Market Overview

| Study Period | 2020 - 2030 |

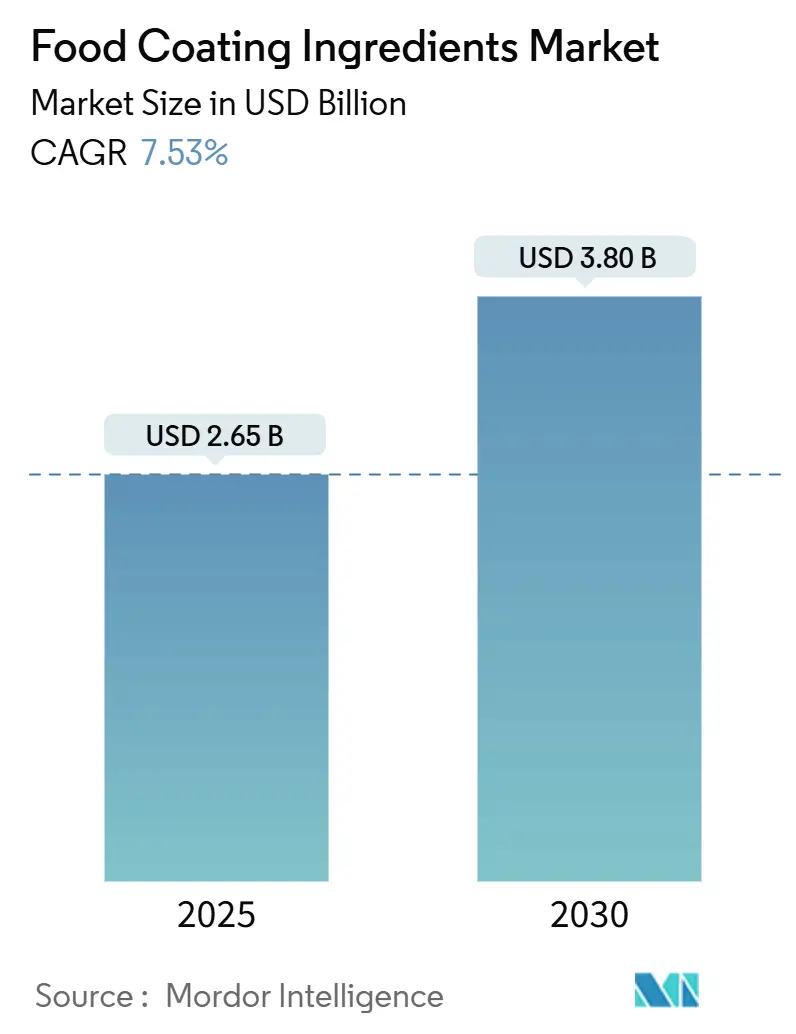

| Market Size (2025) | USD 2.65 Billion |

| Market Size (2030) | USD 3.80 Billion |

| Growth Rate (2025 - 2030) | 7.53% CAGR |

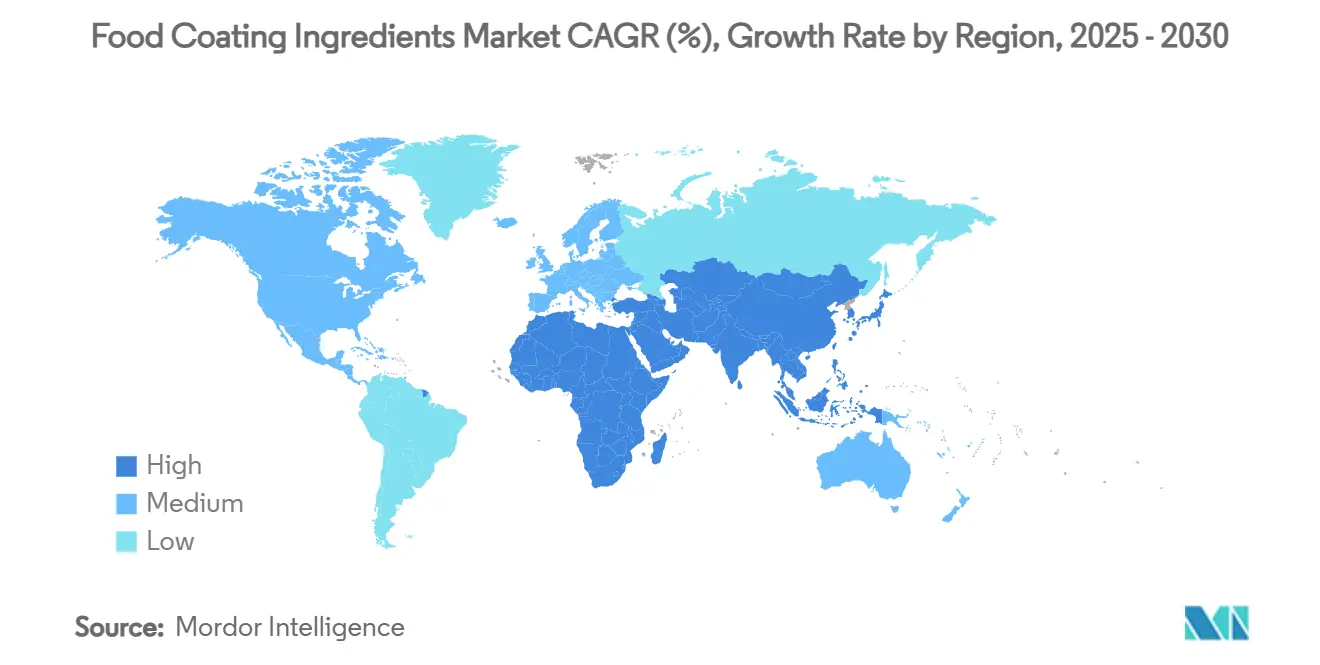

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Coating Ingredients Market Analysis by Mordor Intelligence

The global food coating ingredients market is valued at USD 2.65 billion in 2025 and is projected to reach USD 3.80 billion by 2030, growing at a compound annual growth rate (CAGR) of 7.53% during the forecast period. This growth trajectory reflects the industry's strategic pivot toward functional enhancement and clean-label formulations, driven by evolving consumer preferences and technological advancements in coating application methods. The market's expansion is underpinned by the increasing sophistication of food preservation technologies, where coating ingredients serve dual purposes of extending shelf life while delivering enhanced sensory experiences.

Market dynamics are increasingly influenced by the convergence of regulatory pressures and technological innovation, particularly in antimicrobial coating development. The FDA's recent approval of calcium phosphate and butterfly pea flower extract as color additives, effective June 2025, exemplifies regulatory adaptation to natural ingredient trends [1]Federal Register, "Listing of Color Additives Exempt From Certification; Calcium Phosphate," federalregister.gov . This approval has opened new opportunities for manufacturers to develop innovative coating solutions using natural colorants. The advancement in coating technologies has enabled manufacturers to achieve better adhesion, uniform application, and enhanced functionality. These improvements have led to the development of multi-functional coating ingredients that provide moisture barriers, improved texture, and enhanced nutritional profiles. The industry has also witnessed increased adoption of sustainable coating materials, reflecting the growing environmental consciousness among consumers and manufacturers alike.

Key Report Takeaways

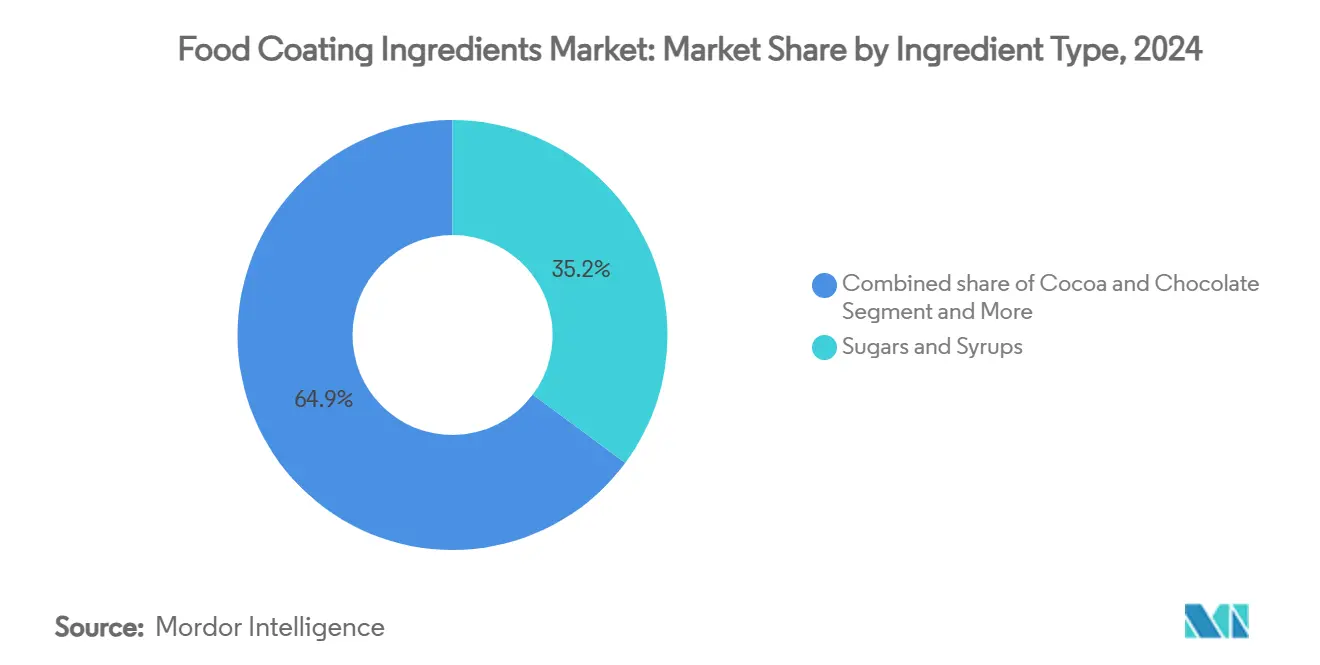

• By ingredient type, sugars and syrups held 35.15% of the food coating ingredients market share in 2024, while cocoa and chocolate are on track for the fastest 8.15% CAGR through 2030.

• By form, liquid coatings captured 65.12% revenue in 2024 and are projected to expand at a 9.15% CAGR between 2025-2030.

• By nature, conventional products retained 73.66% share in 2024, whereas organic lines are forecast to post a 10.27% CAGR to 2030.

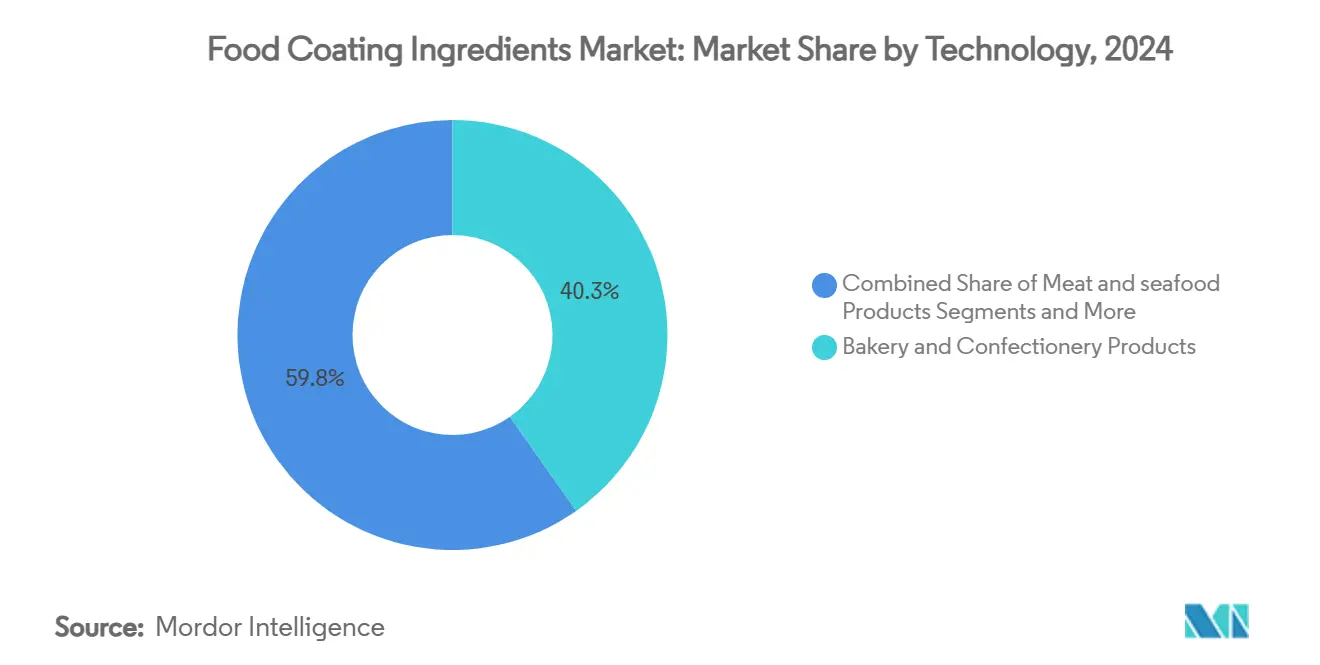

• By application, bakery and confectionery dominated with 40.25% share in 2024, yet meat and seafood coatings are set to grow at a 10.65% CAGR during 2025-2030.

• By geography, North America controlled 42.68% of 2024 revenue, but Asia-Pacific is expected to grow the fastest at 9.96% CAGR over the forecast horizon.

Global Food Coating Ingredients Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Processed and Convenience Foods | 1.8% | Global, with strongest impact in APAC and North America | Medium term (2-4 years) |

| Expansion of the Bakery, Confectionery, and Snack Food Industries | 1.5% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Technological Advancements in Coating Application Methods | 1.2% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Adoption of Clean-Label, Organic, and Plant-Based Ingredients | 1.0% | North America & EU primary, spreading globally | Medium term (2-4 years) |

| Rising Popularity of Frozen, Refrigerated, and Shelf-Stable Products | 0.9% | Global, with emphasis on developed markets | Long term (≥ 4 years) |

| Growing Demand for Functional and Antimicrobial Edible Coatings | 0.8% | Global, with early adoption in food safety-conscious regions | Medium term (2-4 years) |

Source: Mordor Intelligence

Increasing Demand for Processed and Convenience Foods

The surge in processed and convenience food consumption fundamentally reshapes coating ingredient requirements, with manufacturers prioritizing formulations that maintain product integrity during extended storage and transportation cycles. This trend accelerates in emerging markets where urbanization drives dietary pattern shifts toward packaged foods, creating substantial volume opportunities for coating ingredient suppliers. The convenience food sector's growth directly correlates with coating ingredient innovation, as manufacturers seek solutions that deliver consistent texture, flavor release, and visual appeal across diverse storage conditions. Advanced coating technologies now enable extended shelf life without compromising sensory attributes, addressing the dual challenge of food security and consumer expectations. India's food processing sector exemplifies this transformation, with government initiatives like the Production Linked Incentive Scheme driving capacity expansion and technological adoption [2]India Brand Equity Foundation, “Food Processing Industry Overview,” ibef.org.

Expansion of the Bakery, Confectionery, and Snack Food Industries

The bakery and confectionery sector's evolution toward premium and artisanal products creates sophisticated coating ingredient requirements that extend beyond basic preservation to include sensory enhancement and visual differentiation. The surging chocolate market reveals three distinct consumer trends driving coating innovation: intense indulgence focusing on bold flavors, mindful indulgence emphasizing ethical sourcing, and healthy indulgence incorporating functional ingredients. This segmentation forces coating ingredient manufacturers to develop specialized formulations that address each consumer category while maintaining production efficiency. The snack food industry's parallel expansion, particularly in air fryer-compatible products, demands coating ingredients that perform optimally under high-heat, low-oil cooking conditions.

Technological Advancements in Coating Application Methods

Precision application technologies revolutionize coating ingredient utilization efficiency while enabling previously impossible formulation combinations, particularly in nano-enabled antimicrobial systems that deliver targeted preservation effects. The integration of artificial intelligence in coating application, as demonstrated by Kerry Group's AI-powered innovation platforms, enables real-time optimization of coating thickness, ingredient distribution, and curing parameters. These technological advances reduce material waste while improving coating uniformity, directly impacting manufacturers' cost structures and product quality consistency. Bühler's investment in AI-driven sustainability solutions exemplifies how equipment manufacturers are embedding intelligence into coating application systems to optimize resource utilization and minimize environmental impact. The convergence of precision application and smart formulation creates competitive advantages for manufacturers who can deliver superior coating performance with reduced ingredient volumes. Advanced application methods also enable the incorporation of heat-sensitive functional ingredients that previously could not survive traditional coating processes.

Adoption of Clean-Label, Organic, and Plant-Based Ingredients

Consumer demand for transparent ingredient lists drives fundamental reformulation strategies, with manufacturers replacing synthetic additives with plant-derived alternatives that maintain equivalent functional performance while meeting clean-label criteria. The organic segment's 10.27% CAGR through 2030 reflects premium positioning opportunities for manufacturers who can deliver certified organic coating solutions without compromising application properties or shelf life. Sparxell's development of cellulose-based natural colors. Plant-based coating ingredients face unique technical challenges, particularly in achieving the barrier properties and adhesion characteristics traditionally provided by animal-derived components. Farbe Naturals' launch of Natufresh SA, a plant-based sorbic acid alternative derived from rowanberries, illustrates the industry's progress in developing natural preservatives that match synthetic performance standards. The clean-label movement also drives transparency in sourcing and processing methods, requiring coating ingredient suppliers to document and verify their entire supply chain.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Requirements Related to Additives and Allergens | -0.8% | Global, with strictest enforcement in EU and North America | Long term (≥ 4 years) |

| Volatility in Raw Material Prices | -0.6% | Global, with highest impact on commodity-dependent regions | Short term (≤ 2 years) |

| Rising Competition from Alternative Food Preservation and Processing Methods | -0.4% | Developed markets with advanced food technology adoption | Medium term (2-4 years) |

| Limited Shelf Life and Stability of Certain Natural Coating Ingredients | -0.3% | Global, affecting premium natural product segments | Medium term (2-4 years) |

Source: Mordor Intelligence

Stringent Regulatory Requirements Related to Additives and Allergens

Regulatory complexity intensifies as global food safety authorities implement increasingly sophisticated testing protocols and documentation requirements for coating ingredients, particularly those containing potential allergens or novel functional compounds. The FDA's comprehensive framework under 21 CFR Parts 170-186 establishes detailed safety evaluation criteria for food additives, requiring extensive toxicological data and manufacturing process validation that can extend product development timelines. FSIS Directive 7120.1's recent updates to approved substances for meat and poultry products demonstrate the ongoing evolution of regulatory requirements, with specific provisions for antimicrobial agents and film-forming compounds that directly impact coating ingredient formulations [3]U.S. Department of Agriculture, “FSIS Directive 7120.1,” usda.gov. Manufacturers must also navigate varying international standards, with some regions maintaining more restrictive policies on certain coating ingredients, limiting global product standardization opportunities.

Volatility in Raw Material Prices

Raw material price fluctuations create significant margin pressure for coating ingredient manufacturers, particularly those dependent on agricultural commodities subject to weather patterns, geopolitical tensions, and supply chain disruptions. The cocoa crisis exemplifies this challenge, with prices increasing approximately 300% between 2023 and 2024 due to soil degradation and disease in key producing regions of Côte d'Ivoire and Ghana, forcing manufacturers to develop alternative formulations or accept reduced profitability. Price volatility extends beyond individual commodities to affect entire ingredient categories, as manufacturers often lack sufficient pricing power to pass through cost increases to food processors who face their own margin pressures. The situation is compounded by the limited availability of effective hedging instruments for many specialty coating ingredients, leaving manufacturers exposed to spot market fluctuations.

Segment Analysis

Ingredient Type: Cocoa Innovation Drives Premium Growth

The ingredients market segmentation indicates sugars and syrups hold a 35.15% market share in 2024. This dominance stems from their extensive application in confectionery manufacturing and cost-effectiveness. These traditional ingredients maintain their importance in confectionery products by providing essential functions in texture, preservation, and taste. Sugars, including sucrose, glucose, and fructose, serve multiple purposes in confectionery production. They act as bulking agents, enhance shelf life through moisture control, and contribute to the crystallization process in hard candies. Syrups, particularly corn syrup and high-fructose corn syrup, prevent sugar crystallization in soft candies and provide smooth texture in caramels and toffees. The cost-effectiveness of these ingredients is attributed to their widespread availability, established supply chains, and efficient production processes. Additionally, their functional properties in binding, browning reactions, and fermentation make them indispensable in various confectionery applications, from chocolates to gummies and marshmallows.

The cocoa and chocolate segment is projected to grow at a CAGR of 8.15% through 2030. This growth is driven by consumer demand for premium chocolate products, higher disposable incomes, and increased consumption of dark chocolate. Premium chocolate products include single-origin chocolates, organic variants, and specialty flavored bars. The rising health consciousness among consumers has particularly boosted the demand for dark chocolate, which is perceived as a healthier alternative due to its antioxidant properties and lower sugar content. The market expansion is supported by advancements in cocoa processing methods, including improved fermentation techniques, temperature-controlled storage systems, and automated production lines. Additionally, the growth in artisanal chocolate production has introduced diverse flavor profiles and unique product offerings, catering to consumers seeking authentic and high-quality chocolate experiences.

Note: Segment shares of all individual segments available upon report purchase

Form: Liquid Dominance Reflects Application Efficiency

Liquid coatings command 65.12% market share in 2024 and maintain the fastest growth at 9.15% CAGR through 2030, reflecting industry preference for application efficiency and uniform coverage capabilities that reduce material waste while improving product consistency. This dominance stems from liquid coatings' superior penetration characteristics and ability to incorporate heat-sensitive functional ingredients that cannot survive traditional dry coating processes. The liquid segment's growth acceleration reflects technological advances in spray application systems and precision dosing equipment that enable manufacturers to achieve optimal coating thickness with minimal overspray. Dry coatings retain strategic importance in specific applications where moisture sensitivity or extended shelf life requirements favor powder-based formulations, particularly in ambient-stable products destined for emerging markets with limited cold chain infrastructure.

The form segmentation increasingly reflects functional requirements rather than traditional application preferences, with manufacturers selecting coating forms based on specific performance criteria such as adhesion strength, barrier properties, and compatibility with downstream processing steps. Liquid coating innovations include the development of water-based systems that eliminate volatile organic compounds while maintaining application properties, addressing environmental regulations and workplace safety concerns.

Nature: Organic Premium Positioning Accelerates

Conventional products dominate the market with a 73.66% share in 2024. These coatings maintain their market leadership due to lower costs and well-established supply chains, especially in applications where performance requirements outweigh the need for organic certification. The cost advantage stems from economies of scale in production, standardized manufacturing processes, and readily available raw materials. Additionally, conventional coatings benefit from decades of research and development, resulting in proven performance across various industrial applications. The extensive distribution networks and established relationships with suppliers further strengthen their market position, particularly in regions where price sensitivity is a crucial factor in purchasing decisions.

Organic alternatives are expected to grow at a 10.27% CAGR through 2030. This growth in organic coatings reflects consumer preference for certified products and their willingness to pay premium prices. This growth differential indicates successful market segmentation where organic coatings command price premiums sufficient to offset higher raw material costs and certification expenses. The organic segment's expansion is supported by regulatory clarity around organic certification requirements for coating ingredients, enabling manufacturers to develop compliant formulations with confidence in market positioning. The organic segment's growth trajectory reflects broader consumer trends toward transparency and natural ingredients, with manufacturers investing in organic supply chain development to capture premium positioning opportunities.

Application: Meat and Seafood Innovation Leads Growth

The bakery and confectionery segment dominates the market with a 40.25% share in 2024, indicating significant demand in food applications. This segment's prominence is driven by increasing consumer preference for baked goods, growing urbanization, and rising disposable incomes. Manufacturers are focusing on developing innovative products and expanding their product portfolios to meet diverse consumer preferences. The segment's growth is further supported by technological advancements in production processes and the rising trend of premium and artisanal baked products.

Meat and seafood applications emerge as the fastest-growing segment at 10.65% CAGR through 2030, driven by plant-based meat alternative development and advanced preservation requirements. This growth pattern reflects the industry's expansion beyond traditional applications into technically demanding segments where coating ingredients play crucial roles in texture mimicry, preservation, and sensory enhancement. The meat and seafood segment's acceleration benefits from antimicrobial coating innovations that extend shelf life while maintaining product safety, particularly important for high-risk protein products. Plant-based meat alternatives drive significant innovation in coating applications, where ingredients must replicate the texture, appearance, and cooking characteristics of animal proteins while maintaining plant-based certification.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America holds a 42.68% market share in 2024, supported by its advanced food processing infrastructure and regulatory frameworks that promote high-quality coating solutions. Recent FDA approvals of ingredients like calcium phosphate and butterfly pea flower extract as color additives reflect the region's regulatory support for innovation. Strong relationships between coating ingredient manufacturers and food processors facilitate the quick implementation of new formulations and technologies.

Asia-Pacific emerges as the fastest-growing region with 9.96% CAGR through 2030, propelled by the rapid industrialization of food processing sectors and expanding middle-class consumer bases that drive demand for processed and convenience foods. China's food processing industry demonstrates particular strength, with the U.S. ranking as the fourth-largest exporter of consumer-oriented products to China in 2023, indicating substantial import demand for specialized ingredients including coating solutions [4]U.S. Department of Agriculture, "China: Food Processing Ingredients Annual," fas.usda.gov. The region's growth creates opportunities for coating ingredient suppliers who can adapt formulations to local taste preferences while maintaining international quality standards. Tate & Lyle's launch of an automated laboratory in Singapore for mouthfeel solutions demonstrates multinational commitment to regional innovation capabilities.

Europe maintains a significant market presence through advanced regulatory frameworks and consumer preference for natural and organic ingredients, driving innovation in clean-label coating formulations and sustainable production methods. South America and Middle East & Africa represent emerging opportunities where economic development and urbanization drive processed food consumption, creating demand for coating ingredients that enable shelf-stable products suitable for challenging distribution environments.

Note: Regional shares of all individual regions will be available upon report purchase

Competitive Landscape

The food coating ingredients market exhibits moderate concentration with a concentration score of 4 out of 10, with established players leveraging scale advantages in raw material procurement and global distribution networks, while emerging opportunities in functional and clean-label segments create entry points for specialized suppliers with innovative formulations. Market leaders such as Cargill, ADM, and Tate & Lyle maintain competitive positions through vertical integration strategies that control key raw material supplies and enable cost-effective production scaling. The competitive intensity increases in premium segments where differentiation through functional performance and clean-label positioning enables higher margins, attracting both established players and innovative startups. Technology adoption emerges as a critical competitive factor, with companies investing in AI-driven formulation optimization and precision application systems to reduce costs while improving product consistency.

Food Coating Ingredients Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Kerry Group PLC

-

Barry Callebaut AG

-

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: At the Frankfurt IFFA trade fair, Sarda Bio Polymers introduced clean-label, plant-based hydrocolloid solutions for meat and alternative protein applications. Their offerings include guar gum, cassia tora gum, konjac, xanthan, carrageenan, tamarind xyloglucan, and CMC, designed to enhance texture with minimal processing while emphasizing sustainability and performance.

- April 2025: AGRANA, a global producer of specialty starch-based ingredients hailing from Austria, has unveiled a new line of clean-label starches, branded as AGENAPURE, expanding its product portfolio.

- December 2024: Ingredion, Inc. has introduced Novation Indulge 2940 starch, a non-GMO functional native corn starch, to broaden its range of clean label texturizers. The company noted that this starch could enhance the texture for gelling and co-texturizing in dairy products, dairy alternatives, and desserts.

Global Food Coating Ingredients Market Report Scope

Food Coatings are the ingredients used to coat food to add texture, flavor, and nutritional value.

The Food Coating Ingredients Market is segmented by Type (Sugars and Syrups, Cocoa and Chocolates, Fats and Oils, Spices and Seasonings, Flours, Batter and Crumbs, and Other Types), Application (Bakery, Confectionery, Snacks, Dairy, Meat, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The market sizing has been done in value terms in USD for all the abovementioned segments.

| By Ingredient Type | Sugars and Syrups | ||

| Cocoa and Chocolate | |||

| Fats and Oils | |||

| Salts, Spices and Seasonings | |||

| Flours and Starches | |||

| Batter and Crumbs | |||

| Hydrocolloids | |||

| Others | |||

| By Form | Liquid | ||

| Dry | |||

| By Nature | Conventional | ||

| Organic | |||

| By Application | Bakery and Confectionery Products | ||

| Meat and seafood Products | |||

| Snacks and Nutritional Bars | |||

| Dairy Products | |||

| RTE and RTC Foods | |||

| Plant-based Meat Alternatives | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Rest of Middle East and Africa | |||

By Ingredient Type

| Sugars and Syrups |

| Cocoa and Chocolate |

| Fats and Oils |

| Salts, Spices and Seasonings |

| Flours and Starches |

| Batter and Crumbs |

| Hydrocolloids |

| Others |

By Form

| Liquid |

| Dry |

By Nature

| Conventional |

| Organic |

By Application

| Bakery and Confectionery Products |

| Meat and seafood Products |

| Snacks and Nutritional Bars |

| Dairy Products |

| RTE and RTC Foods |

| Plant-based Meat Alternatives |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the food coating ingredients market and how fast is it growing?

The market is valued at USD 2.65 billion in 2025 and is projected to reach USD 3.80 billion by 2030, yielding a 7.53% CAGR.

Which region leads the food coating ingredients market today?

North America holds the largest 2024 share at 42.68%, supported by advanced automation and stringent safety regulations.

Which ingredient sub-category is expanding the fastest?

Cocoa and chocolate coatings are forecast to rise at an 8.15% CAGR as innovators introduce cocoa-replacer systems to mitigate commodity price spikes.

What is driving rapid growth in meat and seafood coating applications?

Rising demand for plant-based and high-protein snacks has lifted the meat and seafood segment, which is on pace for a 10.65% CAGR through 2030 due to antimicrobial and textural innovation. . . . . . . .

Page last updated on: July 3, 2025