Garage And Overhead Doors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.17 Billion |

| Market Size (2031) | USD 9.19 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

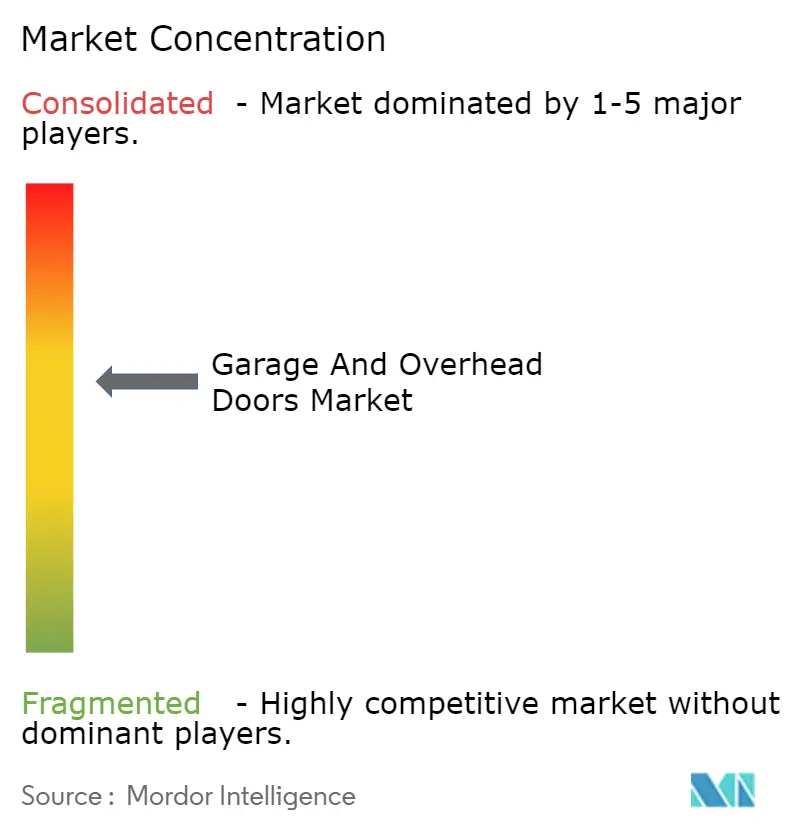

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Garage And Overhead Doors Market Analysis by Mordor Intelligence

The garage and overhead doors market size was valued at USD 6.82 billion in 2025 and estimated to grow from USD 7.17 billion in 2026 to reach USD 9.19 billion by 2031, at a CAGR of 5.10% during the forecast period (2026-2031). Growth rests on three pillars: a rebound in mid-tier-city construction, rising demand for connected access points that integrate with broader smart-home ecosystems, and e-commerce logistics facilities that require high-cycle, energy-efficient bay doors. Competitive behavior shows an uptick in vertical integration as manufacturers secure installation capacity and strengthen direct-to-consumer channels. Strategic opportunities concentrate around aluminum-glass hybrids, hurricane-rated doors, and software-driven service models that convert one-time hardware sales into recurring revenue.

Key Report Takeaways

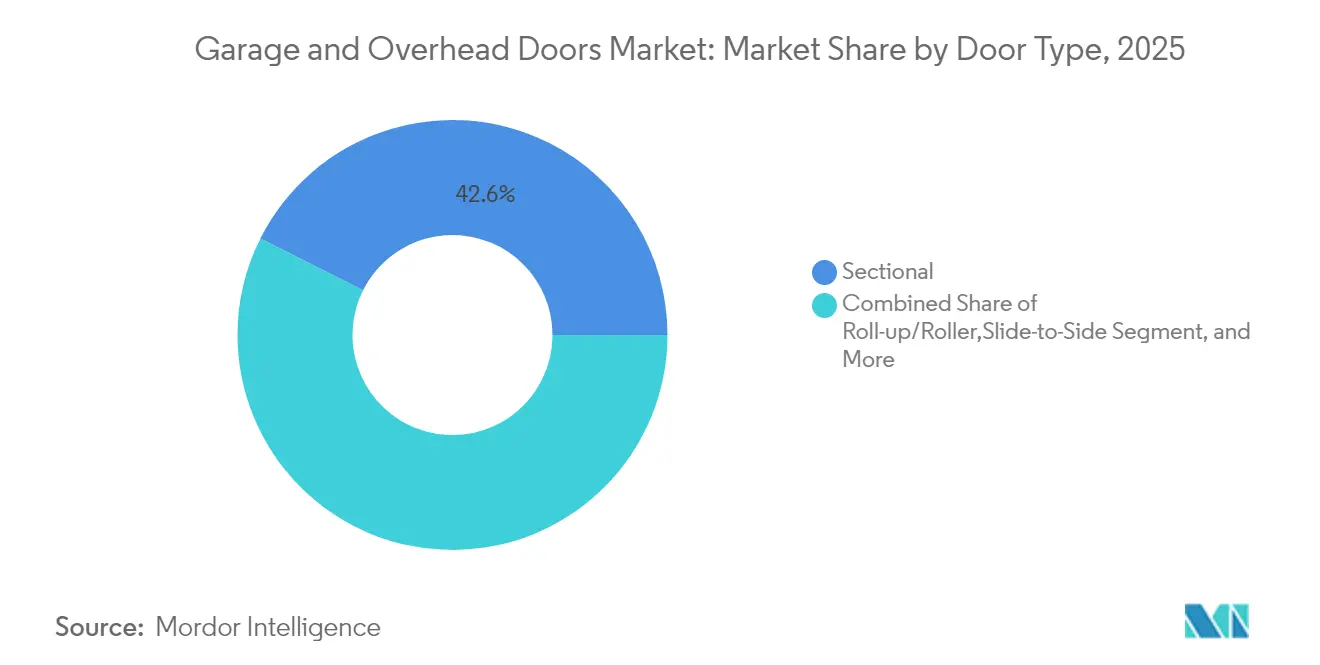

- By door type, sectional doors led with 42.60% of the garage and overhead doors market share in 2025, while roll-up designs are projected to expand at a 5.31% CAGR through 2031.

- By category, manual systems held 55.90% of the garage and overhead doors market size in 2025; automatic variants are growing at a 6.52% CAGR to 2031.

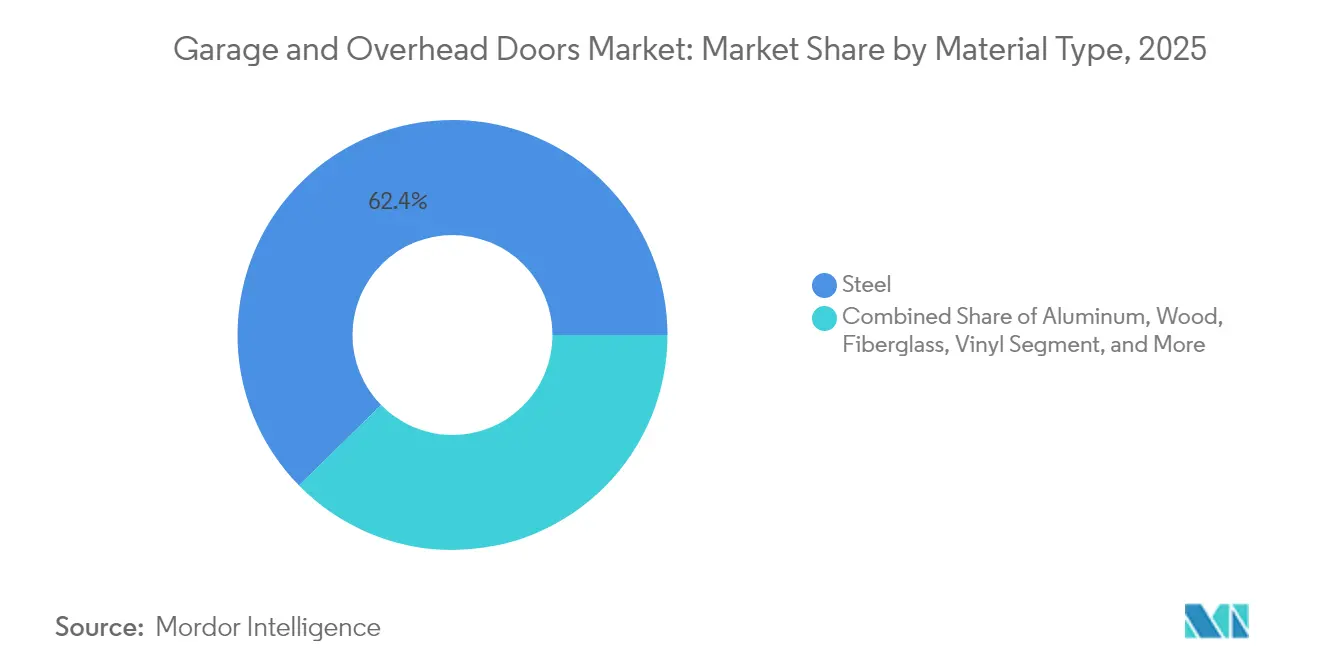

- By material, steel accounted for 62.35% of the garage and overhead doors market size in 2025; aluminum-glass hybrids are advancing at a 6.98% CAGR.

- By end-use, the residential segment commanded 67.35% of the garage and overhead doors market size in 2025, whereas commercial applications will post the fastest 7.39% CAGR.

- By distribution channel, installer‐contractor networks secured 50.40% share of the garage and overhead doors market size in 2025; e-commerce sales will climb at a 5.56% CAGR.

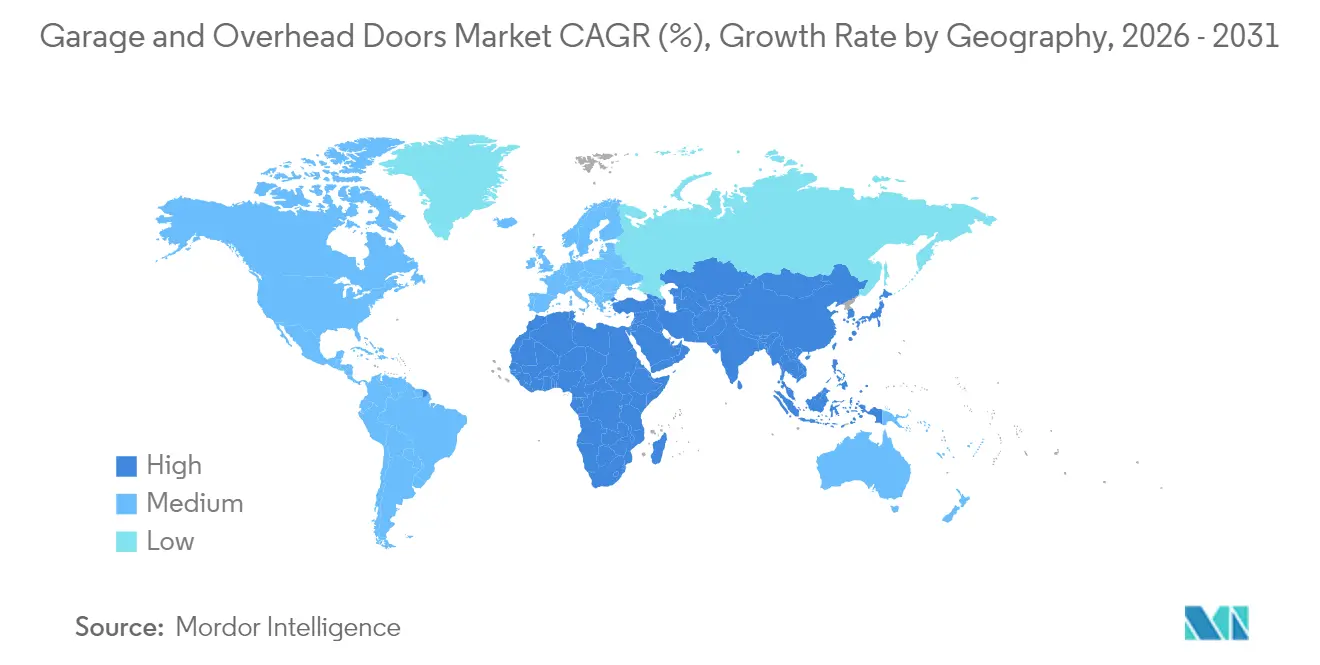

- By geography, North America dominated with 35.45% revenue share in 2025, while Asia Pacific is projected to log an 7.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Garage And Overhead Doors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction rebound in mid-tier cities | +1.2% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Smart-home-ready garage connectivity | +0.9% | Global (early uptake in North America, Europe) | Long term (≥4 years) |

| High-ROI remodeling and curb-appeal upgrades | +0.7% | North America, Europe | Short term (≤2 years) |

| E-commerce fulfillment bay-door demand | +0.6% | Global (focus in Asia Pacific, North America) | Medium term (2-4 years) |

| Insurance-mandated wind-load retrofits | +0.5% | North America coastal, Asia Pacific typhoon | Medium term (2-4 years) |

| Modular-housing integrated door modules | +0.3% | Europe, North America, emerging Asia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Construction rebound in mid-tier cities

During 2024, secondary urban centers in North America recorded sharper growth in new housing starts than major metropolitan areas, aided by remote-work migration and favorable land costs.[1]Minnesota Builders Exchange, “News,” mbex.org Door makers responded by opening regional warehouses that trim delivery times and freight costs. Municipal zoning updates such as St. Petersburg’s 2025 single-bay requirement have further lifted installations revize.com. The result is a distributed demand pattern that cushions the garage and overhead doors market against slowdowns in a single metro and encourages localized product mixes tailored to architectural guidelines.

Smart-home-ready garage connectivity

Connectivity features evolved in 2024 from optional add-ons to default purchase criteria. Systems now pair live video, biometric entry, geofencing, and predictive maintenance analytics in a single hub.[2]Door Master Clinic, “Garage Doors of the Future: Must-Have Smart Features,” doormasterclinic.comManufacturers with proprietary platforms capture subscription fees for software updates and cloud storage, insulating margins from raw-material swings. The capability repositioned a traditionally durable good into a technology refresh cycle, a trend expected to underpin the garage and overhead doors market through the decade.

E-commerce fulfillment bay-door demand

High-throughput fulfillment centers require doors rated for 100+ cycles per day, airtight seals, and rapid opening speeds. Operators differentiate between high-speed and high-performance doors depending on dock location, pushing suppliers to optimize both cycle life and energy performance.[3]Loading Dock, Inc., “Choosing Between High-Speed and High-Performance Commercial Doors,” loadingdock.comThis logistics boom led commercial buyers to pay premiums for engineered solutions, creating a defensible niche within the broader garage and overhead doors market.

Insurance-mandated hurricane / wind-load retrofits

Insurers tightened underwriting standards after recent wind disasters, forcing homeowners in coastal zones to install certified wind-load-rated doors. FEMA’s Marshall Fire report linked inadequate garage doors to structural failure, underscoring this requirement.[4]Federal Emergency Management Agency, “Marshall Fire MAT Report (P-2320),” fema.govCertified products earn 30–40% higher margins, and manufacturers with accredited testing win preferential listings, adding a steady revenue stream detached from normal replacement cycles

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel price volatility and tariffs | -0.8% | Global (higher in North America, Europe) | Short term (≤2 years) |

| Skilled-installer shortage | -0.4% | North America, Europe, emerging Asia | Medium term (2-4 years) |

| Counterfeit torsion-spring recalls | -0.3% | Global (emerging markets focus) | Short term (≤2 years) |

| Stricter fire-code limits for fiberglass | -0.2% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Steel price volatility and tariffs

Metal doors and windows logged a 17.7% price rise in early 2025, widening the gap between fixed-price contracts and actual input costs. Producers are adopting dynamic pricing clauses, diversifying toward aluminum-glass hybrids with steadier inputs, or acquiring steel-processing assets to lock in supply. Short-term margin pressure remains the key brake on the garage and overhead doors market until cost curves stabilize.

Skilled-installer shortage

An aging installer workforce and the added complexity of connected doors pushed installation labor rates upward, lifting average door prices 6% by April 2025. Manufacturers are simplifying hardware, investing in VR-based training, and acquiring service firms to guarantee field capacity. Until the labor pipeline recovers, the bottleneck tempers growth in the garage and overhead doors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Door Type: Sectional Dominance Meets Roll-up Momentum

Sectional doors captured 42.60% of the garage and overhead doors market in 2025, anchored by superior insulation and minimal headroom requirements. Their popularity spans residential and light commercial garages where temperature control and ceiling clearance matter. Innovation focuses on integrating thicker polyurethane cores and low-leakage seals, improvements that keep sectional doors at the center of retrofit spending. The garage and overhead doors market benefits from sectional doors’ broad SKU range that lets dealers serve entry-level price points and premium architectural demands.

Roll-up doors, projected to grow at a 5.31% CAGR to 2031, appeal to high-traffic commercial docks. Advances in tension systems, guide rails, and slat materials have closed historical durability gaps with sectional counterparts. Architects specify roll-ups to free interior ceiling space for hoists, lighting, or HVAC ducting. Interest is also rising in industrial freezer applications where rapid operation reduces air exchange. As adoption widens, the garage and overhead doors market gains a second growth engine that diversifies revenue away from mature sectional sales.

By Category: Automation Shifts Value Toward Software

Manual systems still accounted for 55.90% of revenue in 2025 because of lower upfront cost and mechanical simplicity. Demand remains sticky in entry housing and markets with low smart-home penetration. Nevertheless, automatic doors are forecast to register a 6.52% CAGR as consumers embrace remote monitoring and touchless entry. The garage and overhead doors market size for automatic doors already exceeds USD 3.01 billion, underscoring the speed of the transition.

Connectivity moves margin from hardware to cloud services. Vendors such as Clopay embed AI analytics that send users maintenance alerts and energy-use dashboards. Subscription plans unlock extended video storage or advanced access logs, creating annuity streams. Retailers leverage these features to upsell replacements earlier in the product life cycle. This business model evolution positions the garage and overhead doors market for stable, recurring income even when construction cycles soften.

By Material Type: Hybrids Redefine Aesthetics and Performance

Steel retained a 62.35% share in 2025 by balancing cost, strength, and wind resistance. Builders in hurricane zones rely on its structural capacity to meet stricter codes. However, demand for daylighting and modern façades pushed aluminum-glass hybrids to a 6.98% CAGR trajectory. The garage and overhead doors market size linked to aluminum-glass products is poised to double by 2031, driven by design-oriented commercial storefronts and high-end residences.

Clopay’s VertiStack Avante launch in March 2025 demonstrated that full-height glass panels can meet load requirements while illuminating interiors. Architects specify these hybrids to create seamless transitions between indoor and outdoor spaces, a trend mirrored in hospitality and mixed-use developments. Wood doors remain a niche luxury option, while vinyl gains share in coastal regions thanks to corrosion resistance. As codes grow stricter on thermal performance, composite solutions that combine steel skins with polyiso cores may enter mainstream use, adding another layer of diversification within the garage and overhead doors market.

By End-use: Commercial Growth Outpaces Residential Base

Residential projects represented 67.35% of total demand in 2025, reflecting a robust remodeling market valued at more than USD 600 billion in the United States alone. Homeowners view garage doors as a high-ROI exterior upgrade that improves energy efficiency and curb appeal simultaneously. Replacement cycles shorten when connectivity upgrades or aesthetic trends prompt earlier swaps. These factors keep the residential share dominant within the garage and overhead doors market, even as other segments accelerate.

Commercial installations, forecast to expand at 7.39% CAGR, hinge on e-commerce, cold-chain, and data center construction. Doors in these settings must endure high-frequency operation, integrate with facility management systems, and meet stricter air-infiltration targets. Industrial and agricultural demand is also rising as modern farm structures adopt climate-controlled designs to safeguard livestock and crops. These specialised requirements command higher average selling prices, lifting overall revenue for suppliers focused on the garage and overhead doors market.

By Distribution Channel: Contractors Retain Control as Digital Sales Rise

Installer-contractor networks held 50.40% share in 2025 because accurate measurement, code compliance, and safe spring balancing still require professional expertise. Dealers typically bundle product, installation, and after-sales service under a single invoice, reducing risk for property owners. This service-centric approach maintains loyalty and stabilises pricing, anchoring the garage and overhead doors market’s traditional route to market.

E-commerce, projected to post a 5.56% CAGR, is reshaping buyer behaviour as websites pair configurators with on-demand installation booking. Retail home centers leverage curbside pickup and virtual consults to blend physical and digital journeys. OEM webstores deepen customer insight through direct data capture while mitigating channel conflict by offering unique SKUs or add-on services online only. The net effect is a multichannel garage and overhead doors market where manufacturers must balance dealer relationships with consumer expectations for frictionless digital buying.

Geography Analysis

North America led with 35.45% of 2025 revenue thanks to active renovation, hurricane-proofing mandates, and high adoption of insulated doors. U.S. import investigations into Indian torsion springs underscore the region’s focus on supply-chain security and fair-value enforcement. Canadian demand leans toward high-R-value units, while Mexican growth benefits from near-shoring industrial builds. Collectively, the garage and overhead doors market in North America remains the benchmark for code stringency and premium product penetration.

Asia Pacific is the fastest-growing region, poised for an 7.86% CAGR. China’s steel door sector alone is projected to reach CNY 126.564 billion by 2028, reflecting steady urbanisation and logistics infrastructure. India follows with heavy investment in industrial parks and smart cities, while Japan and South Korea drive demand for advanced automatic systems aligned with energy guidelines. As income levels rise, first-time residential installations lift baseline volumes across ASEAN economies, solidifying Asia’s role as the growth nucleus for the garage and overhead doors market.

Europe presents a design-centric landscape shaped by stringent energy codes. Germany maintains leadership via engineering innovation, whereas the United Kingdom shows solid replacement demand amid constrained housing supply. Mediterranean nations favor aluminum and glass for daylighting. Economic uncertainty tempers new-build momentum, yet retrofit incentives keep the garage and overhead doors market resilient. Manufacturers compete through aesthetics, thermal performance, and heritage-compliant offerings rather than raw price.

Competitive Landscape

Market structure is moderately consolidated, with global producers leveraging scale in materials procurement and R&D while regional specialists exploit local codes and design preferences. Clopay, a Griffon subsidiary, produced USD 1.6 billion in 2024 revenue and USD 501 million in adjusted EBITDA, confirming its position as North America’s largest door maker. Overhead Door Corp. and Wayne Dalton strengthen portfolios through proprietary spring systems and smart controllers, while ASSA ABLOY accelerates M&A to capture adjacent access-control technologies.

Vertical integration into installation mitigates the skilled-labor bottleneck. For example, Wayne Dalton expanded its service center footprint in the U.S. Midwest to secure capacity and control customer experience. Concurrently, companies pursue material shifts such as aluminum-glass hybrids that lift average selling prices and differentiate portfolios. Intellectual-property investment focuses on low-leakage seals, advanced openers, and cloud control platforms that embed revenue beyond initial sale.

Regional challengers carve out share through niche innovations: Raynor addresses premium wood aesthetics, C.H.I. pushes modern overlay designs, and Zonle Doors scales domestic steel production in China. Competitive advantage hinges on code compliance evidence, lead-time reliability, and lifecycle cost analytics. Across these fronts, the garage and overhead doors market rewards suppliers that merge product performance with digital services and channel depth.

Garage And Overhead Doors Industry Leaders

Garaga Inc.

Richards-Wilcox

Wayne-Dalton

Upwardor Inc.

Croskill Overhead Doors Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The U.S. Department of Commerce issued a preliminary determination that overhead door counterbalance torsion springs from India are being sold in the United States at less than fair value, potentially leading to countervailing duties that could significantly impact supply chains and pricing for U.S. manufacturers reliant on imported components.

- March 2025: Clopay Corporation launched the VertiStack Avante aluminum and glass door, winning multiple industry awards for its innovative design that maximizes natural light transmission while maintaining structural integrity. The product represents a significant advancement in the aluminum-glass hybrid category that is projected to grow at 7.2% CAGR through 2030.

- March 2025: Raynor launched the Revival Wood Collection, expanding its premium residential product portfolio with authentic wood doors that target the high-end residential market segment. This launch reflects the company's strategic focus on diversifying its material offerings beyond traditional steel products.

- March 2025: ASSA ABLOY completed the acquisition of SKIDATA, an international provider of access management solutions, strengthening its position in the commercial and institutional segments with advanced access control technologies that complement its existing garage door offerings.

- January 2025: Clopay introduced the Thermiser Max - Low U insulated rolling door, designed specifically to meet increasingly stringent energy efficiency codes with industry-leading thermal performance. The door features advanced insulation technology that significantly reduces air infiltration, addressing a key concern in commercial applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the garage and overhead doors market as revenues generated from the sale of newly manufactured, vertically operating garage-style and industrial overhead doors installed at residential, commercial, industrial, and agricultural premises worldwide. According to Mordor Intelligence, values are expressed in constant 2024 US dollars and cover sectional, roll-up, slide-to-side, tilt-up, swing-out, and similar door formats that seal an exterior vehicle opening.

Scope Exclusions: After-sales service, door operators sold separately, and retrofit hardware kits are outside the present scope.

Segmentation Overview

- By Door Type

- Sectional

- Roll-up/Roller

- Slide-to-Side

- Side-Hinged

- Tilt-Up and Up-and-Over

- Swing-Out Carriage

- By Category (Auto-vs-Manual)

- Automatic

- Manual

- By Material Type

- Steel

- Aluminum

- Wood

- Fiberglass

- Vinyl

- Glass

- Composite/Hybrid

- By End-use

- Residential

- Commercial

- Industrial

- Agricultural/Farm

- By Distribution Channel

- OEM/Direct

- Installer/Contractor

- Retail (Home Centers)

- E-commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- South East Asia

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Desk Research

We started with construction and housing data drawn from public sources such as the US Census Bureau's Building Permits Survey, Eurostat's Production in Construction Index, UN Comtrade import-export codes for HS 730830 (metal doors), and the Japan Construction Industry Association. Trade association briefs from the Door and Access Systems Manufacturers Association, patent analytics accessed via Questel, and company revenue splits from D&B Hoovers added manufacturer-level context.

Next, installer price sheets, energy-efficiency studies in the Journal of Building Engineering, and regional customs filings helped us benchmark average selling prices and material mixes. The sources cited are illustrative; many additional databases, filings, and open datasets contributed to validation and clarification.

Primary Research

Mordor analysts interviewed door fabricators, regional distributors, and certified installers across North America, Europe, Asia-Pacific, and the Gulf to verify shipment volumes, replacement rates, smart-door uptake, and warranty claims.

Follow-up surveys with home-builder associations and warehouse facility managers helped us fine-tune channel splits and emerging automation trends.

Market-Sizing & Forecasting

A top-down build begins with new housing starts, commercial floor-space additions, and industrial capex, which are converted into door demand pools using region-specific penetration ratios. Results are cross-checked through selective bottom-up roll-ups of leading suppliers' shipments and sampled ASP × volume calculations, then adjusted where gaps arise. Key variables feeding the model include residential garage prevalence, average door replacement cycle, smart-door penetration, steel and aluminum price indices, and warehouse construction pipelines. Forecasts employ multivariate regression blended with scenario analysis so shifts in construction spending or raw-material costs reshape the outlook transparently.

Data Validation & Update Cycle

Every draft model passes anomaly checks, variance screens, and a double-analyst review. Before sign-off, outputs are compared with independent housing and industrial production trackers; material deviations trigger re-contact of sources. Reports refresh annually, with interim updates should tariffs, code changes, or major mergers materially alter market dynamics.

Why Mordor's Garage And Overhead Doors Baseline Commands Reliability

Published numbers often diverge because firms choose wider door families, apply uniform ASPs, or freeze exchange rates at different cut-offs. We acknowledge those realities upfront.

Key gap drivers include: some providers merge door panels with openers and security doors; others extrapolate value from broad construction outlays without material-level splits; several apply aggressive smart-home adoption curves or roll forward earlier currency assumptions, inflating totals versus Mordor's 2025 baseline of USD 6.82 billion that is anchored to verified shipment and pricing evidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.82 Bn (2025) | Mordor Intelligence | - |

| USD 7.57 Bn (2025) | Global Consultancy A | Includes basic openers and limited primary validation |

| USD 26.14 Bn (2025) | Tech Analytics Firm B | Bundles security, service, and regional door categories; relies mainly on macro construction spend |

| USD 25.25 Bn (2024) | Industry Portal C | Uses constant ASP uplift without adjusting for material mix or currency movements |

In short, Mordor's disciplined scope definition, mixed-method modeling, and yearly refresh cadence give decision-makers a balanced, transparent baseline that remains traceable to tangible variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the garage and overhead doors market?

The garage and overhead doors market stands at USD 7.17 billion in 2026 and is projected to reach USD 9.19 billion by 2031.

Which region leads global revenue?

North America led in 2025 with 35.45% share, driven by renovation activity and hurricane-resistant code mandates.

Which product segment is growing fastest?

Roll-up doors are forecast to expand at a 5.31% CAGR through 2031 on the back of commercial and industrial demand.

How are smart technologies influencing demand?

Smart-home-ready connectivity shortens replacement cycles and introduces subscription revenue, reinforcing long-term growth.

What material trend should suppliers watch?

Aluminum-glass hybrids are advancing at a 6.98% CAGR as buyers seek modern aesthetics and daylighting benefits.

Why is installation capacity a bottleneck?

An aging installer workforce and added complexity in connected doors pushed labor costs up 6% by April 2025, lengthening project timelines.

Page last updated on: