Firewall-as-a-Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

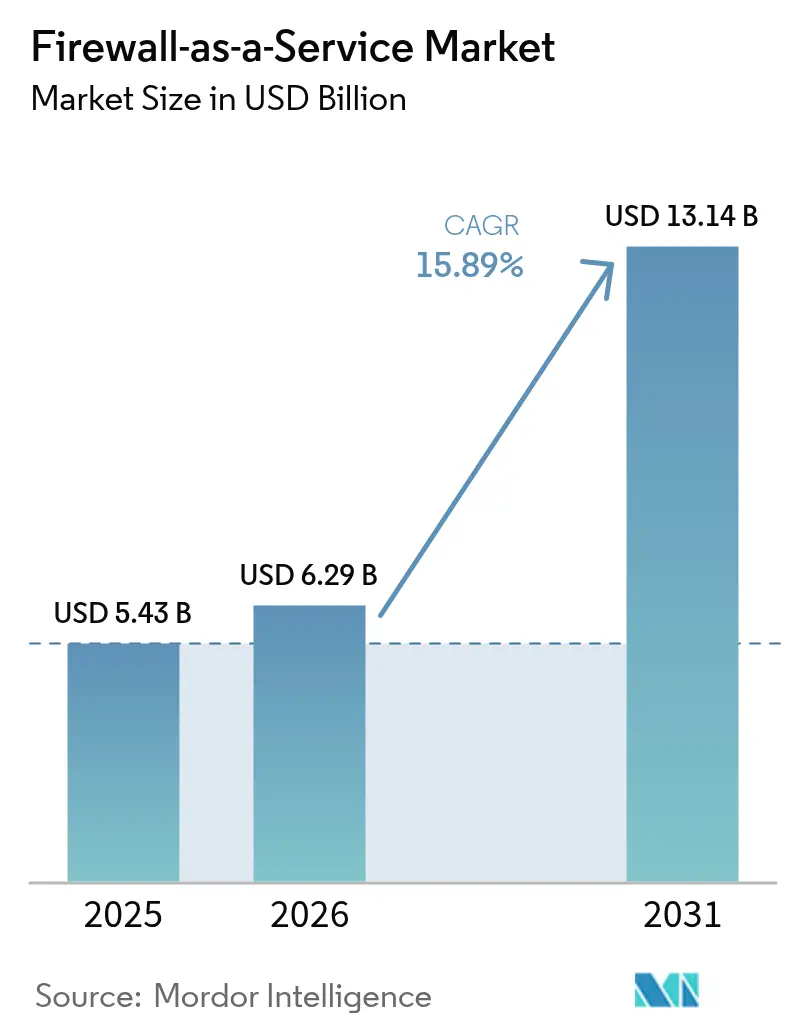

| Market Size (2026) | USD 6.29 Billion |

| Market Size (2031) | USD 13.14 Billion |

| Growth Rate (2026 - 2031) | 15.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Firewall-as-a-Service Market Analysis by Mordor Intelligence

The Firewall-as-a-Service market size was valued at USD 5.43 billion in 2025 and estimated to grow from USD 6.29 billion in 2026 to reach USD 13.14 billion by 2031, at a CAGR of 15.89% during the forecast period (2026-2031). Enterprises are accelerating the transition from appliance-centric security toward cloud-native, distributed firewalls that align with multi-cloud strategies and remote-first workforce models.[1]SonicWall, “Network Security Trends in Hybrid Cloud Environments,” sonicwall.com Persistent hardware supply-chain constraints are reinforcing this pivot by making legacy equipment harder to procure at scale. Rising SaaS adoption, zero-trust mandates, and AI-driven automation are together expanding the total addressable opportunity for vendors able to deliver granular, identity-based policies through a single cloud control plane. Competitive intensity is visible in platform bundling and SASE-centric differentiation as providers seek to lower operating costs, reduce tool sprawl, and capture share in fast-growing emerging regions.

Key Report Takeaways

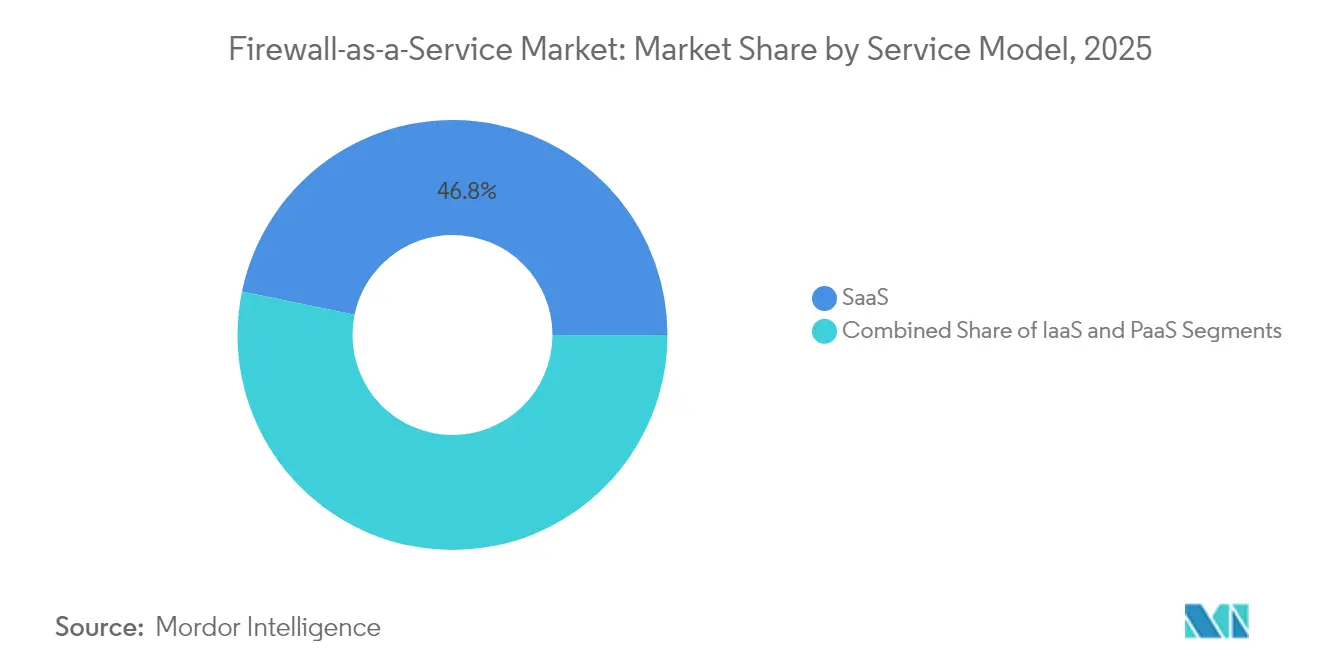

- By service model, Software-as-a-Service led with 46.75% revenue share of the Firewall-as-a-Service market in 2025; Platform-as-a-Service is projected to expand at a 17.08% CAGR to 2031.

- By deployment model, public cloud accounted for 57.95% of the Firewall-as-a-Service market share in 2025, while hybrid cloud is advancing at a 16.84% CAGR through 2031.

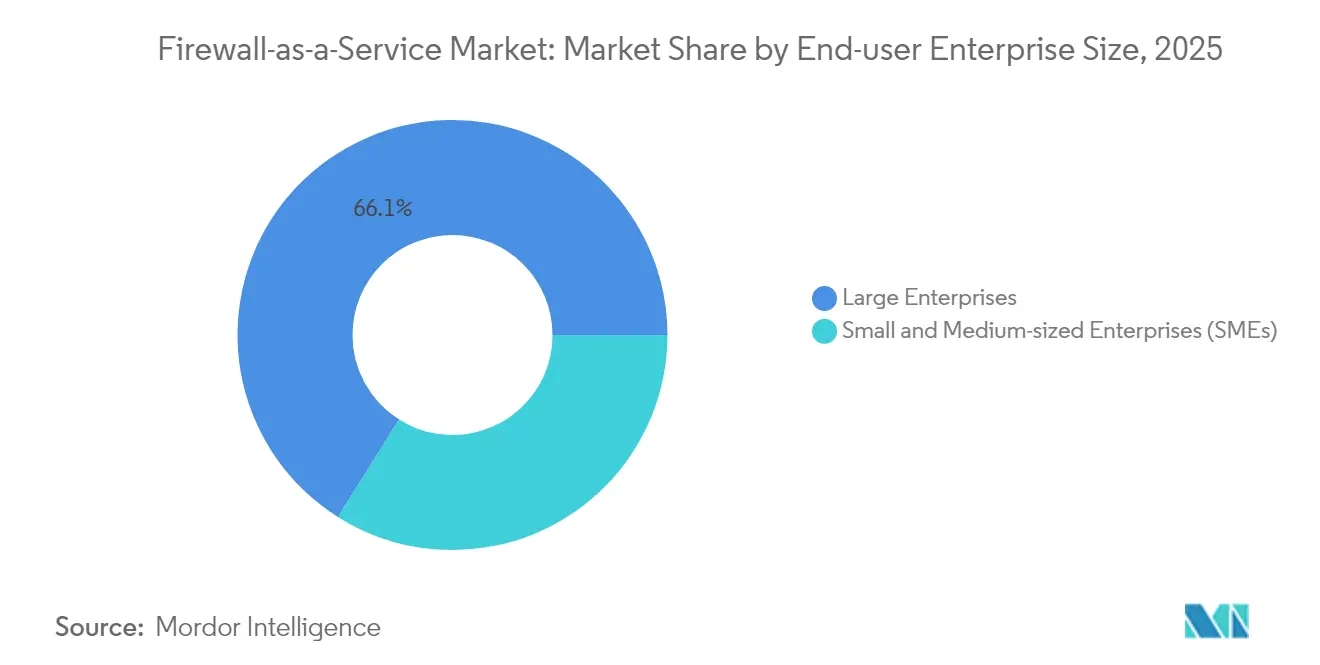

- By enterprise size, large enterprises held 66.05% share of the Firewall-as-a-Service market size in 2025, and SMEs are growing at a 16.58% CAGR to 2031.

- By industry vertical, BFSI captured 27.88% of the Firewall-as-a-Service market share in 2025; healthcare is forecast to register a 17.55% CAGR through 2031.

- By security type, next-generation firewall solutions controlled 41.32% share of the Firewall-as-a-Service market size in 2025, and distributed firewalls are expanding at a 17.19% CAGR during the same horizon.

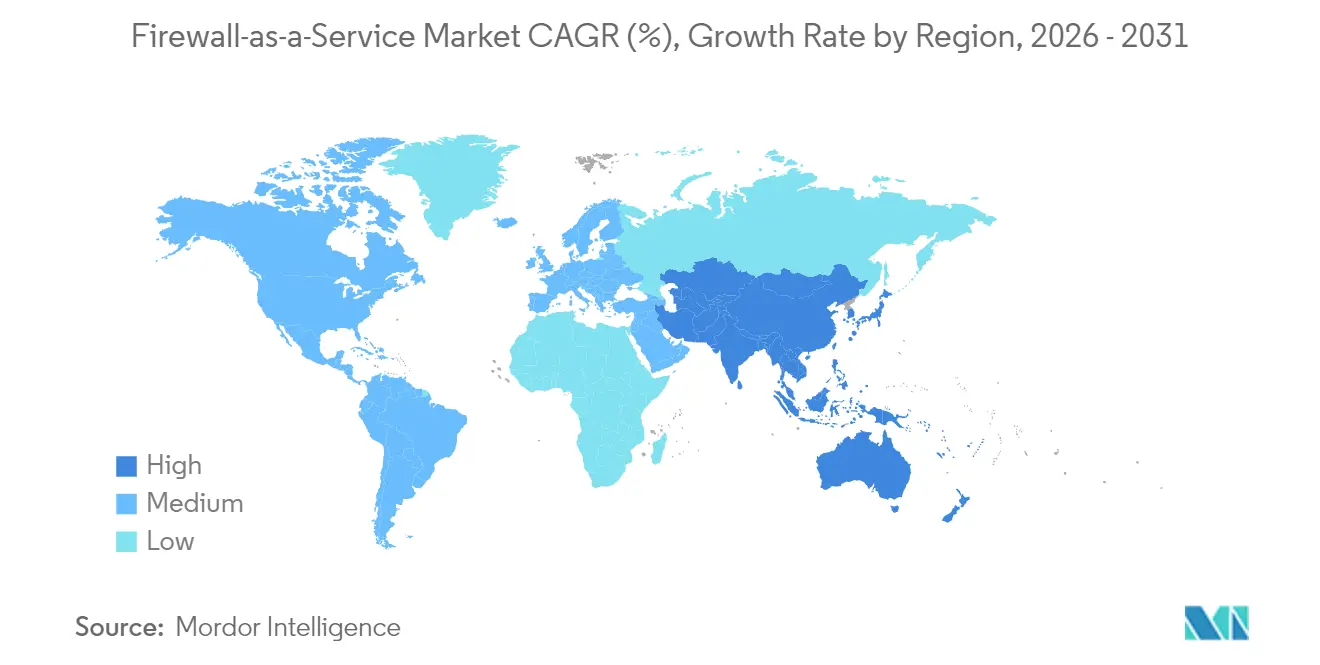

- By geography, North America contributed 35.72% of global revenue of the Firewall-as-a-Service market in 2025; Asia-Pacific is expected to grow at an 17.74% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Firewall-as-a-Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-cloud and SaaS expansion | +4.2% | Global (Asia-Pacific and North America) | Medium term (2-4 years) |

| Cost and frequency of cloud-borne breaches | +3.8% | Global (regulated sectors) | Short term (≤ 2 years) |

| Hybrid/remote workforce security | +3.1% | Global (developed markets) | Medium term (2-4 years) |

| Post-2025 hardware firewall shortages | +2.4% | Global (Asia-Pacific hubs acute) | Long term (≥ 4 years) |

| AI-driven policy automation for SMEs | +1.9% | North America and EU | Long term (≥ 4 years) |

| Cloud-marketplace procurement incentives | +1.1% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Multi-Cloud and SaaS Adoption

Seventy-eight percent of enterprises now run hybrid or multi-cloud estates, a complexity that strains hardware firewalls, unable to enforce uniform policies across AWS, Azure, and Google Cloud workloads.[2]Harris, Frederick, “Key Findings from the 2024 Cloud Security Report,” Fortinet Blog, fortinet.com Cloud-hosted applications bypass legacy perimeters, compelling organizations to adopt elastic, API-driven controls that follow workloads wherever they reside. The Firewall-as-a-Service market, therefore, benefits from enterprises seeking single-pane policy orchestration that aligns with DevOps velocity. SaaS proliferation compounds requirements by introducing thousands of discrete data flows, each demanding consistent governance. As Microsoft Azure becomes the most widely consumed hyperscale platform in 2025, the vendor's ability to integrate natively with its identity and telemetry stack confers a competitive advantage.

Escalating Cost and Frequency of Cloud-Borne Data Breaches

Gigamon’s 2024 survey found one-third of attacks went undetected in the prior year, a 20% uptick that underscores gaps in legacy detection. Breach costs have overtaken on-prem incidents because lateral movement inside cloud fabrics multiplies remediation expense. Attackers are weaponizing AI to bypass signature-based controls, prompting enterprises to invest in real-time threat intelligence and automated response embedded in cloud firewalls. Regulatory exposure heightens urgency: GDPR fines and the incoming NIS2 directive make inadequate cloud controls a financial and reputational risk, turning FWaaS adoption into a board-level mandate rather than an optional enhancement.

Hybrid/Remote Workforces Demanding Distributed Security

Permanent hybrid work has shifted traffic away from centralized data centers, rendering VPN architectures inefficient for latency-sensitive cloud apps. Eighty percent of firms plan Zero-Trust Network Access implementation within 18 months, demanding identity-centric policy enforcement delivered through FWaaS nodes close to users. Integration with secure access service edge (SASE) architectures ensures consistent inspection regardless of location, improving user experience while closing perimeter gaps. Organizations report that traffic tromboning through on-prem firewalls introduces unacceptable latency for SaaS, driving migration toward distributed inspection points natively embedded in cloud PoPs.

AI-Driven Policy Automation Lowering SME TCO

Machine-learning engines now recommend and refine rulesets automatically, slashing manual change windows and reducing misconfiguration risk. Vendors such as Palo Alto Networks and Cisco embed AIOps modules that generate policies based on observed application behavior, a capability critical for SMEs lacking dedicated security staff. Ninety-three percent of organizations cite security-skills shortages; AI-powered automation, therefore, expands addressable demand by lowering the operational barrier to entry. The result is a measurable total cost-of-ownership reduction as error-prone manual workflows are eliminated.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integrating FWaaS with legacy appliances | -2.1% | Global (legacy-heavy enterprises) | Medium term (2-4 years) |

| Latency and data-sovereignty constraints | -1.8% | EU and Asia-Pacific regulated sectors | Long term (≥ 4 years) |

| Public-cloud egress fee escalation | -1.3% | Global (data-intensive verticals) | Short term (≤ 2 years) |

| Vendor-platform consolidation fatigue | -0.9% | North America and EU enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complexity Integrating FWaaS with Legacy Appliances

Enterprises often run heterogeneous firewall estates across campuses, branches, and co-location sites, creating policy-sync challenges when layering in cloud firewalls. Traffic steering, high-availability failover, and unified logging demand architectural redesign that can inflate project timelines. VLAN schemes optimized for on-prem equipment frequently conflict with FWaaS deployment models, obliging network teams to rethink segmentation. These hurdles raise switching costs and dampen short-term growth potential in the Firewall-as-a-Service market even as long-term benefits remain compelling.

Latency and Data-Sovereignty Concerns in Regulated Sectors

Healthcare, finance, and government workloads face stringent data-residency mandates. Sub-millisecond performance requirements for trading systems, or HIPAA restrictions on patient-record processing, sometimes mandate on-prem inspection to avoid compliance risk.[3]WatchGuard Technologies, “About WatchGuard Compliance Reporting,” watchguard.com Cross-border data flows can trigger GDPR penalties, pushing risk-averse organizations to retain local appliances until providers can guarantee sovereign hosting zones in every jurisdiction. Elevated public-cloud egress charges further complicate cost equations for data-heavy workloads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Model: SaaS Preference Steers Innovation

SaaS-delivered firewalls captured 46.75% of 2025 revenue, demonstrating immediate appeal among enterprises seeking turnkey deployment without infrastructure overhead. This segment forms the economic backbone of the Firewall-as-a-Service market, offering pre-tuned policies, elastic scaling, and integrated threat-intel feeds that auto-update with minimal customer intervention. The model resonates with IT teams under pressure to shorten provisioning cycles while maintaining audit readiness, especially in heavily regulated verticals. Vendors capitalize by bundling value-added features such as cloud access security broker (CASB) and secure web gateway (SWG) into a unified SaaS subscription.

Platform-as-a-Service, though smaller, is growing at a 17.08% CAGR as DevOps-oriented organizations demand code-centric security workflows. API-first PaaS firewalls integrate with CI/CD pipelines, enabling “security as code” and automating posture checks pre-deployment. Infrastructure-as-a-Service retains a niche for customers requiring granular control over kernel modules or custom forwarding paths. Together, these models illustrate a continuum of control versus convenience that shapes purchasing decisions across the Firewall-as-a-Service market.

By Deployment Model: Hybrid Momentum Redefines Perimeter

Public cloud remained dominant in 2025 with a 57.95% share of the Firewall-as-a-Service market size; hyperscale fabric presence, integrated IAM, and pre-peered connectivity simplify onboarding. However, hybrid deployments are expanding at a 16.84% CAGR as organizations chase millisecond-level latency and regulatory compliance through on-prem coexistence. This trajectory signals a move away from binary cloud decisions toward workload-specific placement.

Successful providers now abstract policy orchestration so that a single ruleset follows traffic whether it traverses cloud, edge, or campus sites. Private cloud persists for sovereign data repositories and ultra-low-latency industrial controls, reinforcing the need for portable licensing and federated management consoles.

By End-user Enterprise Size: SMEs Accelerate Adoption Curve

Large organizations commanded 66.05% revenue in 2025, leveraging their budgets to license multi-function platforms that converge firewall, SWG, and ZTNA. They typically operate across multiple regions and clouds, making unified, API-driven management a necessity.

Conversely, SMEs represent the fastest-growing cohort at 16.58% CAGR thanks to consumption-based pricing, AI-assisted configuration, and marketplace-embedded procurement incentives. This development expands the Firewall-as-a-Service market by democratizing security capabilities once reserved for the Fortune 500. Vendors targeting SMEs emphasize wizard-based onboarding, flat-rate bundles, and managed-service overlays to offset skill shortages.

By Industry Vertical: Healthcare Surges Under Compliance Weight

The BFSI sector retained a 27.88% share in 2025, driven by transaction integrity mandates and cyber-insurance prerequisites. Financial institutions integrate FWaaS into zero-trust architectures that span trading floors, mobile apps, and SaaS CRM systems.

Meanwhile, healthcare is sprinting ahead with a 17.55% CAGR, propelled by telemedicine expansions and IoT medical devices that extend attack surfaces beyond hospital walls. HIPAA, HITRUST, and similar frameworks press providers to adopt identity-aware segmentation, making FWaaS a compliance enabler. Manufacturing, retail, and energy verticals progress steadily as they digitize OT environments and align security budgets with Industry 4.0 roadmaps.

By Security Type: Distributed Architectures Scale Zero Trust

Next-generation firewalls anchored a 41.32% share in 2025, offering integrated IPS, URL filtering, and sandboxing crucial for inline threat interception. Growth now shifts toward distributed and micro-segmentation firewalls, forecast at 17.19% CAGR, because east-west traffic within containers and microservices demands granular controls unattainable in perimeter-centric models.

Web-application firewalls protect API and SaaS front ends, and virtual firewalls secure hypervisor-based VNets; both ride the broader cloud adoption wave. Forward-leaning vendors optimize inspection engines for microsecond insertion to satisfy performance-sensitive workloads, further widening the appeal of micro-segmented designs.

Geography Analysis

North America generated 35.72% of global 2025 revenue, a reflection of mature cloud adoption, a dense vendor ecosystem, and federal cybersecurity directives that mandate continuous monitoring. Enterprises benefit from abundant local hyperscale regions that reduce latency to FWaaS PoPs and from robust venture investment fueling product innovation. Cross-border data flows under the U.S.-EU Data Privacy Framework also ease compliance for multinationals.

Asia-Pacific is the fastest-growing region with an 17.74% CAGR projected through 2031. Government-funded digital initiatives, expanding 5G backbones, and rising ransomware exposure are together catalyzing spend across India, Australia, Japan, and ASEAN economies. Local hyperscale expansions by AWS, Azure, and Alibaba Cloud multiply PoP density, allowing providers to meet data-localization mandates and latency requirements in heavily populated metros. Competitive entry by regional telcos bundling FWaaS inside managed SD-WAN further lifts adoption curves.

Europe advances steadily as GDPR and the forthcoming NIS2 directive intensify focus on verifiable cyber-controls. Local-cloud strategies, including Gaia-X and sovereign cloud zones, influence provider footprint planning, prompting vendors to open additional data centers in Frankfurt, Paris, and Madrid. While Brexit caused temporary procurement uncertainty, United Kingdom enterprises continue investing in FWaaS to comply with the National Cyber Strategy 2025 objectives.

South America and the Middle East, and Africa represent emerging demand clusters. Cloud adoption curves in Brazil, Mexico, South Africa, and the Gulf Cooperation Council are steep; however, limited local PoPs and price sensitivity slow near-term growth. Global vendors are therefore partnering with regional ISPs to offer edge-hosted inspection that satisfies sovereignty requirements without massive CapEx. This localization effort will be pivotal for capturing long-term revenue as these economies digitize supply chains.

Regulatory Landscape

Firewall-as-a-Service (FWaaS) deployments are shaped by cybersecurity compliance regimes that increasingly emphasize continuous control assurance, cloud-delivered monitoring, and jurisdictional governance for regulated data. In the United States, programs and standards such as FedRAMP (moving to consolidated rules in 2026) and NIST guidance for high-assurance environments influence how cloud security services map controls, document security posture, and maintain ongoing authorization. Department of Defense firewall requirements are operationalized through DISA STIGs aligned to NIST 800-53 control expectations for segmentation, access control, and continuous monitoring.

In Europe, regulatory pull from NIS2 and DORA raises the importance of auditable controls and sovereign operation models, particularly for critical infrastructure and financial services. The European Commission in 2026 advanced a Cybersecurity Act revision package tied to the European Cybersecurity Certification Framework. These dynamics push vendors to provide regionalized enforcement and reporting, with June 2026 sovereign SASE positioning in Europe explicitly aligning to NIS2, DORA, and Germany's KRITIS framework requirements for regulated enterprises.

Value Chain Analysis

The FWaaS value chain starts with core cloud infrastructure and connectivity foundations, where hyperscale providers supply compute, networking, and regional footprints used to host distributed enforcement points and telemetry pipelines. FWaaS vendors build a cloud control plane (policy authoring, APIs, versioning, identity integrations) and a distributed data plane (inspection and enforcement nodes), supported by centralized policy stores and analytics. Critical upstream dependencies include certificate and key management components that enable TLS inspection at scale, along with threat intelligence feeds and malware analysis services that continuously refresh detection and prevention logic.

Midstream, FWaaS is commonly packaged within broader Security Service Edge (SSE) and SASE portfolios alongside SWG, CASB, and ZTNA, delivered through direct enterprise subscriptions, cloud marketplaces, and managed security service providers (MSSPs) that operationalize deployment, policy tuning, and ongoing monitoring. Downstream value is realized through integration into customer identity providers, SIEM/SOAR platforms, and DevSecOps workflows, especially for hybrid and multi-cloud estates that require consistent policy orchestration across AWS, Azure, and Google Cloud environments. Key friction points stem from dependence on third-party cloud regions and certificate ecosystems, and from compliance engineering burdens (for example FedRAMP-aligned delivery) that can limit which vendors can serve government and highly regulated buyers.

Competitive Landscape

The Firewall-as-a-Service market is moderately concentrated. Incumbent hardware vendors Palo Alto Networks, Fortinet, and Cisco are pivoting portfolios toward cloud delivery, leveraging existing account control and channel reach. They integrate FWaaS into broader secure access service edge stacks, simplifying procurement for customers fatigued by point-product sprawl. Cloud-native specialists such as Zscaler and emerging SASE vendors compete on lightweight architecture, per-user pricing, and rapid feature velocity.

AI-driven policy automation, threat-intelligence breadth, and DevSecOps integrations constitute the current battleground. Fortinet’s 2024 acquisition of Lacework added a CNAPP module, enabling code-to-cloud visibility that resonates with DevOps teams.[4]Novinson, Michael, “Fortinet Acquires Unicorn Lacework to Enhance Cloud Security,” BankInfoSecurity, bankinfosecurity.com Zscaler’s partnership with NVIDIA layers GPU-accelerated analytics onto its Zero Trust Exchange, promising sub-second anomaly detection. Check Point’s Quantum R82 release focuses on automated rule-orchestration across multi-cloud estates, reducing human touchpoints.

Acquisition pipelines remain active as vendors plug portfolio gaps, especially in microsegmentation, OT security, and CASB. At the same time, hyperscalers are gradually embedding baseline firewall capabilities, compressing margins on entry-level tiers. To preserve differentiation, pure-play providers are doubling down on cross-cloud policy portability and advanced analytics. The market is expected to witness further convergence among SWG, ZTNA, and FWaaS modules, driven by customer demand for consolidated billing and unified telemetry.

Firewall-as-a-Service Industry Leaders

Barracuda Networks Inc.

Cato Networks Ltd.

Check Point Software Technologies Ltd.

Cisco Systems Inc.

Cloudflare Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity area sits in policy models that better match ephemeral cloud and containerized workloads, where static IP-based rules struggle to keep pace with autoscaling services and microservices. Concrete product direction is visible in June 2026 updates to AWS Network Firewall that add container attribute-based rules referencing Kubernetes and container metadata (for example namespaces, cluster names, and labels). This points to demand for attribute-driven enforcement that follows workloads rather than fixed network constructs. Vendors that can unify identity-aware, workload-aware policy across hybrid estates (public cloud plus on-prem) can reduce integration overhead for enterprises managing heterogeneous firewall environments.

Another opportunity lies in AI-assisted operations and modern cryptography within converged SASE platforms, particularly for organizations dealing with security-skills shortages and rising encrypted traffic volumes. In 2026, Fortinet introduced FortiOS 8.0 with AI-driven security agents and quantum-safe cryptography for deep packet inspection, signaling enterprise willingness to adopt AI-native automation inside firewall and SASE stacks when it reduces policy management effort and improves inspection fidelity. Across regulated sectors facing data-sovereignty constraints, notably EU-aligned NIS2 and DORA programs, there is additional whitespace for regionally operated, sovereign-grade service delivery models paired with compliance-ready reporting and control mapping, rather than one-size-fits-all global PoPs.

Recent Industry Developments

- July 2026: Barracuda Networks acquired Evo Security to add identity and access management capabilities that can be integrated into the BarracudaONE platform. The move strengthens policy decisions tied to user identity and access context, a core requirement as FWaaS converges with ZTNA and broader SSE bundles.

- June 2026: Check Point announced plans to embed OpenAI frontier cyber capabilities through the OpenAI Daybreak Cyber Partner Program into its security products. This extends prevention and response workflows with AI-assisted capabilities, reinforcing the shift toward AI-native security services within cloud-delivered firewall and SASE platforms.

- April 2026: Check Point announced a launch partnership with Google Cloud to integrate its AI Defense Plane with Googles Gemini Enterprise Agent Platform. The integration targets governance and protection for enterprise AI agents and cloud workloads, aligning network security controls with emerging agentic application architectures that traverse multi-cloud environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from delivering firewall functionality as a cloud-managed service, where policies are centrally configured and traffic is inspected and enforced for users, sites, or workloads over the network.

Scope exclusions: This sizing excludes on-premise firewall hardware sales, standalone secure web gateway and VPN-only subscriptions, and pure managed services that do not include an FWaaS platform subscription.

Segmentation Overview

- By Service Model

- SaaS

- IaaS

- PaaS

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By End-user Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By Industry Vertical

- BFSI

- IT and Telecom

- Healthcare

- Retail and E-commerce

- Industrial and Defense

- Energy and Utilities

- Manufacturing

- Other Industry Verticals

- By Security Type

- Next-Generation Firewall (NGFW)

- Web Application Firewall (WAF)

- Distributed / Micro-segmentation Firewall

- Virtual Firewall (vFW)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand signals that typically move with FWaaS adoption and price realization, then aligning those signals to how vendors report cloud security revenue. We used public sources such as NIST guidance, CISA advisories, FCC broadband data (as a proxy for connectivity expansion), U.S. SEC filings, and ITU indicators for regional internet usage, which helps anchor the model in observable activity.

To convert those signals into a usable market model, we also reviewed vendor product documentation, customer case studies, earnings call transcripts, and reputable cybersecurity press for deployment patterns such as branch consolidation and remote access transitions. In addition, paid subscriptions covering company financials and intelligence, patent databases, and news and financials were used to standardize revenue splits and track product-line changes over time. The sources listed above are illustrative, and other public references were also reviewed to collect data, validate assumptions, and close open questions.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with cloud security buyers, channel partners, and product leaders who see pricing, adoption, and renewal behavior in live deployments. For a global market like this, we kept regional feedback balanced across APAC, EMEA, and the Americas so regional cloud maturity, data residency rules, and typical contract terms could be reflected in our assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | APAC: 48% |

| Mid tier: 48% | Functional/Unit leaders: 39% | EMEA: 31% |

| Smaller Players: 17% | Managers: 48% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where cloud security spend is reconstructed into an FWaaS demand pool using adoption and usage indicators, then filtered to what is actually sold as an FWaaS subscription. To keep the totals realistic, the output is checked through selective bottom-up approximations, such as sampled vendor revenue splits, channel feedback on average contract values, and volume assumptions tied to protected users or sites.

The model uses practical inputs, including remote and hybrid workforce penetration, enterprise cloud and multi-cloud adoption, average policy enforcement points per organization (users, branches, and workloads), typical subscription duration and renewal rates, and ASP progression based on feature mix and traffic volumes. Where direct volume information is not consistently available, we fill gaps using ranges validated in interviews and then apply conservative mid-points that are stress-tested against known security budget patterns.

Forecasting is run using scenario analysis supported by short time-series smoothing, because adoption can step up after major regulatory shifts or breach cycles and then normalize. The final outlook is adjusted using expert views on price pressure, consolidation of point products into platforms, and the timing of large enterprise network refresh and migration programs.

Data Validation & Update Cycle

After the first model run, the totals are triangulated against independent signals such as cloud security budget growth, vendor commentary on subscription mix, and region-level adoption indicators, which helps confirm that growth rates are not being overstated. Any large variances are reviewed by analysts, and the assumptions that caused them are rechecked against source notes and interview feedback before sign-off.

Reports are refreshed on an annual cycle, and interim updates are triggered when material events occur, such as major pricing model changes, new regulatory deadlines, or meaningful shifts in cloud adoption. Before a deliverable is finalized, a last-pass validation is completed so clients receive the most current view that can be supported by traceable inputs.

Mordor Intelligence's Firewall As A Service Market Size Compared Against Other Published Estimates

Published numbers for FWaaS do not always match because teams choose different service definitions, year conventions, and pricing logic, and then those choices ripple through every step of the model. Differences also come from how providers treat bundled security platforms, how they convert regional revenue into USD, and how often underlying assumptions are refreshed.

Some estimates expand the scope to include adjacent cloud security services that sit around the firewall function, which can lift the headline size even if usage is similar. In Mordor Intelligence sizing, revenue is counted only when it is attributable to an FWaaS subscription and it is kept separate from on-prem firewall hardware and non-firewall standalone tools. This narrower counting approach is also rechecked using contract duration and renewal patterns from primary validation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.29 B (2026) | |

| Industry Research Publisher A | USD 4.71 B (2025) | Uses a different base year and can understate the 2026 value if it assumes slower early adoption, and its scope language is often interpreted to include only cloud-delivered firewall services without consistently reconciling bundled platform revenue splits. |

| Industry Research Publisher B | USD 6.72 B (2024) | Relies on an earlier base year and a longer forecast window, which can elevate the starting value if historical backcasting blends broader cloud security categories, and ASP progression is typically simplified without explicitly tying it to policy enforcement points or traffic-driven tiers. |

Overall, the spread in published values is mainly explained by base-year selection and whether adjacent security subscriptions are merged into the FWaaS bucket. By keeping the scope tied to subscription-attributable FWaaS revenue and then stress-testing it with practical adoption and pricing checks, the resulting number stays easier to trace and repeat when assumptions are updated.

Key Questions Answered in the Report

What is the 2026 value of the Firewall-as-a-Service market?

The market totals USD 6.29 billion in 2026.

How fast is revenue expected to grow through 2031?

Revenue is projected to rise at a 15.89% CAGR, reaching USD 13.14 billion.

Which service model holds the largest revenue share?

SaaS firewalls lead with 46.75% of 2025 global revenue.

Which deployment model is growing fastest?

Hybrid cloud firewalls are forecast to expand at 16.84% CAGR between 2026 and 2031.

Which region exhibits the highest growth rate?

Asia-Pacific is set to grow at an 17.74% CAGR through 2031.

Who are the leading vendors in this market?

Key vendors include Palo Alto Networks, Fortinet, Cisco, Zscaler, and Check Point.

Page last updated on: