / Bluetooth) | |

| By End-User | Esports Professionals |

| Core / Hardcore Gamers | |

| Casual and Mobile Gamers | |

| By Sales Channel | Online Marketplaces |

| Offline Retail (Electronics Chains, Specialty) |

Key Questions Answered in the Report

What is the current size of the Chinese gaming headsets market?

The gaming headsets market size in China is valued at USD 359.6 million in 2026 and is projected to grow to USD 590.64 million by 2031.

Which compatibility segment is growing fastest?

VR-specific headsets will post the highest 18.53% CAGR through 2031, benefiting from government hardware subsidies and content expansion.

How important are online channels for headset sales?

Online marketplaces and brand websites captured 68.45% of 2025 revenue and are forecast to reach USD 439.2 million by 2031, making them the dominant distribution route.

What is driving demand among esports professionals?

Rising tournament prize pools, league standardisation of approved gear, and aspirational purchasing by amateur players push professional-grade headset demand at a 15.85% CAGR.

How are semiconductor shortages influencing the market?

Chip supply volatility extends production lead times and elevates component costs, shaving an estimated 1.4% off the market’s forecast CAGR until additional domestic fabs come online.

Which region will lead future growth?

Central and West China will register a 13.12% CAGR through 2031, outpacing coastal provinces due to expanding broadband access and government digital economy initiatives.

Page last updated on: