Canada Gaming Headsets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

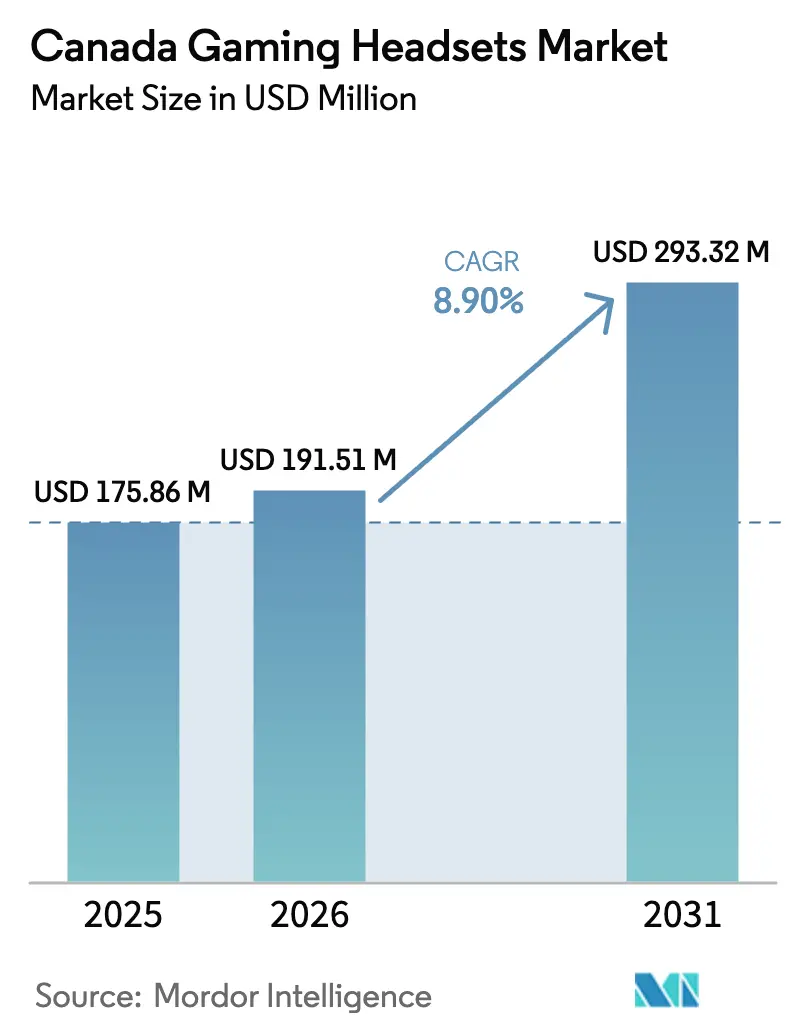

| Base Year Market Size (2025) | USD 175.86 Million |

| Market Size (2026) | USD 191.51 Million |

| Market Size (2031) | USD 293.32 Million |

| Growth Rate (2026 - 2031) | 8.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Gaming Headsets Market Analysis by Mordor Intelligence

The Canada Gaming Headsets Market size was valued at USD 175.86 million in 2025 and estimated to grow from USD 191.51 million in 2026 to reach USD 293.32 million by 2031, at a CAGR of 8.9% during the forecast period (2026-2031). The market’s expansion is aided by the 8% import-tariff removal on audio peripherals, widening console ownership, steady e-commerce gains and a visible shift toward low-latency wireless technologies ero.ontario.ca. Price drops below CAD 120 for 2.4 GHz wireless models have opened premium functionality to budget-minded buyers, while spatial-audio features tied to the PlayStation 5 Tempest engine spur replacement purchasing. Provincial e-waste rules add marginal cost pressure yet encourage durable, recyclable designs, placing sustainability alongside performance as a differentiator. Continued semiconductor output from Ontario and the marshalling of VR content by Quebec studios further reinforce domestic supply-chain resilience and demand elasticity.

Key Report Takeaways

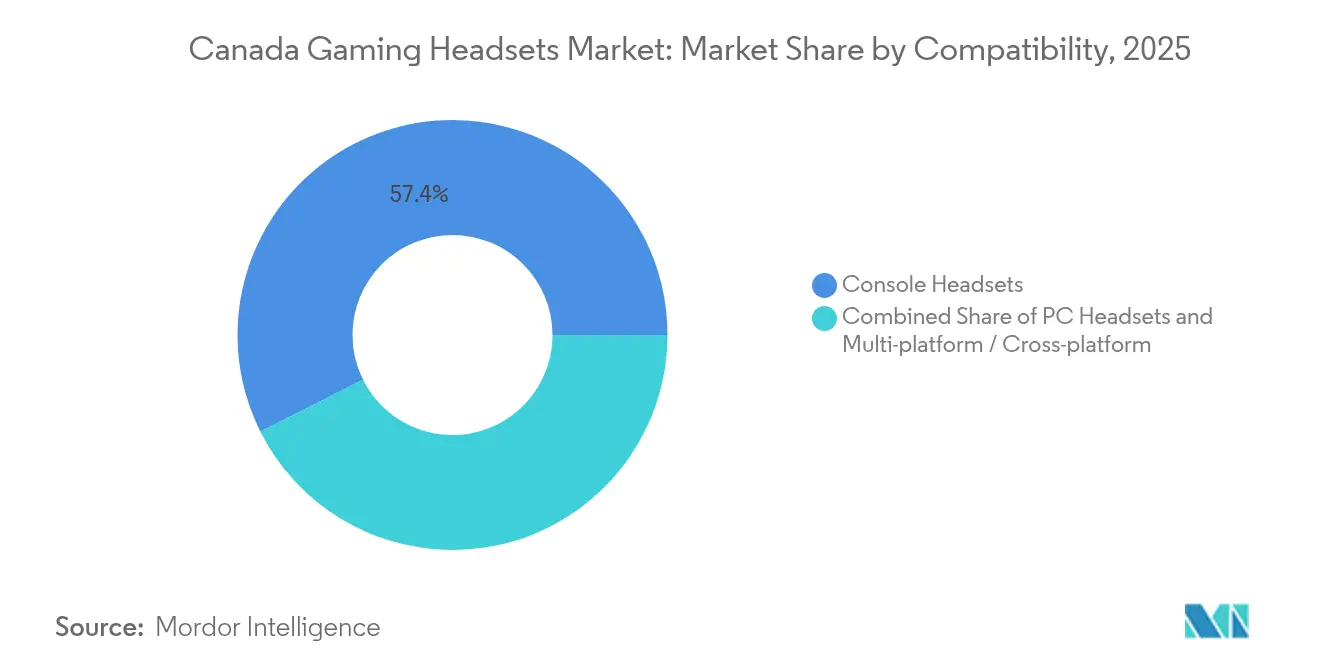

- By compatibility, console headsets held 57.40% of the Canada gaming headsets market share in 2025, whereas multi-platform models are on track for a 11.8% CAGR to 2031.

- By connectivity, wireless 2.4 GHz RF solutions accounted for 62.30% of the Canada gaming headsets market size in 2025 and dual-mode Bluetooth + RF offerings are accelerating at a 13.1% CAGR through 2031.

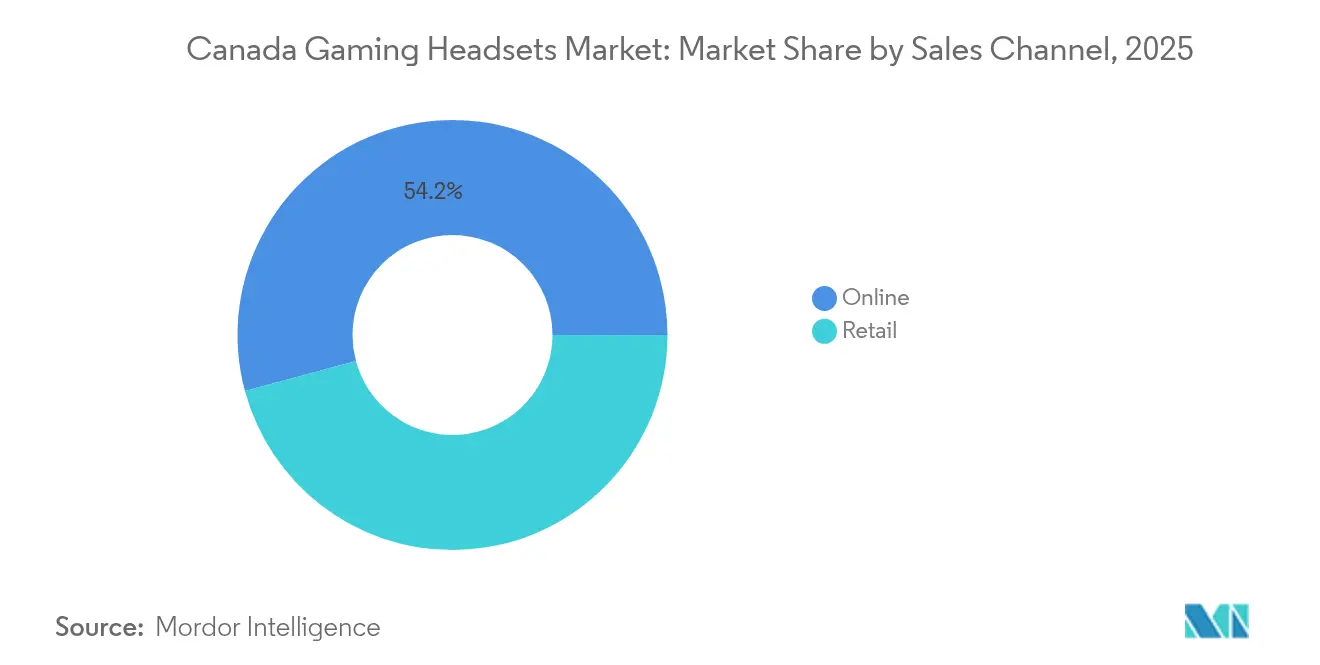

- By sales channel, online sales captured 54.20% share of the Canada gaming headsets market size in 2025 and will expand fastest at a 12.7% CAGR across the outlook period.

- By end-user, casual gamers dominated revenue with a 60.20% slice of the Canada gaming headsets market share in 2025, while the esports and streamers segment is scaling at an 10.6% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

National developments in Canada connect differently with activity unfolding across other parts of the world. In the global gaming headsets market coverage, Mordor Intelligence integrates these into a single analytical framework.

Canada Gaming Headsets Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Esports viewership & sponsorship boom | +1.8% | Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Rapid PS5 /Xbox Series install-base growth | +2.1% | National urban centers | Short term (≤ 2 years) |

| Wireless 2.4 GHz dongle headsets hit sub-CAD 120 price point | +1.4% | National retail markets | Short term (≤ 2 years) |

| VR content localisation deals with Canadian studios | +0.9% | Quebec, Ontario, British Columbia | Long term (≥ 4 years) |

| Elimination of 8% import tariff on audio peripherals | +1.2% | National import-dependent markets | Short term (≤ 2 years) |

| Québec-centric francophone game-streaming surge | +0.6% | Quebec, spillover New Brunswick | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Esports viewership & sponsorship boom

Esports revenue milestones such as Ontario’s iGaming segment eclipsing USD 1.26 billion during FY 2022-23 foster corporate sponsorship budgets that routinely bundle premium headset procurement for pro rosters.[1]iGaming Ontario, “2024-2027 Business Plan,” igamingontario.ca Team standardization contracts lock in seasonal repeat orders, while streamer affiliate codes help lift volume in the casual segment. The resulting halo effect pushes higher driver sizes, better microphones and RGB customization into mid-tier SKUs. Event-linked demand peaks around national qualifiers and global tournaments, smoothing factory utilization in Canada’s headset supply chain.

Rapid PS5 / Xbox Series install-base growth

Sony shipped 8.2 million PlayStation 5 units during Q3 FY 2023, taking cumulative sales past 50 million and cementing a hardware base that requires frequent headset upgrades.[2]Sony Group Corporation, “(E)FY23.3Q_Handout,” sony.com PS5’s Tempest 3D AudioTech and Xbox’s spatial sound suite oblige manufacturers to incorporate larger neodymium drivers and ear-cup venting to reproduce directional cues accurately. Because a typical console owner purchases two to three headsets over a generation, the accessory cycle lengthens the revenue tail after hardware volumes flatten.

Wireless 2.4 GHz dongle headsets hit sub-CAD 120 price point

Single-chip radios capable of throttling cross-protocol interference let vendors cut bill-of-materials costs without sacrificing sub-40 ms latency, bringing street prices under CAD 120.[3]Patents Encyclopedia, “CHANNEL INTERFERENCE REDUCTION,” patentsencyclopedia.com The pocket-friendly threshold encourages impulse buys for upcoming releases and gifting spikes around Black Friday, expanding the Canada gaming headsets market to first-time buyers. Unit volumes rose 20% at Logitech during Q1 FY 25, underscoring elasticity in the mid-range band.

VR content localisation deals with Canadian studios

Canada Media Fund incentives enable Quebec and Ontario studios to adapt VR titles bilingually, demanding headsets that preserve low-latency positional audio in rotating virtual soundscapes. [4]Canada Media Fund, “International Incentives,” cmf-fmc.ca Patented HRTF algorithms from Meta filter down into premium models so Canadian creators test localized builds under production-style acoustic conditions. Because content teams trial multiple builds, they issue bulk orders that amplify headset pull even before consumer launch dates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intermittent semiconductor shortages that disrupt component supply | -1.6% | Felt across Canada because manufacturers depend on globally sourced chips | Medium term (2-4 years) |

| Console hardware life-cycle slowdown expected after 2026 | -1.9% | Affects gamers nationwide as the current PlayStation 5 and Xbox Series generation matures | Long term (≥ 4 years) |

| Price sensitivity among casual gamers, especially first-time buyers | -0.8% | Most visible in rural regions and lower-income households throughout the country | Short term (≤ 2 years) |

| Rising retail prices linked to provincial e-waste recovery fees | -0.7% | Primarily impacts Ontario, Quebec and British Columbia, where environmental fees are highest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyclical semiconductor shortages

Canada imported USD 7.3 billion in semiconductor components while exporting only USD 3.4 billion, highlighting sensitivity to Asian foundry disruptions. Allocation gaps lift controller, codec and power-management chip costs, prompting makers to prioritize high-margin esports SKUs. Design swaps to substitute scarce parts extend validation cycles and squeeze launch calendars, trimming near-term volume for the Canada gaming headsets market.

Maturing console cycle after 2026

Sony’s guidance on tapering PS5 hardware units signals the onset of late-generation stall when buyers delay accessories until next-gen news firm up. The historical pattern shows attach-rate softening, heightening discounting pressure and nudging brands to broaden multi-platform portfolios. Developers temp-test firmware to futureproof against upcoming consoles, elongating R&D and dampening near-term headset launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compatibility: Multi-platform versatility redefines user expectations

Console-specific models retained command in 2025, delivering 57.40% of shipment value across the Canada gaming headsets market. The PS5 install base, together with Xbox Series X/S, underpins steady renewals as players graduate from bundled earbuds to directional-audio headsets. PC-exclusive SKUs cater to competitive play, sustaining higher-fidelity requirements but a narrower audience.

Growth, however, tilts decisively toward multi-platform SKUs which are projected at a 11.8% CAGR to 2031. Patent filings on automatic device-switching enable users to jump between console, PC and handheld without re-pairing, meeting the nomadic session habits of Canadian gamers. The Canada gaming headsets market size attached to multi-platform products is positioned to absorb console-cycle volatility and offers producers healthier margins through premium pricing strategies.

By Connectivity: Dual-mode emerges as the flagship format

Wireless shipments delivered 62.30% of Canada gaming headsets market revenue in 2025, reflecting near-zero perceived latency gains and sofa-to-desk mobility advantages. The cost breakthrough under CAD 120 widened inclusivity, shifting demand mix away from legacy wired lines.

The fastest runway belongs to dual-mode units blending 2.4 GHz RF with Bluetooth 5.x, charting a 13.1% CAGR. Qualcomm’s synchronous channel access patents minimize packet collision when concurrent phone audio and console gameplay occur. Early adopters pay 40-60% premiums, validating higher R&D outlays and steering the Canada gaming headsets market toward software-defined feature roadmaps.

By Sales Channel: Online accelerates direct brand-to-player relationships

The online channel booked 54.20% of 2025 sales, underpinned by same-day fulfilment in urban corridors and manufacturer web shops that offer loyalty bundles and firmware updates. Brand-run e-stores also lower return friction and harvest usage telemetry for iterative design.

Brick-and-mortar chains remain critical, preserving 45.80% share as try-before-buy comfort testing and instant takeaway appeal especially for ergonomic categories. Large retailers shoulder provincial recycling obligations more smoothly than small stores, leveraging national logistics to meet Ontario’s circular-economy framework. This compliance capability shelters their relevance even as e-commerce outpaces.

By End-User: Esports & streaming shape premium spec benchmarks

Casual gamers still formed 60.20% of unit demand in 2025, valuing long battery life and simple plug-and-play. VR enthusiasts, though smaller, insist on headsets certified for full-room tracking acoustics that prevent motion-to-audio desync.

Esports athletes and streamers will post an 10.6% CAGR until 2031, pivoting the Canada gaming headsets market toward broadcast-grade microphones and software EQ that complies with tournament audio rules. Sponsorship visibility lifts demand for customizable ear-cup plates and RGB lighting profiles synchronized with on-screen overlays, reinforcing high-price tiers.

Geography Analysis

Ontario anchored the largest share of the Canada gaming headsets market in 2025 due to dense urban populations in Toronto and Ottawa and proximity to cross-border distribution. The province hosts 62.8% of national semiconductor value add, trimming lead times for locally-sourced audio codecs and batteries. Its e-waste regulation accelerates recyclable headset shell adoption, boosting premium durable plastics over legacy ABS blends. Quebec shows the briskest CAGR to 2031, propelled by francophone streamers whose follower bases surpass English-language peers on certain platforms. Media-fund grants targeted at bilingual VR localization grow headset requirements among developers, while provincial tax incentives offset CapEx for smaller studios. British Columbia and Alberta maintain meaningful slices of the Canada gaming headsets market given their tech-skilled workforces and disposable income stemming from software and resource sectors. West-coast shipping lanes also cut freight on Asian-origin peripherals, enhancing retailer margins. The Prairie provinces witness steady but smaller expansion, hinging on rural broadband upgrades that convert latent gamer interest into active online play. Northern Territories represent a niche wherein extreme weather durability and insulated ear pads justify price premiums, ensuring coverage despite logistically complex routes.

Mordor Intelligence's coverage of the gaming headsets market extends across other regions including Middle East and Africa, North America, and Latin America, while country-specific intelligence is also available for United States, China, India, United Kingdom, Japan, and Germany, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The Canada gaming headsets market features moderate fragmentation, with the top five brands combining for about two-thirds of revenue. Logitech’s 20% YOY headset growth in Q1 FY 25 highlights how iterative feature drops and colourway refreshes nudge continual upgrades. Turtle Beach’s expansion plan spanning Canada and Latin America underscores cross-regional inventory leveraging for scale benefits.

Competition orbits around latency benchmarks, battery endurance and software ecosystems that lock users into proprietary equalizers and chat mixers. Sony’s patents on HRTF simulation sharpen its edge in 3D audio fidelity, pushing rivals to license or invent alternative pipelines. Meanwhile, SteelSeries and HyperX battle within esports sponsorship rosters, granting early-access inventory to championship teams to influence aspirational buyers.

Sustainability grows as an axis of differentiation. Brands with closed-loop plastics score favorably under Ontario’s recycling regime, whereas laggards risk listing delistments at eco-focused retailers. Direct-to-consumer strategies allow niche entrants to bypass shelf-space wars, but high return rates on comfort-driven peripherals test supply-chain agility.

Canada Gaming Headsets Industry Leaders

HyperX (HP Inc.)

Microsoft Corporation

JBL (Harman International Industries, Incorporated)

ASUSTeK COMPUTER INC.

JVCKENWOOD Canada Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sony posted robust Q3 FY 2024 accessory revenue, signalling headsets as a stabilizer amid moderating console hardware sales.

- February 2025: Canada Border Services Agency preserved current headset classifications in the Customs Tariff 2025 schedule.

- November 2024: Statistics Canada updated semiconductor-industry contribution totals, reaffirming Ontario’s centrality for component sourcing.

- October 2024: Turtle Beach unveiled an expanded Canadian distribution blueprint with localized campaigns aimed at urban esports hubs.

Canada Gaming Headsets Market Report Scope

Gaming headsets are primarily specialized headphones designed for video games that boast superior sound quality, integrated microphones for in-game communication, and frequently offer additional features like noise cancellation, surround sound, and wireless connectivity. Enhancing gaming immersion, these devices offer clear audio and seamless communication, which is particularly crucial in multiplayer and competitive gaming.

The Canada gaming headsets market is segmented by compatibility type (console headset and PC headset), by connectivity type (wired and wireless), and by sales channel (retail and online). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Console Headsets | Xbox-Optimised |

| PlayStation-Optimised | |

| PC Headsets | |

| Multi-platform |

| Wired | |

| Wireless | 2.4 GHz RF |

| Bluetooth 5.x | |

| Dual-Mode (Simultaneous BT + RF) |

| Retail | Electronics Specialists |

| Mass Merchandisers | |

| Online | Brand e-Stores |

| Marketplaces and Gaming Portals |

| Casual Gamers |

| Esports and Streamers |

| VR Enthusiasts |

| Content Creators |

| By Compatibility | Console Headsets | Xbox-Optimised |

| PlayStation-Optimised | ||

| PC Headsets | ||

| Multi-platform | ||

| By Connectivity | Wired | |

| Wireless | 2.4 GHz RF | |

| Bluetooth 5.x | ||

| Dual-Mode (Simultaneous BT + RF) | ||

| By Sales Channel | Retail | Electronics Specialists |

| Mass Merchandisers | ||

| Online | Brand e-Stores | |

| Marketplaces and Gaming Portals | ||

| By End-User | Casual Gamers | |

| Esports and Streamers | ||

| VR Enthusiasts | ||

| Content Creators | ||

Key Questions Answered in the Report

What is the current value of the Canada gaming headsets market?

It stands at USD 191.51 million in 2026 with a projected rise to USD 293.32 million by 2031.

Which compatibility segment is growing the fastest?

Multi-platform headsets are forecast to expand at a 11.8% CAGR as gamers demand seamless device switching.

How big is online’s role in headset distribution?

Online platforms account for 54.20% of 2025 sales and hold the top growth rate of 12.7% CAGR, driven by direct-to-consumer storefronts.

Why are dual-mode headsets gaining attention?

They merge low-latency 2.4 GHz gameplay with Bluetooth convenience, supporting a 13.1% CAGR through 2031.

What regulation most affects headset producers in Ontario?

The Resource Recovery and Circular Economy Act obliges producers to fund collection and recycling, shaping sustainable design choices.

How do semiconductor shortages influence headset pricing?

Component scarcity lifts costs for logic and audio chips, prompting makers to prioritize premium SKUs and temporarily constrict supply.

Page last updated on: