Global Gastroparesis Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.25 Billion |

| Market Size (2031) | USD 6.51 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Gastroparesis Drug Market Analysis by Mordor Intelligence

The gastroparesis drugs market size is expected to grow from USD 5.03 billion in 2025 to USD 5.25 billion in 2026 and is forecast to reach USD 6.51 billion by 2031 at 4.38% CAGR over 2026-2031. This outlook reflects a therapeutic field shaped by limited FDA-approved options, frequent off-label prescribing, and regulatory hurdles that slow the entry of novel agents. Metoclopramide remains the only oral drug formally cleared for gastroparesis, yet Evoke Pharma’s GIMOTI nasal spray shows how differentiated delivery can unlock demand, with annual run-rate sales topping USD 10 million in 2024. Prokinetic agents held 42.35% of the gastroparesis drugs market in 2024, but botulinum toxin injections are expanding fastest at 5.25% through 2030, mirroring growth in interventional gastroenterology procedures. North America dominated with a 43.81% share in 2024, supported by specialized care centers, while Asia-Pacific is projected to grow 6.41% a year to 2030 on the back of rising diabetes prevalence and broader healthcare access. Investor interest has rebounded, illustrated by CinDome Pharma’s USD 40 million Series B in 2024 to advance deudomperidone, a next-generation prokinetic that aims to improve cardiac safety.

Key Report Takeaways

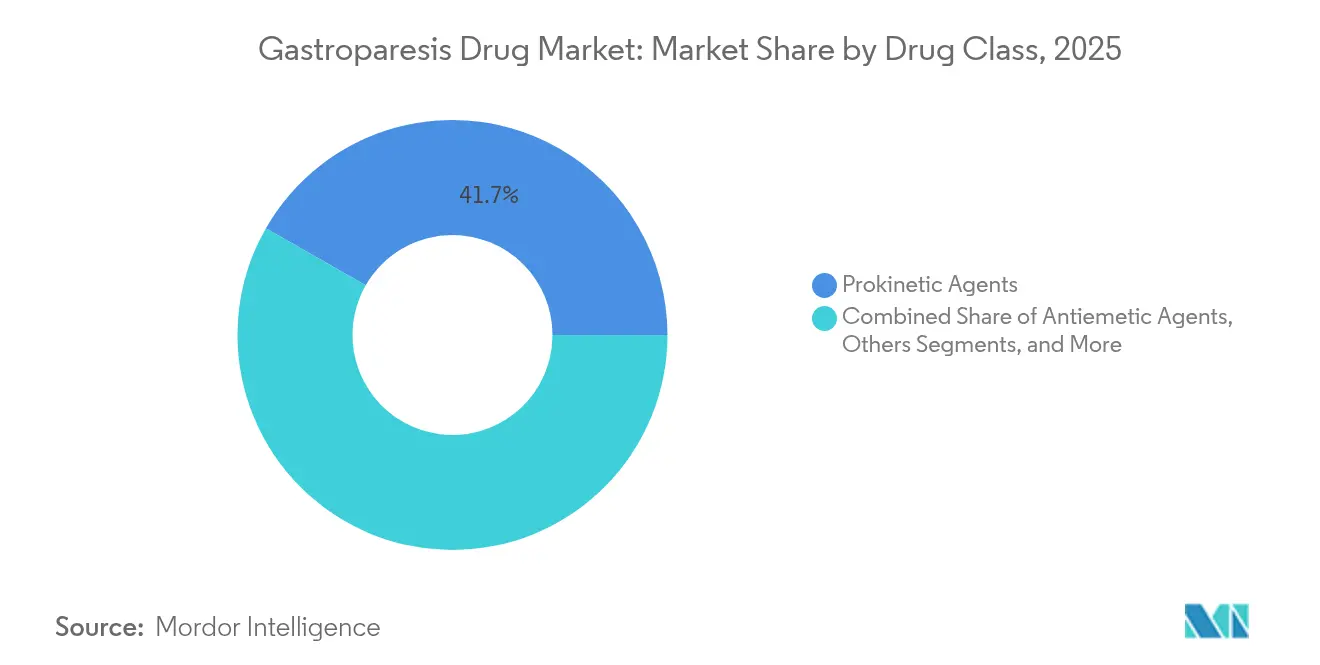

- By drug class, prokinetics led with 41.73% revenue share in 2025; botulinum toxin injections are forecast to advance at a 5.05% CAGR to 2031.

- By disease type, diabetic gastroparesis held 59.55% of the gastroparesis drugs market share in 2025, while post-surgical cases are expected to expand at a 5.62% CAGR through 2031.

- By end user, hospitals accounted for 47.55% of the gastroparesis drugs market size in 2025, and pharmacies are projected to grow at 5.95% CAGR between 2026 and 2031.

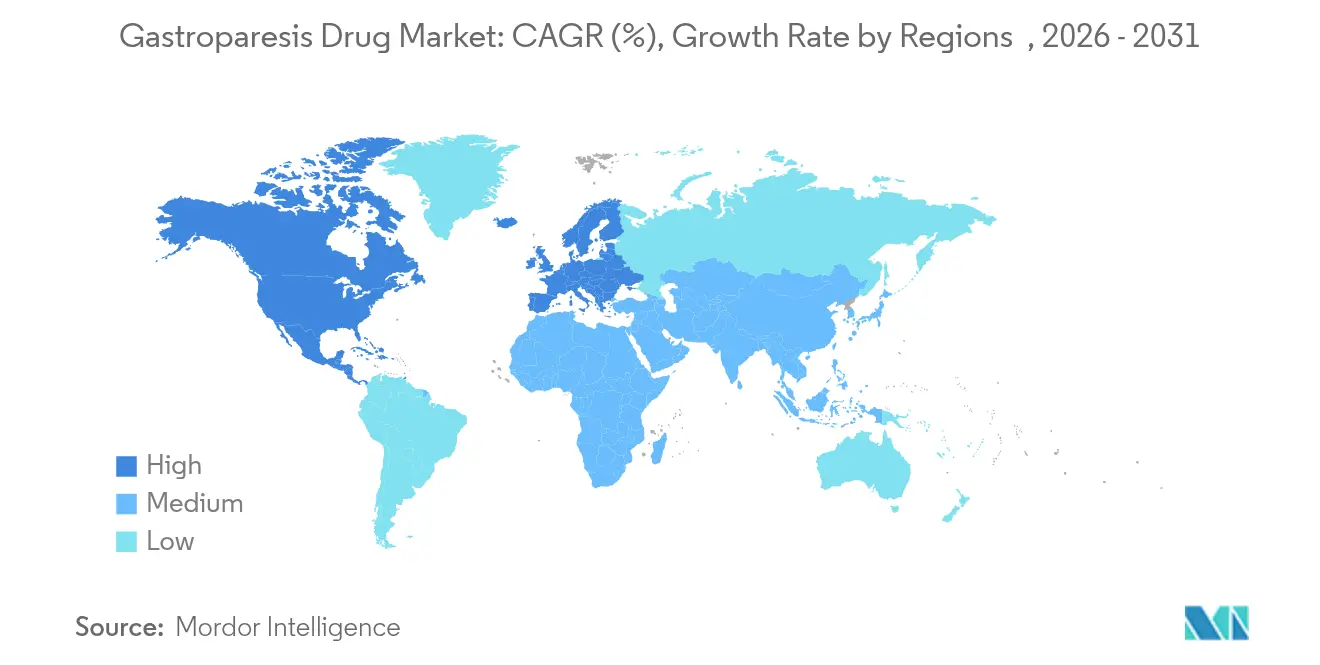

- By geography, North America captured 43.22% revenue share in 2025; Asia-Pacific is set to post the fastest 6.18% CAGR during the forecast period.

- Evoke Pharma, Renexxion, and CinDome Pharma together controlled a combined 18% of prescription sales in 2024, illustrating a moderately consolidated competitive field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gastroparesis Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of diabetes | +1.2% | Global, strongest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Increase in gastric and bariatric surgeries | +0.8% | North America and Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Growing geriatric population | +0.6% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| New approvals of novel prokinetics | +0.9% | North America and Europe first, global rollout | Short term (≤ 2 years) |

| Adoption of gastric electrical stimulators | +0.4% | North America and Europe | Medium term (2-4 years) |

| Expansion of home-based enteral nutrition | +0.3% | Developed markets with mature home care models | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Diabetes

Diabetes is the single largest demand catalyst for gastroparesis interventions, with diabetic cases making up 60.25% of all diagnoses in 2024 [1]Philip D. Chen, “Global Burden of Diabetes-Related Gastroparesis,” Nature Medicine, nature.com. Meta-analysis data place gastroparesis prevalence at 12.5% among adults with type 2 diabetes and 8.3% in type 1 diabetes cohorts. Epidemiological work from Pakistan and Palestine reports symptom rates of 11.5% and 14.5% respectively, underscoring under-recognition in emerging markets. Earlier disease onset means longer treatment duration, increasing lifetime value per patient for drug developers. In parallel, GLP-1 agonist prescriptions, although valuable for glycemic control, can aggravate gastric emptying and create incremental therapy needs.

Increase in Gastric & Bariatric Surgeries

The number of bariatric surgeries is climbing, and post-surgical gastroparesis represents the fastest growing disease sub-segment at 5.81% CAGR to 2030. Roux-en-Y procedures carry higher risk versus sleeve gastrectomy, sharpening the focus on prophylactic and early intervention regimens. Gastric peroral endoscopic myotomy (G-POEM) adds a minimally invasive option, shifting care models toward procedure-drug combinations that command premium pricing.

Growing Geriatric Population

People aged 65 years and older exhibit slower gastric motility, polypharmacy, and higher diabetes rates, creating a distinct phenotype that often requires dose adjustments and careful monitoring. Prevalence studies show rates above 15% in elderly diabetic cohorts, intensifying the need for safer long-term treatments. Hospitals and home-health programs are therefore broadening multidisciplinary support services, integrating nutritional counseling with prokinetic therapy.

New Approvals of Novel Prokinetics

Drug developers are focusing on selective receptor targeting to improve safety. Naronapride received FDA IND clearance in 2024 and is in Phase 2b trials showing favorable cardiac profiles versus legacy agents. Deudomperidone, which applies deuterium chemistry to enhance pharmacokinetics, secured new funding for pivotal studies in 2024. Regulatory agencies have classified gastroparesis as an unmet need, allowing fast-track reviews for candidates that document clear QT-interval advantages over standard drugs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy regulatory approval timelines | -0.7% | Global, most pronounced in North America & Europe | Long term (≥ 4 years) |

| Adverse effects & product withdrawals | -0.5% | Global, with regional variations in risk tolerance | Medium term (2-4 years) |

| Shift toward cannabinoid & herbal alternatives | -0.3% | North America & Europe, limited Asia-Pacific adoption | Medium term (2-4 years) |

| Limited reimbursement for idiopathic cases | -0.4% | North America & Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Regulatory Approval Timelines

Gastroparesis trials face high placebo response and subjective endpoints, complicating proof-of-efficacy. The FDA’s 2024 refusal of tradipitant after an extended review period demonstrates unpredictability in the approval path [2]Office of the Federal Register, “Drug Approvals in Gastrointestinal Disorders,” federalregister.gov. The EMA imposes additional pediatric data demands, stretching development budgets and discouraging smaller biotech entrants.

Adverse Effects & Product Withdrawals

Historical withdrawals of cisapride and restrictions on domperidone have left regulators cautious. Metoclopramide carries a black-box warning for tardive dyskinesia, limiting chronic use. Safety issues remain top of mind because gastroparesis patients often need prolonged therapy and frequently take several other drugs, amplifying risk for interactions and side effects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Prokinetics Maintain Primacy amid Safety Innovation

Prokinetics captured 41.73% of the gastroparesis drugs market in 2025 and continue to anchor first-line therapy despite legacy safety warnings. GIMOTI’s 126% prescription growth in 2024 shows that nasal delivery can revitalize established molecules. Deudomperidone and naronapride are positioned to lift the gastroparesis drugs market size for this class through safer receptor selectivity and improved absorption. Botulinum toxin injections, while holding a smaller base, are rising 5.05% per year as gastroenterologists refine endoscopic pyloric injection techniques, improving symptom relief durability.

Antiemetics such as ondansetron sustain demand for nausea control, while extended-release granisetron is gaining traction in peri-operative settings. The “Others” basket ranges from mirtazapine in refractory cases to ghrelin receptor agonists like TZP-102, which normalized gastric emptying in 52.6% of diabetic patients in a Phase 2 study. This pipeline diversification underscores a trend toward etiology-tailored regimens that combine motility agents with symptom modulators.

By Disease Type: Diabetic Dominance with Post-Surgical Upside

Diabetic gastroparesis accounted for 59.55% of cases and remains the primary revenue engine for the gastroparesis drugs market. However, the segment is complicated by wider GLP-1 agonist use, which may slow gastric emptying and heighten demand for rescue prokinetics. The gastroparesis drugs market share held by post-surgical presentations is small today yet expanding at a 5.62% CAGR as bariatric procedure volumes rise and clinicians implement structured follow-up protocols.

Idiopathic cases challenge standard care and spur research into inflammatory and neurogenic mechanisms. Viral and neurologic etiologies require nuanced approaches, including immunomodulators or neuroprotective agents. Medication-induced forms are becoming more visible in older adults on polypharmacy schedules, highlighting the need for drug-interaction-aware management pathways.

By End User: Hospitals Anchor Care while Pharmacies Expand

Hospitals held 47.55% of 2025 revenue thanks to diagnostic imaging, gastric scintigraphy, and implantable gastric stimulator procedures that remain inpatient tasks. The gastroparesis drugs market size tied to hospital utilization is set to grow steadily as combined device-drug regimens become common practice FDA. Specialty clinics are emerging centers of excellence, offering integrated dietary, psychological, and interventional services that shorten time to therapy optimization.

Pharmacies are projected to post 5.95% CAGR through 2031, reflecting broader chronic-care management, a rise in mailed specialty prescriptions, and home-based enteral nutrition that relies on pharmacy distribution channels . GIMOTI’s cold-chain handling and patient-education needs fit well with specialty pharmacy capabilities, creating an incremental driver for this channel.

Geography Analysis

North America accounted for 43.22% of 2025 revenue, anchored by large academic medical centers and favorable reimbursement for procedure-drug combinations. FDA designation of gastroparesis as an unmet medical need supports accelerated review for new entrants. The Cleveland Clinic reported 82% clinical response when combining gastric electrical stimulation with pyloromyotomy, reinforcing the region’s leadership in integrated care models. However, the tradipitant rejection shows that regulatory thresholds remain stringent.

Europe follows with a smaller but mature base. EMA guidelines and divergent national formularies lengthen rollout times, yet Germany showcases innovation through botanical combination therapy Iberogast Advance, supported by post-marketing data. Cross-border academic collaborations, such as Dr. Falk Pharma and Renexxion’s clinical partnership on naronapride, sustain a flow of late-stage assets. Professional societies, including the European Society of Neurogastroenterology and Motility, issue prescribing recommendations that shape clinical adoption.

Asia-Pacific is the fastest-growing region at 6.18% CAGR, propelled by high diabetes incidence, rapid urbanization, and expanding diagnostic capacity. Prevalence studies from Pakistan and Palestine highlight sizable undiagnosed populations, pointing to latent demand Cureus. Regulators in markets such as South Korea now grant reimbursement for new acid-suppressive agents that can be co-administered with prokinetics, signaling greater openness to novel gastrointestinal therapies. Pharmaceutical alliances, including the Lupin–Takeda tie-up for vonoprazan in India, illustrate the value multinationals place on regional partnerships to navigate pricing and distribution complexities.

Competitive Landscape

The gastroparesis drugs market features moderate concentration, with the top five suppliers controlling nearly 45% of prescription revenue in 2024. Evoke Pharma leveraged a differentiated nasal formulation to gain rapid uptake, achieving an annual run rate above USD 10 million within four years of launch. Renexxion focuses on dual-mechanism prokinetics, while CinDome Pharma applies deuterium chemistry to enhance cardiac safety. Each firm partners strategically for geographic reach: Renexxion with Dr. Falk in Europe and CinDome exploring out-licensing in Asia-Pacific.

Pipeline intensity is rising as investors recognize unmet need. Midsize firms and academic spin-outs concentrate on receptor-specific compounds, ghrelin agonists, and serotonin modulators that target distinct gastroparesis subtypes. Device makers are also entering the competitive mix; gastric electrical stimulator suppliers collaborate with drug developers to bundle procedural and pharmaceutical solutions, boosting switching costs for clinicians and payers.

Large multinationals participate selectively, often through licensing rather than internal R&D, preferring risk-managed exposure while monitoring safety outcomes from novel agents. This dynamic leaves room for nimble entrants to secure orphan indications, pediatric extensions, and real-world evidence packages that strengthen access negotiations with payers.

Global Gastroparesis Drug Industry Leaders

Evoke Pharma

AstraZeneca

Cadila Pharmaceuticals

Neurogastrx, Inc.

AbbVie Inc. ( Allergan Plc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Entero Therapeutics agreed to a reverse merger with Journey Therapeutics to form a Nasdaq-listed entity focused on gastrointestinal diseases, including capeserod for gastroparesis.

- September 2024: Lupin and Takeda partnered to commercialize vonoprazan in India, broadening the acid-disorder portfolio relevant to overlap cases of gastroparesis and reflux.

- May 2024: CinDome Pharma raised USD 40 million in Series B funding to advance deudomperidone clinical trials targeting diabetic gastroparesis.

- March 2024: Dr. Falk Pharma gained FDA IND clearance for naronapride, enabling United States studies of this selective prokinetic.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the gastroparesis drug market as all prescription and over-the-counter pharmacological agents that restore gastric motility or control nausea and vomiting in confirmed gastroparesis cases, served through hospital, retail, and online channels worldwide. Drug classes covered include prokinetic agents, dopamine and serotonin antagonists, macrolide antibiotics applied off label, and emerging ghrelin or motilin agonists.

Scope Exclusions: We exclude gastric electrical stimulation devices, surgical procedures, enteral feeding products, and dietary supplements.

Segmentation Overview

- By Drug Class

- Antiemetic Agents

- 5-HT3 Antagonists

- NK-1 Antagonists

- Dopamine Antagonists

- Prokinetic Agents

- Metoclopramide

- Domperidone

- Macrolide Antibiotics

- Ghrelin Receptor Agonists

- Botulinum Toxin Injections

- Others

- Antiemetic Agents

- By Disease Type

- Diabetic Gastroparesis

- Post-Surgical Gastroparesis

- Idiopathic Gastroparesis

- Viral & Neurological-Induced Gastroparesis

- Others

- By End User

- Hospitals

- Specialty Clinics

- Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We validate secondary cues through interviews with gastroenterologists, hospital pharmacists, and regional distributors across North America, Europe, Asia-Pacific, and the Gulf. These conversations refine patient pools, dose adherence, and price dispersion, enabling our team to adjust assumptions with on-ground realities before final modeling.

Desk Research

We begin by gathering prevalence and treatment data from public sources such as the International Diabetes Federation, the National Institute of Diabetes and Digestive and Kidney Diseases, Eurostat, and peer-reviewed journals like Gut. Regulatory filings (FDA Orange Book, EMA approvals) plus company 10-Ks supply launch timelines and average selling prices, while paid tools housed within Mordor Intelligence, including D&B Hoovers and Dow Jones Factiva, corroborate revenue splits. Trade bodies (American Gastroenterological Association), import trackers Volza for macrolides, and Questel patent analytics complement the dataset, letting us monitor pipeline momentum. The sources listed are illustrative, and many additional open and paid references feed data collection, validation, and clarification.

Market-Sizing & Forecasting

Mordor analysts apply a top-down prevalence-to-treated cohort build that converts global diabetic and idiopathic prevalence into addressable patients, then multiplies by therapy penetration and annualized dose cost. Supplier roll-ups of sampled ASP multiplied by volume act as a bottom-up cross-check. Key variables tracked include diabetic incidence trends, diagnosis rates, average daily dosing, therapy discontinuation, reimbursement shifts, and pipeline launch impact. A multivariate regression supported by ARIMA projects these inputs to 2030, while scenario analysis cushions regulatory or pricing shocks.

Data Validation & Update Cycle

Outputs face variance checks against hospital procurement logs, quarterly pharma filings, and customs data. Senior reviewers sign off once anomalies are resolved. We refresh the model annually, with interim updates triggered by major approvals or safety withdrawals, ensuring clients receive the latest view.

Why Mordor's Global Gastroparesis Drug Baseline Earns Trust

Published values differ because firms vary disorder coverage, currency dates, and refresh cadence, and we acknowledge those gaps up front. Key gap drivers include inclusion of device therapy by some publishers, reliance on constant global ASPs without regional discounts, limited primary validation, and less frequent model updates.

Mordor's disciplined scope and annual patient-based rebuild yield a balanced midpoint stakeholders can rely on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.03 B (2025) | Mordor Intelligence | |

| USD 6.63 B (2024) | Global Consultancy A | Includes device and nutritional therapies, single growth scenario |

| USD 5.90 B (2023) | Industry Journal B | Adds OTC antacid revenues, historic FX rates, minimal expert validation |

| USD 8.33 B (2025) | Regional Consultancy C | Blends wider gastric motility drugs, uses constant ASP escalation |

These comparisons show how scope breadth, base year, and validation depth swing headline figures. Mordor Intelligence anchors its estimate in clearly defined drug classes, validated patient pools, and annually refreshed inputs, delivering a dependable baseline for strategic planning.

Key Questions Answered in the Report

What is the current Global Gastroparesis Drug Market size?

The gastroparesis drugs market size reached USD 5.25 billion in 2026.

Who are the key players in Global Gastroparesis Drug Market?

Evoke Pharma, AstraZeneca, Cadila Pharmaceuticals, Neurogastrx, Inc. and AbbVie Inc. ( Allergan Plc) are the major companies operating in the Global Gastroparesis Drug Market.

Why is Asia-Pacific the fastest-growing region?

A surge in diabetes prevalence and expanding diagnostic capacity are driving a 6.18% CAGR in Asia-Pacific through 2031.

Which drug class leads the gastroparesis drugs market?

Prokinetic agents led with a 41.73% share in 2025 due to their direct effect on gastric motility.

Page last updated on: