Mulch Films Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

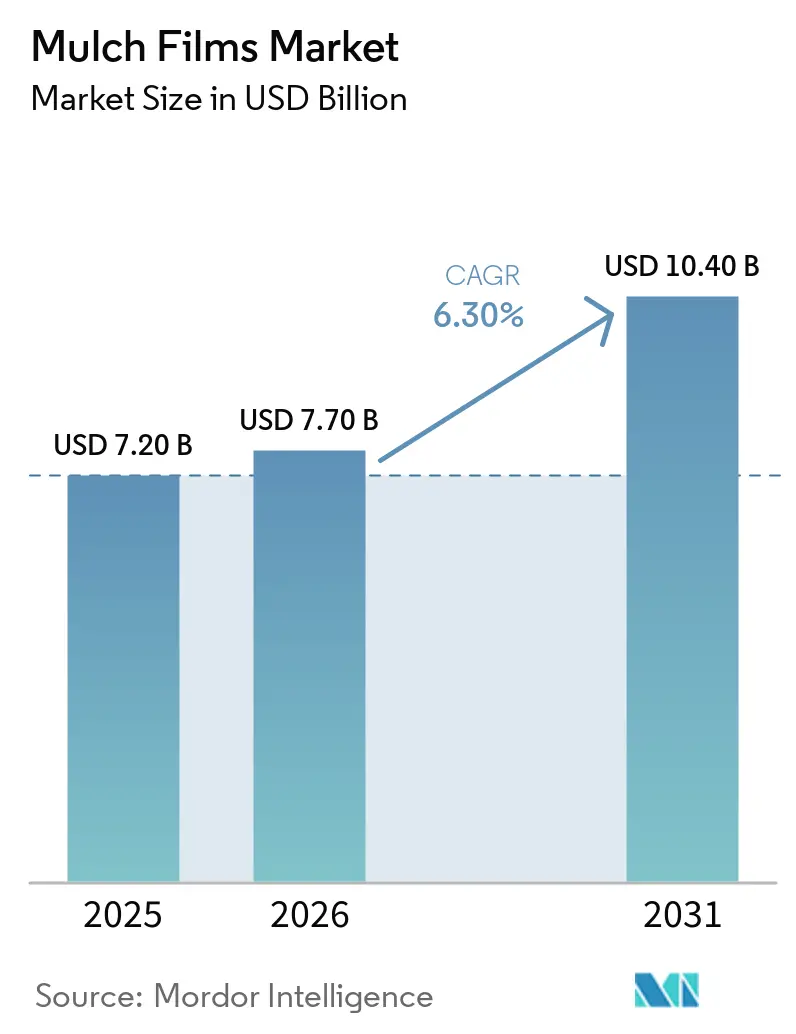

| Market Size (2026) | USD 7.70 Billion |

| Market Size (2031) | USD 10.40 Billion |

| Growth Rate (2026 - 2031) | 6.30% CAGR |

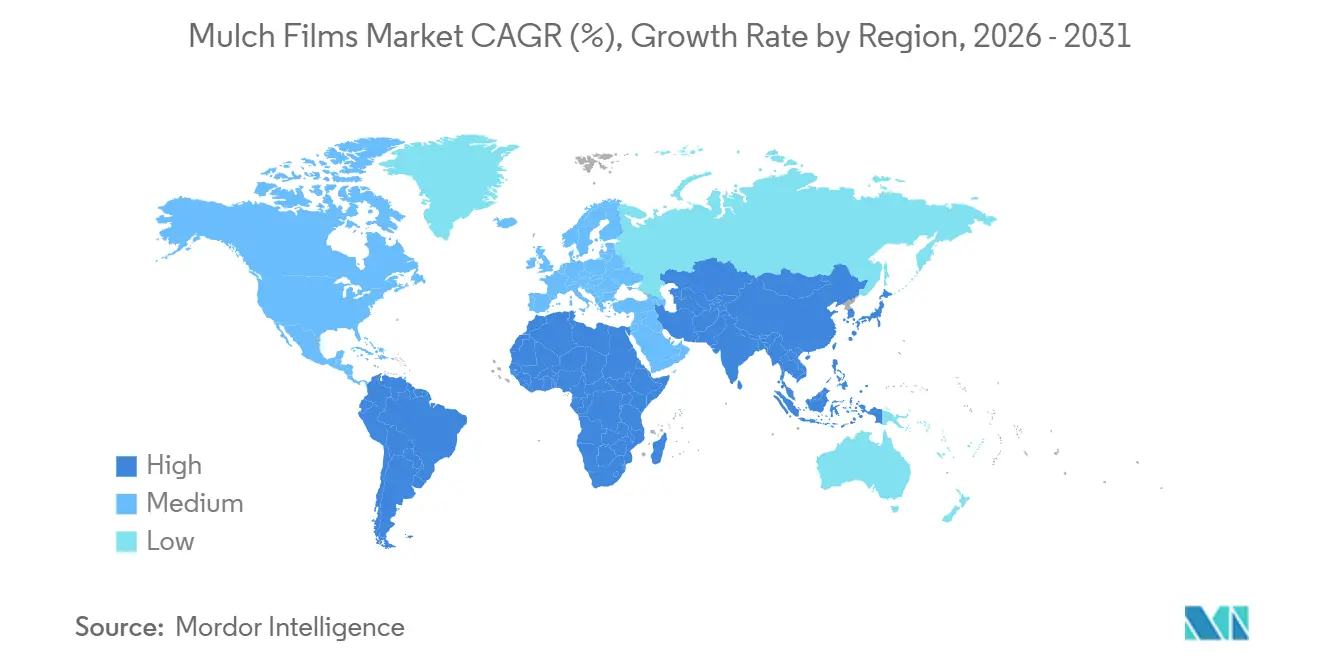

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mulch Films Market Analysis by Mordor Intelligence

The mulch films market size is projected to grow from USD 7.2 billion in 2025 and USD 7.7 billion in 2026 to USD 10.4 billion by 2031, registering a CAGR of 6.3% during the forecast period of 2026-2031. The demand for mulch films is increasing as growers transition from bare-soil cultivation to film-based systems, which offer benefits such as improved water efficiency, weed suppression, and soil temperature regulation. While conventional polyethylene films continue to dominate the market, factors such as regulatory pressures, cost-saving opportunities, and the growing adoption of precision agriculture are driving the penetration of biodegradable films. Government subsidies in countries like India, China, and Argentina are reducing payback periods for small-scale farmers, while advancements such as drone-enabled film-laying services and robotics are addressing labor challenges. Although feedstock price volatility and potential microplastic regulations pose short-term uncertainties, the market's medium-term growth is supported by the strategic importance of soil health compliance, carbon credit opportunities, and the expansion of protected cultivation practices.

Key Report Takeaways

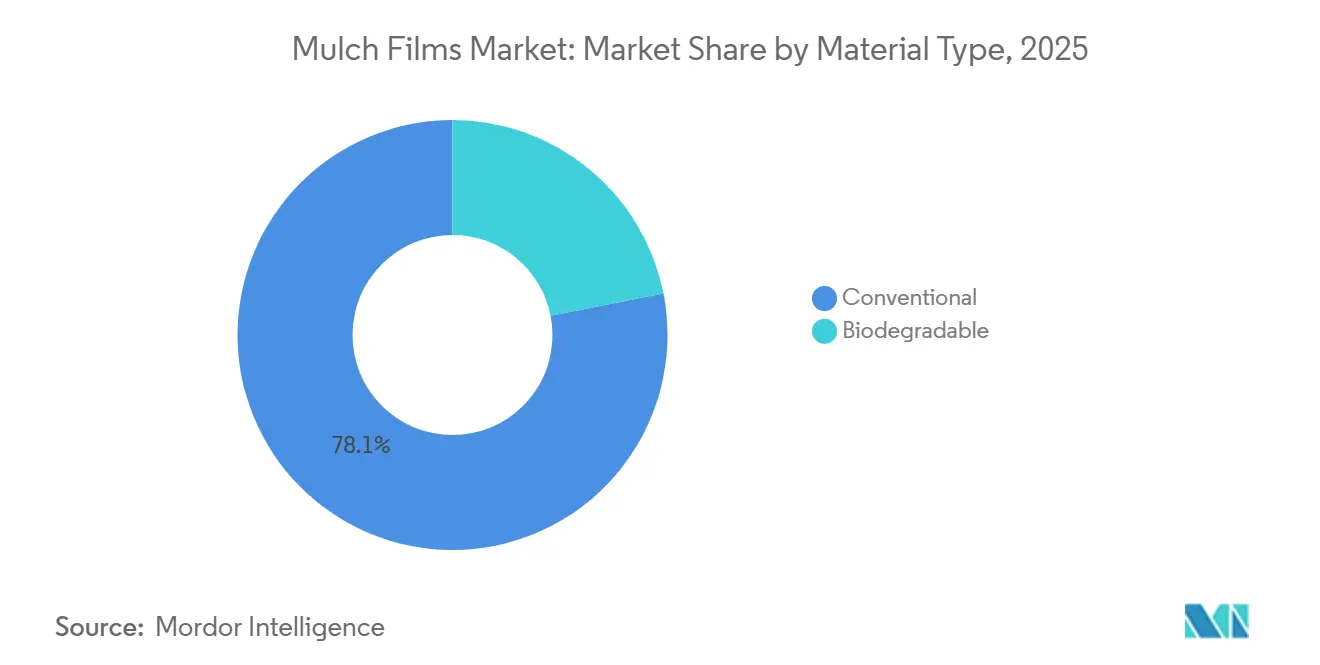

- By material type, conventional films led with the largest 78.1% of the mulch films market share in 2025. The biodegradable films market size is projected to grow at the fastest 8.9% CAGR from 2026 to 2031.

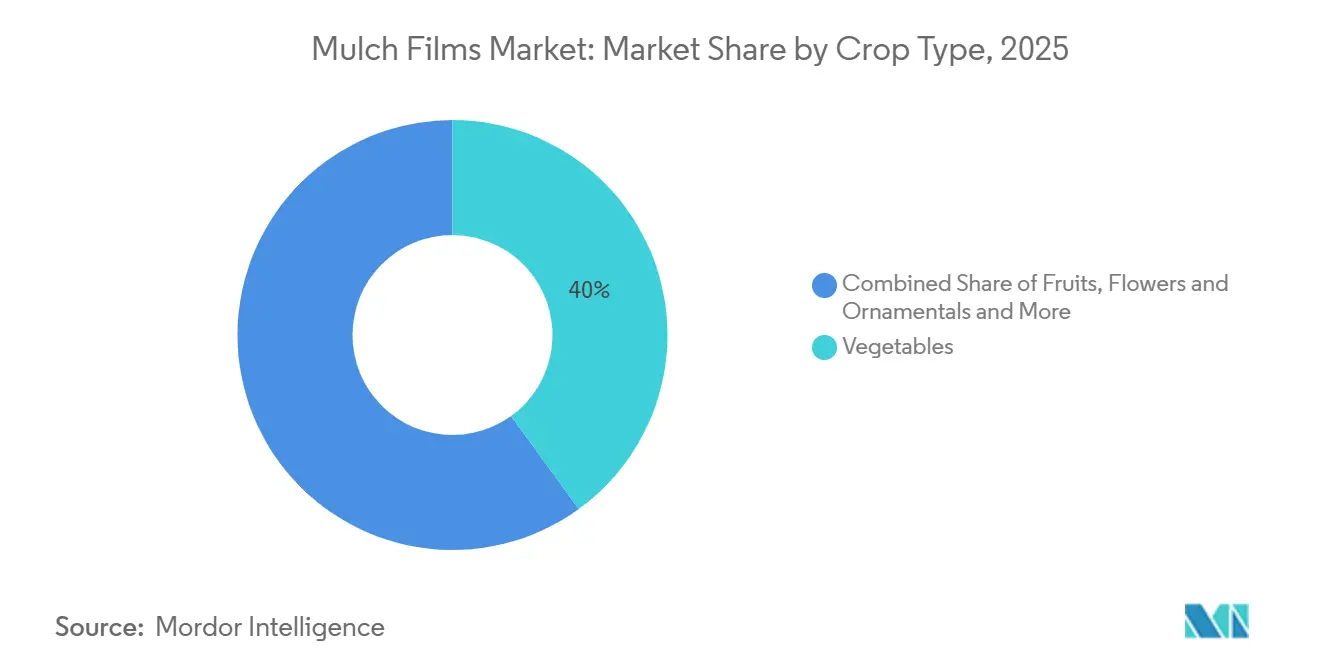

- By crop type, vegetables accounted for the largest 40% of the mulch films market share in 2025. The flowers and ornamentals market size is anticipated to expand at the fastest 8.5% CAGR from 2026 to 2031.

- By geography, Asia-Pacific held the largest 46.1% of the mulch films market share in 2025. The South America market size is projected to grow at the fastest 7.5% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mulch Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for plasticulture | +1.2% | India, China, Argentina, and Brazil | Medium term (2-4 years) |

| Surging demand for protected cultivation | +1.5% | Europe, Middle East, and Asia-Pacific | Long term (≥ 4 years) |

| Rise of precision-agriculture solutions | +0.8% | North America, Europe, and South America | Medium term (2-4 years) |

| Carbon-credit monetization of biochar-enriched films | +0.3% | Europe and North America pilots | Long term (≥ 4 years) |

| Soil-health mandates accelerating degradable films | +1.4% | European Union-27, California, and Japan | Short term (≤ 2 years) |

| Drone-based film-laying services lowering small-farm barriers | +0.5% | South America, Southern Europe, and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Plasticulture

Subsidy programs are lowering initial costs and promoting the adoption of mulch films among farmers. According to the Mission for Integrated Development of Horticulture (MIDH) Operational Guidelines issued on December 31, 2024, the Government of India provides 50% financial assistance for mulching materials, including plastic, jute, agro-textiles, and biodegradable options. The cost norm is set at INR 40,000 per hectare (USD 480/ha), with support limited to a maximum of 2 hectares [1]Source: Government of India, “Mission for Integrated Development of Horticulture (MIDH) Operational Guidelines,” nccd.gov.in. Additionally, these subsidy frameworks are facilitating a gradual transition to biodegradable mulch films, particularly in fruit and vegetable cultivation, where shorter return periods make such investments more viable.

Surging Demand for Protected Cultivation

Surging demand for protected cultivation is accelerating the adoption of mulch films, particularly in horticulture, where soil temperature and moisture control are critical. Mulch films help regulate soil microclimate, reduce evaporation losses, and enhance yield stability under controlled environments. A study conducted by researchers from Northwest A&F University and other Chinese agricultural research institutions in 2024 revealed that plastic film mulching increased crop yield by 26% and water-use efficiency by 33% compared to non-mulched conditions. These advantages are encouraging farmers to adopt mulch films in protected cultivation systems to optimize resource use and enhance crop performance.

Rise of Precision-Agriculture Solutions

Advancements in precision agriculture are enhancing the efficiency and effectiveness of mulch film usage by enabling precise water and nutrient management. Technologies such as drip irrigation combined with plastic mulching help minimize evaporation losses and improve crop performance. A study conducted by researchers from Sichuan University and the Chinese Academy of Agricultural Sciences in 2025 found that combining plastic film mulching with drip irrigation improved water productivity by 8.5%. These results emphasize the benefits of integrating these systems, encouraging farmers to use mulch films to enhance productivity, particularly in regions with limited water and resources.

Carbon-Credit Monetization of Biochar-Enriched Films

Sustainability trends are driving the adoption of biodegradable and advanced mulch films that enhance soil health. Biodegradable mulch films minimize residual plastic accumulation and improve soil organic carbon levels compared to conventional polyethylene films. These films decompose naturally, reducing long-term environmental pollution and contributing to healthier ecosystems. Additionally, these environmental advantages align with emerging carbon credit frameworks, providing additional economic incentives for farmers to transition to sustainable mulch film alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in fossil-based resin prices | -0.9% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Stringent single-use-plastic regulations | -0.6% | European Union-27, North America states, China, and Japan | Medium term (2-4 years) |

| Imminent micro-plastic caps on (Poly butylene adipate-co-terephthalate) PBAT blends | -0.4% | European Union (REACH) and potential North America | Medium term (2-4 years) |

| Competition from paper and spray-on biopolymer mulches | -0.5% | Netherlands, Spain, California, and Oregon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Fossil-Based Resin Prices

Fluctuations in fossil-based raw material prices are creating cost uncertainties for mulch film manufacturers and farmers. Polyethylene, a primary component of conventional mulch films, is particularly affected by crude oil price variations and supply-demand dynamics. Data from the Federal Reserve Economic Data shows that the Producer Price Index (PPI) for plastics material and resin manufacturing rose from 302.52 in December 2025 to 312.51 in March 2026, reflecting a significant increase in resin production costs[2]Source: U.S. Bureau of Labor Statistics, Federal Reserve Bank of St. Louis, “Producer Price Index by Industry: Plastics Material and Resin Manufacturing”, fred.stlouisfed.org . These price changes elevate the production costs of plastic mulch films and narrow the cost difference between conventional and biodegradable alternatives, promoting a gradual shift toward more sustainable materials.

Stringent Single-Use-Plastic Regulations

Regulatory pressure on single-use plastics is significantly limiting the growth of conventional mulch films. Governments are increasingly enforcing extended producer responsibility frameworks and implementing stricter compliance standards for plastic use in agriculture. These regulations require manufacturers to not only adjust product portfolios across regions but also invest in research and development to meet evolving environmental standards. This has led to increased operational complexity and higher costs for manufacturers. Consequently, such policy measures are accelerating the adoption of biodegradable mulch films, which are seen as a more sustainable alternative, while simultaneously creating compliance-related challenges for suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Biodegradable Films Gain Despite Cost Gap

Conventional films are projected to dominate the segment, accounting for 78.1% of the mulch films market share in 2025, primarily due to their cost efficiency and durability across various cropping systems. Polyethylene-based films continue to be widely used in developing regions where affordability and ease of application are essential. Their high tensile strength and moisture retention properties contribute to consistent crop yields. Additionally, their availability in various thicknesses and formats enhances their appeal, particularly for long-cycle crops and in areas lacking structured waste management systems for agricultural plastics.

The biodegradable films market size is projected to grow at the fastest CAGR of 8.9% from 2026 to 2031, driven by regulatory support and labor-saving advantages. These films eliminate the need for post-harvest removal and reduce soil contamination risks, making them increasingly suitable for high-value horticultural crops. Certification standards are bolstering product acceptance in regulated markets. Advances in polymer formulations and localized production are gradually addressing cost-related challenges. Adoption is increasing in regions focusing on sustainability compliance and minimizing environmental impact, particularly where agricultural labor costs are rising and disposal regulations are becoming more stringent.

By Crop Type: Vegetables Lead, Ornamentals Accelerate

Vegetables accounted for the largest 40% of the mulch films market share in 2025, driven by their sensitivity to soil temperature and moisture conditions. Mulch films improve germination rates, suppress weed growth, and enable earlier harvesting cycles for crops such as tomatoes, peppers, and cucumbers. Their role in stabilizing soil conditions enhances yield consistency and quality, which is crucial for commercial vegetable farming. Adoption is particularly strong in intensive cultivation systems, where maximizing productivity per hectare is vital for profitability and supply chain efficiency.

The flowers and ornamentals market size is projected to expand at the fastest 8.5% CAGR from 2026 to 2031, fueled by increasing demand for high-quality, visually consistent produce in export markets. Mulch films contribute to soil cleanliness and improved aesthetic output, which are essential for achieving premium pricing. Growers in greenhouse environments are increasingly utilizing specialized films to minimize fungal infections and optimize microclimate conditions. This segment benefits from the growth of global floriculture trade and stricter quality standards, which encourage the adoption of advanced agricultural inputs to enhance yield quality and reduce post-harvest losses.

Geography Analysis

Asia-Pacific accounted for the largest 46.1% share of the mulch films market in 2025, primarily due to extensive agricultural activity and robust government support for plasticulture practices. Countries like China and India are actively promoting mulch film adoption through subsidy programs and horticulture missions. The region benefits from a significant base of smallholder farmers transitioning to productivity-enhancing inputs. Additionally, increasing vegetable cultivation and the adoption of protected farming systems are driving demand. Local manufacturing capabilities and the availability of cost-effective products further facilitate widespread adoption across diverse climatic and cropping conditions.

South America is projected to grow at the fastest CAGR of 7.5% from 2026 to 2031, supported by the expansion of horticulture and fruit cultivation sectors. Countries such as Brazil and Argentina are experiencing increased adoption of mulch films due to their ability to enhance crop yield and quality under varying climatic conditions. Government-backed agricultural initiatives and rising export demand for fruits are encouraging farmers to adopt modern farming inputs. Local production capabilities and customized product offerings are further strengthening market penetration across various crop segments and farming practices.

Europe leads in sustainability-driven adoption within the mulch films market, driven by growing demand for biodegradable solutions and circular agriculture practices. Mediterranean countries prioritize thicker, hail-resistant films to address climate variability, while the Middle East focuses on sulfur-resistant, long-life films designed for harsh climatic conditions. In Africa, there is increasing demand for climate-resilient agricultural inputs to enhance productivity. According to a 2024, United Nations Educational, Scientific and Cultural Organization report, agriculture accounts for 70% of global freshwater withdrawals, highlighting the significance of water-efficient practices like mulching across these regions [3]Source: United Nations Educational, Scientific and Cultural Organization, “United Nations World Water Development Report 2024: Water for Prosperity and Peace,” unesco.org.

Competitive Landscape

The market is fragmented, with leading players including BASF SE, Berry Global Group, Inc. (Amcor plc.), Armando Alvarez, S.A., RKW Group, and Dow Inc. Global companies leverage combined resin manufacturing and film production to achieve cost control and supply chain efficiency. Regional players focus on differentiation through customization, faster delivery, and localized customer support. Product innovation and adaptability are critical competitive factors, particularly in addressing diverse agricultural needs across regions. The ability to provide tailored film solutions based on crop type, climate, and soil conditions offers a strategic advantage in capturing market share.

Regulatory compliance is becoming a significant competitive differentiator as manufacturers align their products with global biodegradability and compostability standards. Companies that meet multiple certification requirements across regions are gaining pricing advantages and stronger market positioning. Increasing environmental regulations are driving investments in biodegradable product lines. Simultaneously, cost competitiveness remains crucial, prompting manufacturers to optimize production processes and explore alternative raw materials. Strategic partnerships and localized manufacturing are further facilitating expansion into emerging markets with evolving regulatory frameworks.

Competitive positioning is increasingly shaped by technological advancements and sustainability initiatives. Industry players are integrating precision agriculture solutions and adopting circular economy models to enhance product value. Mulch film applications can improve water-use efficiency and reduce input costs, reinforcing their role in modern agricultural systems. These innovations enable companies to differentiate their offerings while addressing environmental concerns, supporting long-term growth and competitive resilience in the evolving agricultural landscape.

Mulch Films Industry Leaders

BASF SE

Berry Global Group, Inc. (Amcor plc.)

Armando Alvarez, S.A.

RKW Group

Dow Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor plc acquired Berry Global Group Inc., consolidating manufacturing capacity and expanding presence across major agricultural regions. The acquisition enhanced innovation capabilities in biodegradable and specialty mulch films while optimizing distribution networks.

- June 2024: Dow Inc. introduced the REVOLOOP PCR-based film resins, underscoring the increasing focus on sustainable film materials. These resins, made from post-consumer recycled content, could significantly influence the future development of biodegradable and recyclable films.

- April 2024: BASF SE expanded the application and commercialization of its ecovio M 2351 biodegradable polymer for mulch films. This product is certified under EN 17033 and is designed for agricultural use to enhance yield and minimize microplastic residue.

Global Mulch Films Market Report Scope

Mulch films are thin sheets made of plastic or biodegradable materials, applied over soil to conserve moisture, suppress weed growth, and regulate soil temperature. They contribute to increased crop yield, improved soil quality, and reduced water evaporation in agricultural practices. The mulch films market report is segmented by material type (conventional and biodegradable), by crop type (vegetables, fruits, flowers and ornamentals, and other crop types), and by geography (North America, South America, Europe, Asia-Pacific, the Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Conventional |

| Biodegradable |

| Vegetables |

| Fruits |

| Flowers and Ornamentals |

| Other Crop Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Material Type | Conventional | |

| Biodegradable | ||

| By Crop Type | Vegetables | |

| Fruits | ||

| Flowers and Ornamentals | ||

| Other Crop Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the mulch films market in 2026?

The mulch films market size stands at USD 7.7 billion in 2026 and is projected to reach USD 10.4 billion by 2031.

Which material holds the largest share?

Conventional material accounts for the largest 78.1% of mulch films market share, owing to its low cost and mechanical strength.

Which region is growing the fastest?

South America is forecast to expand at the fastest 7.5% CAGR from 2026 to 2031.

What is the main short-term risk for suppliers?

Volatility in fossil-based resin prices can compress margins and delay grower purchases, trimming growth by an estimated 0.9% point.

Page last updated on: