Fuel Cell UAV Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

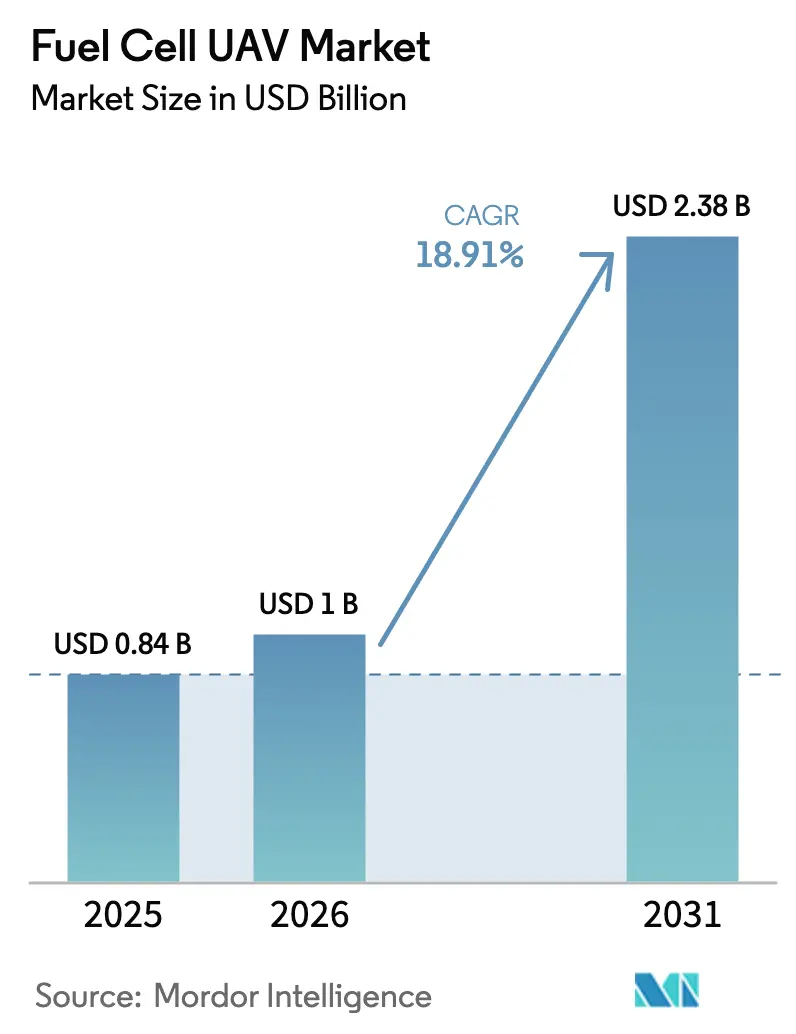

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 2.38 Billion |

| Growth Rate (2026 - 2031) | 18.91% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fuel Cell UAV Market Analysis by Mordor Intelligence

The fuel cell UAV market size is expected to grow from USD 0.84 billion in 2025 to USD 1.00 billion in 2026 and is forecasted to reach USD 2.38 billion by 2031 at 18.91% CAGR over 2026-2031. Growth rests on three pillars: the eight-to-thirteen-hour flight endurance that hydrogen propulsion routinely delivers, the acoustic stealth that shields missions from early detection, and the US Department of Defense’s (DoD's) pivot toward hydrogen-ready forward bases that slash greenhouse gas emissions. Falling PEM stack costs, which are expected to drop to USD 60 per kilowatt by 2025, further accelerate adoption. Platform developers now blend PEM and SOFC stacks to extend patrols beyond 24 hours, while on-site micro-refineries reduce the need for cylinder transport and mitigate logistical risk.[1]Source: Defense Innovation Unit, “HyTEC Program,” diu.mil Parallel regulatory action in Europe and Asia-Pacific smooths certification paths for 350-bar and 700-bar tanks, removing a historic bottleneck.

Key Report Takeaways

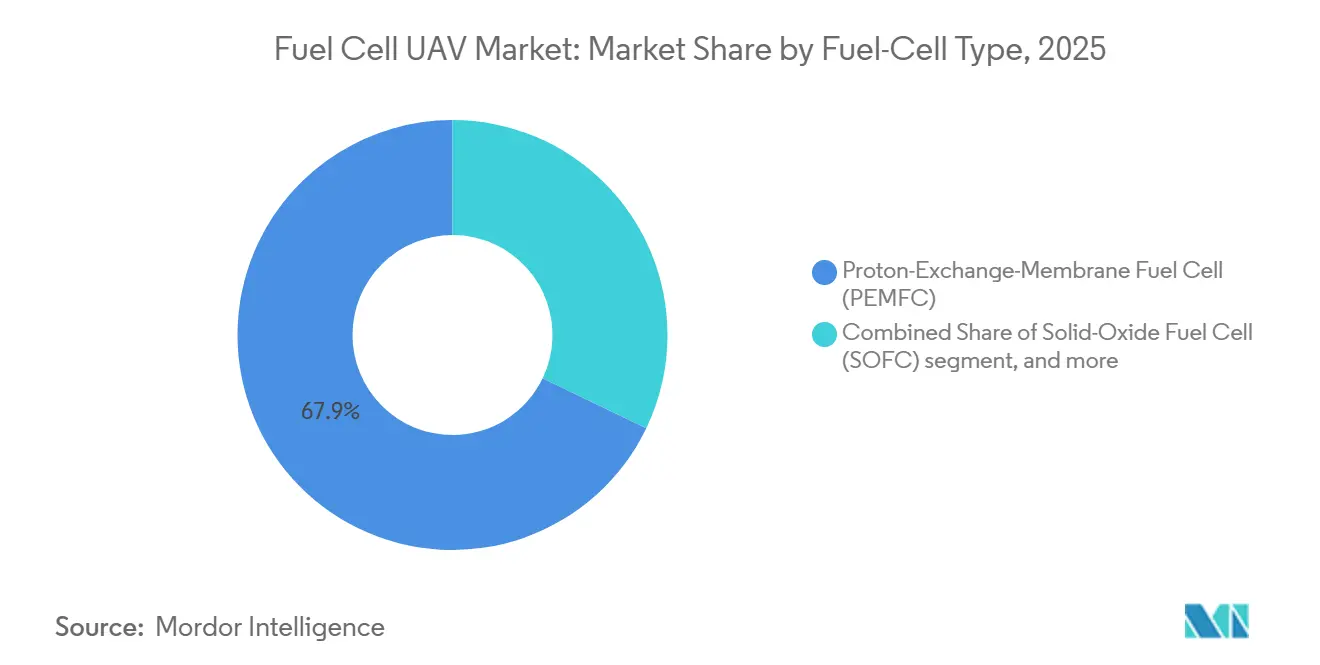

- By fuel cell type, PEMFC led with 67.87% fuel cell UAV market share in 2025, while SOFC variants posted the fastest 22.10% CAGR through 2031.

- By platform type, fixed-wing designs held 52.20% share in 2025, and hybrid VTOL platforms are on track for a 24.55% CAGR to 2031.

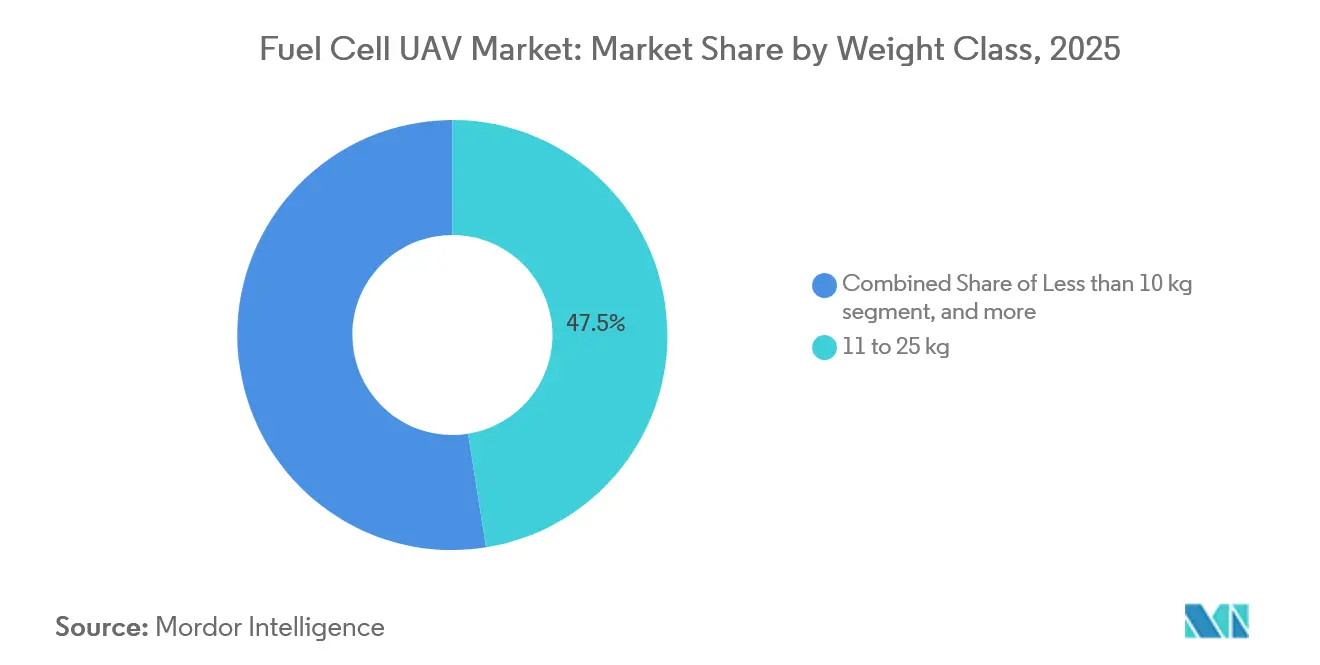

- By weight class, the 11 - 25 kg segment captured 47.50% share in 2025, whereas UAVs above 26 kg expanded at a 22.75% CAGR.

- By application, ISR accounted for a 57.60% share in 2025; however, the logistics segment is expected to advance at a 22.45% CAGR over the same horizon.

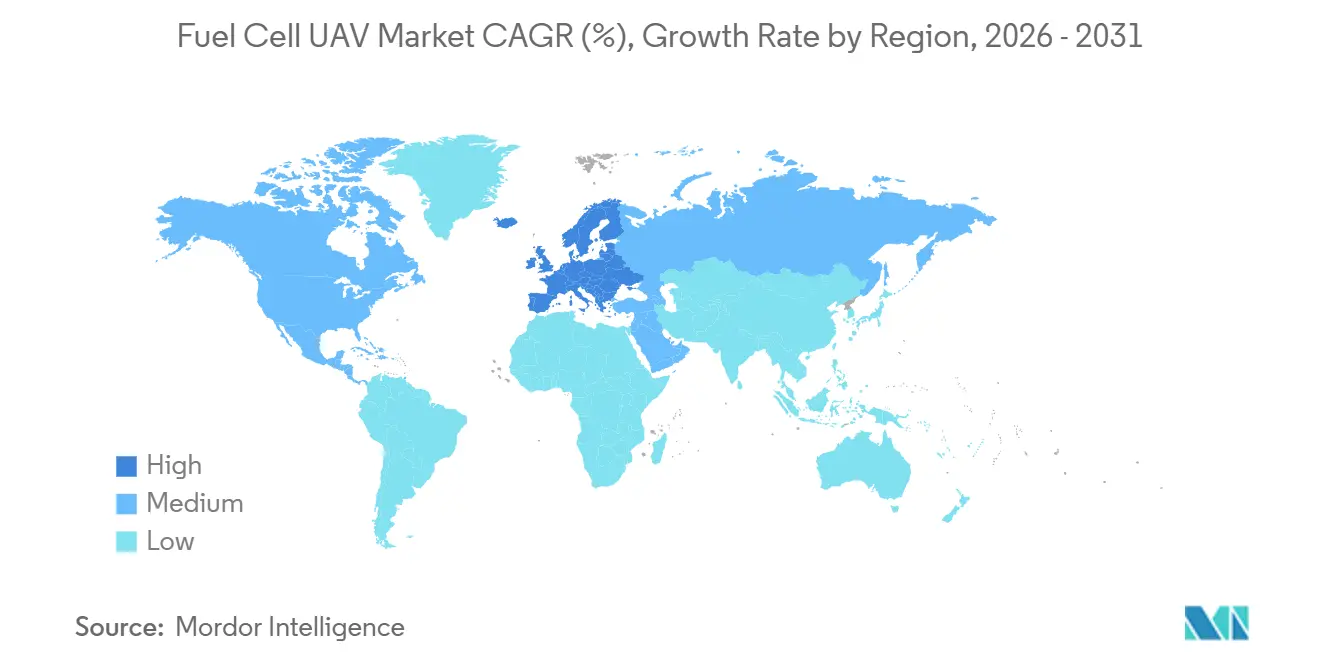

- By geography, North America held a 41.2% share in 2025, and Europe registered the fastest 21.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fuel Cell UAV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid-deployment need for long-endurance ISR | 3.5% | Indo-Pacific, Eastern Europe | Medium term (2-4 years) |

| DoD hydrogen-logistics decarbonization mandates | 2.8% | North America, NATO Europe | Short term (≤ 2 years) |

| Falling cost of high-power-density PEM stacks | 3.2% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Growing defense-sector interest in quiet propulsion | 2.1% | North America, Europe, Middle East | Medium term (2-4 years) |

| PEM–SOFC hybridization boosting sortie duration | 2.4% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| On-site green-hydrogen micro-refineries | 1.9% | Middle East, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid-Deployment Need for Long-Endurance ISR in Contested Airspace

Missions over Ukraine’s eastern corridor and the South China Sea underscore the importance of persistent surveillance. Fuel-cell UAVs extend loiter times from 90 minutes to beyond 13 hours, as demonstrated by the DS30-powered airframe during 2025 desert trials. The US Marine Corps validated similar endurance at Twentynine Palms, confirming operational viability at 40 °C. Planners value the reduced acoustic and infrared signatures that hydrogen propulsion offers, delaying adversary detection loops. Procurement offices are now considering squadron-level conversions, which will drive sustained growth in the fuel cell UAV market in the medium term. As allied forces standardize tactics around longer UAV station times, ISR fleets worldwide increasingly specify fuel-cell systems at the request-for-proposal stage.

DoD Hydrogen-Logistics Decarbonization Mandates

The 2024 Climate Adaptation Plan instructs US forces to halve operational emissions by 2030. HyTEC prototypes delivered in March 2025 produce 5 kg of hydrogen per day from renewable power, underscoring a shift away from diesel generators toward on-site electrolysis. NATO’s 2025 Energy Security Framework mirrors this push, ensuring aligned funding for hydrogen infrastructure among allies. Early rollouts at Fort Eustis and Ramstein Air Base indicate a 20% reduction in convoy traffic once cylinder deliveries cease. These early wins translate into rapid growth in the fuel cell UAV market as hydrogen refueling becomes integral to forward-base design.

Falling Cost of High-Power-Density PEM Stacks

Mass-production lines in Kansas and Incheon now produce membranes with sub-micron tolerances, reducing stack prices from USD 80 to USD 60 per kilowatt between 2023 and 2025.[2]Source: U.S. Department of Energy, “Hydrogen and Fuel Cell Technologies Office,” energy.gov Honeywell’s 1200U module launched in February 2025 at a 20% discount to incumbents. Platinum-catalyst recycling loops and automated gasket application heighten yield rates, passing savings downstream. Lower hardware costs shrink the payback period for operators, prompting fresh tenders in Australia and Poland that explicitly list hydrogen propulsion. Given continued growth in scale, analysts expect stack prices to fall below USD 50 per kilowatt by 2028, reinforcing positive price-elasticity feedback in the fuel cell UAV market.

Growing Defense-Sector Interest in Quiet Propulsion for Stealth

Hydrogen fuel-cell systems register below 55 dB at 100 m, a substantial cut from gasoline UAV noise signatures. Reduced thermal plumes also downgrade infrared exposure, extending UAV survivability over radar-dense regions. In November 2025, Cranfield’s ST-5 Stingray showcased low-observable profiles in a joint RAF-French trial, and customer feedback cited silent cruise as the top procurement differentiator. Special operations units in the Middle East and the Balkans now list acoustic stealth alongside payload capacity, adding fresh volume to the fuel cell UAV market over the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High battlefield refueling complexity | -2.3% | Global expeditionary theaters | Short term (≤ 2 years) |

| Safety certification hurdles for compressed H₂ above 350 bar | -1.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Scarcity of mil-spec fuel-cell supply chain | -1.6% | Global | Long term (≥ 4 years) |

| Cold-start performance degradation at high altitude | -1.4% | Asia-Pacific, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Battlefield Refueling Complexity

Hydrogen cylinders require three times the volume of diesel to deliver the same energy, significantly increasing supply chain demands and logistical challenges. In May 2025, marine technicians at Twentynine Palms took 15 minutes to refuel each UAV, which is three times longer than the battery swap process, further highlighting operational inefficiencies. In regions where potable water scarcity prevents on-site electrolysis, commanders are compelled to transport cylinders over long distances, reintroducing logistical risks and increasing operational complexity. These inefficiencies currently limit near-term scalability but are expected to diminish as 700-bar quick-connect systems and water-recovery units become more advanced and widely implemented.

Safety Certification Hurdles for Compressed H₂ Above 350 Bar

The UK Civil Aviation Authority (CAA) reduced approval cycles from 24 months to 18 months in 2025. However, 700-bar tanks still require ballistic-impact testing that exceeds automotive standards, which remains a significant challenge for manufacturers.[3]Source: UK Civil Aviation Authority, “Hydrogen Storage Guidance,” caa.co.uk While SAE J2579 and ISO 19881 regulations establish baseline requirements for safety and performance, interoperability audits among NATO members are not anticipated to conclude until 2027, further complicating the certification process. These certification delays hinder procurement processes, creating supply chain bottlenecks and slowing the medium-term growth of the Fuel Cell UAV market. As a result, stakeholders face increased uncertainty, which is impacting investment and development timelines in the industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Cell Type: Endurance Drives SOFC Upswing

PEMFC units dominated the market with a 67.87% share in 2025, due to their fast cold-start capabilities and lower mass. SOFC stacks, however, are projected to grow at a 22.10% CAGR through 2031, surpassing the overall fuel cell UAV market growth by 3.19 points. Continuous-loiter ISR missions now specify 24-hour thresholds, prompting buyers to consider hybrid PEM–SOFC packages. The fuel cell UAV market for SOFC solutions is expected to more than double by 2031, as heat-recovery loops reduce cold-start wait times. Engineers use PEM exhaust to preheat SOFC cores, a design that extends the operating ceiling above 3,000 m without incurring mass penalties. Suppliers report rising backlog from European border agencies that view hybrid systems as hedge-free endurance insurance.

The fuel cell UAV industry remains cautious about methanol-reformed SOFCs because logistics chains prefer a common hydrogen supply. Tests with Chile’s high-altitude police units reveal methanol cartridges could permit sub-zero patrols. While PEMFC retains the majority of the fuel cell UAV market revenue, the trajectory of SOFC shifts competitive roadmaps, prompting stack makers to invest in ceramic electrolyte lines. By 2028, at least three Asian vendors plan to launch SOFCs to dilute the currently Western-heavy supply chain.

By UAV Platform Type: Hybrid VTOL Shapes the Future

Fixed-wing airframes secured 52.20% of 2025 revenue due to aerodynamic economy over long legs. Hybrid VTOL, combining quad rotors for lift and a wing for cruise, posts the market’s quickest 24.55% CAGR. Operators crave truck-bed launch without runway dependence, positioning hybrid designs at the sweet spot for procurement. The fuel cell UAV market for hybrid VTOL is forecasted to expand strongly by 2031 compared with 2026 levels. End-users from Norway to Indonesia field-test tilt-rotor drones that can fly for eight hours while landing with a footprint the size of a football field.

Rotary-wing demand lags but remains a niche for urban ISR. Fuel cells enable flights of up to three hours on 2-kW stacks, but high hover loads still limit the range. Consequently, integrators prioritize weight shaving via carbon-composite tanks. Hybrids sidestep this hurdle by cruising on half the power, a pattern likely to redirect fuel cell UAV market share away from pure rotorcraft after 2027.

By Weight Class: Heavy Frames Gain Favor

The 11 to 25 kg weight category accounted for 47.50% of the market share in 2025, aligning with the 1–2 kW stack output range, which is considered optimal for UAVs in this bracket. This category continues to dominate due to its balance between performance and efficiency, making it a preferred choice for various applications. UAVs weighing over 26 kg are experiencing a 22.75% CAGR, driven by increasing demand for integrated ISR capabilities and cargo-carrying capacity, which enhance operational versatility. By 2031, aircraft exceeding 26 kg are projected to gain share, supported by 5–8 kW stacks, such as the ST-5 Stingray, which exemplifies advancements in power output for larger UAVs. Larger UAV frames also support 700-bar tanks, enabling a doubling of onboard hydrogen capacity without increasing the tank's volume in proportion, thereby significantly extending operational range and endurance.

Sub-10 kg platforms, though maneuverable, face power-density trade-offs. Honeywell's 600U targets this niche, but its 4-6 hour endurance still trails that of heavier peers. Unless catalyst breakthroughs push watt-per-kilo higher, the fuel cell UAV market will tilt toward mid-weight and heavy categories where endurance and payload synergize.

By Military Application: Logistics Takes Off

ISR retained 57.60% of the revenue in 2025, driven by border patrol and reconnaissance budgets. However, logistics drones carrying 10 kg payloads are racing ahead at a 22.45% CAGR as medevac and ammo resupply use cases win funding. Fuel-cell power plants give these craft a 50 km range and triple the battery alternatives. The Fuel Cell UAV market size for logistics missions is forecast to expand rapidly by 2031, closing the gap with ISR. Precision strike remains niche due to the mass of missile integration, yet may unlock incremental demand once lighter munitions reach TRL 8.

Communications relay and electronic warfare fill the “Others” bucket, profiting from silent endurance that keeps airborne nodes aloft during blackout events. Stakeholders are now drafting doctrines that use a trio of fuel-cell relays to replace tethered balloons, thereby reducing workforce requirements and shortening deployment timelines.

Geography Analysis

North America led with 41.2% of 2025 revenue, buoyed by the Blue UAS Framework's inclusion of hydrogen models. The US Army Futures Command allocates multi-year funding for squadron rollouts, thereby anchoring the regional fuel cell UAV market. Canada's DRDC partners with Intelligent Energy to trial Arctic patrol variants, signaling continental breadth of demand. The fuel cell UAV market in North America is expected to expand rapidly by 2031 as HyTEC micro-refineries proliferate at Marine Corps bases.

Europe, projected to grow at a 21.95% CAGR, benefits from European Defence Fund grants that help de-risk prototype costs: the UK, France, and Germany co-finance compressed-hydrogen tank testing and condense certification calendars. Cranfield's ST-5 Stingray illustrates domestic content strategies that bolster sovereign supply chains. Once pan-European tank interoperability is ratified in 2027, procurement pipelines are expected to flow more efficiently, propelling the fuel cell UAV market across NATO borders.

The Asia-Pacific region is home to active suppliers, notably South Korea's Doosan Mobility and Japan's new SOFC consortium. India's DRDO began flight tests using PEM-powered fixed-wing aircraft for high-altitude surveillance in Ladakh, despite experiencing cold-start issues. ASEAN members are trialling logistics drones for island resupply, albeit at a pilot scale. Market expansion hinges on the rollout of hydrogen infrastructure, which lags behind that of industrial economies but is receiving fresh impetus from Japan's 2026 "Green Defense" roadmap.

The Middle East channels petrodollar surpluses into Green-Hydrogen cities, laying the groundwork for military adoption. Saudi Arabia's NEOM hosts a test corridor where autonomous fuel-cell drones haul medical cargo between clinics. Regulatory clarity remains limited, slowing acquisitions but foreshadowing eventual upticks once airworthiness rules are finalized. South America and Africa are showing early signs of traction. Brazil's border-policing agency eyes fixed-wing fuel-cell drones for Amazon patrols, while South Africa investigates anti-poaching oversight. These regions account for less than 5% of 2025 revenue yet present long-term upside as hydrogen prices decline.

Competitive Landscape

The fuel cell UAV market is moderately concentrated. Lockheed Martin and AeroVironment retrofit proven airframes with Intelligent Energy stacks, leveraging incumbent contracts. Doosan Mobility Innovation dominates the module supply market, offering the DS30 and DP30 lines, which span 2-5 kW. Cranfield Aerospace offers turnkey packages, marketing the ST-5 Stingray alongside ground refueling systems. Zepher Flight Labs focuses on US defense channels, achieving Blue UAS status that simplifies acquisitions.

Emerging players compete on thermal-management IP. H3 Dynamics patented waste-heat pre-heaters linking PEM and SOFC cores, trimming altitude start delays. Heven AeroTech prioritizes tilt-rotor architecture, bundling Sesame Solar micro-refineries for turnkey field capability. Patent filings for fuel-cell UAV tech rose 35% in 2025, hinting at later consolidation once winning chemistries and architectures surface.

Downstream, connector and tank suppliers craft proprietary interfaces. While SAE J2579 promotes standardization, leading primes still lock buyers into branded quick-connect couplers. Observers expect an eventual interoperability push as NATO procurement teams balk at spare parts silos, a change that is likely to reshuffle the Fuel Cell UAV market share among subsystem manufacturers.

Fuel Cell UAV Industry Leaders

Israel Aerospace Industries Ltd.

AeroVironment, Inc.

ISS Group Ltd.

Lockheed Martin Corporation

Doosan Mobility Innovation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Cranfield Aerospace Solutions (CAeS) launched its hydrogen-electric ST-5 ‘Stingray’ UAV at the Dubai Airshow, marking a strategic advancement in zero-emission aviation technology. With applications spanning military reconnaissance and environmental monitoring, the collaboration with the UK’s National Oceanography Centre (NOC) highlights the drone’s versatility. This development highlights the growing integration of hydrogen propulsion in aerospace, driving innovation in long-endurance, multi-role UAV platforms with significant implications for both defense and the environment.

- July 2025: XSun and H3 Dynamics announced a collaboration to develop a solar-powered UAV powered by hydrogen fuel cells and batteries, with significant implications for military applications. The hybrid-electric system, including the H2-Field mobile hydrogen refueling unit, is undergoing field testing with the US Army. This innovation highlights the strategic potential for zero-emission, high-endurance UAVs in defense operations, offering enhanced mission flexibility and reduced logistical dependencies.

Global Fuel Cell UAV Market Report Scope

A fuel cell propulsion system powers a fuel-cell unmanned aerial vehicle (UAV). A fuel cell is an electrochemical device that generates electricity by combining hydrogen (usually stored in a tank) with oxygen from the air, producing water and releasing energy. This energy is then used to power the UAV's motors and other systems. The Scope of the reports includes only UAVs equipped with a fuel cell.

The fuel cell UAV market is segmented by fuel cell type, UAV platform type, weight class, military application, and geography. By fuel-cell type, the market is segmented into proton-exchange membrane fuel cells (PEMFC), solid-oxide fuel cells (SOFC), and hydrogen fuel cells. By weight class, the market is segmented into the less than 10 kg, 11-25 kg, and more than 25 kg. By military application, the market is segmented by ISR, border patrol, precision strike, logistics and transportation, and others. The report also covers the market sizes and forecasts for the fuel cell UAV market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Proton-Exchange-Membrane Fuel Cells (PEMFC) |

| Solid-Oxide Fuel Cells (SOFC) |

| Hydrogen Fuel Cells |

| Fixed-Wing |

| Rotary-Wing |

| Hybrid |

| Less than 10 kg |

| 11 to 25 kg |

| More than 26 kg |

| Intelligence, Surveillance and Reconnaissance (ISR) |

| Border Patrol |

| Precision Strike |

| Logistics and Transportation |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Fuel Cell Type | Proton-Exchange-Membrane Fuel Cells (PEMFC) | ||

| Solid-Oxide Fuel Cells (SOFC) | |||

| Hydrogen Fuel Cells | |||

| By UAV Platform Type | Fixed-Wing | ||

| Rotary-Wing | |||

| Hybrid | |||

| By Weight Class | Less than 10 kg | ||

| 11 to 25 kg | |||

| More than 26 kg | |||

| By Military Application | Intelligence, Surveillance and Reconnaissance (ISR) | ||

| Border Patrol | |||

| Precision Strike | |||

| Logistics and Transportation | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the fuel cell UAV market growing through 2031?

Revenue expands at an 18.91% CAGR, lifting value from USD 1 billion in 2026 to USD 2.38 billion by 2031.

Which platform category will add the most new revenue?

Hybrid VTOL airframes post the highest 24.55% CAGR thanks to runway-free launch and cruise efficiency.

What drives military demand for hydrogen-powered drones?

Eight-plus-hour endurance, acoustic stealth below 55 dB, and alignment with defense decarbonization mandates.

Why is Europe the fastest-growing regional market?

European Defence Fund co-financing and streamlined 350-bar certification are pushing a 21.95% CAGR.

What is the main barrier to wider adoption?

Battlefield refueling complexity and 700-bar safety certification remain the leading constraints.

Which fuel-cell technology is set to gain share?

SOFC stacks will outpace overall growth at 22.10% CAGR as hybrid architectures target 24-hour sorties.

Page last updated on: