Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

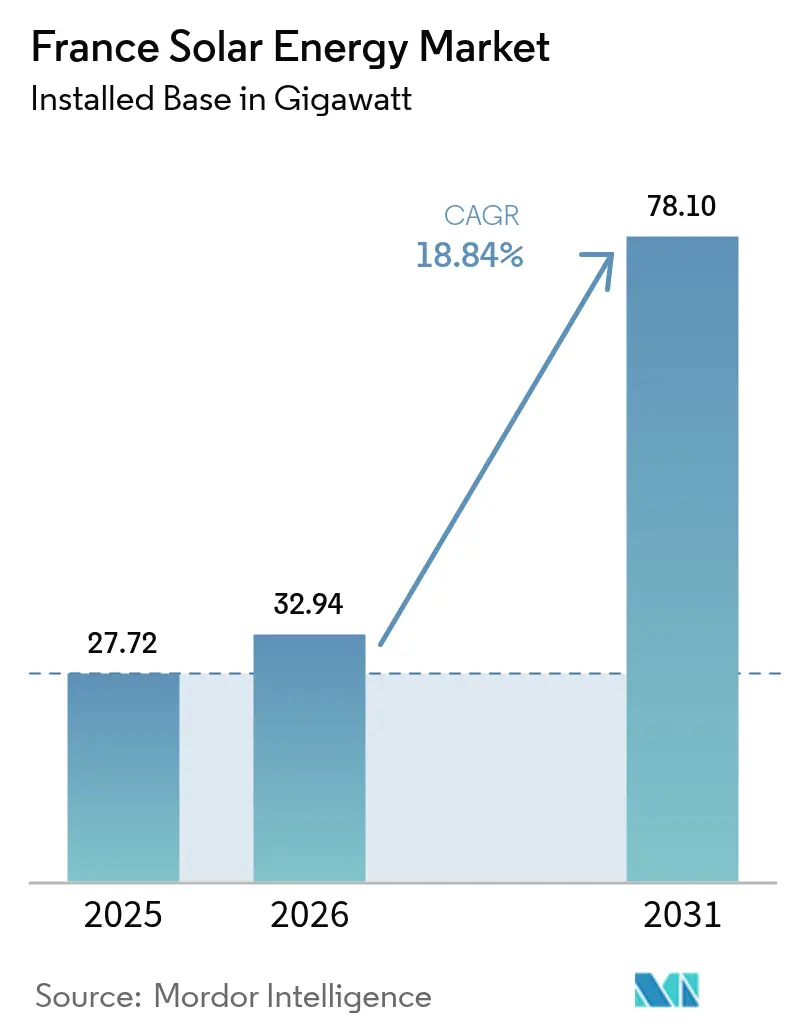

| Base Year Market Size (2025) | 27.72 gigawatt |

| Market Volume (2026) | 32.94 gigawatt |

| Market Volume (2031) | 78.1 gigawatt |

| Growth Rate (2026 - 2031) | 18.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Solar Energy Market Analysis by Mordor Intelligence

France Solar Energy Market size in 2026 is estimated at 32.94 gigawatt, growing from 2025 value of 27.72 gigawatt with 2031 projections showing 78.1 gigawatt, growing at 18.84% CAGR over 2026-2031.

Government policies that shifted from feed-in tariffs to 20-year contract-for-difference (CfD) auctions have preserved developer returns even as clearing prices fell below EUR 60/MWh, reinforcing investor confidence. Mandatory photovoltaic (PV) deployment on large parking lots and commercial rooftops under the 2023 APER law, combined with the national 60 GW target in the draft PPE3 plan, adds structural momentum to the France solar energy market. Technology learning curves that lowered utility-scale levelized cost of electricity (LCOE) to EUR 42-48/MWh in 2024, as well as rising corporate power-purchase agreements (PPAs), further stimulate capacity additions.[1]International Renewable Energy Agency, “Renewable Power Generation Costs 2024,” irena.org Competitive intensity is rising as integrated utilities and independent power producers pivot toward bifacial modules, single-axis trackers, and co-located battery storage to meet grid-stability requirements.

Key Report Takeaways

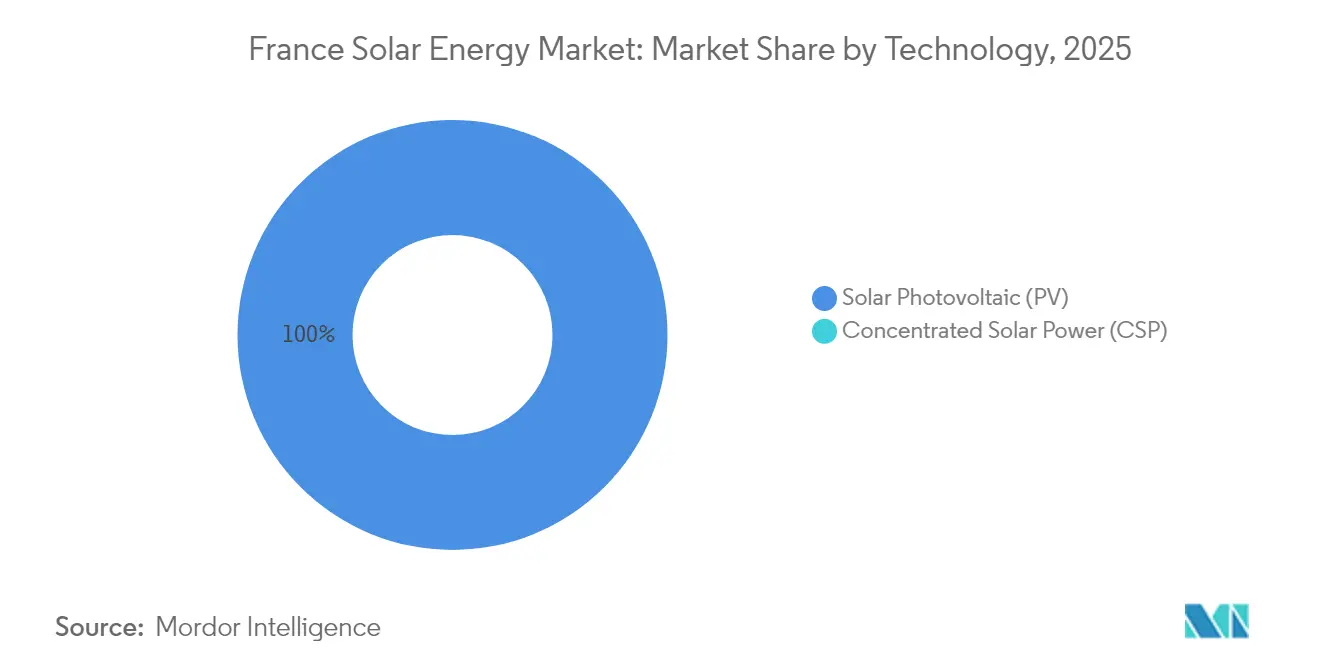

- By technology, solar photovoltaic held 100.00% of the France solar energy market share in 2025 and is expanding at a 18.84% CAGR through 2031.

- By grid type, on-grid systems commanded 99.03% of the France solar energy market size in 2025 and are accelerating at a 20.02% CAGR between 2026-2031.

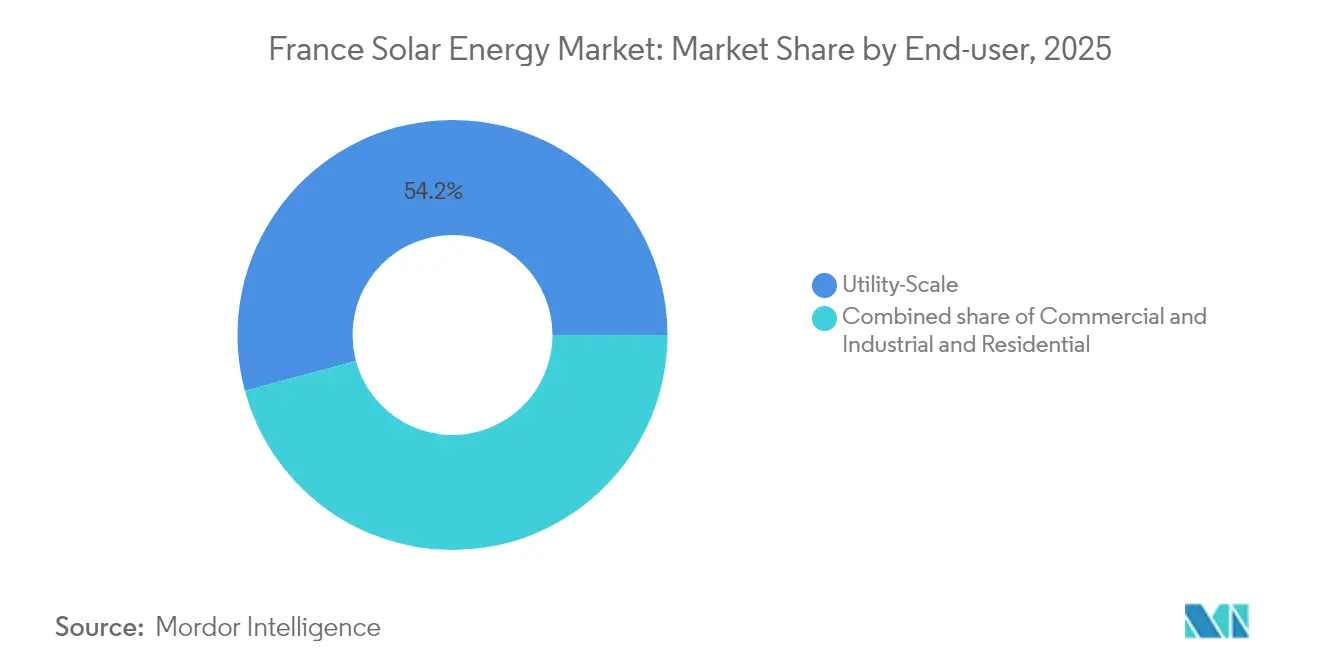

- By end user, commercial and industrial installations are growing at a 24.05% CAGR to 2031, while utility-scale projects retained a 54.18% France solar energy market in 2025.

- EDF Renewables, ENGIE, TotalEnergies, Neoen, and Voltalia collectively controlled nearly 40% of the project pipeline in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FiT-to-CfD transition sustaining investor IRR | +3.20% | National, with early gains in Occitanie, Nouvelle-Aquitaine, Provence-Alpes-Côte d'Azur | Medium term (2-4 years) |

| Declining LCOE & auction clearing prices | +4.10% | National, concentrated in southern high-irradiance regions | Short term (≤ 2 years) |

| 2030 Solar Plan: 60 GW target | +5.80% | National, policy-driven acceleration across all regions | Long term (≥ 4 years) |

| Mandatory PV on parking lots & large roofs | +2.70% | National, urban and peri-urban zones with commercial density | Medium term (2-4 years) |

| Agri-PV pilots unlocking farmland pipeline | +1.90% | Rural regions: Occitanie, Nouvelle-Aquitaine, Pays de la Loire | Long term (≥ 4 years) |

| Hybrid PV-storage design in CRE tenders | +1.60% | National, grid-constrained areas prioritizing dispatchability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FiT-to-CfD Transition Sustaining Investor IRR

The move from administratively set tariffs to competitive CfD auctions cut taxpayer exposure while giving developers 20-year revenue certainty. The 2024 ground-mounted tender cleared at EUR 54.45/MWh versus EUR 63.3/MWh a year earlier, yet unlevered internal rates of return held near 7-8% as banks underwrite contracted cash flows instead of merchant prices. Independent power producers captured 48% of the awarded volume, proving that CfDs democratize participation and diversify the France solar energy market. Bid-bond forfeiture clauses now oblige developers to reach financial close within 18 months, prompting early grid-connection reservations and more rigorous due diligence practices. The structure also allows the state to claw back excess revenues if spot prices exceed the strike price, preserving public support for renewables.

Declining LCOE and Auction Clearing Prices

Utility-scale LCOE fell to EUR 42-48/MWh in 2024 as bifacial efficiencies hit 21-22% and tracker adoption boosted yields by 15-20%. Rooftop auctions mirrored this decline, averaging EUR 89/MWh for 100-500 kW systems in 2024, down from EUR 105/MWh in 2023. Developers responded by streamlining supply chains and standardizing designs to protect double-digit margins. Corporate buyers quickly seized the opportunity: a 15-year PPA signed by TotalEnergies in 2024 priced power at EUR 52/MWh, which is cheaper than retail tariffs and below grid parity.[2]TotalEnergies, “Solar PPA Press Release, 2024,” totalenergies.com Lower generation costs have shortened payback periods for behind-the-meter arrays to under six years, catalyzing distributed adoption in the France solar energy market.

2030 Solar Plan 60 GW Target

The draft PPE3 plan obliges France to triple installed solar capacity by 2030, translating into 6-8 GW of annual additions. CRE boosted ground-mounted auction volumes to 3 GW per year, with an extra 2 GW earmarked for rooftop and agri-PV installations, ensuring project-pipeline visibility. Regions tailor implementation: sun-rich Occitanie plans 12 GW by 2030, while densely populated Île-de-France relies on rooftop deployment to balance land use. RTE estimates that EUR 100 billion of network strengthening is needed by 2035 to absorb renewable penetration above 50%, underlining the importance of synchronized grid investment. Without it, up to 10 GW of awarded projects risk being stranded, tempering the otherwise robust outlook for the France solar energy market.

Mandatory PV on Parking Lots and Large Roofs

Under the 2023 APER legislation, parking lots above 1,500 m² and rooftops larger than 500 m² must install PV between 2026 and 2028. The rule could unlock 3-5 GW of distributed capacity, especially for retail, logistics, and industrial sites. Companies such as Carrefour announced a 200 MW program in 2024, while Amazon targets 150 MW across its French fulfillment network. Turn-key leasing and third-party ownership models allow property owners to comply without capex. Technical barriers remain, roof-load limits, fire codes, and grid upgrades, but compliant projects benefit from self-consumption rules that let offtakers use up to 80% of generation on-site.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid connection queue & permitting delays | -2.80% | National, acute in Occitanie, Nouvelle-Aquitaine, Provence-Alpes-Côte d'Azur | Short term (≤ 2 years) |

| Land-use & biodiversity opposition | -1.40% | Rural and peri-urban zones with agricultural or protected land designations | Medium term (2-4 years) |

| Module price volatility amid global oversupply | -1.10% | National, supply-chain dependent developers | Short term (≤ 2 years) |

| Rising local-content requirements raising capex | -0.90% | National, EU-wide regulatory compliance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Connection Queue and Permitting Delays

Average connection times lengthened to 18-24 months in 2024 as RTE’s substations could not keep up with the surge in applications. Environmental impact assessments now take 12-18 months under stricter biodiversity rules, while appeals add up to another year, placing 20-25% of auctioned capacity in danger of missing commissioning deadlines. Although fast-track procedures for projects along railways and highways were introduced in 2024, higher land costs have slowed uptake. Funding constraints also loom; RTE invests EUR 2-3 billion annually against a EUR 100 billion need through 2035, implying sustained bottlenecks that could dampen the France solar energy market.

Module Price Volatility

Chinese polysilicon oversupply drove module prices down by 35-40% between 2023 and mid-2024, then threatened to rebound once anti-dumping probes began in Europe. Price swings undermined fixed-price engineering, procurement, and construction contracts signed months earlier, compressing margins by up to 12% and prompting renegotiations. Tariffs as high as 25% could lift module costs by EUR 0.03/W, inflating capex by 5-7%. Larger players hedged by signing multi-year deals with Southeast Asian suppliers, but smaller developers lack bargaining power, increasing financing costs by 25–50 basis points as lenders demand price-escalation clauses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominance Reflects Insolation Profile

Solar photovoltaic accounted for 100.00% of installations, underscoring the absolute dominance of PV within the France solar energy market at 27.72 GW in 2025. Concentrated solar power (CSP) remains commercially absent because direct normal irradiance seldom exceeds 1,400 kWh/m², far below the threshold for CSP viability. Crystalline-silicon modules hold 95% share, while bifacial panels now appear in 45% of ground-mounted arrays, improving yields by 10-15%. Perovskite-silicon tandem cells reached 28% efficiency in pilot settings, hinting at future upgrades. Floating PV is small but growing on reservoirs where land is scarce, and CRE tenders continue to prioritize hybrid projects that integrate storage.

The France solar energy market benefits from rapid technology maturity, evidenced by single-axis tracker penetration of 60% in southern provinces and digital asset-management tools that raise performance ratios by 2-3 percentage points. Policy levers reinforce PV’s edge; 80% of auction capacity is allocated to ground-mounted and rooftop PV, with the rest reserved for hybrid or agri-PV designs. Looking ahead, domestic module factories such as Carbon’s 3.4 GW heterojunction facility improve supply-chain resilience and may satisfy local-content rules by 2026.

By Grid Type: On-Grid Systems Drive Scale

On-grid assets represented 99.03% of the 2025 France solar energy market share and are forecast to grow at a 20.02% CAGR to 2031, outpacing total additions because of CRE auction volumes and corporate PPAs. Utility-scale plants above 5 MW supplied 54.50% of on-grid capacity, whereas rooftop commercial systems captured 35.00% and residential 10.50%. Developers leverage CfDs for bankable revenue streams, while C&I clients deploy behind-the-meter arrays to dodge EUR 0.18/kWh retail tariffs and network fees.

Off-grid deployments stay below 1% of the France solar energy market size, limited to island territories and remote farms. However, rising diesel costs encourage hybrid mini-grids on Corsica, where EDF installed 12 MW of solar-battery capacity in 2024. Net-metering for surplus generation is capped at EUR 0.10/kWh, a rate under review as grid operators reassess cost-recovery mechanisms amid higher distributed penetration.

By End User: C&I Segment Accelerates on PPA Economics

Utility-scale plants held a 54.18% France solar energy market share in 2025, but commercial and industrial sites show the fastest expansion at 24.05% CAGR through 2031, facilitated by mandatory rooftop rules and accessible third-party financing. Paybacks are now below six years as PV LCOE slips to EUR 0.08-0.10/kWh, well under retail tariffs. Corporate PPAs surged to 850 MW in 2024, closing the gap between green-power demand and supply.

Residential arrays add diversity yet contribute only 10.00% of capacity because average system sizes are under 5 kW, and financing choices remain scarce. Still, feed-in tariffs of EUR 0.13-0.17/kWh, coupled with rising electricity prices, foster a 14.58% CAGR in household uptake. Utility-scale growth continues at 16.44% CAGR, but land-use conflicts and permitting delays impose greater execution risk.

Geography Analysis

Southern regions, Occitanie, Provence-Alpes-Côte d’Azur, and Nouvelle-Aquitaine, made up 54.65% of national capacity in 2025 because irradiance exceeds 1,600 kWh/m² and land for utility-scale arrays is abundant. Occitanie alone operates 8 GW and targets 12 GW by 2030 through streamlined agri-PV rules that permit dual land use, yet grid queues create 12-18-month commissioning lags. Provence-Alpes-Côte d’Azur trials floating PV and requires EUR 1.2 billion of grid upgrades to absorb its 4.5 GW fleet. Nouvelle-Aquitaine is a hotspot for agri-PV pilots, tallying 250 MW of viticulture-compatible capacity in 2024.

Northern provinces, Île-de-France, Hauts-de-France, and Grand Est, account for 40.35% of installations. Île-de-France added 400 MW of rooftops in 2024 despite lower sun hours, propelled by APER compliance and data-center PPAs. Brownfield redevelopment drives utility-scale growth in Hauts-de-France and Grand Est, where 600 MW went online in 2024 on remediated industrial land. Corsica and overseas departments comprise 5.00% of capacity, with dedicated CRE tenders and tariffs of EUR 0.18-0.22/kWh to offset higher logistics costs.

The locational mix is set to rebalance modestly as rooftop mandates lift northern share, yet superior irradiance secures southern leadership. Regional permitting timelines still vary markedly: 10-12 months in Occitanie versus up to 18 months in Île-de-France, a disparity that influences site selection. RTE’s investment plan earmarks 60% of network expenditure for southern corridors, reinforcing the dominant role of these regions in the France solar energy market.

Competitive Landscape

Market concentration is moderate. EDF Renewables, ENGIE, and TotalEnergies pursue scale via CfDs and PPAs, while Neoen, Voltalia, and Akuo Energy harness hybrid storage to differentiate bids. The top five developers control about 40% of the active pipeline, yet niches such as agri-PV and building-integrated PV allow regional specialists, Urbasolar, Photosol, to flourish. Neoen won 1.2 GW of contracts since 2022 by co-locating 100 MW batteries with solar arrays, meeting RTE’s dispatchability criteria. TotalEnergies leverages its retail arm to strike PPAs at EUR 50-55/MWh, locking in 15-year cash flows outside auction cycles.

Agri-PV represents fertile ground: Urbasolar and Photosol hold 30% of the 2024 pipeline by collaborating with farm cooperatives under new dual-use rules. BIPV remains nascent at 80 MW, hampered by limited module supply, but carries long-term promise as retrofits accelerate. Digitalization is the new battleground; asset-management platforms that use predictive algorithms raise energy yields and cut operating expenditure, lifting project IRR by up to 30 basis points. CRE’s innovation criteria reserve 20% of capacity for projects with storage or recycled components, rewarding developers with R&D muscle or ties to European factories like Carbon’s heterojunction line or Holosolis’ planned 5 GW plant.

France Solar Energy Industry Leaders

Engie SA

EDF Renewables

Albioma SA

TotalEnergies SE

Meeco AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: ENGIE announced a EUR 500 million (USD 545 million) investment to develop 1 GW of solar and hybrid storage projects in Occitanie and Nouvelle-Aquitaine by 2027, targeting CRE tender participation and corporate PPA offtake. The portfolio includes 600 MW of ground-mounted solar and 400 MW of co-located battery storage, with commissioning scheduled between 2026 and 2027 to align with grid connection availability.

- September 2024: Neoen secured a 300 MW solar project in Provence-Alpes-Côte d'Azur under the CRE ground-mounted tender, with a clearing price of EUR 54.45/MWh and a 20-year CfD contract. The project integrates 100 MW of battery storage to provide grid balancing services, with financial close expected in Q1 2025 and commissioning in late 2026.

- August 2024: TotalEnergies signed a 15-year corporate PPA with a consortium of French manufacturing plants for 200 MW of solar generation at EUR 52/MWh, below grid parity. The agreement includes a 50 MW rooftop portfolio and a 150 MW ground-mounted project in Nouvelle-Aquitaine, with operations commencing in 2026.

- July 2024: Voltalia commissioned a 120 MW agri-PV project in Occitanie, combining solar generation with sheep grazing across 150 hectares. The project complies with the 2024 agri-PV decree, maintaining 85% light transmission and generating EUR 18 million in annual revenue, split 70-30 between electricity sales and agricultural output.

France Solar Energy Market Report Scope

Solar energy is heat and radiant light from the Sun that can be harnessed with technologies such as solar power (used to generate electricity) and solar thermal energy (used for applications such as water heating).

The France Solar Energy Market is segmented by technology, grid type, and end-user. By technology, the market is segmented into solar Photovoltaic, concentrated solar power. By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial, Industrial, and residential. The report also covers the market size and forecasts for France.

For each segment, the market sizing and forecasts have been done based on the installed capacity (GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How large is the France solar energy market in 2026?

Installed capacity is 27.72 GW in 2025 and is on track to reach 32.94 GW in 2026.

What is the expected capacity of solar power in France by 2031?

The France solar energy market size is forecast to reach 78.10 GW by 2031, based on the 18.84% CAGR over 2026-2031.

Which segment is growing fastest within French solar deployments?

Commercial and industrial rooftops and ground-mount systems expand at a 24.05% CAGR through 2031.

How do CfD auctions benefit solar developers?

They give 20-year price certainty, stabilize unlevered IRR at 7-8%, and reduce reliance on feed-in tariffs.

Where is most French solar capacity located?

Southern regions, Occitanie, Provence-Alpes-Côte d’Azur, and Nouvelle-Aquitaine, hold 54.65% of installations.

Page last updated on: