Cooling Tower Rental Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 1.97 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

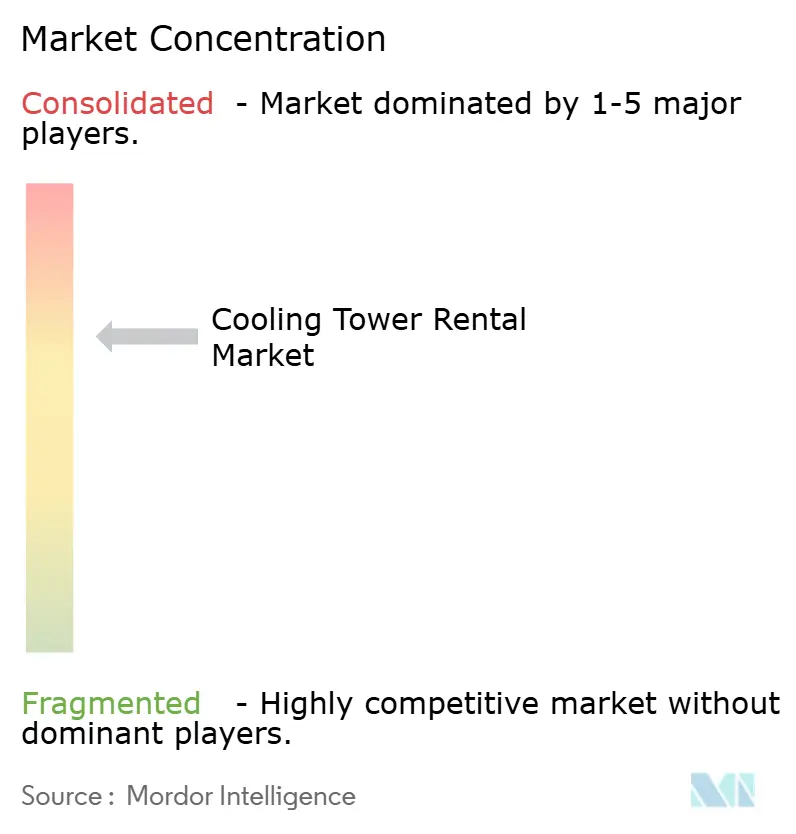

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cooling Tower Rental Market Analysis by Mordor Intelligence

The Cooling Tower Rental Market size is expected to grow from USD 1.39 billion in 2025 to USD 1.47 billion in 2026 and is forecast to reach USD 1.97 billion by 2031 at 5.98% CAGR over 2026-2031.

Expanding data center footprints, longer industrial maintenance cycles, and climate-driven cooling needs collectively reshape the demand profile for cooling tower rentals. Providers benefit from modular tower designs that shorten installation times, while hyperscale data centers drive orders exceeding 20 MW, which in turn lift average contract values. Clients view rental cooling as an operational service rather than a fixed asset, which redirects capital budgets toward core production upgrades. Consolidation among rental specialists accelerates global coverage, although regional players continue to capture niche events that require rapid deployment.

Key Report Takeaways

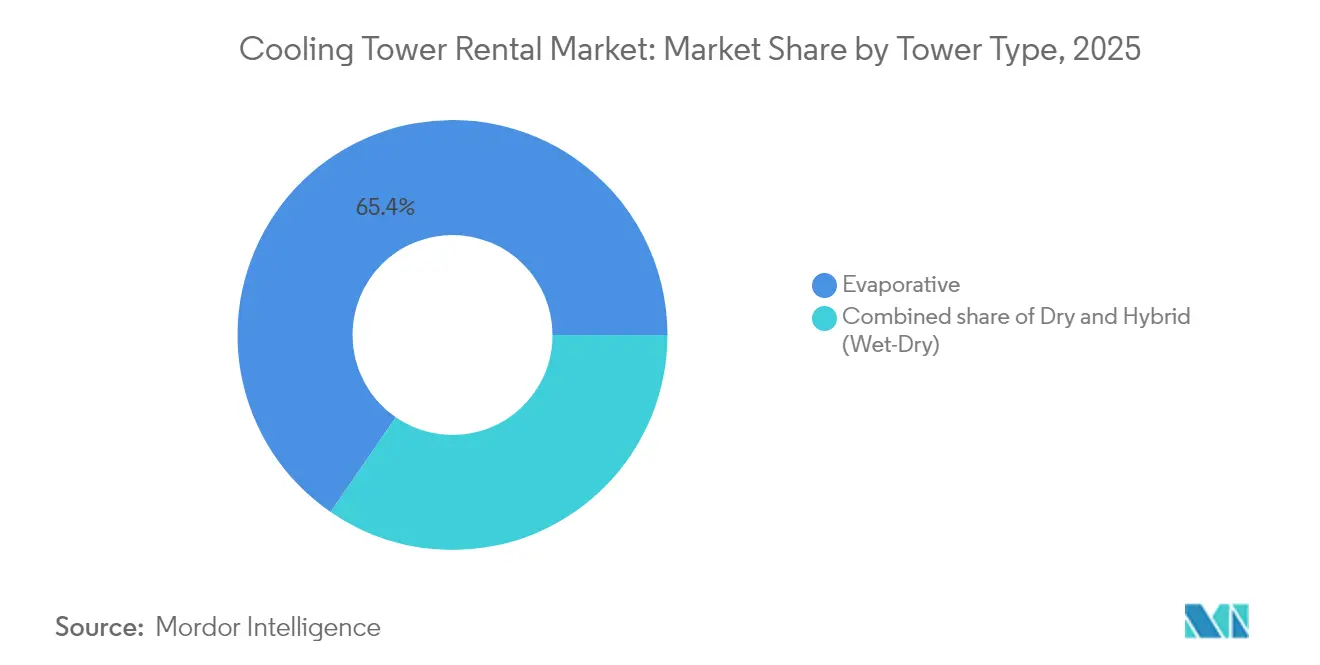

- By tower type, evaporative systems held 65.40% of the cooling tower rental market share in 2025, while hybrid towers are projected to post an 8.35% CAGR through 2031.

- By capacity range, 5-20 MW installations accounted for 42.60% of the cooling tower rental market size in 2025; units above 20 MW are projected to grow at a 7.55% CAGR through 2031.

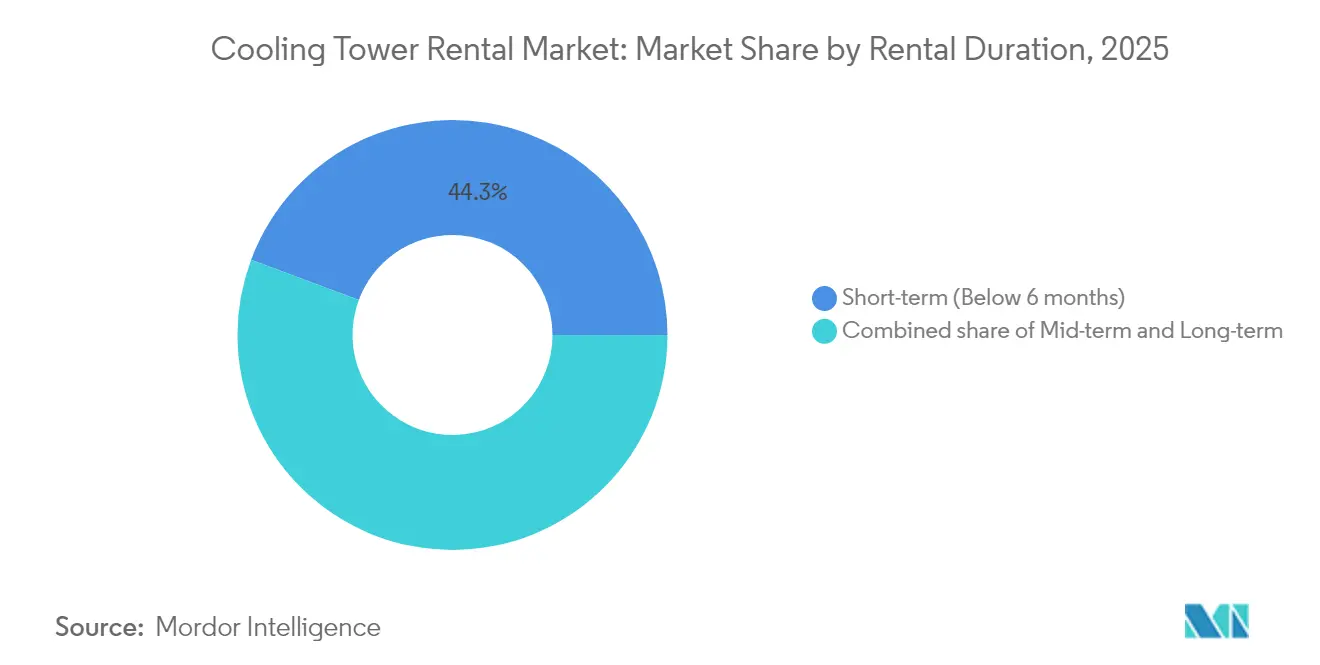

- By rental duration, short-term contracts of under six months captured a 44.30% share of the cooling tower rental market in 2025, whereas mid-term rentals of six to 24 months are expected to expand at a 7.12% CAGR.

- By end-user industry, the oil and gas sector commanded 27.40% of the cooling tower rental market size in 2025, but data centers are expected to record the fastest growth rate of 9.28% through 2031.

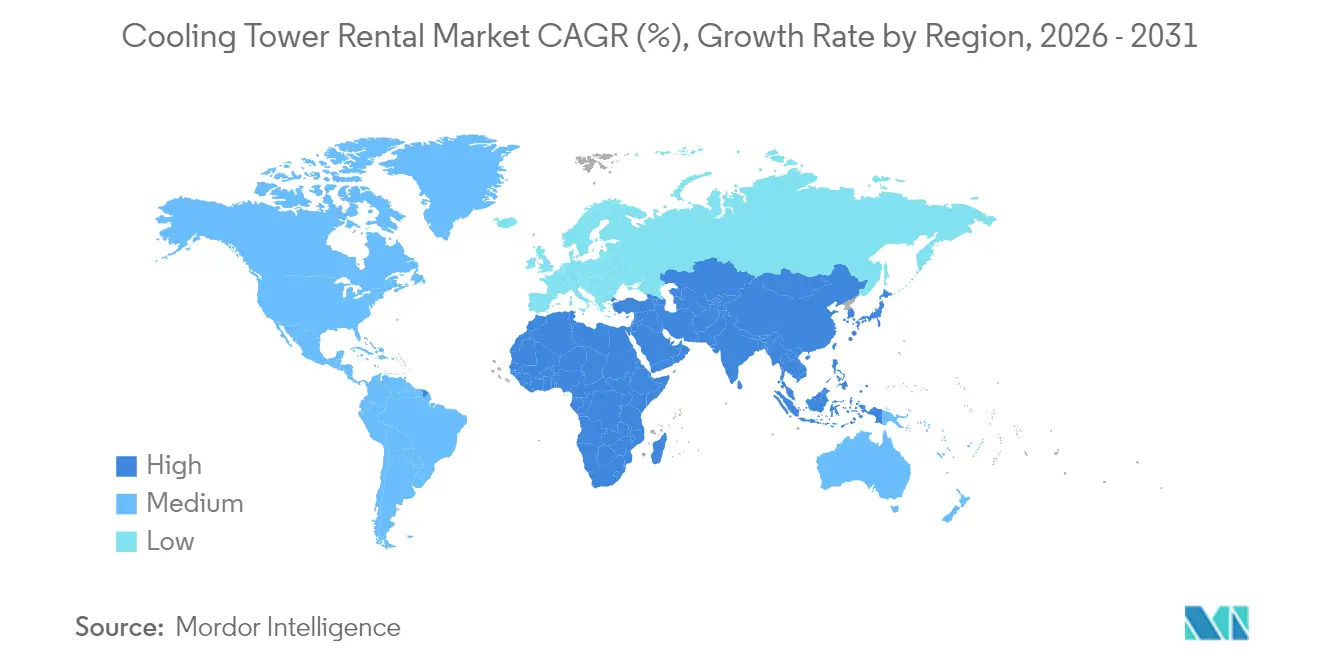

- By geography, North America led with a 36.40% revenue share in 2025; the Asia-Pacific region is forecast to register a 10.02% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cooling Tower Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing frequency of industrial maintenance shutdowns | +1.20% | Global, with concentration in North America & Europe industrial hubs | Medium term (2-4 years) |

| Rapid build-out of data centres requiring temporary cooling redundancy | +1.80% | North America & Asia-Pacific, spill-over to Europe | Short term (≤ 2 years) |

| Stricter environmental regulations favouring high-efficiency rental towers | +0.90% | Europe & North America, early adoption in developed APAC markets | Long term (≥ 4 years) |

| Surge in mega-events in emerging economies driving short-term demand | +0.60% | Asia-Pacific & Middle East, with gains in Qatar, UAE, India | Short term (≤ 2 years) |

| Climate-induced heatwaves triggering emergency cooling deployments | +0.80% | Global, with acute impact in Middle East, Southern Europe, Southwest US | Medium term (2-4 years) |

| Modular plug-and-play designs reducing installation time and cost | +0.70% | Global, with early gains in North America, Europe, developed APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Frequency of Industrial Maintenance Shutdowns

Longer turnarounds increase temporary cooling requirements, especially within petrochemical and refining hubs, where shutdown windows now extend to eight weeks. Rental partnerships enable operators to avoid permanent capital outlays while ensuring heat-rejection reliability during overhaul periods. Contracts for refinery cooling now account for 60% of one leading provider’s industrial revenue, a shift from emergency-only demand. Vendors that bundle water treatment and on-site technicians tend to strengthen renewal rates, as clients prefer single-invoice service packages. This driver underpins baseline growth in the cooling tower rental market across mature economies.

Rapid Build-out of Data Centres Requiring Temporary Cooling Redundancy

Hyperscale projects often commission permanent chillers late in the construction process, leaving a 3- to 6-month gap in which rental towers maintain server-safe temperatures. The Asia-Pacific region added 1,622 MW of new IT load in 2024, creating an unprecedented surge in short-term rentals. Rental fleets integrate variable-speed fans and low-GWP refrigerants, enabling data center owners to meet sustainability targets during the ramp-up phase. Providers offering 24-hour remote monitoring reduce onsite staffing costs for clients operating around-the-clock facilities. These advantages position rental cooling as an essential bridge technology in the digital infrastructure buildout.(1)Cushman & Wakefield, “Global Data Center Market Comparison 2025,” cushmanwakefield.com

Stricter Environmental Regulations Favouring High-Efficiency Rental Towers

National emission and Legionella control rules increase compliance complexity for fixed towers, encouraging temporary solutions with built-in monitoring. The U.S. EPA standards on hazardous air pollutants encourage factories to adopt rental fleets equipped with high-efficiency drift eliminators. In New York, mandatory cooling-tower registries drive demand for rental units equipped with certified water-treatment protocols, thereby sparing property owners the costly expense of retrofits. Providers differentiate through IoT-enabled dosing systems that maintain water chemistry within mandated limits. These developments steadily raise the minimum performance bar in the cooling tower rental market(2)U.S. Environmental Protection Agency, “National Emission Standards for Hazardous Air Pollutants,” epa.gov

Modular Plug-and-Play Designs Reducing Installation Time and Cost

Containerised towers arrive pre-wired and pre-piped, shrinking onsite assembly from three days to less than eight hours. Quick-connect manifolds cut crane hours, a significant cost element on congested brownfield sites. Standardised skids also simplify cross-border redeployments, letting owners reposition assets to meet seasonal peaks. Faster mobilisation increases asset turnover, enhancing overall fleet utilisation and revenue yield. Vendors investing in modularity thus capture a lasting efficiency dividend.(3)SPX Technologies, “MD Everest Cooling Tower Brochure,” spx.com

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating expense relative to permanent installations | -0.80% | Global, with higher sensitivity in cost-conscious emerging markets | Long term (≥ 4 years) |

| Logistics complexity for large-scale towers in remote sites | -0.50% | Global, with acute impact in remote oil & gas sites, mining locations | Medium term (2-4 years) |

| Skilled labour shortages for on-site setup and water treatment | -0.40% | North America & Europe, spill-over to developed APAC markets | Long term (≥ 4 years) |

| Growing preference for air-cooled chillers as substitute rentals | -0.30% | Global, with early adoption in water-scarce regions like Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Operating Expense Relative to Permanent Installations

Total rental outlays exceed ownership costs after two years in many emerging markets where low-cost labor reduces maintenance overhead for fixed towers. Capital-rich petrochemical operators in the Gulf Cooperation Council often favour ownership for projects with 10-year horizons. This cost gap challenges providers to develop energy-efficient motors and automated dosing systems that lower runtime expenses. Fleet digitalisation also cuts technician call-outs, narrowing the long-term cost delta. Price-sensitive regions will remain selective users, thereby curbing the cooling tower rental market's penetration in multi-year applications.

Logistics Complexity for Large-Scale Towers in Remote Sites

Above-20 MW towers require multi-axle trailers and heavy-lift cranes that are scarce in remote basins. Freight and rigging charges can triple the equipment fee, making rentals unattractive for some well pads and mines. Providers invest in knock-down modules that fit inside ISO containers to bypass oversize road permits. Coordinating cross-border shipments, however, still demands specialist experience and local brokerage networks. These hurdles slow adoption in frontier geographies despite latent demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tower Type: Evaporative Systems Retain Primacy Amid Hybrid Uptake

Evaporative units accounted for 65.40% of the cooling tower rental market in 2025, reflecting decades-long industrial familiarity and superior heat-rejection efficiency. Hybrid wet-dry models are forecast to grow at an 8.35% CAGR through 2031 as governments tighten regulations on water draw and plume drift.

Rental providers bulk up hybrid fleets to address pharmaceutical plants and data halls located in drought-prone regions. The cooling tower rental market size for hybrid designs benefits from modular cells that operators can incrementally add during hot seasons and then downsize in cooler months. Dry towers remain vital in areas where water discharge is restricted, such as semiconductor fabs that must limit their effluent. Evaporative systems nevertheless maintain cost leadership on a per-megawatt basis, preserving their dominance in refinery turnarounds and petrochemical debottlenecking. Suppliers integrate variable-frequency drives and drift eliminator upgrades to meet emerging efficiency codes without sacrificing baseline performance.

Incremental design innovations support both water stewardship and rapid deployment. Telescoping fan stacks reduce freight height, cutting transport fees on interstate hauls. Composite fill media extends service intervals, lowering chemical consumption by 15%. Providers able to balance these operational advantages position themselves for sustained share retention across the cooling tower rental market.

By Capacity Range: Mid-Range Comfort Zone Faces Hyperscale Pull

Installations between 5-20 MW accounted for 42.60% of the cooling tower rental market size in 2025, as this band aligns with typical refinery units and colocation data halls. Contracts exceeding 20 MW are projected to rise at a 7.55% CAGR through 2031, driven by hyperscale cloud deployments and large LNG terminal upgrades.

Clients with multi-rack AI clusters need sustained high-density cooling loads that push rental tower banks to new capacities. Vendors respond by grouping modular cells into 30 MW clusters with common header piping, which cuts onsite labor by one-third. Below-5 MW rentals continue to serve food processing lines and commercial HVAC retrofits, but offer limited revenue upside per contract.

Hyperscale growth also drives ancillary services such as power distribution skids and real-time SCADA portals, deepening provider account penetration. This momentum reshapes fleet mix, shifting capital budgets toward heavier lift modules while still retaining mid-range units for bread-and-butter industrial maintenance cycles. High-capacity adoption thus rebalances utilization ratios while broadening revenue potential within the cooling tower rental market.

By Rental Duration: Strategic Mid-Term Hires Gain Momentum

Contracts shorter than six months remained the largest slice, at 44.30%, in 2025, due to emergency outages and planned shutdowns. Mid-term rentals lasting six to 24 months will grow at a 7.12% CAGR, indicating that users now embed temporary cooling into broader capital planning.

Data center developers frequently book 12-month agreements to hedge commissioning delays. Specialty chemical producers schedule extended pilots that require flexible heat rejection without permanent capital allocation. The shift lengthens revenue recognition per asset and stabilises seasonal swings for providers. Long-term rentals exceeding two years are a niche market, servicing remote pipeline camps and contracted power barges where permanent towers are impractical.

Suppliers equip mid-term deals with IoT gateways that transmit vibration and conductivity data, enabling predictive maintenance that keeps uptime above 99.5%. This service overlay cements client loyalty and raises switching barriers. Accordingly, mid-term growth has a material influence on cash-flow durability within the cooling tower rental market.

By End-User Industry: Oil & Gas Holds Sway as Data Center Surge Accelerates

Oil & gas users held 27.40% of the cooling tower rental market in 2025, anchored by refinery shutdowns and gas-processing debottlenecks. Data centers are expected to post the fastest 9.28% CAGR to 2031, driven by surging AI and cloud workloads.

Chemical and petrochemical complexes secure steady demand due to multi-year maintenance cycles and strict process-temperature control. Power utilities rent towers to smooth out peaking output during heatwaves, particularly as grids incorporate more renewable variability. HVACR managers in high-rise commercial buildings adopt rental units during chiller replacements to avoid occupant downtime.

Data center operators prioritise energy efficiency and water stewardship, prompting vendors to supply hybrid towers coupled with adiabatic coolers that lower water use by 60%. Bundled telemetry enables colocation firms to demonstrate environmental metrics to hyperscale tenants, solidifying the rental model as part of sustainability reporting. This end-user realignment diversifies the cooling tower rental market revenue base beyond traditional hydrocarbons.

Geography Analysis

North American revenue dominance stems from mature logistics corridors that enable same-day tower mobilisation across most industrial zones. The United States ranks first in fleet density, serving both Permian Basin gas plants and Virginia’s data-center alley. Canada’s oil-sand upgraders favour rentals during spring thaw maintenance, while Mexico’s automotive belt opts for mid-term hires that align with capacity ramp-ups. Continued refinery decarbonization retrofits support demand of 5-20 MW, preserving North America’s leadership position in the cooling tower rental market.

The Asia-Pacific’s double-digit CAGR stems from national broadband agendas and cloud-service localization policies that necessitate rapid data hall buildouts. China’s Eastern Data Western Compute strategy places hyperscale campuses in cooler northern provinces, yet construction phases still depend on rental towers to bridge commissioning delays. India’s renewable-powered IT parks adopt hybrid wet-dry units to limit water draw, while Japan’s seismic codes favour modular skids that cut onsite crane lifts. Regional governments also sponsor mega-events, further broadening short-term rental opportunities.

Europe advances at a steadier pace, led by Germany’s industrial retrofits and the United Kingdom’s edge-data roll-outs. Stricter Legionella rules push hospitals and commercial estates toward rental swaps during permanent tower refurbishments. Southern Europe’s heatwaves drive seasonal spikes in grid-support cooling, raising off-balance-sheet demand. Eastern Europe utilizes rentals to maintain legacy power plants online during turbine overhauls, thereby reinforcing cross-border fleet redeployment efficiencies across the cooling tower rental market.

Competitive Landscape

The market structure remains moderately fragmented, with the top five vendors collectively holding approximately 42% of the revenue, resulting in a medium concentration score. United Rentals’ USD 4.8 billion purchase of H&E Equipment Services in 2025 added nearly 64,000 assets and strengthened its specialty divisions, focusing on power and HVAC. Aggreko expands its petrochemical turnkey services by bundling fuel management with cooling, enabling the locking in of multi-site contracts. Sunbelt Rentals acquires regional firms to secure depots within 50 miles of major industrial clusters, thereby maintaining competitive response times.

Technology partnerships differentiate leaders. Johnson Controls created a Global Data Center Solutions unit that integrates YORK magnetic-bearing chillers with rental towers, offering energy savings of up to 40% for temporary deployments. SPX Technologies markets composite-fill retrofit kits that cut water consumption by 20%, appealing to sustainability-minded data tenants. Smaller regional players compete through deep local knowledge and flexible pricing, winning rapid-response projects such as stadium retrofits and remote mine shutdowns.

Digital capabilities shape the next battleground. Providers deploy edge-installed vibration sensors that feed cloud analytics, forecasting bearing wear ten days in advance, thereby minimizing unplanned downtime. Augmented-reality support accelerates field training, easing skilled-labour bottlenecks. Companies that merge equipment scale with data intelligence are set to outpace rivals as the cooling tower rental market shifts toward performance-based service agreements.

Cooling Tower Rental Industry Leaders

Aggreko plc

Caterpillar Inc.

United Rentals, Inc.

SPX Cooling Technologies, Inc.

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Johnson Controls has established a new Global Data Center Solutions organization to enhance its capacity to deliver specialized cooling solutions for large-scale data centers, particularly for hyperscale projects.

- January 2025: United Rentals finalized the acquisition of H&E Equipment Services for USD 4.8 billion, adding approximately 64,000 units to its rental fleet and aiming for USD 130 million in annual cost synergies. The deal is expected to close in the first quarter of 2025.

- December 2024: AirX Climate Solutions, Inc., a leading full-service provider of specialty HVAC solutions, announced today that it has acquired Powrmatic USA, a premier designer and manufacturer of specialty HVAC products and solutions, including cooling and heating air turnover systems.

- June 2024: Johnson Controls has introduced the YORK YVAM chiller, which achieves a 40% reduction in energy consumption compared to conventional chillers and requires no on-site water.

- May 2024: Sunbelt Rentals finalized the acquisition of Rentalmax, one of 26 acquisitions totaling USD 845.6 million. This purchase is part of a broader strategy to expand Sunbelt's presence in the equipment rental market.

Global Cooling Tower Rental Market Report Scope

The cooling tower rental market report includes:

| Evaporative |

| Dry |

| Hybrid (Wet-Dry) |

| Below 5 MW |

| 5 to 20 MW |

| Above 20 MW |

| Short-term (Less than 6 months) |

| Mid-term (6-24 months) |

| Long-term (Greater than 24 months) |

| Oil and Gas |

| Chemical and Petrochemical |

| Power Generation |

| HVACR (Commercial Buildings) |

| Data Centers |

| Pulp and Paper |

| Food and Beverage |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Tower Type | Evaporative | |

| Dry | ||

| Hybrid (Wet-Dry) | ||

| By Capacity Range | Below 5 MW | |

| 5 to 20 MW | ||

| Above 20 MW | ||

| By Rental Duration | Short-term (Less than 6 months) | |

| Mid-term (6-24 months) | ||

| Long-term (Greater than 24 months) | ||

| By End-user Industry | Oil and Gas | |

| Chemical and Petrochemical | ||

| Power Generation | ||

| HVACR (Commercial Buildings) | ||

| Data Centers | ||

| Pulp and Paper | ||

| Food and Beverage | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current cooling tower rental market size?

The cooling tower rental market size stands at USD 1.47 billion in 2026 and is projected to reach USD 1.97 billion by 2031 based on a 5.98% CAGR.

Which tower type leads the cooling tower rental market?

Evaporative systems lead with a 65.40% share, while hybrids are the fastest-growing on an 8.35% CAGR to 2031.

Why are data centers boosting demand for rental cooling?

Hyperscale builds use rental towers for 3-to-6-month commissioning gaps, driving a 9.28% CAGR for data-center demand through 2031.

Which region is the fastest-growing?

Asia-Pacific is forecast to post a 10.02% CAGR due to massive digital-infrastructure investments and supportive government policies.

How does rental duration influence provider revenue?

Mid-term rentals of six-to-24 months are growing at 7.12% CAGR, lengthening contract value and stabilising fleet utilisation for vendors.

Who are the major players in the cooling tower rental market?

United Rentals, Aggreko, Sunbelt Rentals, and Johnson Controls lead through acquisitions, specialty services, and technology-integrated offerings.

Page last updated on: