Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

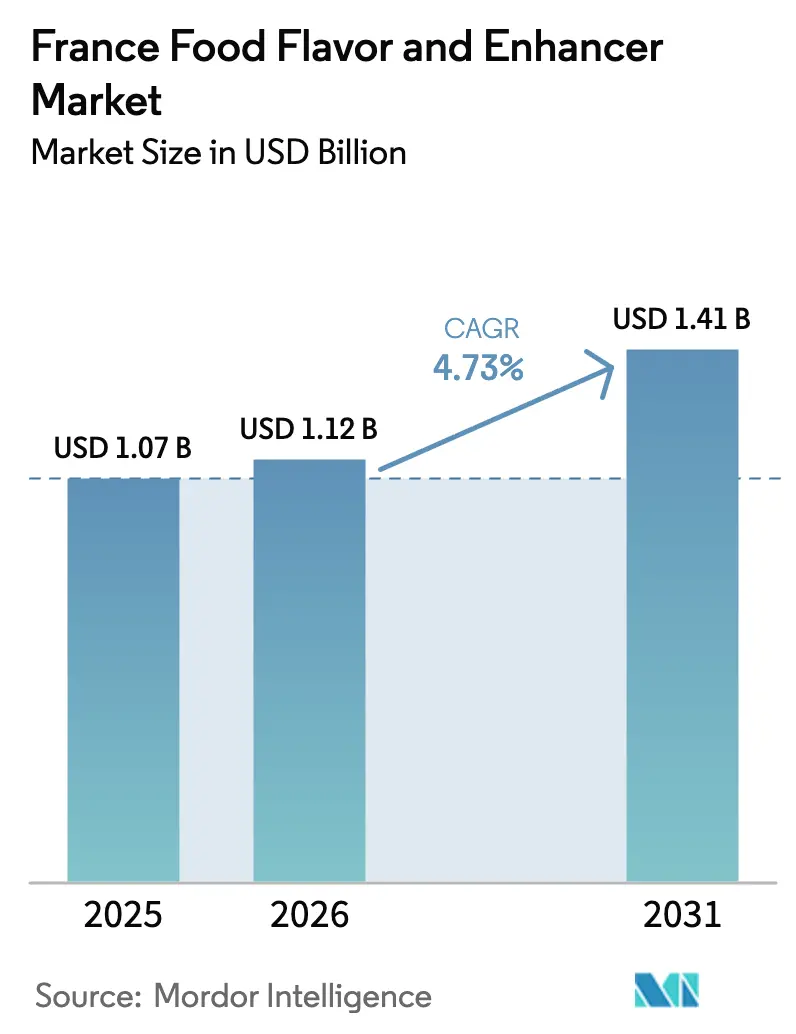

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

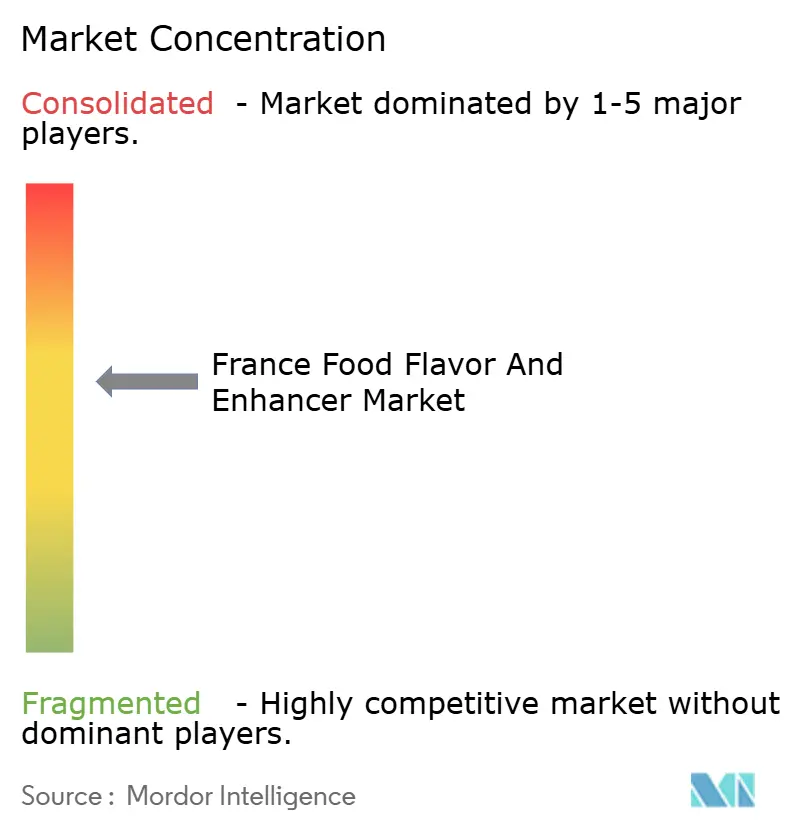

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Food Flavors And Enhancers Market Analysis by Mordor Intelligence

The France Food Flavors And Enhancers Market was valued at USD 1.07 billion in 2025 and estimated to grow from USD 1.12 billion in 2026 to reach USD 1.41 billion by 2031, registering a compound annual growth rate (CAGR) of 4.73% during the forecast period. The France Food Flavors And Enhancers Market is growing, driven by a blend of traditional culinary culture and evolving consumption patterns. Increasing demand for premium and authentic taste profiles in packaged foods, ready meals, bakery products, dairy items, and plant-based alternatives is prompting manufacturers to adopt more advanced flavor systems. Simultaneously, clean-label trends are fostering the use of natural extracts, fermentation-derived enhancers, herbs, and yeast-based solutions as alternatives to artificial additives. The widespread consumption of gourmet and convenience foods, supported by busy urban lifestyles and a well-developed retail and food-service sector, is further boosting the need for flavor optimization and shelf-life enhancement. Moreover, reformulation efforts aimed at reducing salt, sugar, and fat content while maintaining taste are driving the use of umami enhancers and masking agents. Ongoing product innovation by European food companies and increasing exports of processed foods are also sustaining the demand for advanced flavor technologies in France.

Key Report Takeaways

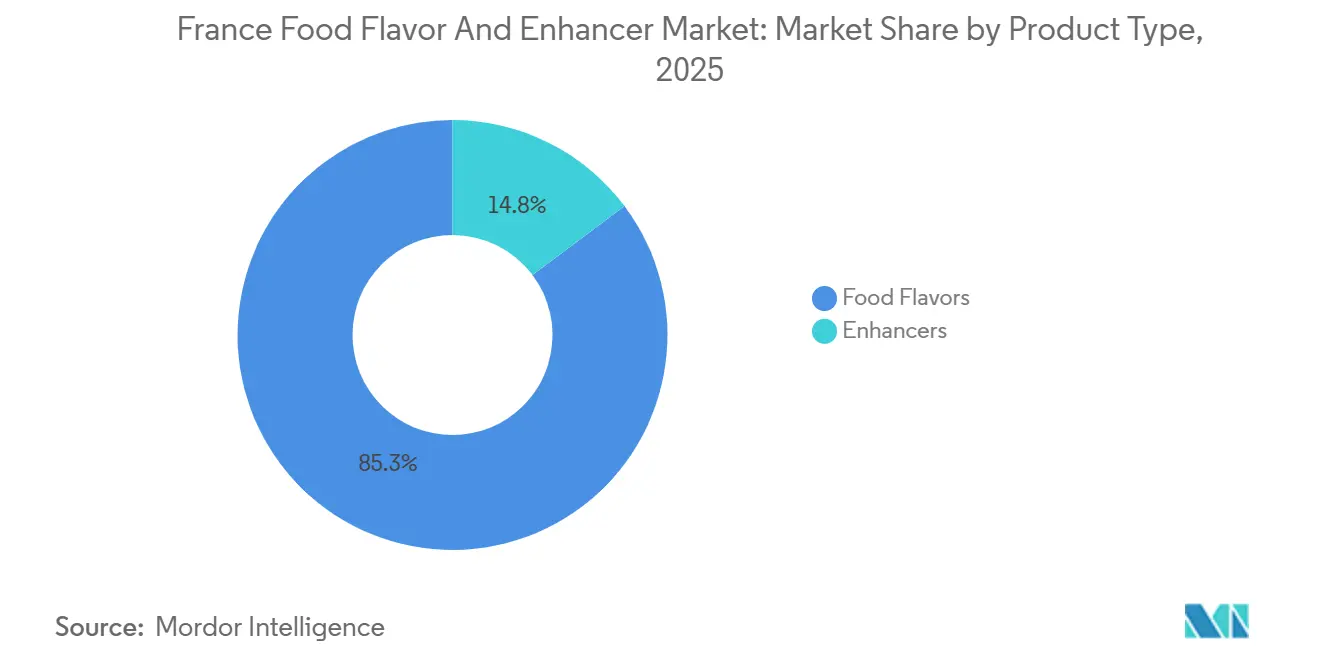

- Food Flavors led with 85.25% revenue share of the France Food Flavors And Enhancers Market in 2025 and the segment is forecast to expand at a 5.81% CAGR through 2031.

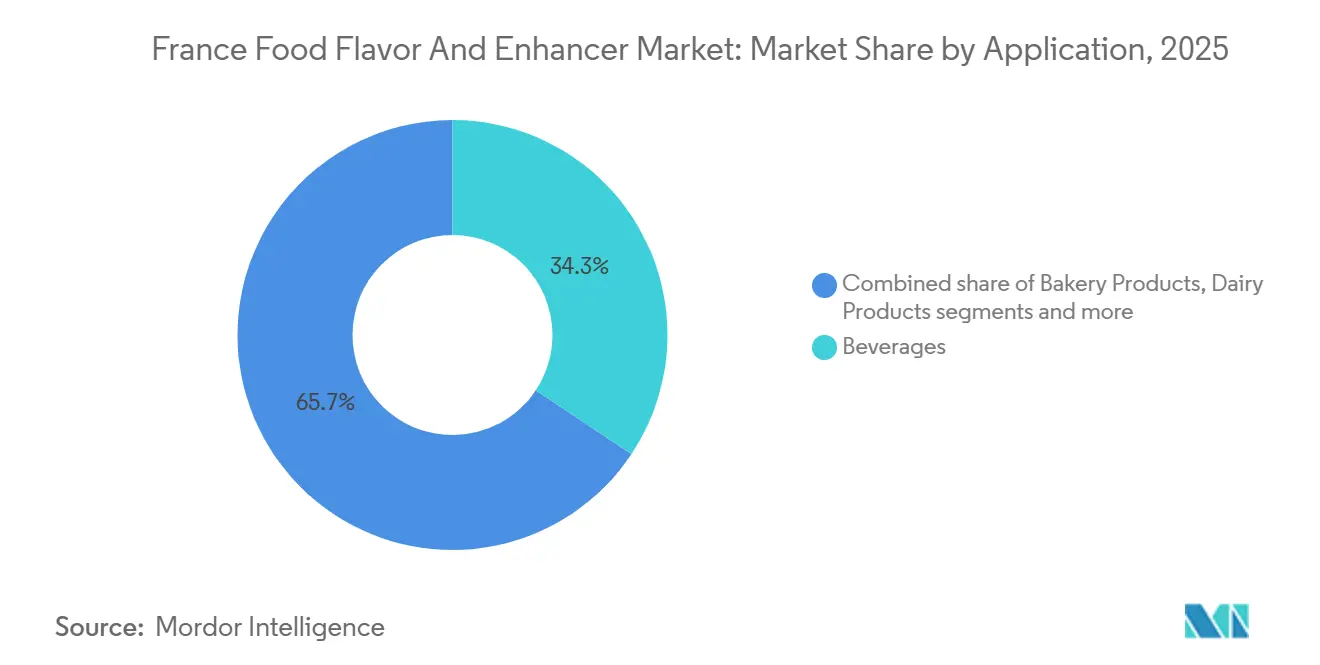

- By application, Beverages commanded 34.33% of the France Food Flavors And Enhancers Market size in 2025 and is projected to grow at a 6.01% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Food Flavors And Enhancers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing clean-label preference is boosting demand for natural and nature-identical flavors | +1.2% | France, with spillover to urban centers | Medium term (2-4 years) |

| Health awareness is encouraging low-sugar, low-sodium, and additive-free flavor solutions | +0.9% | National, with early gains in Paris, Lyon, Marseille | Short term (≤ 2 years) |

| Expansion of plant-based diets is driving development of plant-derived taste enhancers | +0.8% | France, accelerating in urban centers | Medium term (2-4 years) |

| Demand for ethnic and fusion flavor profiles | +0.7% | France, particularly Paris metropolitan area | Short term (≤ 2 years) |

| Advances in extraction, encapsulation, and biotechnology enable stable and functional flavor systems | +1.0% | France as early adopter | Long term (≥ 4 years) |

| Sustainability expectations are pushing eco-friendly sourcing and production methods | +0.6% | France and European Union, driven by corporate ESG mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing clean-label preference is boosting demand for natural and nature-identical flavors

In France, consumer preferences for food ingredients are increasingly influenced by concerns over transparency and safety, resulting in a notable shift toward clean-label formulations. Consumers are now more attentive to ingredient lists, actively avoiding artificial additives. This trend is prompting food manufacturers to replace synthetic flavorings with natural extracts, fermentation-derived enhancers, essential oils, and nature-identical compounds that provide familiar tastes while being perceived as more acceptable on product labels. This shift is further supported by regulatory developments across the European Union. Commission Regulation (EU) 2024/234, effective from January 15, 2024, amended Annex I to Regulation (EC) No 1334/2008 by removing certain flavoring substances from the Union list[1]Source: European Union, "Regulation - EU - 2024/234 - EN - EUR-Lex," eur-lex.europa.eu. Consequently, French food manufacturers, spanning categories such as dairy, bakery, ready meals, and snacks, are reformulating their products to preserve taste while aligning with both regulatory requirements and consumer expectations. This has significantly accelerated the demand for natural and nature-identical flavor and enhancer solutions in the market.

Health awareness is encouraging low-sugar, low-sodium, and additive-free flavor solutions

Increasing public concern in France regarding cardiovascular health, obesity, and overall nutrition is prompting food manufacturers to reformulate products with reduced sugar, salt, and artificial additives while maintaining taste. This trend has led to a growing reliance on advanced flavor and enhancer technologies. Consumers are demanding healthier packaged foods without compromising on flavor, driving the adoption of umami enhancers, bitterness blockers, sweetness modulators, and fermentation-based flavor systems to offset reduced sodium or sugar levels. Government initiatives are further supporting this transition. In 2019, France set a national goal to reduce salt consumption by 30%, and in 2022, authorities and bread producers signed a voluntary agreement to lower salt content by 2025. Bread, particularly the baguette, is a dietary staple in France and traditionally accounted for approximately 25% of the recommended daily salt intake. Reformulation has become essential, and by 2023, most bread produced in France already meet the new sodium standards[2]Source: American Heart Association, Inc., "Reducing sodium in everyday foods may yield heart-health benefits across populations," heart.org. These regulatory measures and public health priorities are driving demand for flavor enhancers that preserve taste intensity in healthier formulations. As a result, reduced-salt, reduced-sugar, and additive-free flavor solutions are emerging as a significant growth driver in the French food flavor and enhancer market.

Expansion of plant-based diets is driving development of plant-derived taste enhancers

The increasing adoption of flexitarian and plant-based diets in France is driving significant demand for flavor technologies capable of replicating the depth and mouthfeel traditionally associated with animal-derived ingredients. As consumers transition to meat alternatives, dairy substitutes, and vegetable-based ready meals, manufacturers face challenges such as bland flavors, beany off-notes, and a lack of savory richness. This has led to the growing use of plant-derived taste enhancers, including yeast extracts, mushroom concentrates, fermented vegetable bases, seaweed ingredients, and natural umami compounds, which enhance body and complexity without relying on artificial additives. This trend aligns with evolving dietary habits. According to a ProVeg survey published in April 2024, 58% of French meat consumers are actively reducing their annual meat consumption[3]Source: ProVeg, "58% of French meat consumers are reducing their annual meat consumption," proveg.org. In response, food producers are investing in advanced plant-based flavor systems to replicate familiar taste profiles in vegetarian and vegan products. As a result, plant-derived enhancers are becoming a key growth driver in the French food flavor and enhancer market.

Demand for ethnic and fusion flavor profiles

Consumer curiosity and multicultural culinary influences are playing a significant role in shaping the France Food Flavors And Enhancers Market. Shoppers are increasingly seeking diverse taste experiences that go beyond traditional French cuisine. Exposure to global food trends through travel, social media, street-food culture, and international restaurant chains has driven demand for Asian, Middle Eastern, Latin American, and African flavor profiles in packaged meals, snacks, sauces, and ready-to-cook products. To address these preferences, manufacturers are incorporating complex spice blends, fermented ingredients, chili pastes, smoked flavors, and layered umami enhancers to replicate authentic regional tastes while tailoring them to local preferences. Fusion concepts, such as combining French culinary techniques with global seasonings, require advanced flavor formulation to ensure balance in intensity, aroma, and aftertaste stability during processing and storage. Consequently, food companies increasingly depend on specialized flavor houses to develop customized and heat-stable flavor systems. This growing demand for ethnic and hybrid taste profiles is emerging as a key growth driver in the France Food Flavors And Enhancers Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict EU Regulatory & EFSA Approval Complexity | -0.8% | France and the European Union-wide | Medium term (2-4 years) |

| High Reformulation Cost | -0.6% | France, particularly SME manufacturers | Short term (≤ 2 years) |

| Climate-Driven Raw Material Volatility | -0.5% | France, exposed via import dependence | Long term (≥ 4 years) |

| High R&D Expenses Make Clean-Label Innovation Difficult | -0.4% | France, affecting mid-tier flavor houses | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict EU Regulatory & EFSA Approval Complexity

The France Food Flavors And Enhancers Market is significantly constrained by the stringent regulatory framework governing food ingredients within the European Union. Any introduction of a new flavoring substance or modification of an existing one requires extensive safety evaluations, toxicological assessments, and comprehensive documentation. This approval process is often both time-consuming and costly. Additionally, the periodic re-assessment of previously approved compounds can necessitate sudden reformulations, compelling manufacturers to invest in new ingredient sourcing, stability testing, and label updates. Smaller flavor houses and food producers are particularly impacted, as compliance demands specialized expertise, detailed traceability, and repeated validation across various product categories. Furthermore, strict labeling requirements and limitations on certain additives restrict formulation flexibility, delaying product launches and slowing innovation compared to markets with less stringent regulations. Consequently, the complexity of EU and EFSA approval procedures increases operational costs, extends development timelines, and poses a significant restraint on the growth of the France Food Flavors And Enhancers Market.

High Reformulation cost

Frequent recipe adjustments to align with evolving consumer preferences and regulatory requirements substantially increase operational costs for companies in the France Food Flavors And Enhancers Market. Reducing or replacing artificial additives, excess salt, or sugar levels necessitates more than the simple removal of ingredients; it requires a complete redesign of the sensory profile to preserve taste, texture, aroma, and shelf stability. This process involves multiple pilot trials, sensory evaluations, stability testing, and validation under various processing conditions, including baking, freezing, and pasteurization. Additionally, alternative natural or fermentation-derived flavor solutions often come at a higher cost and may require new supplier agreements or modifications to production processes. Further financial strain arises from packaging and labeling updates, inventory write-offs of outdated stock, and potential manufacturing line downtime. These factors collectively increase production costs and reduce profit margins, posing a significant challenge to growth in the France Food Flavors And Enhancers Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Natural Systems Gain Preference Amid Regulatory Challenges for Synthetics

Food flavors accounted for 85.25% of the market value in 2025 and are projected to grow CAGR of 5.81% through 2031, surpassing enhancers as manufacturers focus on sensory complexity rather than basic taste modulation. The demand for food flavors in France is driven by consumers seeking premium taste experiences in packaged foods, bakery products, dairy items, and ready meals, while prioritizing natural ingredient labels. The rising popularity of international cuisines, the growth of convenience foods, and the expansion of plant-based alternatives compel manufacturers to develop authentic and stable flavor profiles that can withstand industrial processing. Simultaneously, reformulation efforts aimed at reducing artificial additives are promoting the use of botanical extracts, fermented notes, and nature-identical flavorings, encouraging food companies to invest in ongoing flavor innovation.

The food enhancers market in France is primarily driven by health-focused reformulations, as producers reduce salt, sugar, and fat levels while maintaining taste intensity. Umami compounds, yeast extracts, and masking agents are increasingly utilized to restore mouthfeel and balance bitterness in healthier recipes and plant-based foods. Additionally, strong demand from food-service chains and ready-to-eat meals emphasizes the need for consistent taste across large production volumes. This makes enhancers crucial for flavor standardization and shelf-life stability, thereby contributing to steady market growth.

By Application: Beverages Drive Growth with Functional and Low-Alcohol Trends

Beverages accounted for 34.33% of application revenue in 2025 and are projected to grow at a CAGR of 6.01% through 2031. The use of food flavors in French beverages is increasing as consumers gravitate toward flavored waters, low-sugar soft drinks, functional beverages, plant-based drinks, and premium coffee products that provide distinctive tastes without excessive sweetness. Manufacturers are utilizing advanced flavor systems to incorporate fruit, botanical, and indulgent notes while maintaining clean labels and lower calorie content. Seasonal and limited-edition product launches, along with the growing demand for natural aromas in sparkling drinks and dairy alternatives, are driving innovation. This includes the development of stable, heat- and acid-resistant flavor formulations designed for large-scale processing and extended shelf life.

The demand for food enhancers in these applications is driven by reformulation efforts and convenience-focused eating habits. Ready-made sauces, soups, and condiments rely on umami boosters and masking agents to maintain flavor depth when reducing salt, fat, or artificial additives. Similarly, bakery products utilize enhancers to strengthen aroma and offset sugar reduction in healthier formulations. Additionally, prepared meals and snack products depend on flavor enhancers to ensure batch-to-batch consistency and preserve sensory quality during storage and reheating. The growing popularity of plant-based cooking and home meal preparation further increases the need for ingredients that deliver savory richness and balance in a variety of everyday foods.

Competitive Landscape

Top Companies in France Food Flavors And Enhancers Market

The France Food Flavors And Enhancers Market is moderately concentrated, with multinational companies such as Givaudan, dsm-firmenich, Kerry, IFF, and Symrise leading in core formulation technologies, extraction capabilities, and long-term supply relationships with major food manufacturers. In addition to these global players, regional specialists like Robertet and Mane hold significant positions by emphasizing locally sourced botanicals, close collaboration with chefs, and tailored development for artisanal producers in areas where larger firms often lack flexibility.

Competition in the market is influenced by strategies such as vertical integration into raw material sourcing, diversification into adjacent food and nutrition segments, and licensing proprietary technologies to smaller manufacturers. The competitive dynamics are evolving with advancements in biotechnology and digital formulation tools, enabling new entrants to produce natural-style flavor compounds through fermentation and predictive sensory modeling.

Startups are disrupting traditional supply chains by introducing alternative ingredient production methods, prompting established companies to respond through acquisitions and partnerships rather than relying solely on internal research and development. Additionally, stringent regulatory requirements and the complexity of reformulation processes favor larger players with robust compliance expertise and technical infrastructure. This environment encourages smaller firms to collaborate, specialize, or focus on niche applications.

France Food Flavors And Enhancers Industry Leaders

-

Symrise AG

-

International Flavors & Fragrances Inc.

-

Kerry Group plc

-

dsm-Firmenich

-

Givaudan SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Syensqo announced the restart of its synthetic vanillin manufacturing facility in Saint-Fons, France, after a temporary shutdown in May 2024. The plant is expected to become operational, reflecting improved market dynamics and the company's commitment to better serving European food, flavor, and fragrance customers.

- March 2025: French botanical extract producer Plantex launched Smok’EXTRACT, a product line developed as a natural alternative to traditional smoke flavorings. This solution combines thermally treated wood extracts with additional ingredients to replicate the aroma and sensory complexity of conventional smoking, including the characteristic base notes and trigeminal sensations found in smoked foods.

France Food Flavors And Enhancers Market Report Scope

France Food Flavors And Enhancers Market is segmented by product type, which includes flavors and enhancers. By flavor, the market is further segmented into natural flavors, synthetic flavors, and natural identical flavors.

By application, the study's scope includes bakery products, sauces, soups, condiments, dairy products, beverages, savory snacks, meat and meat products, and other applications.

The beverages segment has been further bifurcated into alcoholic and non-alcoholic beverages. Non-alcoholic beverages are sub-segmented into carbonated beverages, fruit and vegetable juice, sports and energy drinks, and other non-alcoholic beverages.

By Product Type

| Food Flavors | Natural Flavors |

| Synthetic Flavors | |

| Nature-Identical Flavors | |

| Enhancers |

By Application

| Bakery Products | ||

| Sauces, Soups, and Condiments | ||

| Dairy Products | ||

| Savory Snacks | ||

| Meat and Meat Products | ||

| Beverages | Alcoholic | |

| Non-Alcoholic | Carbonated Beverages | |

| Fruit and Vegetable Juice | ||

| Sports and Energy Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Others | ||

| By Product Type | Food Flavors | Natural Flavors | |

| Synthetic Flavors | |||

| Nature-Identical Flavors | |||

| Enhancers | |||

| By Application | Bakery Products | ||

| Sauces, Soups, and Condiments | |||

| Dairy Products | |||

| Savory Snacks | |||

| Meat and Meat Products | |||

| Beverages | Alcoholic | ||

| Non-Alcoholic | Carbonated Beverages | ||

| Fruit and Vegetable Juice | |||

| Sports and Energy Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Others | |||

Key Questions Answered in the Report

What is the current value of the France Food Flavors And Enhancers Market?

The market stands at USD 1.12 billion in 2026 and is on track to reach USD 1.41 billion by 2031.

Which application is growing the fastest?

Beverages lead growth with a 6.01% CAGR expected over 2026-2031 as brands launch functional and low-alcohol drinks that need advanced flavor systems.

Why are natural flavors gaining share?

EFSA has tightened approval for synthetics and consumers reject E-numbers, so manufacturers shift to botanical or fermentation-derived options that qualify as natural.

What technologies shape future competition?

Precision fermentation, supercritical CO₂ extraction, and advanced encapsulation platforms will define product performance and margin gains through 2031.

Page last updated on: