Market Overview

| Study Period | 2021 - 2031 |

|---|---|

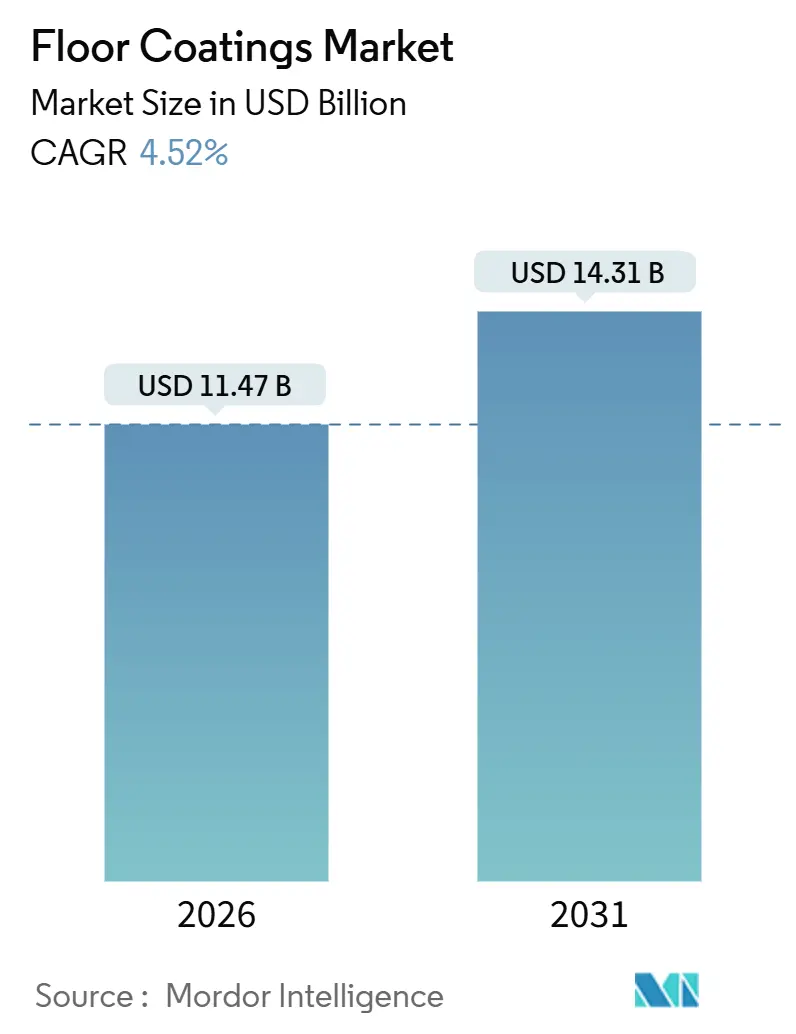

| Market Size (2026) | USD 11.47 Billion |

| Market Size (2031) | USD 14.31 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

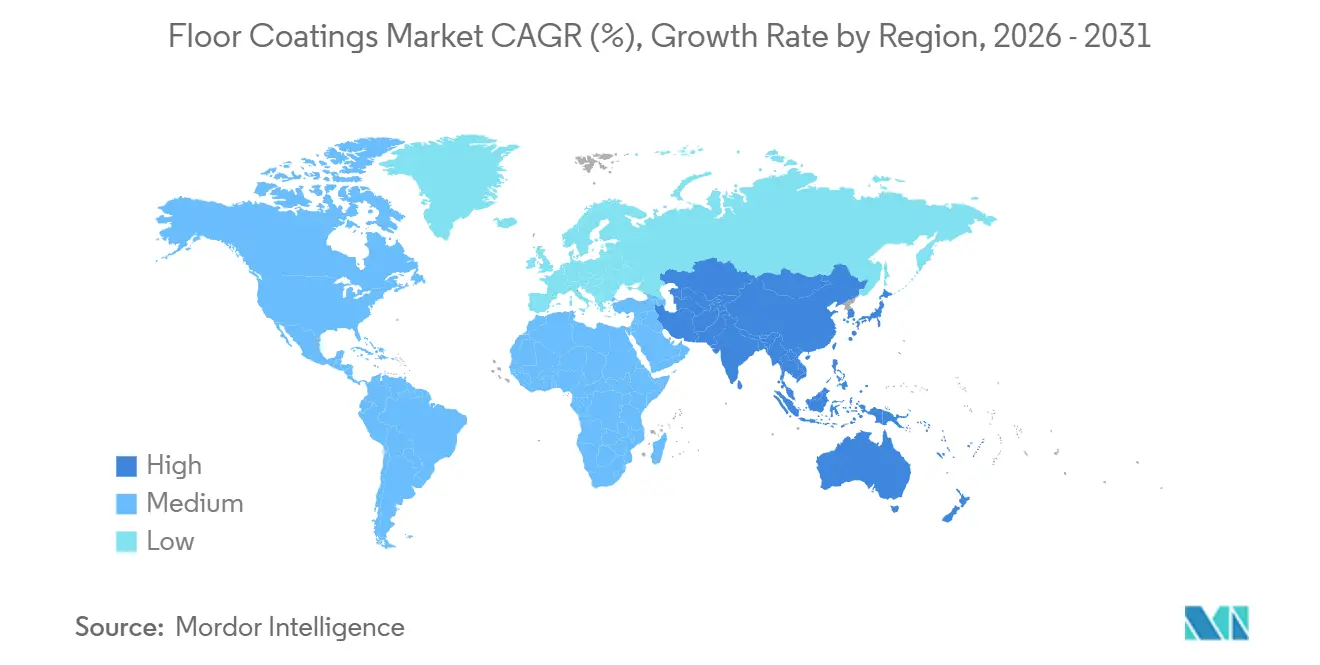

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

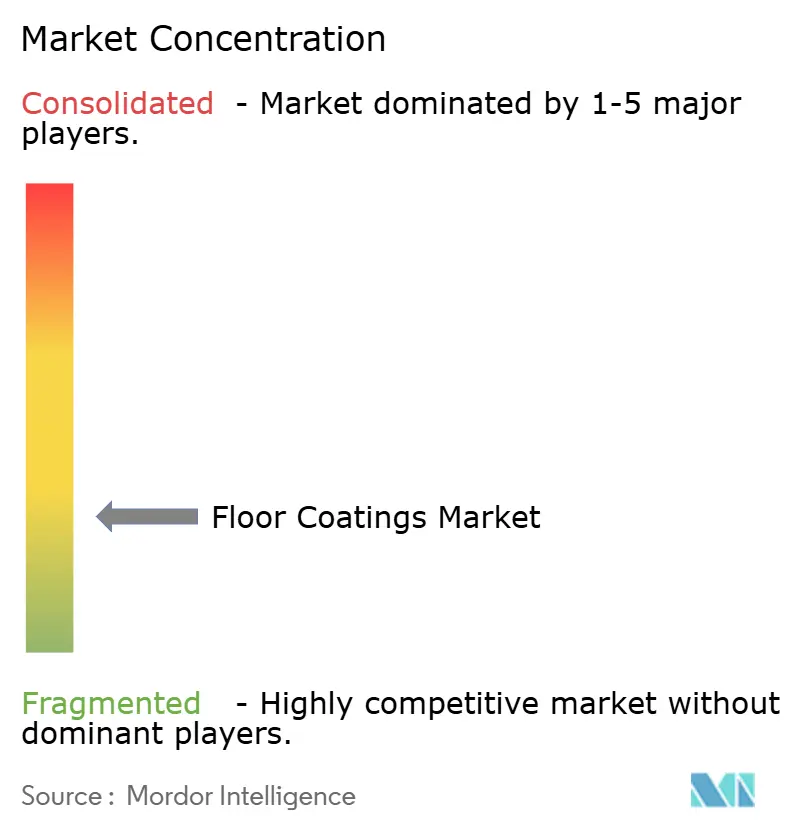

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Floor Coatings Market Analysis by Mordor Intelligence

The Floor Coatings Market size is estimated at USD 11.47 billion in 2026, and is expected to reach USD 14.31 billion by 2031, at a CAGR of 4.52% during the forecast period (2026-2031). Growth is fueled by rising demand for antimicrobial epoxy systems in cold-storage logistics, conductive floors in EV-battery gigafactories, and UV-cured formulations that minimize downtime in 24/7 production plants. Logistics real-estate development, aggressive clean-room standards across electronics and pharmaceuticals, and tightening VOC rules in Europe and the Nordics are steadily shifting specifications toward low-emission, high-performance chemistries. Simultaneously, raw-material cost swings and a persistent installer shortage are widening price spreads across regions, favoring suppliers with vertically integrated resin capacity and strong applicator networks. Competitive intensity remains high because regional specialists can gain share quickly by tailoring products to local regulatory and climatic conditions.

Key Report Takeaways

- By product type, epoxy commanded 50.15% revenue share of the floor coatings market in 2025, and is projected to expand at a 4.71% CAGR to 2031.

- By technology, UV-cured systems captured 35.22% share of the floor coatings market in 2025 and are projected to grow at a 4.82% CAGR through 2031.

- By floor material, concrete commanded 70.06% revenue share of the floor coatings market in 2025, and is forecast to expand at a 4.94% CAGR to 2031.

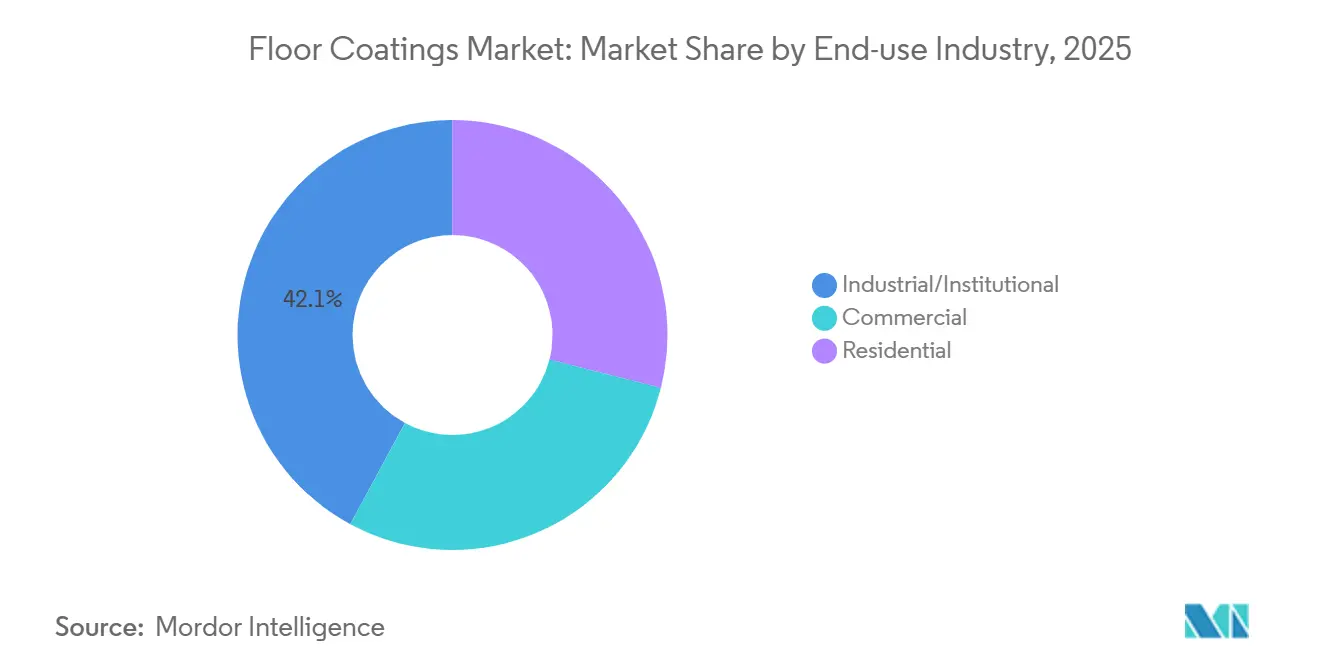

- By end-use industry, the industrial/institutional segment held 42.12% of the floor coatings market size in 2025 and is advancing at a 4.63% CAGR to 2031.

- By geography, Asia Pacific accounted for 38.27% of the floor coatings market share in 2025 and is projected to grow at a 4.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Floor Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of cold-storage warehousing needing antimicrobial coatings | +0.8% | North America, Europe, APAC cold-chain hubs | Medium term (2-4 years) |

| E-commerce fulfillment centers boosting abrasion-resistant epoxies | +1.1% | North America and APAC, spillover to MEA | Short term (≤ 2 years) |

| Renovation boom in multifamily housing driving decorative polyaspartics | +0.6% | Urban North America and Europe | Medium term (2-4 years) |

| Antistatic mandates in EV-battery gigafactories stimulating conductive floors | +0.7% | China, South Korea, Indonesia, Europe, North America | Long term (≥ 4 years) |

| Government incentives for VOC-free water-borne systems in Nordics | +0.4% | Sweden, Norway, Denmark, Finland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Cold-Storage Warehousing Needing Antimicrobial Coatings

Cold-storage operators specify antimicrobial epoxies that withstand freeze-thaw cycling and high-pressure washdowns. Jotun’s Jotafloor Hygiene achieves a 99.9% bacterial reduction within 24 hours, aligning with FDA Food Code §3-304.14 on non-porous, cleanable surfaces[1]Jotun Technical Team, “Jotafloor Hygiene Performance Data,” jotun.com. Flowcrete’s Flowfresh polyurethane embeds silver-ion biocides that remain active for the life of the floor, satisfying USDA 9 CFR Part 416 on moisture-impervious construction. Regulatory audits under the Global Food Safety Initiative have accelerated the replacement of legacy floors installed before 2020 that lack integrated antimicrobial agents, thereby shortening recoating cycles. The trend is global but most pronounced in North American and European distribution hubs where grocery retailers pledge to expand chilled capacity. As consolidation in cold-chain logistics continues, single operators increasingly award multi-site coating contracts, favoring suppliers with large geographic service networks.

E-Commerce Fulfillment Centers Boosting Abrasion-Resistant Epoxies

Fulfillment centers expose floors to forklift traffic exceeding 10,000 cycles per day, automated guided vehicles, and robotic sorters that generate concentrated loads above 5,000 psi. Epoxy systems formulated with novolac resins and aggregate hardeners deliver compressive strengths above 10,000 psi, preventing delamination under repetitive impacts. Sherwin-Williams’ Macropoxy 646 Fast Cure Epoxy reaches full cure in 16 hours at 70°F, allowing phased installations without shutting down active aisles. As online retailers regionalize inventory to cut delivery times, new warehouses and retrofits demand quick-turn coatings that minimize lost operational hours. The Asian Development Bank projects 4.9% GDP growth for developing Asia in 2025, supporting logistics infrastructure expansion. Short-cycle economic fluctuations have not altered long-range commitments to automation and high-throughput flooring standards.

Renovation Boom in Multifamily Housing Driving Decorative Polyaspartics

Polyaspartic coatings cure at temperatures as low as -20°F and exhibit superior UV stability, making them ideal for balconies, corridors, and amenity spaces in multifamily buildings. The White House allocated USD 10 billion in Community Development Block Grants for commercial-to-residential conversions, unlocking projects that require low-odor, same-day-return-to-service coatings. Flexmar Polyaspartics reach tack-free status in 30 minutes, enabling contractors to limit tenant disruption. More than 400,000 multifamily units were delivered in 2024, many specifying decorative polyaspartics that replicate terrazzo aesthetics at lower installed cost. Architects now integrate floor-finish decisions earlier in project schedules to secure installers during persistent labor shortages. The American Institute of Architects anticipates nonresidential construction spending to rise 2% in 2025, sustaining renovation momentum.

Antistatic Mandates in EV-Battery Gigafactories Stimulating Conductive Floors

Lithium-ion cell assembly requires electrostatic discharge floors with surface resistivity between 1×10⁶ and 1×10⁹ ohms per square to avoid ignition of flammable electrolytes. Sherwin-Williams’ Perma-Crete ESD Urethane meets this range while resisting N-methyl-2-pyrrolidone, a solvent common in electrode production. Sika’s Sikafloor-2530 W conductive epoxy embeds carbon nanotubes, eliminating copper grounding strips and cutting installation labor by around 20%. ASEAN countries attracted roughly USD 12 billion per year in semiconductor and electronics greenfield investment between 2021 and 2024, much of it earmarked for battery components. National industrial policies in Indonesia, Malaysia, Thailand, and Vietnam incentivize local floor-coating supply, prompting multinational formulators to build regional production capacity. These investments support steady long-term demand for conductive coatings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.9% | Europe and North America | Short term (≤ 2 years) |

| Skilled-installer shortage in emerging economies | -0.5% | APAC, MEA, Latin America | Medium term (2-4 years) |

| PFAS bans limiting high-performance fluorinated top-coats | -0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Epoxy resin prices in Germany rose in January 2025, and the US suppliers posted an increase in the same month, largely due to tighter bisphenol-A availability and anti-dumping investigations on Chinese imports. Concurrent refinery maintenance lifted toluene costs, squeezing polyurethane margins. The US International Trade Commission has initiated provisional duties of 15-35% on imported epoxy, pushing distributors toward regional supply despite higher base prices. BASF’s carve-out of its coatings division to the Carlyle Group underscores how integrated producers are exiting lower-margin businesses, heightening exposure of downstream formulators to spot resin markets. Price swings drive purchasing managers to extend contracts and hold higher inventories, which ties up working capital and slows specification shifts toward next-generation chemistries.

Skilled-Installer Shortage in Emerging Economies

The National Association of Home Builders estimates the US homebuilding sector faces USD 10.8 billion in annual costs from labor shortages, delaying roughly 19,000 homes and associated floor installations[2]National Association of Home Builders, “2025 Housing Market Labor Survey,” nahb.org. Finish carpenters, an occupational group that includes floor installers, rank second in shortage severity, with 56% of builders reporting hiring difficulties. Emerging markets encounter even sharper gaps because vocational programs have not kept pace with construction pipelines. Saudi Arabia’s Vision 2030 megaprojects draw international contractors who compete for limited certified resinous-floor applicators, pushing labor inflation above general construction indices. Insufficient installer capacity lengthens project timelines and raises the risk of coating failure due to improper substrate preparation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Epoxy Dominance Anchored in Concrete Adhesion

Epoxy resins generated 50.15% of 2025 revenue and are forecast to expand at 4.71% to 2031. Pharmaceutical cleanrooms specify seamless epoxy to meet FDA 21 CFR §211.56 for hard, easily cleanable surfaces. Food-processing plants use similar systems to satisfy USDA FSIS 9 CFR Part 416 on moisture-impervious floors. Polyurethane earns a share in cold storage, where thermal-shock resistance prevents cracking. Decorative polyaspartic demand rises in multifamily refurbishments because same-day occupancy avoids tenant displacement penalties. Acrylic and methyl methacrylate variants remain niche for light-duty retail. The floor coatings market continues to favor epoxy because no alternative matches its cost-to-performance ratio for heavy-load environments, preserving the segment’s leadership through 2031.

Epoxy’s grip on the floor coatings market is also reinforced by extensive installer familiarity, a deep accessories ecosystem, and decades of published application guides. Innovations such as carbon-nanotube conductive fillers and antimicrobial additives extend the chemistry’s addressable end uses without raising complexity for contractors. Polyurethane formulators are responding with silver-ion antibacterial grades, but adoption is slower due to higher raw-material costs. Overall, resin competition will intensify around high-value formulations, yet the epoxy segment is well positioned to defend its 50% floor coatings market share.

By Technology: UV-Cured Systems Redefine Installation Economics

UV-cured coatings captured a 35.22% share in 2025 and will grow at 4.82% through 2031. Instant curing under LED lamps eliminates oven energy costs and supports ISO 14001 certification goals. Sherwin-Williams documents 99% curing efficiency, trimming energy use by up to 70% compared with thermal processes. Water-borne epoxies are accelerating in Europe as solvent taxes and VOC caps raise costs on traditional two-component systems. Teknos’ Teknofloor 7300, emitting just 25 g/L VOC, demonstrates that water-borne options can rival solvent-borne abrasion resistance. Powder coatings are limited to metal panels in data centers. The floor coatings market size tied to UV-cured and water-borne technologies will widen as public buyers require ecolabel compliance, particularly in the Nordics.

Production managers cite two factors for adopting UV-cure: elimination of extended shutdowns and predictable cure depth regardless of ambient humidity. Packaging lines, pharma fill-finish suites, and food bottling halls leverage those benefits to upgrade during weekend maintenance windows. Suppliers that bundle lamp systems with coatings capture incremental revenue. As LED prices fall, smaller job-shops can afford mobile UV units, expanding the addressable floor coatings industry customer base.

By Floor Material: Concrete’s 70% Share Reflects Industrial Construction Scale

Concrete substrates accounted for 70.06% of 2025 revenue and are set to grow at 4.94% through 2031. Asia drives the floor coatings market size tied to concrete; Asia Pacific manufacturing FDI reached USD 226 billion in 2024, with half directed to factory construction. International Concrete Repair Institute profiles ranging from CSP 3 to CSP 5 dominate preparation specifications, ensuring mechanical interlock. ASTM F2170 moisture testing at 40% slab depth is now standard in FDA-audited facilities. Shot-blasting and diamond grinding equipment vendors report double-digit sales growth because contractors cannot risk delamination on fast-track projects.

Wood floors occupy a smaller share in commercial interiors, where UV-cured polyurethanes provide scratch resistance. Metal raised floors supporting data centers rely on powder top-coats that dissipate static while releasing zero VOCs. Maintenance cycles differ: sealed concrete in warehouses may last 7–10 years, while decorative wood finishes often require touch-up every 3–5 years. As capital allocation favors concrete superstructures, coating suppliers align R&D toward crack-bridging, conductive, and antimicrobial enhancements specifically for this substrate.

By End-Use Industry: Industrial and Institutional Sectors Lead at 42% Share

Industrial and institutional facilities held 42.12% revenue in 2025 and will grow at 4.63% through 2031. EV-battery gigafactories, semiconductor fabs, and pharma plants mandate specialty floors that dissipate static, withstand solvents, and resist microbial growth, pushing average coating system value higher than in commercial settings. Healthcare operators adopt epoxy with coved bases to satisfy NIH guidelines on seamless, sanitizable surfaces. Clean-room-grade flooring remains a requirement in contract-manufacturing organizations serving global drug pipelines.

Commercial retail and hospitality emphasize aesthetics and rapid re-entry, favoring polyaspartic and acrylic chemistries. Residential demand is concentrated in North American and European multifamily conversions backed by federal or municipal incentives. Labor shortages in North America may slow installation rates but also raise margins for certified applicators. Overall, industrial and institutional projects will keep anchoring the floor coatings market because compliance costs deter substitution toward lower-priced materials.

Geography Analysis

Asia Pacific generated 38.27% of global revenue in 2025 and is forecast to grow at 4.78% through 2031. ASEAN attracted USD 226 billion of foreign direct investment in 2024, with half destined for manufacturing facilities that require industrial-grade flooring. China, India, Japan, and South Korea remain core contributors, while Indonesia, Malaysia, Thailand, and Vietnam emerge as battery-supply-chain hubs enforcing IEC 61340-5-1 standards. Data-center capacity in the sub-region climbed from 800 MW in 2019 to 1,700 MW in 2023, bolstering demand for raised-floor systems finished with powder or UV-cured coatings. Government incentives for local resin production are attracting multinational formulators who build plants in export-processing zones, ensuring proximity to end users.

North American demand is powered by new logistics facilities and high apartment renovation activity. Warehouse construction exceeded half of all commercial starts in 2023 and continues to outpace offices and retail. The White House’s USD 10 billion allocation for adaptive-reuse conversions adds a pipeline that values fast-cure, low-odor products. Skilled-labor deficits, however, stretch project timelines and increase the premium paid for unionized flooring crews. Canada mirrors US trends, with an added push toward low-carbon concrete substrates that require compatible water-borne or cementitious primers.

Europe undergoes a technology pivot as VOC limits tighten. Sweden terminated its exemption for solvent-rich coatings, Denmark applies a solvent tax, and the EU Decopaint Directive imposes 500 g/L caps on two-component systems. Public tenders increasingly favor Nordic Swan-certified products emitting fewer than 30 g/L VOC. Germany, France, and Italy promote energy-efficient production lines; consequently, UV-cure adoption accelerates in auto plants and packaging factories. Eastern European data-center builds add conductive raised-floor opportunities, but labor migration to Western Europe constrains local installer capacity.

The Middle East and Africa gain momentum from sovereign infrastructure programs. Saudi Vision 2030 funnels capital into megaprojects such as NEOM, whose 20,000 m³-per-day concrete output drives large-volume epoxy consumption. The International Monetary Fund projects Saudi GDP growth of 3.5% in 2025 and 3.9% in 2026, supporting sustained construction. United Arab Emirates, Nigeria, and Egypt diversify away from oil dependence with manufacturing free-zones that demand chemically resistant floors. Latin America’s growth is steadier; Brazil and Mexico modernize agro-processing plants using antimicrobial epoxies to comply with export inspection regimes.

Competitive Landscape

The Floor Coatings market is fragmented. Regional specialists win share by conforming to local VOC ceilings or by integrating antimicrobial and conductive additives tailored to niche regulatory needs. Marketing strategies stress sustainability credentials, such as EPDs (Environmental Product Declarations) and third-party ecolabels. Suppliers that can document cradle-to-gate carbon footprints below benchmark thresholds secure advantageous scoring in public tenders across Scandinavia and Western Europe.

Floor Coatings Industry Leaders

The Sherwin-Williams Company

PPG Industries Inc.

Sika AG

BASF

RPM International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DYCO, a coatings brand under the ICP Group, introduced DYCO Court & Floor. This new anti-slip coating is designed for both commercial and residential recreational surfaces, including porches, steps, and walkways.

- March 2025: BASF and Sika AG launched a new amine building block for curing epoxy resins, now commercially available as BASF’s Baxxodur EC 151. This product is made for flooring applications, including production plants, storage and assembly halls, and parking decks.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the floor coatings market covers all resin-based and cementitious finishes that are trowelled, rolled, or sprayed onto concrete, wood, and other hard substrates in industrial, commercial, and residential facilities to deliver abrasion resistance, chemical protection, and aesthetic upgrade. Products span epoxy, polyurethane, polyaspartic, acrylic, powder, UV-cured, and emerging bio-based chemistries applied as single, dual, or multi-component systems across new-build and refurbishment projects worldwide.

Scope exclusion: temporary wax polishes, carpet tiles, and sheet vinyl finishes fall outside the study.

Segmentation Overview

- By Product Type

- Epoxy

- Polyurethane

- Polyaspartic

- Acrylic

- Others

- By Technology

- Solvent-borne

- Water-borne

- Powder

- UV cured

- By Floor Material

- Concrete

- Wood

- Others

- By End-use Industry

- Industrial/Institutional

- Commercial

- Residential

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordic Countries

- Turkey

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We interviewed factory applicators, resin formulators, and building-materials distributors across Asia-Pacific, North America, Europe, and the Gulf to validate installed floor areas, cure time preferences, and price ladders. Follow-up surveys with facilities managers helped us verify replacement cycles and emerging demand for antimicrobial or ESD-safe coatings.

Desk Research

Our analysts collected macro and sector data from tier-1, publicly available sources such as the UN Comtrade trade codes for epoxy and polyurethane dispersions, U.S. Census construction spending tables, Eurostat building permit series, the American Coatings Association technical papers, and concrete flooring guidelines issued by the European Federation of National Industrial Flooring Associations. Company filings, investor decks, and reputable news flows retrieved through Dow Jones Factiva and D&B Hoovers supplied shipment volumes and average selling prices that baseline regional demand curves. Additional context on regulatory drivers (VOC caps, worker safety rules) was drawn from OSHA and ECHA notices. These references illustrate, not exhaust, the broader pool we used for triangulation.

Market-Sizing & Forecasting

A top-down and bottom-up blend anchors the model. We first rebuilt global coated floor area by overlaying new industrial floor space additions, warehouse completions, and renovation ratios onto regional construction statistics, and then multiplied these footprints by typical wet-film build rates to derive volume demand. Supplier roll-ups and sampled ASP × volume checks supplied a bottom-up sense check that closes material gaps. Key variables include epoxy resin price indices, industrial capacity utilization, e-commerce warehouse stock, concrete repair cycles, and VOC regulation milestones. Multivariate regression on these drivers shapes the 2025-2030 outlook, while scenario analysis tests high inflation and rapid urbanization cases. Where distributor data were thin, channel checks filled the gap before final reconciliation.

Data Validation & Update Cycle

Model outputs pass a three-layer review that flags variance against historical trade flows, producer revenues, and installation crew hours. Anomalies trigger re-contact of sources. Reports refresh annually, with mid-cycle updates when raw material shocks or regulatory shifts materially change assumptions. Before release, a fresh analyst pass ensures clients receive the latest view.

Why Mordor's Floor Coatings Baseline Commands Reliability

Published estimates differ. Definitions shift, price decks vary, and refresh cadences drift, so headline numbers rarely align. We acknowledge those realities upfront.

Key gap drivers include narrower resin scopes used by some publishers, exclusion of refurbishment demand, limited country rolls, currency mix choices, and older base years. Mordor's broader chemistry coverage, yearly refresh, and validated ASP curves temper extremes and offer a balanced midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.98 B (2025) | Mordor Intelligence | - |

| USD 3.42 B (2024) | Global Consultancy A | Counts only epoxy and polyurethane, omits decorative overlays, 42-country scope |

| USD 4.50 B (2024) | Trade Journal B | Uses 2020 demand base then linear growth, limited installer interviews |

| USD 2.69 B (2019) | Industry Analytics C | Older base year and excludes water-borne technologies |

In sum, variations stem less from "right or wrong" calculations than from what each firm chooses to count. By pairing a transparent scope with disciplined variable selection, Mordor Intelligence delivers a dependable baseline that decision-makers can trace, replicate, and confidently build upon.

Key Questions Answered in the Report

What is the current value of the floor coatings market?

The floor coatings market size is valued at USD 11.47 billion in 2026.

How fast is demand for floor coatings expected to grow?

Revenue is projected to reach USD 14.31 billion by 2031, reflecting a 4.52% CAGR over the forecast period.

Which product type leads global sales?

Epoxy resins hold the top position, capturing 50.15% of 2025 revenue due to superior adhesion and chemical resistance.

Why are UV-cured floor coatings gaining popularity?

They cure instantly under LED lamps, cutting plant downtime and meeting strict VOC limits without ovens, enabling faster project turnaround.

Which region represents the largest opportunity?

Asia Pacific, already generating 38.27% of global revenue, benefits from heavy manufacturing FDI and is forecast to expand at 4.78% through 2031.

Page last updated on: