Flare Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flare Monitoring Market Analysis by Mordor Intelligence

The flare monitoring market size is expected to grow from USD 1.07 billion in 2025 to USD 1.13 billion in 2026 and is forecast to reach USD 1.49 billion by 2031 at 5.65% CAGR over 2026-2031. This growth trajectory is underpinned by tightening environmental regulations such as the U.S. EPA NSPS OOOOb methane rules and the widening reach of the EU Emissions Trading System, both of which reward precise emissions reporting. Operators are responding by integrating continuous monitoring to avoid carbon liabilities and to unlock operational efficiencies that can cut fuel loss. Investments in LNG export terminals, refinery expansions in Asia, and digital twin deployments offshore are also expanding the installed base. Meanwhile, AI-enabled video analytics and edge-connected sensors reduce downtime and improve combustion efficiency, making compliance more cost-effective and automated.

Key Report Takeaways

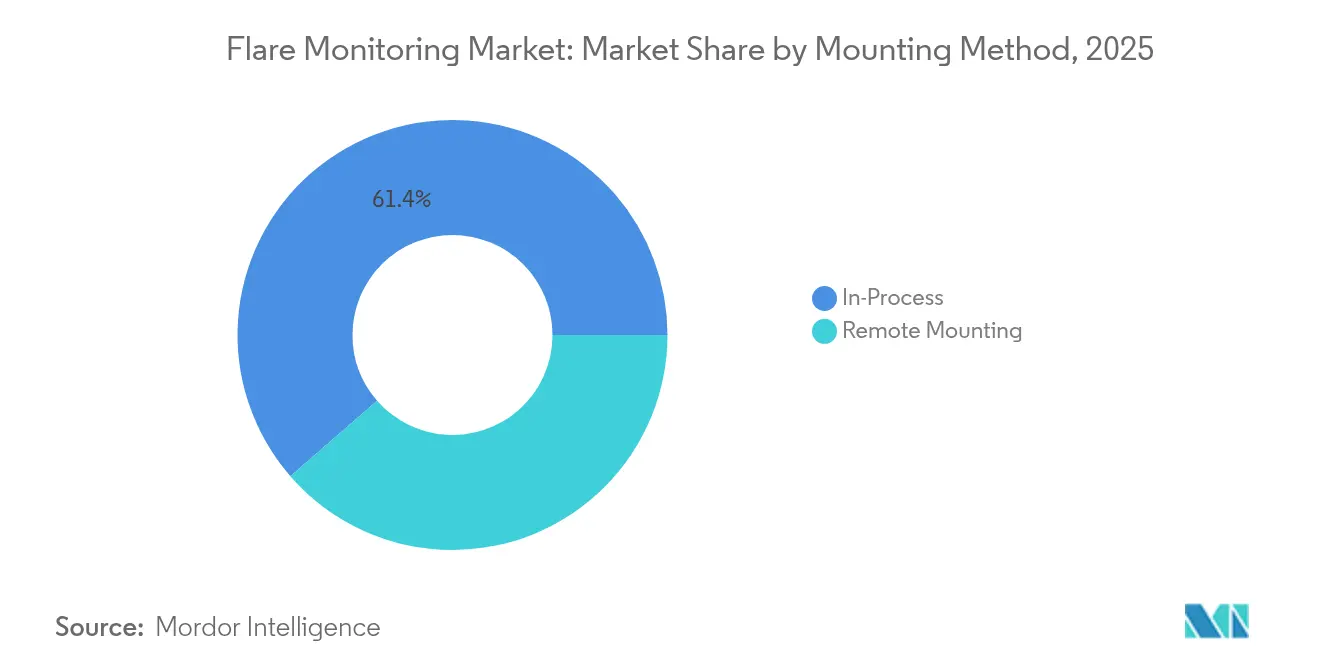

- By mounting method, in-process systems held 61.40% revenue share in 2025, while remote mounting posted the fastest CAGR at 6.05% through 2031.

- By component, hardware dominated the flare monitoring market with a 73.10% market share in 2025; services are forecast to grow the fastest at 6.85% CAGR by 2031.

- By installation type, onshore facilities accounted for 57.20% share of the flare monitoring market size in 2025, yet offshore installations are on track for a 6.25% CAGR to 2031.

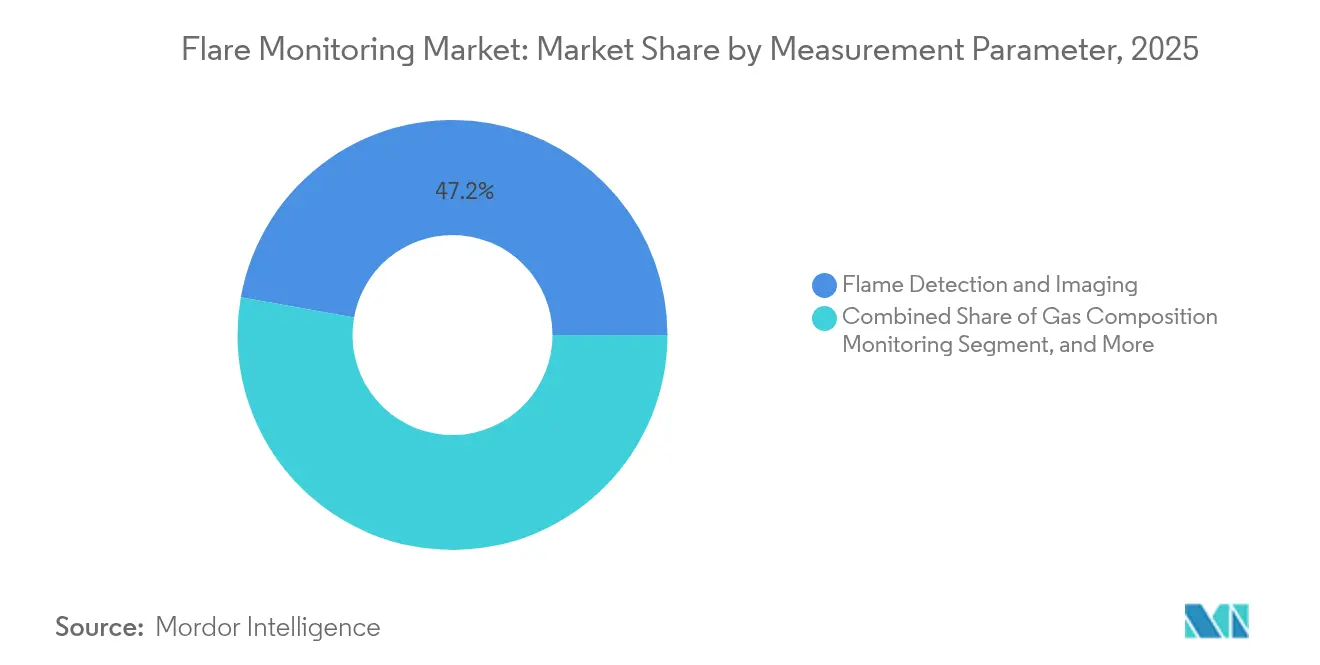

- By measurement parameter, flame detection and imaging led with 47.20% share in 2025, whereas gas-composition monitoring is expected to expand at 7.95% CAGR to 2031.

- By end-user, oil refineries captured 39.60% of the flare monitoring market share in 2025; upstream offshore operations are projected to surge at 6.95% CAGR through 2031.

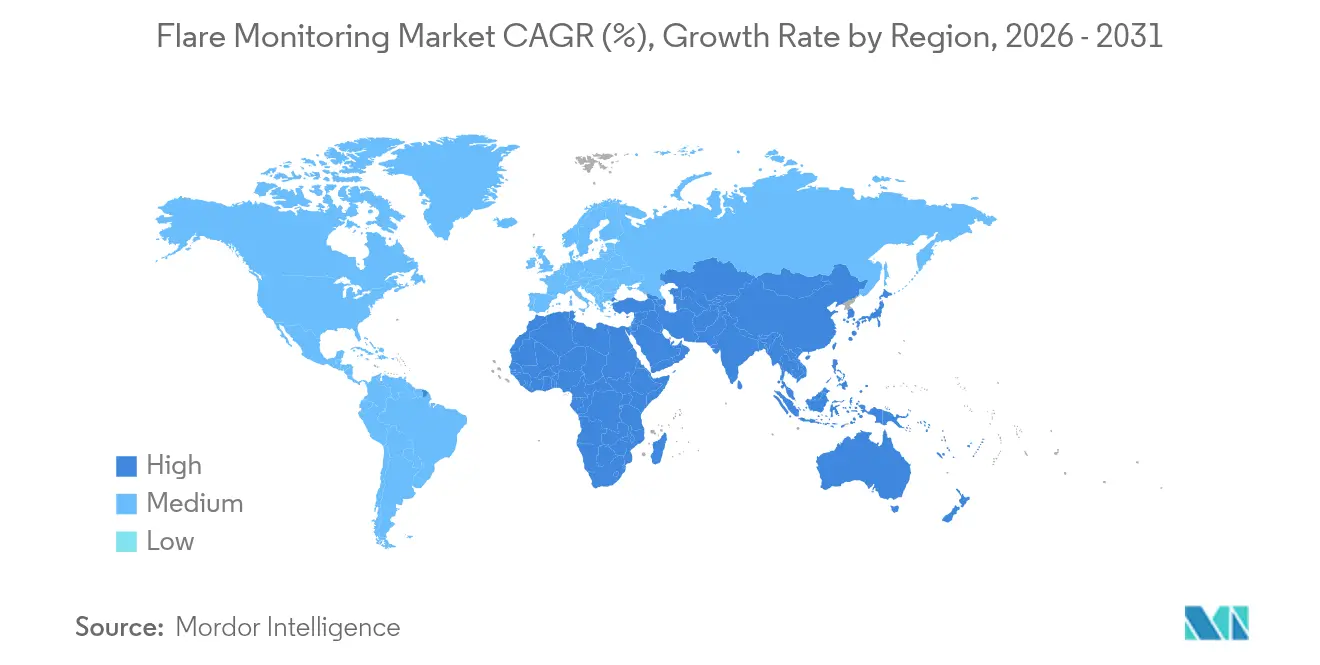

- By geography, North America led with 33.90% share in 2025, while Asia-Pacific is set to record a 6.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flare Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon-pricing schemes in Canada & EU ETS | +1.20% | North America and EU | Medium term (2-4 years) |

| AI-enabled video analytics | +0.80% | Global | Short term (≤ 2 years) |

| Shale-driven EPA Quad Oa monitoring (US) | +1.50% | North America | Short term (≤ 2 years) |

| Flare-gas capture incentives by Middle-East NOCs | +0.70% | Middle East and Africa | Medium term (2-4 years) |

| Rapid LNG export-terminal build-out | +1.10% | North America and Asia-Pacific | Medium term (2-4 years) |

| Digital-twin remote operations offshore | +0.40% | Global, offshore focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Implementation of Carbon-Pricing Schemes in Canada and EU ETS

Mandatory carbon fees convert accurate flare data into direct cost savings. The EU ETS trimmed emissions from covered sites by 16.5% in 2023, sustaining price signals that favor robust measurement climate. [1]Directorate-General for Climate Action, “2024 Carbon Market Report,” climate.ec.europa.eu Canada’s federal carbon price parallels that incentive, and the upcoming ETS2 expansion will extend fees to transport and buildings. With more assets falling under capped systems, operators increasingly view precise flare metrics as a hedge against escalating liabilities, stimulating procurement across the flare monitoring market.

AI-Enabled Video Analytics to Optimise Combustion Efficiency

Edge-deployed machine learning detects poor combustion within milliseconds, allowing real-time valve adjustments that raise flare destruction efficiency and trim fuel gas use. Honeywell’s suite demonstrates double-digit gains in worker productivity when AI supports monitoring workloads. [2]Honeywell, “Honeywell To Power Energy Sector With New Artificial Intelligence Solutions,” honeywell.com As offshore assets funnel 10 TB/day of video and sensor data, automated analytics turn that stream into actionable insights, underpinning predictive maintenance and safer operating envelopes.

Shale-Driven Tight-Oil Growth Mandating EPA Quad Oa Compliance (US)

Super-emitter provisions now obligate every basin producer to investigate methane spikes above 100 kg/h and to file third-party-verified reports within 15 days. [3]U.S. Environmental Protection Agency, “Small Entity Compliance Guide for Oil and Natural Gas Sector: Subpart OOOOb,” epa.govThe distributed nature of shale, with thousands of pads spread across a wide geography, amplifies the demand for scalable, remote-mount solutions that integrate seamlessly into existing SCADA systems. Avoiding the new Methane Waste Emission Charge hinges on deploying certified flare sensors, thereby directly expanding the flare monitoring market.

Flare-Gas Capture Incentives by Middle-East NOCs

Saudi Aramco’s USD 25 billion Jafurah build-out and near-zero routine flaring benchmark compel continuous verification systems to track captured volumes. ADNOC’s CCS projects likewise rely on high-resolution flare data to document sequestration gains. These programs transform monitoring from compliance overhead into a profit center that maximizes sales of previously wasted gas, nurturing regional demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retrofit costs for brown-field SE-Asia refineries | -0.60% | Southeast Asia | Medium term (2-4 years) |

| Data-latency & cyber-security limits offshore | -0.40% | Global, offshore focus | Short term (≤ 2 years) |

| Measurement uncertainty in methane-slip | -0.30% | Global | Long term (≥ 4 years) |

| Zero-routine-flaring 2030 pledges | -0.80% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retrofit Cost for Brown-Field Refineries in SE Asia

Projects such as Vietnam’s Dung Quat upgrade require multi-million-dollar piping and electrical modifications before sensors can be mounted. Smaller operators face cash-flow hurdles and elect phased installations that stretch timelines, muting near-term uptake across the flare monitoring market.

Data-Latency and Cyber-Security Limitations on Remote Platforms

Maritime OT infrastructure lags behind modern IT standards, increasing vulnerability to ransomware and limiting real-time data speed. The 2021 Colonial Pipeline incident highlighted financial exposure; consequently, some offshore operators throttle bandwidth or isolate networks, which undermines instantaneous analytics and tempers growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mounting Method: Remote Technologies Gaining Momentum

In-process mounting systems controlled 61.40% of the flare monitoring market in 2025 thanks to embedded gas analyzers that feed refinery DCS platforms for instant compliance reporting. Remote-mount optics are gaining traction because they eliminate the need for scaffolding, cable trays, and hot-work permits, allowing brownfield assets to add continuous surveillance with minimal downtime. Saudi Aramco’s Marjan GOSP-4 pilot streams infrared imagery into a cloud twin that supervisors can open from any control room. The savings from avoided mobility rounds and faster anomaly detection now outweigh the capital premium for hardened multi-spectrum lenses.

Remote solutions are expanding at a 6.05% CAGR and will lift their contribution to the overall flare monitoring market size when new LNG terminals finish commissioning in 2028. UV-IR cameras, drone-mounted gas imagers, and acoustic detectors now connect through wireless mesh nodes rated for Class 1/Division 2 areas. That architecture supports unmanned facilities in shale plays, reducing travel emissions while maintaining real-time visibility into every stack. Because operators can verify pilot flames and combustion indices without setting foot on site, the flare monitoring market is expected to see remote systems transition from niche to mainstream by the end of the decade.

By Component: Services Segment Accelerating Growth

Hardware-cameras, pyrometers, ultrasonic meters-delivered 73.10% of 2025 revenue, but its dominance is eroding as customers seek turnkey compliance. The services stream logs the fastest 6.85% CAGR, riding demand for lifecycle calibration, AI algorithm tuning, and quarterly reporting that satisfies voluntary methane-intensity scorecards. Baker Hughes’ flare. The IQ rollout across 65 bp sites offers a blueprint. Sensors feed a cloud engine that emails root-cause diagnostics to site leads within minutes of an efficiency slip.

Under outcome-based contracts, integrators guarantee uptime and regulatory filing accuracy, turning the flare monitoring market into a recurring-revenue engine. Firmware updates now push new neural-network models straight to edge devices, so performance improves without metal replacement. As a result, the flare monitoring market size for services is expected to surpass USD 472.6 million by 2031, while hardware revenue is projected to remain relatively stable.

By Installation Type: Offshore Segment Driving Innovation

Onshore plants still held 57.20% of flare monitoring market share in 2025 because refinery clusters on the U.S. Gulf Coast and East China Plain run multiple stacks side by side. Offshore production hubs, however, are expanding at 6.25% CAGR as methane slip in shallow-water flares reaches 23–66%, a range that draws investor scrutiny. Noble’s Energy Efficiency Insights tool now tracks diesel burn, generator load, and flare destruction efficiency across its drillship fleet, cutting fuel cost and greenhouse-gas intensity in one move.

Harsh sea spray, vibration, and corrosion force vendors to ruggedize housings, add redundant fiber loops, and embed AI at the edge to overcome satellite latency. Digital-twin dashboards let shore-based specialists overlay flare KPIs onto topside 3-D models, saving helicopter trips while meeting class-society audit rules. These advances will raise offshore installations’ slice of flare monitoring market size through 2031, especially as Brazil and Guyana sanction new FPSOs that require Tier III combustion monitoring from day one.

By Measurement Parameter: Gas Composition Monitoring Emerging

Flame detection and imaging accounted for 47.20% of 2025 revenue, as safety rules still require visible confirmation of pilot lights and smoke. The fastest rising parameter, gas-composition monitoring, is projected to expand at an 7.95% CAGR, as regulators shift from volume-only reporting to component-level disclosure. SLB’s easy-install methane meter clamps to a line in under two hours yet records parts-per-million accuracy, allowing continuous reconciliation with reported flare recovery.

Real-time speciation enables operators to tune air-to-fuel ratios, thereby curbing soot while maximizing destruction efficiency. Laser-based spectroscopy, Fourier-transform infrared (FT-IR) cells, and tunable diode arrays are now integrated into a single skid that auto-calibrates with every shift. As carbon taxation expands, compositional analytics transform flare readings into a “fiscal” signal that prevents overpaying on methane charges, thereby increasing this segment’s share of the overall flare monitoring market size.

By End-User: Upstream Offshore Leading Growth

Oil refineries captured 39.60% of 2025 demand, buoyed by Tier III fuel rules and the requirement to certify flare performance during every major turnaround. Upstream offshore operations hold the steepest growth curve at 6.95% CAGR because deep-water developments require remote diagnostics capable of flagging leaks under varying wind vectors. Aker BP’s Yggdrasil field folds flare data into reservoir models, showing how production engineers now co-opt environmental data for process optimization.

LNG liquefaction trains, petrochemical crackers, and even landfill-gas plants round out adoption. Each faces corporate-level ESG audits that rank methane intensity against peers. Here, a central analytics cockpit aggregates feeds from hundreds of flare stacks worldwide, comparing combustion slip in real time. With investors penalizing any facility with outlier emissions, the flare monitoring market sees multi-industry uptake accelerating across the back half of the forecast window.

Geography Analysis

North America led the flare monitoring market with 33.90% share in 2025, bolstered by the EPA’s super-emitter rule and LNG export capacity poised to rise from 11.4 Bcf/d to 24.3 Bcf/d by 2027. U.S. shale pads in the Permian and Haynesville deploy networked imagers that relay alerts within minutes, while Canada’s carbon fee amplifies ROI on accurate metering. Mexico’s Pacific Coast LNG ventures add incremental demand as they seek U.S.-grade compliance to satisfy Asian offtakers.

Europe sits in second place, its market defined by the EU ETS and a 16.5% drop in covered emissions during 2023. North Sea operators retrofit electrified platforms that rely on high-resolution flare data to validate the gains from electrification. Germany’s downstream sector and the U.K.’s mature fields both favor integrated hardware-software suites to streamline annual EU MRV audits.

Asia-Pacific is the fastest-growing territory at 6.15% CAGR to 2031. China’s carbon-neutral pledge drives large-scale refinery revamps that embed automated flaring dashboards. India’s public refiner expansions and Vietnam’s 30% capacity bump at Dung Quat increase tender flow for turnkey solutions. Japan and South Korea, armed with advanced sensor OEMs, serve as technology testbeds before broader regional rollouts. Collectively, these investments ensure the region’s contribution to flare monitoring market size will keep edging upward.

Regulatory Landscape

Regulation is tightening around measurement and documentation of flare-related emissions, which is raising the role of continuous monitoring. In the United States, the EPA updated oil and gas sector requirements on April 9, 2026 through amendments to NSPS and Emission Guidelines for Subparts OOOOb/OOOOc, including adjustments to vent gas net heating value (NHV) monitoring requirements for flares and enclosed combustion devices. The revisions also extended the compliance date for NHV monitoring to June 1, 2026, with initial annual report submissions due by November 30, 2026. This creates a clear near-term compliance milestone for auditable monitoring systems.

In Europe, methane-specific rules add another layer to carbon-pricing mechanisms. EU Regulation 2024/1787 mandates methane measurement, monitoring, reporting, and verification (MRV) requirements, and it prohibits routine flaring and venting applicable from February 5, 2026. The regulation requires prompt notification of major flaring events and annual reporting on flaring activities, increasing demand for systems that generate traceable, verification-ready data for regulators and third-party reviewers.

Value Chain Analysis

The flare monitoring value chain starts with core sensing and measurement technologies, including optical and infrared imaging (UV-IR and multispectral IR), ultrasonic flow meters, calorimeters, gas chromatographs, mass spectrometers, and supporting transmitters and industrial edge hardware. These inputs are combined into monitoring architectures that align with parameters emphasized in compliance frameworks, such as vent gas NHV, flare tip velocity, and inlet flow for combustion assurance, and then deliver validated signals into plant DCS/SCADA, historians, and reporting tools. EPA-recognized methods such as OTM-56, which uses Video Imaging Spectral Radiometer (VISR) technology for continuous autonomous monitoring of flare NHV, reinforce demand for integrated hardware and software rather than periodic manual sampling.

Downstream, systems integrators and OEMs bundle installation, calibration, and ongoing services, including quality control programs, monitoring plans, and audit support, that operators need to maintain continuous parameter monitoring systems. The ecosystem is also expanding with digital layers that turn raw sensor streams into compliance-grade evidence and operational workflows, including edge analytics for real-time combustion efficiency and destruction or removal efficiency calculations tied to standardized reporting requirements (for example, OGMP 2.0 Level 4 reporting practices). Procurement increasingly evaluates the full chain, from certified measurement capability through secure data transport and defensible reporting, because reporting timetables and audit readiness are now central to total cost of ownership.

Competitive Landscape

The competitive arena is moderately fragmented. ABB, Siemens, Honeywell, and Emerson integrate DCS platforms with multispectral imagers and IIoT gateways to secure customer loyalty. Honeywell’s January 2025 Emissions Management Suite rollout for marine and offshore zones exemplifies product tailoring for niche environments automation. Siemens counters with AI-driven edge firmware that is embedded directly in networked cameras, thereby lowering latency.

Specialists such as Baker Hughes and SLB target pain points, namely methane analytics and easy-install hardware. Baker Hughes’ flare.IQ's collaboration with BP encompasses 65 flares across seven regions, illustrating the scale of their partnership through service contracts. SLB’s May 2024 clamp-on meters cut install time to hours, enticing fast-track LNG builders. Consolidation is underway; CECO Environmental’s USD 122.7 million acquisition of Profire Energy augments burner management alongside emissions sensors.

White-space remains around SaaS dashboards that translate raw stack data into investor-grade ESG metrics. Partnerships, such as those between Endress+Hauser and SICK, merge flow-measurement prowess with gas analytics, signaling the future convergence of instrumentation and cloud analytics. Competitive intensity is expected to rise as regional start-ups exploit lower entry barriers offered by open-protocol edge computing.

Flare Monitoring Industry Leaders

ABB

Siemens AG

Honeywell International Inc.

Emerson Electric Co.

Teledyne FLIR Systems

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is the shift from estimation and periodic checks to regulator-recognized continuous monitoring methods for flare gas quality and performance. In the United States, requirements tied to NSPS OOOOb/OOOOc and related frameworks emphasize monitoring of NHV and other operating parameters, while EPA OTM-56 establishes an authorized pathway for remote, continuous, autonomous flare combustion-zone NHV determination using VISR. This creates whitespace for remote-mount platforms, edge analytics, and monitoring-as-a-service offerings that reduce field work and make compliance documentation more repeatable across distributed assets.

Technology qualification and alternative-method acceptance also support near-term commercialization for advanced analyzers and spectroscopy. In July 2024, Flotek Industries stated that its JP3 Measurement NIR spectroscopy system received EPA approval as an alternative method for NHV monitoring under NSPS OOOOb flare gas measurement requirements, signaling that approved non-traditional measurement approaches can move from pilots into broader deployments. As operators operationalize documented quality control programs and on-site monitoring plans required for continuous systems, demand is building for integrated packages that combine measurement hardware, automated QA/QC, and audit-ready reporting, particularly for brownfield sites that need compliance upgrades without extended downtime.

Recent Industry Developments

- February 2026: Emerson introduced the Rosemount QX1000 Continuous Gas Analyzer for emissions monitoring, combining paramagnetic O2 measurement with quantum cascade laser direct absorption spectroscopy for regulatory gas streams. The launch broadens Emersons analyzer portfolio for continuous compliance-oriented measurement, strengthening its ability to bundle analyzers with control, edge, and reporting layers used in flare monitoring deployments.

- November 2025: Honeywell and TotalEnergies piloted AI-assisted control room operations software at the Port Arthur Refinery, reporting earlier prediction of alarm events and reduced flaring emissions during the pilot. The initiative links flare reduction to control-room digitalization, reinforcing demand for monitoring platforms that feed real-time analytics and enable proactive mitigation rather than post-event reporting.

- July 2024: Flotek Industries announced that its JP3 Measurement NIR spectroscopy system received EPA approval as an alternative method for net heating value monitoring under NSPS OOOOb flare monitoring regulations. The approval supports broader adoption of spectroscopy-based continuous measurement approaches, offering operators an additional compliance pathway beyond conventional analyzer configurations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the flare monitoring market covers fixed systems used to monitor industrial flare stacks, where flame presence, combustion performance, and related operating signals are tracked using sensors, analytics, and supporting services.

Scope exclusions: Portable hand-held gas sniffers and generic thermal cameras that are not integrated into fixed flare monitoring systems are excluded.

Segmentation Overview

- By Mounting Method

- In-Process Mounting

- Gas Analyzer

- Calorimeter

- Mass Spectrometer

- Gas Chromatograph

- Remote Mounting

- Multi-Spectrum IR (MSIR)

- Thermal Imager (IR)

- UV-IR Imager

- Other Remote Mounting

- In-Process Mounting

- By Component

- Hardware

- Detectors and Sensors

- Imaging Devices

- Video Cameras

- Transmitters

- Software

- Services

- Hardware

- By Installation Type

- Onshore

- Offshore

- By Measurement Parameter

- Gas Composition Monitoring

- Flow Rate Monitoring

- Flame Detection and Imaging

- Smoke/Black-Carbon Emission

- By End-User

- Oil Refineries

- Petrochemical Plants

- Upstream Oil and Gas (Onshore)

- Upstream Oil and Gas (Offshore)

- LNG and Gas-Processing Facilities

- Landfills and Biogas Plants

- Chemical Manufacturing

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- Southeast Asia

- Rest of Asia-Pacific

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, map typical use cases, and collect reference indicators that explain where flare monitoring demand is being created. Public sources such as US Environmental Protection Agency rules and guidance, European Commission industrial emissions references, World Bank methane and flaring statistics, and energy agency datasets were reviewed to understand regulatory pressure and flaring intensity. We also used association materials and technical papers (including combustion and optical sensing studies in peer-reviewed journals) to cross-check what is technically counted as flare monitoring versus adjacent instrumentation.

On the commercial side, we reviewed company filings, investor presentations, product catalogs, and credible press coverage to understand how solutions are packaged and priced across hardware, software, and services. Select paid subscriptions were used only for company financials and intelligence, news and financials, and patent databases, so product cycles and pricing logic could be checked against recent announcements. These desk sources are illustrative and not exhaustive, since many other public documents and datasets were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were run to confirm what buyers actually purchase as a flare monitoring system, and how spending splits between new projects, replacements, and service renewals. We spoke with operators, engineering teams, and solution-side experts across oil and gas, refining, petrochemicals, and regulated landfill environments. Coverage was spread across APAC, EMEA, and the Americas so regional compliance practices could be compared and reflected in buying behavior assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 43% |

| Mid tier: 59% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 15% | Managers: 53% | Americas: 22% |

Market-Sizing & Forecasting

The core model uses a top-down build based on the installed base of flare stacks and flaring intensity signals, which are then translated into monitorable sites and expected system spending. To keep the outputs grounded, we corroborated totals with selective bottom-up approximations, including sampled system pricing by technology, a reasoned split of hardware versus software and services, and channel checks on typical replacement cycles.

Key inputs used in the model include the count of regulated facilities with flare stacks, flare utilization patterns (routine vs intermittent), emissions reporting requirements that trigger monitoring, typical system configuration (camera or sensor types plus analytics), and service attachment rates for calibration and maintenance. Pricing is handled through average selling price bands that are refreshed by product generation and integration depth. Where facility-level data is incomplete, gaps are handled using conservative adoption ranges rather than extending current penetration rates. Forecasting is done with scenario analysis, where base, conservative, and accelerated compliance cases are applied, and the final path is selected after aligning with expert views on enforcement timing and project lead times.

Data Validation & Update Cycle

Validation is done in several steps so the market total stays aligned with real-world signals. We compare model outputs against independent checks such as changes in reported flaring activity, new regulatory deadlines, and the expected timing of large facility upgrades, and then investigate outliers before sign-off. When interview feedback shows a meaningful shift in pricing, buying bundles, or service intensity, the assumptions are reworked and the affected regions are rechecked.

Reports are refreshed annually, and interim updates are triggered by material events such as major rule changes or sharp shifts in energy activity. Before delivery, an analyst performs a fresh pass across key inputs and currency conversions so clients receive an up-to-date view.

Mordor Intelligence's Flare Monitoring Market Estimate Compared With Other Published Estimates

Published market sizes for flare monitoring often vary, even when the same words are used, because boundaries, pricing logic, and the timing of updates are not handled the same way. Differences also show up when one study leans heavily on a single demand proxy, while another uses a broader set of operational and compliance signals.

In this study, the refresh cadence and currency timing are treated as practical drivers of variance because many flare projects are quoted in local currencies and then converted at different points in the year, which changes the reported USD total. ASPs are also kept practical by separating full fixed systems from adjacent tools, and the estimate is rechecked against regulatory reporting triggers and service attachment behavior. That is why the final number for Mordor Intelligence does not move in lockstep with faster-growth assumptions used elsewhere.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.13 B (2026) | |

| Trade Publisher A | USD 1.82 B (2026) | Uses a factory-gate revenue view that bundles a wider services set (such as remote monitoring and compliance reporting sold by creators of the goods) and can apply faster growth assumptions from a different historical base, which lifts the 2026 total. |

| Consultancy B | USD 1.33 B (2024) | Anchors the series on an earlier base year and a shorter study window, and the scope description relies on broad segment labels with fewer observable checks on installed base and replacement timing, which can shift the level and slope of the curve. |

The comparison points to a spread that is mainly explained by timing and scope choices, plus how pricing and services are packaged into the counted revenue. By keeping assumptions tied to practical site counts, compliance triggers, and refreshed ASP bands, our estimate stays traceable to steps that can be repeated and revalidated as new project and regulation signals appear.

Key Questions Answered in the Report

What is the current value of the flare monitoring market?

The flare monitoring market is valued at USD 1.13 billion in 2026 and is projected to reach USD 1.49 billion by 2031

Which region leads the market today?

North America holds the largest regional position with 33.90% share in 2025, driven by stringent EPA methane rules and rapid LNG export growth.

What segment is growing the fastest?

Remote mounting systems show the highest segment growth at a 6.05% CAGR as operators move toward unmanned and digital-twin operations.

Why are services gaining popularity?

Services are attractive because monitoring-as-a-service spreads costs, bundles compliance reporting, and keeps systems optimized—leading to a 6.85% CAGR in the services segment.

How do carbon-pricing schemes influence adoption?

Carbon fees in the EU and Canada make accurate flare data essential for cost control; operators that monitor precisely can offset liabilities and avoid penalties, spurring investment in monitoring systems.

What challenges limit faster adoption?

High retrofit costs for older refineries in Southeast Asia and cyber-security constraints on remote offshore platforms can slow deployment timelines and raise project risk.

Page last updated on: