Gas Insulated Substation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 37.51 Billion |

| Market Size (2031) | USD 55.55 Billion |

| Growth Rate (2026 - 2031) | 8.17% CAGR |

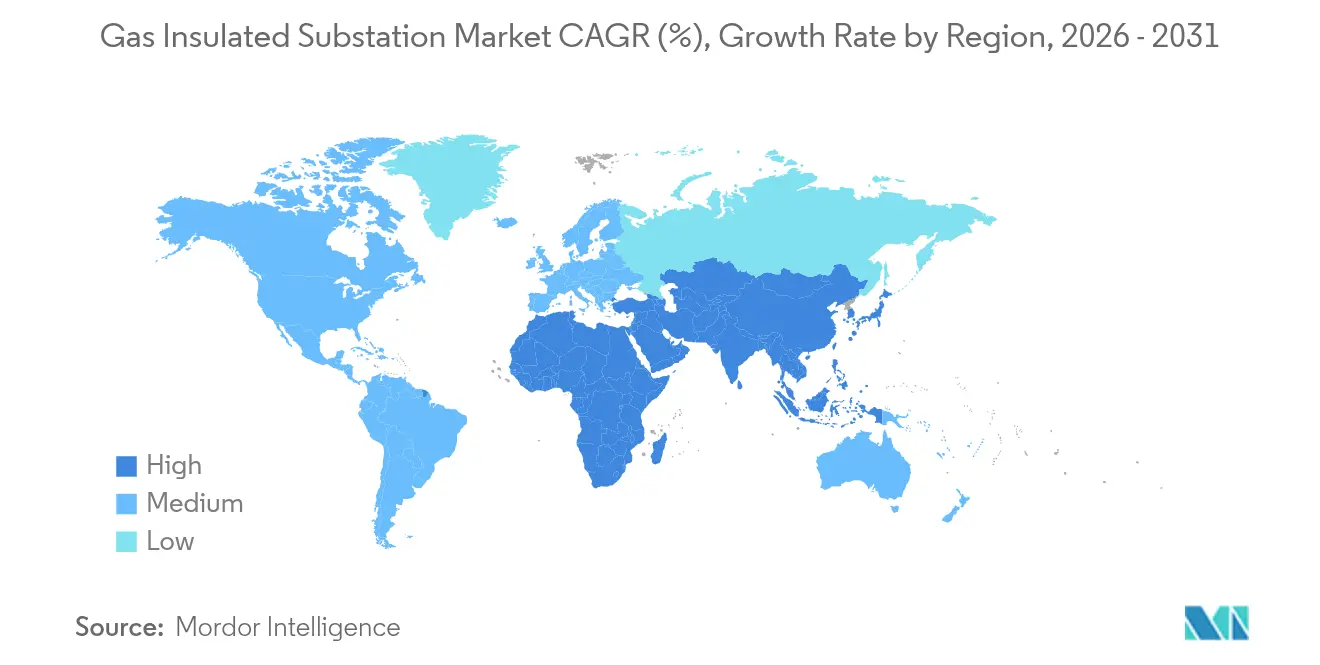

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gas Insulated Substation Market Analysis by Mordor Intelligence

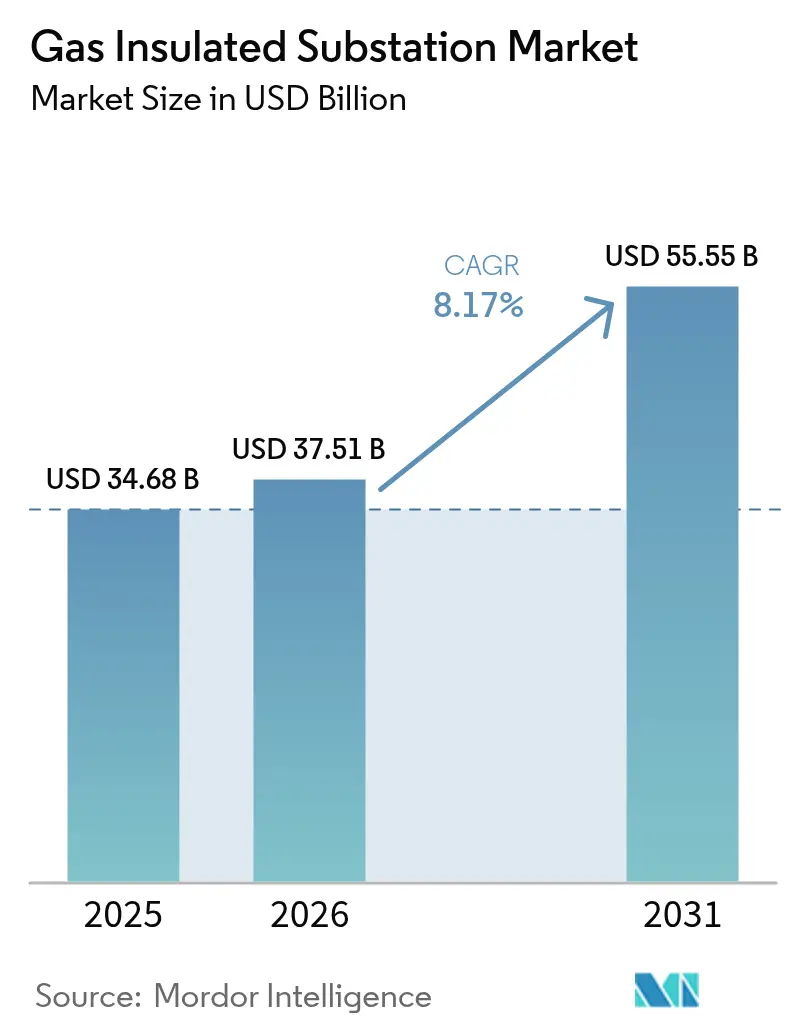

The Gas Insulated Substation Market size was valued at USD 34.68 billion in 2025 and estimated to grow from USD 37.51 billion in 2026 to reach USD 55.55 billion by 2031, at a CAGR of 8.17% during the forecast period (2026-2031).

Accelerating urbanization, large-scale renewable integration, and widespread replacement of aging air-insulated assets keep demand on an upward curve, while utilities elevate GIS adoption to balance compact footprints with heightened reliability requirements. Regulatory deadlines that phase out SF₆ in California by 2033 and across the European Union in 2030-2032 are reshaping technology choices, creating both disruption and new commercial openings. The Asia-Pacific region retains its position as the largest demand center, supported by a record USD 89 billion in grid spending by China’s State Grid Corporation in 2024. High Voltage (72.5–245 kV) systems account for just over half of global installations, yet the Extra-High-Voltage class above 300 kV is expanding faster as transmission operators build long-distance corridors for variable renewable power. At the same time, the share of mobile and skid-mounted units is rising because utilities need equipment that can be assembled off-site and energized within days for disaster recovery and planned maintenance scenarios

Key Report Takeaways

- By voltage, High-Voltage systems led with 51.90% share of the Gas Insulated Substation market size in 2025; Extra-High-Voltage applications are projected to expand at a 10.15% CAGR through 2031.

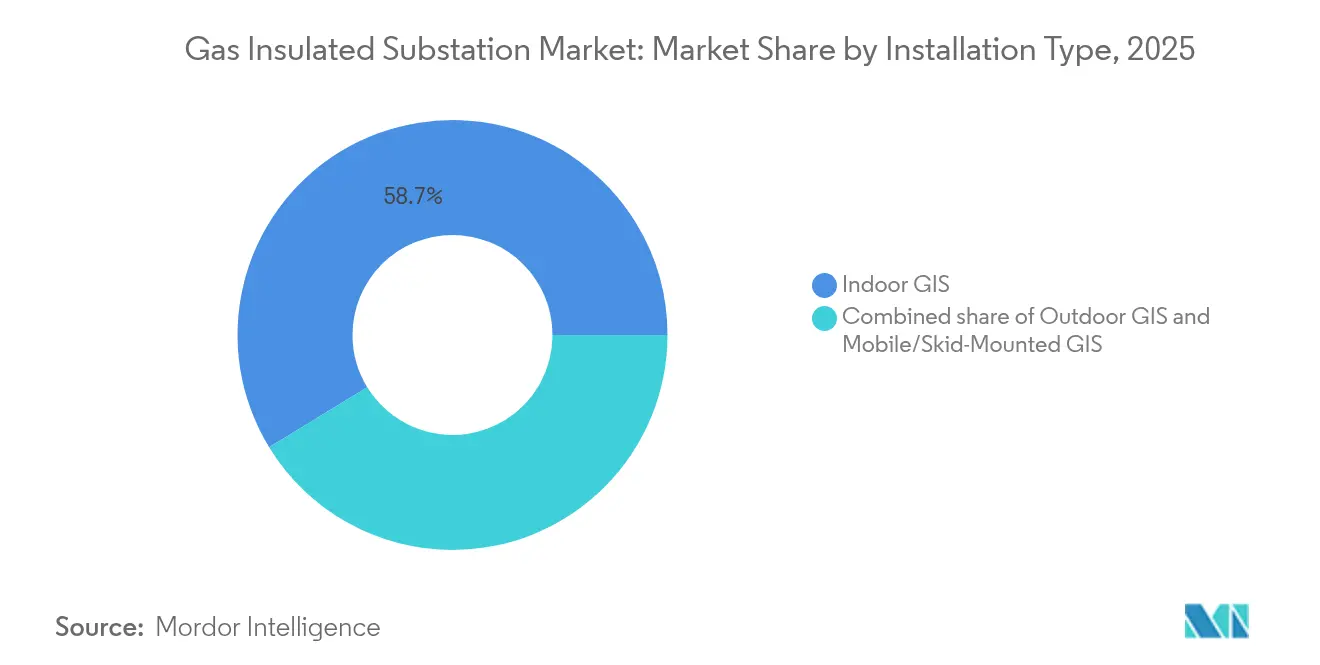

- By installation type, Indoor GIS dominated with a 58.74% share in 2025; Mobile and skid-mounted systems are forecast to grow at an 11.02% CAGR through 2031.

- By technology, SF₆-based switchgear retained 85.10% share in 2025; SF₆-free alternatives are advancing at a 18.65% CAGR to 2031.

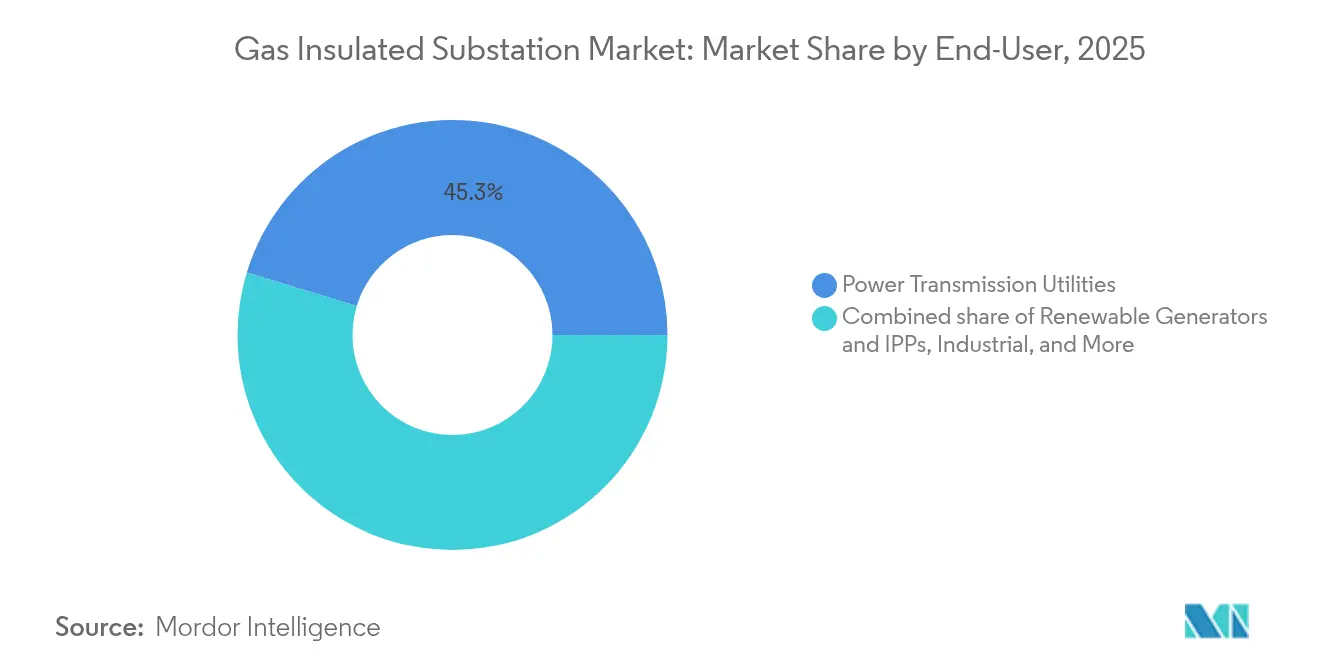

- By end-user, Power Transmission Utilities commanded a 45.30% share in 2025; Renewable Generators and Independent Power Producers are poised to grow at a 12.14% CAGR to 2031.

- By geography, the Asia-Pacific region accounted for 46.70% of the gas-insulated substation market share in 2025; it is anticipated to rise at a 9.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gas Insulated Substation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban land-use constraints propel compact GIS adoption | 2.20% | Global, concentrated in Asian megacities and European capitals | Medium term (2-4 years) |

| Renewable integration demands reliable HV infrastructure | 1.80% | North America, EU offshore wind hubs, APAC solar belts | Long term (≥ 4 years) |

| Modernization of aging AIS fleets in OECD countries | 2.10% | North America and EU, spillover into developed APAC | Long term (≥ 4 years) |

| Grid-upgrade programs in APAC & North America | 1.50% | APAC core markets and U.S. transmission corridors | Medium term (2-4 years) |

| Offshore wind & floating solar electrification needs | 0.90% | North Sea, U.S. East Coast, Japan, Netherlands, Singapore | Long term (≥ 4 years) |

| Climate-resilient substation designs for disaster zones | 0.80% | Hurricane-prone U.S. Gulf, typhoon-hit APAC, global flood plains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Land-Use Constraints Propel Compact GIS Adoption

Dense metropolitan growth leaves utilities scrambling for real estate, and gas-insulated substation market participants respond by delivering installations that occupy roughly 60% less space than air-insulated equivalents[1]Eaton, “Technical Comparison of Gas and Air-Insulated Substations,” eaton.com. Singapore’s 230 kV underground “figure-eight” GIS, developed by SP Group, demonstrates how vertically stacked layouts preserve surface land without compromising grid capacity[2]T&D World Editors, “Singapore’s Underground Substation Breaks Ground,” tdworld.com. Similar logic drove the construction of Cambridge, Massachusetts’ fully underground substation, which supports a life-sciences campus where premium surface space was repurposed for community amenities. These projects demonstrate how the Gas Insulated Substation market aligns with emerging urban master plans that favor mixed-use zoning over large utility corridors. As real estate values climb, major Asian and European cities are increasingly stipulating compact GIS for new or replacement substations, turning space savings into a quantifiable economic benefit.

Renewable Integration Demands Reliable HV Infrastructure

Variable generation from offshore wind and utility-scale solar introduces power-flow swings that require fast-acting, high-voltage equipment for reactive compensation and fault isolation. Floating wind platforms off the Fukushima coast employ gas-insulated switchgear rated for dynamic motion and salt-spray exposure, proving GIS viability in maritime conditions.[3]DNV, “Floating Offshore Substations: State of the Art,” dnv.com Massive ground-mounted solar clusters in Louisiana integrate collector substations equipped with GIS to maintain grid code compliance during irradiance fluctuations. In parallel, the World Bank identifies 400 GWp in floating-solar potential, a figure that points toward future demand for marine-grade substations.[4]World Bank Group, “Where Sun Meets Water,” worldbank.org Collectively, these deployments reposition the Gas Insulated Substation market from a space-saving niche toward a reliability backbone for renewables-heavy grids.

Modernization of Aging AIS Fleets in OECD Countries

Air-insulated switchgear, commissioned in the 1970s and 1980s, is nearing the end of its life across North America and Europe, prompting utilities to opt for GIS during refurbishment cycles. Pacific Gas & Electric has already halved its operational SF₆ inventory while swapping aging units for dry-air and vacuum-based alternatives that come packaged as compact GIS. A Southern California refinery’s 10-year program replaces 50-year-old substations with modern GIS layouts that embed advanced safety clearances on smaller footprints. As retired engineers take decades of AIS expertise with them, utilities accelerate migrations to low-maintenance GIS designs, thereby extending service intervals and simplifying workforce training.

Grid-Upgrade Programs in APAC & North America

Public-sector stimulus drives multiyear procurement pipelines. The U.S. Department of Energy’s USD 2.2 billion Grid Resilience and Innovation Partnerships grants champion 18 state-wide projects, many of which specify factory-assembled GIS for rapid energization. National Grid commits USD 35 billion between 2024 and 2028 to reinforce the Northeastern U.S. corridors, where high humidity and extreme temperatures favor sealed-gas equipment. Parallel initiatives in India, Indonesia, and the Philippines channel concessional finance into transmission build-outs, cementing Asia-Pacific’s lead in the Gas Insulated Substation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX versus AIS alternatives | -1.20% | Global, most acute in cost-sensitive emerging markets | Short term (≤ 2 years) |

| SF₆ phase-out regulations increase compliance costs | -0.70% | EU, California, Massachusetts and pending jurisdictions | Medium term (2-4 years) |

| Long lead-times for critical GIS components | -0.50% | Global supply chain, clustered in APAC factories | Short term (≤ 2 years) |

| Talent gap for SF₆-free technology commissioning | -0.40% | OECD grids with senior workforce retiring, emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX Versus AIS Alternatives

The Gas-Insulated Substation market still competes with lower-cost air-insulated designs, and project quotations often show a 5-30% premium, depending on voltage, enclosure type, and seismic requirements. However, lifecycle models reveal that reduced maintenance offsets initial capital; budget-constrained utilities in Latin America and parts of Africa continue to select AIS for straightforward rural applications. The European Commission confirms that SF₆-free GIS technologies add a further 5-30% to base prices, reinforcing cost sensitivity until volumes scale and manufacturing learning curves kick in. Procurement officers, therefore, conduct exhaustive total-cost-of-ownership analyses that incorporate carbon levies, leakage penalties, and land-purchasing costs before authorizing GIS expenditure.

SF₆ Phase-Out Regulations Increase Compliance Costs

California bars new SF₆-filled gear from 2033 onward, and Massachusetts enforces a 1% annual leak ceiling, obligating utilities to calibrate densimeters, overhaul seals, and maintain inventory tracking software. The EU’s updated F-gas regulation introduces quota auctions, which increase equipment prices because OEMs must purchase allowances if they continue to sell SF₆ variants. New York’s draft rule proposes scaling leakage baselines down 5% every five years after 2035, an approach that shifts the capital budget forward as operators accelerate fleet replacement. These frameworks require utilities to allocate compliance line items across multi-year rate cases, temporarily reducing order volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: Extra-High-Voltage Systems Anchor Backbone Expansion

Extra-high-voltage installations above 300 kV are growing at a 10.15% CAGR, a figure that surpasses the overall Gas Insulated Substation market CAGR as grid planners bring bulk renewable power from remote deserts and offshore zones to demand centers. The class enjoys regulatory backing because its low line-loss profile aligns with national efficiency mandates, and operators value GIS for its sealed architecture, which preserves dielectric integrity at altitude and in corrosive coastal air. High-Voltage systems, which held 51.90% of the Gas Insulated Substation market share in 2025, remain the workhorse for regional networks, sub-transmission rings, and heavy-industry feeders.

Hitachi Energy’s delivery of the first SF₆-free 550 kV GIS to State Grid marks the removal of the last technical barrier to eco-efficient systems at the top of the voltage pyramid, signalling a pivot point where investment decisions can align sustainability with megavolt-class performance. Utilities in Europe and Japan are already piloting similar units to stay ahead of 2030 legislative cut-offs, and North American operators are watching closely to evaluate lifespan economics. Medium-Voltage GIS below 72.5 kV continues to penetrate space-constrained distribution nodes where transformer substations must coexist with residential or commercial real estate.

By Installation Type: Mobility Adds Agility to Substation Strategy

Indoor halls account for 58.74% of the Gas Insulated Substation market, reflecting mature engineering standards and the prevalence of urban load centers that prioritize aesthetics and environmental control. However, mobile and skid-mounted packages, growing at 11.02% CAGR, illustrate how the Gas Insulated Substation market values agility during extreme-weather recovery, festival or event electrification, and planned equipment outages. Integrating breaker, disconnector, and control cubicles inside a single ISO container enables energization within one week, an advantage that outweighs the rental premium in outage cost calculations.

Midwest Energy’s first factory-assembled skid reduced field construction from six months to 30 days, shrinking labor exposure and simplifying permitting because the design qualifies as temporary equipment. Oil-rich Gulf nations are increasingly adopting trailer-mounted GIS systems to maintain power during refinery turnarounds, thereby avoiding multimillion-dollar penalties associated with unplanned downtime. These examples demonstrate how mobility shifts substation planning from static infrastructure toward an operational toolkit that utilities can reposition as system conditions dictate.

By Technology: SF₆-Free Solutions Move Toward Commercial Maturity

SF₆-based equipment still delivers proven arc-quenching performance and commands 85.10% of 2025 shipments. Yet utilities face intensifying regulatory pressure and reputational risk because each kilogram of leaked SF₆ warms the planet 25,200 times more than CO₂ over a 100-year period. The Gas Insulated Substation market therefore sees a 18.65% CAGR surge in clean-air, vacuum, and fluoronitrile blends that replicate dielectric strength while cutting greenhouse-gas footprint by 99% or more. Early adopters gain carbon-accounting credits and avoid future retrofit charges, which increasingly influence cost-benefit analyses in boardrooms.

General Electric’s 420 kV g³ breaker meets IEC short-circuit and switch-duty requirements without SF₆, proving that eco-efficiency no longer stops at distribution levels. Siemens Energy’s Clean Air units eliminate the need for gas-handling licenses because the mixture consists of purified, filtered ambient air, thereby lowering health and safety administrative overhead. Over 30 European and Korean utilities have issued framework contracts for these alternatives, providing a volume that should push unit costs closer to those of incumbent technology by 2028.

By End-User: Renewable Generators Reshape Procurement Patterns

Power Transmission Utilities hold 45.30% of end-user demand due to their statutory obligation to maintain national grids in a balanced and resilient state. Yet Renewable Generators and Independent Power Producers are the fastest-growing cohort, with a 12.14% CAGR, propelled by record solar and wind project pipelines that require collector, inter-array, and converter stations to be built on compressed schedules. Large developers prefer turnkey GIS because factory-tested modules reduce interface risk when multiple EPC consortia share a single site.

Industrial customers—such as chemicals, metals, and oil & gas—continue to source GIS for brownfield plant revamps where clearance envelopes are restricted and ambient particulates pose reliability hazards. Distribution utilities, especially in Southeast Asia, mix AIS and GIS depending on district density, often opting for hybrid substations where gas-insulated switchgear feeds overhead lines, thereby optimizing land use without compromising operational familiarity. The Gas Insulated Substation market thus mirrors broader decentralization trends, with procurement now spanning megawatt-scale rooftop solar exporters to gigawatt-class interconnectors.

Geography Analysis

The Asia-Pacific region, which accounted for 46.70% of 2025 revenue, is expected to sustain a 9.47% CAGR through 2031 as China and India develop ultra-high-voltage corridors from renewable-rich hinterlands to coastal load hubs. State Grid’s USD 89 billion outlay underwrites ±1,100 kV DC and 1,000 kV AC schemes where sealed-gas enclosures maintain dielectric strength at altitude, mitigating corona losses that plague open-air busbars. Concurrently, Southern Power Grid’s 2024-2027 budget of USD 195.3 billion emphasizes digital twin diagnostics for substation fleets, accelerating demand for smart-sensor-ready GIS bays. Japan’s floating offshore substation serves as a regional lighthouse project, while ASEAN governments unlock concessional financing for solar and storage hybrids, each requiring compact collector hubs that integrate smoothly with urban load pockets.

North America leverages policy catalysts, such as the DOE’s Grid Resilience grants, which funnel USD 2.2 billion into hardware upgrades that specify Gas Insulated Substation market equipment with embedded digital monitoring. National Grid’s USD 35 billion plan encompasses 70 transmission enhancements, spanning from upstate New York to eastern Massachusetts, each engineered for weatherproof operation during prolonged heatwaves and ice storms. California’s binding SF₆ sunset prompts utilities like PG&E to standardize eco-efficient GIS, anchoring a procurement cycle likely to ripple across the West and into Canada as carbon-price convergence tightens. Supply-chain snarls for transformers remain a headwind; however, multi-year frameworks help OEMs justify capacity expansions in Texas and Mexico.

Europe channels a EUR 584 billion grid investment target into cross-border interconnectors and offshore wind hubs, enforcing tight environmental criteria that automatically elevate demand for SF₆-free devices. Germany’s TransnetBW swaps 26 bays at the Daxlanden site for Siemens Clean Air panels by 2029, while Norway’s BKK Nett locks in a six-year framework for similar replacements. Scandinavia’s wind cluster drives specialized marine GIS procurement for jacket-foundation substations, and the Iberian Peninsula’s solar surge calls for desert-rated enclosures that handle dust-laden airflow. Although the regulatory environment incurs short-term costs, it also provides a predictable runway for OEM R&D investments aligned with net-zero goals.

Competitive Landscape

Traditional titans—ABB, Siemens, and Hitachi Energy—still anchor the Gas Insulated Substation market, leveraging global service networks, in-house sensor ecosystems, and vertically integrated manufacturing lines that stretch from breaker drives to digital relays. Their combined footprint grants volume economies, allowing them to match local currency tenders without compromising engineered-to-order capabilities. Yet the competitive calculus is evolving as eco-efficiency migrates from a marketing slogan to an entry ticket for regulated utilities in Europe and several U.S. states. General Electric’s g³ portfolio, for example, is now qualified by more than 30 utilities, illustrating how first-mover advantage in SF₆-free solutions converts into purchase-order momentum.

Specialist suppliers seize white-space opportunities in mobile GIS and floating substations, domains where historical manufacturing lines cannot be simply repurposed. Nordic engineering firms collaborate with shipyards to certify enclosures under marine classification rules, while U.S. trailer fabricators partner with switchgear OEMs to deliver rapid-deployment units for FEMA-backed recovery efforts. Digital overlays further change the pecking order: cloud-based condition-monitoring platforms become tie-breakers in competitive bids, prompting incumbents to embed cybersecurity hardware roots-of-trust and edge analytics that comply with NERC CIP-013.

Price competition persists for conventional SF₆-filled panels in jurisdictions where phase-out timelines remain distant, and Chinese OEMs capitalize on volume leverage at home to discount export offers in Africa and Latin America. However, as more countries announce leak-rate penalties and carbon taxes, total-cost-of-ownership calculations tilt the balance toward eco-efficient lineups. Industry analysts therefore expect market concentration to erode slightly by 2030 as nimble technology entrants carve niches in regulatory-driven segments, even as incumbents preserve baseline revenue through service contracts and modernization programs.

Gas Insulated Substation Industry Leaders

ABB Ltd

Mitsubishi Electric Corporation

General Electric Company

Siemens AG

Hitachi Energy Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hitachi Energy delivered the world’s first SF₆-free 550 kV gas-insulated switchgear to China’s State Grid, marking a breakthrough in sustainable high-voltage technology and supporting national carbon-neutrality goals.

- February 2025: Siemens Energy has signed a six-year framework agreement with Norway’s Norgesnett for Clean Air-insulated switchgear, which is expected to avoid an estimated 1,200 tons of CO₂ over the lifecycle of the equipment.

- January 2025: General Electric unveiled the first 420 kV g³ circuit breaker for GIS applications, reducing its global-warming potential by over 99% compared to SF₆ units.

- August 2024: The U.S. Department of Energy awarded USD 2.2 billion to eight transmission and storage projects under its Grid Resilience and Innovation Partnerships program.

Global Gas Insulated Substation Market Report Scope

The gas insulated substation market report includes:

| Medium Voltage (Up to 72.5 kV) |

| High Voltage (72.5 to 245 kV) |

| Extra-High Voltage (Above 300 kV) |

| Indoor GIS |

| Outdoor GIS |

| Mobile/Skid-Mounted GIS |

| SF₆-based GIS |

| SF₆-free (g³, Clean-Air, Vacuum) GIS |

| Power Transmission Utilities |

| Power Distribution Utilities |

| Renewable Generators and IPPs |

| Industrial (Oil and Gas, Mining, Metals, Chemicals) |

| Commercial and Residential Buildings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Voltage | Medium Voltage (Up to 72.5 kV) | |

| High Voltage (72.5 to 245 kV) | ||

| Extra-High Voltage (Above 300 kV) | ||

| By Installation Type | Indoor GIS | |

| Outdoor GIS | ||

| Mobile/Skid-Mounted GIS | ||

| By Technology | SF₆-based GIS | |

| SF₆-free (g³, Clean-Air, Vacuum) GIS | ||

| By End-User | Power Transmission Utilities | |

| Power Distribution Utilities | ||

| Renewable Generators and IPPs | ||

| Industrial (Oil and Gas, Mining, Metals, Chemicals) | ||

| Commercial and Residential Buildings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Gas Insulated Substation market in 2026?

The Gas Insulated Substation market size is USD 37.51 billion in 2026, keeping pace with its 8.17% CAGR trajectory to 2031.

Which voltage class is expanding fastest?

Extra-High-Voltage GIS installations above 300 kV are growing at a 10.15% CAGR, the quickest among all voltage segments.

Why are utilities shifting toward SF₆-free switchgear?

SF₆-free switchgear eliminates a greenhouse gas with a 25,200-fold global-warming potential versus CO₂ and meets new bans in California (2033) and the EU (2030-2032).

What share does Asia-Pacific hold in global demand?

Asia-Pacific accounts for 46.70% of 2025 revenue and remains the dominant regional buyer through 2031.

How fast are mobile or skid-mounted GIS units growing?

Mobile and skid-mounted installations are advancing at an 11.02% CAGR as utilities prioritize rapid deployment and disaster recovery readiness.

Which companies lead in SF₆-free technology?

Hitachi Energy, Siemens Energy, and General Electric currently trailblaze SF₆-free offerings, each launching high-voltage products between 2024 and 2025.

Page last updated on: