Field-Erected Cooling Tower Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.09 Billion |

| Market Size (2031) | USD 4.06 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Field-Erected Cooling Tower Market Analysis by Mordor Intelligence

The Field-Erected Cooling Tower Market size was valued at USD 2.93 billion in 2025 and estimated to grow from USD 3.09 billion in 2026 to reach USD 4.06 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

Heightened investment in thermal power generation, stringent environmental rules, and a visible shift toward modular fiber-reinforced plastic (FRP) structures are the most influential growth levers. Rising electricity demand across emerging economies, rapid industrialization, and stricter plume-abatement requirements are driving end users toward hybrid and dry technologies that conserve water without compromising heat-rejection performance. At the same time, recurring refurbishment cycles in North America and Europe are converting legacy assets into steady aftermarket revenue for suppliers with advanced retrofit capabilities. Global manufacturers are pursuing localized fabrication to shorten delivery schedules and counteract raw-material price swings, while also broadening their digital service portfolios that promise predictive maintenance and lower lifetime operating expenses.

Key Report Takeaways

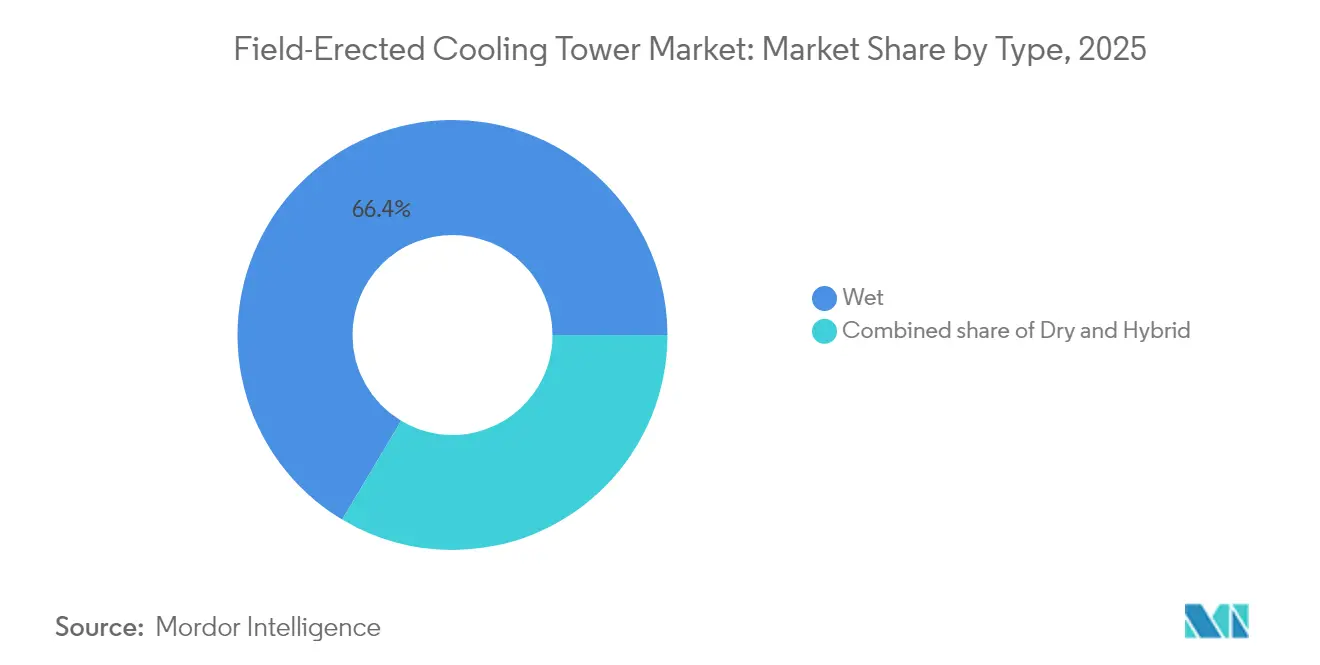

- By type, wet towers accounted for 66.42% of 2025 revenue, while hybrid towers are expected to post the fastest growth rate of 6.55% from 2026 to 2031.

- By design, induced draft systems accounted for 61.80% of the field-erected cooling tower market size in 2025 and are projected to grow at a 5.74% CAGR over 2026-2031.

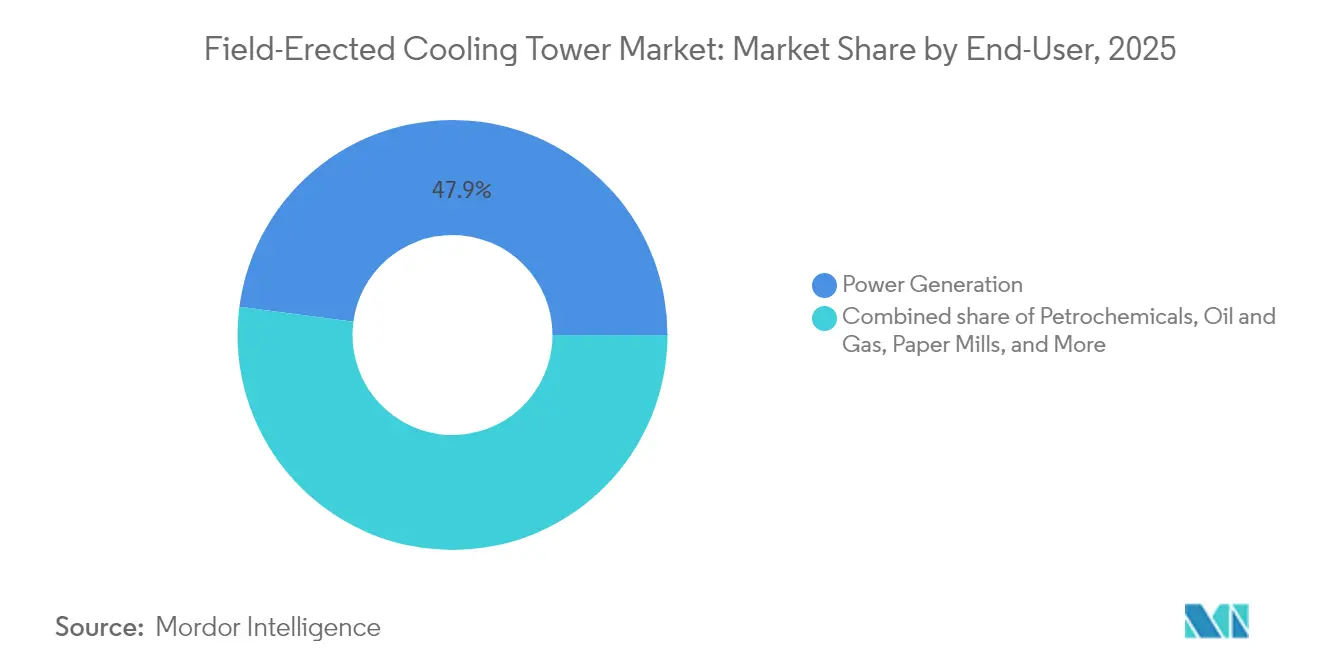

- By end user, power generation led with 47.90% of the field-erected cooling tower market share in 2025 and is forecast to expand at a 5.83% CAGR through 2031.

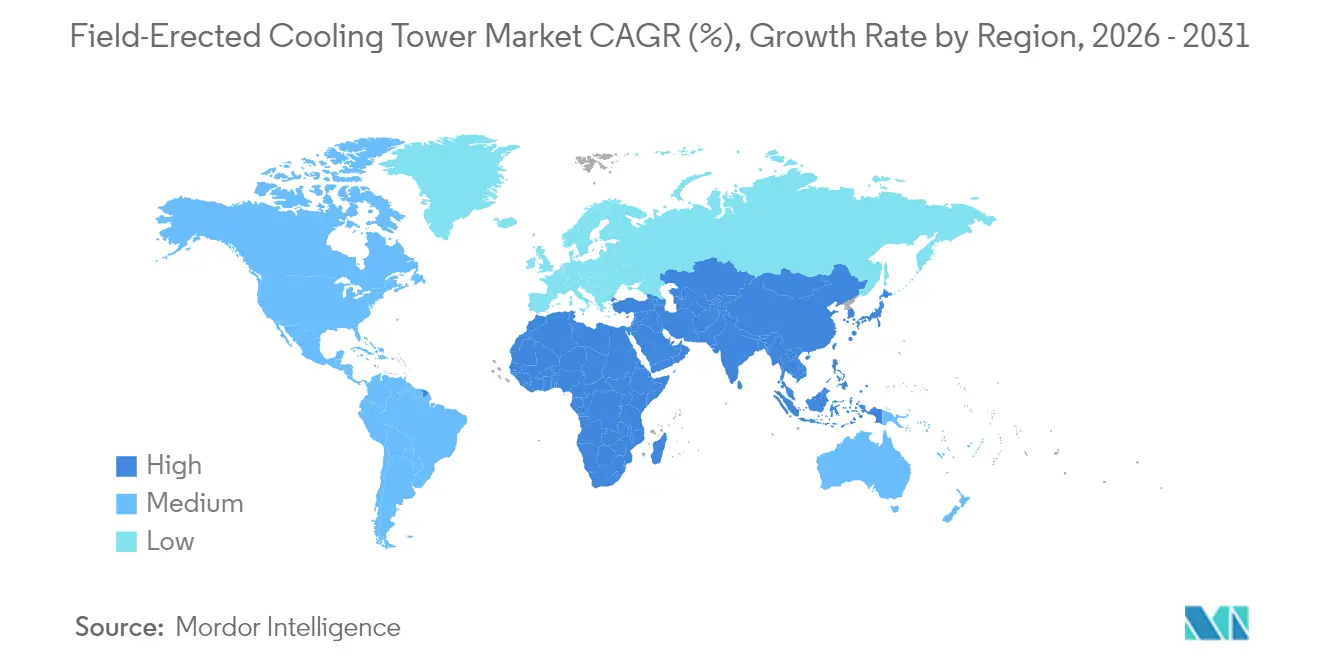

- By geography, Asia-Pacific captured 42.10% revenue in 2025 and is set to register the highest 6.92% CAGR during the forecast period.

- SPX Technologies, Babcock & Wilcox, and EVAPCO together controlled an estimated mid-double-digit share of global revenue in 2024, reflecting a moderately consolidated supplier base.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Field-Erected Cooling Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of thermal-power capacity in emerging economies | 1.80% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Mandatory refurbishment of aging plant cooling assets | 1.20% | North America & EU | Short term (≤ 2 years) |

| Tightening plume-abatement norms favouring hybrid towers | 0.90% | Global | Long term (≥ 4 years) |

| Geothermal & WtE projects seeking low-water dry towers | 0.60% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| District-scale data-centre heat-reuse cooling demand | 0.40% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Modular FRP components reducing on-site labour costs | 0.70% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Thermal-Power Capacity in Emerging Economies

Surging electricity demand in India, China, and Southeast Asia is driving large-scale steam-cycle investments that rely on high-capacity, field-erected cooling towers for optimal condenser performance. NTPC’s Lara Super Thermal Power Project extension in India and Nantong Tongzhou Bay ultra-supercritical units in China illustrate how mega-projects are setting new standards for tower dimensions, material durability, and water-saving capabilities. Utility engineers are increasingly mandating performance guarantees for drift loss, plume visibility, and lifecycle corrosion resistance, elevating suppliers with proven computational fluid dynamics design and in-house FRP fabrication capabilities. Local joint-venture manufacturing hubs in Gujarat, Guangxi, and Ho Chi Minh City also help reduce transport costs and expedite erection schedules, thereby strengthening regional ties between equipment vendors and engineering, procurement, and construction (EPC) contractors. With most national energy plans extending to 2030 and beyond, the driver supports a continuous, multi-year procurement pipeline in the Asia-Pacific region.

Mandatory Refurbishment of Aging Plant Cooling Assets

In North America and the European Union, the majority of fossil and nuclear generating units entered service before 1995; condenser vacuum losses, fan inefficiencies, and structural corrosion now threaten output and compliance with permit requirements.[1]World-Nuclear-News Staff, “Holtec Starts Palisades Cooling Upgrade,” world-nuclear-news.org Utilities are allocating rising capital budgets to replace fill media, upgrade gearboxes, and install high-efficiency fans that restore approach temperatures without extended outages. Holtec’s heat-exchanger replacement at the Palisades facility exemplifies how modular skid assemblies reduce tie-in windows and minimize costly civil works. Retrofit demand also benefits aftermarket divisions of global suppliers such as Baltimore Aircoil Company, which offer turnkey rebuild programs involving thermal audits, vibration monitoring, and drift-elimination upgrades.[2]Baltimore Aircoil Company, “Retrofit and Rebuild Services,” baltimoreaircoil.com Because refurbishment programs often lock in service contracts for 10 years or more, this revenue stream helps temper the cyclical swings associated with new-build projects.

Tightening Plume-Abatement Norms Favouring Hybrid Towers

Urban encroachment around industrial sites has transformed the once-benign water-vapor plume into a source of public complaints and occasionally aviation concerns. Hybrid towers blend wet and dry heat-rejection surfaces, allowing operators to toggle modes that suppress visible plume during cold, humid conditions while preserving evaporative efficiency most of the year. Nooter Eriksen’s composite NEXT series embodies the trend; its integrated plume-control module uses finned-tube add-ons that reclaim water droplets and prevent icing at roadways.[3]Nooter Eriksen, “NEXT Hybrid Cooling Solutions,” nootereriksen.com Regulatory pressure is strongest in Germany, Japan, and certain parts of the United States, where state environmental agencies incorporate plume visibility limits into air quality permits. Although hybrid systems carry a 10-15% capital premium, the payback often materializes through avoided community mitigation costs and simpler planning approvals, prompting wider adoption across combined-cycle gas and biomass plants.

Geothermal & Waste-to-Energy Projects Seeking Low-Water Dry Towers

Developers of high-enthalpy geothermal and next-generation waste-to-energy (WtE) plants operate in regions where cooling water is scarce or effluent discharge is tightly regulated. They are turning to dry or dry-assisted designs that cut water withdrawal by as much as 95% relative to wet systems. Air-cooled condenser (ACC) banks sized for 10 MW to 200 MW facilities can now be erected in compact A-frame arrays using prefabricated steel modules that reduce site crane time. Aggressive deployment incentives in Europe and North America, along with the inclusion of net-water-use metrics in green-bond reporting frameworks, position dry towers as a bankable standard for these niche but fast-growing markets. Suppliers capitalizing on this demand are integrating variable-frequency drive (VFD) fan packages and digital twins that predict seasonal performance swings, helping owners optimize dispatch economics under flexible power purchase agreements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High water-use penalties in arid regions | -0.80% | Arid regions globally, particularly Western US, Middle East | Short term (≤ 2 years) |

| Raw-material price volatility (steel, FRP resins) | -0.60% | Global | Short term (≤ 2 years) |

| FRP-shaft CU-deposit cracking in coastal plants | -0.30% | Coastal regions globally | Medium term (2-4 years) |

| Stricter acoustic rules driving costly fan retrofits | -0.40% | Urban and residential proximity areas globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Water-Use Penalties in Arid Regions

Utility commissions in Arizona, Nevada, and parts of the Middle East have introduced volumetric surcharges that punish evaporative losses above specified thresholds.[4]Broward County, “Cooling Tower Water Efficiency Ordinance,” broward.org For coal, gas-fired, and concentrating solar power stations located far from abundant freshwater sources, these fees erode generation margins and complicate dispatch economics. Although dry cooling offers a compliance pathway, lower heat-transfer coefficients translate into higher turbine back-pressure and reduced net output. Project sponsors, therefore, face a trade-off between water savings and fuel efficiency, which can undermine the economics of thermal projects in already challenging merchant power markets. The policy environment encourages hybridization but simultaneously raises financing hurdles for pure wet tower projects in water-stressed geographies, capping near-term field-erected cooling tower market growth potential.

Raw-Material Price Volatility (Steel, FRP Resins)

Average hot-rolled coil steel prices doubled between 2021 and 2024, before retracing, while epoxy resin costs fluctuated in line with crude oil and petrochemical supply disruptions. Since field-erected towers can require more than 1,500 tons of steel and substantial FRP content, small and medium-sized manufacturers struggle to hedge exposure during multiyear build cycles. Fixed-price EPC contracts negotiated during low-price windows become liabilities when input costs rise, eroding gross margins or forcing renegotiations that delay project execution. Larger enterprises mitigate risk through volume discounts, forward-buying programs, and vertical integration, which support consolidation trends visible across the supply chain.[5]EVAPCO, “Air-Cooled Condenser Solutions,” evapco.com Persistent volatility may deter new entrants and temper competitive intensity, yet pricing uncertainty still hinders overall market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hybrid Growth Accelerates Despite Wet Dominance

Wet systems contributed 66.42% of global revenue in 2025, underscoring their unrivalled thermodynamic efficiency wherever water is readily available. These units are the default choice for coal-, gas-, and biomass-fired plants aiming to maximize cycle efficiency because evaporative cooling lowers condenser temperatures well below dry-bulb levels. As a result, the field-erected cooling tower market continues to see sizeable procurement volumes for wet designs across Asia-Pacific and parts of Latin America. Yet, the hybrid subsegment is expanding at a 6.55% CAGR, benefiting from rule changes that cap visible plume height in metropolitan jurisdictions, as well as corporate water-stewardship targets linked to ESG reporting.

The premium for hybrid systems narrows every year thanks to modular add-on sections that retrofit onto existing basins and eliminate the need for separate dry coolers. Innovation in fill-material geometry and drift-eliminator blade profiles also enhances wet-mode efficiency, allowing plants in moderate climates to operate hybrids with minimal water penalty. Conversely, dry towers represent an essential solution for arid or drought-prone areas, although their high capital intensity limits their adoption outside government-mandated contexts. Suppliers are countering the cost hurdle through taller finned-tube bundles and enhanced tube-surface coatings that elevate heat-transfer coefficients, thereby reducing footprint. Collectively, these advances illustrate how product evolution, rather than outright technology substitution, sustains momentum in the field-erected cooling tower market.

By Design: Induced Draft Maintains Technical Leadership

Induced draft configurations represented 61.80% of 2025 revenue and will likely preserve dominance through 2031 as the design balances strong airflow with structural adaptability. Mounting the fan stack at the top of the tower creates a negative pressure zone that draws uniform air through the fill media, yielding high heat-transfer rates while minimizing recirculation. This aerodynamic advantage enables induced draft units to support variable load profiles typical of grid-balancing gas turbines, peaking boilers, and combined heat and power plants. The design’s inherent flexibility supports segmentation, for example,e multi-cell arrays that can be isolated for maintenance without derating entire power blocks.

Natural draft towers, in contrast, utilize buoyancy rise to move air and thus consume little to no auxiliary power. They remain favored for baseload nuclear installations exceeding 1 GW, but command significant civil works budgets because hyperbolic concrete shells can reach heights of up to 200 m. Forced draft designs remain relevant in space-constrained industrial facilities where a low overall height is mandatory; however, bottom-mounted fans can draw warm discharge air back into the tower, thereby degrading thermal performance. Adoption choices are therefore project-specific; yet, incremental gains in low-noise axial fans, composite gear housings, and high-efficiency drift eliminators continue to reinforce induced draft supremacy within the field-erected cooling tower market.

By End User: Power Generation Drives Market Evolution

Power producers accounted for 47.90% of global revenue in 2025, underscoring the integral relationship between condenser back-pressure and plant heat-rate performance. Every percentage point improvement in condenser vacuum can increase net thermal efficiency by several basis points, resulting in fuel savings and lower emission intensity. That economic lever, combined with continual capacity additions in coal-, gas-, and biomass-fired sectors, ensures that power generation will remain the primary demand center. The field-erected cooling tower market size for power producers is projected to grow ata 5.83% CAGR, outpacing population-weighted electricity consumption due to stringent efficiency upgrades even at existing stations.

Beyond utilities, refineries and petrochemical complexes collectively form the second-largest customer block. Their process streams require tight temperature control to protect catalysts and maximize throughput, making high-reliability cooling towers essential. Continuous casting lines in steel mills and high-vacuum digesters in pulp and paper plants also rely on robust heat-rejection infrastructure. Meanwhile, data-centre operators are emerging as a fast-rising niche. Hyperscale facilities exceeding 100 MW are evaluating district heat-reuse schemes, which often require customized tower configurations with two-stage heat-exchanger loops, redundancies, and ultra-low noise ceilings. This expanding vertical diversification contributes additional resilience to the field-erected cooling tower market over the forecast horizon.

Geography Analysis

The Asia-Pacific region retained 42.10% of global revenue in 2025 and is projected to grow at a 6.92% CAGR to 2031, driven by aggressive thermal power additions, industrial expansion, and supportive state investment in transmission infrastructure. China’s deployment of ultra-supercritical coal units and India’s pipeline of >80 GW of new capacity demonstrate the scale of ongoing demand. The rapid build-out of petrochemical clusters in Indonesia and Vietnam further amplifies the regional pull for advanced cooling technologies. Local tower fabrication yards in China’s Jiangsu province and India’s Maharashtra state reduce logistics costs and nurture domestic skill bases, reinforcing competitive cost advantages that keep Asia-Pacific at the heart of the field-erected cooling tower market.

North America ranks second by value, anchored by an entrenched fleet of coal and nuclear stations facing tightening environmental performance standards. The region’s market grows largely through retrofits, hybrid conversions, and life-extension projects rather than fresh capacity. Environmental Protection Agency (EPA) rules on water intake and hazardous air pollutants increase compliance complexity, prompting utilities to adopt high-efficiency drift eliminators, plume control modules,, advanced water chemistry systems. Parallel demand emerges from data centre clusters in Virginia’s Loudoun County and Oregon’s Columbia River corridor, where utility rebates for heat reuse strengthen the business case for field-erected installations capable of district energy integration.

Europe maintains a technology-driven profile centered on decarbonization, noise abatement, and water stewardship. Most EU member states enforce stringent pollution visibility thresholds, which accelerate the adoption of hybrid towers. Hydrogen-ready gas turbines and waste-to-energy plants also require bespoke cooling solutions, a trend exemplified by Denmark’s first WtE plant with integrated carbon capture in Aalborg. Composite fill packs engineered for low-chloride, high-alkalinity water accommodate recirculated condensate streams, underscoring the interplay between process chemistry and tower design.

Latin America and the Middle East & Africa together add a smaller yet important growth pocket. Brazil and Saudi Arabia are advancing combined-cycle plants tied to gas discoveries, while South Africa examines dry-cooling retrofits to mitigate freshwater shortages. Local engineering expertise remains uneven; therefore, global suppliers often partner with regional EPC firms for civil works and commissioning. Financial closure challenges arise when sovereign credit risk increases lending costs, yet multilateral climate funds are increasingly supporting hybrid or dry installations that conserve water, thereby gradually enhancing market viability in these regions.

Competitive Landscape

The field-erected cooling tower market is moderately consolidated. SPX Technologies, Babcock & Wilcox, EVAPCO, Jiangsu Shuangliang, and Hamon collectively controlled slightly more than 60% of the global revenue in 2024, according to company disclosures. Scale affords these firms broad reference lists, vertical integration of key components such as gearboxes and FRP panels, and the capacity to absorb commodity price shocks. SPX Technologies recorded 32.5% year-over-year growth in 2024 cooling product sales, driven by large retrofit orders in the United States and turnkey hybrid installations in Germany.

Babcock & Wilcox displayed similar momentum, booking USD 889.6 million in new orders in Q4 2024, its largest quarterly intake on record, as utilities adopted its SolveBright™ modular carbon-capture tower retrofits, which dovetail with thermal-plant cooling upgrades. EVAPCO, in turn, expanded its dry-cooling footprint by acquiring a Dutch finned-tube specialist, reinforcing European market access and adding proprietary tube-coating technology that reduces fouling in biomass applications.

Competitive differentiation now centres on lifecycle digital services, acoustic optimisation, and ESG-linked performance guarantees. Suppliers embed IIoT sensors that feed cloud-based analytics, predicting fill fouling, fan vibration, and drift losses. They also pursue design-for-disassembly principles to meet circular economy directives and offer carbon footprint certification at the component level. New entrants gravitate toward niche segments, such as geothermal, data-center district energy, and solar tower CSP, leveraging agile engineering teams and composite expertise. However, market entry barriers remain elevated because multi-megawatt installations require proven computational modeling, global logistics capabilities, and access to dedicated erection crews.

Field-Erected Cooling Tower Industry Leaders

SPX Cooling Technologies, Inc.

Hamon & Cie International SA

Paharpur Cooling Towers Ltd

Enexio Management GmbH

Babcock & Wilcox Enterprises Inc. (SPIG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tower Tech showcased modular composite towers at the 2025 AHR Expo, while Delta Cooling Towers launched the TMX Series featuring non-corrosive casings and reduced footprint.

- September 2024: Babcock & Wilcox secured a FEED contract for Canada’s first WtE plant with carbon capture in Alberta, covering waste-fired boilers and associated cooling infrastructure.

- August 2024: Holtec initiated a major cooling-system upgrade at the Palisades nuclear plant in Michigan, installing a heat exchanger that is double the previous size to manage rising Lake Michigan temperatures.

- June 2024: Babcock & Wilcox agreed to advance a biomass-fuelled carbon-capture project at Filer City, Michigan, capable of removing 550,000 tons of CO₂ annually.

Global Field-Erected Cooling Tower Market Report Scope

The field-erected cooling tower market report includes:

| Wet |

| Dry |

| Hybrid |

| Natural Draft |

| Induced Draft |

| Forced Draft |

| Power Generation |

| Petrochemicals |

| Oil and Gas |

| Iron and Steel and Metallurgy |

| Paper Mills |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Wet | |

| Dry | ||

| Hybrid | ||

| By Design | Natural Draft | |

| Induced Draft | ||

| Forced Draft | ||

| By End User | Power Generation | |

| Petrochemicals | ||

| Oil and Gas | ||

| Iron and Steel and Metallurgy | ||

| Paper Mills | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the field-erected cooling tower market?

The field-erected cooling tower market size reached USD 3.09 billion in 2026 and is projected to grow to USD 4.06 billion by 2031.

Which end-user sector dominates demand?

Power generation leads, accounting for 47.90% of 2025 revenue and expected to advance at a 5.83% CAGR through 2031.

Why are hybrid cooling towers gaining popularity?

Hybrid systems comply with stricter plume-abatement regulations while retaining the thermal efficiency of wet cooling in most operating hours.

Which region offers the highest growth potential?

Asia-Pacific is forecast to record a 6.92% CAGR to 2031 due to extensive thermal-power additions and expanding industrial capacity.

How are raw-material price swings affecting suppliers?

Volatility in steel and resin prices compresses margins for small firms, accelerating consolidation toward larger players with hedging capabilities.

What technological trends are shaping future competition?

Modular FRP construction, IoT-enabled performance monitoring and low-noise fan designs are central to differentiation among leading vendors.

Page last updated on: