Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

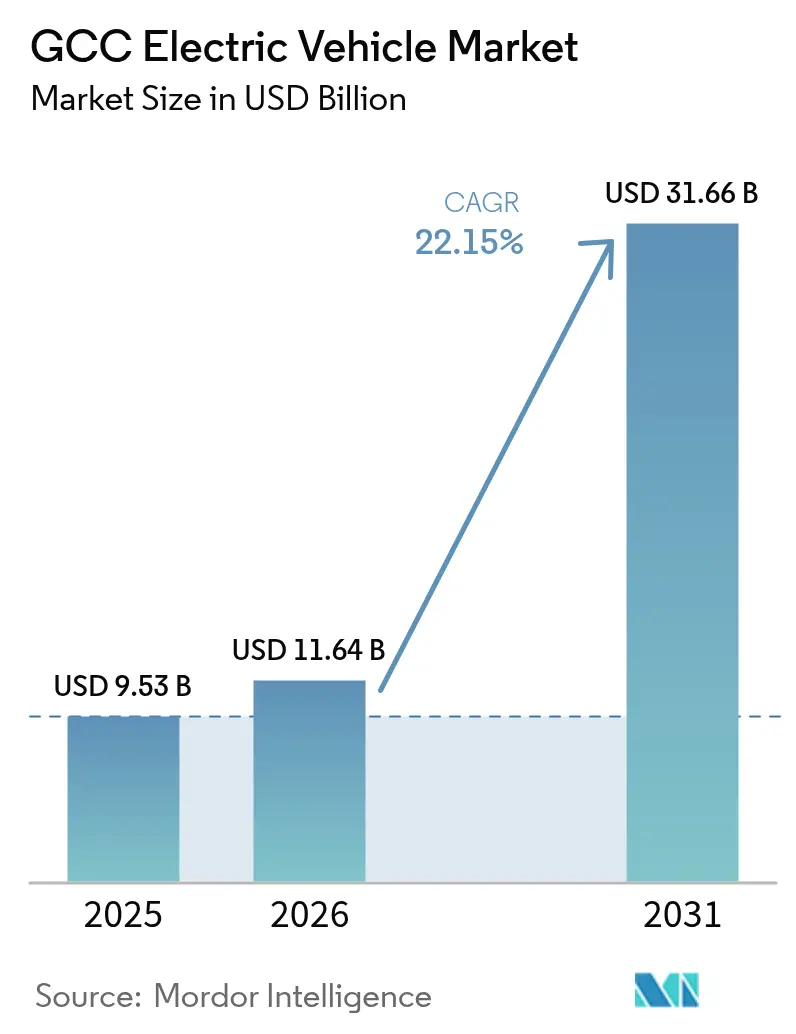

| Base Year Market Size (2025) | USD 9.53 Billion |

| Market Size (2026) | USD 11.64 Billion |

| Market Size (2031) | USD 31.66 Billion |

| Growth Rate (2026 - 2031) | 22.15% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC Electric Vehicle Market Analysis by Mordor Intelligence

The GCC electric vehicle market size will rise from USD 9.53 billion in 2025 to USD 11.64 billion in 2026, reaching USD 31.66 billion by 2031, expanding at a CAGR of 22.15% over 2026-2031. Early-mover policy mandates, sovereign-wealth funding, and a rapid build-out of ultra-fast public chargers are synchronizing to accelerate adoption across every Gulf state. Automakers are localizing assembly to trim landed costs, while battery suppliers court regional gigafactory proposals that promise deeper supply-chain integration. Commercial fleets are electrifying faster as the total cost of ownership becomes more favorable, yet passenger cars still dominate absolute volumes. Competition remains moderate because no single brand controls more than 15% of the GCC electric vehicle market, creating space for regional entrants to win government and corporate tenders.

Key Report Takeaways

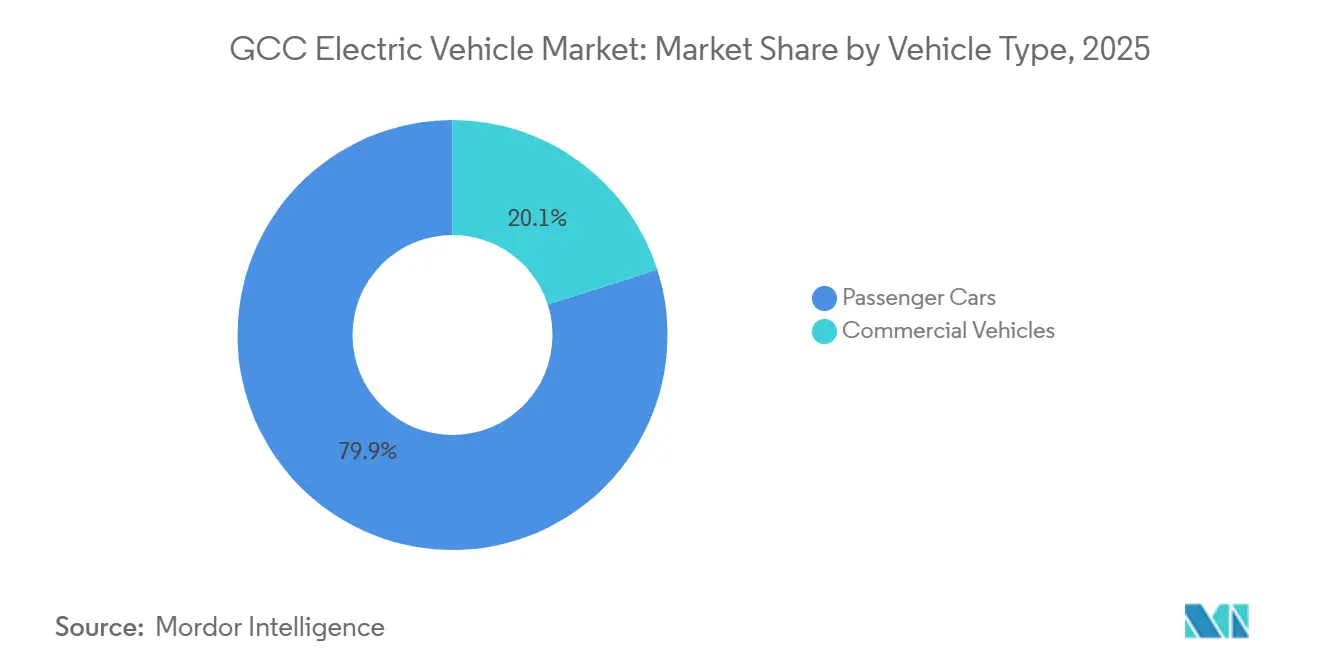

- By vehicle type, passenger cars hold 79.92% of the GCC electric vehicle market share in 2025, while commercial vehicles are forecast to grow at a 23.22% CAGR through 2031.

- By propulsion type, battery-electric vehicles captured 67.83% of the GCC electric vehicle market share in 2025; fuel-cell electric vehicles are projected to exhibit the highest CAGR of 23.98% through 2031.

- By battery capacity, 40–60 kWh packs accounted for 44.57% of the GCC electric vehicle market share in 2025, and packs above 100 kWh are advancing at a 22.99% CAGR through 2031.

- By charging infrastructure, AC slow chargers held 53.38% of the GCC electric vehicle market share in 2025, whereas ultra-fast units above 150 kW are set to post the fastest 28.51% CAGR through 2031.

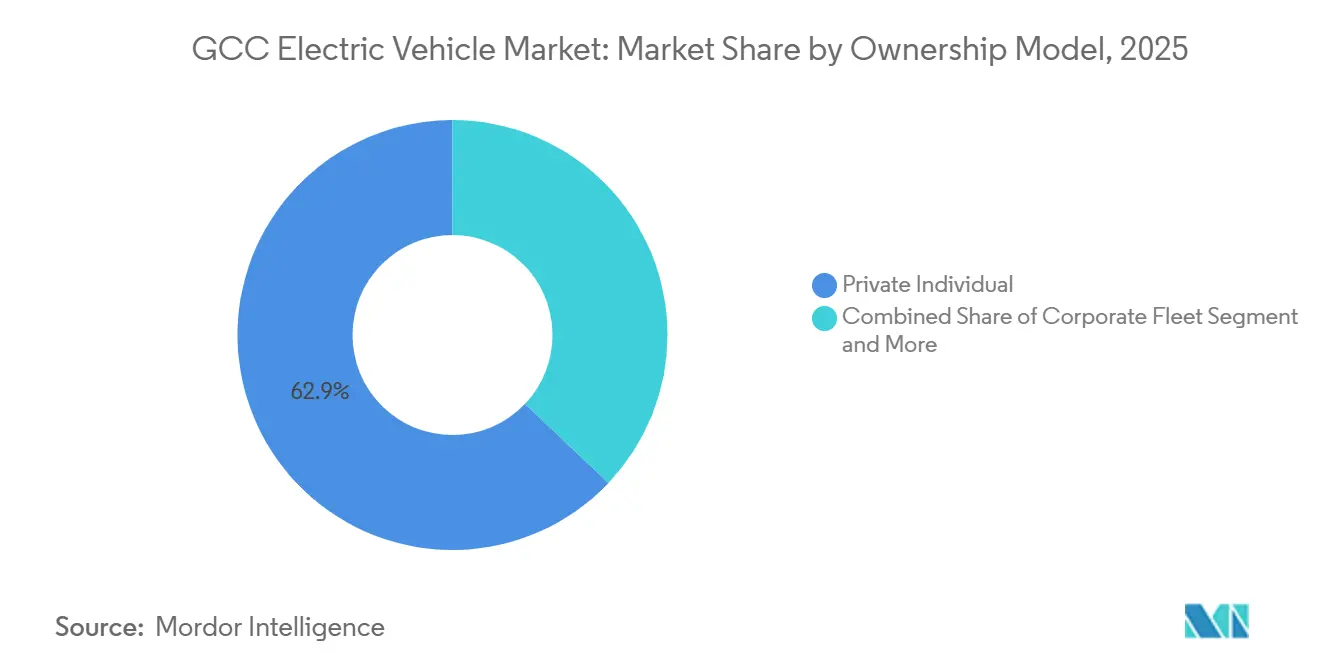

- By ownership model, private individuals accounted for 62.91% of the GCC electric vehicle market share in 2025, while corporate fleets are forecasted to record a 23.73% CAGR to 2031.

- By price segment, the USD 35,000–60,000 mid-range commanded 49.49% of the GCC electric vehicle market share in 2025, while the economy tier below USD 35,000 is projected to expand at 23.91% CAGR through 2031.

- By country, the United Arab Emirates accounted for 42.01% of the GCC electric vehicle market share in 2025; Saudi Arabia is forecast to post a 23.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonization Mandates and Zero-Emission Targets | +5.5% | Saudi Arabia, UAE, Qatar, Oman, Kuwait, Bahrain | Medium term (2-4 years) |

| Expenditure on Regional Assembly Plants | +4.2% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Expansion of Public Charging Infrastructure | +3.8% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Falling Battery Pack Costs | +3.5% | Saudi Arabia, UAE, Qatar, Oman, Kuwait, Bahrain | Medium term (2-4 years) |

| Wealth Fund Equity in EV Start-Ups | +2.8% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Cross-Border Green-Hydrogen Corridors | +2.0% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Decarbonization Mandates and Zero-Emission Targets

National programs such as Saudi Vision 2030’s 30% zero-emission vehicle goal for Riyadh and the UAE Climate Change Plan’s 50% cut in transport emissions are locking in long-term demand signals[1]"Saudi Arabia", Climate Action Tracker, climateactiontracker.org. These mandates compel automakers to allocate production slots to the GCC electric vehicle market before other regions. Tier-1 suppliers are now scouting factory sites in Jeddah and Abu Dhabi to meet local content requirements. Fleet tenders embed zero-emission clauses, forcing bus and taxi operators to adopt electric drivetrains. As compliance windows tighten, incremental incentives such as reduced registration fees amplify consumer pull.

Automaker Capital Expenditure on Regional Assembly Plants

Ceer Motors, Lucid, and Hyundai together committed more than USD 5 billion to Saudi assembly capacity slated to start output in 2026. Local build lowers shipping and duty costs that historically inflated sticker prices in the GCC electric vehicle market. Assembly footprints anchor ancillary suppliers, nurturing a regional parts ecosystem. Shorter supply chains cut lead times, letting dealers hold leaner inventory. Over time, assembly plants may pivot to export, enhancing utilization and cost efficiency.

Rapid Expansion of Public Charging Infrastructure

EVIQ, ADNOC, DEWA, and Kahramaa collectively plan over 5,500 additional chargers by 2030, with ultra-fast sites spaced at 150-kilometer intervals on intercity corridors[2]Basem Bawazeer Al-Eqtisadiah, "EVIQ to complete 60 EV charging stations by end of 2025, focus shifts to highways", Arab News, arabnews.com. 15-minute recharge windows meet commercial-fleet uptime requirements, unlocking long-range battery-electric adoption. Charger density eases range anxiety for private buyers and supports tourism traffic across Gulf borders. Grid operators deploy smart-load software to align charging peaks with solar output, limiting new-build power-generation needs. Pilot battery-swap stations offer a complementary refueling model for ride-hailing fleets.

Falling Lithium-Ion Battery Pack Costs

Average pack prices slid to USD 108 per kWh in 2025 and trended toward the USD 100 threshold in 2026, narrowing the upfront premium versus gasoline cars. Cost parity accelerates the economy segment’s advance in the GCC electric vehicle market. Automakers channel savings into larger-capacity packs without higher retail prices, extending real-world range. Chinese LFP chemistries dominate import flows, balancing thermal stability with cost. Future breakthroughs in solid-state or sodium-ion could unlock another step-change if raw-material prices stabilize.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High EV Price Vs ICE Parity | -2.8% | GCC-wide, particularly Kuwait, Oman | Short term (≤ 2 years) |

| Limited Model Availability | -1.9% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Grid-Scale Desalination | -1.4% | UAE, Saudi Arabia, Kuwait | Long term (≥ 4 years) |

| Sharia-Compliant Financing Structures | -1.1% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront EV Purchase Price Vs ICE Parity

Sticker prices remain significantly above internal-combustion equivalents across most Gulf showrooms, despite falling battery costs. Chinese brands partially bridge the gap below USD 35,000, yet luxury trims skew segment averages higher. Import duties in Kuwait and legacy financing norms elsewhere inflate effective ownership costs. Domestic assembly should shave 10–15% from prices as plants ramp, but broad parity for mass-market buyers is unlikely before 2027. Short-term subsidies or fee waivers can soften the transition for price-sensitive households.

Limited Model Availability for Extreme-Temperature Climates

Temperatures soaring past 40 °C can cut battery range by as much as 23%, dissuading potential buyers who frequently navigate long desert routes. Only a select few models come equipped with advanced thermal management and extended heat-warranty coverage. While added cooling hardware can elevate production costs, many entry-level imports choose to forgo it. Due to the absence of localized R&D, automakers are reluctant to certify their compact models for the sweltering Gulf summers. To fully embrace the market, there's a pressing need for advancements in heat-resistant chemistries and a more diverse model portfolio.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Accelerate Electrification

Passenger cars accounted for 79.92% of the GCC electric vehicle market share in 2025, underscoring the early dominance of private purchases. However, fleet operators’ focus on predictable duty cycles and bulk-energy contracts is steadily tilting momentum toward vans, buses, and trucks. Public-sector procurement aligns with low-emission targets, and logistics firms cite maintenance and fuel savings as pivotal factors. Depot-based overnight charging simplifies energy management, while governments grant preferential electricity tariffs to high-utilization fleets.

Commercial vehicles, expanding at a 23.22% CAGR through 2031, underscore the structural shift underway. Cities from Riyadh to Doha earmark dedicated bus lanes for zero-emission units, reinforcing modal confidence. Parcel-delivery networks deploy electric light vans that dovetail with e-commerce surge patterns. Pilot programs in medium-duty freight refine performance data under desert conditions, preparing the segment for scale. As corporate buyers aggregate demand, OEMs can justify sourcing chassis and batteries locally.

By Propulsion Type: Fuel Cells Gain Traction

Battery electric vehicles captured 67.83% of the GCC electric vehicle market size in 2025 by leveraging ubiquitous charger roll-outs and competitive total ownership costs. Incremental improvements in pack energy density address range anxiety for most daily routes. In tandem, software-based thermal controls mitigate degradation caused by high ambient heat, extending the usable lifespan. Fuel-cell electric vehicles are projected to deliver the fastest 23.98% CAGR through 2031, driven by funded green-hydrogen megaprojects in Saudi Arabia and Oman.

Three-minute refueling and heavy-load suitability position FCEVs as credible solutions for long-haul freight and intercity coaches. Early corridors anchor refueling nodes at existing truck stops, promoting operational familiarity. Policy makers monitor hydrogen price trajectories, aiming for sub-USD 4-per-kilogram parity milestones that could further diversify the GCC electric vehicle market's propulsion mix.

By Battery Capacity: High-Capacity Packs Gain Share

The 40–60 kWh band accounted for 44.57% of the GCC electric vehicle market share in 2025, mirroring the popularity of compact SUVs among urban drivers who prioritize affordability. Energy density gains enable this class to deliver well over 300 kilometers of real-world range, adequate for daily commuting and weekend trips within single emirates.

Packs above 100 kWh, forecasted to grow at 22.99% CAGR through 2031, headline the premium and commercial classes. Their extended range matches the Dubai–Riyadh round-trip flights with minimal stops, satisfying fleet-uptime imperatives. Luxury buyers also prize the thermal buffer that large packs afford during peak-heat months. As pack production scales in new regional facilities, the cost delta versus mid-size batteries is narrowing, accelerating adoption at both ends of the GCC electric vehicle market spectrum.

By Charging Infrastructure: Ultra-Fast Charging Accelerates

AC slow chargers below 22 kW constituted 53.38% of the GCC electric vehicle market share in 2025, a legacy of early residential incentives. Workplace landlords then layered mid-tier DC fast units to shorten top-up sessions during office hours, cultivating daily-use convenience for staff commuters. Ultra-fast chargers above 150 kW, advancing at a 28.51% CAGR through 2031, enable end-to-end Gulf crossings within standard driving breaks.

Energy companies retrofit highway service areas to host 350 kW dispensers that deliver 300 kilometers of range in about 10 minutes. Integration with solar-plus-storage arrays helps mitigate demand spikes. As high-power connectors become more universal, OEMs ensure next-generation models ship with compatible hardware, cementing ultra-fast’s role in the GCC electric vehicle market infrastructure mix.

By Ownership Model: Corporate Fleets Surge

Private individuals retained a 62.91% of the GCC electric vehicle market share in 2025, thanks to early adopters and expanding showroom availability. Government fee reductions, free parking, and subsidized home chargers sustained momentum in the premium districts of Dubai and Abu Dhabi. Corporate fleets, expected to grow at 23.73% CAGR through 2031, aggregate vehicle demand into multi-year contracts that reward OEM scale efficiencies.

Bulk procurements secure lower per-unit pricing and priority production slots. Ride-hailing and last-mile delivery firms piloting battery-swap platforms further emphasize the importance of uptime economics. Public bodies follow suit via tender mandates, channeling predictable volumes into domestic assembly pipelines and anchoring local supply chains inside the GCC electric vehicle market.

By Price Segment: Economy Tier Expands

The USD 35,000–60,000 mid-range held 49.49% of the GCC electric vehicle market share in 2025, buoyed by crossover models that blend practicality with brand cachet. Government salary profiles and consumer credit norms align naturally with this bracket, sustaining showroom traffic. Economy models priced below USD 35,000 are forecast to deliver the fastest CAGR of 23.91% through 2031, as Chinese brands expand their dealer networks across Riyadh, Jeddah, and Kuwait City.

Lithium-iron-phosphate chemistry slashes battery costs, and stripped-down trim lines cater to first-time buyers' budgets. When local assembly reaches volume, additional duty relief and logistics savings should propel mass-market adoption. Luxury tiers remain niche, constrained by sparse service networks and heat-warranty skepticism, yet they provide halo visibility that benefits the wider GCC electric vehicle market.

Geography Analysis

The United Arab Emirates accounted for 42.01% of the GCC electric vehicle market in 2025, reflecting Dubai and Abu Dhabi’s early investments in more than 3,000 public charging stations and generous registration incentives. Rapid consumer uptake snowballed as taxi, police, and municipal fleets integrated zero-emission targets. Showrooms clustered along Sheikh Zayed Road offered broad model ranges, sustaining brand competition—policy certainty, such as free Salik toll access for EVs, reinforced resale values, and buyer confidence.

Saudi Arabia is set to eclipse the UAE by 2031 on a 23.56% CAGR path, underpinned by Vision 2030’s 500,000-unit domestic-production mandate and the Public Investment Fund’s multi-billion-dollar commitments. Assembly lines for Ceer, Lucid, and Hyundai shorten delivery pipelines, while EVIQ’s 5,000-charger plan closes infrastructure gaps on major highways. Fleet conversions by SAPTCO and Aramco boost visibility and normalize EV usage in conservative consumer segments. Incentive frameworks, waiving import duties on battery cells, and guaranteeing low industrial-electricity tariffs further tilt the scales in favor of economics.

Qatar, Oman, Kuwait, and Bahrain collectively accounted for less than 15% of the GCC electric vehicle market in 2025, yet they pursue differentiated strategies to expand regional connectivity. Qatar’s Kahramaa eyes 600 to 1,000 public chargers and hydrogen ties to gas-export facilities, positioning Doha as a hub for fuel-cell freight to South Asia. Oman’s green-hydrogen megaproject pipeline secures financing that could underwrite FCEV refueling corridors. Kuwait trims customs duties on Chinese imports to stimulate demand from the economy tier, and Bahrain halves EV registration fees to accelerate mainstream adoption. Harmonized GCC technical standards aid cross-border interoperability, setting the stage for a more balanced geographic split in the GCC electric vehicle market by 2031.

Competitive Landscape

Fragmentation defines the current GCC electric vehicle market, with Tesla, Nissan, Hyundai, BMW, and BYD together holding a modest plurality. Tesla leverages a proprietary Supercharger backbone to anchor premium buyers, while BYD scales swiftly in the economy tier by exploiting lithium-iron-phosphate cost advantages. Hyundai and Lucid pursue localized assembly to trim duties and freight costs, aligning product pipelines with evolving fleet tenders. Newcomer Ceer benefits from government procurement preferences and technology-transfer deals that shortcut time-to-market.

White-space opportunities appear most acute in commercial vehicles as bus operators and logistics majors seek turnkey electrification partners. Chinese truck OEMs are evaluating CKD kit assembly in the Gulf to avoid import levies and meet local-content rules. Battery-swap innovators, led by Ample, pitch five-minute refueling for ride-hailing fleets, challenging charger incumbents and enticing platform operators with higher asset utilization. Component suppliers such as Rimac embed thermal management and high-voltage expertise into regional factories, bolstering EV resilience in desert conditions.

Consolidation pressures will intensify after 2028 once assembly plants hit scale and charging networks mature. Brands without local manufacturing or a clear fleet proposition risk marginalization. Conversely, first movers that secure government and corporate volume contracts can lock in multiyear production visibility. As warranty data de-risks extreme-temperature operation, follow-on buyers could gravitate toward proven platforms, gradually raising concentration within the GCC electric vehicle market.

GCC Electric Vehicle Industry Leaders

-

Hyundai Motor Company

-

Tesla, Inc.

-

BMW AG

-

Nissan Motor Co., Ltd.

-

BYD Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Cherry Group unveiled its new brand, iCAUR, focusing on hybrid and electric vehicles. Leading the charge for iCAUR in the Middle East is the debut of its versatile mid-to-large hybrid SUV, the iCAUR V27.

- November 2025: Emirates Petroleum Company PJSC (Emarat) inaugurated its 158th service station, named “Al Buhaira,” in Barsha South. This move not only broadens Emarat’s footprint in New Dubai but also unveils the region’s inaugural dedicated Electric Vehicle Service Center.

- August 2025: Omega Seiki Mobility opened its first overseas assembly plant in Dubai’s Jebel Ali Free Zone, with a planned investment of USD 25 million.

GCC Electric Vehicle Market Report Scope

An electric vehicle operates on an electric motor rather than an internal combustion engine. Therefore, the electric vehicle is a possible replacement for the current-generation automobile in the near future to address environmental challenges.

The GCC Electric Vehicle market is segmented by vehicle type, propulsion type, battery capacity (kWh range), charging infrastructure type, ownership model, price segment, and country. By Vehicle Type, the market is segmented into Passenger Cars (Hatchbacks, Sedans, SUVs, and Crossovers) and Commercial Vehicles (Light Commercial Van, Buses and Coaches, and Medium and Heavy Trucks). By Propulsion Type, the market is segmented into Battery Electric Vehicles (BEV), Plug-in Hybrid Electric Vehicles (PHEV), Hybrid Electric Vehicles (HEV), and Fuel Cell Electric Vehicles (FCEV). By Battery Capacity (kWh Range), the market is segmented into Below 40 kWh, 40 to 60 kWh, 61 to 100 kWh, and Above 100 kWh. By Charging Infrastructure Type, the market is segmented into AC Slow Chargers (Below 22 kW), DC Fast Chargers (22 to 150 kW), Ultra-Fast Chargers (Above 150 kW), and Battery Swap Stations. By Ownership Model, the market is segmented into Private Individual, Corporate Fleet, Ride-hailing / Car-sharing, and Government and Municipal. By Price Segment, the market is segmented into Economy (Below USD35k), Mid-range (USD35k to 60k), and Luxury (Above USD60k). By Country, the market is segmented into the United Arab Emirates, Saudi Arabia, Qatar, Oman, Kuwait, and Bahrain.

Market forecasts are provided in terms of Value (USD) and Volume (Units).

By Vehicle Type

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUVs and Crossovers | |

| Commercial Vehicles | Light Commercial Vans |

| Buses and Coaches | |

| Medium and Heavy Trucks |

By Propulsion Type

| Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Hybrid Electric Vehicles (HEV) |

| Fuel Cell Electric Vehicles (FCEV) |

By Battery Capacity (kWh Range)

| Below 40 kWh |

| 40 to 60 kWh |

| 61 to 100 kWh |

| Above 100 kWh |

By Charging Infrastructure Type

| AC Slow Chargers (Below 22 kW) |

| DC Fast Chargers (22 to 150 kW) |

| Ultra-Fast Chargers (Above 150 kW) |

| Battery Swap Stations |

By Ownership Model

| Private Individual |

| Corporate Fleet |

| Ride-hailing / Car-sharing |

| Government and Municipal |

By Price Segment

| Economy (Below USD 35k) |

| Mid-range (USD 35k to 60k) |

| Luxury (Above USD 60k) |

By Country

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUVs and Crossovers | ||

| Commercial Vehicles | Light Commercial Vans | |

| Buses and Coaches | ||

| Medium and Heavy Trucks | ||

| By Propulsion Type | Battery Electric Vehicles (BEV) | |

| Plug-in Hybrid Electric Vehicles (PHEV) | ||

| Hybrid Electric Vehicles (HEV) | ||

| Fuel Cell Electric Vehicles (FCEV) | ||

| By Battery Capacity (kWh Range) | Below 40 kWh | |

| 40 to 60 kWh | ||

| 61 to 100 kWh | ||

| Above 100 kWh | ||

| By Charging Infrastructure Type | AC Slow Chargers (Below 22 kW) | |

| DC Fast Chargers (22 to 150 kW) | ||

| Ultra-Fast Chargers (Above 150 kW) | ||

| Battery Swap Stations | ||

| By Ownership Model | Private Individual | |

| Corporate Fleet | ||

| Ride-hailing / Car-sharing | ||

| Government and Municipal | ||

| By Price Segment | Economy (Below USD 35k) | |

| Mid-range (USD 35k to 60k) | ||

| Luxury (Above USD 60k) | ||

| By Country | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Oman | ||

| Kuwait | ||

| Bahrain | ||

Key Questions Answered in the Report

What is the valuation of the GCC electric vehicle market?

It is valued at USD 11.64 billion in 2026 and projected to reach USD 31.66 billion by 2031.

Which Gulf country is growing fastest in EV adoption?

Saudi Arabia shows the fastest growth trajectory, supported by Vision 2030 production mandates and large-scale charging roll-outs.

How quickly are commercial EV fleets expanding in the GCC?

Commercial vehicles are forecast to grow at an annual 23.22% rate through 2031, outpacing passenger cars.

Which propulsion technology leads in 2025?

Battery-electric vehicles accounted for 67.83% of the GCC electric vehicle market in 2025, though fuel-cell electric vehicles have the highest projected growth rate.

What charging technology is scaling most rapidly?

Ultra-fast chargers above 150 kW are advancing at an 28.51% CAGR as operators focus on intercity corridors.

Page last updated on: