FEVE Fluoropolymer Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

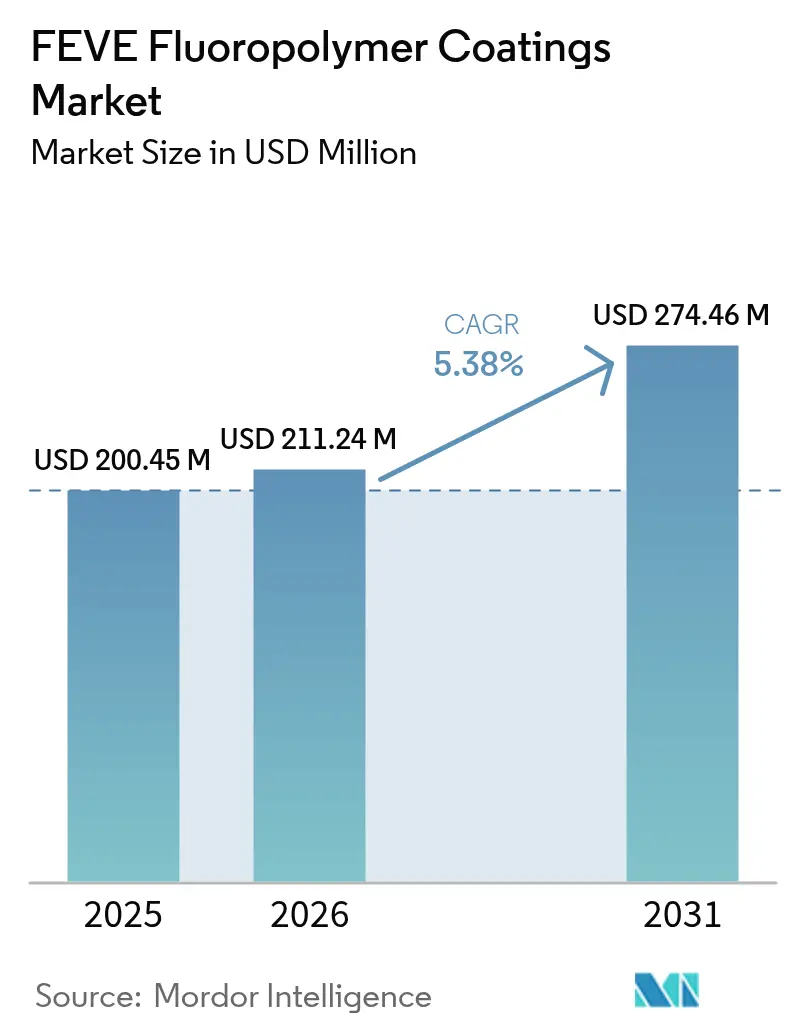

| Market Size (2026) | USD 211.24 Million |

| Market Size (2031) | USD 274.46 Million |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

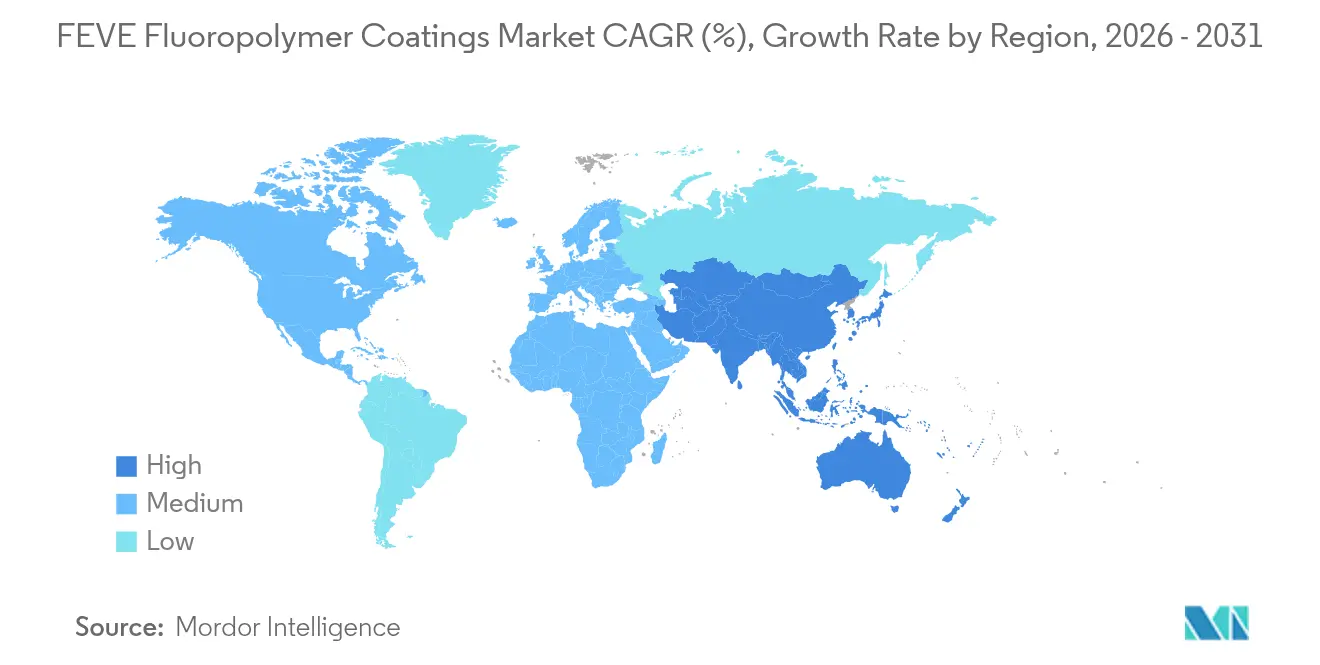

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

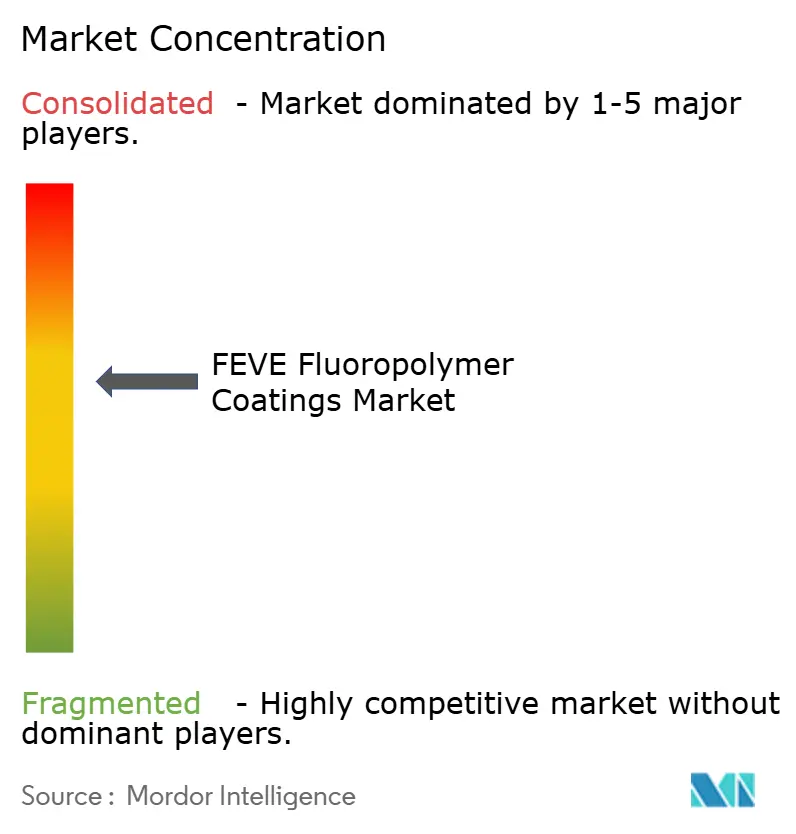

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

FEVE Fluoropolymer Coatings Market Analysis by Mordor Intelligence

The FEVE Fluoropolymer Coatings market size is expected to grow from USD 200.45 million in 2025 to USD 211.24 million in 2026 and is forecast to reach USD 274.46 million by 2031 at 5.38% CAGR over 2026-2031. Demand rests on the resin’s ability to stretch service intervals to 30-60 years, a span that offsets its 2-4 times premium over polyurethane. Infrastructure owners are aligning with new 75-year bridge design lives, while renewable-energy manufacturers require durable powder finishes for solar and wind assets. Additionally, environmental rules favor zero-VOC chemistries. These factors mitigate the impact of headline price sensitivity and emerging polysiloxane substitutes. Moderate supplier concentration lets AGC and Daikin set resin prices, yet evolving manufacturing routes promise cost relief and lower fluorinated by-products.

Key Report Takeaways

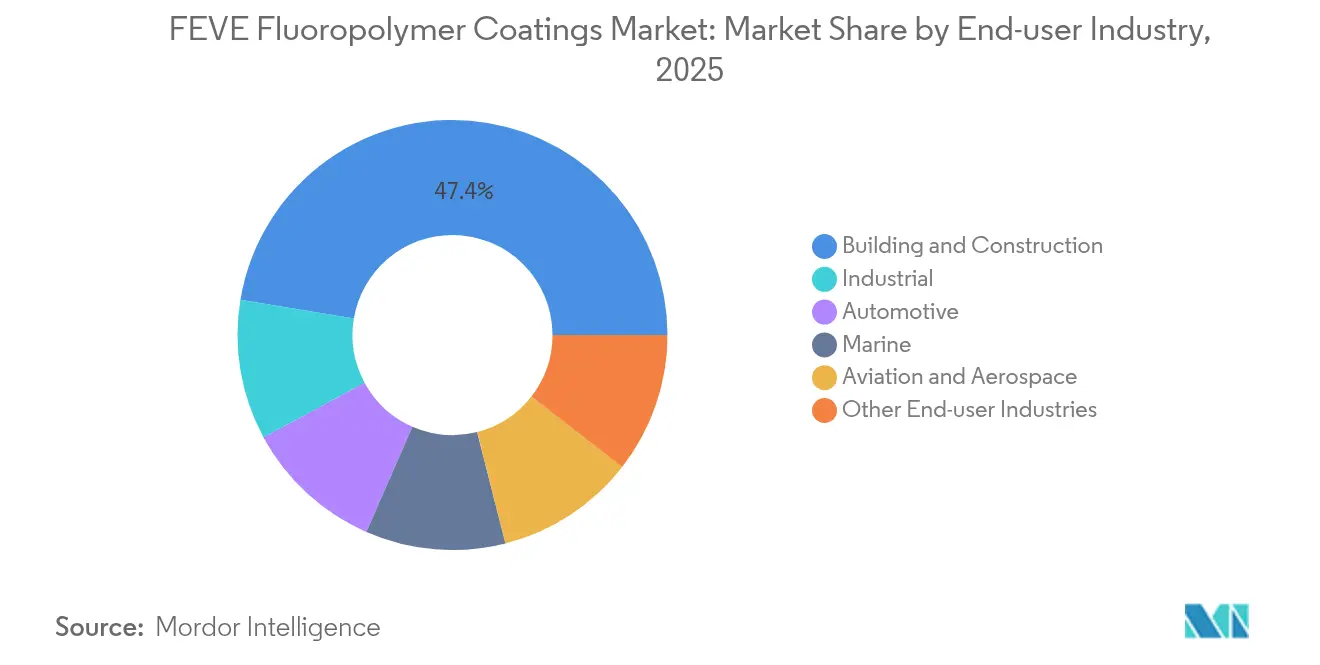

- By end-user industry, the building and construction sector accounted for the largest market share of 47.38% in 2025, and this share is expected to grow at the fastest CAGR of 6.59% during the forecast period (2026-2031).

- By geography, the Asia-Pacific region held a 51.05% share in the FEVE Fluoropolymer Coatings market, and this share is expected to increase at a CAGR of 6.42% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global FEVE Fluoropolymer Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-life facade demand in global construction boom | +1.8% | Global, with concentration in APAC megacities and Middle East | Medium term (2-4 years) |

| Industrial infrastructure corrosion-control programs | +1.2% | North America, Europe, coastal APAC (Japan, South Korea) | Long term (≥ 4 years) |

| Regulatory pivot to low-VOC/high-durability coatings | +1.0% | North America & EU; spillover to ASEAN via multinational specs | Short term (≤ 2 years) |

| Renewable-energy hardware (solar/wind) adoption of FEVE powders | +1.4% | Global, led by China solar capacity and offshore wind (EU, APAC) | Medium term (2-4 years) |

| Government service-life mandates for public bridges & tanks | +0.9% | United States (AASHTO), Japan (MLIT), select EU member states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long-Life Façade Demand in Global Construction Boom

Skyscraper developers select FEVE curtain-wall coatings because the annual film erosion rate stays below 0.1 µm, roughly half that of polyurethane, which limits expensive scaffold cycles. The Japan Paint Manufacturers Association values the total 30-year costs at 37% of those for chlorinated rubber systems when repainting savings are factored in. China, the Gulf states, and Southeast Asia supply the largest pipelines of high-rise projects needing American Architectural Manufacturers Association 2605 compliance. Case studies such as Ferrari World Abu Dhabi and Burj al Arab show FEVE protecting aluminum panels under UV swings exceeding 50°C[1]AGC Chemicals, “Architectural Idea Book,” agcchem.com. Lighter cladding panels permitted by seismic codes intensify the need for low-temperature cures that FEVE powders deliver without panel distortion.

Renewable-Energy Hardware Adoption of FEVE Powders

Photovoltaic module backsheets coated with FEVE sustain more than 95% of initial power after one year of outdoor exposure, outperforming uncoated controls by 10 percentage points. Wind-turbine towers utilize single-coat FEVE powder finishes that cure at temperatures below 200 °C, recycle overspray, and resist salt-spray corrosion in offshore environments. Hybrid FEVE/polyurethane blends reinforced with graphene achieve up to 99% leading-edge erosion resistance, supporting megawatt-scale blade production targets in Europe and China. Supply chains value the resin’s zero-VOC profile as the U.S. and EU ratchet solvent regulations.

Industrial Infrastructure Corrosion-Control Programs

Oil and gas operators confirm that FEVE topcoats maintain 80% electrochemical impedance after 350 hours of combined UV and salt exposure, compared with 35% for polysiloxane. These results justify service specifications of 30-60 years for tanks and offshore platforms. North American bridge agencies, citing National Research Council Canada lifecycle models, note lower direct and social costs where long-life coatings cut traffic disruption.

Regulatory Pivot to Low-VOC/High-Durability Coatings

The US 40 CFR Part 59 caps VOC at 800 g/L for extreme-durability finishes, a ceiling FEVE powders undercut to zero. Europe’s Industrial Emissions Directive mandates substitution assessments by 2027, guiding asset owners toward durable fluoropolymer systems that eliminate the use of heavy-metal primers. Japan’s 4-star formaldehyde rating pushes growth in low-odor FEVE grades for occupied renovations[2]Nippon Paint, “DF Series Launch Release,” nipponpaint.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price versus polyurethane & acrylic systems | -1.1% | Global, most acute in price-sensitive markets (Latin America, Southeast Asia) | Short term (≤ 2 years) |

| Rising PFAS-related regulatory scrutiny in United States/European Union | -0.8% | North America & EU; indirect impact via supply-chain compliance costs globally | Medium term (2-4 years) |

| Shortage of trained applicators & specialized spray equipment | -0.5% | North America, Europe; less acute in APAC where factory coil-coating dominates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Price Versus Polyurethane Systems

FEVE lists at two to four times the price of polyurethane, discouraging adoption in budget-constrained regions. ChemQuest survey data show 2023 architectural volumes dipped 4.6% as remodelers delayed projects, squeezing budgets and elevating first-cost hurdles. Polysiloxane topcoats, priced at 1.5 times the cost of polyurethane, now capture mid-range demand, especially where operators calculate only five- to 15-year horizons. FEVE vendors respond with lifecycle calculators and training to spotlight 15-30% total cost savings over decades.

Rising PFAS-Related Regulatory Scrutiny

The European Chemicals Agency proposes a 50 ppm total-fluorine limit with time-bound derogations as low as 6.5 years, which will inflate testing and documentation costs. The US EPA’s new PFAS reporting rule forces manufacturers to disclose volumes dating back to 2011, exposing potential remediation liability. While no non-fluorinated topcoat currently offers equivalent 30-year gloss retention, regulatory pressure is prompting investment in hybrid chemistries and low-by-product production routes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Building and Construction Maintains Leadership

Building and Construction commanded 47.38% of the FEVE Fluoropolymer Coatings market share in 2025, reflecting the segment’s early embrace of 30-year, single-coat façade programs. The FEVE Fluoropolymer Coatings market size for this segment is projected to expand at a 6.59% CAGR from 2026 to 2031. Curtain-wall owners credit service life extensions that defer two to three repaint cycles, cutting scaffold expenses and tenant disruption in dense urban cores. Japan’s updated bridge standards, which name FEVE as the sole approved topcoat, embed demand across public works.

Industrial equipment follows at a measured pace. Operators in oil and gas weigh FEVE’s longer intervals against polysiloxane options that cost 30-40% less. Automotive applications remain niche, covering specialty vehicles and aluminum trim that require UV and chip resistance. Marine and aviation buyers pursue FEVE for antifouling and wire-bundle protection where acceptable alternatives are scarce. Growing retrofit markets in Asia and North America lean on low-odor, waterborne FEVE grades to avoid occupant evacuation. Powder variants win share in factory-coated roof panels and aluminum extrusions because they cure below 200 °C and recycle overspray. Hybrid FEVE-ceramic blends emerge in bridge arch ribs needing color stability and barrier strength. Demand remains price-sensitive in Latin American municipal projects, yet lifecycle calculators reveal 15-30% cost savings that gradually shift procurement criteria.

Geography Analysis

The Asia-Pacific governs the FEVE Fluoropolymer Coatings market with a 51.05% share in 2025 and a forecasted 6.42% CAGR, driven by Chinese urbanization, Japanese bridge standards, and South Korean offshore fabrication. Chinese coil coaters offer waterborne grades that meet HG/T 4104-2019 to bypass VOC penalties while preserving a 30-year gloss. Japan’s Ministry of Land, Infrastructure, Transport, and Tourism restricts topcoats on public bridges to FEVE, securing premium prices. South Korean yards specify long-life finishes for LNG carrier topsides, reducing dry-dock frequency.

North America accounts for approximately 24.85% of the market. AASHTO’s 75-year bridge design life shifts new construction and rehabilitation to FEVE, illustrated by the I-74 Mississippi River Bridge, where Sherwin-Williams Fluorokem shields 3,400 ft of steel. The EPA’s aerosol rule tightens VOC controls yet raises compliance efforts through PFAS reporting. Canadian lifecycle studies promote low-VOC solutions that reduce social costs, such as traffic congestion. Mexico sees a selective uptake in refinery and specialty vehicle projects, where long service life offsets capital expenditures.

Europe accounts for 17.80% of the value but faces the steepest regulatory tests. The proposed 50 ppm total-fluorine cap will complicate supply chains. Germany and the Nordics lean on FEVE powder grades for offshore wind towers under QUALICOAT Class 3 standards. Southern Europe’s public budgets lag, though airport and retail façades still specify FEVE. Russia’s Arctic pipeline opportunities remain limited amid trade sanctions.

Competitive Landscape

The FEVE Fluoropolymer Coatings market is moderately concentrated. AGC and Daikin supply most base resins, licensing technology to global formulators including PPG, Sherwin-Williams, Axalta, Akzo Nobel, Kansai Paint, and Tnemec. AGC’s 2024 surfactant-free emulsion route aims for commercialization by 2030 and may reduce upstream fluorinated by-products and feedstock costs. Formulators differentiate through application engineering rather than polymer design. Powder lines now deliver single-coat coverage, waterborne systems extend pot life, and hybrid blends marry FEVE’s weatherability with polysiloxane’s lower cost. Chinese newcomers, such as Futant Uliao, offer certified waterborne options for domestic high-rise projects, although AAMA 2605 accreditation and brand recognition limit their export share.

FEVE Fluoropolymer Coatings Industry Leaders

PPG Industries, Inc.

Akzo Nobel N.V.

The Sherwin-Williams Company

AGC Inc.

DAIKIN INDUSTRIES, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mitsubishi Chemical America's (MCA) ALPOLIC Division unveiled its latest metal composite material finishes. These finishes boast the FEVE textured paint system, a result of a strategic collaboration with Sherwin-Williams Coil Coatings.

- May 2025: Elevate unveiled Mountain Black, its latest metal hue, crafted with FEVE (fluoroethylene vinyl ether) resin-based coating technology. Mountain Black is featured across Elevate's portfolios, including metal roofing, edge metal, and wall panels.

Global FEVE Fluoropolymer Coatings Market Report Scope

The FEVE fluoropolymer coatings market report includes:

| Industrial |

| Building & Construction |

| Automotive |

| Marine |

| Aviation & Aerospace |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of APAC | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middel-East and Africa |

| By End-user Industry | Industrial | |

| Building & Construction | ||

| Automotive | ||

| Marine | ||

| Aviation & Aerospace | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of APAC | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middel-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the FEVE Fluoropolymer Coatings market in 2031?

The market is forecast to reach USD 274.46 million by 2031, growing at a 5.38% CAGR.

Which end-user segment leads current demand for FEVE coatings?

Building and Construction dominates with 47.38% market share in 2025 and the fastest 6.59% CAGR through 2031.

Why are FEVE powders gaining traction in renewable energy?

They cure below 200°C, carry zero VOC, and extend solar panel and wind tower lifetimes beyond 25 years.

How does upcoming PFAS regulation affect FEVE suppliers?

Proposed 50 ppm total-fluorine limits in the EU and new US reporting rules will raise testing and traceability costs.

Which region shows the fastest growth?

Asia-Pacific combines a 51.05% share with a 6.42% CAGR, supported by infrastructure spending and long-life bridge standards.

Page last updated on: