Fluorochemical Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

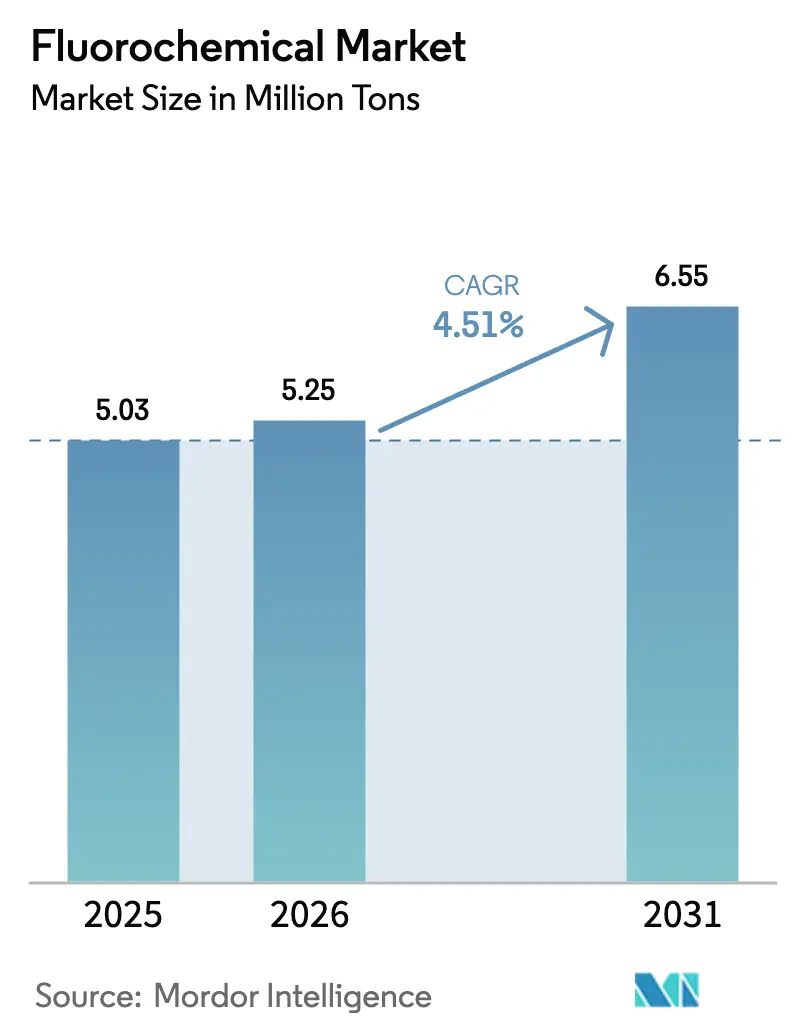

| Market Volume (2026) | 5.25 Million tons |

| Market Volume (2031) | 6.55 Million tons |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fluorochemical Market Analysis by Mordor Intelligence

The Fluorochemical Market size is expected to grow from 5.03 million tons in 2025 to 5.25 million tons in 2026 and is forecast to reach 6.55 million tons by 2031 at a 4.51% CAGR over 2026-2031. Healthy semiconductor capital expenditure, policy-driven refrigerant phase-downs, and widening medical demand keep the Fluorochemicals market on an upward trajectory despite PFAS-related headwinds. Etching-gas uptake at new fabs in Arizona, Texas, Taiwan, and South Korea provides a high-purity revenue stream that offsets shrinking legacy HFC volumes. Accelerating cold-chain deployment in India, ASEAN, and the Gulf economies sustains first-installation demand, while automotive R-1234yf adoption locks in a multiyear replacement cycle for cabin-cooling systems. Feedstock volatility in fluorspar and regulatory uncertainty around PFAS containment temper margins, yet vertical integration and recycling initiatives enable leading suppliers to defend profitability in the Fluorochemicals market.

Key Report Takeaways

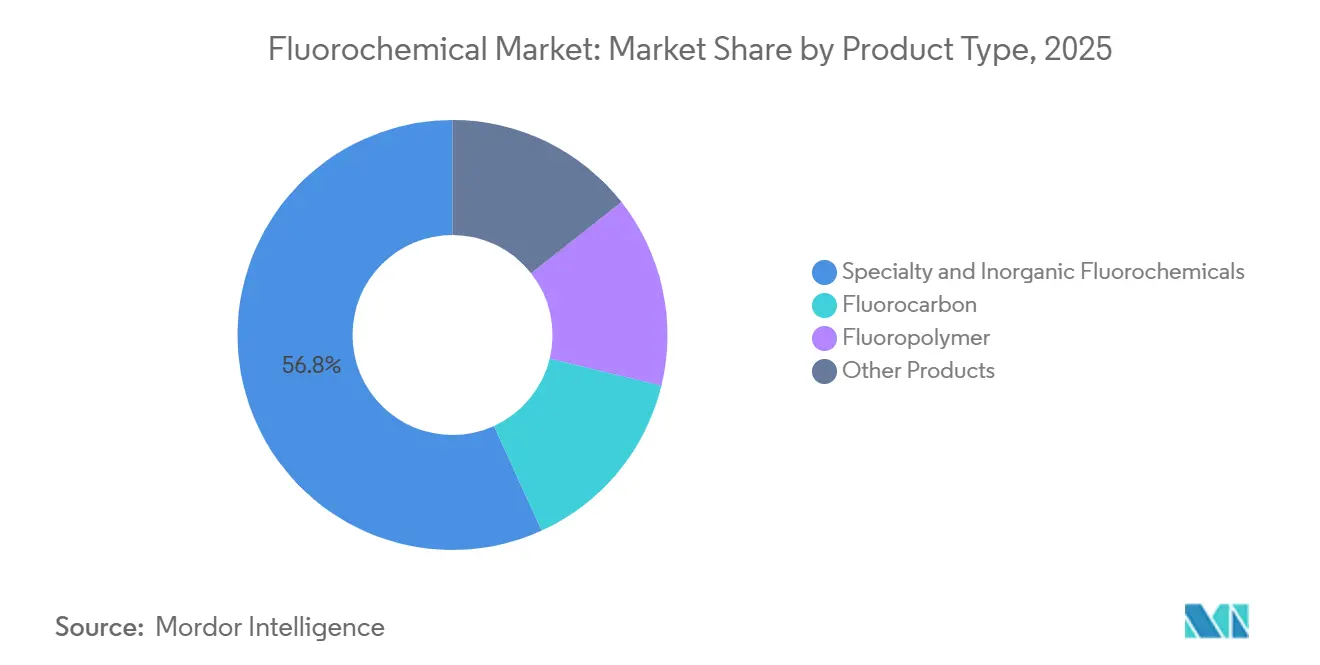

- By product type, specialty and inorganic fluorochemicals led with 56.81% of the Fluorochemicals market share in 2025; fluoropolymers are forecast to expand at an 8.65% CAGR through 2031.

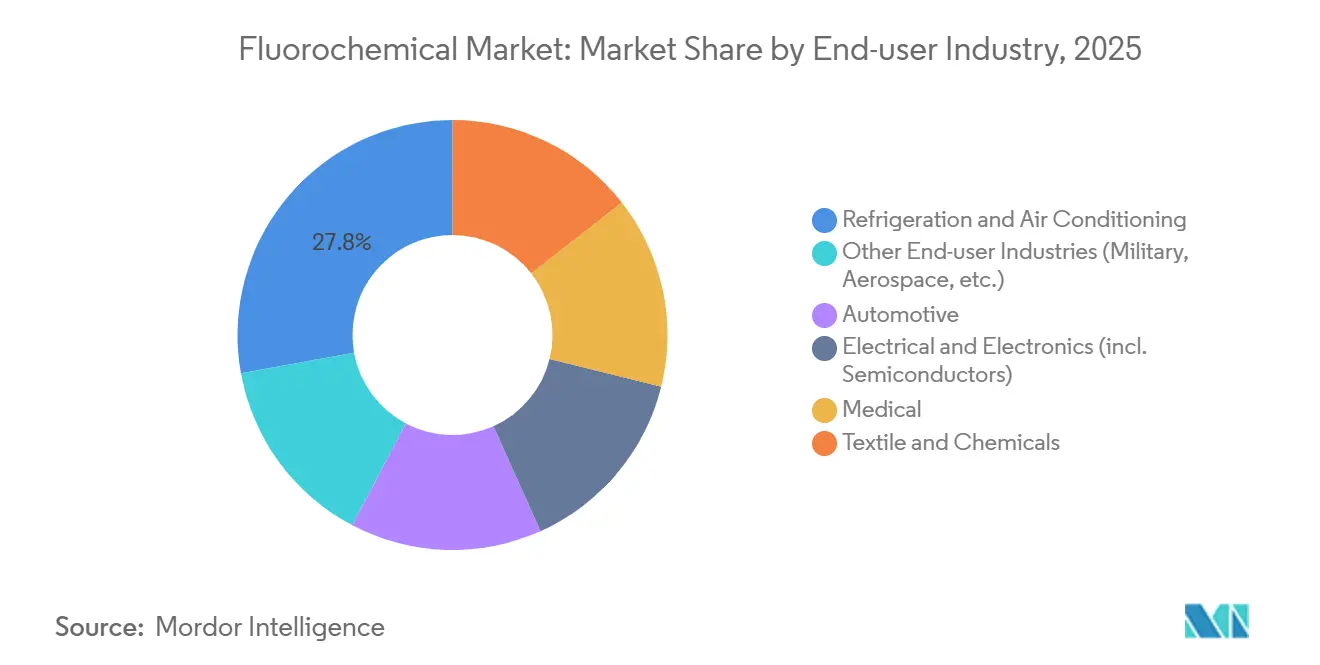

- By end-user industry, refrigeration and air conditioning held 27.84% of the Fluorochemicals market size in 2025; medical end-user industry segment is advancing at a 5.95% CAGR to 2031.

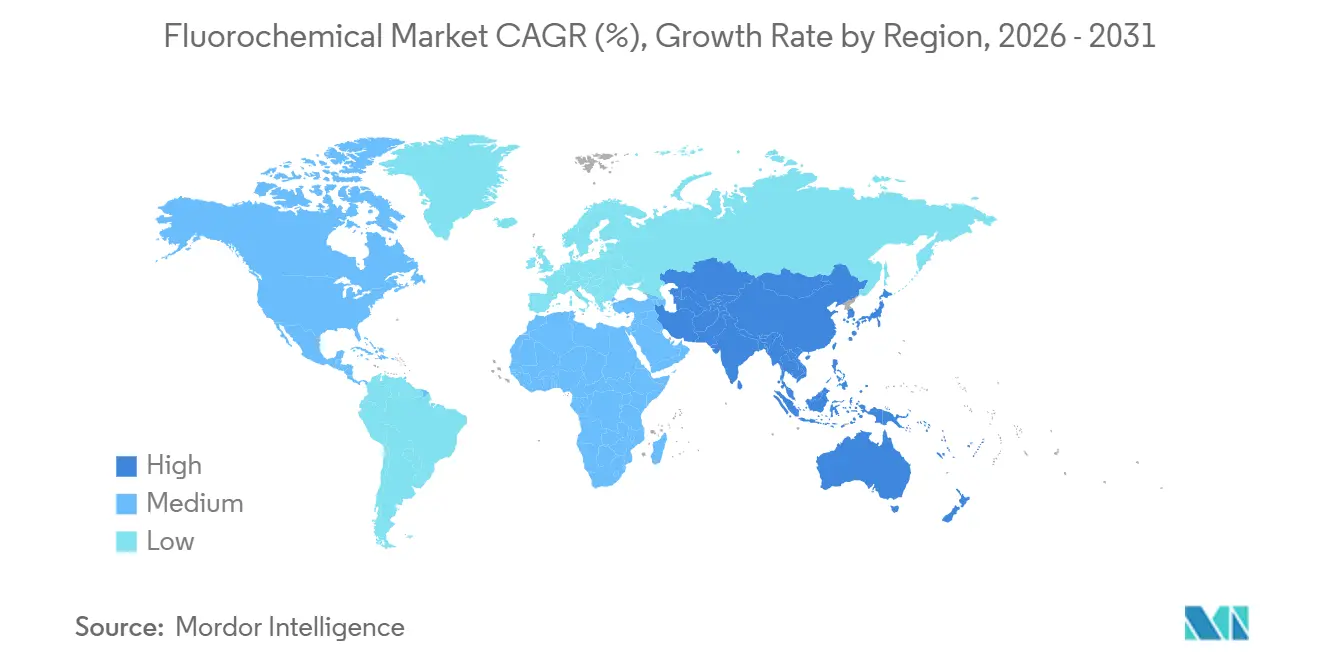

- By geography, Asia-Pacific accounted for 61.52% of the Fluorochemicals market in 2025; the same region is set to register the fastest 4.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fluorochemical Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HVAC and cold-chain build-out in emerging economies | +1.2% | Asia-Pacific (India, ASEAN), Middle East & Africa | Medium term (2-4 years) |

| Growing transition to low-GWP HFO refrigerants | +0.9% | Global, with EU and North America leading | Short term (≤ 2 years) |

| Semiconductor boom in East Asia drives high-purity demand | +0.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| EV battery chemistries adopting fluorinated binders and salts | +0.7% | Global, concentrated in China, Europe, North America | Long term (≥ 4 years) |

| Increasing demand for hydrogen turbines needing ultra-high-temperature fluoropolymer seals | +0.3% | Europe, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HVAC and Cold-Chain Build-Out in Emerging Economies

Cold-storage infrastructure spending in India is rising toward USD 47.4 billion by 2032, spurred by government programs to cut post-harvest food loss. New warehouses and supermarkets across Thailand, Vietnam, and Indonesia follow similar trajectories, albeit under looser efficiency rules, allowing medium-GWP blends to remain relevant for two to three more years. Gulf states back food-security targets with chilled warehouses that prefer factory-charged HFO systems to avoid Kigali quota penalties, compressing equipment-replacement cycles. These installations add steady volume to the Fluorochemicals market as each split air-conditioner typically contains one to two kilograms of refrigerant, while commercial walk-ins carry five to 10 kilograms. Strict urban-fire codes delay propane uptake in densely populated cities, further extending demand for fluorocarbon options.

Growing Transition to Low-GWP HFO Refrigerants

EU Regulation 2024/573 and the U.S. AIM Act together force an 85% HFC reduction before 2036, accelerating adoption of R-1234yf and R-1234ze in vehicles and chillers. Light-duty vehicles in the EU, U.S., Japan, and South Korea switched almost entirely to R-1234yf by 2025, yet the product remains priced at roughly triple that of phased-out R-134a because production is concentrated at two patent-holders. Commercial HVAC retrofits favor R-513A but often require lubricant and gasket upgrades that prolong payback periods. China’s OEMs still push R-32 for domestic sales, deferring a broad HFO transition until export compliance demands take hold late in the decade. Natural refrigerant installations, particularly CO₂ transcritical supermarkets, keep gaining share in Europe, but higher energy costs and regulatory lag in North America slow similar substitution trends.

Semiconductor Boom in East Asia Drives High-Purity Demand

Ongoing fab construction by TSMC, Samsung, and Intel is set to add 1.2 million wafer starts per month by 2027, lifting demand for NF₃ and CF₄ that must meet 99.999% purity standards. China’s push for local semiconductor self-sufficiency multiplies the requirement for mature-node plasma gases despite export control hurdles. Recycling initiatives under SEMI’s 2024 F-gas program remain under-deployed, so virgin gas demand persists, directly benefiting the Fluorochemicals market[1]SEMI, “SEMI Launches F-Gas Abatement Initiative,” semi.org. Japan and South Korea tightened import permits in 2025, prompting producers such as Daikin and AGC to colocate gas output near cluster hubs, ensuring supply continuity during geopolitical disruptions.

EV Battery Chemistries Adopting Fluorinated Binders and Salts

PVDF binder and LiPF₆ salt together represent only 2%–3% of battery mass but deliver critical adhesion and ionic conductivity. China houses nearly 70% of global PVDF capacity and most LiPF₆ production, creating sourcing risk for Western cell makers. Arkema and Solvay are adding lines in Kentucky and Belgium, yet capital intensity above USD 500 million per 50 kt slows diversification. Solid-state roadmaps could reduce LiPF₆ volumes post-2030, but incumbent liquid-cell designs will dominate through the forecast period, keeping the Fluorochemicals market lifted by battery growth. FEC additive penetration further raises fluorine loading per kilowatt-hour.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global PFAS regulatory clamp-down | −0.6% | North America, Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Fluorspar feedstock supply volatility | −0.4% | Global, with import-dependent regions most exposed | Medium term (2-4 years) |

| Uptake of natural refrigerants and fluorine-free solvents | −0.3% | Europe leading, North America and Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global PFAS Regulatory Clamp-Down

In April 2024, the U.S. EPA set 4 ppt limits for PFOA and PFOS in drinking water, triggering CERCLA liability and exposing producers to remediation settlements that can exceed USD 10 billion[2]U.S. EPA, “National Primary Drinking Water Regulation for PFAS,” epa.gov. The EU’s broad PFAS restriction proposal advanced to final opinion in 2025; exemptions for chips and medical devices remain uncertain and delay investment commitments. Germany now requires proof of containment at fluorochemical sites, raising operating costs, while Japan issued monitoring guidelines that foreshadow stricter rules. Semiconductor and medical stakeholders argue that PTFE and other fluoropolymers lack substitutes, but public pressure complicates approval processes, weighing on the Fluorochemicals market.

Fluorspar Feedstock Supply Volatility

China supplies up to 65% of worldwide fluorspar, and export-quota shifts or environmental inspections in Inner Mongolia routinely spike delivered prices by 30%–40%. Mongolia and Mexico offer alternatives, yet volumes cannot fully offset a sustained Chinese cutback, and overland transport adds double-digit logistics premiums. New mines in South Africa and Kenya remain at permitting stages, while Western HF plants face siting barriers due to hazardous-substance rules. Long-term offtake agreements help integrated majors secure feedstock but reduce spot liquidity for smaller players, raising barriers to entry and injecting cost uncertainty into the Fluorochemicals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fluoropolymers Outpace Legacy Refrigerants

Fluoropolymers are forecast to expand at an 8.65% CAGR through 2031, nearly doubling overall Fluorochemicals market growth. Specialty and inorganic products held 56.81% of the Fluorochemicals market share in 2025 as semiconductor gases and pharma intermediates continued to dominate premium niches. PTFE remains the volume leader because of unmatched chemical inertness in seals and gaskets, while PVDF’s binder role in EV batteries advances at double-digit rates that elevate the Fluorochemicals market size for battery materials. Fluoroelastomers command the highest per-kilogram pricing due to aerospace and under-hood specifications that tolerate no substitution.

Growth momentum in PTFE and PVDF contrasts with shrinking HFC volumes under Kigali quotas. HFO uptake only partially offsets this contraction, leaving overall fluorocarbon demand flat to slightly down. China’s fast-tracked PVDF and PTFE expansions introduce oversupply risk if PFAS import rules tighten in Europe or the United States, yet low cost and captive fluorspar keep Chinese volumes competitive. “Other products,” notably fluorinated surfactants, face the harshest regulatory scrutiny and could shrink outright once broad PFAS bans crystallize.

By End-User Industry: Medical Segment Accelerates Amid Refrigeration Maturity

Refrigeration and air conditioning held 27.84% of the Fluorochemicals market size in 2025, but natural-refrigerant substitution and better energy efficiency slow incremental volume. Medical devices grow at a 5.95% CAGR, led by PTFE vascular grafts, PVDF stent coatings, and fluoropolymer catheters that leverage biocompatibility and sterilization resistance. Semiconductor demand continues to rise steadily as fabs consume high-purity NF₃ and PTFE wire insulation, keeping the Fluorochemicals market balanced between electronics and medical growth vectors.

Automotive demand is in transition: internal-combustion fleets still need HFO cabin cooling, while EV adoption shifts usage toward PVDF binder and LiPF₆ salt. Textile and outdoor-wear makers phase out fluorotelomer DWR coatings under corporate sustainability pledges, trimming consumption in that niche. Aerospace and military users stay stable thanks to mission-critical exemptions that protect fluoroelastomer and PTFE applications from regulatory bans.

Geography Analysis

Asia-Pacific held 61.52% of the Fluorochemicals market in 2025 and is forecast to post a 4.88% CAGR through 2031. China’s vertically integrated majors leverage captive fluorspar and HF to defend cost leadership, while India’s USD 47.4 billion cold-chain build elevates HFC and R-32 demand. Japan and South Korea import more high-purity gases after capacity relocations to China, spurring re-shoring incentives that could boost regional Fluorochemicals market volumes from 2027 onward.

North America ranked second in 2025, lifted by semiconductor megaprojects in Arizona, Texas, and Ohio and by mandatory R-1234yf adoption in cars. Permitting delays and labor shortages slightly postpone new fab startups, tempering near-term volume, but once operational the additional NF₃ and CF₄ pull-through will materially enlarge the regional Fluorochemicals market. Canada’s oil-sands processing and aerospace production sustain PTFE and fluoroelastomer demand, while Mexico strengthens its role as a fluorspar supplier to U.S. HF plants.

Europe’s share slipped as F-gas quotas constrained new HFC sales and PFAS compliance costs deterred capacity additions. Producers now focus on high-margin specialty niches and fluoropolymer recycling, leveraging regulatory exemptions for aerospace and medical devices. South America and Middle East & Africa remain smaller bases yet post above-average growth, aided by refrigeration infrastructure, district-cooling projects, and rising living standards that spur first-time appliance ownership.

Competitive Landscape

The Fluorochemicals market is moderately consolidated. Success in the fluorochemical industry increasingly relies on the ability of companies to deliver sustainable solutions while maintaining cost efficiency. Leading market players are making substantial investments in next-generation products designed to reduce environmental impact, driven by evolving regulations on greenhouse gas emissions. These companies are also prioritizing high-growth application segments by directing targeted research and development efforts. Establishing strong relationships with end-users through technical support and customized solutions has become essential for preserving market share. Effectively navigating complex regulatory frameworks and ensuring resilient supply chains will be critical for achieving long-term business success.

Emerging players can strengthen their market position by focusing on niche applications and regional markets, where they can cultivate strong customer relationships and develop specialized expertise. Success factors include delivering innovative solutions to address specific industry challenges, building efficient distribution networks, and maintaining production flexibility. Additionally, companies must recognize the growing importance of sustainability credentials and environmental compliance in influencing customer decisions. The market's future will depend on the ability of players to balance environmental considerations with performance requirements while mitigating risks associated with substitution by alternative materials and technologies. Strategic partnerships with research institutions and technology providers will play an increasingly significant role in sustaining competitive advantage.

Fluorochemical Industry Leaders

The Chemours Company

Daikin Industries, Ltd.

Honeywell International Inc.

3M

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Daikin Industries committed USD 800 million to expand PTFE and FEP output by 40% at Decatur, Alabama, with abatement gear designed to cut fluorinated-gas emissions by 50%.

- July 2025: Honeywell signed a USD 500 million multiyear deal to supply ultra-high-purity NF₃ and CF₄ to Samsung fabs, including joint work on next-generation low-GWP plasma gases.

Global Fluorochemical Market Report Scope

Fluorochemicals are hydrocarbons that consist of fluorine. These are the chemical compounds in which at least one hydrogen atom is replaced by fluorine. Fluorochemicals are popular in the fields of medical and dental care and chemical manufacturing. It is used in plasma etching in semiconductors and light bulbs and to produce flat display panels and plastics such as polytetrafluoroethylene (PTFE).

The fluorochemical market is segmented by product, end-user industry, and geography. By product, the market is segmented into fluorocarbon, fluoropolymer, specialty and inorganic fluorochemicals, and other products. By end-user industry, the market is segmented into refrigeration and air conditioning, automotive, electrical and electronics, medical, textile and chemicals, and other end-user industries (military, aerospace, etc.). The report offers market sizes and forecasts for 16 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of volume (tons).

| Fluorocarbon | HFCs |

| HFOs | |

| HCFCs | |

| Fluoropolymer | PTFE |

| PVDF | |

| PCTFE | |

| Fluoroelastomers | |

| Others | |

| Specialty and Inorganic Fluorochemicals | |

| Other Products |

| Refrigeration and Air Conditioning |

| Automotive |

| Electrical and Electronics (incl. Semiconductors) |

| Medical |

| Textile and Chemicals |

| Other End-user Industries (Military, Aerospace, etc.) |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Fluorocarbon | HFCs |

| HFOs | ||

| HCFCs | ||

| Fluoropolymer | PTFE | |

| PVDF | ||

| PCTFE | ||

| Fluoroelastomers | ||

| Others | ||

| Specialty and Inorganic Fluorochemicals | ||

| Other Products | ||

| End-user Industry | Refrigeration and Air Conditioning | |

| Automotive | ||

| Electrical and Electronics (incl. Semiconductors) | ||

| Medical | ||

| Textile and Chemicals | ||

| Other End-user Industries (Military, Aerospace, etc.) | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected volume of the Fluorochemicals market in 2031?

The Fluorochemicals market is forecast to reach 6.55 million tons by 2031, up from 5.25 million tons in 2026.

Which product segment is growing fastest through 2031?

Fluoropolymers are expanding at an 8.65% CAGR, nearly twice the overall market pace due to semiconductor, EV-battery, and medical uptake.

Why is Asia-Pacific the largest regional consumer?

China’s integrated production, India’s cold-chain build-out, and East-Asian semiconductor investments together give Asia-Pacific 61.52% of global demand.

How will PFAS regulations influence supply?

Stricter rules in the U.S. and EU add remediation costs and investment uncertainty, trimming 0.6 percentage points from the forecast CAGR.

Which companies dominate low-GWP refrigerant supply?

Chemours and Honeywell hold key patents for R-1234yf and R-1234ze, sustaining a pricing advantage despite incoming capacity from Chinese competitors.

Page last updated on: