Fetal Bovine Serum Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.30 Billion |

| Market Size (2031) | USD 1.75 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

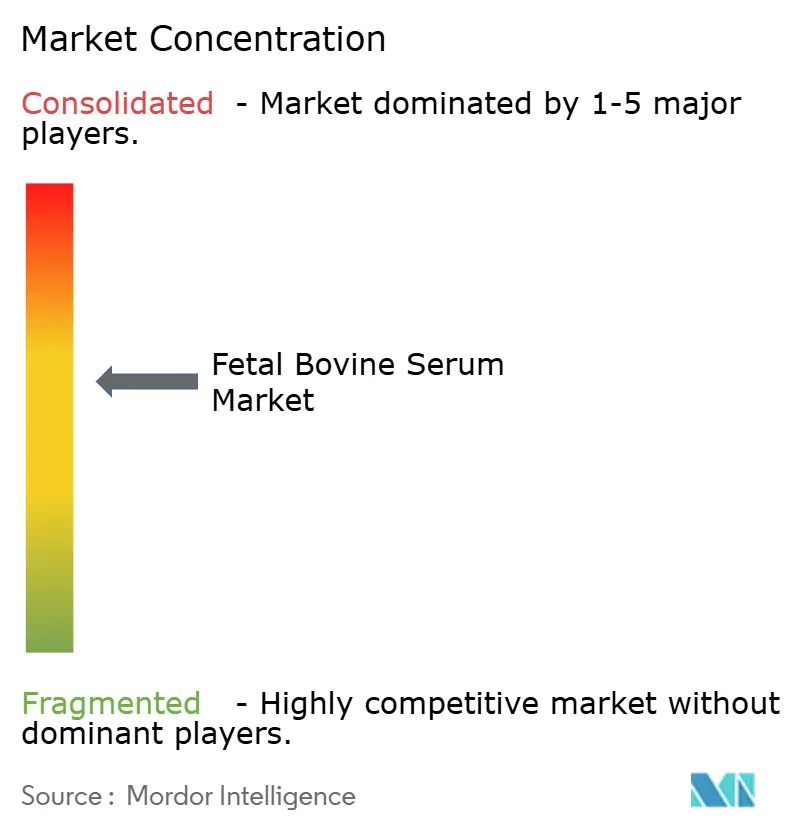

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fetal Bovine Serum Market Analysis by Mordor Intelligence

The fetal bovine serum market size is projected to expand from USD 1.22 billion in 2025 and USD 1.30 billion in 2026 to USD 1.75 billion by 2031, registering a CAGR of 6.2% between 2026 and 2031. Structural demand comes from cell- and gene-therapy pipelines whose clinical assets climbed to 3,049 in Q3 2025, locking in serum use well beyond the current validation cycle. Tight raw-material supply reinforces pricing power; the U.S. cattle inventory fell to 87.2 million head in January 2025, the lowest since 1951. Specialized grades such as charcoal/dextran-stripped serum command premium pricing because they resolve hormone-related assay noise, while stem-cell-qualified lots are gaining share as regenerative-medicine trials scale. Competitive strategy has bifurcated: global suppliers are buying collection networks to secure inputs, whereas regional traders compete on origin traceability.

Key Report Takeaways

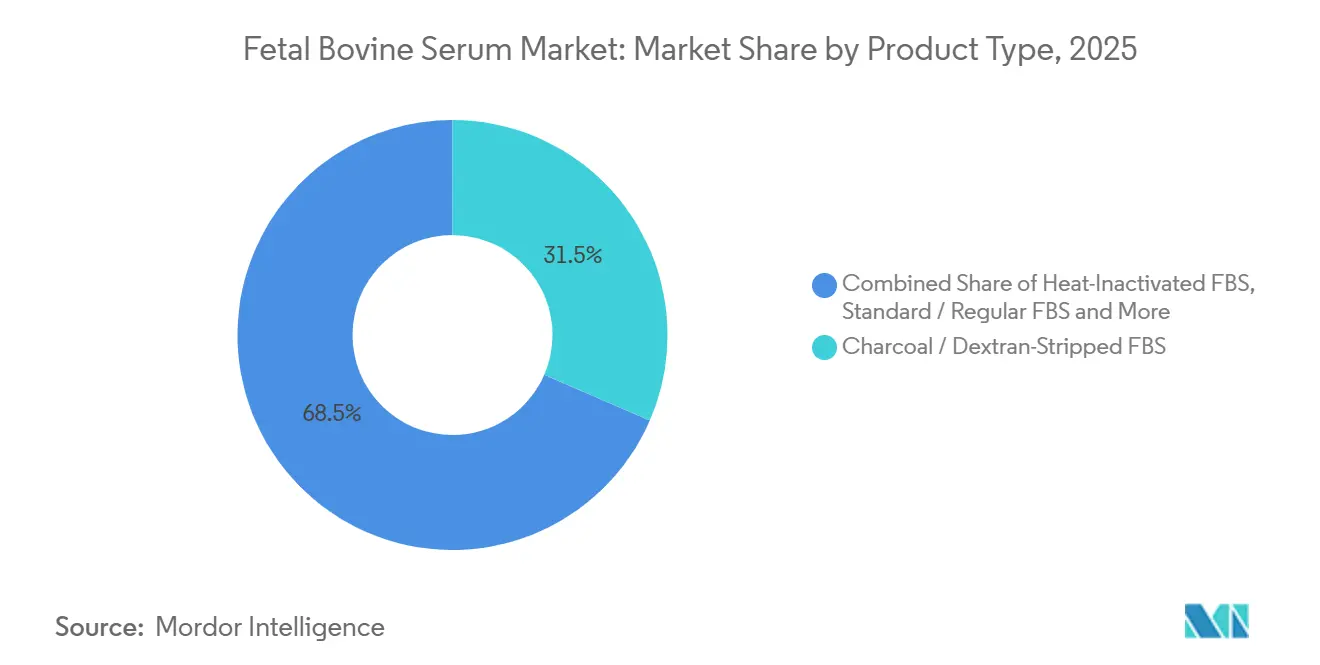

- By product type, charcoal/dextran-stripped serum led with 31.55% of the fetal bovine serum market share in 2025, while stem-cell-qualified FBS is advancing at a 7.25% CAGR to 2031.

- By application, biopharmaceutical production accounted for 32.53% share of the fetal bovine serum market size in 2025, cell-culture maintenance & expansion is advancing at a 6.75% CAGR to 2031.

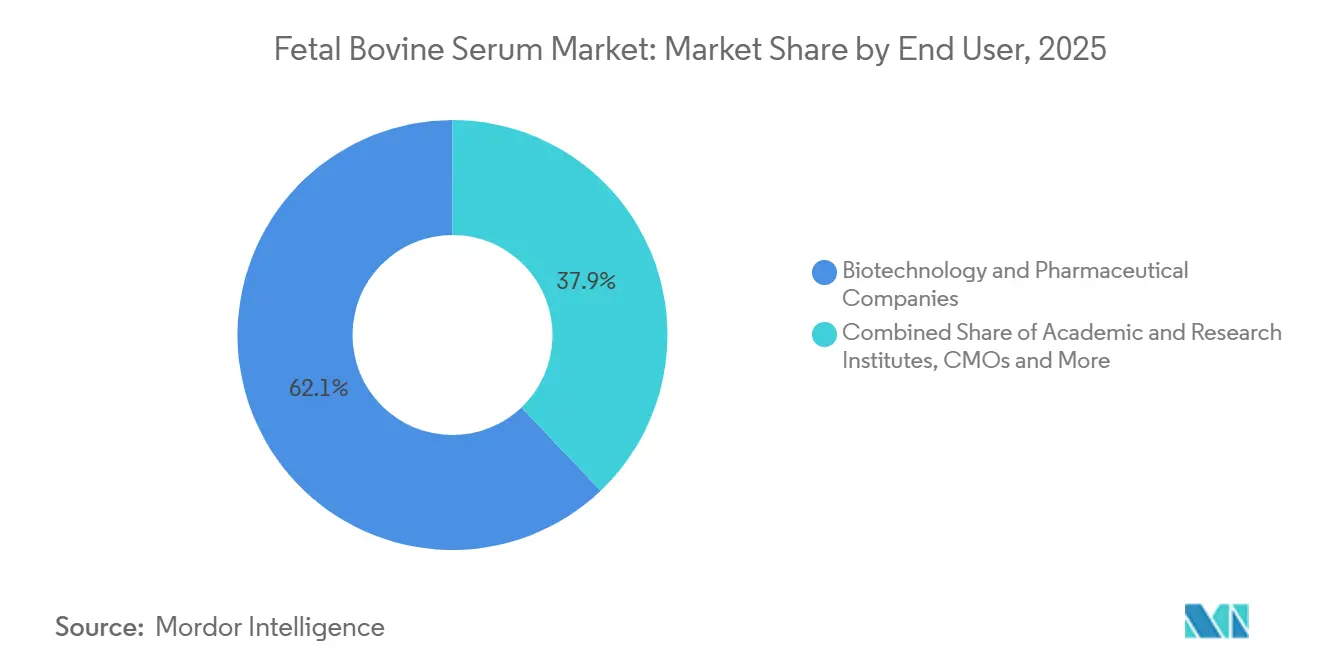

- By end user, biotechnology and pharmaceutical companies controlled 62.15% of 2025 revenue, while academic institutes are advancing at a 6.82% CAGR to 2031.

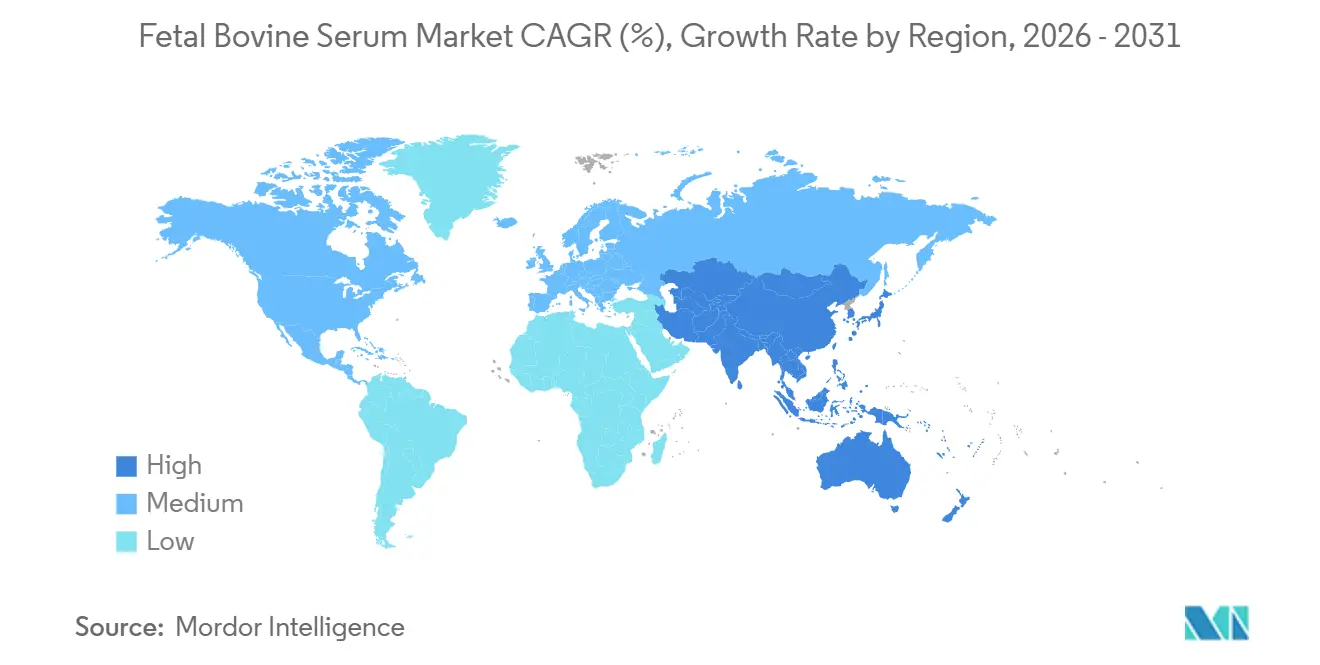

- By geography, North America captured 41.55% of 2025 revenue; Asia-Pacific is projected to grow at 7.22% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fetal Bovine Serum Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid biopharma scale-up post-COVID-19 | +1.8% | Global, with concentration in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Expanding cell & gene-therapy pipelines | +1.5% | North America and Europe lead; Asia-Pacific emerging | Long term (≥ 4 years) |

| Growth in animal & human vaccine output | +1.0% | Global, with emphasis on Asia-Pacific and South America | Medium term (2-4 years) |

| Rise of contract cell-culture manufacturing (CMOs/CROs) | +0.9% | North America and Asia-Pacific | Medium term (2-4 years) |

| Cultured-meat R&D funding surge | +0.4% | North America, Europe, and select Asia-Pacific hubs | Long term (≥ 4 years) |

| U.S. cattle-herd decline tightening FBS supply | +0.6% | Global supply impact, most acute in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Biopharma Scale-Up Post-COVID-19

Capacity built for pandemic biologics is still online and requires routine seed-train maintenance with FBS-supplemented media. A USD 1.6 billion single-use bioreactor expansion announced by Cytiva in 2025 will use serum for process-development runs until at least 2029. Samsung Biologics’ Plant 5 brought 180,000 liters of perfusion volume online in late 2024 and confirms that seed trains remain serum dependent even when production reactors use defined media[1]Samsung Biologics IR Team, “Investor Presentation Q4 2025,” Samsung Biologics, samsungbiologics.com. CMOs, which held 38% of global biologics capacity in 2025, follow client-mandated protocols that specify FBS grades and lot testing, effectively locking in baseline volume. These conditions create a floor under fetal bovine serum market demand despite innovation in serum-free systems.

Expanding Cell & Gene-Therapy Pipelines

Six new cell-therapy indications cleared the U.S. FDA in 2025, each requiring commercial-scale ex vivo culture steps that consume serum. Novartis disclosed that Kymriah sites used 12,000 liters of stem-cell-qualified FBS in 2024, a 19% rise over 2023. Regulatory precedent discourages mid-trial media switches; comparability risks deter sponsors from abandoning validated serum processes. The International Society for Cell & Gene Therapy’s 2025 guidelines call for FBS lot pre-qualification, further embedding serum into late-stage trials. As a result, the fetal bovine serum market receives durable volumes from advanced-therapy pipelines.

Growth in Animal & Human Vaccine Output

Global influenza vaccine capacity climbed to 1.53 billion doses in 2024, up from 1.42 billion in 2023, and primary cell lines used for master-seed preparation still require serum. India’s Serum Institute consumes 8,000 liters of FBS annually for cell-bank maintenance. Brazil’s agriculture ministry documented a 12% rise in foot-and-mouth disease doses in 2024, which lifts veterinary vaccine serum needs. Large animal-health firms keep legacy lines on FBS because revalidation is costly and regulators have not mandated a switch, sustaining incremental growth in the fetal bovine serum market.

Rise of Contract Cell-Culture Manufacturing

Lonza’s USD 1.2 billion CDMO acquisition in 2025 highlights the premium on flexible cell-culture platforms accepting client-specified media. Charles River Laboratories recorded 16% biologics-testing revenue growth in Q3 2025, driven by FBS lot testing for CMO customers. WuXi Biologics qualified 47 serum lots in 2024 to meet diverse sponsor specs. Each additional CMO in a development chain multiplies procurement touchpoints, pushing up fetal bovine serum market volumes even as individual sponsors plan serum-free conversions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility linked to beef-industry cycle | -0.8% | Global, most acute in North America and South America | Short term (≤ 2 years) |

| Ethical concerns & regulatory scrutiny | -0.6% | Europe and North America lead; Asia-Pacific following | Medium term (2-4 years) |

| Acceleration of serum-free-media adoption | -1.2% | Global, with fastest uptake in Europe and North America | Long term (≥ 4 years) |

| Recombinant albumin substitutes gaining traction | -0.5% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ethical Concerns & Regulatory Scrutiny

The European Medicines Agency now requires individual-herd traceability for serum used in advanced-therapy medicinal products, raising compliance costs for small suppliers[2]European Medicines Agency, “Guideline on TSE/BSE Testing for ATMPs,” EMA, ema.europa.eu. USDA-APHIS proposed similar oversight for U.S. exporters in June 2025. The University of California system demands justification for every FBS purchase in grant-funded research. These measures do not eliminate demand but slow the fetal bovine serum industry growth rate as developers weigh long-term reputational risk.

Acceleration of Serum-Free-Media Adoption

Thermo Fisher’s serum-free media revenue outpaced FBS sales in 2025 by a ratio of 24% to 9%. Merck KGaA bought Mirus Bio for USD 290 million to couple transfection reagents with defined media, easing the path away from serum. Sartorius derived 22% of 2025 bioprocess revenue from chemically defined platforms and targets 35% by 2028. Early-stage projects move first because switching costs are low, placing a ceiling on very long-term expansion of the fetal bovine serum market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialized Grades Capture Premium Pricing

Stem-cell-qualified serum is forecast to grow 7.25% annually, outstripping the overall fetal bovine serum market size, because regenerative trials demand rigorous contaminant testing[3]National Institutes of Health, “Stem Cell Research Funding FY 2025,” NIH, nih.gov. Charcoal/dextran-stripped lots already control 31.55% of 2025 revenue and remain entrenched in hybridoma and endocrine research. Heat-inactivated and dialyzed variants serve routine culture and metabolic assays, while exosome-depleted grades gain traction after 2025 ISEV guidelines. Gamma-irradiated and low-IgG options protect viral-vaccine and immunology workflows, reinforcing a price hierarchy within the fetal bovine serum market.

Commodity-grade serum faces margin pressure as defined media substitutes arrive, yet premium grades retain bargaining power. ATCC’s 2025 authentication standards require full certificates of analysis, disadvantaging low-cost suppliers. Mesenchymal stem-cell-qualified lots remain supply constrained because fewer than ten producers meet multilineage-differentiation specs. Embryonic stem-cell protocols are shifting to defined media, but legacy feeder-dependent lines still specify FBS. This bifurcation signals widening spread in the fetal bovine serum market between cost-sensitive and performance-critical niches.

By Application: Biopharmaceutical Production Anchors Demand

Biopharmaceutical production delivered 32.53% of 2025 revenue and underpins current fetal bovine serum market size. However, its share may plateau because new facilities start directly with serum-free platforms. Cell-culture maintenance and expansion is projected to grow 6.75% through 2031 as CMOs scale client-bank inventories. Vaccine manufacturing, both human and veterinary, retained 18% of volume in 2025, with India and Brazil leading orders.

Stem-cell research gained momentum on the back of USD 2.1 billion in NIH awards in fiscal 2025, lifting specialized FBS volumes. Diagnostics and IVF remain niche yet price-inelastic, demanding ultra-low endotoxin lots for assay reproducibility and embryo viability. Hybridoma antibody production is slowly transitioning to defined media, but historical cell banks ensure persistent though tapering contributions to fetal bovine serum market demand.

By End User: Biotech and Pharma Dominance Masks Academic Growth

Biotechnology and pharmaceutical companies owned 62.15% of 2025 revenue, reflecting legacy manufacturing lines that still require FBS seed trains. Academic and research institutes are expected to post a 6.82% CAGR because grant-funded exploratory work stays with validated serum protocols. CMOs procure in bulk, passing costs through to sponsors, which keeps them less price sensitive than captive labs.

Cell banks such as ATCC continue to draw modest but steady lots for master-cell collection. Diagnostic labs and veterinary clinics contribute minor but stable orders. The segmentation confirms that the fetal bovine serum market draws its resilience from a mix of regulatory inertia in commercial plants and experimentation needs in academia.

Geography Analysis

North America held 41.55% of 2025 revenue, but drought-driven cattle-herd contraction threatens supply even as local biologics demand rises. Few Midwest abattoirs with GMP-grade cold chains create single-point-of-failure risk, nudging buyers toward South American collections secured by acquisitions such as Thermo Fisher’s 2025 deal. Serum-free adoption is fastest in the United States and Canada, implying regional growth will trail the global fetal bovine serum market by the late forecast period.

Asia-Pacific is projected to grow 7.22% through 2031 on expanding biosimilar output and vaccine capacity. China relies on imported serum because local suppliers struggle with TSE compliance, while India’s vaccine hubs keep seed-train steps on FBS. Japan’s conditional approval pathway boosts regenerative-medicine applications, and South Korean CMOs add bioreactor capacity that still starts with serum seed trains. Australia and New Zealand collect high-grade serum but lack herd volume to satisfy regional growth, driving cross-border logistics complexity.

Europe maintains demand through mature pharma clusters and strict traceability rules that favor vertically integrated suppliers. Germany and the United Kingdom anchor R&D needs for specialty grades, while France sustains vaccine lines that remain serum dependent. South America is primarily a supply region; Brazil’s 220 million-head herd underpins export flows though domestic demand is moderate. Africa and the Middle East contribute marginal consumption because local biomanufacturing infrastructure is limited.

Regulatory Landscape

Global trade and use of fetal bovine serum (FBS) are shaped by animal-health status, origin controls, and batch safety testing requirements that differ by importing region. In Europe, the European Medicines Agency (EMA) Note for Guidance (BWP/1793/02) for bovine serum used in human biological medicinal products sets expectations for source-country controls and documented quality systems, and the report context also points to tighter traceability expectations for advanced-therapy use. Across major markets, compliance depends on country and facility documentation aligned to World Organisation for Animal Health (WOAH) standards for transboundary animal diseases, with foot-and-mouth disease highlighted in the report context, alongside importer requirements for certificates and auditable traceability. Great Britain and other markets use formal export certification pathways for animal-derived products.

In the United States, USDA-APHIS oversight and viral safety expectations in applicable frameworks, including the testing panels referenced in the evidence pack, place the onus on suppliers to demonstrate freedom from key adventitious agents. Government testing capacity can also become a practical gating factor for imports. A June 2025 USDA-APHIS stakeholder alert cited delays at the National Veterinary Services Laboratories (NVSL) for required bioassays tied to imported commercial FBS, which can affect lead times and inventory planning for buyers. These controls increase the value of documented lot history, validated viral testing, and standardized traceability programs, including ISIA-aligned practices, for suppliers serving regulated biopharma and advanced-therapy workflows.

Competitive Landscape

The top five suppliers—Thermo Fisher Scientific, Merck KGaA, Sartorius, Cytiva, and Corning—accounted for a significant share of 2025 revenue, indicating moderate concentration in the fetal bovine serum market. Vertically integrated players control collection, processing, and global distribution, allowing them to meet new traceability mandates at lower incremental cost. Large vendors are also hedging with serum-free portfolios; Sartorius derived 22% of 2025 bioprocess revenue from chemically defined media and plans capacity additions in Germany.

Regional suppliers, numbering 30 to 40, compete on origin claims and spot availability but struggle to meet enhanced regulatory audits under EMA and FDA guidance. Exosome-depleted and stem-cell-qualified niches offer margin opportunity because fewer than ten producers achieve consistent specs defined by ISEV and ISCT guidelines. Upstream control is strategic; Thermo Fisher’s South American buyout protects access as North American cattle herds shrink.

Technological differentiation is emerging through blockchain lot tracking and inline contaminant analytics, which resonate with risk-averse pharma buyers. Recombinant albumin suppliers such as Albumedix present long-run substitution risk, but limited production scale and high cost keep immediate impact modest. Overall, the fetal bovine serum industry is set for gradual consolidation as traceability and biosecurity costs squeeze small traders.

Fetal Bovine Serum Industry Leaders

Thermo Fisher Scientific Inc.

Merck KGaA (Sigma-Aldrich)

Sartorius AG

Danaher Corp. (Cytiva)

Corning Incorporated

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunities focus on supply assurance and compliance-grade traceability as regulated buyers keep serum dependence while tightening documentation requirements. Tight input availability linked to cattle supply, including the US cattle inventory of 87.2 million head in January 2025, supports higher pricing for suppliers that can offer multi-origin sourcing, verified country-of-origin health status, and lot-release packages that align with regulator expectations and ISIA-style traceability certification. A visible investment signal is Auckland BioSciences opening a sterile filtration site in Uruguay in October 2025, with annual processing and export capacity cited at 250,000 liters through a partnership with Montesera. That capacity helps support additional qualified supply routes and regional processing options.

A second opportunity track is the continued coexistence of premium FBS grades with animal-origin-free workflow expansion. Stem-cell-qualified and charcoal/dextran-stripped grades still command value where assay performance, comparability, and protocol lock-in limit substitutions, supported by the International Society for Cell and Gene Therapy (ISCT) lot pre-qualification practices referenced in the report context. At the same time, suppliers that combine FBS portfolios with chemically defined media and recombinant components are gaining leverage with customers building hybrid strategies, supported by industry moves toward defined platforms, such as Sartorius expanding serum-free media capacity and Merck KGaA adding defined-media adjacencies through Mirus Bio. This supports demand for offerings that bundle FBS lot qualification, risk-mitigation inventory programs, and validated transition toolkits for customers migrating specific workflows away from serum while protecting regulated comparability.

Recent Industry Developments

- July 2026: Qkine announced a global distribution agreement for Media City Scientifics FRS Pioneer, positioned as a chemically defined, animal-free serum replacement for cell culture. The agreement broadens commercial access to serum-replacement options and increases competitive pressure on traditional FBS suppliers in research and early process-development workflows where switching barriers are lower.

- April 2025: AusGeneX LLC signed Targeted Bioscience Inc. as a North American channel partner to distribute Australian-origin serum products, including FBS. The arrangement expands regional access and supports multi-origin procurement strategies as buyers diversify sourcing to manage volatility and traceability requirements.

- December 2024: Gemini Bioproducts completed the acquisition and transition of selected Bio-Techne (R&D Systems) FBS product rights and inventory, including the Optima, Premium Select, and Premium lines. Consolidating these premium serum brands under GeminiBio increases portfolio depth and supports continuity for customers that standardize on specific lots and grades.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues generated from fetal bovine serum used as a cell culture supplement across research, testing, and biomanufacturing workflows, where demand is tied to how many cell culture processes are run and the quality grade selected.

Scope exclusions: This sizing does not count non-bovine serum substitutes, serum-free media, or general cell culture media formulations where fetal bovine serum is not sold as the priced component.

Segmentation Overview

- By Product Type

- Standard / Regular FBS

- Heat-Inactivated FBS

- Charcoal / Dextran-Stripped FBS

- Dialyzed FBS

- Chromatographically-Purified (Low-IgG) FBS

- Stem-Cell-Qualified FBS

- Embryonic SC-Qualified

- Mesenchymal SC-Qualified

- Exosome-Depleted FBS

- Gamma-Irradiated FBS

- By Application

- Biopharmaceutical Production

- Vaccine Manufacturing (Human & Animal)

- Cell-Culture Maintenance & Expansion

- Stem-Cell Research & Therapy

- Diagnostics / IVD

- IVF & Reproductive Medicine

- Exosome Studies

- Antibody Production & Hybridoma

- By End User

- Biotechnology & Pharmaceutical Companies

- Academic & Research Institutes

- CMOs & CROs

- Cell Banks & Biorepositories

- Diagnostic Laboratories

- Veterinary Clinics & Research

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a plain fact base for supply and demand signals that influence serum usage and pricing. Public sources such as USDA livestock and slaughter statistics, UN Comtrade trade data, World Bank macro indicators, and FDA and EMA biologics and vaccine approvals are used to sense volume drivers and any abrupt shifts in manufacturing activity.

We also review peer-reviewed cell culture and bioprocess journals for typical serum inclusion rates, quality requirements, and the shift toward defined media, which affects the addressable pool. Company filings, investor decks, association websites, and reputed press are then used to map where supply is coming from, how the grade mix is changing, and what creates premium pricing. For cross-checks, we use paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export visibility when available. The sources listed here are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what drives paid prices and actual purchase behavior, since FBS is often bought under annual supply agreements and quality specs can change the realized price quickly. We spoke with stakeholders across serum collection and processing, distribution, and end users such as biopharma manufacturing teams, research labs, and CMOs and CROs. Feedback was balanced across APAC, EMEA, and the Americas to avoid one-region bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | APAC: 53% |

| Mid tier: 56% | Functional/Unit leaders: 40% | EMEA: 29% |

| Smaller Players: 18% | Managers: 48% | Americas: 18% |

Market-Sizing & Forecasting

The model is built using a top-down demand pool, where cell culture activity is reconstructed using biopharma production intensity, clinical and research throughput, and region-wise adoption of serum-based workflows. That demand pool is then converted into serum volume and value through typical inclusion rates. Once the demand pool is set, results are corroborated with selective bottom-up approximations such as sampled supplier and distributor revenue checks, channel feedback on grade mix, and volume times average selling price (ASP) sanity tests, before final totals are locked.

Inputs that matter most include estimated liters consumed per workflow type, the share of heat-inactivated and specialty grades in total mix, observed price spreads by grade and origin, import and export movement patterns, and the pace of movement toward reduced-serum or defined media in key applications. When supplier disclosure is limited, gaps are handled by using regional proxies from trade flows and by applying interview-backed utilization ranges, and then the implied ASP is checked against recent quotations to avoid unrealistic jumps.

Forecasting is done using scenario analysis supported by trend-driven variables, and the assumptions are reviewed with experts so changes in grade premium, supply constraints, and demand from vaccines and advanced therapies do not get overstated.

Data Validation & Update Cycle

Validation is done through multiple checks so one data point does not over-influence the total. Outputs are compared with independent signals such as trade movement direction, bioprocess expansion cues, and observed pricing bands, and then anomalies are reviewed in a second analyst pass before sign-off.

The report is refreshed annually, and interim updates are triggered when material events occur, such as abrupt raw material constraints, major regulatory changes impacting collection and traceability, or sharp currency movement that affects reported USD values. Before delivery, a fresh review is completed so clients receive the most current view based on the latest available data and re-contacts where needed.

Mordor Intelligence's Fetal Bovine Serum Market Size Compared Against Other Published Estimates

Published numbers for fetal bovine serum rarely match because the market is sensitive to short-term pricing and grade mix shifts, and because not every study locks the same year and currency conversion timing. Differences also come from whether demand is tied to actual cell culture activity and procurement patterns, or inferred mainly from high-level life sciences growth trends.

A refresh-led gap shows up when ASP assumptions are rolled forward without being rechecked against new quotations, and when specialty grades are bundled into one price even though they carry distinct premiums. Extra spread also comes from base-case versus aggressive scenario choices, and from whether trade movement and supply tightness are used as real-world checks. With a more frequent pricing recheck cycle and FX timing aligned to the stated year, Mordor Intelligence keeps the total closer to what buyers and sellers report in current contracting discussions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.30 B (2026) | |

| Global Research Publisher A | USD 1.01 B (2024) | Uses an earlier base year and appears to smooth ASP movement over time, which can understate value when grade premiums rise and spot shortages lift prices. Scope timing and currency conversion year alignment are not always clearly tied to procurement reality. |

| Industry Analyst Desk B | USD 2.07 B (2024) | Implied growth and forecast trajectory suggest a broader value pool or higher assumed ASP progression, which can happen if adjacent cell culture inputs or downstream services are partially included. Limited clarity on how specialty-grade premiums and regional price spreads are validated. |

Across the three figures, the spread is mostly explained by year alignment and how quickly pricing and grade premiums are refreshed, and then by how tightly the demand pool is connected to measurable cell culture activity. When scope boundaries and the ASP logic are made explicit, the market total becomes easier to trace and repeat for planning.

Key Questions Answered in the Report

What is the projected value of the fetal bovine serum market in 2031?

It is forecast to reach USD 1.75 billion by 2031 on a 6.2% CAGR.

Which product grade currently leads sales?

Charcoal/dextran-stripped serum held 31.55% of 2025 revenue.

Why does cell- and gene-therapy manufacturing sustain serum demand?

Validated clinical protocols rely on FBS for ex vivo expansion, and switching would require costly revalidation.

Which region is expected to register the fastest growth?

Asia-Pacific is projected to expand at a 7.22% CAGR between 2026 and 2031.

Page last updated on: