Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Growth Rate | 12.09% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Distributed Solar Power Generation Market Analysis by Mordor Intelligence

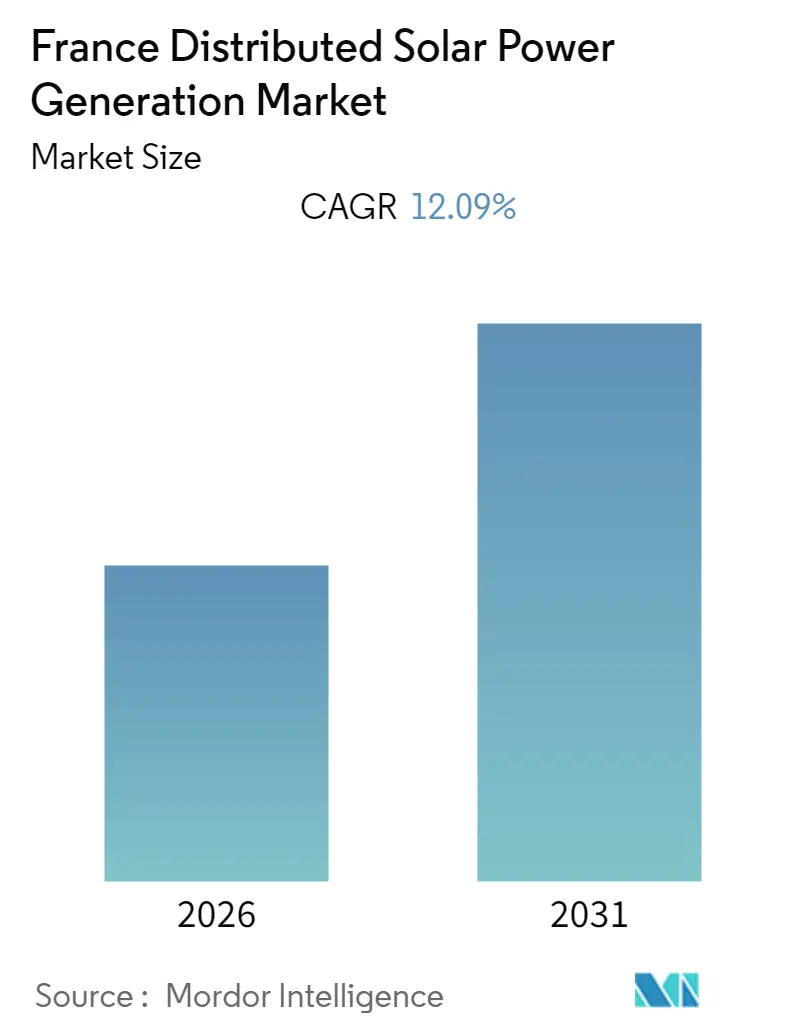

The France Distributed Solar Power Generation Market size is expected to register a CAGR of 12.09% during the forecast period 2026-2031.

- The gradual shift from energy generation from conventional sources such as coal and natural gas to clean energy is expected to help grow France distributed solar power generation market.

- Commercial and industrial sectors are showing a growing interest in distributed solar power generation due to various economic benefits and a constant source of energy to eliminate downtimes and equipment damage due to voltage fluctuations in conventional power grids. This has created a huge opportunity for distributed solar power generation market in the region.

- France is expected to witness significant growth in the forecast period, over rising environmental concerns, and economic benefits of domestic distributed solar power generation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Distributed Solar Power Generation Market Trends and Insights

Increasing Demand for Clean Electricity to Drive the Market

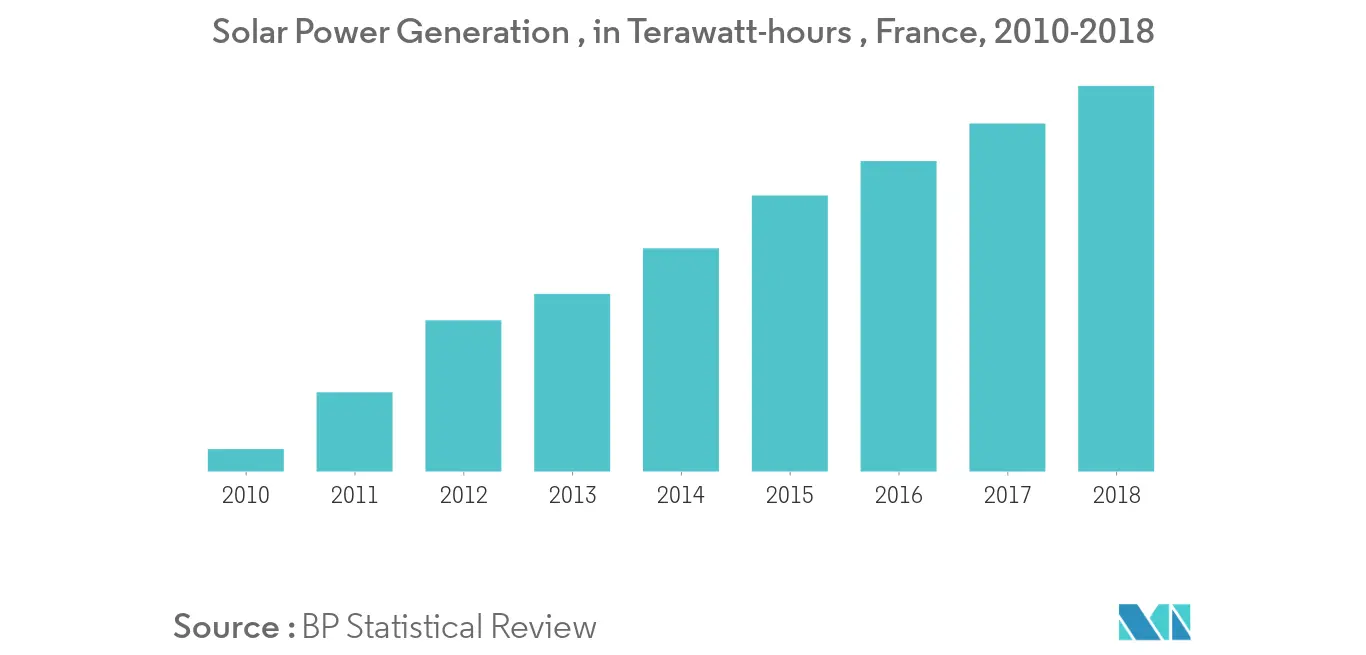

- Increasing demand for clean energy is one of the primary drivers for the distributed solar power generation market in the country. The country has one of the highest electricity generation from nuclear energy in the world just behind the United States, with over 71% of electricity produced from nuclear energy, in 2018.

- Rooftop solar offers the benefits of modern electricity services to households that had no access to electricity, reducing electricity costs on islands and in other remote locations that are dependent on oil-fired generation, as well as enabling residents and small businesses to generate their own electricity.

- Commercial and industrial systems are expected to become the largest growth segment because they are usually more inexpensive and have a relatively stable load profile during the day that can enable larger savings on electricity bills, depending on the policy scheme in place.

- Therefore, the aforementioned factors are expected to drive the market in the forecast period.

Electricity Generation from Nuclear Energy to Restraint the Market

- France is the world's second-largest nuclear electricity producer after the United States. The country produced over 413.2 TWh of electricity from nuclear power, in 2018.

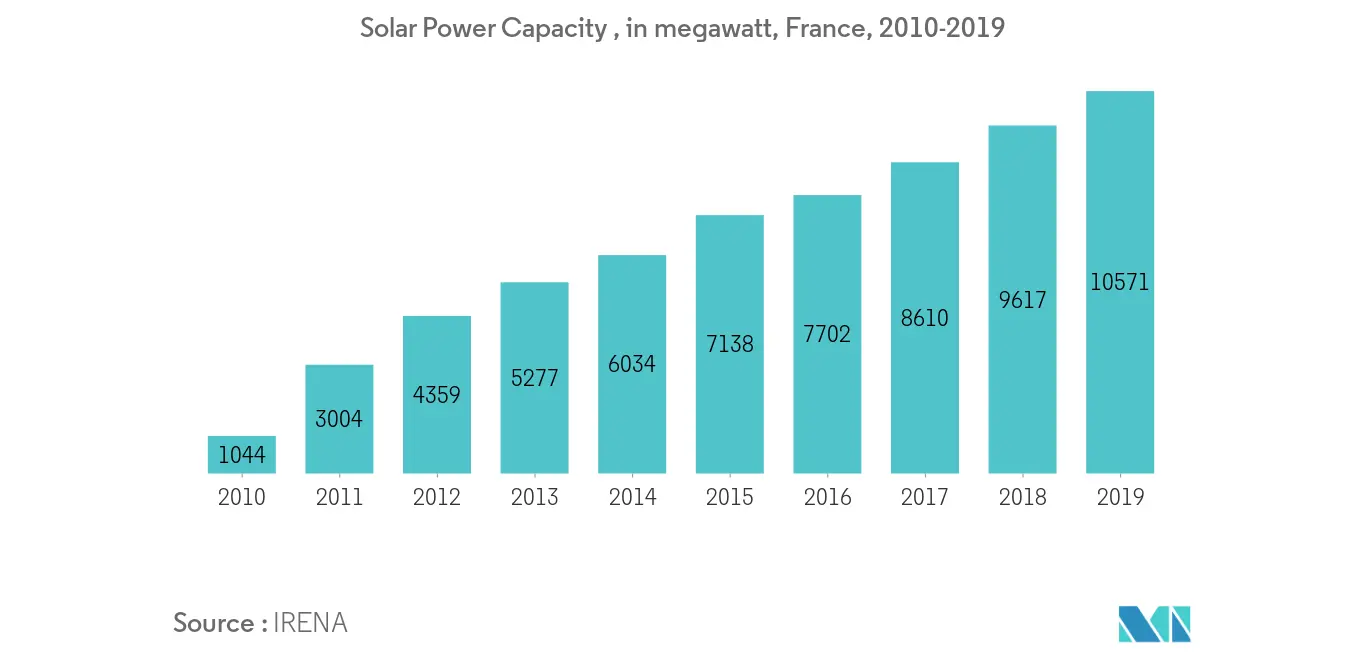

- The country has a history of over a decade of electricity generation from nuclear energy starting before 1960. The country has over 57 nuclear reactors spread over the country.

- Nuclear Energy maintains an edge over other forms of energy generation energy resources in the country due to the long-standing policy based on energy security. France's total nuclear capacity stands at 62.3 GWe.

- Therefore, the cheaper electricity generation from nuclear energy and more reliability on nuclear energy produced electricity is expected to be the major restraint of the distributed solar power generation market in the country.

Competitive Landscape

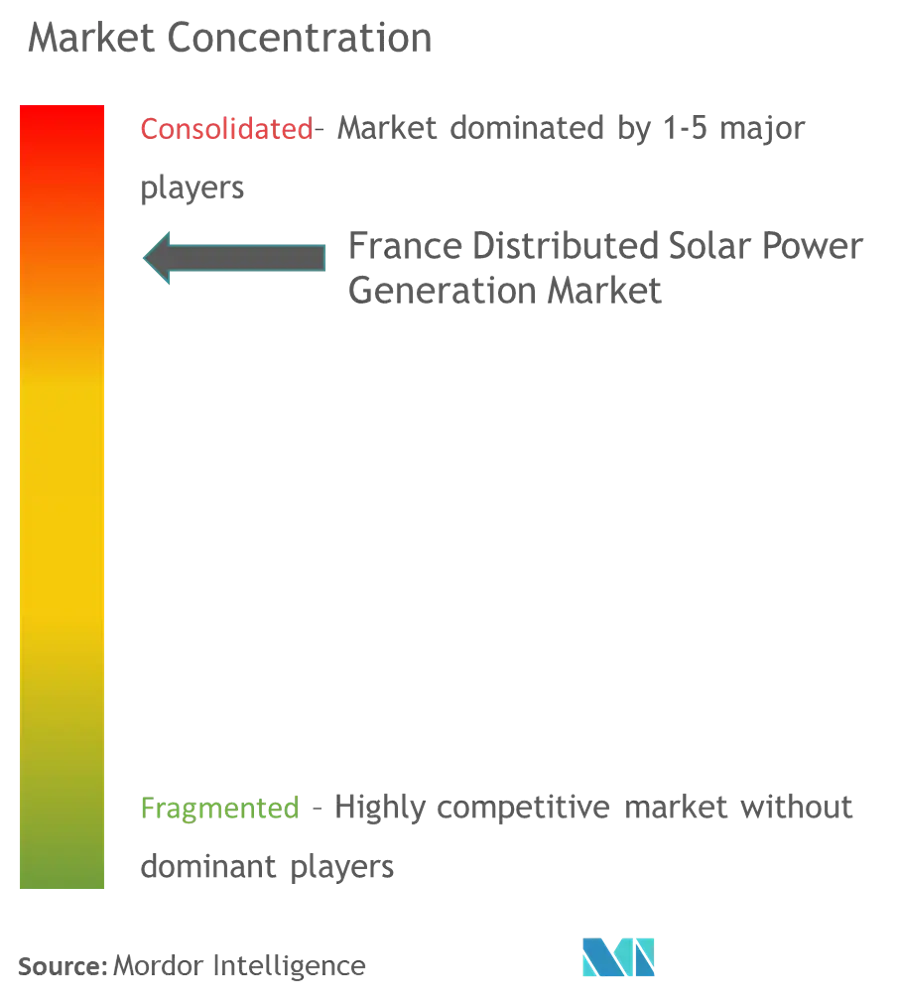

France distributed solar power generation market is partially consolidated. Some of the major companies are ENGIE, Sunpower, EDF EN, Saint Gobain, and Wagner Solar among others.

France Distributed Solar Power Generation Industry Leaders

ENGIE

Sunpower

EDF EN

Saint Gobain

Wagner Solar

- *Disclaimer: Major Players sorted in no particular order

France Distributed Solar Power Generation Market Report Scope

The France distributed solar power generation market report include:

By End-user

| Commercial |

| Residential |

| Industrial |

| By End-user | Commercial |

| Residential | |

| Industrial |

Key Questions Answered in the Report

What is the current France Distributed Solar Power Generation Market size?

The France Distributed Solar Power Generation Market is projected to register a CAGR of 12.09% during the forecast period (2026-2031)

Who are the key players in France Distributed Solar Power Generation Market?

ENGIE, Sunpower, EDF EN, Saint Gobain and Wagner Solar are the major companies operating in the France Distributed Solar Power Generation Market.

What years does this France Distributed Solar Power Generation Market cover?

The report covers the France Distributed Solar Power Generation Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the France Distributed Solar Power Generation Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: