Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

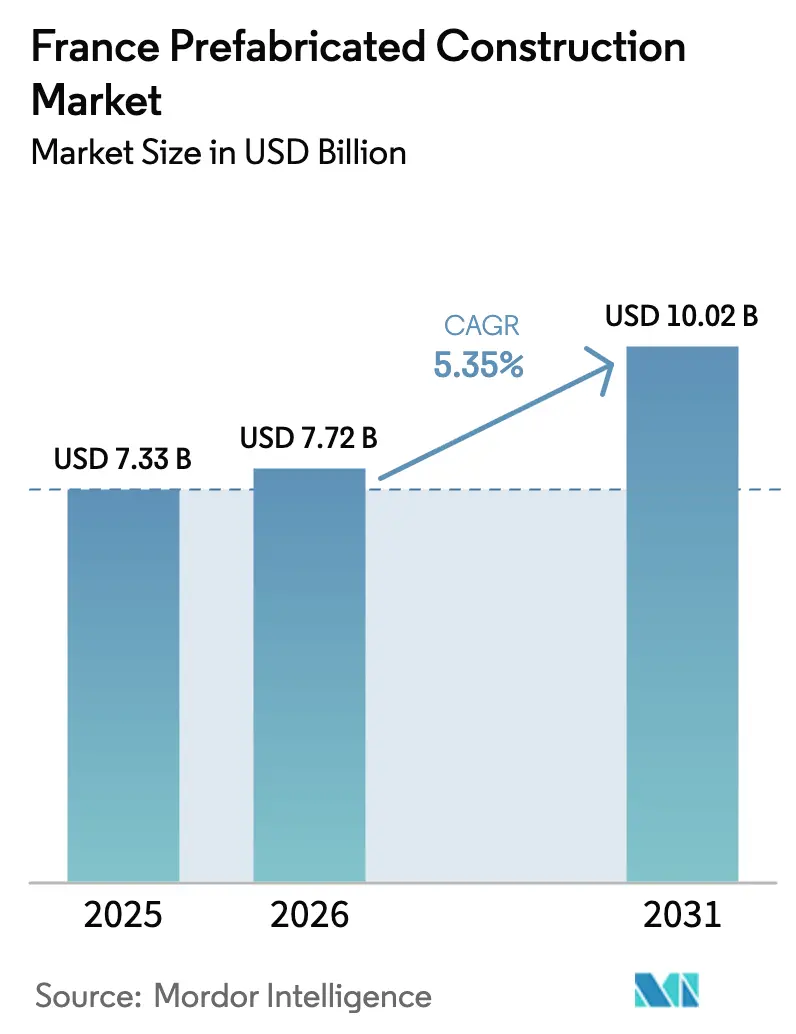

| Base Year Market Size (2025) | USD 7.33 Billion |

| Market Size (2026) | USD 7.72 Billion |

| Market Size (2031) | USD 10.02 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Prefabricated Construction Market Analysis by Mordor Intelligence

The France Prefabricated Construction Market size is projected to expand from USD 7.33 billion in 2025 and USD 7.72 billion in 2026 to USD 10.02 billion by 2031, registering a CAGR of 5.35% between 2026 to 2031.

Stringent RE2020 carbon limits, rising urban land prices, and persistent labor shortages prompt developers to favor factory-controlled assemblies that cut embodied emissions and shorten build programs. Public procurement for schools, clinics, and defense sites increasingly demands modular delivery to secure cost certainty and reduce neighborhood disruption. Private demand also gains momentum as data center and last-mile logistics operators place a premium on speed to revenue and on-site MEP integration. At the same time, timber-hybrid solutions attract investment because each cubic meter of cross-laminated timber (CLT) stores roughly 1 tonne of CO₂, a biogenic credit that helps projects comply with tightening caps without costly offsets.

Key Report Takeaways

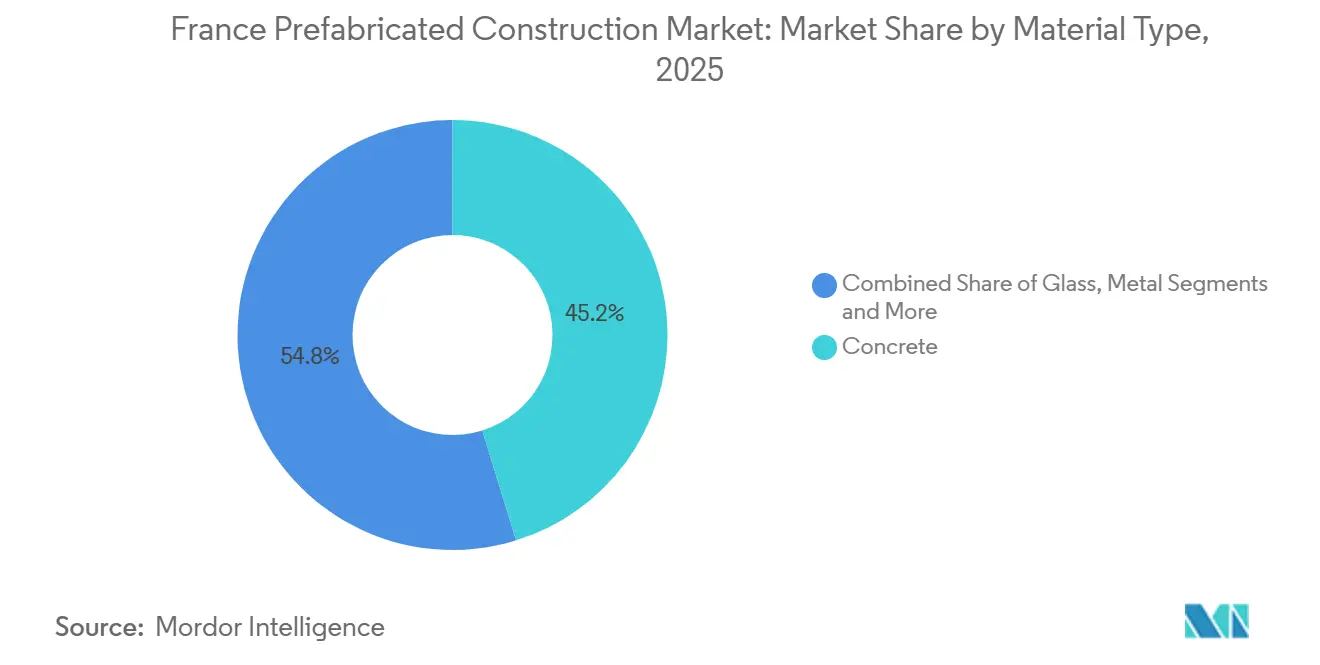

- By material type, concrete led with 45.2% of France prefabricated buildings market share in 2025, while timber is projected to post the fastest 6.12% CAGR through 2031.

- By application, the residential segment accounted for 59.4% of the France prefabricated buildings market size in 2025, whereas commercial projects are advancing at a 6.40% CAGR to 2031.

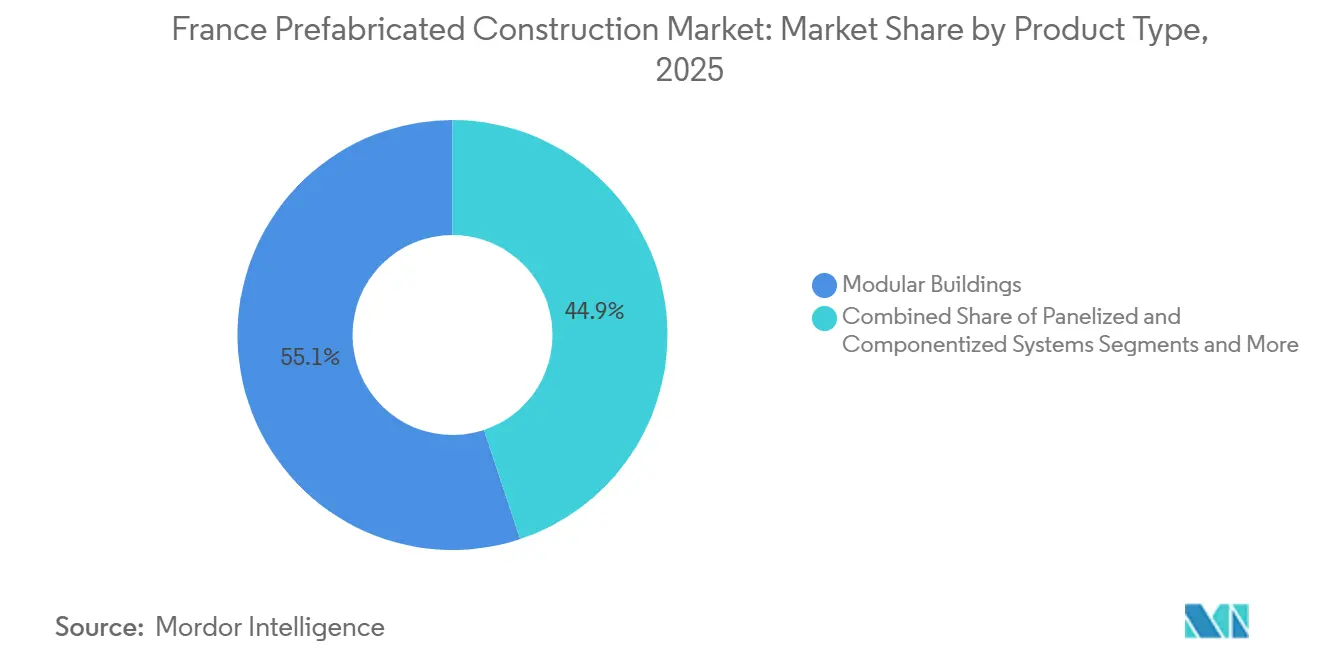

- By product type, modular buildings captured 55.1% of 2025 revenue, and panelized systems are forecast to expand at a 6.79% CAGR through 2031.

- By city, Paris contributed 39.7% of 2025 activity, yet Lyon records the strongest 7.08% city-level CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Prefabricated Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RE2020 energy and carbon standards | +1.8% | National with early adoption in Paris, Lyon, Grenoble | Medium term (2-4 years) |

| Public programs for schools, healthcare, defense | +1.2% | National, concentrated in Île-de-France, Auvergne-Rhône-Alpes, Provence-Alpes-Côte d’Azur | Short term (≤2 years) |

| Timber and hybrid prefab for decarbonization goals | +1.0% | National, leadership in Paris, Lyon, Bordeaux | Long term (≥4 years) |

| Urban infill and brownfield redevelopment | +0.9% | Paris, Lyon, Marseille, Lille | Medium term (2-4 years) |

| Industrial, logistics, and data center expansion | +0.8% | Île-de-France, Hauts-de-France, Auvergne-Rhône-Alpes | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

RE2020 Energy and Carbon Standards

France’s RE2020 code adds lifecycle-carbon caps that tighten in 2025, 2028, and 2031, forcing developers to quantify embodied emissions from structure to end-of-life. Factory-built envelopes minimize waste, assure airtightness, and allow detailed tracing of material provenance, helping projects document compliance without costly redesigns[1]CSTB, “Guidance technique RE2020 pour la construction bois,” CSTB.FR. Carbon accounting rules credit each cubic meter of structural timber with about 1 tonne of stored CO₂, a benefit that offsets emissions from foundations and MEP services[2]ADEME, “RE2020 : Seuils carbone et exigences,” ADEME.FR. These advantages translate into lower risk premiums for lenders and insurers, accelerating specification of modular and panelized solutions in new tenders. As the caps tighten, manufacturers that certify product footprints now are positioned to win repeat orders later.

Public-Sector Programs

French ministries responsible for education, health, and defense now embed offsite delivery in bid documents to shorten schedules and hold contractors to fixed price points[3]Bouygues Construction, “Projects and Innovation,” BOUYGUES-CONSTRUCTION.COM. A 12-classroom primary school in Bagneux opened in 2024 after only four months on site, demonstrating how volumetric units limit noise complaints in dense neighborhoods. Hospital extensions in Argenteuil and Rennes used modular patient rooms to maintain sterile zones while building new capacity, an approach that would have required phased closures with conventional methods. The military quietly deploys containerized barracks that relocate with troop rotations, proving the versatility of prefabrication for mission-critical assets. These examples build political confidence, ensuring that future public budgets continue to earmark funds for factory-made solutions.

Timber and Hybrid Prefab for Decarbonization

CLT and glued-laminated timber (GLT) lines expanded nationwide after landmark high-rise projects in Bordeaux and Grenoble validated fire and acoustic performance. Vertical integration deals, such as Eiffage’s 2024 purchase of B3 Ecodesign, secure local fiber supply and lock in price stability over multi-year frameworks. RE2020’s biogenic-carbon credit of up to 2 kg CO₂ per kilogram of dry wood enables mid-rise residential towers to achieve net-negative embodied carbon when coupled with low-carbon concrete podiums. National circular-economy guidelines now favor bolted rather than glued connections so panels can be recovered and redeployed, improving residual values at end-of-life. Timber’s dual climate and circular benefits are compelling private investors to include hybrid frames in sustainability-linked loan covenants.

Urban Infill and Brownfield Redevelopment

Tight urban plots face restrictions on working hours, crane pads, and truck routes, so contractors choose panelized facades and floor cassettes that lift into place in minutes and need fewer deliveries. The Bercy Village project in Paris kept weekend Metro service running by limiting heavy lifts to off-peak nighttime windows and finishing interiors with pre-fitted MEP risers. Lyon’s Part-Dieu masterplan inserts modular cores into towers beside active rail lines, minimizing track closures that would disrupt 140,000 passengers a day. Brownfield conversions enjoy a double benefit: lighter timber-hybrid frames reduce foundation loads on contaminated soils, and factory machining reduces worker exposure to onsite pollutants. These performance gains encourage planners to approve offsite methods as the default for infill projects.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex permitting and heritage protections | -0.7% | National, acute in historic Paris, Bordeaux, Strasbourg | Medium term (2-4 years) |

| Transport and cranage limits in dense cities | -0.5% | Paris, Lyon, Marseille, Lille | Short term (≤2 years) |

| Cultural preference for masonry and cost perceptions | -0.4% | National, strongest in rural and peri-urban areas | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Complex Permitting and Heritage Protections

Municipal planners apply varied aesthetic rules under the Code de l’urbanisme, and heritage officials may veto modular facades within 500 meters of protected monuments. A 2024 survey by the French Building Federation found modular permits in historic districts average 14 months, five months longer than conventional builds. Custom tweaks required to satisfy local appearance guidelines erase some factory efficiencies and inflate design fees. National agencies are drafting pre-approved typologies, yet uptake remains slow because mayors fear backlash if projects seem “industrial.” Until zoning harmonizes, developers must budget extra time and contingency funds for landmark sites.

Transport and Cranage Limits

French road law caps standard module width at 2.55 meters, height at 4 meters, and vehicle weight at 44 tonnes; oversize loads need escorts that increase cost and limit delivery windows. Urban cores tighten the squeeze with night-only deliveries and narrow turning radii, so cranes must be booked in brief windows at daily rates of EUR 3,000-5,000 (USD 3,300-5,500) plus standby charges. To cope, manufacturers redesign units to fit transport envelopes rather than optimal layouts, which raises per-square-foot costs. Panelized kits reduce haulage headaches but shift more labor back to site, diluting some productivity gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Concrete Holds Scale as Timber Accelerates

Concrete retained a 45.2% France prefabricated construction market share in 2025 thanks to its dominance in multi-story social housing and industrial sheds. Pre-cast stair cores and bathroom pods made with low-carbon cement allow developers to meet fire and acoustic codes while leveraging established supply chains. However, RE2020 charges higher embodied-carbon penalties on ordinary Portland cement, nudging contractors to adopt blends with granulated slag or calcined clay. Timber is the fastest climber, expanding at a 6.12% CAGR toward 2031 as CLT prices fall in line with rising domestic capacity, exemplified by Hexaom’s investment in POBI Industrie’s Vendée plant. Hybrid frames that marry timber floors to concrete podiums now anchor many 8-10 story towers, demonstrating how the France prefabricated construction market can balance structural resilience with decarbonization.

Growth momentum favors materials that meet both carbon and schedule targets. Timber cores cut building weight by up to 30%, enabling shallower foundations on weak soils and lowering spoil disposal costs in brownfield sites. Regional sawmills around Auvergne now machine CLT panels to 3.2-meter widths, maximizing truck payloads within French road limits. Meanwhile, steel holds a steady niche in wide-span logistics halls yet faces slower growth because virgin steel attracts hefty carbon coefficients. Composite sandwich panels and recycled-aggregate blocks are emerging as wildcard options for façades and interior partitions, but they still command a fraction of current demand. Overall, material substitution trends enrich supplier diversity and reinforce competitive dynamics within the France prefabricated construction market.

By Application: Residential Dominates while Commercial Gains Pace

Residential schemes contributed 59.4% of the France prefabricated construction market in 2025 as social-housing authorities raced to relieve a chronic shortage of affordable units. Modular typologies reduce tenant rehousing costs by shortening on-site programs, and RE2020 incentives make timber apartments attractive for public landlords pursuing BBCA certification. Yet buyer sentiment still leans toward masonry, so private developers proceed cautiously, focusing on peri-urban subdivisions where land savings offset the prefabrication premium. The Athletes’ Village, converted into 2,800 apartments after the 2024 Olympics, showcases how factory production scales in high-profile urban contexts and helps normalize offsite delivery to the broader market.

Commercial construction grows the fastest at a 6.40% CAGR through 2031, fueled by data-center and logistics investments that require precise MEP integration and flawless uptime. Prefabricated cooling modules, electrical rooms, and rooftop plant reduce commissioning risk and allow phased capacity additions in response to customer demand. Warehouses benefit from panelized steel frames that erect quickly during summer harvests when rural labor is scarce. Offices recover more slowly because hybrid work dampens demand; nonetheless, trophy towers in Paris and Lyon adopt curtain-wall cassettes and prefitted service risers to achieve HQE Excellent scores within compressed tenant fit-out windows. Healthcare, education, and defense remain smaller slices yet deliver marquee case studies that influence policy and procurement standards across the France prefabricated construction market.

By Product Type: Modular Leads, Panelized Surges

Modular buildings commanded 55.1% of 2025 revenue as volumetric classrooms, site offices, and worker dormitories formed an established rental fleet managed by Algeco, Portakabin, and Cougnaud. Permanent volumetric housing also gains share, though transport size limits and public-image concerns temper progress. The France prefabricated construction market size for panelized and componentized systems is smaller today, but recorded the strongest 6.79% CAGR outlook because the flat-pack format navigates narrow streets without escorts. Builders assemble wall panels and floor cassettes using conventional cranes, allowing architectural freedom and easier façade customization in heritage districts.

Manufacturers respond with advanced digital fabrication. VINCI’s robotics cuts and welds panels with millimeter precision in four weeks, giving contractors just-in-time delivery within dense city sites. Sub-segments such as precast lift shafts, staircases, and bathroom pods remain stable because they integrate seamlessly into both modular and traditional builds. Looking ahead, hybrid procurement that combines volumetric wet cores with panelized dry areas will likely dominate mixed-use towers, blending factory quality with on-site flexibility. This mix supports sustained value creation across the France prefabricated construction market.

Geography Analysis

Paris retained a commanding 39.7% share of the France prefabricated construction market in 2025 as contractors leveraged factory precision to meet non-negotiable Olympic handover deadlines without breaching tight noise ordinances. RE2020 enforcement also favors off-site in the capital because multi-award processes penalize high-carbon materials. Data-center operators situate new halls in Seine-Saint-Denis and Val-de-Marne, where land is cheaper, drawing large orders for prefitted MEP skids that shorten power-up cycles. Despite these strengths, narrow streets and heritage reviews still inflate craneage and design costs, nudging some developers toward panelized kits that can slip through standard transport envelopes.

Lyon is the fastest-growing metropolitan area at a projected 7.08% CAGR through 2031, thanks to the Part-Dieu redevelopment and a vibrant biopharma cluster that demands cleanroom modules. Municipal planners embrace prefabrication as a tool to limit rail-station disruption and to accelerate affordable-housing completions in Villeurbanne and Vénissieux. Logistics parks at Saint-Quentin-Fallavier adopt panelized steel frames to meet e-commerce growth, reinforcing a positive loop of industrial demand and supplier investment.

Marseille and the wider regions together account for the balance of market activity. Euroméditerranée’s waterfront masterplan integrates modular apartments that respect strict daytime noise caps while reducing truck trips through the port district. Elsewhere, prefabricated extensions to provincial hospitals in Rennes and Poitiers illustrate how offsite methods tackle service backlogs without suspending operations. Cultural skepticism and fragmented crane supply keep rural uptake modest, yet national targets to retrofit public buildings for energy efficiency will likely drive gradual diffusion of modular façades into smaller towns, ensuring steady though uneven expansion of the France prefabricated construction market.

Competitive Landscape

Competition is moderately fragmented: even the five largest suppliers capture only a modest share of industry revenue, leaving ample white space for regional specialists and niche offerings - particularly in healthcare and data-center product lines. Large contractors pivot faster toward vertical integration after RE2020 elevated embodied-carbon metrics in tender scoring. Eiffage grouped its concrete, timber, and panel operations into a single Off-Site division targeting USD 220 million equivalent revenue by 2027, while Bouygues opened the Scale One center to test digital twins that cut on-site rework by 15%.

Mergers and acquisitions accelerate as mid-tier housebuilders lock in factory slots. Hexaom bought timber specialist POBI Industrie in July 2025, combining a 12,000-square-meter line with its Trecobat brand to secure supply and protect margins against rising carbon tariffs. Investors also see value in rental fleets; Antin Infrastructure Partners acquired Portakabin for GBP 1 billion (USD 1.3 billion), funding a new French production line that targets healthcare and education orders. These moves increase capacity and raise the technological bar for smaller rivals.

Technology defines competitive gaps. VINCI robotizes panel cutting and welding, reducing lead times to four weeks and enabling just-in-time deliveries in constrained city sites. Cougnaud’s Citeden line incorporates digital patient-monitoring infrastructure, creating a turnkey solution that commands a premium in hospital tenders. Smaller fabricators remain viable by offering highly customized façades or localized after-sales service, but they risk margin compression as standards converge. Continued regulatory tightening and client demand for assured carbon footprints point to further consolidation within the France prefabricated construction market.

France Prefabricated Construction Industry Leaders

Bouygues Construction

VINCI Construction

Eiffage Construction

Cougnaud Construction

Bodard Construction Modulaire

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Digital Realty announced a USD 165 million expansion of its Paris data-center campus using prefabricated cooling blocks that shaved six months off commissioning.

- July 2025: Hexaom closed the acquisition of POBI Industrie, integrating its timber-frame line with the Trecobat brand to accelerate low-carbon housing delivery.

- January 2025: Hexaom acquired HDV, adding EUR 45 million (USD 49.5 million) in annual revenue and extending its prefabrication reach into eastern France.

- 2024: Eiffage consolidated prefabricated concrete and timber operations into a single Off-Site division targeting USD 220 million turnover by 2027.

France Prefabricated Construction Market Report Scope

Prefabricated construction is a one-of-a-kind method in which the different parts of a building structure are made in a factory and then brought to the building site to be put together and finished.This form of the building has various advantages.

The prefabricated buildings industry in France is segmented by material type (concrete, glass, metal, timber, and other material types) and application (residential, commercial, and other applications (infrastructure and industrial).

The report offers the market sizes and forecasts for the France prefabricated buildings industry in value (USD billion) for all the above segments. The impact of COVID-19 has also been incorporated and considered during the study.

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By City

| Paris |

| Lyon |

| Marseille |

| Rest of France |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By City | Paris |

| Lyon | |

| Marseille | |

| Rest of France |

Key Questions Answered in the Report

How large is the France prefabricated construction market in 2026?

The France prefabricated buildings market size stands at USD 7.72 billion in 2026 and is forecast to reach USD 10.02 billion by 2031.

What CAGR is expected for prefabricated construction in France to 2031?

Market revenue is projected to grow at a 5.35% CAGR over the 2026-2031 period.

Which material is gaining the most momentum in French offsite construction?

Timber-hybrid assemblies post the fastest 6.12% CAGR because RE2020 awards carbon credits for biogenic storage.

Why is Lyon growing faster than other French cities for prefab adoption?

The Part-Dieu redevelopment and a strong biotechnology and logistics base push Lyon to a 7.08% growth pace through 2031.

Who are the leading companies in this market today?

Bouygues Construction, VINCI Construction, Eiffage Construction, Cougnaud Construction, and Bodard Construction Modulaire are among the leading companies operating in this market.

What are the main barriers to wider prefab uptake in France?

Complex permitting in heritage districts, transport size limits in dense cities, and lingering consumer preference for traditional masonry slow broader adoption despite clear carbon and speed advantages.

Page last updated on: