Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

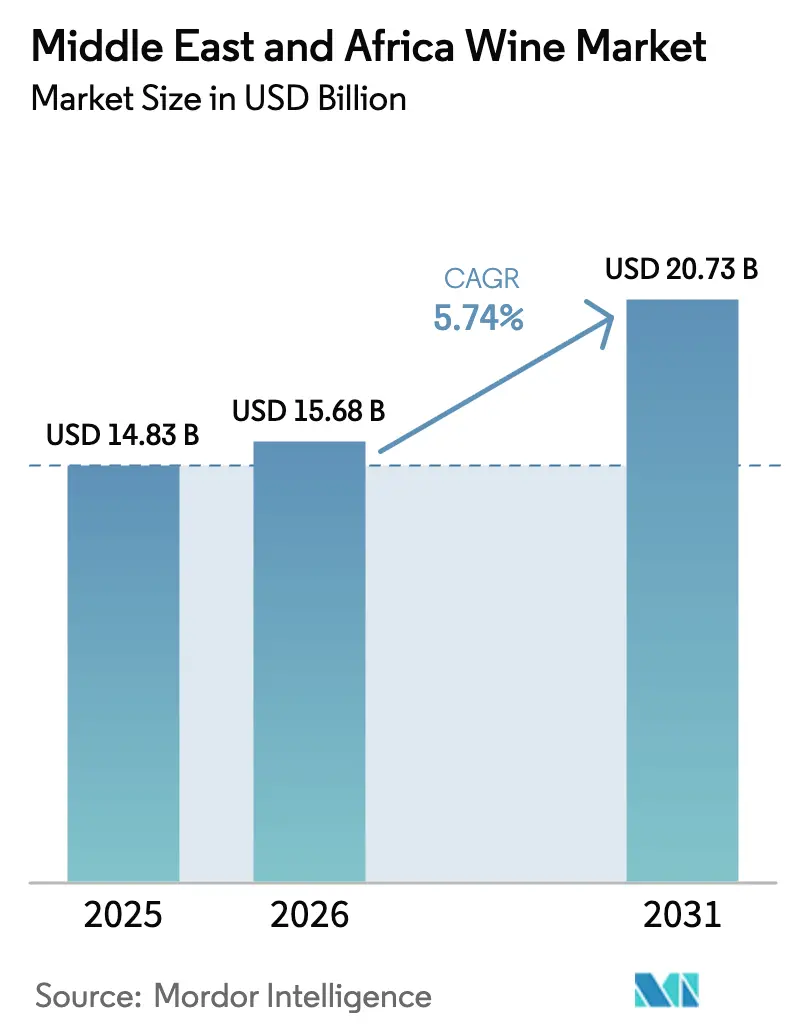

| Base Year Market Size (2025) | USD 14.83 Billion |

| Market Size (2026) | USD 15.68 Billion |

| Market Size (2031) | USD 20.73 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Wine Market Analysis by Mordor Intelligence

The Middle East and Africa wine market size was valued at USD 14.83 billion in 2025 and estimated to grow from USD 15.68 billion in 2026 to reach USD 20.73 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031). This upward trajectory is buoyed by regulatory shifts in the Gulf, a surge in tourism investments, and an uptick in disposable incomes, all steering consumers towards premium labels. Saudi Arabia's 2026 move to permit controlled alcohol sales in tourism zones broadens the market's reach. Concurrently, infrastructure enhancements in Egypt, Morocco, and the UAE are streamlining the supply chain. Innovations in climate-resilient varietals and non-alcoholic offerings not only meet sustainability goals but also respect regional religious sentiments. The formation of Vinarchy underscores a trend towards consolidation, enhancing market reach and brand investment returns. While counterfeit risks and inconsistent tax regimes pose challenges, they also drive the adoption of blockchain traceability and heightened import inspection measures.

Key Report Takeaways

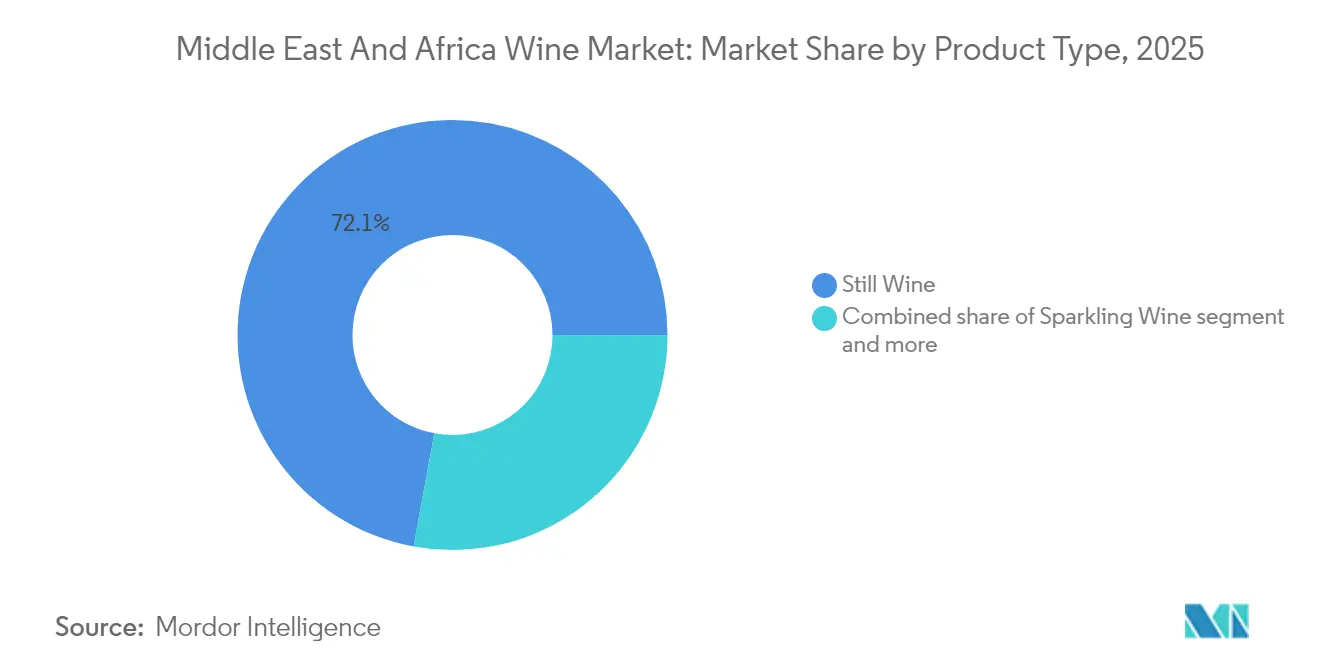

- By product type, still wine led with a 72.10% share of the Middle East and Africa wine market in 2025, whereas sparkling wine is projected to advance at a 7.14% CAGR through 2031.

- By color, red wine accounted for 57.88% share of the Middle East and Africa wine market size in 2025, whereas rosé wine is projected to expand at a 6.72% CAGR to 2031.

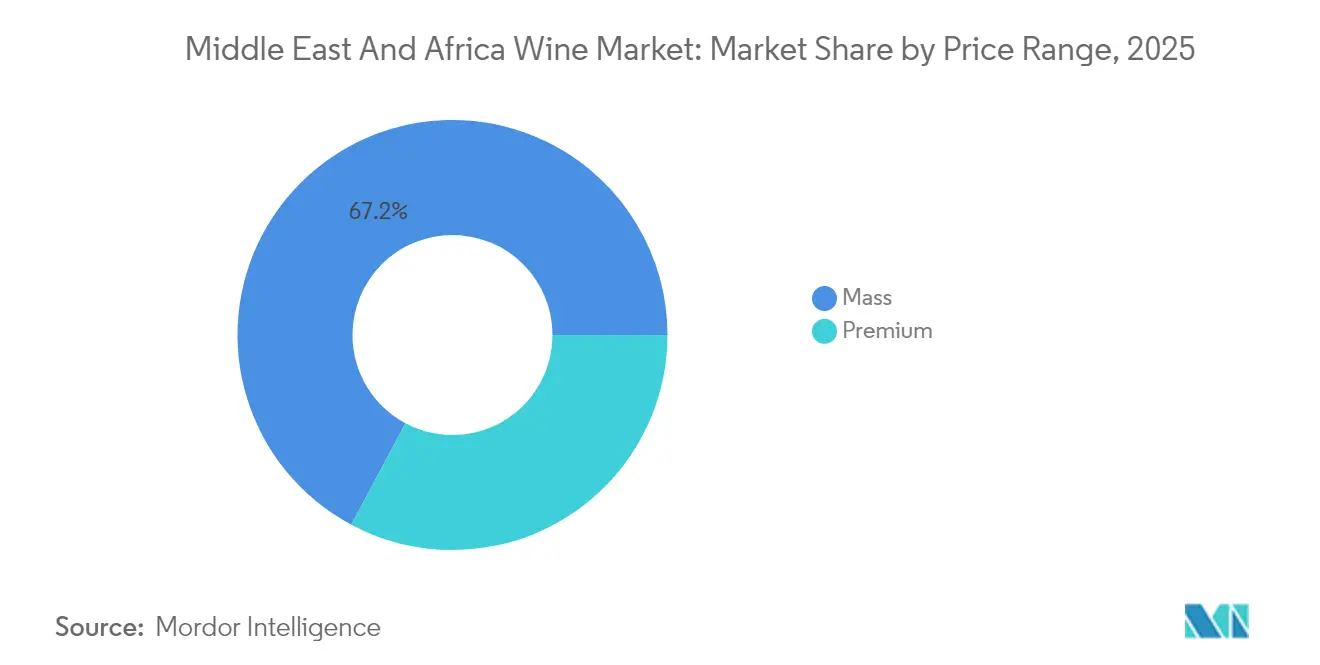

- By price range, the premium tier accounted for 32.80% share of the Middle East and Africa wine market size in 2025 and is forecast to expand at a 7.39% CAGR to 2031.

- By end user, men retained 60.82% participation in 2025, while women are set to deliver a 6.02% CAGR through 2031 as social norms shift and purchasing power rises.

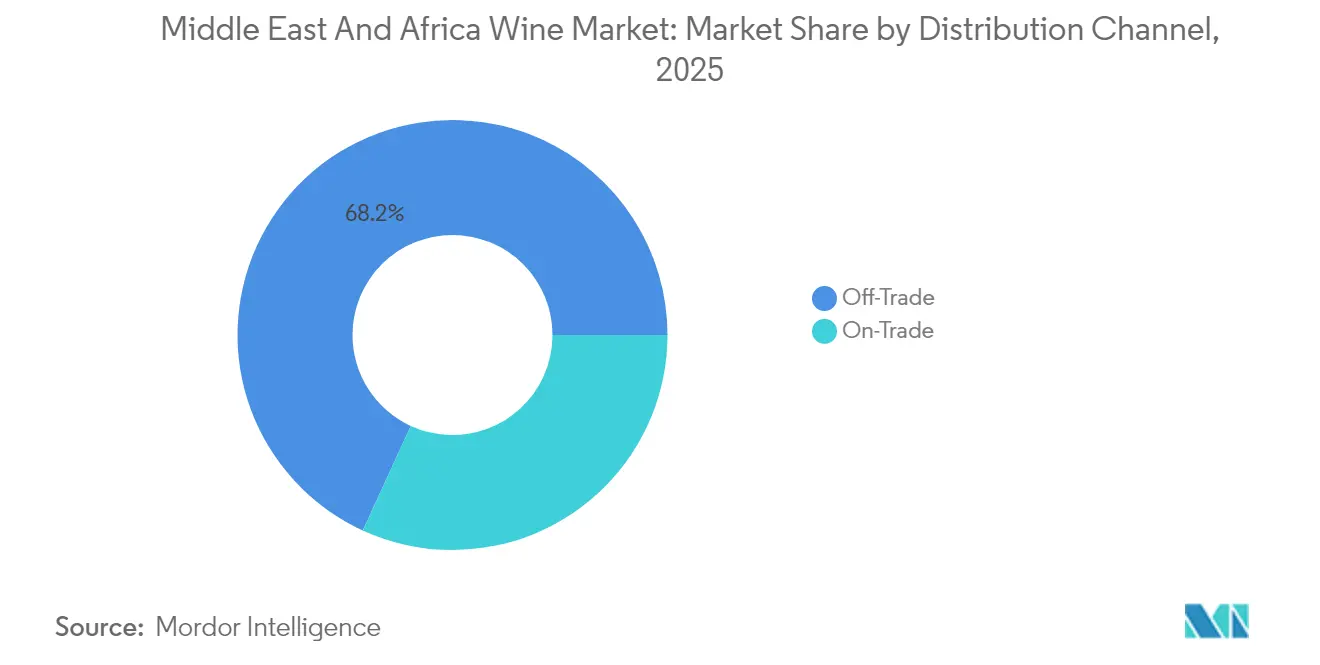

- By distribution channel, the off-trade captured 68.15% of the Middle East and Africa wine market size in 2025, as the on-trade accelerated at a 6.52% CAGR, driven by new hospitality projects.

- By geography, South Africa commanded 38.61% revenue share of the Middle East and Africa wine market size in 2025, while the United Arab Emirates is on track for the fastest 7.69% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Wine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising premiumization and gifting culture | +1.2% | UAE, Saudi Arabia, South Africa, Egypt | Medium term (2-4 years) |

| Hospitality-tourism boom | +0.9% | UAE, Saudi Arabia, Turkey, Egypt, Morocco | Short term (≤ 2 years) |

| Exotic flavor exploration and new taste preferences | +0.7% | Urban centers across region | Medium term (2-4 years) |

| Rising disposable income | +0.8% | Nigeria, Egypt, South Africa, UAE | Long term (≥ 4 years) |

| Technological advances in viticulture and winemaking | +0.5% | South Africa, Morocco, Turkey | Long term (≥ 4 years) |

| Halal-certified de-alcoholised wines | +0.4% | Saudi Arabia, UAE, Egypt, Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising premiumization and gifting culture

As urban affluence rises, Middle Eastern and African markets witness a surge in premium wine consumption, driven by sophisticated drinking occasions and corporate gifting. The UAE, through ADGM, showcases its regulatory flexibility by granting alcohol service permits, underscoring its commitment to premium hospitality. Meanwhile, buoyed by record agricultural exports hitting USD 13.7 billion in 2024, South Africa's wine industry is now eyeing higher-value exports, as noted by Wandile Sihlobo. In West Africa, as local spirits are rebranded as luxury items, there's a noticeable spillover demand for imported premium wines. This cultural evolution, positioning wine as a status symbol and preferred gift, especially favors the sparkling wine segment, known for its higher margins and celebratory appeal. With enhancing port infrastructure and streamlined customs procedures, premium wine selections are becoming staples in corporate entertainment and diplomatic events across these regions.

Hospitality-tourism boom

As Egypt aims for a USD 30 billion tourism revenue by 2025 and 30 million visitors by 2032, the country will need an additional 200,000 hotel rooms, as highlighted by the New Zealand Ministry of Foreign Affairs and Trade[1]Source: New Zealand Ministry of Foreign Affairs and Trade, “Egypt Economic Report 2025,” mfat.govt.nz. Saudi Arabia's Vision 2030, featuring initiatives like the Red Sea Global megaprojects and Qiddiya entertainment hubs, sees alcohol licensing in select tourism zones as a strategy for economic diversification. The UAE's well-established hospitality sector is broadening its premium dining offerings. Meanwhile, Turkey's strong sales of Chivas and other premium brands indicate a shift towards more sophisticated consumption patterns, according to Pernod Ricard. Cultural tourism is on the rise in Morocco and Egypt, spurring a demand for wine pairings with local dishes. As hotels expand their capacities, there's a growing need for refined beverage programs, leading to increased bulk wine imports for on-premise use and presenting opportunities for regional distributors.

Exotic flavor exploration and new taste preferences

As consumer tastes shift, there's a growing embrace of indigenous varietals and innovative production methods that resonate with regional terroirs and cultural nuances. In Rwanda, the development of locally-sourced banana wine yeast cultures showcases a leap in technological innovation, tapping into alternative fermentation substrates. Meanwhile, Malawi's foray into banana wine production not only highlights a response to climate challenges but also serves as a means for income diversification. Across Egypt, Turkey, and South Africa, pomegranate wine is making waves. Leveraging established fruit production infrastructures, these regions are crafting antioxidant-rich pomegranate wines, boasting bioactive compounds up to tenfold higher than their traditional grape counterparts. South African wine regions are not just resting on their laurels; they're experimenting with climate-adapted varieties like Assyrtiko and Vermentino. Coupled with precision viticulture technologies, they're honing terroir-specific flavors, as noted by the London Wine Competition. These strides in innovation not only bolster climate resilience but also cater to a burgeoning consumer appetite for distinct flavor profiles, setting regional offerings apart from global contenders.

Rising disposable income

Key African markets are witnessing economic growth, bolstering wine purchasing power. Projections from the USDA indicate that Sub-Saharan Africa is set to achieve an average GDP growth of 3.8% through 2033, while North Africa is on track with a steady 3.7% growth rate[2]Source: USDA, “USDA Agricultural Projections to 2033,” usda.gov. In Nigeria, an expanding middle class is fueling a surge in wine import demand, even in the face of regulatory hurdles. Meanwhile, Egypt, buoyed by currency stabilization and backing from the IMF, is enhancing its capacity to import premium beverages. Côte d'Ivoire has emerged as the largest wine importer in Sub-Saharan Africa, bringing in wines worth USD 64.1 million in 2023, outpacing South Africa's imports valued at USD 54.3 million. This shift underscores the nation's robust economic growth and urbanization trends, as highlighted by the USDA Foreign Agricultural Service. Urban dwellers are increasingly dedicating discretionary funds to lifestyle products, with wine taking center stage for both home enjoyment and social gatherings. As incomes rise, there's a noticeable shift from informal alcohol consumption to branded, regulated wine products. This transition is particularly advantageous for international imports and the burgeoning premium segment of domestic production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent counterfeit risk undermining consumer trust | -0.8% | Nigeria, Egypt, South Africa | Short term (≤ 2 years) |

| Strict alcohol regulation and religious norms | -1.1% | Saudi Arabia, Egypt, Morocco | Long term (≥ 4 years) |

| Youth shift toward flavoured RTDs and spirits | -0.6% | Global, concentrated in urban areas | Medium term (2-4 years) |

| High import tariffs and excise taxes | -0.9% | Nigeria, Egypt, Morocco, Turkey | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent counterfeit risk undermining consumer trust

Illicit alcohol trade accounts for 25-40% of global consumption, leading to annual fiscal losses of USD 8.9 billion. The World Customs Organization highlighted a 30% surge in alcohol trafficking cases in 2022, with a primary focus on wine and grape-distilled products[3]Source: World Trade Organization, “Illicit Trade in Food and Food Fraud,” wto.org. In South Africa, a fragmented food control system has paved the way for counterfeit wine circulation. This has resulted in documented deaths from methanol-adulterated alcohol in 2022 and seizures valued at R24 million in Cape Town alone, according to BMC Public Health. The region's limited laboratory capacity hampers authentication efforts. Furthermore, modest statutory fines (R400 for first offences under South Africa's FCD Act) prove ineffective in deterring large-scale fraud operations. The rise of e-commerce has introduced new avenues for counterfeit distribution, especially impacting premium wine segments where brand authenticity significantly influences pricing. While regional coordination via INTERPOL's OPSON operations and blockchain traceability initiatives present potential solutions, their successful implementation demands considerable investment in enforcement infrastructure and enhanced cross-border collaboration.]

Strict alcohol regulation and religious norms

Across Muslim-majority nations, market penetration faces hurdles due to religious and cultural constraints. Notably, Saudi Arabia, long known for its stringent 73-year alcohol ban, has recently begun to ease restrictions, but only for select tourism venues. In Egypt, the National Food Safety Authority enforces rigorous registration processes and mandates halal certification. Meanwhile, Morocco's licensing frameworks are skewed to favor domestic production, imposing restrictions on imports. In Nigeria, the NAFDAC's registration process, which includes factory inspections and a mountain of documentation, poses significant challenges for international wine producers eyeing the market. Turkey's Ministry of Agriculture has added another layer of complexity, requiring labels to be in Turkish during production. This stipulation not only bars modifications post-import but also inflates compliance costs. Such regulatory landscapes underscore the profound cultural sensitivities surrounding alcohol consumption in these nations. As a result, any market entry strategy must tread carefully, honoring local customs while pinpointing acceptable consumption occasions and target consumer segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Still Wine Dominance Amid Sparkling Acceleration

In 2025, still wine holds a commanding 72.10% share of the market, underscoring the region's entrenched consumption habits and well-established distribution channels. Sparkling wine, however, is making waves as the fastest-growing segment, boasting a 7.14% CAGR projected through 2031. This surge is largely attributed to its rising popularity in celebrations and a trend towards premium offerings in the hospitality sector. While fortified wine enjoys consistent demand in traditional markets, the "Others" category spanning ice wines, aromatized varieties, and low/no-alcohol options is gaining momentum. This shift is largely driven by health-conscious consumers exploring alternatives. Notably, the halal-certified de-alcoholized wine segment is carving out a niche in Muslim-majority markets. Here, evolving regulatory frameworks are becoming more accommodating, allowing these non-alcoholic alternatives to retain their cultural and ceremonial significance.

Producers in South Africa are adapting to climate change, experimenting with late-harvest and fortified styles to better endure temperature swings. Meanwhile, technological strides in dealcoholization are paving the way for premium non-alcoholic offerings, as highlighted by the Italian Journal of Food Science. Sparkling wine producers are leveraging controlled fermentation technologies to uphold quality, even in the face of challenging climatic conditions. This resilience positions the segment for continued growth, especially as regional economies flourish and celebratory occasions become more frequent.

By Colour: Red Wine Leadership Challenged by Rosé Innovation

In 2025, red wine commands a dominant 57.88% share of the market, buoyed by longstanding traditions and food pairing practices prevalent in Mediterranean and African cuisines. Rosé wine, however, is on a rapid ascent, projected to grow at a 6.72% CAGR through 2031. Its appeal resonates with younger consumers and is particularly favored during warm-climate occasions, a hallmark of the region. Meanwhile, white wine carves out a notable presence in coastal markets and premium segments, reaping benefits from a surge in tourism and its affinity for seafood pairings. The segmentation by color not only mirrors cultural inclinations but also climatic factors, with rosé's upward trajectory echoing a global shift towards lighter, more refreshing wine styles.

South Africa's 2025 vintage stands out for its exceptional quality across all color categories. Favorable growing conditions have not only preserved acidity but also cultivated optimal color and flavor profiles. This is especially evident in the enhanced expressions of Pinotage and Shiraz red wines, alongside a more pronounced Chardonnay white wine. As regional producers hone in on color-specific marketing strategies, rosé is being strategically positioned for the bustling summer tourism season, while red wines are being marketed for the cozy winter months and upscale dining experiences.

By Price Range: Premium Segment Drives Value Creation

In 2025, mass market wines dominate with a 67.20% market share, underscoring the influence of price-sensitive consumers and robust off-trade distribution channels. Meanwhile, the premium wine segment is on a growth spurt, boasting a 7.39% CAGR through 2031. This surge is fueled by rising disposable incomes and a growing penchant for sophisticated consumption, especially in urban hubs and tourist hotspots. Notably, this trend of premiumization not only aligns with global wine market movements but also highlights regional economic growth and a deepening cultural appreciation for wine.

Strategies in the premium wine sector are increasingly honing in on terroir expression, sustainable production, and genuine regional characteristics. For instance, South African vintners are capitalizing on the "Wine of Origin" certification and estate-specific branding, allowing them to command premium prices. Furthermore, regional regulatory frameworks are becoming more accommodating to premium wine imports. Egypt has streamlined its customs procedures, while the UAE's well-established hospitality licensing is paving the way for these high-value products. Given the premium segment's upward trajectory, producers who prioritize quality differentiation and brand development stand to reap significant margin expansions.

By End User: Women Consumers Drive Market Evolution

In 2025, men hold a 60.82% share of the market, a reflection of the region's entrenched consumption patterns and cultural norms. Meanwhile, women are propelling a more rapid growth rate of 6.02% CAGR, a trend projected to continue through 2031. This surge is buoyed by shifting social dynamics, heightened economic engagement, and changing lifestyle choices. Such demographic transitions are reshaping product development and marketing strategies, influencing everything from packaging and flavor profiles to preferred distribution channels.

According to Diageo's Foresight Report 2025, key consumer trends spotlight conscious wellbeing and a sense of collective belonging. Notably, women are at the forefront, championing moderation and community-centric consumption. However, the gender landscape isn't uniform. In markets like the UAE and South Africa, more lenient regulations have paved the way for greater female involvement in wine consumption. In contrast, traditional markets are witnessing a more gradual shift towards social acceptance and purchasing behaviors.

By Distribution Channel: Off-Trade Dominance with On-Trade Acceleration

In 2025, off-trade channels capture a commanding 68.15% market share, led by specialty liquor stores that expertly curate and premium-position wine products. Meanwhile, on-trade channels, buoyed by an expanding hospitality sector and bolstered tourism infrastructure in key markets, are set to grow at a robust 6.52% CAGR through 2031. Specialty liquor stores leverage their product expertise, premium positioning, and adeptness at navigating regulatory landscapes. At the same time, other off-trade avenues, notably e-commerce platforms, are resonating with younger consumers.

The distribution landscape is shaped by regulatory constraints and cultural inclinations. While off-trade channels cater to private consumption, the growth of on-trade channels underscores their role in social and business entertainment. Egypt's burgeoning tourism and Saudi Arabia's proactive hospitality licensing pave the way for significant on-trade prospects. Conversely, Nigeria's regulatory landscape leans towards established distribution networks, especially those adept with NAFDAC compliance. Embracing technology, the distribution sector is turning to blockchain for traceability and digital tools for inventory management, tackling authenticity challenges and streamlining supply chain operations.

Geography Analysis

In 2025, South Africa holds a 38.61% share of the African wine market, benefiting from its strong viticulture infrastructure, export capacity, and proximity to major regional markets. Challenges such as Cape Town’s port congestion, Eskom’s load shedding, and climate change require adaptive strategies, yet the 2025 vintage delivered 1.244 million tonnes from 86,544 hectares. This supports premiumization, diversifies exports to over 120 countries, and aligns with transformation initiatives emphasizing Black ownership and sustainable production.

The United Arab Emirates is the fastest-growing market, with a projected CAGR of 7.69% through 2031, driven by tourism, a rising expatriate population, and advanced hospitality infrastructure. Dubai’s automated customs and ADGM alcohol licensing simplify the import of premium wines, while the UAE’s strategic location strengthens its role as a distribution hub for Gulf Cooperation Council markets. Saudi Arabia is poised for growth with the implementation of Vision 2030 reforms and preparations for the 2034 FIFA World Cup, where the introduction of controlled alcohol licensing in tourism venues could boost demand.

Nigeria, Egypt, Morocco, and Turkey hold notable shares but face distinct regulatory and cultural conditions. In Nigeria, NAFDAC registration and a sachet alcohol ban reflect stricter consumer protection and market formalization. Egypt’s 14% VAT and Arabic labeling requirements increase compliance costs, yet tourism and economic stabilization efforts support alcohol imports. Morocco and Turkey balance wine production with religious and cultural sensitivities, focusing on domestic production and selective imports for tourists and expatriates.

Competitive Landscape

The wine market in the Middle East and Africa is moderately fragmented, with the top five groups holding a significant share. The merger of Accolade Wines and Pernod Ricard's regional assets has birthed Vinarchy, a 32-million-case powerhouse with a focus on premium exports. This merger streamlines overlapping distributors and injects capital for vineyard enhancements in South Africa and Spain. Constellation Brands has divested its mainstream labels, choosing instead to focus on higher-margin SKUs, reflecting a regional shift towards premiumization.

Castel Group's USD 81 million acquisition of Diageo's stake in Guinness Ghana highlights a trend of consolidation in Africa, aiming to boost scale and regulatory sway. Treasury Wine Estates, initially set to divest its commercial portfolio in 2025, has reversed course, underscoring the importance of mass-market coverage for stable cash flow. Technological advancements are making waves: from blockchain authentication and AI-driven irrigation to predictive demand modeling. While smaller estates in Morocco and Turkey find their footing through eco-certifications and agro-tourism, South African cooperatives are bundling logistics to make inroads into Nigerian retail.

Strategies are increasingly shaped by the need to combat counterfeiting. Leading firms are adopting tamper-proof neck tags and collaborating with customs agencies for swift authenticity checks. Sustainability is also a major focus; producers are outlining carbon-reduction strategies to meet the expectations of importers in Europe and Asia. A shortage of talent in enology and vineyard management has led to internship exchanges between South Africa and France, elevating technical standards throughout the region.

Middle East And Africa Wine Industry Leaders

Accolade Wines

E. & J. Gallo Winery

Pernod Ricard

Castel Group

Distell Group Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Diageo completed the sale of its 80.4% shareholding in Guinness Ghana Breweries plc to Castel Group, retaining brand ownership while establishing long-term licensing agreements for continued production and distribution of Diageo brands in Ghana.

- June 2025: Constellation Brands closed its transaction with The Wine Group, divesting mainstream wine brands including Woodbridge, Meiomi, and Robert Mondavi Private Selection while retaining a premium-focused portfolio priced predominantly above USD 15.

Middle East And Africa Wine Market Report Scope

Wine is an alcoholic drink typically made from fermented grape juice. Wines are extensively used for consumption and cooking purposes since it intensifies the flavor and aroma of finished dishes. The wine market is segmented by product type, distribution channel, and country. By product type, the market is segmented into still wine, sparkling wine, dessert wine, and fortified wine. By distribution channel, the market is segmented into on-trade and off-trade. Off-trade is further segmented into supermarkets/hypermarkets, specialty stores, and other distribution channels. Based on country, the market is segmented into South Africa, the United Arab Emirates, Saudi Arabia, and the Rest of the Middle East & Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Fortified Wine |

| Still Wine |

| Sparkling Wine |

| Others Wine Types (Ice, Aromatised, Low/No-Alc) |

By Colour

| Red Wine |

| White Wine |

| Rose Wine |

By Price Range

| Mass |

| Premium |

By End User

| Men |

| Women |

By Distribution Channel

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Others Off Trade Channels |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Fortified Wine | |

| Still Wine | ||

| Sparkling Wine | ||

| Others Wine Types (Ice, Aromatised, Low/No-Alc) | ||

| By Colour | Red Wine | |

| White Wine | ||

| Rose Wine | ||

| By Price Range | Mass | |

| Premium | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Others Off Trade Channels | ||

| By Geography | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Middle East and Africa wine market?

The market is valued at USD 15.68 billion in 2026 and is forecast to hit USD 20.73 billion by 2031.

Which country leads regional sales?

South Africa leads with 38.61% share, supported by a mature viticulture base and export reach.

Which segment is growing fastest?

Sparkling wine shows the highest 7.14% CAGR through 2031, buoyed by premium tourism and gifting.

Which distribution channel holds the greatest share?

Off-trade channels, notably specialty liquor stores, account for 68.15% of 2025 value, though on-trade is trending up.

How will Saudi Arabia’s policy shift affect demand?

Controlled licenses tied to Vision 2030 and FIFA 2034 are expected to open new on-trade channels from 2026 forward.

Page last updated on: