Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

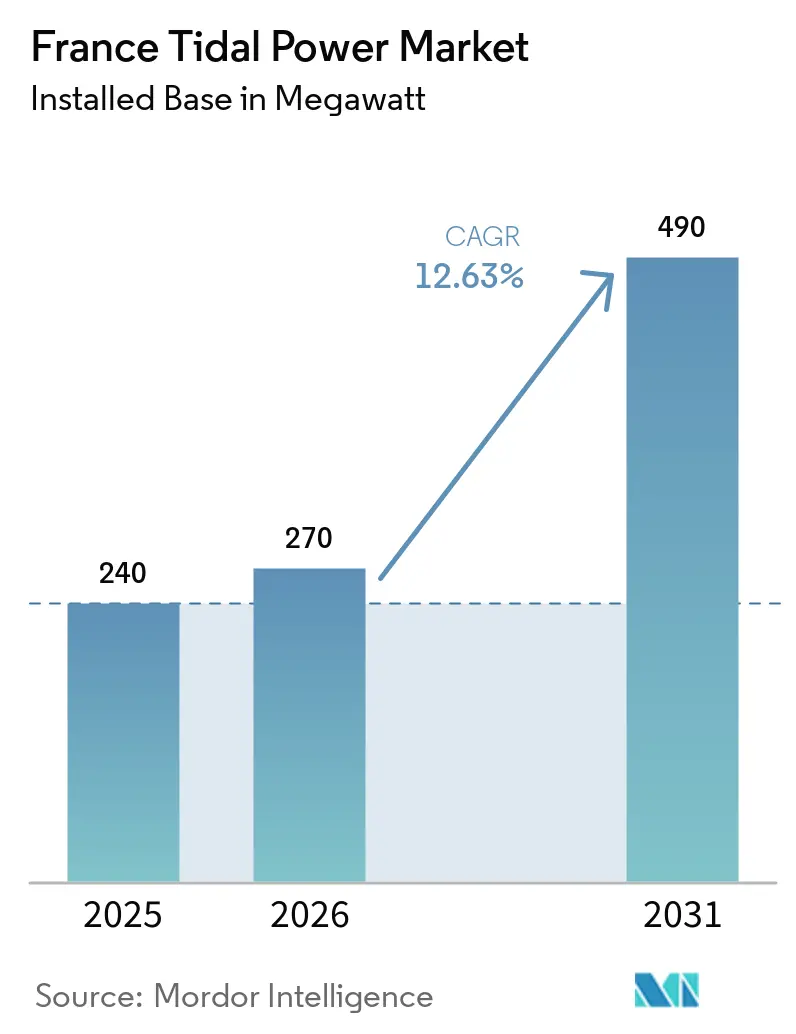

| Base Year Market Size (2025) | 240 megawatt |

| Market Volume (2026) | 270 megawatt |

| Market Volume (2031) | 490 megawatt |

| Growth Rate (2026 - 2031) | 12.63% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Tidal Power Market Analysis by Mordor Intelligence

The France Tidal Power Market size in terms of installed base is expected to grow from 240 megawatt in 2025 to 270 megawatt in 2026 and is forecast to reach 490 megawatt by 2031 at 12.63% CAGR over 2026-2031.

France’s policy backdrop has become more defined because PPE3 commits 250 MW to tidal stream energy and points to a first commercial tender by 2030, which gives developers and suppliers a clearer project pipeline than they had in earlier years.[1] Normandie Hydroliennes, “France Confirms 250 MW Tidal Energy Target as NH1 Advances Toward Industrial Deployment,” Normandie Hydroliennes, normandiehydroliennes.fr The France tidal power market is now moving out of a long demonstration phase, with the FloWatt and NH1 arrays at Raz Blanchard giving the country 2 visible projects that can prove construction methods, operating performance, and financing discipline at a more commercial scale. Public funding from the EU Innovation Fund and France 2030 is reducing early project risk, while local manufacturing activity in Cherbourg is helping the supply chain gain repeat work instead of one-off prototype orders. The competitive field remains moderate, but it is becoming tighter around a small set of developers that have funding access, industrial partners, and site rights, while Sabella’s failure showed that technical credibility alone is still not enough to secure long-term bankability in the France tidal power market. Cost is still the main constraint, yet the independent validation of NH1’s path toward sub EUR 100/MWh at large scale supports the view that learning effects and larger arrays can improve the economics of the France tidal power market over time.

Key Report Takeaways

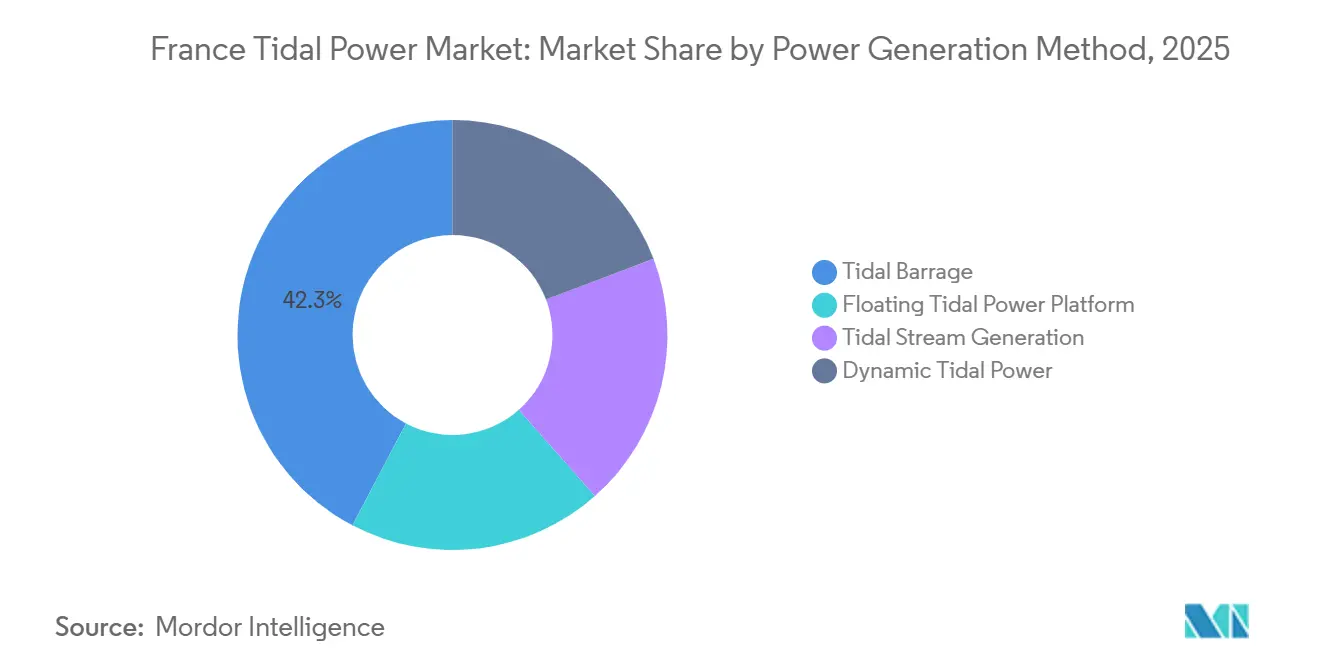

- By power generation method, tidal barrage held 42.3% share of the France tidal power market size in 2025, while floating tidal power platforms are projected to expand at 19.4% CAGR through 2031.

- By tidal energy converters, horizontal axis turbines captured 61.5% share of the France tidal power market size in 2025 and are also set to grow at 17.4% CAGR through 2031.

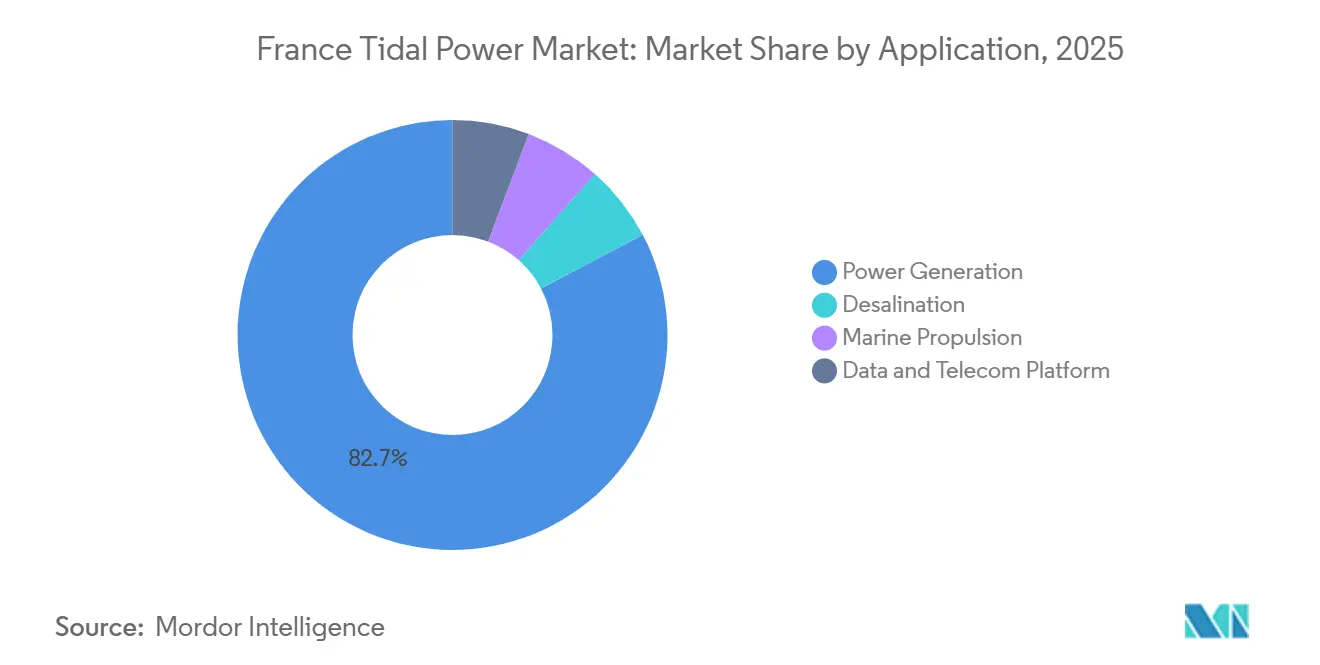

- By application, power generation held 82.7% of France tidal power market share in 2025, while desalination is projected to expand at 20.2% CAGR through 2031.

- By end-user, utilities and IPPs accounted for 61.2% of France tidal power market share in 2025, while the industrial segment is forecast to grow at 16.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Tidal Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust state-backed tidal R&D funding | +2.5% | Normandy, Brittany, with national spillover | Medium term (2-4 years) |

| Forthcoming commercial-scale projects | +3.8% | Normandy coast, North Brittany | Medium term (2-4 years) |

| Coastal grid-congestion relief opportunities | +1.8% | Atlantic and Channel coastal zones | Medium term (2-4 years) |

| Maritime cluster decarbonisation mandates | +1.5% | Cherbourg, Brest, Le Havre, Lorient | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust State-Backed Tidal R&D Funding

France has spent years building the France tidal power market through public support that moved step by step from isolated device trials toward larger arrays that can test installation, maintenance, and revenue models under real operating conditions. The NH1 project alone received EUR 31.3 million, or USD 34.1 million, from the EU Innovation Fund, and that support sits alongside France 2030 backing, which lowers the burden on a first-of-a-kind commercial pilot and gives lenders a stronger public policy signal.[2]European Commission, “Innovation Fund Project Fiche 101191445,” European Commission, ec.europa.euThe same project also received independent validation from the European Investment Bank on its cost reduction path, which matters because future projects in the France tidal power market will be judged not only on turbine design but also on how credible their path to lower power costs looks to investors. Public funding is also creating a wider benefit because environmental and operating data gathered at Raz Blanchard can be reused by later arrays, which reduces duplicated study work and shortens the learning cycle for each new development. This matters in the France tidal power market because early projects carry a high information burden, and every dataset that becomes reusable makes the next project easier to permit and finance. Over time, this approach turns state support from simple capital aid into a shared knowledge base that improves the sector’s overall risk profile.

Forthcoming Commercial-Scale Projects at Raz Blanchard and Paimpol-Bréhat

The strongest near-term growth driver in the France tidal power market is the move from prototypes to pre-commercial arrays at Raz Blanchard and the continued role of Paimpol-Bréhat as a qualification site. FloWatt’s 17 MW farm is progressing with 6 HQ 2.8 turbines being built at CMN’s Cherbourg facility, backed by EUR 75 million, or USD 81.8 million, in French government support and a 20-year feed-in tariff, while commissioning is targeted for 2028. NH1 adds another 12 MW at the same broad development corridor and is also targeted for operation in 2028, which means the France tidal power market will soon be assessed on real array performance rather than only on pilot turbine data. These projects matter beyond their megawatt totals because they are giving domestic manufacturers, subsea suppliers, and marine service companies repeatable work packages that can support lower unit costs on future arrays. Paimpol-Bréhat continues to strengthen this transition because it offers a grid-connected site where developers can validate power curves and operating behavior under French marine conditions before moving into larger projects. As a result, the France tidal power market is starting to look less like a collection of isolated engineering experiments and more like a pipeline with linked testing, manufacturing, and deployment stages.

Coastal Grid-Congestion Relief Opportunities

Grid access is emerging as a practical advantage for the France tidal power market because tidal output is more predictable than most wind and solar generation, which helps system planners size connections with greater confidence. At sites linked to the Raz Blanchard build-out, developers are able to design connection needs around a narrower and better-understood production range, which reduces the risk of building network capacity only for rare production peaks. That predictability also improves the value of each coastal interconnection point, especially in locations where several renewable technologies are competing for limited capacity at the same time. In the France tidal power market, this does not remove connection challenges, but it does improve the quality of the generation profile that reaches the grid. The result is that tidal projects can support coastal power planning in a different way from intermittent sources, which strengthens their case even when headline generation costs remain higher. This effect is still emerging, but it becomes more relevant as the project pipeline moves from single devices to arrays that can supply steadier and more measurable output.

Maritime Cluster Decarbonisation Mandates

France’s major maritime zones are adding demand-side support to the France tidal power market because industrial sites near the coast are looking for lower-carbon power that is local, firm, and less exposed to wholesale price swings. Cherbourg is the clearest example today because turbine manufacturing for FloWatt is taking place there, which links clean power deployment to regional industrial activity instead of treating the two as separate agendas. This local industrial connection matters because marine manufacturing, port operations, and heavy coastal facilities value supply reliability as much as headline price, and that gives tidal energy a practical role in decarbonization planning. In the France tidal power market, this creates a direct link between where the resource sits and where part of the future demand base may come from. The effect is likely to build over time, because industrial users tend to engage only after they see firm policy support, visible projects, and a clearer route to contracted supply. Once those conditions are met, the sector gains a wider customer base than utilities alone, which should support larger array economics and stronger regional supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High levelised cost versus offshore wind | -1.5% | National, affecting financing across all sites | Short term (≤ 2 years) |

| Lengthy environmental approval cycles | -1.2% | Normandy, Brittany, Gulf of Morbihan | Medium term (2-4 years) |

| Limited bankable track record deterring financiers | -1.0% | National | Short term (≤ 2 years) |

| Mining of rare-earth magnets facing NGO opposition | -0.8% | Global supply chain, with local manufacturing relevance in Cherbourg | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Levelised Cost Versus Offshore Wind

High power cost remains the main brake on the France tidal power market because current tidal projects still need support structures that reflect early-stage deployment risk and limited installed volume. The supplied material places current tidal LCOE in a EUR 150 to EUR 350 per MWh range, or USD 163 to USD 381 per MWh, and that level is still well above the cost base expected from more mature offshore renewable technologies. Independent work referenced through Tethys Engineering and ORE Catapult showed that meaningful cost reduction depends on cumulative deployment, with at least 783 MW in France needed to push the cost path below EUR 116 per MWh by 2030. That threshold is important because the current 250 MW policy target helps the France tidal power market, but it is still below the level at which stronger manufacturing learning and supply chain scale effects would be expected to show fully. FloWatt’s feed-in tariff structure suggests policymakers recognize this issue and are protecting early arrays from direct cost competition while the sector builds volume. Until more megawatts are installed and operated, cost will continue to shape which projects move first and how quickly private capital becomes comfortable with the sector.

Lengthy Environmental Approval Cycles

Permitting is another major restraint for the France tidal power market because long review cycles delay revenue visibility and raise pre-construction costs for developers that are already working with new technology. The supplied material notes that offshore energy installations in France can take 6 years from project award to commissioning, which is a difficult timeline for lenders and equity investors to carry in a high-capex sector. The March 2025 Conseil d’État decision that annulled the environmental authorization for the Morbihan Gulf tidal project showed that approval risk does not end once a permit is secured, because legal challenges can still reverse years of preparatory work. In the France tidal power market, that kind of uncertainty affects financing as much as compliance, since lenders usually want final environmental clearance before committing long-term debt. It also hurts smaller developers more than larger ones because they have less balance sheet capacity to carry long development periods. Even when the policy direction is supportive, slow approvals can hold back real capacity growth by widening the gap between project announcement and project execution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Generation Method: Tidal Barrage Dominates, Floating Platforms Set to Redefine Growth

Tidal barrage accounted for 42.3% of installed capacity in 2025, which made it the largest power generation method in the France tidal power market because France still carries a legacy base of barrage infrastructure. That installed base gives the segment a lead that is rooted in existing assets rather than in the strongest future project flow. Tidal stream generation ranked behind barrage, but it is a part of the France tidal power industry that is receiving the clearest commercial momentum from the Raz Blanchard pipeline. Dynamic tidal power remained at a conceptual stage in France, with no meaningful installed position in the current capacity mix. Floating tidal power platforms are forecast to expand at 19.4% CAGR through 2031, which makes them the strongest growth pocket within this split. Their appeal comes from the ability to work in deeper and faster-flowing waters where bottom-fixed designs are harder to deploy, maintain, or scale. This matters at sites such as Raz Blanchard, where water depth and operating conditions can limit the practical use of conventional foundations. As a result, floating systems are moving from a niche engineering idea toward a real growth lever for the France tidal power market.

The second part of the story is operational rather than purely technical, because floating systems can be assembled and checked onshore before tow-out, which reduces the time crews need to spend in harsh marine conditions. That matters in high-energy channels where weather windows are short and vessel costs are high, since a smaller offshore work scope can visibly change project economics. EEL Energy is targeting in-situ marine testing for its 1 MW biomimetic tidal generator by 2026, which shows that new platform approaches are still entering the field even as the market begins to consolidate around larger array developers. France Energies Marines has also highlighted hydrodynamic and environmental research at Raz Blanchard through its tidal stream programs, and those data will support better array layout decisions for future platform deployments. In practical terms, the floating segment expands site accessibility for the France tidal power market rather than simply adding another device category. It also gives developers more flexibility on maintenance strategy because some interventions can be done with tow-back procedures instead of full offshore heavy-lift work. That combination of broader site access and shorter marine installation windows explains why the growth outlook is stronger here than in the more mature barrage segment. It also suggests that future capacity additions will be shaped more by deployability and serviceability than by installed legacy infrastructure.

By Tidal Energy Converters: Horizontal Axis Turbines Lead Across Both Share and Growth

Horizontal axis turbines held 61.5% of installed capacity in 2025 and are also projected to grow at 17.4% CAGR through 2031, which gives them a rare position as both the largest and the fastest-growing converter type in the France tidal power market size. That lead reflects a mix of technical maturity, wider lender familiarity, and direct alignment with flagship French projects that are now moving toward commercial operation. The NH1 project is built around Proteus AR3000 turbines rated at 3 MW each with a 24-meter rotor diameter, and the project’s cost pathway received independent validation through the European Investment Bank process. This gives the horizontal axis category a strong reference point at a time when the France tidal power market is starting to value bankability and standardization more heavily than novelty alone. The category also benefits from the fact that larger projects can source more structured performance evidence from these machines than from less mature alternatives. In an early commercial market, that matters because developers need technologies that can satisfy insurers, public funders, and debt providers at the same time. For now, horizontal-axis turbines sit closest to that requirement set. Their continued scale-up should therefore shape both the supply chain and the financing standards applied across future projects.

Vertical axis turbines still retain a meaningful role, largely because HydroQuest’s design is the basis of the FloWatt farm and has already been tested at Paimpol-Bréhat under demanding operating conditions. FloWatt reported full availability over a 2-year campaign at the test site, which gives the vertical axis concept a practical operating credential, even though its market position is smaller than that of horizontal axis turbines. Other tidal energy converters, including biomimetic systems, remain small in installed terms but still matter because they expand the innovation base of the France tidal power industry. EEL Energy’s work on a membrane-based device shows that alternative architectures are still being pursued where developers see potential gains in flow capture, durability, or maintenance handling. Even so, qualification standards and investor expectations continue to favor converters with stronger testing histories and clearer operating records. This is why the near-term market will likely stay centered on the more established turbine families. Over time, alternative converters may find room in specialized applications or difficult site conditions rather than in the first wave of larger arrays. The balance of evidence still points to horizontal axis machines as the reference design for the France tidal power market over the current forecast period.

By Application: Power Generation Dominates While Desalination Redefines Market Boundaries

Power generation commanded 82.7% of installed tidal capacity in 2025, which made it the dominant application in the France tidal power market because nearly all active projects are still built around electricity export to the grid. That dominance is logical at this stage, since project finance and public support mechanisms are easier to structure around power sales than around newer use cases. Desalination is the fastest-growing application, however, with a projected 20.2% CAGR through 2031, which shows that the France tidal power market is starting to stretch beyond pure electricity generation. The main reason is not large-scale water scarcity in mainland France, but the usefulness of predictable marine power for island and isolated coastal systems that still depend heavily on imported fuels. Marine propulsion and data and telecom platforms remain small today, but both segments fit the steady-output profile of tidal generation better than many intermittent alternatives. Reliability matters more than lowest unit cost in those uses, especially where downtime has a high operational penalty. This is why smaller applications can still become strategically important even if they do not represent the largest near-term capacity blocks. Their growth broadens the role of the France tidal power market and reduces dependence on a single revenue logic.

The desalination opportunity is best understood as a system-level choice for isolated communities rather than as a mass-market water solution. Ushant offers a practical reference because the D10 turbine there has been kept in operation under Inyanga’s control, maintaining grid supply on an island system where supply reliability carries obvious value beyond simple energy pricing. That type of operating example supports the case for pairing predictable tidal output with local water treatment or other essential services in places where diesel displacement matters. France Energies Marines has also highlighted the OPTILE research program, which focuses on optimization for isolated grid supply and helps frame how hybrid island systems can be assessed and designed. In that sense, the application mix is widening because the France tidal power market can serve communities that need resilient local infrastructure, not only large utilities that want bulk renewable generation. The desalination segment, therefore, represents a change in use case as much as a change in technology. It also shows how the sector can create value where firm local service matters more than absolute cost parity with mainstream renewables. Over the forecast period, this should keep power generation dominant while giving desalination a much faster expansion rate from a smaller base.

By End-User: Utilities Anchor Capacity While Industrial Demand Accelerates

Utilities and IPPs held 61.2% of France’s tidal capacity in 2025, which means they remain the anchor buyers and project sponsors in the France tidal power market. This reflects where the current project base sits, because utility-linked or independently financed generation assets are still the easiest way to move tidal power from engineering concept to grid-connected business case. EDF remains structurally important through its role at Paimpol-Bréhat, where the test site includes around 15 km of submarine cable and a direct link to the French grid. That infrastructure role matters even when EDF is not the turbine developer, because access to grid-connected testing and marine know-how shapes who can qualify equipment at a commercial standard. The industrial segment is forecast to grow at 16.7% CAGR through 2031, which makes it the fastest-growing end-user group in the France tidal power market. This is closely tied to coastal manufacturing clusters, especially around Cherbourg, where turbine production and marine engineering activity create a clearer direct use case for local low-carbon supply. In practical terms, the industrial segment is growing because some coastal facilities want firmer renewable power than wind and solar can provide on their own. That gives tidal developers a possible path toward contracted demand beyond the traditional utility route.

Commercial demand is smaller, but it is not insignificant for the France tidal power market because coastal tourism, port-side businesses, and aquaculture operators also face growing pressure to manage energy cost and carbon exposure. These users are less likely to anchor the first large arrays, but they can support diversified off-take structures once operating performance is proven and pricing becomes more predictable. The presence of local industrial and commercial demand also helps reduce the sector’s dependence on one buyer class, which is important in a market that is still maturing. In the France tidal power industry, that wider demand base could eventually improve financing flexibility because lenders tend to favor revenue sources that are not tied to a single policy mechanism. Utilities and IPPs will still lead the near-term market, since they control most development rights, grid relationships, and capital access. Even so, industrial demand is becoming more relevant because it sits close to the resource, close to the supply chain, and close to the decarbonization challenge that the sector is trying to solve. This makes the end-user mix gradually more balanced, even if the installed base still leans heavily toward utility-linked projects today. The shift will likely be slow, but it could become one of the more important structural changes in the France tidal power market after the first pilot arrays are operating.

Geography Analysis

Normandy is set to carry most of the capacity build-out in the France tidal power market through 2031, with the Raz Blanchard corridor and the wider Cotentin coast forming the main commercial focus. The clearest evidence is the pairing of FloWatt’s 17 MW project and NH1’s 12 MW project, both of which are progressing toward 2028 operation and give Normandy the strongest near-term project visibility in the country. Public support has also been concentrated here, with NH1 receiving EUR 31.3 million, or USD 34.1 million, from the EU Innovation Fund and FloWatt receiving EUR 20 million, or USD 21.8 million, from the same program in addition to French government backing. The presence of Cherbourg reinforces Normandy’s lead as a manufacturing and maritime services base, which means the region combines resource quality, project activity, and industrial support in one geography. That combination gives Normandy an advantage that goes beyond raw resource strength, because developers can source fabrication, logistics, and marine support closer to the deployment corridor.

Brittany remains the second major geography in the France tidal power market, centered on the Forêt de la Forêt Strait and the Paimpol-Bréhat test site in Côtes d’Armor. Paimpol-Bréhat is especially important because it is a full-scale offshore tidal turbine test site connected to the French national grid, with an operating history that gives developers a practical route to equipment qualification under real sea conditions. This makes Brittany central to validation work, even if it may not match Normandy’s near-term project pipeline in absolute megawatts. The region also benefits from accumulated operational experience, which is valuable in a sector where performance proof matters as much as theoretical resource strength. Scientific work on the Fromveur area shows why site detail matters, because local flow asymmetry and seabed effects can influence turbine layout and energy extraction in ways that are not visible from headline resource maps alone. For the France tidal power market, that means Brittany’s role is not only to host projects but also to reduce technical uncertainty before larger arrays move ahead elsewhere.

Island locations form a smaller but distinct part of the France tidal power market, with Ushant showing how tidal generation can support isolated systems where diesel displacement has direct economic and operational value. Inyanga Marine Energy Group took over operation of the D10 turbine in the Fromveur Passage and secured permissions through August 2028, which keeps France’s first grid-connected tidal turbine active and preserves a live island reference case. Research by France Energies Marines and related marine programs is also improving the evidence base for environmental and hydrodynamic effects, which is important for future projects in sensitive coastal and island waters. These smaller geographies will not define the total capacity of the France tidal power market, but they could play an outsized role in proving hybrid local energy models such as power plus desalination or other critical services.

Competitive Landscape

The France tidal power market is fragmented at the technology level but more concentrated at the active project level, because only a small group of developers currently combine site access, funding support, and credible delivery plans. HydroQuest and Qair are advancing FloWatt, Normandie Hydroliennes is leading NH1, and EEL Energy remains active on an alternative biomimetic technology path, which gives the market more than one technical route but not a crowded field of bankable developers. Industrial groups such as CMN Naval and EDF play key roles further up the value chain through manufacturing and infrastructure, which means influence in the France tidal power market is not limited to turbine designers alone. Because France is still in a pre-commercial phase, competition is shaped less by pure price and more by execution credibility, technology validation, and the ability to convert public support into operating assets. That keeps rivalry meaningful, but it also limits the field to players that can carry long development cycles and complex marine work.

Recent strategic moves show this clearly. In 2026, HydroQuest and Qair began construction of 6 turbines for the 17 MW FloWatt farm at CMN’s Cherbourg yard, which ties technology deployment to domestic industrial capacity and gives the project a visible manufacturing base. Normandie Hydroliennes also confirmed active delivery work for NH1 and is targeting financial close by December 2026, with entry into operation planned for December 2028. Inyanga’s takeover of the D10 turbine at Ushant was another notable move, because it preserved an operating tidal asset in France after Sabella’s liquidation and gave an external player a direct platform inside the market. EEL Energy is taking a different route by pushing its biomimetic generator toward marine testing, which shows that novel concepts are still trying to secure a foothold before the France tidal power market settles around a narrower set of commercial standards. Together, these moves show a market where strategic positioning depends on who can prove delivery, not only on who can present the most original design.

The failure of Sabella remains an important competitive signal because it showed how exposed single-asset developers can be when financing and route-to-market support are not secure. In the France tidal power market, financing readiness and permitting strength can be just as decisive as turbine performance, especially when project timelines are long and marine installation risk is high. That gives an advantage to companies that can combine technology with manufacturing partners, testing access, and institutional support. It also means leadership in the France tidal power market is likely to remain with a small number of developers and partners that can move from pilot success to repeat deployment without losing financial discipline. The market is active and competitive, but it is not yet broad enough to support many parallel commercial winners at scale.

France Tidal Power Industry Leaders

Sabella SAS

HydroQuest SAS

EDF Renewables (tidal assets)

Naval Energies

Nova Innovation Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: France PPE3 confirms 250 MW tidal allocation and first commercial tender by 2030. France’s Multiannual Energy Plan formally designated tidal stream energy as a pillar of the national energy mix, giving the France tidal power market better visibility for future investment in manufacturing, turbines, and installation capability.

- February 2026: Normandie Hydroliennes advances NH1 delivery activities. The company confirmed active delivery work for the 12 MW NH1 pilot farm at Raz Blanchard, with financial close targeted for December 2026 and entry into operation planned for December 2028.

France Tidal Power Market Report Scope

Tidal energy is a form of power produced by the rise and fall of tides caused by the gravitational interaction between the Earth, the sun, and the moon. Tidal currents with sufficient energy for harvesting occur when water passes through a constriction, causing the water to move faster.

The France Tidal Power Market is segmented into generation method, energy converters, application, end-user, and geography. By generation method, the market is segmented into tidal barrage, floating tidal platform, tidal stream, and dynamic tidal power. By energy converters, the market is segmented into horizontal axis turbine, vertical axis turbine, and others. By application, the market is segmented into power generation, desalination, marine propulsion, and data and telecom applications. By end-user, the market is segmented into utilities and independent power producers (IPPs), industrial, and commercial sectors. For each segment, the market sizing and forecasts have been done on the basis of volume (MW).

By Power Generation Method

| Tidal Barrage |

| Floating Tidal Power Platform |

| Tidal Stream Generation |

| Dynamic Tidal Power |

By Tidal Energy Converters

| Horizontal Axis Turbine |

| Vertical Axis Turbine |

| Other Tidal Energy Converters |

By Application

| Power Generation |

| Desalination |

| Marine Propulsion |

| Data & Telecom Platforms |

By End-User

| Utilities and IPPs |

| Industrial |

| Commercial |

| By Power Generation Method | Tidal Barrage |

| Floating Tidal Power Platform | |

| Tidal Stream Generation | |

| Dynamic Tidal Power | |

| By Tidal Energy Converters | Horizontal Axis Turbine |

| Vertical Axis Turbine | |

| Other Tidal Energy Converters | |

| By Application | Power Generation |

| Desalination | |

| Marine Propulsion | |

| Data & Telecom Platforms | |

| By End-User | Utilities and IPPs |

| Industrial | |

| Commercial |

Key Questions Answered in the Report

How fast is tidal capacity in France expected to grow through 2031?

Installed capacity stood at 270 MW in 2026 and is forecast to reach 490 MW by 2031, which implies 12.63% CAGR over 2026 to 2031.

What is driving project activity in Normandy?

Normandy holds the clearest near-term pipeline because FloWatt and NH1 are both advancing at Raz Blanchard, supported by EU and French public funding and a strong Cherbourg supply base.

Which technology is leading deployment today?

Horizontal axis turbines lead with 61.5% of installed capacity in 2025 and are also the fastest-growing converter type at 17.4% CAGR through 2031.

Why is desalination growing faster than other applications?

Desalination starts from a smaller base, but it fits island and isolated coastal systems where predictable tidal output can replace diesel-based energy services.

What is the main challenge holding back wider rollout?

Cost and permitting remain the main barriers, because current tidal LCOE is still high and environmental approvals can take years before financing closes.

Who are the key active players in France today?

The most visible active names in the supplied material are HydroQuest, Qair, Normandie Hydroliennes, EEL Energy, EDF, CMN Naval, and Inyanga Marine Energy Group.

Page last updated on: