Polyimides (PI) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

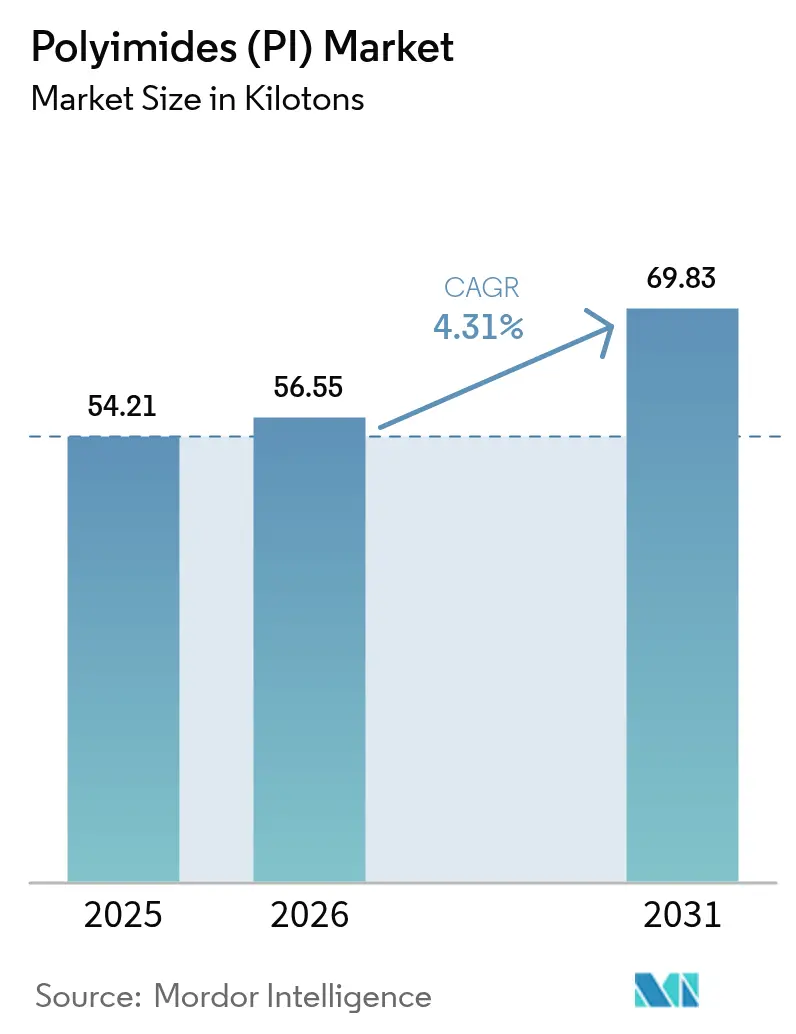

| Market Volume (2026) | 56.55 kilotons |

| Market Volume (2031) | 69.83 kilotons |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyimides (PI) Market Analysis by Mordor Intelligence

The Polyimides Market size was valued at 54.21 kilotons in 2025 and is estimated to grow from 56.55 kilotons in 2026 to reach 69.83 kilotons by 2031, at a CAGR of 4.31% during the forecast period (2026-2031). Mounting demand for flexible printed circuits in foldable smartphones, 800-volt electric-vehicle traction motors, and space-sector thermal shielding is reshaping material specifications toward melt-processable and colorless grades that lower processing costs and meet optical mandates. Regional capacity additions in China continue to erode price barriers, pushing polyimides into applications that once defaulted to polyesters or polyamides. Meanwhile, OEMs in aerospace, high-frequency 5G/6G electronics, and energy storage pay premiums for ultra-thin or composite films that withstand 260 °C operating envelopes and atomic-oxygen exposure. Together, these divergent needs are tilting the polyimides market toward a mixed volume-plus-value growth pattern in which specialty grades command rising revenue per kilogram.

Key Report Takeaways

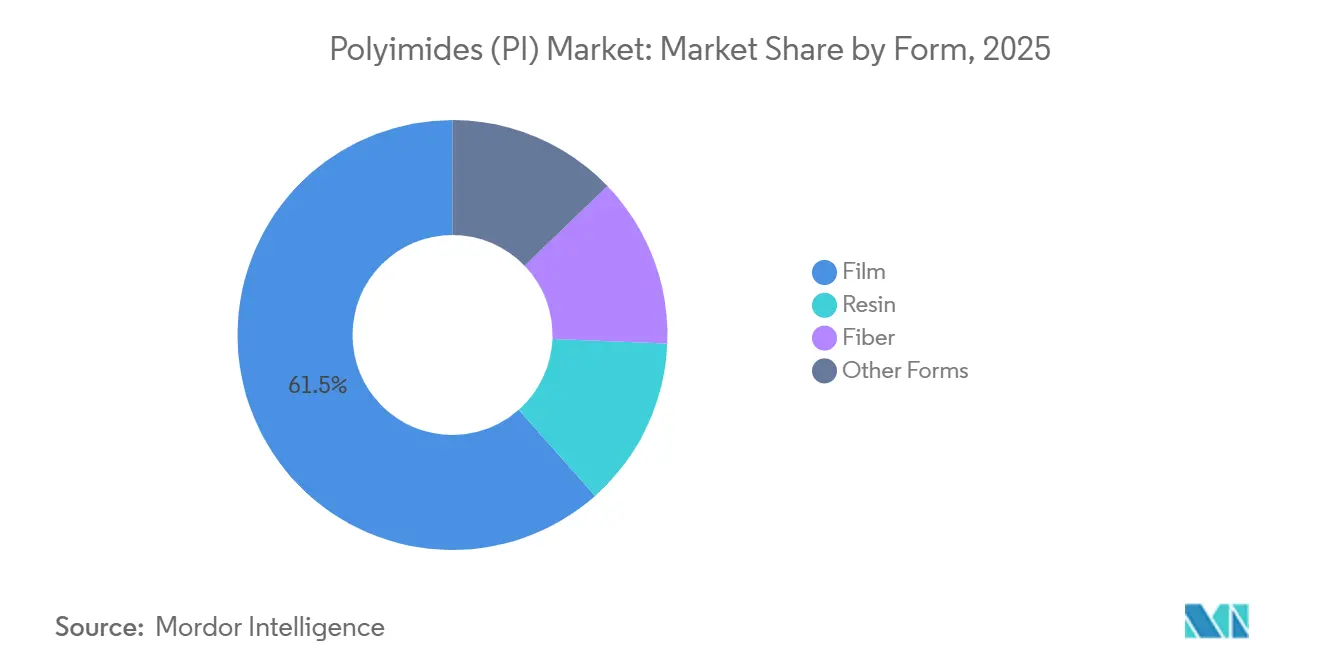

- By form, film led with 61.55% of polyimides market share in 2025 and is advancing at a 5.12% CAGR through 2031.

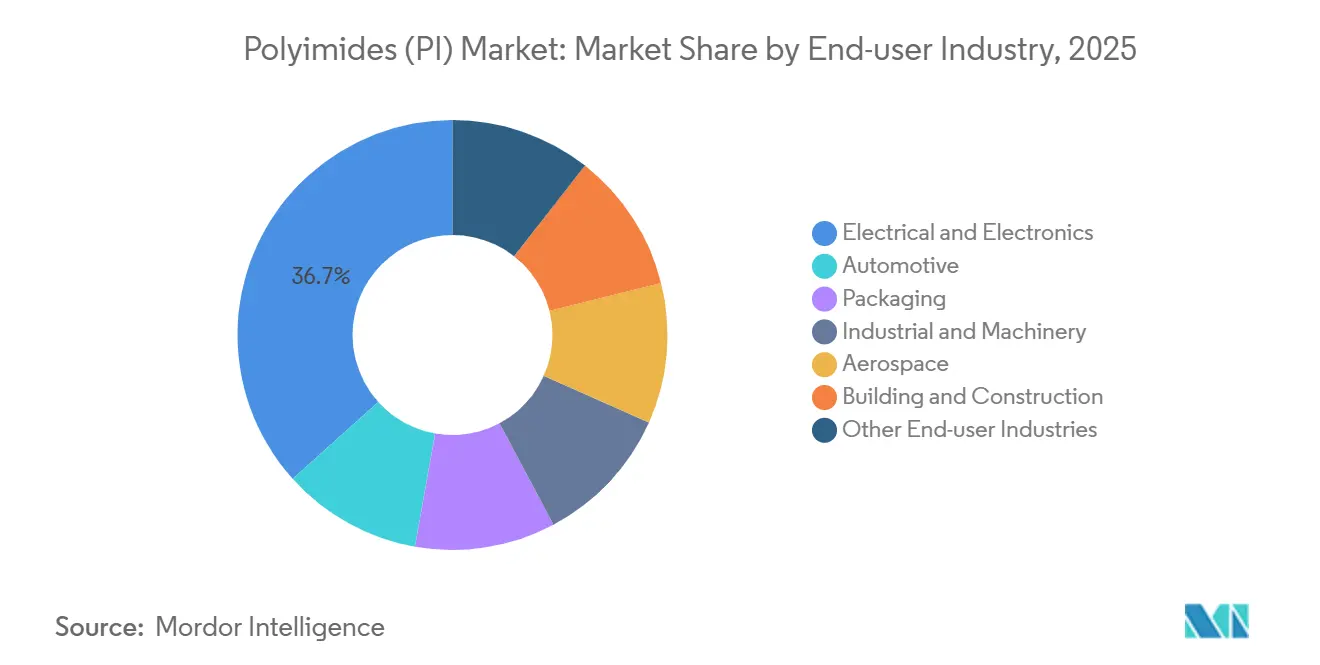

- By end-user industry, electrical and electronics captured 36.67% share of the polyimides market size in 2025, while the other end-user industries posts the fastest 5.20% CAGR to 2031.

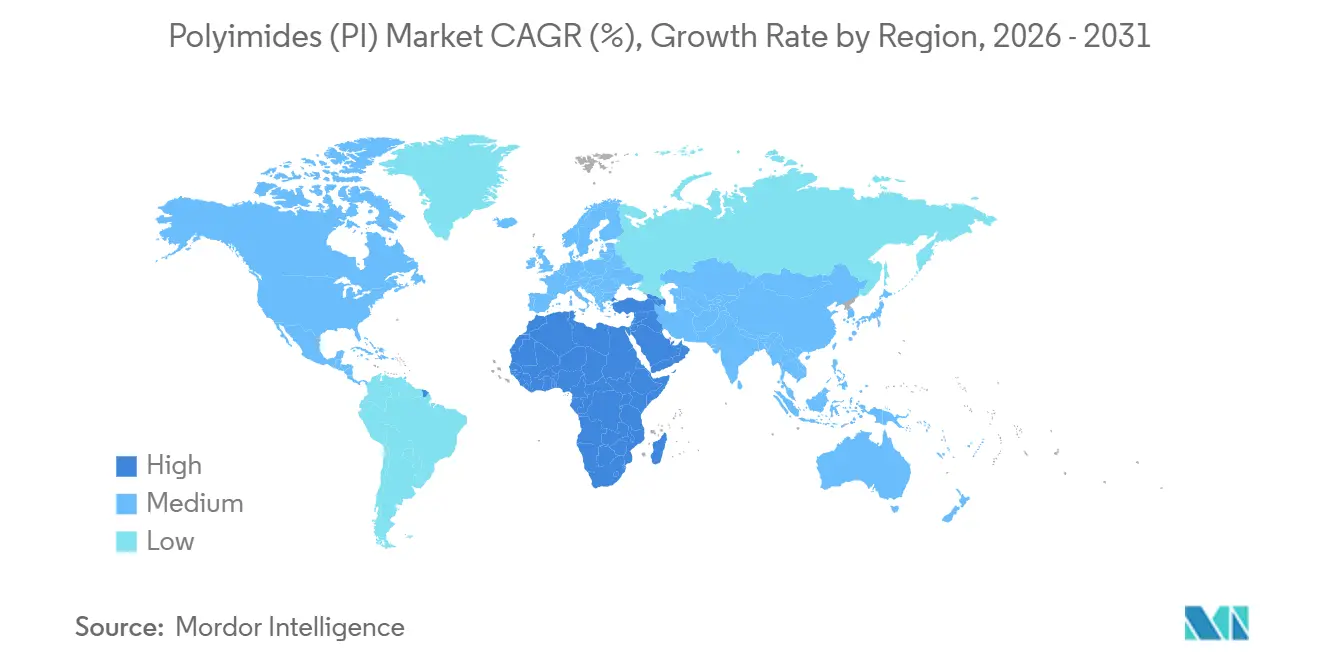

- By geography, Asia-Pacific held 40.61% of 2025 volume, whereas Middle-East and Africa is forecast to expand at 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyimides (PI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronics Miniaturisation and Foldable-Display Boom | +1.5% | Asia-Pacific core, spillover to North America | Short term (≤ 2 years) |

| EV High-Voltage Insulation Demand Surge | +1.2% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| 5G/6G High-Frequency PCB Adoption | +0.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| Space-Sector Lightweight Thermal Shielding Expansion | +0.4% | North America, Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| China-Led Capacity Additions Lowering Price Barriers | +0.9% | Global, originating in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electronics Miniaturization and Foldable-Display Boom

Foldable smartphones require substrates that survive repeated 180-degree bending at radii below 5 mm, a benchmark that only colorless polyimide films consistently hit. Eternal Materials’ 2024 contract with LG Display underscores how guaranteed supply underwrites rapid scale-up of foldable lines. Positive-tone photosensitive polyimide from Fujifilm trims lithography steps for OLED pixel patterning, boosting yield at Samsung fabs. Weight savings of 30-40% over glass substrates matter for wearable and in-car displays. As film thickness drops below 10 µm for chip-on-film drivers, handling losses rise, yet device makers accept the premium because no alternative provides the same bend radius and thermal budget.

EV High-Voltage Insulation Demand Surge

Traction motors operating at 800 V generate hot spots that exceed 200 °C, beyond polyester enamel thresholds; polyimide-varnished flat wire raises copper fill and motor efficiency by up to 10%[1]R. Smith, “High-Voltage EV Motor Insulation Needs,” SAE International, sae.org . DuPont’s new Vespel grade posts a 55 MPa·m/s PV limit, empowering gearbox downsizing in electric drivetrains. Hydrogen permeability 26 × lower than PEEK positions the resin for seals in fuel-cell vehicles. Slot liners and phase separators in lithium-ion packs now specify polyimide because it remains dimensionally stable from –40 °C to 150 °C and is inherently non-flammable, meeting automaker safety protocols.

5G/6G High-Frequency PCB Adoption

Millimeter-wave RF modules need substrates with dielectric constants under 3.0 and dissipation factors below 0.002 above 28 GHz. Kaneka’s Pixeo 1IB film hits those targets via backbone engineering, enabling conformal antenna arrays in smartphones and automotive radar units. IEEE testing in 2024 showed low-loss polyimides keep their dielectric profile from 25-330 GHz, aligning with nascent 6G terahertz bands. Infrastructure transition from 4G to 5G already lifted polyimide use per base station by 40%, and 6G prototypes are driving co-development efforts between material suppliers and RF-package foundries.

Space-Sector Lightweight Thermal Shielding Expansion

Low-Earth-orbit satellites encounter atomic-oxygen erosion that strips unprotected polyimide at roughly 3 µm per year. SmartMat research on ZnO/CuNi-reinforced films cut erosion yield to 2.29% of pristine polymer and resisted 353.4 dpa Fe⁺ irradiation. Omniseal’s Meldin brackets shave 20-30% launch mass versus aluminum. Polyimide-insulated harnesses meet AS50881 while saving 30% weight, critical for Mars rovers and next-gen satellites. NASA’s Perseverance and the ISS both rely on polyimide wiring that endures 260 °C spikes and cryogenic lows alike, validating mission-critical reliability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Dianhydride and Diamine Feedstock Pricing | -0.6% | Global, acute in non-integrated producers | Short term (≤ 2 years) |

| VOC-Emission Compliance Costs for Solvent Casting | -0.4% | Europe, North America, China | Medium term (2-4 years) |

| Processing Skill Gap Outside East Asia | -0.3% | North America, Europe, emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Dianhydride and Diamine Feedstock Pricing

Aromatic dianhydride and diamine prices swing 20-30% inside a quarter, and raw materials make up roughly 65% of film cost, leaving non-integrated producers exposed to margin shock. Longer-term supply contracts with price collars require scale that smaller players lack, reinforcing incumbent advantage. Two Asian outages during 2024 jacked up dianhydride quotes and forced reformulation or temporary yield sacrifice at several mid-tier film plants. Buyers increasingly insist on vertical-integration proof when awarding multiyear deals.

VOC-Emission Compliance Costs for Solvent Casting

Solvent-cast polyimide emits N-methyl-2-pyrrolidone and dimethylacetamide, both facing tighter caps under the EU Industrial Emissions Directive. Retrofitting one casting line with 95% solvent recovery can cost USD 5-15 million. Water-borne systems cut VOCs yet sacrifice high-temperature performance, limiting use to labels and low-stress insulation. Some producers are shifting lines to regions with laxer rules, raising supply-chain complexity for European OEMs that require local content.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Flexible Substrates Drive Miniaturization

Film dominated with 61.55% of polyimides market share in 2025 and is projected to capture 5.12% CAGR through 2031, outpacing the broader polyimides market as foldable displays and 5G flexible antennas proliferate. This leadership reflects superior bend radius, 15 W/m·K thermal conductivity sheets for xEV power modules, and viable sub-10 µm processing windows. Resin grades serve bearing cages and thrust washers where the polyimides market size for automotive drivetrains is expanding with electrification, thanks to a 55 MPa·m/s PV ceiling that beats alternative polymers.

Fiber captures aerospace filtration and flame-resistant fabrics, while foams and aerogels insulate cryogenic tanks on launch vehicles. Although these forms represent modest tonnage, their unit price vastly exceeds commodity film, buoying revenue. Producers integrate across multiple forms to leverage shared monomer streams and diversify risk. Film, however, remains the anchor for scale, dictating capacity-planning and feedstock contracts that ripple through every echelon of the polyimides market.

By End-user Industry: Electronics Anchor Volume, Niche Sectors Drive Value

Electrical and electronics held 36.67% of 2025 volume, using polyimide flexible circuits and chip-on-film packages in smartphones, laptops, and servers. Automotive polyimide demand is climbing as high-voltage insulation, battery separators, and turbo heat shields migrate away from polyester. Packaging remains small but rising: retort-sterilized food pouches need barrier films that tolerate 150 °C cycles, an arena where polyimides market size gains are modest yet profitable.

Other end-user industries—log the fastest 5.20% CAGR, reinforcing the performance-driven narrative. Melt-processable thermoplastic composites with boron-nitride fillers deliver a 276 °C glass-transition temperature and 110% thermal-conductivity lift, expanding aerospace electric-motor insulation options. Polyimide’s biocompatibility is attracting catheter and implant manufacturers that need radiation-sterilizable polymers. These high-specification opportunities underpin premium pricing even as commodity-film segments face margin pressure.

Geography Analysis

Asia-Pacific commanded 40.61% of 2025 volume as China, Japan, and South Korea house the densest cluster of flexible-circuit makers and semiconductor packagers. Recent JPY 16 billion capacity expansion by Asahi Kasei illustrates the sustained build-out in specialty photo-polyimides for foldable OLEDs. India and Malaysia are emerging nodes, bolstered by smartphone assembly incentives and auto-component hubs that require local polyimide sourcing.

North America trails in volume yet captures premium grade sales tied to NASA, commercial-space, and EV supply chains. Validation of Mitsui’s Aurum polyimide for 200 °C motor wiring solidifies the region’s role as a technology testbed. DuPont’s Circleville, Ohio, capacity increase underscores reshoring moves that aim to shorten lead times for EV battery customers. Still, the U.S. depends on Asian imports for ultra-thin photo-polyimide, necessitating strategic inventory buffers.

Europe balances strong automotive and aerospace demand with rigorous VOC regulations. Germany and France lead adoption in 800-V drivetrains and Airbus interior parts. The bloc’s push for bio-based and recyclable polymers could propel EU-origin innovations if performance parity is reached post-2028. Eastern-European converters are courting investment but lag in process know-how, perpetuating reliance on Japanese and Korean master rolls.

Competitive Landscape

The polyimides market sits in moderate concentration: DuPont, Toray, Kaneka, Arkema, and Kolon Industries together supply roughly 48% of global volume through vertical integration and long-standing OEM approvals. Backward ownership of dianhydride and diamine streams cushions feedstock shocks, an edge smaller rivals lack. Chinese entrants are scaling commodity film and improving yields on sub-10 µm formats, squeezing price but not yet matching aerospace-grade reliability.

Technology leadership now hinges on specialty moves. DuPont’s high-PV Vespel readies electric-vehicle gearboxes for downsizing, while Toray’s 15 W/m·K thermal-interface films answer xEV inverter heat-flux spikes[2]DuPont Materials Group, “Vespel High-PV Grade Datasheet,” dupont.com. Kaneka’s low-loss RF films and Mitsui’s melt-processable Aurum address 6G and spaceflight insulation. Start-ups chase recyclable or bio-based chemistries, claiming 94% material recovery via cleavable imine bonds, but must navigate multiyear aerospace and medical approvals.

Price competition is fiercest in flexible-circuit film, where lead-time and defect rate often trump brand. Aerospace and defense grades, by contrast, involve five-year qualification cycles and strict AS9100 audits, deterring new entrants. Service depth—design assistance, failure-analysis labs, rapid-sample lines—has become a differentiator as OEMs push for simultaneous engineering.

Polyimides (PI) Industry Leaders

DuPont

UBE Corporation

Kaneka Corporation

Arkema

Kolon Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Toray Industries Inc. developed a negative photo-definable polyimide sheet designed for glass core substrates. This material allowed for simultaneous microfabrication of layers and resin filling, reducing costs and streamlining processes.

- December 2024: PI Advanced Materials, an affiliate of Arkema, introduced the world's first 4 μm ultra-thin polyimide film. The film was designed for use in smartphones, tablets, and wearable devices, enhancing their slimness, heat resistance, and durability.

Global Polyimides (PI) Market Report Scope

Polyimides (PI) are a class of ultra-high-performance polymers characterized by the presence of imide groups (–CO–N–CO–) in their main chain. Renowned for their exceptional thermal stability and mechanical toughness, they are extensively used in challenging environments where conventional plastics are inadequate, such as spacecraft insulation and flexible electronics.

The polyimides (PI) market is segmented by form, end-user industry, and geography. By form, the market is segmented into film, resin, fiber, and other forms. By end-user industry, the market is segmented into automotive, electrical and electronics, packaging, industrial and machinery, aerospace, building and construction, and other end-user industries. The report also covers the market size and forecasts for polyimides (PI) in 20 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Film |

| Resin |

| Fiber |

| Other Forms |

| Electrical and Electronics |

| Automotive |

| Packaging |

| Industrial and Machinery |

| Aerospace |

| Building and Construction |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| Italy | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Film | |

| Resin | ||

| Fiber | ||

| Other Forms | ||

| By End-user Industry | Electrical and Electronics | |

| Automotive | ||

| Packaging | ||

| Industrial and Machinery | ||

| Aerospace | ||

| Building and Construction | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Market Definition

- End-user Industry - Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyimide market.

- Resin - Under the scope of the study, virgin thermosetting and thermoplastic polyimide resins in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms