Pharmaceutical Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

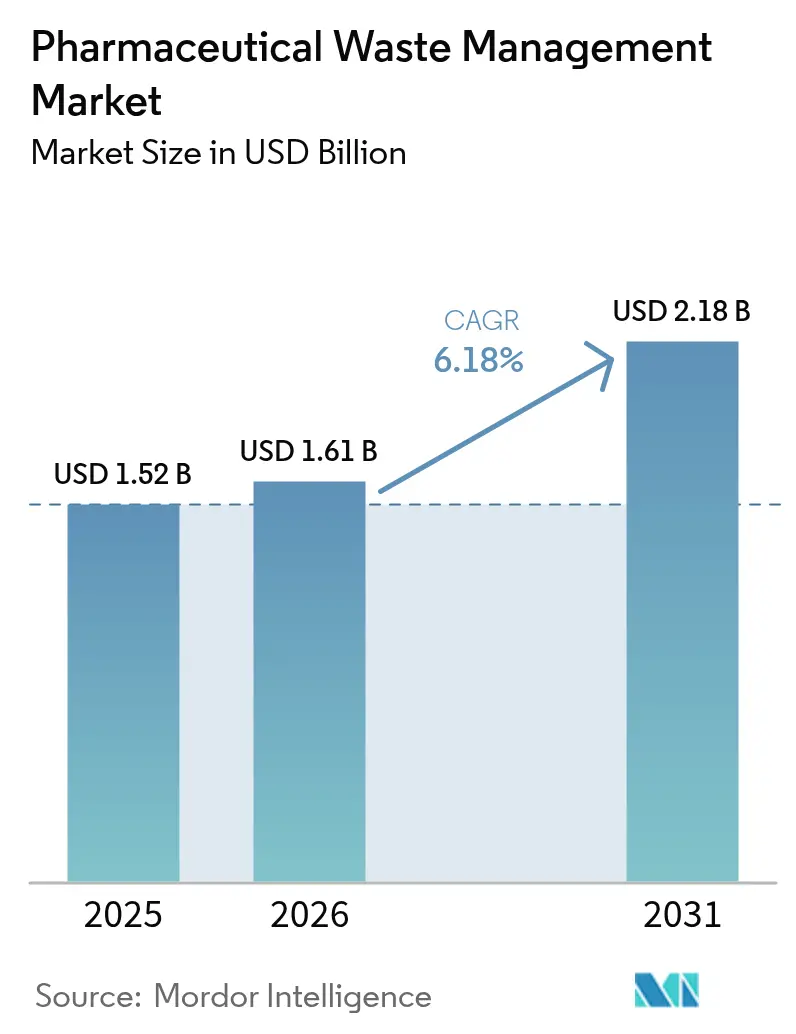

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Waste Management Market Analysis by Mordor Intelligence

The Pharmaceutical Waste Management Market size is expected to grow from USD 1.52 billion in 2025 to USD 1.61 billion in 2026 and is forecast to reach USD 2.18 billion by 2031 at 6.18% CAGR over 2026-2031.

Rising enforcement of EPA Subpart P rules, the European Union’s Urban Wastewater Treatment Directive, and similar measures in Asia-Pacific are pushing healthcare facilities to adopt comprehensive disposal programs rather than reactive fixes. Expansion of biopharmaceutical manufacturing, rapid consumer take-back initiatives, and sustained investment in advanced oxidation, microwave, and supercritical water technologies further reinforce demand. Intensifying environmental scrutiny and public transparency expectations motivate hospitals and manufacturers to link waste stewardship with broader climate and ESG objectives, while market consolidation allows large players to spread compliance costs across wider networks and invest in innovation that smaller competitors cannot easily replicate.

Key Report Takeaways

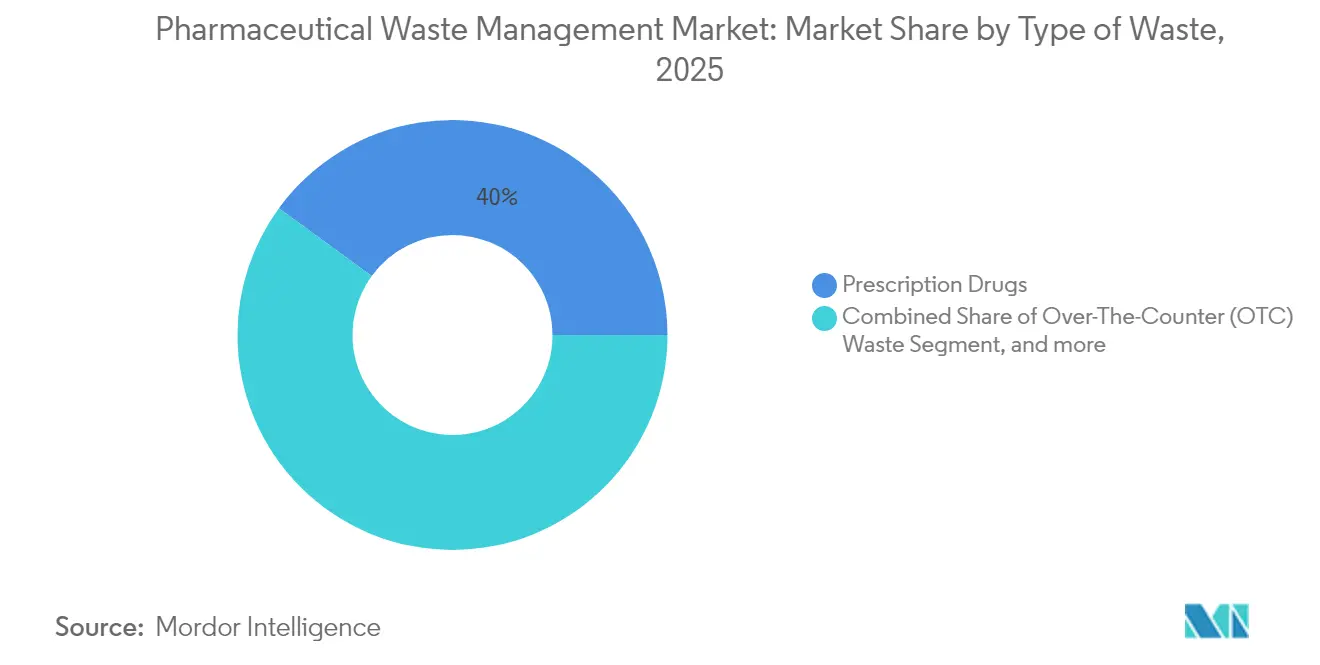

- By waste type, prescription drugs led with 39.96% of pharmaceutical waste management market share in 2025; controlled substances are projected to advance at a 7.35% CAGR through 2031.

- By waste generator, hospitals and clinics held 55.02% of the pharmaceutical waste management market share in 2025, whereas retail pharmacies are poised for the fastest 8.05% CAGR to 2031.

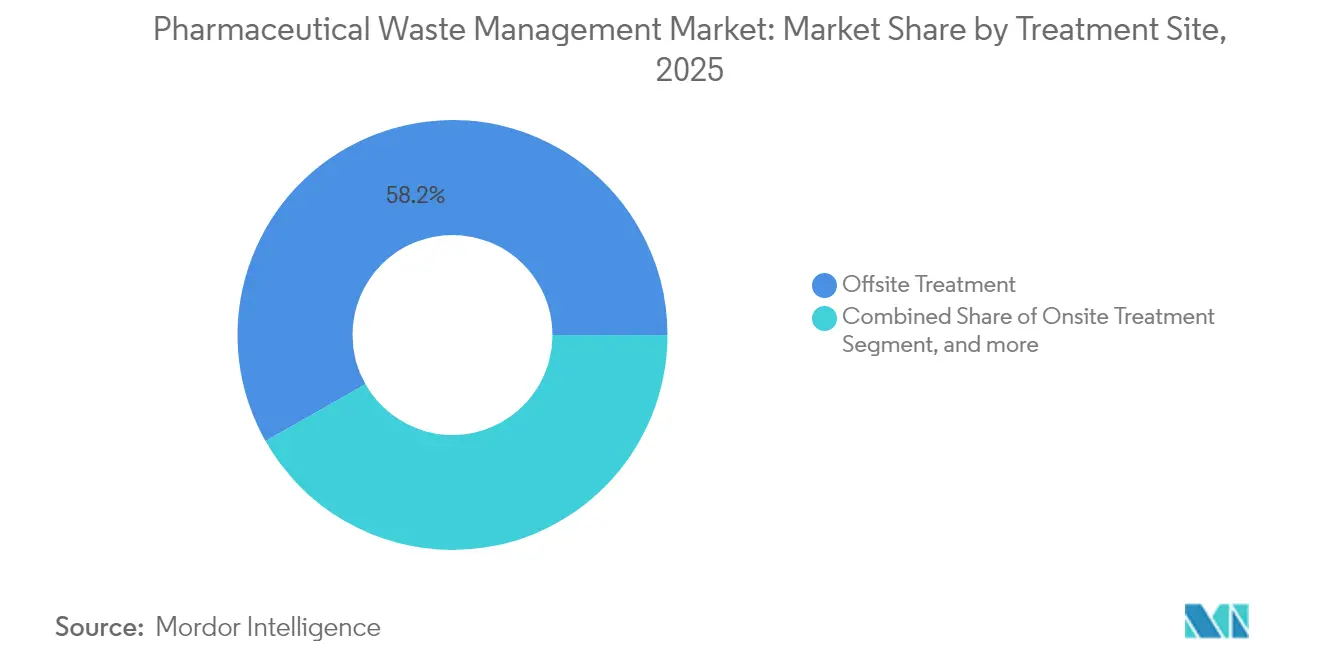

- By treatment site, offsite processing accounted for 58.21% share of the pharmaceutical waste management market size in 2025, while onsite solutions are expanding at an 8.21% CAGR between 2026-2031.

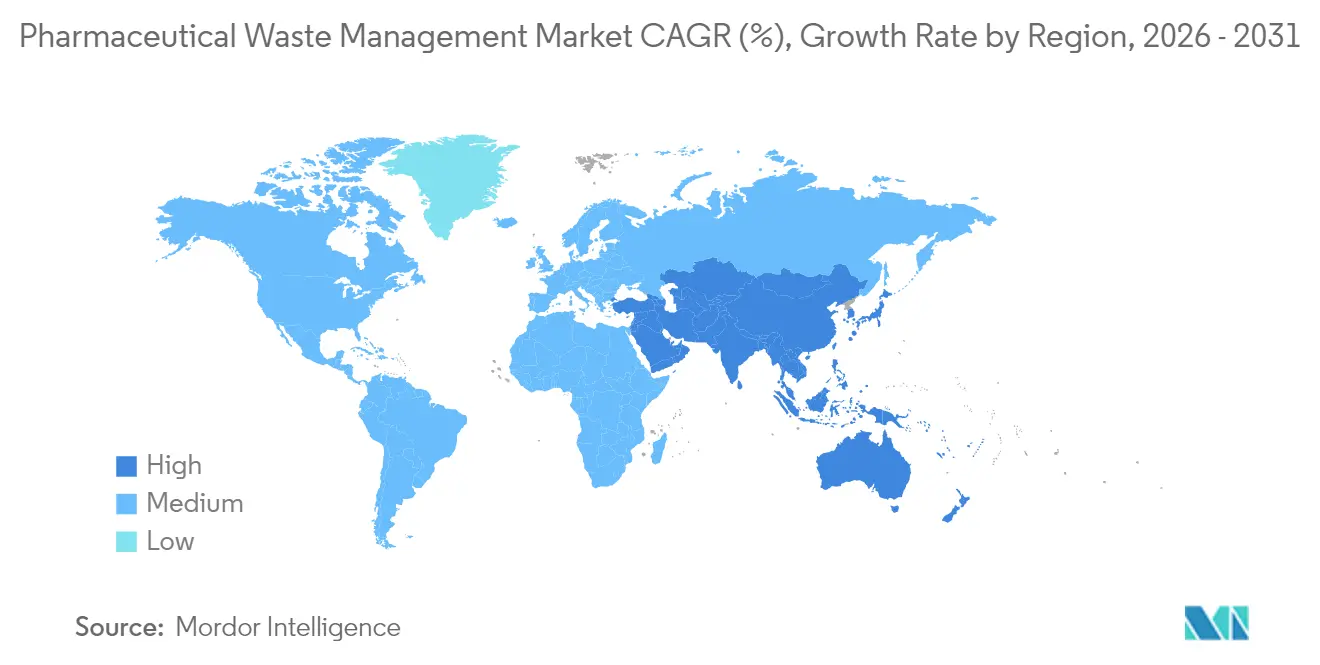

- By geography, North America dominated with 39.55% of pharmaceutical waste management market share in 2025; Asia-Pacific is set to grow at an 8.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Pharmaceutical Production | +1.5% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Stringent Regulatory Compliance | +1.2% | North America & EU; APAC gaining pace | Short term (≤ 2 years) |

| Growing Environmental Concerns | +0.8% | Developed markets worldwide | Long term (≥ 4 years) |

| Advancements in Waste Treatment Technologies | +1.1% | North America & Europe first; APAC following | Medium term (2-4 years) |

| Public Awareness and Corporate Responsibility | +0.7% | Global, strongest in consumer-facing segments | Long term (≥ 4 years) |

| Expansion of Healthcare and Biopharma Manufacturing | +0.9% | Asia-Pacific core, spill-over to MEA & Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Pharmaceutical Production

Global drug output continues to climb, and biologics add complex cytotoxic residues that require specialized containment and high-temperature destruction. Single-use bioprocessing lowers cross-contamination risk but raises plastic volumes that many recyclers cannot handle. Manufacturers pursuing zero-liquid-discharge have cut biological and chemical oxygen demand by up to 90%, showing clear operational savings alongside compliance gains. Emerging production hubs in India, Vietnam, and the Philippines deepen the pharmaceutical waste management market as these regions race to match disposal infrastructure with capacity expansion. Full-service providers able to integrate solid, liquid, and cytotoxic waste solutions now enjoy a competitive edge.

Stringent Regulatory Compliance

The EPA ban on sewering hazardous pharmaceuticals, the DEA review of non-incineration destruction options, and Europe’s Extended Producer Responsibility cost-recovery model shift disposal costs upstream.[1]Drug Enforcement Administration, “Controlled Substance Public Meeting on Destruction Technologies,” dea.gov Hospitals in jurisdictions adopting Subpart P now maintain detailed cradle-to-grave manifests, and very small quantity generators face sharper training mandates.[2]Stericycle Inc., “Nevada Hospital, Medical and Infectious Waste Incinerator Opening,” stericycle.com German drug makers alone expect EUR 36 billion in micropollutant removal fees over three decades, underscoring why pharmaceutical waste management market participants with robust compliance consulting departments win larger contracts. Cross-border operators also navigate differing take-back, labeling, and reverse-logistics rules, reinforcing the value of global scale.

Growing Environmental Concerns

Healthcare leaders increasingly treat waste minimization as a climate and brand imperative. United States operating rooms account for 20-30% of hospital waste, driving systemwide audits that save USD 700 million in five years by classifying waste more accurately. Advanced oxidation using nanoscale zero-valent iron shows 96.8% pollutant removal, offering hospitals measurable ESG benefits. Circular-economy programs built around the 10Rs framework allow facilities to cut plastics and recover solvents, reinforcing demand for vendors who can document downstream carbon impacts of every disposal method.

Advancements in Waste Treatment Technologies

Supercritical water oxidation now reaches 99.99% destruction of PFAS and cytotoxic residues at lower temperatures than legacy incinerators. Electrochemical units enable onsite PFAS breakdown, while microwave systems slash waste volume by over 80%. AI-driven sorting and blockchain-based chain-of-custody tools improve segregation accuracy and audit readiness. The pharmaceutical waste management market rewards firms that bundle these modular technologies into tiered service plans for hospitals of every size.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Disposal & Compliance Costs for Hazardous Pharma Waste | -0.9% | Global, hardest in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Resistance to Adoption of New Technologies | -0.6% | Traditional systems in developed markets, rural facilities worldwide | Medium term (2-4 years) |

| Limited Infrastructure in Developing Regions | -0.5% | Emerging Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Fragmented Reverse Logistics Regulations Across Borders | -0.4% | Multinational operations worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Disposal & Compliance Costs for Hazardous Pharma Waste

Regulated medical waste often costs USD 0.20-0.50 per pound versus USD 0.03-0.08 for general trash, straining small clinics that spend USD 160-360 monthly on disposal. CMS refund rules on discarded single-dose drugs add further administrative burden.[3]Centers for Medicare & Medicaid Services, “Discarded Drug Refunds Final Rule,” cms.gov Misclassification remains rampant—studies show education programs can boost correct segregation by 65%, but facilities lacking budget postpone training. Price pressure pushes buyers to competitive bids, compressing margins even as operators shoulder higher capital outlays for new kilns or advanced oxidation units.

Resistance to Adoption of New Technologies

Some healthcare executives distrust novel methods, citing upfront cost, staff retraining, and perceived regulatory uncertainty. Rural hospitals in North America and smaller European clinics still rely on manual segregation and basic autoclaves. Vendors must therefore offer financing models, turnkey maintenance, and robust validation data to reduce perceived risk and accelerate changeover.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Waste: Controlled Substances Drive Regulatory Innovation

Prescription drugs represented 39.96% of pharmaceutical waste management market size in 2025. Hospitals, long-term care facilities, and retail pharmacies treat these as mixed hazardous streams demanding incineration or advanced oxidation for safe destruction. Meanwhile, controlled substances comprise the fastest-growing slice, logging a 7.35% CAGR as regulators tighten diversion controls.

Heightened DEA oversight fuels mail-back envelope schemes for opioids, and pilot chemical degradation systems now deliver complete molecular breakdown without incineration. The pharmaceutical waste management market increasingly prizes vendors capable of preserving chain-of-custody integrity through tracked containers, monitored vaults, and blockchain logs. Cytotoxic chemotherapy agents form a smaller yet high-margin segment requiring closed-system transfer devices, while veterinary pharmaceuticals and OTC products round out the mix with simplified protocols under updated EPA nicotine exclusion rules.

By Waste Generator: Retail Pharmacies Accelerate Take-Back Programs

Hospitals and clinics generated commanding 55.02% of overall pharmaceutical waste management market size in 2025. Their environmental services teams already partner with full-service vendors for sharps, chemotherapy, controlled substance destruction, and cradle-to-grave documentation.

Retail pharmacies, however, are on track for the most robust 8.05% CAGR. Chain drugstores now operate thousands of in-store kiosks and coordinate national take-back events, converting public foot traffic into safe return streams. Biopharma manufacturing plants face mounting polymer and solvent loads from single-use systems, while research labs generate sporadic volumes of experimental compounds that nonetheless require meticulous characterization. The upshot is a diversification of customer profiles, compelling providers to tailor service bundles from small-quantity mailers to bulk tanker pickups.

By Treatment Site: Onsite Solutions Gain Momentum

Centralized offsite plants captured 58.21% of 2025 revenue, benefiting from scale, rotary-kiln capacity, and established logistics. Nonetheless, onsite systems are posting an 8.21% CAGR as hospitals prioritize immediate compliance control and shrink transport expenses.

Microwave units installed in tertiary hospitals process 88 kg per hour, cut waste volume by 80%, and meet global infectious waste standards. Some pharmaceutical plants deploy continuous supercritical water reactors that treat isopropyl alcohol effluent for water reuse, illustrating circular-economy payoffs. Hybrid models onsite pre-treatment followed by offsite final destruction are also gaining favor, giving facilities flexibility without capital outlay for incinerators.

Geography Analysis

North America led the pharmaceutical waste management market with 39.55% share in 2025, anchored by mature regulatory enforcement and capital-intensive infrastructure. Recent investments include a USD 110 million Nevada incinerator that couples waste-to-energy with water reuse, plus a planned Arkansas facility that guarantees incineration capacity for another five years. Cross-border harmonization under the Basel Convention streamlines shipments between the United States, Canada, and Mexico, enabling nationwide service networks to optimize routing and reduce emissions.

Asia-Pacific is the fastest-growing region at an 8.47% CAGR through 2031. China’s anti-espionage rules complicate API exports and raise domestic disposal demand, while India’s draft Liquid Waste Management Rules 2024 impose extended responsibility on high-volume water users. Japan’s push for membrane-based water-for-injection systems underscores the region’s tilt toward energy-efficient treatment methods. Southeast Asian countries continue to attract contract manufacturing, creating sizeable yet infrastructure-limited demand for advanced destruction services.

Europe is undergoing a regulatory overhaul that links pharmaceutical packaging, wastewater micropollutant removal, and producer responsibility. Germany’s EUR 36 billion compliance tab over 30 years epitomizes the financial magnitude of forthcoming upgrades. European Medicines Agency guidelines now embed persistence, bio-accumulation, and toxicity criteria in environmental risk assessments, compelling manufacturers to support downstream treatment costs. Providers with pan-EU compliance platforms and specialized high-temperature capacity stand to consolidate market share as smaller collectors exit due to capital constraints.

Competitive Landscape

Consolidation is reshaping the pharmaceutical waste management market as regulatory complexity and technology needs outpace small operators’ resources. Waste Management’s USD 7.2 billion acquisition of Stericycle combines the country’s largest logistics network with medical waste expertise, promising USD 125 million in annual synergies and a unified platform offering regulated medical waste, secure information destruction, and take-back program management.

Technology capability remains a key differentiator. General Atomics’ supercritical water systems posting 99.9% PFAS destruction and electrochemical oxidation units designed for hospital basements highlight a pivot toward cleaner, resource-efficient solutions. Microwave technology suppliers promote rapid cycle times and low emissions, attracting facilities seeking to minimize Scope 3 greenhouse-gas disclosures.

Regional specialists leverage local knowledge and cultural acceptance to penetrate emerging markets. Firms partnering with municipal authorities in Brazil or state-owned enterprises in India offer modular plants that address infrastructure gaps. Nevertheless, capital intensity favors multinationals that can amortize R&D across global footprints while fulfilling multi-jurisdictional chain-of-custody obligations.

Pharmaceutical Waste Management Industry Leaders

BioMedical Waste Solutions, LLC

Clean Harbors, Inc.

Sharps Compliance, Inc.

US Ecology, Inc.

Waste Management Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Perma-Fix Environmental Services expanded PFAS treatment operations by launching a 1,000-gallon PFAS Destruction Reactor in Florida, demonstrating high effectiveness in destroying PFAS contaminants across various carbon-fluorine chains. The company collaborates with waste generators and disposal firms handling Aqueous Film-Forming Foam waste while planning a second-generation treatment unit to enhance capacity and efficiency.

- October 2024: Stericycle opened a USD 110 million Hospital, Medical, and Infectious Waste Incinerator facility in McCarran, Nevada, featuring advanced systems for safely treating infectious materials and disposing of unwanted medications. The facility incorporates water reuse and waste-to-energy technologies while operating under stringent emissions standards.

- June 2024: Waste Management announced its USD 7.2 billion acquisition of Stericycle, enhancing environmental solutions in the healthcare market through comprehensive regulated medical waste and secure information destruction services. The transaction generates expected annual synergies exceeding USD 125 million while supporting sustainability initiatives.

- June 2024: Unither Pharmaceuticals announced a USD 106 million investment to modernize its 350,000 square-foot facility in Monroe County, New York, including a 43,000 square-foot expansion with energy-efficient upgrades aimed at reducing carbon emissions. The project enhances production capabilities for preservative-free sterile products while creating up to 180 new jobs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pharmaceutical waste management market as the collection, transport, treatment, and final disposal of expired, unused, or contaminated human and veterinary drugs generated by healthcare providers, retail pharmacies, households, and research laboratories. Activities evaluated cover both hazardous and non-hazardous drug waste streams across on-site and off-site treatment routes.

Scope exclusion: General biomedical items with no active-ingredient residue and process scrap arising inside manufacturing plants lie outside this assessment.

Segmentation Overview

- By Type of Waste

- Prescription Drugs

- Over-The-Counter (OTC) Waste

- Controlled Substances

- Chemotherapy Drugs

- Veterinary Pharmaceuticals

- Other Waste Type

- By Waste Generator

- Hospitals & Clinics

- Retail Pharmacies

- Biopharma Manufacturing Sites

- Long-term Care & Nursing Homes

- Research Laboratories

- By Treatment Site

- Onsite Treatment

- Offsite Treatment

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts interviewed waste-treatment operators, hospital compliance officers, retail-pharmacy chains, and regional regulators across North America, Europe, Asia-Pacific, and the Gulf. These discussions validated disposal tariffs, average drug-return volumes, technology adoption rates, and upcoming rule changes, filling data gaps left by public records and guiding assumption ranges.

Desk Research

We began with open datasets from bodies such as the US Environmental Protection Agency, Eurostat, the World Health Organization, and the European Medicines Agency, supplemented by trade association bulletins from the Healthcare Waste Institute and national take-back program records. Company filings, investor decks, and reputable news archives accessed through D&B Hoovers and Dow Jones Factiva helped us size leading service providers and flag capacity additions. Customs shipment logs, patent abstracts on advanced oxidation units, and peer-reviewed journals on incinerator emission factors grounded our unit economics. The sources listed illustrate the breadth of material consulted and are not exhaustive.

Market-Sizing & Forecasting

Our base year value rests on a top-down reconstruction of waste volumes using national prescription data, typical return ratios, and treatment fees, which are then cross-checked through selective bottom-up supplier roll-ups. Key variables, such as annual pharmaceutical sales, average shelf-life expiry rates, incineration capacity utilization, take-back program penetration, and enforcement fine incidence, drive the model. Multivariate regression projects each driver through the forecast period, while scenario analysis tests regulatory or technology shocks. Where bottom-up totals diverged, adjustment followed the midpoint of primary-source guidance.

Data Validation & Update Cycle

Outputs pass a two-tier analyst review, variance checks against independent waste tonnage benchmarks, and anomaly flags generated by our automated dashboards. Mordor refreshes every study annually, and analysts trigger interim updates when material events, such as new disposal mandates, occur, ensuring clients always receive the latest market view.

Why Mordor's Pharmaceutical Waste Management Baseline Commands Reliability

Published market values often differ because each firm selects unique waste categories, pricing assumptions, and forecast cadences. Those choices, once compounded, widen the gap that decision-makers must understand.

Key gap drivers here include whether household take-back volumes are counted, if hazardous and non-hazardous fees are blended, how foreign-currency revenues are converted, and the refresh timing that captures the 2024 Stericycle acquisition impact.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.52 bn (2025) | Mordor Intelligence | - |

| USD 40.3 bn (2024) | Global Consultancy A | Rolls broader medical and industrial drug residues into scope and uses uniform global average pricing |

| USD 1.66 bn (2024) | Research House B | Excludes household returns and applies 2023 exchange rates without inflation adjustment |

| USD 3.0 bn (2024) | Trade Journal C | Counts only hazardous waste and models forward using constant volume, high growth price escalators |

The comparison shows that when scope, price ladders, and update cadence shift, so do totals. By anchoring volumes to transparent prescription data, validating through on-ground interviews, and updating each year, Mordor delivers a balanced baseline that executives can retrace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the pharmaceutical waste management market?

The pharmaceutical waste management market size reached USD 1.61 billion in 2026 and is projected to hit USD 2.18 billion by 2031.

Which region leads the pharmaceutical waste management market?

North America held 39.55% of revenue in 2025, reflecting stringent EPA regulations and well-developed treatment infrastructure.

Why are controlled substances the fastest-growing waste type?

Escalating DEA diversion controls and innovation in non-incineration destruction methods are driving a 7.35% CAGR for controlled-substance disposal services.

How fast are onsite treatment solutions growing?

Onsite technologies such as microwave disinfection are expanding at an 8.21% CAGR as hospitals seek tighter compliance control and lower logistics costs.

What is fueling pharmaceutical waste management market growth in Asia-Pacific?

Rapid expansion of biopharma manufacturing and newly enacted extended-producer-responsibility rules are pushing Asia-Pacific to an 8.47% CAGR through 2031.

How is industry consolidation affecting competition?

Large players like Waste Management and Stericycle are merging to offer integrated services and absorb rising compliance costs, raising barriers for smaller firms while accelerating technology investment.

Page last updated on: