Foundry Coke Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

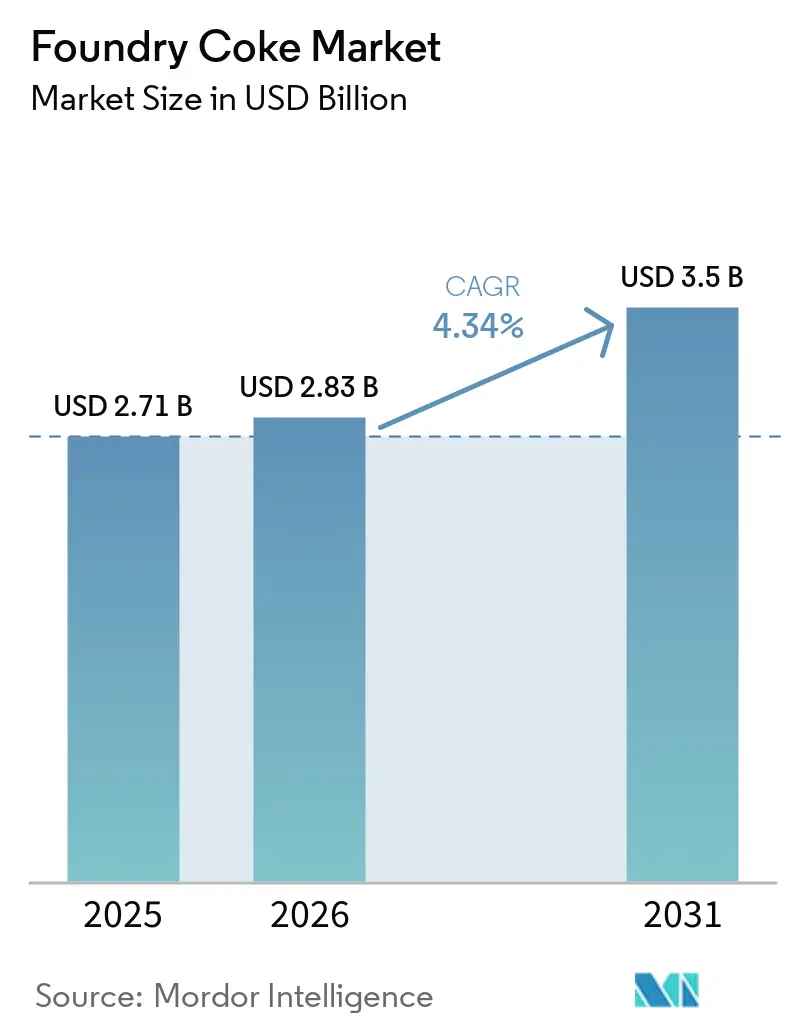

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 3.5 Billion |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

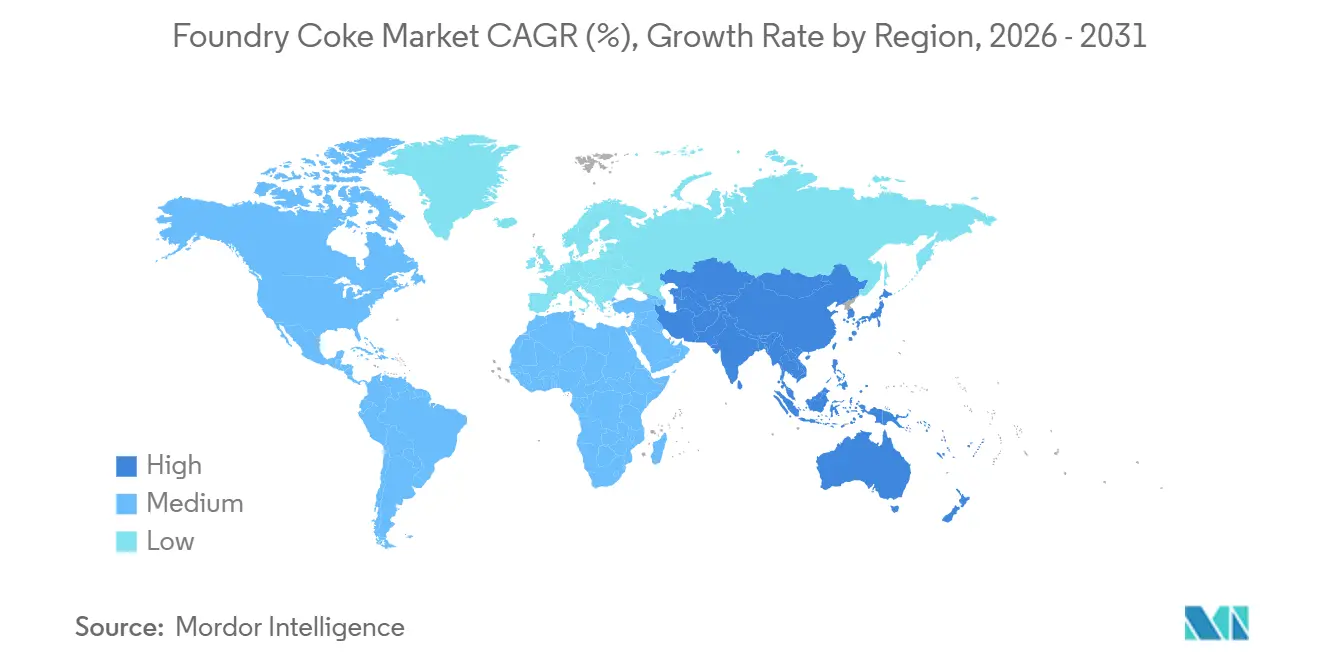

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foundry Coke Market Analysis by Mordor Intelligence

The Foundry Coke Market size was valued at USD 2.71 billion in 2025 and is estimated to grow from USD 2.83 billion in 2026 to reach USD 3.5 billion by 2031, at a CAGR of 4.34% during the forecast period (2026-2031). Recent growth hides a widening split between high-growth Asia-Pacific centers that continue to commission new cupola capacity and mature North American and European hubs that are removing cupolas altogether or converting to electric melting in response to decarbonization mandates. The European Union (EU) Carbon Border Adjustment Mechanism (CBAM) began its definitive phase in January 2026, effectively adding EUR 60-80 per ton CO₂ to the landed cost of coke-fired castings and undermining the competitiveness of cupolas in the region. At the same time, the United States Department of Energy awarded more than USD 150 million to two of the largest ductile-iron producers to replace coke-fired cupolas with induction furnaces, removing an estimated 50,000-70,000 tons of annual foundry-coke demand. Petroleum-coke blending, anthracite briquetting, and low-ash product premiums are reshaping procurement practices as OEMs (original equipment manufacturers) push Scope 3 carbon targets into supplier contracts and cupola operators scramble to document fuel traceability.

Key Report Takeaways

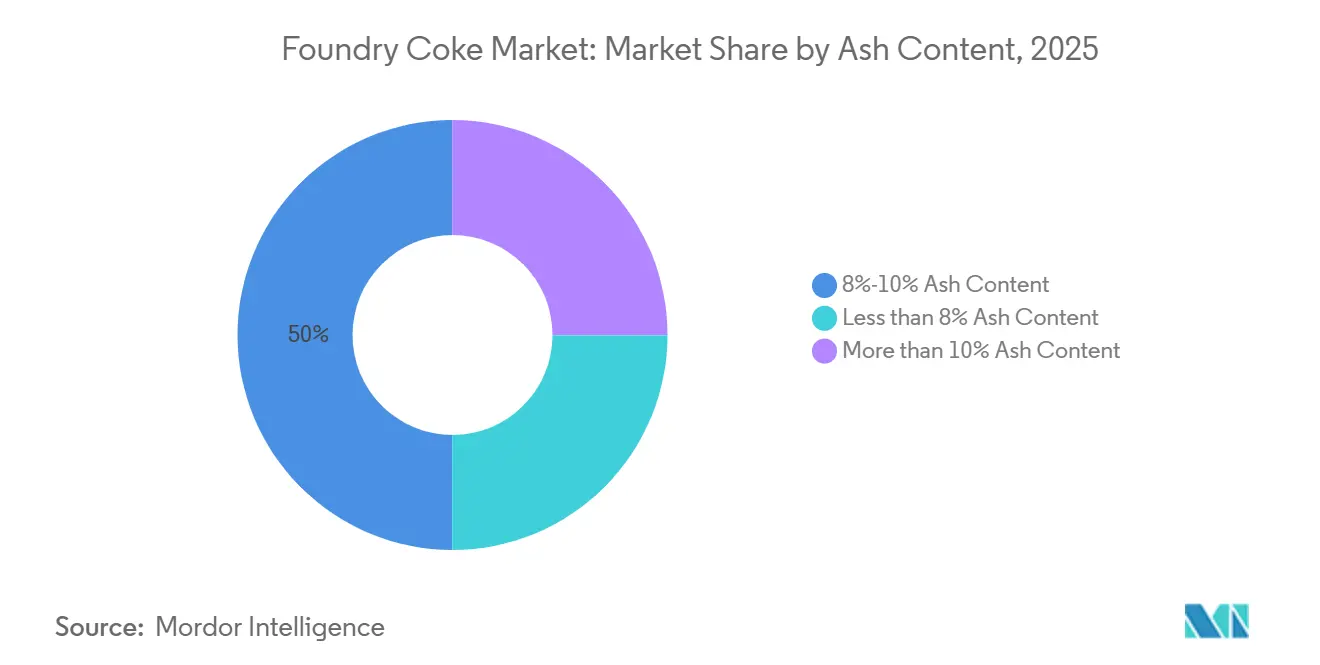

- By ash content, the 8%-10% segment led with 49.98% revenue share in 2025; while less than 8% ash content is projected to expand at 4.77% CAGR through 2031.

- By carbon type, metallurgical coke accounted for 67.78% of the foundry coke market share in 2025, while petroleum coke is advancing at 4.89% CAGR through 2031.

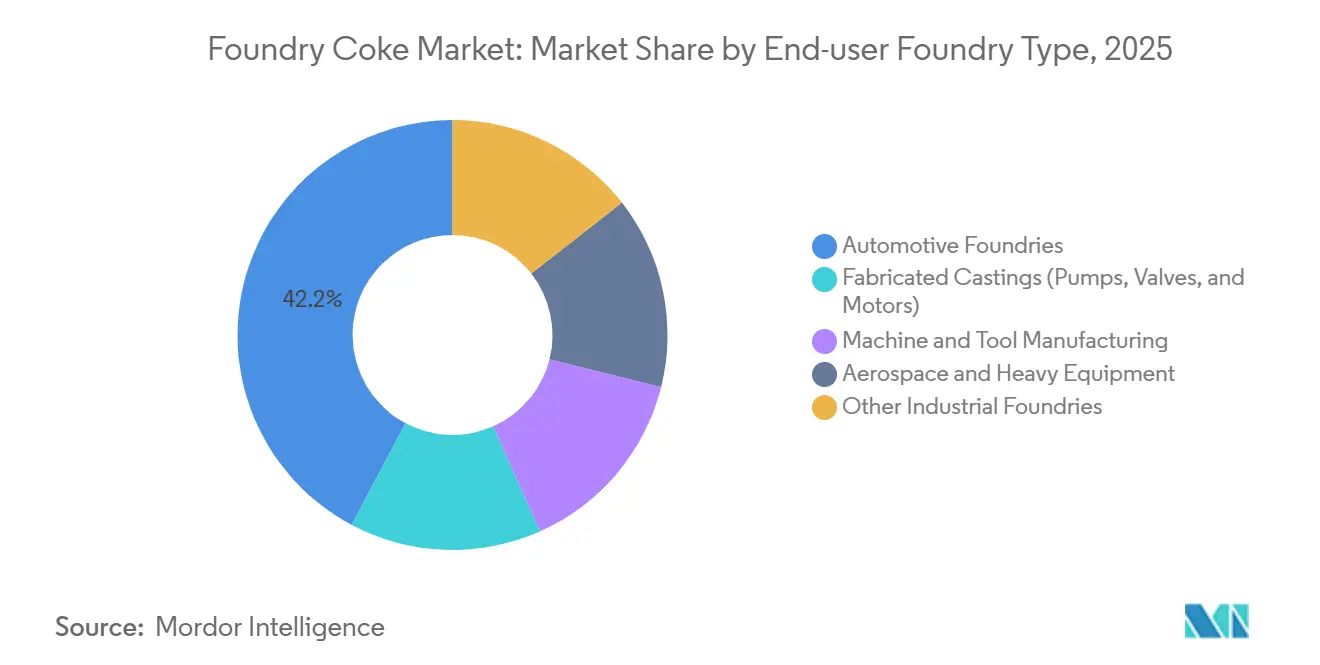

- By end-user foundry type, automotive foundries commanded 42.23% of the foundry coke market size in 2025; aerospace and heavy equipment are forecast to grow at 4.66% CAGR to 2031.

- By geography, Asia-Pacific captured 57.91% revenue share in 2025; the region is on track for a 5.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Foundry Coke Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Southeast-Asian foundry clusters | +0.9% | Indonesia, Vietnam, Thailand, India | Medium term (2-4 years) |

| High-strength thin-wall casting investment | +0.7% | North America, EU, global automotive hubs | Medium term (2-4 years) |

| Construction-equipment rebound | +0.5% | India, Brazil | Short term (≤2 years) |

| Wind-turbine gearbox demand | +0.6% | China, India, EU offshore, North America | Long term (≥4 years) |

| OEM Scope 3 decarbonization push | +0.8% | EU and North America first movers, global diffusion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Southeast-Asian Foundry Clusters

Rising foreign direct investment in Indonesia, Vietnam, and Thailand is integrating nickel smelting, stainless steel, and ductile-iron cupolas inside special-economic zones that run their own coke ovens. The 3.2 million tonnes per annum (Mtpa) Morowali Industrial Park in Central Sulawesi supplies 51 customers across 17 countries, showcasing a self-sufficient model that bypasses CBAM-type carbon surcharges and achieves logistics savings that out-compete traditional merchant suppliers. Buoyant infrastructure expenditure and battery-supply-chain localization sustain multi-year demand visibility, establishing Southeast Asia as the fastest-growing pocket within the broader foundry coke market.

Investments in High-Strength Thin-Wall Castings for Lightweighting

Automotive regulations on fuel economy and emissions are pushing foundries toward 3-5 mm thin-wall ductile-iron and compacted-graphite-iron castings. These castings require premium low-ash coke (less than 8%) with high mechanical strength (M40 greater than or equal to 75%) to limit slag and maintain tight dimensional tolerances. OEM audits that extend to Scope 3 reporting now incentivize supply contracts that guarantee consistent low-ash chemistry and full batch traceability[1]Volvo Group, “Low-CO₂ Steel in Volvo Trucks,” volvogroup.com. Foundries unable to secure quality coke face higher scrap rates or must blend higher-sulfur petroleum coke and anthracite, which complicates melt chemistry control.

Recovery of Construction-Equipment Output in India and Brazil

Indian and Brazilian procurement cycles for excavators, wheel loaders, and earth-moving equipment have revived after pandemic-era delays, lifting gray-iron and ductile-iron casting volumes. Although exact unit-build data remain limited, FDI (foreign direct investment) inflows to India’s manufacturing clusters and public-sector infrastructure announcements point to rising domestic casting tonnage. Brazilian mining-sector capital spending supports heavy-equipment output, while currency depreciation favors local sourcing of components that are traditionally price-sensitive and hence rely on mid-grade 8-10% ash coke.

Renewable-Energy Stimulus Driving Wind-Turbine Gearbox Castings

Global offshore and onshore wind build-outs demand massive ductile-iron castings for hubs, main frames, and yaw drives. Large cupolas remain cost-effective for such heavy castings, provided they run on ultra-low-sulfur coke that keeps inclusions below specification. Chinese foundries supply Europe’s offshore projects under ISO 9001-compliant documentation, and Indian turbine OEMs are ramping up similar capacity as state auctions bundle local-content rules[2]International Energy Agency, “Renewables 2026,” iea.org. The segment delivers a relatively recession-resilient outlet for premium foundry coke and recarburizers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile premium low-sulfur coal prices | -0.6% | Import-dependent nations: India, Japan, South Korea | Short term (≤2 years) |

| Cupola-to-electric melt migration in the U.S. | -0.9% | North America, selective EU adoption | Medium term (2-4 years) |

| EU CBAM carbon surcharge on cupolas | -0.7% | EU, indirect on exporters to the bloc | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Premium Low-Sulfur Coking-Coal Pricing

Australian cyclone disruptions lifted Fitch’s 2026 premium coal forecast to USD 190/ton, but 2025 Free On Board (FOB) prices had already fallen 21% year-on-year, undercutting producer margins. Coke makers lacking captive mines face squeezed spreads, and foundries endure quotation windows of only 6-12 months, complicating long-range order books and delaying furnace-upgrade decisions that underpin demand stability.

Cupola-to-Electric-Melt Migration at Large U.S. Foundries

United States Pipe & Foundry and American Cast Iron Pipe jointly received USD 150.5 million in 2025 to switch to induction furnaces that will slash CO₂ by up to 95%, removing a combined 50,000-70,000 tons of annual foundry-coke offtake once the conversions finalize in 2027. The precedent accelerates similar studies among municipal and water-infrastructure foundries across Canada and Mexico.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ash Content: Premium Grades Outpace the Mid-Tier

Low-ash (less than 8%) grades cut slag-related defects, extend lining life, and demonstrate a 4.77% CAGR through 2031, outstripping the 8-10% mainstream segment that nonetheless held 49.98% of the 2025 foundry coke market share. AM/NS India’s 1.5 Mtpa Hazira battery, commissioned in December 2025, secures captive premium supply and reduces reliance on spot imports. Western European and North American automotive foundries now mandate low-ash contracts to meet Scope 3 disclosure rules, pushing demand for documented batches with ash below 7% and sulfur under 0.8 %.

Mid-grade 8-10% coke remains the volume workhorse for construction-equipment and municipal castings. Russian GOST 3340-88 limits ash at 11-12%; upgrading to 9% ash allows Chinese and Indonesian exporters to approach EU benchmarks without full premium-grade costs. Blending premium and standard coke is an increasingly common strategy to meet OEM audits without inflating melt costs, preserving the relevance of mid-grade supply for another investment cycle.

By Carbon Type: Petroleum Coke Carves Share as Cost Volatility Bites

Metallurgical coke accounted for 67.78% of the 2025 foundry coke market, favored for its M40 strength and predictable reactivity that keeps cupola shafts stable. Yet petroleum coke, with carbon purity near 99% and energy density of 8,100 kcal/kg, is advancing at 4.89% CAGR to 2031 owing to cost advantages and increasing tolerance for higher sulfur where specifications allow. Thyssenkrupp’s trading arm now bundles calcined petcoke with low-ash met coke and anode butts in blended lots tailored to individual furnace chemistries.

Anthracite briquettes that replace up to 25% of met coke without degrading melt ratios offer a route to emission reduction at lower capital intensity, particularly in markets where energy costs penalize long coking cycles. Specialty pitch coke remains niche but prized as a recarburizer in induction melting, commanding premiums that few foundries can justify outside aerospace or defense contracts.

By End-user Foundry Type: Automotive Dominates, Aerospace Accelerates

Automotive Foundries consumed 42.23% of 2025 demand, reflecting the continued need for ductile-iron engine blocks and suspension parts even as light-vehicle electrification rises. Volvo Trucks’ 2025 low-CO₂ steel pilot, which saved 6,600 tons of emissions, demonstrates the cascading effect of OEM materials policies on coke selection. Electric-vehicle motor housings and structural battery frames still use ductile iron in high-stress zones, sustaining baseline demand for high-quality coke throughout the forecast window.

Aerospace and heavy-equipment foundries, at 4.66% CAGR for the forecast period (2026-2031), are the fastest-growing buyers as North American investment-casting output surged nearly 25% in 2024 on Boeing and Airbus backlogs. These segments specify ash under 8% and sulfur below 0.7% to avert inclusion-related rework in safety-critical parts. Municipal infrastructure and agricultural equipment remain price-driven buyers of standard 10-12% ash coke, providing a demand floor when higher-value sectors soften.

Geography Analysis

Asia-Pacific held 57.91% of global consumption in 2025 and is projected to advance at 5.08% CAGR during the forecast period (2026-2031), the fastest regional pace, underpinned by more than 70 million tons of new blast-furnace iron capacity scheduled between 2024 and 2027. Indonesia’s Morowali cluster anchors exports to India and Japan, while Vietnam’s Haiphong and Thailand’s Chonburi corridors add captive coke ovens for domestic cupolas that supply water-infrastructure and automotive parts. India’s December 2024 import quota on low-ash coke tightened supply and prompted integrated producers to accelerate self-sufficiency projects, a policy that paradoxically stimulates domestic coking-coal washing investments.

North America is contracting in absolute tonnage as the Department of Energy (DOE)-funded furnace switches begin to bite. SunCoke’s domestic offtake fell 360,000 tons in 2025 and is guided lower for 2026, though cross-border supply chains under the United States-Mexico-Canada Agreement (USMCA) still absorb mid-grade coke for gray-iron auto and agricultural castings. Broader uptake of Section 45X clean-manufacturing tax credits will decide whether cupola retirements proceed beyond the water-infrastructure niche.

Europe faces CBAM costs that elevate low-ash coke demand even as total volume shrinks. Saint-Gobain PAM’s French plant documented a 95% CO₂ cut after switching to induction melting, eliminating 7,800 tons/year of coal and setting a compliance benchmark for other EU foundries. Eastern European operators remain on cupolas but must document emission factors, boosting demand for dry-quenched coke with full traceability from Chinese or Indonesian suppliers able to certify sub-10% ash lots.

South America remains cyclical. Brazil benefits from mining-sector capex and a weak real that encourages local casting procurement, yet high borrowing costs limit capacity build-outs. Argentina and the Andean nations purchase coke on a spot basis for municipal and mining castings, rendering the region cost-sensitive and slow to adopt premium low-ash contracts.

Middle East and Africa shows scattered demand concentrated in Saudi Arabia’s metals diversification and South Africa’s mining-machinery exports. End-users import coke primarily from India and China, with logistics bottlenecks and financing constraints capping uptake of premium low-ash material. Without explicit carbon-pricing or Scope 3 mandates, coke quality decisions remain dictated by furnace yield economics rather than sustainability targets.

Competitive Landscape

The Foundry Coke market is moderately fragmented. Competitive intensity bifurcates: a premium, compliance-driven low-ash tier in Europe and North America, and a volume-driven mid-ash tier in Asia-Pacific and Latin America. Producers with dry-quenching, coal-washing, and traceability capabilities are positioned for the former, while vertically integrated Indonesian and Chinese clusters thrive in the latter by leveraging coal sourcing, captive logistics, and flexible product mixes.

Foundry Coke Industry Leaders

Shanxi Coking Coal Group

ArcelorMittal

Drummond Company, Inc.

NIPPON COKE & ENGINEERING. CO., LTD.

China Risun Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SunCoke Energy, Inc. secured a one-year extension on its coke-making agreement with United States Steel. This extension ensures that SunCoke will keep supplying metallurgical coke to United States Steel, sourced from its Granite City cokemaking facility.

- December 2025: ArcelorMittal Nippon Steel India commissioned a new coke oven battery at its Hazira plant with a designed capacity of 1.5 million tons per year. This addition enhances self-sufficiency in raw materials for blast furnace operations and reduces reliance on merchant metallurgical coke imports.

Global Foundry Coke Market Report Scope

Foundry coke is a high-carbon, dense, and strong fuel produced by carbonizing selected coal at high temperatures, primarily used to melt iron in foundry cupolas.

The foundry coke market is segmented by ash content, carbon type, end-user foundry type, and geography. By ash content, the market is segmented into 8%-10% ash content, less than 8% ash content, and More than 10% ash content. By carbon type, the market is segmented into metallurgical coke, petroleum coke, pitch coke, anthracite coke, and others. By end-user foundry type, the market is segmented into automotive foundries, fabricated castings (pumps, valves, and motors), machine and tool manufacturing, aerospace and heavy equipment, and other industrial foundries. The report also covers the market size and forecasts for foundry coke in 15 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| 8%-10% Ash Content |

| Less than 8% Ash Content |

| More than 10% Ash Content |

| Metallurgical Coke |

| Petroleum Coke |

| Pitch Coke |

| Anthracite Coke |

| Others |

| Automotive Foundries |

| Fabricated Castings (Pumps, Valves, and Motors) |

| Machine and Tool Manufacturing |

| Aerospace and Heavy Equipment |

| Other Industrial Foundries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Ash Content | 8%-10% Ash Content | |

| Less than 8% Ash Content | ||

| More than 10% Ash Content | ||

| By Carbon Type | Metallurgical Coke | |

| Petroleum Coke | ||

| Pitch Coke | ||

| Anthracite Coke | ||

| Others | ||

| By End-user Foundry Type | Automotive Foundries | |

| Fabricated Castings (Pumps, Valves, and Motors) | ||

| Machine and Tool Manufacturing | ||

| Aerospace and Heavy Equipment | ||

| Other Industrial Foundries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the foundry coke market in 2026?

The foundry coke market is valued at USD 2.83 billion in 2026, up from USD 2.71 billion in 2025.

What CAGR is projected for foundry coke between 2026-2031?

The foundry coke market is projected to grow from USD 2.83 billion in 2026 to USD 3.50 billion in 2031 at a CAGR of 4.34%.

Which region buys the most foundry coke?

Asia-Pacific accounts for 57.91% of consumption and grows the fastest at 5.08% CAGR.

Why is petroleum coke gaining popularity in cupolas?

It offers lower cost and high fixed-carbon purity, driving a 4.89% CAGR despite higher sulfur that requires blending.

Page last updated on: