Freight Forwarding Market Overview

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 581.94 Billion |

| Market Size (2030) | USD 724.16 Billion |

| Growth Rate (2025 - 2030) | 4.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

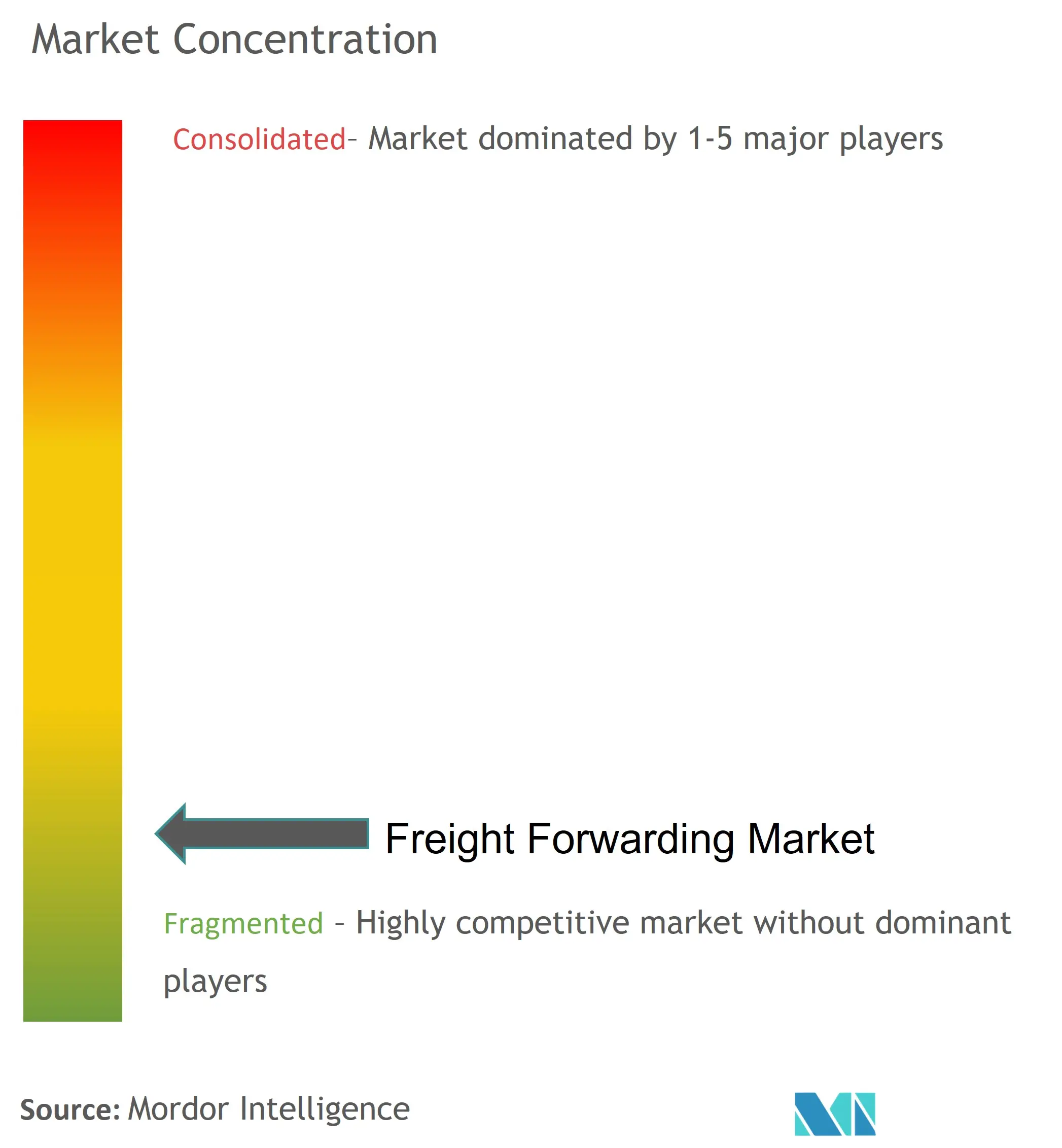

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Freight Forwarding Industry Analysis

The Freight Forwarding Market size is estimated at USD 581.94 billion in 2025, and is expected to reach USD 724.16 billion by 2030, at a CAGR of 4.47% during the forecast period (2025-2030).

The freight forwarding industry is undergoing a significant technological transformation, with artificial intelligence, blockchain, and cloud computing becoming essential components of operational efficiency. This digital revolution is exemplified by Uber Freight's September 2023 announcement of its logistics technology evolution, managing freight worth USD 18 billion through AI-powered software and advanced technology development capabilities. The integration of these technologies is reshaping traditional forwarding processes, enabling real-time tracking, automated documentation, and enhanced supply chain visibility, while simultaneously creating new challenges for companies that must invest in digital infrastructure to remain competitive.

Global supply chains are experiencing a fundamental restructuring as companies diversify their sourcing strategies beyond traditional manufacturing hubs. This shift is particularly evident in the movement away from China-centric supply chains, with companies actively exploring alternatives in Southeast Asia and South Asia. The transformation is driven by ongoing trade restrictions and geopolitical tensions between major economies, including China, the United States, Russia, Ukraine, and Europe, leading to the emergence of new trade corridors and regional manufacturing hubs.

The ocean freight forwarding sector is witnessing a dramatic market correction, transitioning from a capacity-constrained environment to one characterized by oversupply in both vessels and containers. This shift has significant implications for pricing dynamics and carrier strategies, as shipping lines adjust their operations to match reduced demand levels. The industry's evolution is further shaped by governmental initiatives to develop alternative shipping routes, as evidenced by the March 2023 discussions between India and Russia regarding the utilization of the Northern Sea Route across the Arctic for maritime transportation.

The air freight sector is experiencing a notable recovery in capacity and service offerings, with international air travel returning to pre-pandemic levels in 2023. This restoration of passenger flights has significantly increased belly cargo capacity, providing more options for freight forwarders and their clients. The industry is adapting to these changes through innovative service combinations, enhanced route planning, and the development of specialized solutions for high-value and time-sensitive cargo, reflecting the sector's ability to evolve in response to changing market conditions and customer requirements.

Freight Forwarding Market Trends

Growing International Trade and Cross-Border E-commerce

The expansion of international trade and cross-border e-commerce has emerged as a primary driver for the freight forwarding market. The increasing globalization of supply chains and the need for efficient logistics solutions have led to significant investments in cross-border infrastructure and services. This is evidenced by major industry developments in 2023, such as C.H. Robinson's establishment of the largest cross-border logistics facility in Laredo, Texas, featuring 400,000 square feet of warehousing space, 154 dock doors, and capacity for 700 trailers. The facility's strategic location and extensive capabilities demonstrate the growing demand for sophisticated cross-border logistics solutions to handle increasing trade volumes.

The development of new trade corridors and logistics centers further underscores the market's response to growing international trade demands. For instance, in September 2023, Kazakhstan initiated the construction of major transport, logistics, and trade centers along its borders with China, Russia, the Kyrgyz Republic, Uzbekistan, and the Caspian Sea. These developments are designed to accommodate substantial cargo volumes, with facilities capable of handling various cargo types including general cargo, grain, liquid cargo, and universal cargo, with a combined annual capacity of 10 million tons. Such infrastructure investments reflect the increasing importance of efficient freight forwarding services in facilitating global trade flows.

Understand The Key Trends Shaping This Market

Download PDF

Infrastructure Development and Modernization

The freight forwarding industry is experiencing significant growth driven by extensive infrastructure development and modernization initiatives across global trade routes. Major investments in logistics facilities and transportation hubs are enhancing the efficiency and capacity of freight forwarding operations. The development of modern logistics facilities, such as C.H. Robinson's new cross-border facility, which expands their Mexican border footprint to 1.5 million square feet, demonstrates the scale of infrastructure investments being made to meet growing market demands. These facilities incorporate advanced features and technologies to optimize freight handling and distribution processes.

Strategic infrastructure projects are also being implemented to strengthen international trade corridors. Kazakhstan's comprehensive development plan through 2030 exemplifies this trend, with the construction of specialized terminals including a 1-million-ton general cargo terminal, a 1.5-million-ton grain terminal, a 5.5-million-ton liquid cargo terminal, and a 2-million-ton universal terminal. These infrastructure developments are creating new opportunities for freight forwarders by establishing more efficient trade routes and reducing bottlenecks in global supply chains. The modernization of existing facilities and the creation of new logistics hubs are essential in supporting the growing complexity and volume of international trade.

Expansion of Air Freight Services

The air freight sector is experiencing substantial growth driven by increasing demand for rapid and efficient transportation solutions, particularly for time-sensitive and high-value shipments. Major airlines are expanding their cargo capabilities and routes to meet this growing demand. This is exemplified by American Airlines Cargo's significant expansion of their winter schedule for 2023-2024, which includes more than 12,500 round-trip flights and over 6,900 widebody flights dedicated to transatlantic routes. This expansion demonstrates the industry's response to the growing need for reliable and frequent air freight services across major international markets.

The development of specialized air freight solutions is further driving market growth, as evidenced by new service launches from major logistics providers. For instance, in August 2023, Cargo-partner introduced a new air freight solution connecting Chicago to London Heathrow Airport, offering weekly departures and specialized trade expertise. These new services are enhancing the efficiency and reliability of international air freight transportation, particularly for time-critical shipments and high-value goods. The continuous expansion of air freight services and routes is creating new opportunities for freight forwarders to offer more comprehensive and flexible logistics solutions to their clients. These advancements are pivotal in the international freight forwarding services market, contributing to the overall growth of the freight forwarding market.

Segment Analysis: By Mode

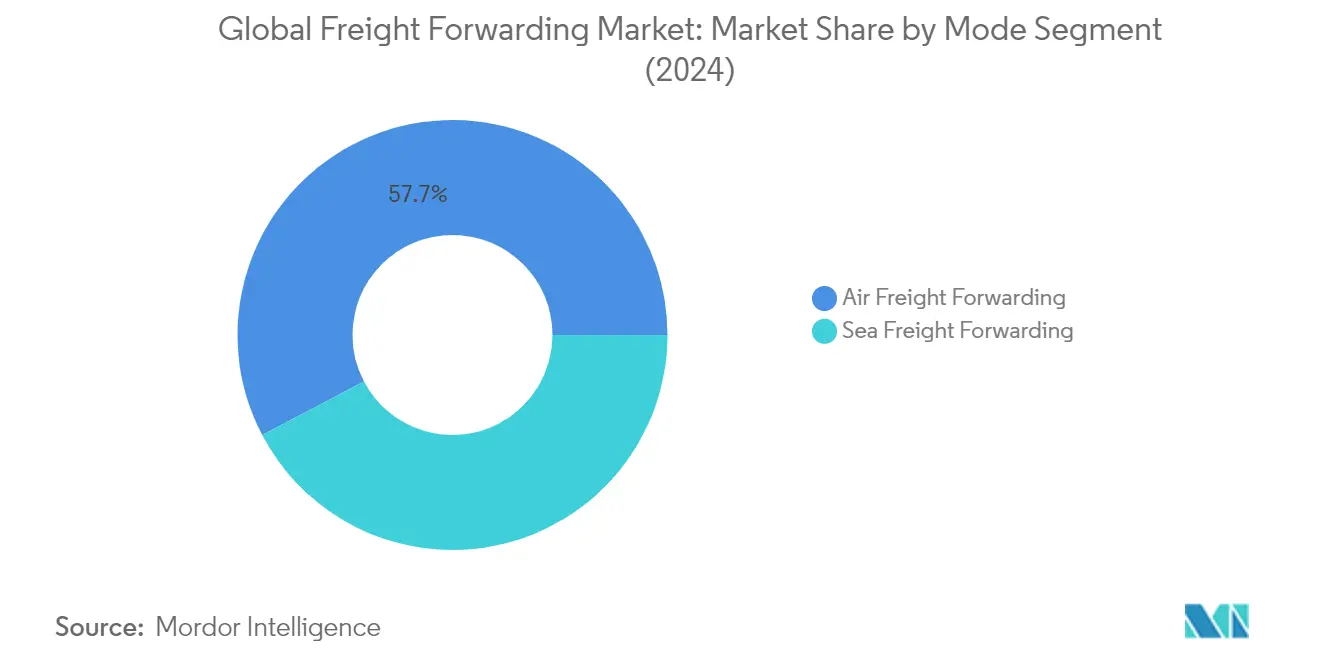

Air Freight Forwarding Segment in Global Freight Forwarding Market

Air freight forwarding continues to dominate the global air freight forwarding market, commanding approximately 58% of the total freight forwarding market share in 2024. This segment's prominence is driven by the increasing demand for time-sensitive deliveries, particularly in sectors like pharmaceuticals, high-tech electronics, and perishable goods. The segment has witnessed substantial growth due to the expansion of cross-border e-commerce activities and the need for rapid delivery services. Air freight forwarding has become particularly crucial for industries requiring temperature-controlled transportation, such as healthcare and biotechnology. The segment's growth is further supported by technological advancements in cargo handling, improved airport infrastructure, and the integration of digital solutions for real-time tracking and monitoring. Additionally, the rise in international trade and the need for expedited shipping solutions have reinforced air freight forwarding's position as the preferred choice for high-value and time-critical shipments.

Sea Freight Forwarding Segment in Global Freight Forwarding Market

Sea freight forwarding is emerging as the fastest-growing segment in the global sea freight forwarding market, with a projected growth rate of approximately 5% during the forecast period 2024-2029. This accelerated growth is primarily attributed to the increasing adoption of containerization, development of advanced port infrastructure, and optimization of shipping routes. The segment is experiencing significant technological transformation with the implementation of smart container solutions, blockchain technology for enhanced transparency, and automated port operations. Maritime transport's cost-effectiveness for bulk shipments, coupled with its lower environmental impact compared to other modes, is driving its adoption among businesses focusing on sustainable logistics solutions. The expansion of trade corridors, particularly along the Asia-Pacific routes, and investments in port modernization projects are further catalyzing the segment's growth. Additionally, the integration of digital platforms for booking and tracking maritime shipments is streamlining operations and improving efficiency in sea freight forwarding market size.

Freight Forwarding Market Geography Segment Analysis

Freight Forwarding Market in North America

The North American freight forwarding market demonstrates robust infrastructure and sophisticated logistics networks across the United States, Canada, and Mexico. The region benefits from well-established trade corridors, advanced technological adoption in logistics operations, and strong cross-border trade relationships. The market is characterized by increasing integration of digital solutions, growing e-commerce activities, and continuous infrastructure development to support efficient freight movement. The presence of major ports, extensive rail networks, and advanced air cargo facilities further strengthens the region's position in global trade. Freight forwarding companies in North America are leveraging these advantages to enhance their service offerings.

Freight Forwarding Market in United States

The United States dominates the North American freight forwarding landscape with approximately 82% market share in the region. The country's market is driven by domestic manufacturing output and international trade levels. The U.S. benefits from an extensive transportation infrastructure, including major seaports, airports, and an integrated rail network. The adoption of green logistics solutions has been witnessed in recent years due to rising environmental concerns. The country's strategic geographical position, coupled with advanced logistics technologies and extensive relationships in shipper and carrier networks, continues to reinforce its market leadership. The presence of both large multinational corporations and specialized local operators creates a dynamic and competitive market environment. International freight forwarding companies are increasingly focusing on the U.S. market to capitalize on these opportunities.

Freight Forwarding Market in Mexico

Mexico emerges as the fastest-growing market in North America, with an expected growth rate of approximately 6% during 2024-2029. The country's strategic position as a manufacturing hub and its strong trade relationships with both North and South America contribute to this growth trajectory. Mexico's market is experiencing significant transformation through infrastructure development, particularly in its port facilities and cross-border transportation networks. The implementation of various government initiatives and trade agreements has created new opportunities for freight forwarders. The country's growing automotive and electronics sectors, combined with increasing cross-border e-commerce activities, are driving demand for sophisticated logistics services. Freight forwarding companies in Mexico are well-positioned to leverage these developments.

Freight Forwarding Market in Europe

The European freight forwarding market showcases a sophisticated network of logistics operations spanning Germany, France, the United Kingdom, the Netherlands, and Italy. The region benefits from advanced transportation infrastructure, seamless cross-border operations, and strong integration of multimodal transport systems. The market is characterized by increasing digitalization of logistics operations, growing emphasis on sustainable transport solutions, and strong intra-regional trade flows. The presence of major ports, extensive rail networks, and advanced air cargo facilities contributes to the region's efficient freight movement capabilities. International freight companies in Europe are increasingly adopting digital solutions to enhance operational efficiency.

Freight Forwarding Market in Germany

Germany maintains its position as Europe's leading freight forwarding market, commanding approximately 33% of the regional market share. The country serves as Europe's prime logistics center point with best-in-class transportation systems and dense national and international air terminals. Germany's central location in Europe enables efficient coordination of logistics activities across national borders. The country's strong manufacturing base, particularly in the automotive and industrial sectors, drives significant freight volumes. The presence of major ports, extensive rail infrastructure, and advanced logistics technologies reinforces Germany's position as a key logistics hub. Largest freight forwarding companies are actively investing in Germany to capitalize on its strategic advantages.

Freight Forwarding Market in Italy

Italy emerges as Europe's fastest-growing freight forwarding market, with an anticipated growth rate of approximately 6% during 2024-2029. The country's strategic position in the Mediterranean Sea makes it a crucial gateway for trade between Europe, North Africa, and the Middle East. Italy's market is undergoing significant transformation through port modernization initiatives and digital integration in logistics operations. The country's diverse industrial base, strong export orientation, and growing e-commerce sector drive the demand for freight forwarding services. The implementation of innovative technological solutions and automation in ports and logistics facilities further supports market growth. Top freight forwarding companies in the world are increasingly focusing on Italy to tap into its growing market potential.

Freight Forwarding Market in Asia-Pacific

The Asia-Pacific freight forwarding market encompasses a diverse range of economies, including China, Japan, Australia, India, Singapore, Malaysia, Indonesia, Vietnam, and South Korea. The region demonstrates dynamic growth driven by increasing international trade, rapid industrialization, and expanding e-commerce activities. The market benefits from continuous infrastructure development, technological advancement in logistics operations, and growing regional economic integration. The diversity of markets within the region creates varied opportunities and challenges for freight forwarders. Top 10 freight forwarding companies in India are contributing significantly to the region's growth through innovative logistics solutions.

Freight Forwarding Market in China

China maintains its position as the dominant force in the Asia-Pacific freight forwarding market. The country's extensive manufacturing base, robust export activities, and strategic infrastructure investments through initiatives like the Belt and Road Initiative reinforce its market leadership. China's market is characterized by rapid technological adoption, expanding e-commerce logistics, and continuous development of port and airport infrastructure. The integration of digital solutions and automation in logistics operations further strengthens China's competitive position. Global freight companies are increasingly investing in China to leverage its robust market dynamics.

Freight Forwarding Market in Indonesia

Indonesia emerges as the fastest-growing market in the Asia-Pacific region. The country's archipelagic geography creates unique opportunities for multimodal freight transportation solutions. Indonesia's market is driven by growing domestic consumption, expanding manufacturing activities, and increasing international trade. The government's focus on infrastructure development, particularly in port facilities and connectivity improvements, supports market growth. The rising adoption of digital logistics solutions and e-commerce activities further contributes to market expansion. Freight forwarding companies in Indonesia are capitalizing on these opportunities to expand their market presence.

Freight Forwarding Market in South America

The South American freight forwarding market, primarily represented by Brazil and Chile, demonstrates growing potential despite infrastructure challenges. The region's market is characterized by increasing international trade activities, growing domestic consumption, and ongoing infrastructure development initiatives. Brazil emerges as the largest market in the region, benefiting from its extensive coastline and diverse industrial base, while Chile shows the fastest growth potential driven by its strong mining sector and international trade relationships. The market continues to evolve with increasing adoption of digital solutions and modernization of port infrastructure. International freight forwarding companies are exploring opportunities in South America to tap into its emerging market potential.

Freight Forwarding Market in Middle East & Africa

The Middle East & Africa freight forwarding market, encompassing South Africa, the United Arab Emirates, Saudi Arabia, and Qatar, showcases diverse growth opportunities. The region benefits from a strategic geographical location between Asia and Europe, significant investments in logistics infrastructure, and growing trade activities. The United Arab Emirates emerges as the largest market, leveraging its position as a global logistics hub, while Qatar demonstrates the fastest growth potential driven by infrastructure development and economic diversification initiatives. The market is characterized by increasing adoption of digital solutions, expansion of port facilities, and growing focus on e-commerce logistics. Freight forwarding companies in South Africa are increasingly adopting digital solutions to enhance their competitive edge.

Get Analysis on Important Geographic Markets

Download PDF

Freight Forwarding Industry Overview

Top Companies in Freight Forwarding Market

The freight forwarding market is dominated by established players like DHL Global Forwarding, Kuehne + Nagel, DB Schenker, DSV Panalpina, and Sinotrans, leading the industry. These companies are often recognized among the world's top 10 freight forwarding companies. Companies across the sector are increasingly focusing on technological innovation through the implementation of AI, blockchain, and digital platforms to enhance operational efficiency and customer experience. The industry is witnessing a significant shift towards automation and digitalization of processes, with major players investing in cloud-based solutions and advanced tracking systems. Strategic partnerships and acquisitions remain key growth drivers, particularly in emerging markets and specialized sectors like e-commerce logistics. Companies are expanding their geographical footprint while simultaneously developing specialized solutions for industry-specific requirements, such as pharmaceutical logistics and temperature-controlled transportation. The emphasis on sustainable practices and green logistics solutions has become a crucial differentiator in the market.

Consolidated Market with Strong Regional Players

The freight forwarding market exhibits a consolidated structure at the global level, with the top twenty players accounting for more than half of the market share. These major players operate extensive global networks while maintaining strong regional presences through local partnerships and subsidiaries. The market is characterized by a mix of global logistics conglomerates offering end-to-end supply chain solutions and specialized regional players focusing on specific trade lanes or industry verticals. The industry has witnessed significant consolidation through mergers and acquisitions, as exemplified by DSV's acquisition of Panalpina and the integration of various regional players into larger networks.

The competitive landscape is evolving with the emergence of digital freight forwarders and technology-driven logistics platforms challenging traditional business models. These new entrants are leveraging technology to provide more transparent, efficient, and cost-effective solutions to customers. The market also sees strong competition from asset-based carriers expanding into forwarding services and regional specialists with deep expertise in specific markets or industries. The industry structure is further influenced by strategic alliances and partnerships, particularly in developing markets where local knowledge and networks are crucial for success.

Innovation and Adaptability Drive Market Success

Success in the freight forwarding market increasingly depends on companies' ability to adapt to changing customer demands and technological advancements. Market leaders, often among the largest freight forwarders, are investing heavily in digital transformation, developing proprietary platforms for seamless booking, tracking, and documentation processes. The ability to provide value-added services, such as customs clearance, warehousing, and supply chain consulting, has become crucial for maintaining a competitive advantage. Companies are also focusing on developing industry-specific expertise, particularly in high-growth sectors like healthcare, technology, and e-commerce, while building resilient networks capable of handling supply chain disruptions.

For new entrants and smaller players, success lies in identifying and serving niche markets or specific trade lanes where they can build specialized expertise. The focus on sustainability and environmental compliance is becoming a key differentiator, with companies investing in green technologies and sustainable practices to meet evolving customer expectations and regulatory requirements. Building strong relationships with carriers and maintaining pricing flexibility while ensuring service quality remains crucial. The ability to offer personalized solutions, maintain operational agility, and leverage data analytics for decision-making will be critical factors in determining market success, particularly as the industry continues to evolve with changing global trade patterns and technological advancements.

Freight Forwarding Market Leaders

-

Kuehne + Nagel International AG

-

DB Schenker

-

Bollore Logistics

-

DHL Global Forwarding

-

Nippon Express Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Freight Forwarding Market News

- June 2023: Kuehne+Nagel, a global logistics company, marked an agreement to acquire Morgan Cargo, a leading South African, United Kingdom, and Kenyan freight forwarder specializing in transporting and handling perishable goods. The acquisition strengthens the company's perishables logistics service offering while enhancing connectivity for customers to and from South Africa, the United Kingdom, and Kenya, which includes state-of-the-art cold chain facilities.

- April 2023: DHL Global Forwarding signed an MoU with Turkish Cargo to extend its operations to SMARTIST, a cargo facility for Turkish Cargo at the Istanbul airport. This agreement enhances the company's operation efficiencies and further boosts Istanbul's ability to emerge as a global logistics hub.

Freight Forwarding Industry Segmentation

Freight forwarding refers to the coordination and transport of goods from one place to another using one or more carriers by air, sea, rail, or road. The principles of freight forwarding focus on the cost-effective and efficient transfer of goods that are always kept in reasonable condition during transport.

A complete freight forwarding industry analysis, comprising the assessment of the economy and contribution of sectors in the economy, freight forwarding industry overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, freight forwarder market share, geographical trends, and the COVID-19 impact is included in the report.

The freight forwarding market is segmented by mode of transport (air freight forwarding, ocean freight forwarding, road freight forwarding, rail freight forwarding), customer type (B2C and B2B), application (industrial and manufacturing, retail, healthcare, oil and gas, food and beverages, and other applications), and geography (North America, Europe, Asia-Pacific, and LAMEA). The report offers freight forwarding market size, forecasts and freight forwarder market share for all the above-mentioned segments in value (USD).

| By Mode Of Transport | Air Freight Forwarding | ||

| Ocean Freight Forwarding | |||

| Road Freight Forwarding | |||

| Rail Freight Forwarding | |||

| By Customer Type | B2B | ||

| B2C | |||

| By Application | Industrial And Manufacturing | ||

| Retail | |||

| Healthcare | |||

| Oil And Gas | |||

| Food And Beverages | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| LAMEA | Brazil | ||

| South Africa | |||

| GCC | |||

| Rest of LAMEA | |||

Need A Different Region or Segment?

Customize Now

Freight Forwarding Market Research Faqs

How big is the Freight Forwarding Market?

The Freight Forwarding Market size is expected to reach USD 581.94 billion in 2025 and grow at a CAGR of 4.47% to reach USD 724.16 billion by 2030.

What is the current Freight Forwarding Market size?

In 2025, the Freight Forwarding Market size is expected to reach USD 581.94 billion.

Who are the key players in Freight Forwarding Market?

Kuehne + Nagel International AG, DB Schenker, Bollore Logistics, DHL Global Forwarding and Nippon Express Co., Ltd. are the major companies operating in the Freight Forwarding Market.

Which is the fastest growing region in Freight Forwarding Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Freight Forwarding Market?

In 2025, the North America accounts for the largest market share in Freight Forwarding Market.

What years does this Freight Forwarding Market cover, and what was the market size in 2024?

In 2024, the Freight Forwarding Market size was estimated at USD 555.93 billion. The report covers the Freight Forwarding Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Freight Forwarding Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Freight Forwarding Market Research

Mordor Intelligence offers a comprehensive analysis of the global freight forwarding industry. We leverage our extensive expertise in freight forwarding services research and consulting to provide this detailed report. It examines the evolving landscape of international freight forwarding companies and delivers in-depth insights into freight forwarding sector dynamics. The analysis covers crucial aspects of the freight forwarding market size, including emerging trends in global freight companies and developments in key regions such as freight forwarding companies in South Africa and India.

Stakeholders gain valuable insights through our extensive coverage of the largest freight forwarding companies. The report includes a detailed analysis of international freight companies operations. It examines global freight forwarding services and offers strategic information about the top freight forwarding companies in world, including detailed profiles of industry leaders. Our research encompasses international forwarding companies across various segments, with particular attention to the top 10 freight forwarding companies in India and other emerging markets. The comprehensive report is available as an easy-to-download PDF, featuring detailed data on freight forwarding services and market projections that help businesses make informed decisions in this dynamic industry.