Market Overview

| Study Period | 2021 - 2031 |

|---|---|

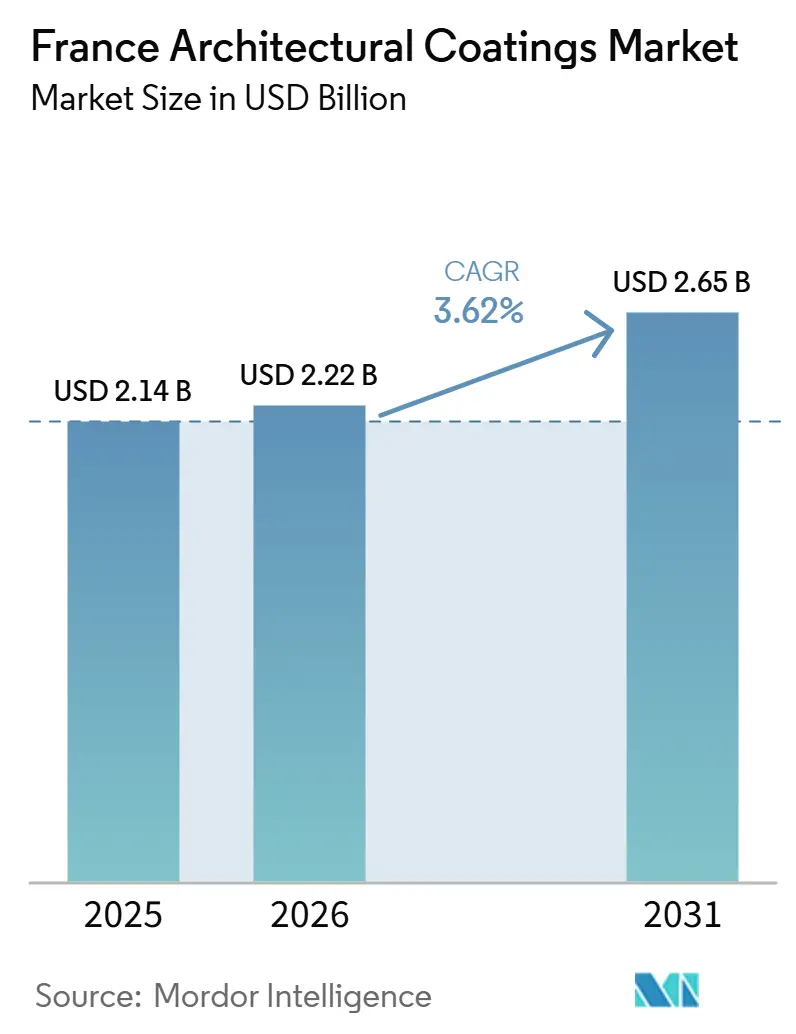

| Base Year Market Size (2025) | USD 2.14 Billion |

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 2.65 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Fastest Growing Market | Residential |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Architectural Coatings Market Analysis by Mordor Intelligence

The France architectural coatings market size is expected to increase from USD 2.14 billion in 2025 to USD 2.22 billion in 2026 and reach USD 2.65 billion by 2031, growing at a CAGR of 3.62% over 2026-2031. Demand is shaped by stricter indoor-air-quality rules, a vigorous shift to water-borne technologies, and persistent labor shortages that push homeowners toward do-it-yourself solutions. Producers are retreating from low-margin commodity segments and redirecting capital toward premium, certified lines that satisfy the A+ emissions label and the revised European Union (EU) Ecolabel. Imports fill much of the low-price void left by this strategic realignment, leaving domestic manufacturers to focus on differentiated performance, digital color tools, and sustainability credentials. Raw-material inflation, most visibly the EUR 300-per-tonne hike in titanium dioxide, compresses gross margins and forces value-engineering of formulas and packaging.

Key Report Takeaways

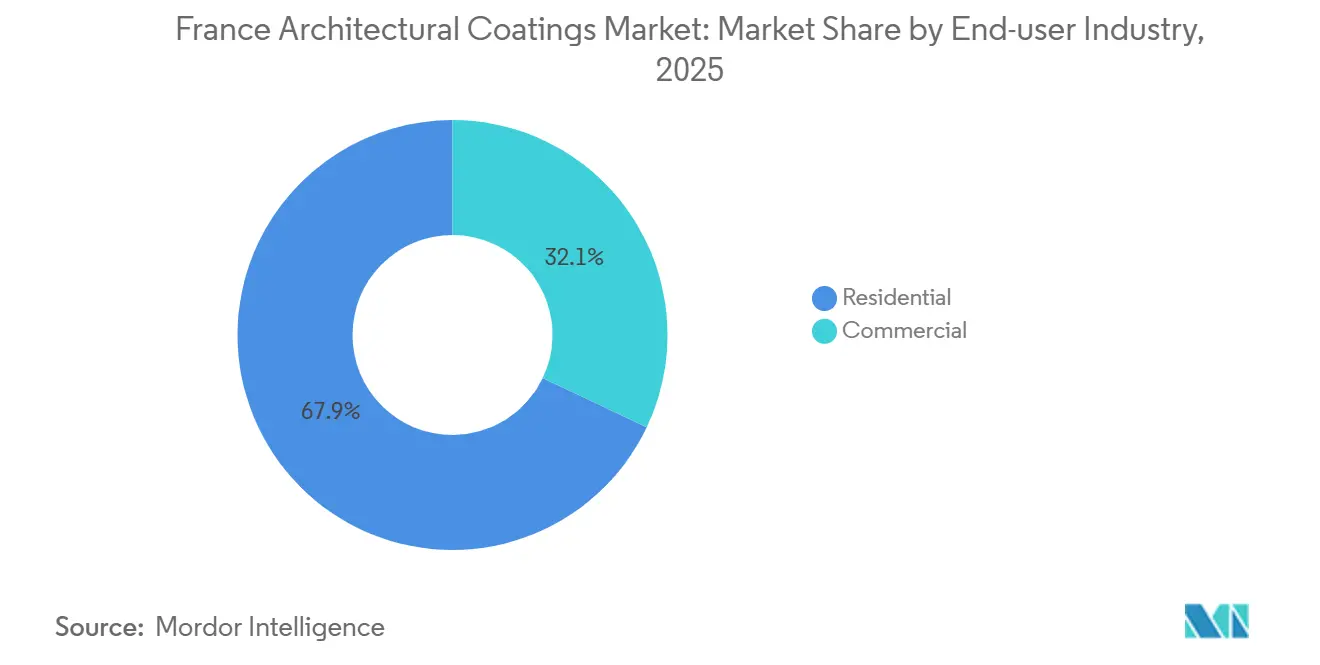

- In 2025, the residential sector accounted for 67.94% share of the France Architectural Coatings market. Forecasts predict this segment will grow at a 4.05% CAGR from 2026 to 2031.

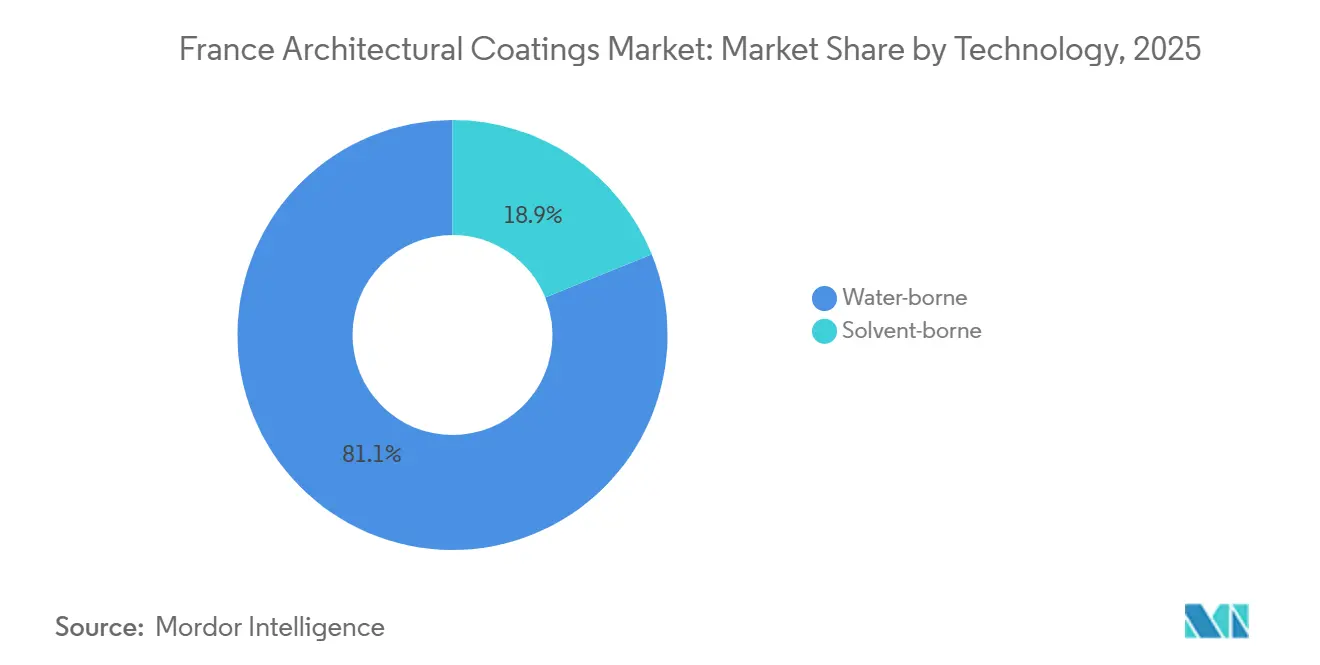

- Water-borne technology led the France Architectural Coatings market with 81.12% share in 2025. Projections indicate that water-borne will achieve the fastest growth, with a 4.21% CAGR from 2026 to 2031.

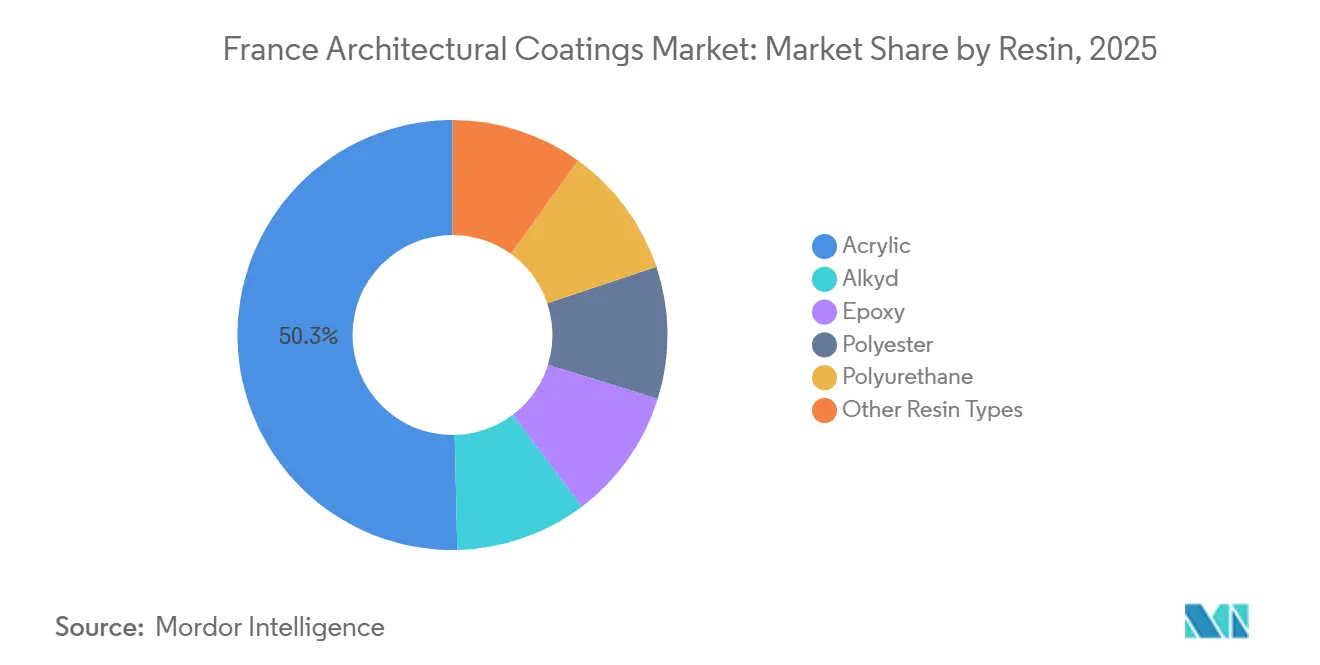

- Acrylic resins accounted for 50.35% of the 2025 revenue. Looking ahead, acrylic is poised for a 4.18% CAGR growth from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory sustainability-driven renovations | +0.8% | National, concentrated in Île-de-France, Rhône-Alpes, Atlantique-Bretagne | Medium term (2-4 years) |

| Surge in DIY interior-refresh purchases post-COVID | +0.6% | National, with stronger uptake in Occitanie (42% renovation intent) | Short term (≤ 2 years) |

| Shift to water-based binders to meet VOC caps | +0.9% | National, aligned with EU Directive 2004/42/EC and French A+ labeling | Long term (≥ 4 years) |

| Pro-contractor loyalty-reward platforms by retail chains | +0.4% | National, led by Castorama, Leroy Merlin, Brico Dépôt networks | Medium term (2-4 years) |

| AI-enabled color-matching kiosks in French DIY stores | +0.3% | National, urban centers with high digital penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory Sustainability-Driven Renovations

France has enacted Decree 2011-321, mandating that all interior paints display an emissions label. This label's A+ class sets formaldehyde limits at 10 µg/m³ and Total Volatile Organic Compounds (TVOC) at 1,000 µg/m³, standards that are more stringent than the European Union Lowest Concentration of Interest (EU-LCI) guidelines[1]Legifrance, “Décret 2011-321,” legifrance.gouv.fr. The zero-interest PAR+ advance, offering up to EUR 50,000 for energy renovations, faces challenges as 2026 subsidy reductions to MaPrimeRénov’ and diminished Certificats d’Économies d’Énergie (CEE) (Energy Savings Certificates) credits shrink the pool of eligible projects. Demand is increasingly directed towards low-emission, certified coatings because of the RGE contractor certification. However, with funding becoming tighter, manufacturers are pivoting towards self-funded premium refurbishments and commercial retrofits driven by Environmental, Social, and Governance (ESG) considerations. Builders who adjust their formulations to meet the stricter 2025 EU Ecolabel criteria stand to gain a competitive edge. These regulations are driving the growth of high-performance water-borne systems in France's architectural coatings market.

Shift to Water-Based Binders to Meet VOC Caps

Since 2010, EU Directive 2004/42/EC has capped VOC levels at 30 g/L for interior matt paints, effectively sidelining solvent-borne products from homes. The 2025 revision of the EU Ecolabel tightens the TVOC limit to 300 µg/m³ after 28 days and introduces ceilings on TiO₂ process emissions. This compels a further shift towards advanced water-borne chemistries[2]Joint Research Centre, “EU Ecolabel Revised Criteria 2025,” joint-research-centre.ec.europa.eu. AkzoNobel’s RUBBOL WF 3350 demonstrates that bio-based acrylics, containing 20% renewable carbon, can achieve durability targets. Furthermore, self-crosslinking acrylics now provide block resistance without the need for volatile coalescents, bridging historical performance gaps. Consequently, water-borne formulas are poised to strengthen their dominance in the French architectural coatings market.

Pro-Contractor Loyalty-Reward Platforms by Retail Chains

Castorama, a prominent player in the French architectural coatings market, categorizes its professional clientele into three spending tiers. By offering discounts of up to 10% and granting early-morning access at select stores, Castorama solidifies its loyalty among budget-conscious painters. In a strategic move, AkzoNobel transitioned in July 2025 to a hybrid model, integrating 57 of its own outlets with 51 partner locations across four densely populated territories. This shift not only reduces fixed costs but also ensures contractors remain within easy reach. Retailers, leveraging loyalty data, can fine-tune their product assortments, introduce private labels, and engage in tougher negotiations with suppliers. As a result, national chains are increasingly shifting channel power away from smaller wholesalers, intensifying competition in the French architectural coatings arena.

AI-Enabled Color-Matching Kiosks in DIY Stores

In the France architectural coatings market, where labor is scarce, digital tools are reshaping the landscape. Leroy Merlin's innovative simulator seamlessly merges uploaded images with digital swatches, streamlining the ordering process and minimizing returns. AkzoNobel, leveraging its MIXIT cloud library alongside Automatchic spectrophotometers, has significantly reduced matching times and waste, boosting productivity for professional painters. Meanwhile, Sherwin-Williams is testing automated dosing machines that can prepare four shades in just six minutes, achieving an impressive accuracy of 0.01 grams. These advancements not only elevate job-site efficiency but also lower the skill barriers for users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spike in titanium dioxide prices and supply shocks | -0.7% | National, with spillover from EMEA-wide cost pressures | Short term (≤ 2 years) |

| Labor shortages in skilled painting contractors | -0.5% | National, acute in urban centers and high-demand regions | Medium term (2-4 years) |

| Home-improvement spend squeeze from high mortgage rates | -0.4% | National, concentrated in Île-de-France and high-cost housing markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Spike in Titanium Dioxide Prices and Supply Shocks

In February 2025, Venator raised TiO₂ prices by EUR 300 per tonne, citing surging energy and CO₂-credit costs. This price hike translates to an additional EUR 60 per finished tonne for wall paints containing 20% TiO₂, accounting for about 3 to 4% of the ex-factory value. The EU Ecolabel's new regulation caps sulfate discharge at 300 kg per TiO₂ tonne, leading to heightened compliance costs for pigment manufacturers. While hiding-power extenders can reduce TiO₂ usage by 20 to 30%, the need for consistent performance limits their widespread adoption. As a result, the architectural coatings market in France feels the squeeze, prompting selective price adjustments and reformulations.

Home-Improvement Spend Squeeze from High Mortgage Rates

ING forecasts a mere 0.5% growth in construction for 2026 in France, attributing the slowdown to rising borrowing costs. Building permits have seen a decline since August 2025, despite a slight uptick earlier that year. Rollbacks on tax incentives, like the Pinel exit, have dampened landlord enthusiasm. Additionally, cuts to the 'MaPrimeRénov’ subsidy' have reduced projected energy-retrofit work by 1.3%. Payment delays from public clients are straining contractor cash flows and lengthening project timelines. As a result, constrained household and builder budgets are expected to limit the growth of France's architectural coatings market in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Residential Renovation Drives Share Despite Policy Headwinds

In 2025, residential projects dominated the France architectural coatings market with 67.94% market share, and they are projected to achieve a CAGR of 4.05% through 2031. Younger homeowners are increasingly opting for stay-and-upgrade strategies. With trade labor in short supply, DIY projects now account for over half of the market execution. This trend has heightened the demand for user-friendly products, particularly single-coat solutions that merge primer and topcoat functionalities. While cuts to MaPrimeRénov’ and CEE credits are set to diminish subsidized thermal retrofits in 2026, they concurrently invigorate a niche for aesthetic refreshes, funded by household savings. As a result, the residential segment continues to be the driving force behind the France architectural coatings market.

New non-residential output for commercial and institutional buildings is projected to rise by a modest 0.5% in 2026. The office sector is lagging, hindered by hybrid work models that delay tenant relocations. However, sectors like data centers, healthcare, and educational institutions are carving out specialized niches, emphasizing the need for hygienic and fire-retardant systems. Furthermore, as ESG finance gains traction, property owners are increasingly turning to low-VOC paints to attain coveted green-building certifications. Even with a slowdown in construction starts, retrofit mandates from the Tertiary Decree are bolstering baseline demand, highlighting the resilience of the France architectural coatings industry amidst challenging macroeconomic conditions.

By Technology: Water-Borne Formulations Capture Regulatory and Consumer Preference

In 2025, water-borne coatings led the architectural coatings market in France with 81.12%, and they're projected to grow at a 4.21% CAGR through 2031. The EU's Phase 2 VOC cap of 30 g/L for interior matt coatings has largely pushed solvent-borne options out of homes. This shift is further solidified by France's A+ label. Meanwhile, new self-crosslinking acrylics provide durability without the need for coalescents, rivaling the gloss and block resistance of traditional alkyds. To sidestep regulatory risks, retailers are prominently featuring water-borne lines in their planograms, bolstering their market share.

Solvent-borne products still find their place on heritage façades, high-exposure exteriors, and specific primers where performance overshadows emission concerns. However, even in these specialized areas, water-borne alkyd emulsions are beginning to challenge the status quo. Additionally, imports from more affordable EU plants are filling supply gaps, showcasing the adaptability of supply chains within France's architectural coatings landscape.

By Resin Type: Acrylic Dominance Reinforced by Innovation in Bio-Based and Self-Crosslinking Systems

In 2025, acrylic resins dominated the French architectural coatings market, securing 50.35% of the share. With their versatility, cost-effectiveness, and compliance with EU Ecolabel toxicity limits, these resins are set to grow at a CAGR of 4.18% through 2031. Bio-content blends, exemplified by RUBBOL WF 3350, demonstrate that renewable carbon can achieve long-term durability. Additionally, high-opacity acrylic binders enable formulators to remain under the NF Environnement's 40 g/m² TiO₂ limit, leading to savings on raw materials and a reduction in embodied CO₂.

While alkyds continue to find their place in wood stains and gloss enamels, they're facing increasing competition from water-borne emulsions, which are gradually overtaking solvent grades. Polyurethane dispersions are the go-to choice for high-traffic floors that demand abrasion resistance. In contrast, epoxies are primarily used for industrial flooring and secondary containment. Hybrid silicone-modified acrylics are gaining traction in exterior walls due to their self-cleaning properties. This diversification in resins is pushing technical boundaries, yet acrylics remain central to the French architectural coatings landscape.

Competitive Landscape

The France architectural coatings market exhibits a moderately consolidated nature, with global giants like AkzoNobel, PPG, and Sherwin-Williams face off against regional players such as Cromology, V33, and Caparol. AkzoNobel, for instance, pumped EUR 22 million into elevating Montataire to a flagship status and streamlined its Sikkens stores, reducing the count from 99 to 57. In a strategic move, it partnered with 26 sites to alleviate overhead costs. Meanwhile, Cromology, in early 2025, merged its Tollens and Zolpan networks, capitalizing on Tollens’ accolade of “Meilleure Enseigne 2026” to draw in talent.

Digital innovations and automation set larger players apart. PPG's collaboration with Toyota in 2025 introduced MOONWALK automated mixers and VISUALIZID digital color tools in body shops, hinting at a model adaptable for architectural sectors. On another front, Sherwin-Williams is testing automated dosing and analytics systems, significantly reducing mixing time and paint wastage, thus tackling labor challenges.

Retail private labels from Leroy Merlin and Castorama are making inroads into entry-price segments, leveraging loyalty program insights and strategic shelf space control. While updates to the EU Ecolabel and France’s A+ emissions law escalate certification expenses, they also benefit suppliers with a strong compliance backbone. These dynamics create a competitive yet controlled environment, placing the France architectural coatings market at a moderate concentration level.

France Architectural Coatings Industry Leaders

AkzoNobel N.V.

DAW SE

PPG Industries, Inc.

Cromology

V33 Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: AkzoNobel launched Autowave Optima, a water-borne basecoat that reduces process time by 50% and carbon emissions by 60%.

- January 2025: AkzoNobel committed EUR 22 million to modernize its Montataire decorative-paint plant and streamline French operations.

France Architectural Coatings Market Report Scope

Architectural coatings are protective and decorative finishes applied to stationary, on-site structures, such as residential, commercial, and industrial buildings. These products, including paints, stains, sealers, and varnishes, are designed for both exterior and interior surfaces to offer durability, aesthetics, and resistance to environmental damage.

The France Architectural Coatings market is segmented by end-user industry, technology and resin. By end-user industry, the market is segmented into commercial and residential. By technology, the market is segmented into solvent-borne and water-borne. By resin, the market is segmented into acrylic, alkyd, epoxy, polyester, polyurethane, and other resin types. For each segment, market sizing and forecasts are provided in terms of value (USD).

By End-User Industry

| Commercial |

| Residential |

By Technology

| Solvent-borne |

| Water-borne |

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

| By End-User Industry | Commercial |

| Residential | |

| By Technology | Solvent-borne |

| Water-borne | |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms