Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

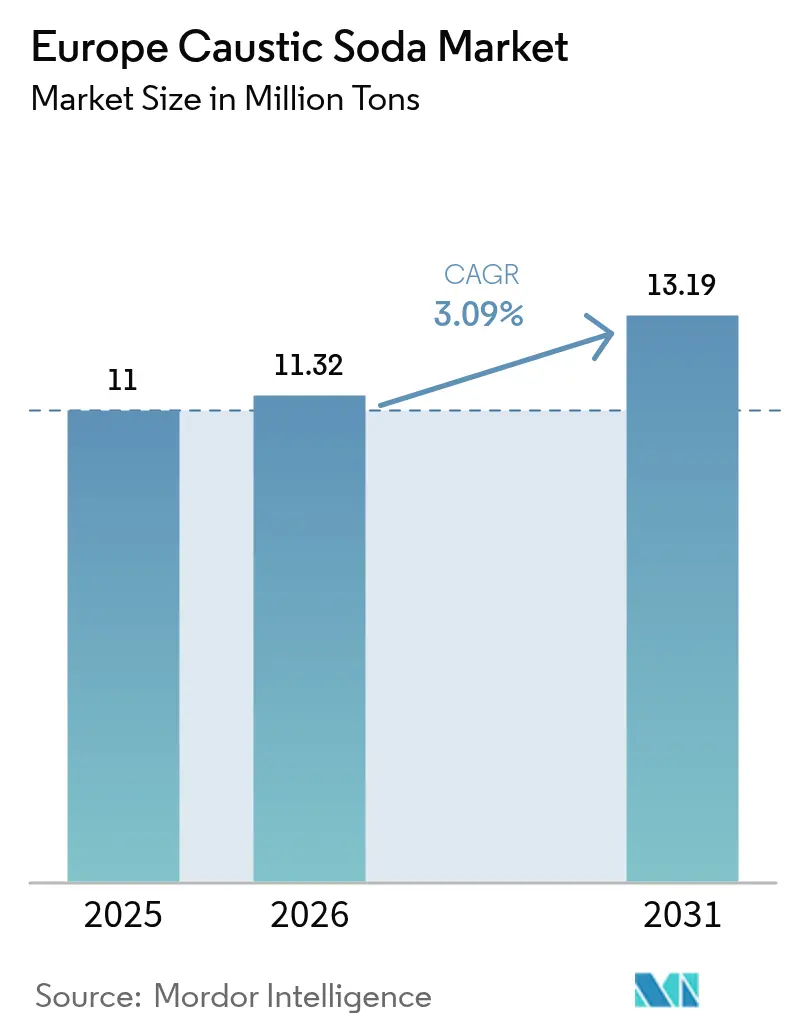

| Base Year Market Size (2025) | 11 Million tons |

| Market Volume (2026) | 11.32 Million tons |

| Market Volume (2031) | 13.19 Million tons |

| Growth Rate (2026 - 2031) | 3.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Caustic Soda Market Analysis by Mordor Intelligence

The Europe Caustic Soda Market size is expected to grow from 11 Million tons in 2025 to 11.32 Million tons in 2026 and is forecast to reach 13.19 Million tons by 2031 at 3.09% CAGR over 2026-2031. Tight electricity supplies, cost‐inflation across chlor-alkali value chains, and the need to keep chlorine-caustic balances in check after persistent polyvinyl-chloride (PVC) capacity reductions are reshaping investment priorities. Large producers are ring-fencing renewable-power contracts, smaller operators are exiting high-cost diaphragm assets, and downstream users are switching to liquid grades to streamline logistics. Regulatory tailwinds from wastewater upgrades, fiber-based packaging, and battery-grade alumina projects are anchoring structural demand, while elevated energy tariffs and stringent REACH obligations remain the principal counterweights. Together, these forces explain why the Europe caustic soda market is expanding at a steady, rather than explosive, clip.

Key Report Takeaways

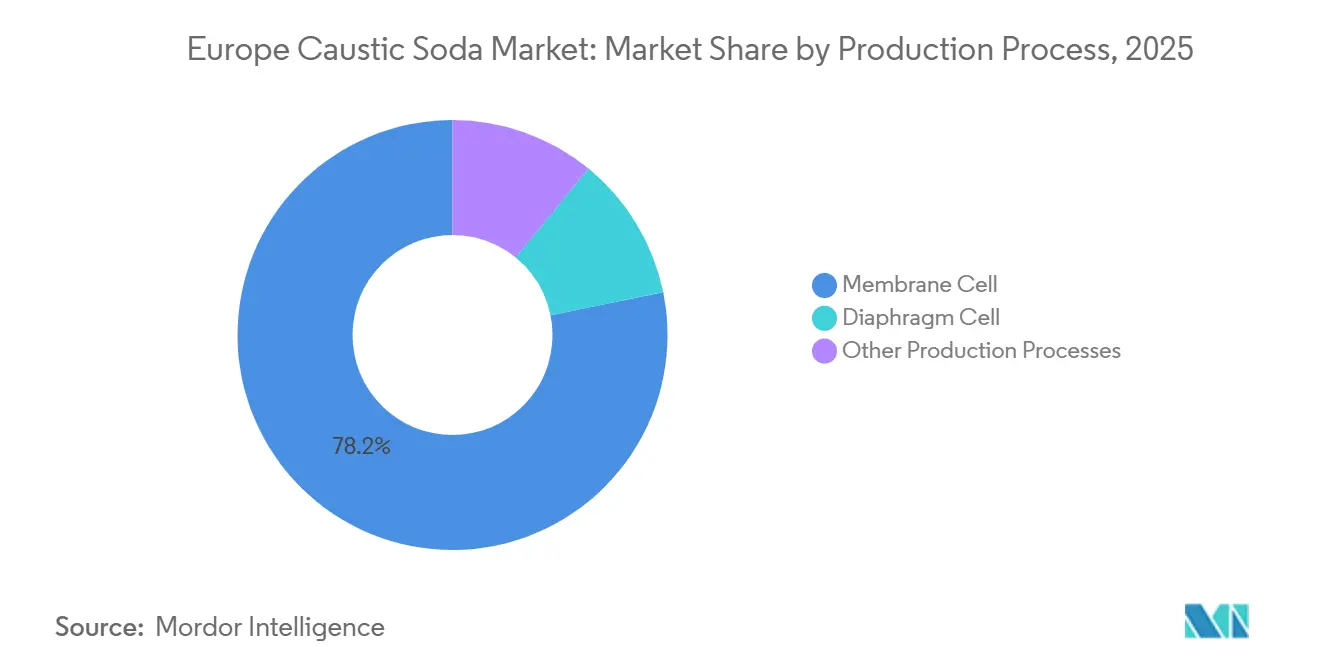

- Membrane cell technology led with 78.18% of Europe caustic soda market share in 2025 and remains the most energy-efficient route, while other production processes are forecast to grow at 3.22% CAGR through 2031.

- Liquid grades accounted for 61.22% of 2025 volumes and are on track to increase at 4.29% CAGR to 2031, outpacing solid forms thanks to lower freight outlays and rapid plant-wide dosing adoption.

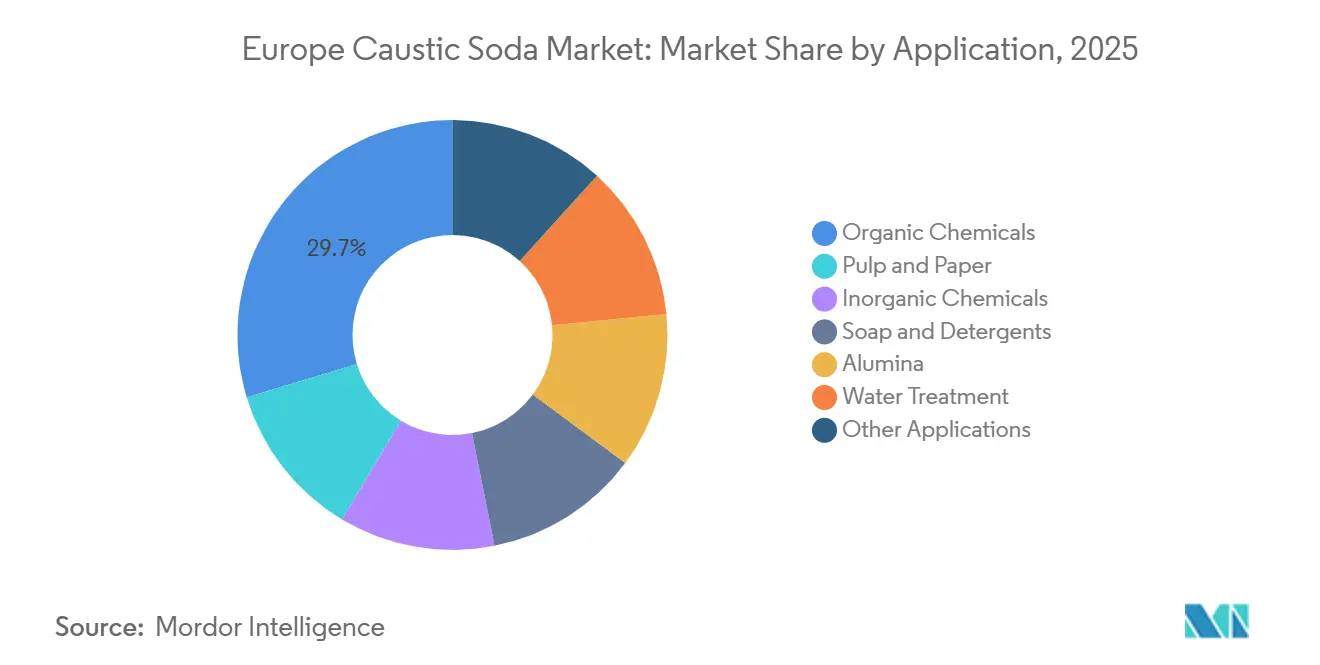

- Organic chemicals captured 29.69% of demand in 2025; alumina refining is set to record the fastest 3.47% CAGR as battery-grade projects restart idled Iberian refineries.

- Rest of Europe commanded 38.98% volume share in 2025, whereas Spain is expected to log a 4.77% CAGR, buoyed by Ercros’ capacity additions and municipal wastewater spending.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Caustic Soda Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand from Water Treatment Application | +0.6% | Germany, France, Italy, Spain, Poland | Medium term (2-4 years) |

| Rising Alumina Demand from EV-Battery Supply Chain | +0.5% | Spain, Italy, Germany | Long term (≥4 years) |

| Growth of Fiber-Based Packaging | +0.4% | Nordic Region, Germany, France | Medium term (2-4 years) |

| Expansion of Soap and Detergent Manufacturing Hubs | +0.3% | Germany, France, Netherlands | Short term (≤2 years) |

| Growing Requirement for Chemical Synthesis | +0.5% | Germany, Belgium, Netherlands | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increasing Demand from Water Treatment Application

Municipal and industrial wastewater plants must now satisfy the 2024/3019 revision of the Urban Wastewater Treatment Directive, widening tertiary treatment to towns above 1,000 population equivalents and calling for net-zero-energy operations by 2045[1]European Environment Agency, “Urban Wastewater Treatment Directive Factsheet 2025,” eea.europa.eu. This mandates EUR 257 billion of upgrades by 2050, lifting caustic-soda use for nutrient removal and pH control by 15-20% over the outlook period. Germany and France, together holding roughly 35% of installed treatment capacity, earmarked EUR 3.2 billion and EUR 2.1 billion, respectively, in 2025 budgets for phosphorus-cut programs. Spain and Italy are channeling cohesion funds into coastal schemes, while Poland and the Czech Republic are decentralizing small-scale units that favor bagged solid NaOH. Suppliers of liquid 50% grades are winning multi-year supply contracts as utilities automate dosing and tighten occupational-safety protocols.

Rising Alumina Demand from EV-Battery Supply Chain

Alcoa opened negotiations in 2024 to revive its 465 kiloton/year San Ciprián refinery and is exploring a partial restart of the 800 kiloton/year Portovesme asset, contingent on sub-EUR 50/MWh renewable-power agreements[2]Alcoa, “Investor Presentation Q3 2025,” alcoa.com. Both projects hinge on sodium hydroxide at 50–80 kg per ton of alumina, with battery-grade specifications lifting purity thresholds. Norway-based Norsk Hydro pledged 100% renewable inputs across European alumina and aluminum operations by 2030, establishing co-location prospects for membrane-cell plants near wind and solar clusters. Sodium-ion cathode chemistries referenced in the IEA Critical Minerals Outlook further expand long-term caustic requirements.

Growth of Fiber-Based Packaging

The Packaging and Packaging Waste Regulation (2025/40), together with the Single-Use Plastics Directive, encourages kraft pulp mills to raise the output of recyclable board and molded-fiber products. Mills across Finland, Sweden, Germany, and France consumed 40–80 kg NaOH per ton of pulp in 2025, and leading players UPM, Stora Enso, and Smurfit Kappa posted 8–12% year-on-year pulp gains over 2024–2025. Finland injected EUR 120 million into bio-packaging research and development grants, supporting dissolving-grade pulp lines that run exclusively on liquid caustic soda for continuous digesters. Mandatory recycled-content rules under the EU Ecodesign framework make paper substrates more attractive than virgin plastics, firming long-range demand visibility.

Expansion of Soap and Detergent Manufacturing Hubs

Unilever, Henkel, and Procter & Gamble are consolidating Western and Central European production into fewer mega-sites. Henkel invested EUR 200 million at Düsseldorf in 2025 and will add 25,000 tons/year NaOH demand once the new liquid-detergent lines reach steady state by 2027. P&G’s EUR 150 million compaction tower in Amiens pushes powder-detergent output up 18%, translating into higher caustic-soda throughput. Formulation rules restricting phosphates stimulate greater use of soda ash and silicates, both upstream NaOH derivatives, and Unilever has publicly committed to sourcing only renewable-electricity-derived caustic soda by 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High European Energy Costs | −0.8% | Germany, Italy, the Netherlands | Short term (≤2 years) |

| REACH and Occupational-Safety Compliance | −0.2% | EU-wide | Medium term (2-4 years) |

| Chlorine-Balance-Driven Rate Cuts | −0.5% | Germany, France, Netherlands | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High European Energy Costs

Electricity makes up more than half of total chlor-alkali cash costs in Europe. Despite the retreat from 2023 peaks, 2024 industrial tariffs averaged 197 EUR/MWh, still 85% over the 2020 base. France, shielded by ARENH, pays 32–46 EUR/MWh, but Dutch and German producers contend with triple-digit quotes. Natural-gas parity against Henry Hub stays adverse. Consequently, Ercros saw average selling prices plunge 41% year-on-year, and margins compressed to 6.5% in H1 2024. Covestro’s 1.2 GW renewable-power deal with RWE, effective 2026, aims to cap delivered electricity below 60 EUR/MWh for a decade.

REACH and Occupational-Safety Compliance

Mandatory membrane conversion for legacy diaphragm units by 2028 under the sector BAT reference note intensifies capex. Czech producer Spolchemie disclosed EUR 8 million in REACH fees and monitoring upgrades in 2024,12% of revenue, forcing state-backed guarantees. Closed-loop transfer systems are now compulsory for NaOH above 25 wt%, adding EUR 15–25 million per site.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process: Membrane Cells Sustain Dominance with Energy Savings

Membrane technology held 78.18% of 2025 volume, while other production processes segment is growing at a faster CAGR of 3.22%. The Europe caustic soda market size for membrane output is poised to benefit as every diaphragm retrofit delivers 20-30% electricity savings. Emerging routes such as oxygen-depolarized cathode cells could cut power draw under 2,000 kWh/t, and Horizon Europe earmarked EUR 45 million to pilot this technology.

Legacy diaphragm share, still near 10–12% in Poland, the Czech Republic, and Romania, will narrow as 2028 conversion deadlines approach. Producers that delay upgrades risk REACH penalties and customer flight toward low-carbon NaOH. Mercury cells have already vanished after the Minamata Convention. The Europe caustic soda market thus rotates firmly around membrane capacity, and any new build is expected to deploy next-generation cell rooms compatible with green hydrogen valorization.

By Form: Liquid Grades Accelerate on Freight and Automation Economics

Liquid NaOH represented 61.22% of shipments in 2025 and is forecast to grow 4.29% to 2031. End-users prefer the dilution-free form because it slashes handling cost by 15–20% and integrates seamlessly with automated dosing systems in pulp digesters and municipal clarifiers. A single 25-ton road tanker delivers 12.5 ton active NaOH, often within a 500 km radius, making it attractive against flakes, which require capital-intensive dissolution tanks. Therefore, the Europe caustic soda market is tilting ever more liquid, and transport fleets equipped with stainless-steel iso-containers are experiencing high asset utilization.

Solid forms, however, defend niches in pharma, food-processing, and rural water works that buy 25 kg bags for dosing precision. Textile mercerization in Turkey and Central Europe also values 98 wt% purity. Consequently, although flakes face slower growth, they stabilize margin spreads for sellers that can swing between packaging formats in response to seasonality.

By Application: Organic Chemicals Lead, Alumina Sets the Pace

Organic chemicals drew 29.69% of 2025 volume, anchored in epoxies, polycarbonates, and high-purity pharma intermediates. Domestic resin makers shield themselves via antidumping walls, but they still chase cost relief through captive NaOH pipelines, tying the Europe caustic soda market ever closer to downstream chemical synthesis clusters along the Rhine-Scheldt corridor.

Alumina refining clocks the fastest 3.47% CAGR to 2031 as Spain and Italy progress toward refinery restarts bound for battery-grade supply chains. Each ton of Bayer-route alumina absorbs up to 80 kg NaOH, so San Ciprián’s reactivation alone could consume an extra 30–35 kiloton yearly. Pulp and paper sits at a robust but lower trajectory, buoyed by kraft-linerboard orders from e-commerce packaging converts.

Geography Analysis

Rest of Europe covered 38.98% of 2025 demand as Poland, the Netherlands, and Nordic pulp territory preserved healthy procurement programs. PCC SE’s Brzeg Dolny hub moves liquid shipments across Central Europe via rail, while Nobian’s Delfzijl and Hengelo units benefit from maritime access to North-Sea customers. Nordic mills import sizable NaOH volumes to Kymi, Kaukas, and Skutskär, leveraging steady liquefied-cargo corridors from Baltic producers.

Spain is the volume growth outlier with a 4.77% CAGR projection. Ercros lifted first-half 2024 output to 207 kiloton and has lined up membrane upgrades at Vila-seca and Tarragona. Coupled with EUR 1.8 billion of wastewater capex in 2026-2028, Spanish utilities alone could lift NaOH pull by high-single-digit percentages. The logistics footprint is geared for truck distribution south of the Pyrenees, aided by port links in Tarragona and Bilbao.

Germany remains the single-largest consumer, backed by Covestro’s 900 kiloton nameplate capacity and clustered organic-chemical plants. Starting in 2026, the RWE-linked 1.2 GW renewable block contract stabilizes cost curves, enabling Brunsbüttel and Krefeld-Uerdingen to market “green” NaOH at sub-0.5 ton CO2/ton of product. France’s Berre and Belgium’s Jemeppe assets exploit ARENH’s power cap, keeping unit cash costs competitive. The United Kingdom’s Runcorn struggles with volatile post-Brexit energy tariffs near 180–200 EUR/MWh, and Russia’s flows have rerouted eastward after 2022 sanctions, leaving the continental Europe caustic soda market more inward-looking than at any time in the past decade.

Competitive Landscape

The Europe caustic soda market is moderately consolidated. INEOS debuted ISCC PLUS-certified NaOH with a 70% carbon-cut in 2024 and closed Rheingarten in 2025 when chlorine economics went negative. Dow will shutter Stade by 2027, freeing capital for performance-materials lines.

Covestro’s decade-long power deal with RWE underwrites Scope 2 below 0.5 ton CO2 per ton, a level customers in pharmaceuticals and food now stipulate in purchasing frameworks. Olin leverages internal epoxide units to absorb chlorine co-production, hedging margin swings across the integrated chain. Nobian re-branded from AkzoNobel Specialties, refocusing on Dutch-based captive chlorine loops feeding water-treatment hypochlorite.

Second-tier producers Ercros, Spolchemie, Vynova, PCC SE, and Kem One collectively split most of the remaining 40%. Spolchemie’s 2024 bailout attests to the burden of retrofit and REACH overheads at sub-200 kiloton scale.

Europe Caustic Soda Industry Leaders

INEOS

Nobian

Vynova Group

Kem One

Ercros

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Henkel confirmed a EUR 200 million upgrade at Düsseldorf, adding 30% liquid-detergent capacity with an incremental 25 kilotons/year caustic-soda demand from 2027.

- August 2024: INEOS launched an ISCC PLUS-certified ultra-low carbon NaOH line, claiming 70% lower life-cycle emissions than a standard membrane product.

Europe Caustic Soda Market Report Scope

Caustic soda (sodium hydroxide (NaOH)) is an essential ingredient in manufacturing soaps, cleaners, and detergents. Sodium hydroxide is widely used due to its ability to dissolve oils, grease, fats, and protein-based deposits.

The Europe caustic soda market is segmented by production process, form, application, and geography. By production process, the market is segmented into membrane cell, diaphragm cell, and other production processes. By form, the market is segmented into solid and liquid. By application, the market is segmented into pulp and paper, organic chemicals, inorganic chemicals, soap and detergents, alumina, water treatment, and other applications. The report also covers the market size and forecasts for 6 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

By Production Process

| Membrane Cell |

| Diaphragm Cell |

| Other Production Processes (Mercury Cell (legacy), Emerging Electro-electrodialysis and Direct Electro-synthesis) |

By Form

| Solid |

| Liquid |

By Application

| Pulp and Paper |

| Organic Chemicals |

| Inorganic Chemicals |

| Soap and Detergents |

| Alumina |

| Water Treatment |

| Other Applications (Food and Feed Processing, etc.) |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Production Process | Membrane Cell |

| Diaphragm Cell | |

| Other Production Processes (Mercury Cell (legacy), Emerging Electro-electrodialysis and Direct Electro-synthesis) | |

| By Form | Solid |

| Liquid | |

| By Application | Pulp and Paper |

| Organic Chemicals | |

| Inorganic Chemicals | |

| Soap and Detergents | |

| Alumina | |

| Water Treatment | |

| Other Applications (Food and Feed Processing, etc.) | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large will European caustic-soda demand be by 2031?

Volume is forecast to reach 13.19 million tons by 2031, reflecting a 3.09% CAGR from 2026 levels.

Which production process will dominate supply?

Membrane-cell technology remains dominant, providing 78.18% of 2025 output and offering 20–30% power savings over diaphragm units.

Why is Spain the fastest-growing consumer?

Spain benefits from Ercros expansions and the potential restart of Alcoa’s San Ciprián alumina refinery, pushing caustic-soda volumes at a 4.77% CAGR.

What role does wastewater regulation play in demand?

The revised Urban Wastewater Treatment Directive mandates EUR 257 billion of upgrades, lifting sodium-hydroxide use for pH and nutrient control by 15–20%.

How are producers tackling high electricity costs?

Majors such as Covestro and INEOS are signing long-term renewable-power deals that fix delivered prices below 60 EUR/MWh and cut Scope 2 emissions below 0.5 ton CO2/ton.

Page last updated on: