Fermented Foods And Beverages Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

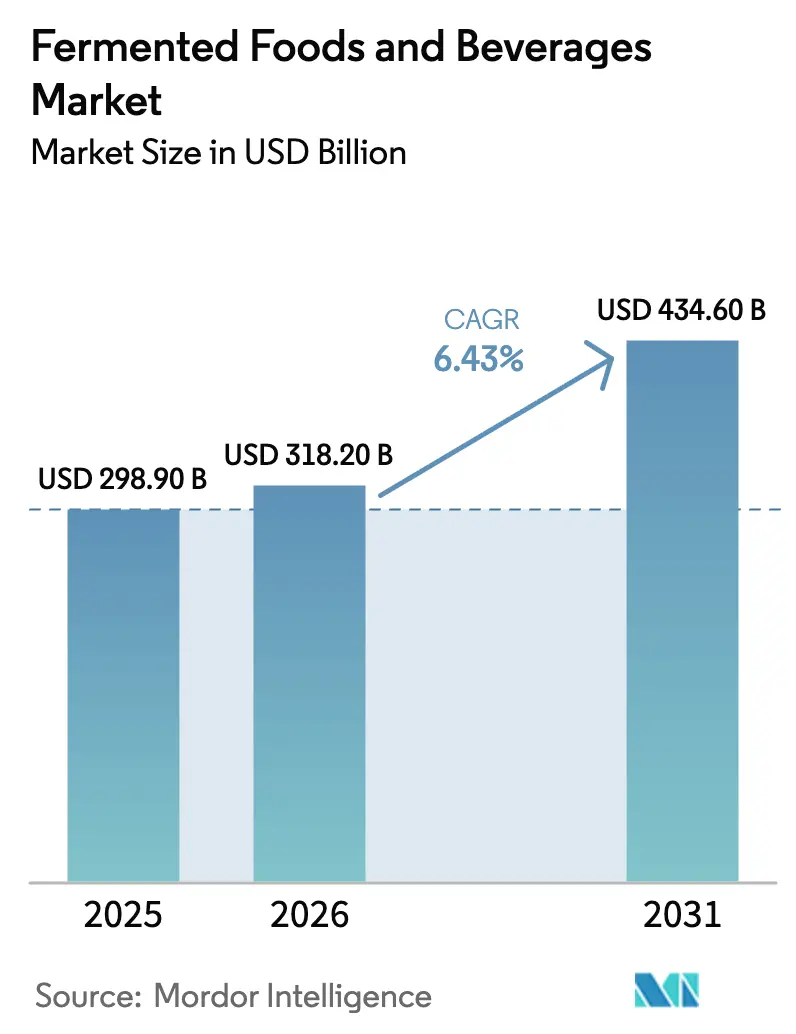

| Market Size (2026) | USD 318.20 Billion |

| Market Size (2031) | USD 434.60 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

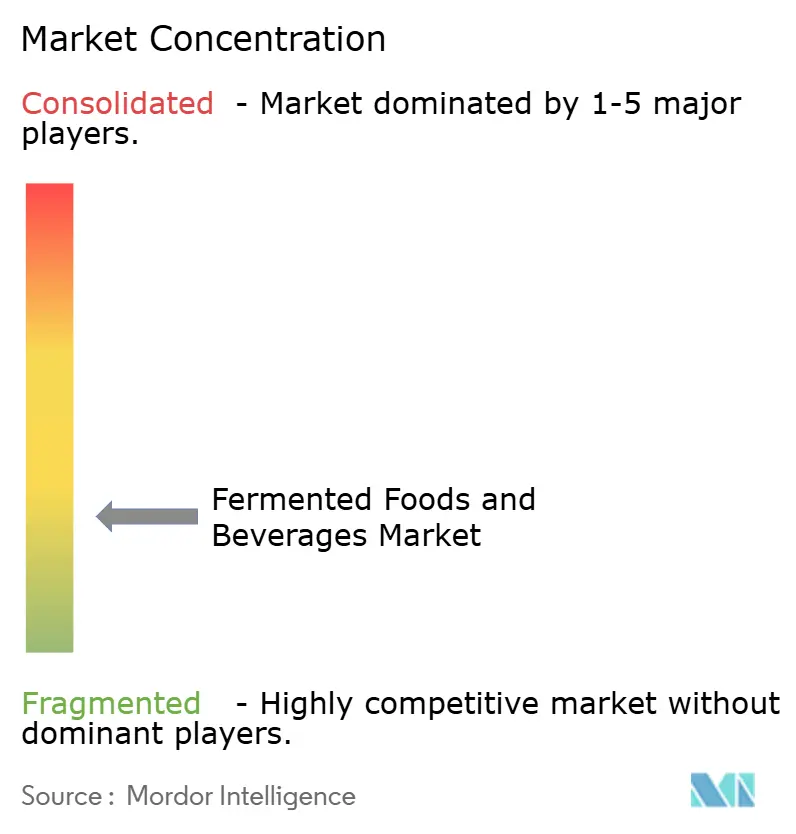

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fermented Foods And Beverages Market Analysis by Mordor Intelligence

The fermented foods and beverages market was valued at USD 298.90 billion in 2025 and is expected to grow to USD 318.20 billion in 2026, reaching USD 434.60 billion by 2031, with a CAGR of 6.43%. This growth is driven by a rising consumer focus on digestive health and a growing preference for foods that naturally promote gut wellness. Consumers are increasingly favoring probiotic-rich, minimally processed, and clean-label products, while traditional fermented items are experiencing renewed demand in global diets. Manufacturers are addressing these trends by introducing innovative products, including plant-based fermented alternatives such as dairy-free yogurts and cheeses, which cater to sustainability and vegan preferences. For example, Nush launched a high-protein vegan yogurt in the UK. While fermented foods hold the largest market share, fermented beverages are witnessing rapid growth due to the rising popularity of functional drinks. Dairy-based products continue to dominate the market, but plant-based options are experiencing the fastest growth. Supermarkets and hypermarkets remain the leading sales channels, with e-commerce emerging as a rapidly growing distribution platform. Regionally, Asia-Pacific leads in both consumption and growth, supported by its deep-rooted fermentation traditions and changing lifestyles. Increasing concerns about digestive health, interest in functional nutrition, and experimentation with new flavors and fortified formulations are further driving market expansion.

Key Report Takeaways

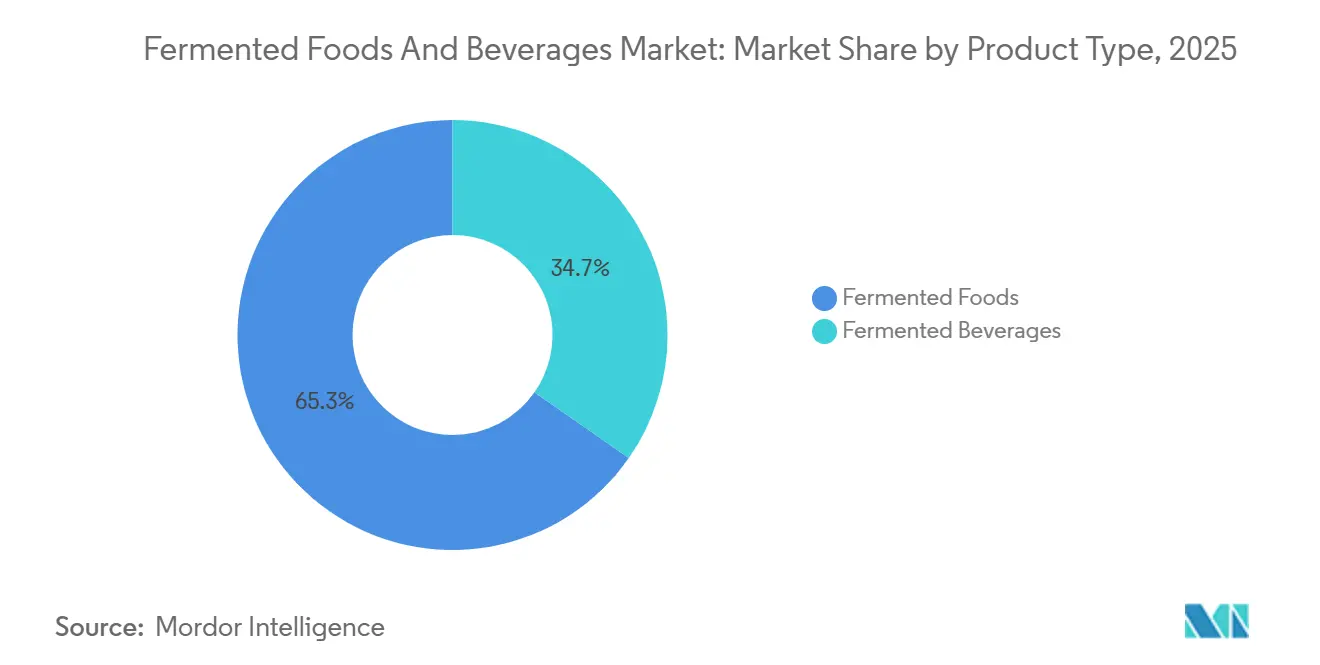

- By product type, fermented foods dominated with 65.31% of the fermented foods and beverages market share in 2025, whereas fermented beverages are projected to expand at a 7.42% CAGR through 2031.

- By ingredient source, dairy-based formulations held 51.12% share of the fermented foods and beverages market size in 2025; plant-based alternatives carry the highest forecast growth at 8.87% CAGR to 2031.

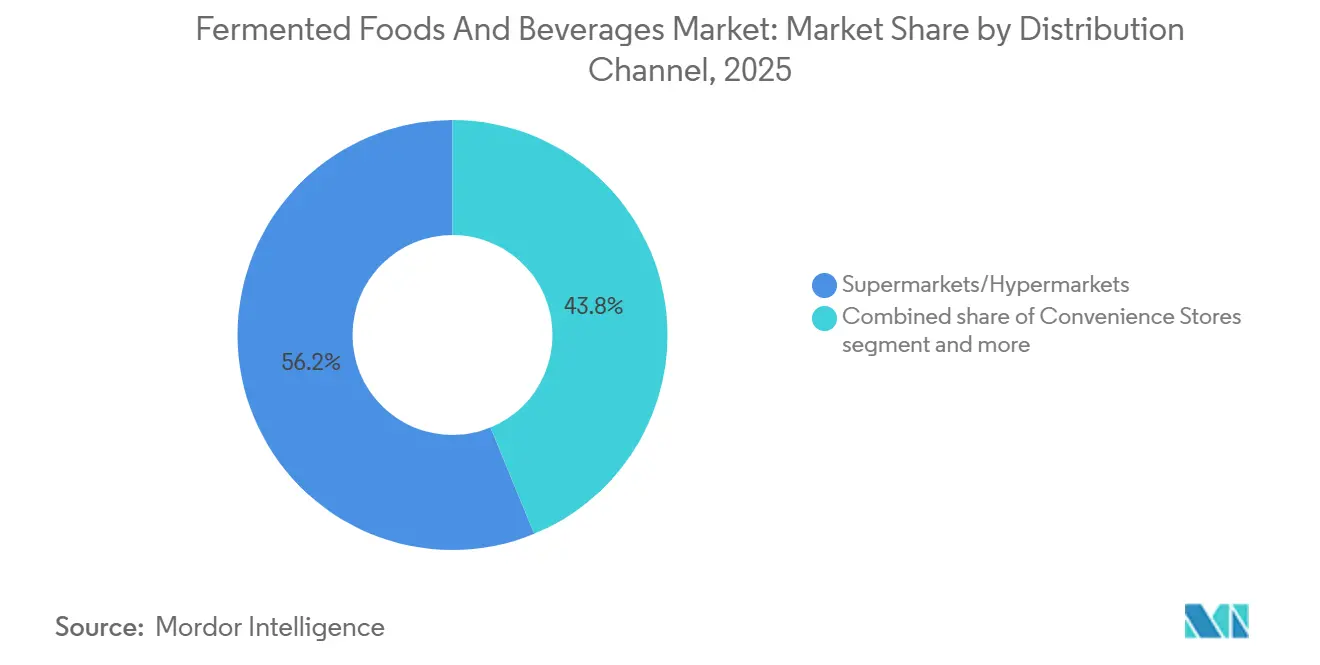

- By distribution channel, supermarkets/hypermarkets retained 56.21% revenue share in 2025, while online retail is the fastest-growing route at an 8.04% CAGR.

- By geography, Asia-Pacific led with 33.53% of the fermented foods and beverages market size in 2025 and is advancing at a 7.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fermented Foods And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer demand for probiotic-rich foods for gut health | +1.8% | Global, with strongest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising popularity of plant-based and vegan diets | +1.2% | Europe and North America core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of supermarket/private-label fermented ranges | +0.9% | Global, with early gains in Europe and North America | Short term (≤ 2 years) |

| Emergence of precision fermentation | +1.5% | North America and Europe leading, Asia-Pacific following | Long term (≥ 4 years) |

| Cultural revival and ethnic cuisine popularity | +0.7% | Global, with regional variations in traditional products | Medium term (2-4 years) |

| Clean label and minimal processing preferences | +0.6% | North America and Europe primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing consumer demand for probiotic-rich foods for gut health

The fermented foods and beverages market is witnessing significant growth as consumers increasingly prioritize products linked to gut health and functional nutrition. This trend has driven market diversification, spurred innovation in product formats, and created opportunities for premium positioning, with fermented foods becoming a staple in daily diets across various regions. Rising awareness of the connection between digestive health and overall well-being has also led consumers to spend more on fermented products perceived as credible, effective, and beneficial for health. Efforts within the industry to build trust and credibility are shaping this development. For instance, the International Dairy Foods Association’s relaunch of the Live and Active Cultures seal in March 2024, which certifies products containing at least 100 million live cultures per gram, underscores the market's emphasis on verification and transparency [1]Source: International Dairy Foods Association, “IDFA Relaunches Live and Active Cultures Seal for Yogurt and Cultured Dairy Product Makers to Showcase Benefits of Gut Health", IDFA, idfa.org. Such initiatives enable informed consumer decisions and set higher quality standards. Consequently, manufacturers are focusing on evidence-based product development, investing in clinical validation, precision fermentation techniques, and supply chain traceability to substantiate health claims and stand out in an increasingly competitive landscape.

Rising popularity of plant-based and vegan diets

The growth of the fermented foods and beverages market is being driven by the increasing adoption of plant-based and vegan diets, influenced by consumer focus on personal health, environmental sustainability, and ethical considerations. Awareness of the environmental impact of livestock production, including its role in carbon emissions, land use, and water consumption, is prompting consumers to opt for more sustainable food options. Fermented products align well with plant-based diets due to their recognized nutritional benefits, such as supporting digestive health, providing probiotics, and enhancing nutrient bioavailability. Additionally, market growth is supported by public-sector initiatives and policies aimed at fostering innovation in alternative proteins and fermentation technologies. For instance, in February 2024, the UK government allocated EUR 12 million to establish an alternative protein research center, led by UK Research and Innovation (UKRI), focusing on fermentation-based advancements. The combination of shifting consumer preferences, health-conscious dietary trends, and institutional support is fostering innovation and driving long-term growth in the global fermented foods market.

Clean label and minimal processing preferences

The fermented foods and beverages market is experiencing significant changes as consumers increasingly focus on clean-label products with minimal artificial ingredients. This shift is driven by a demand for greater transparency, authenticity, and perceived health benefits, alongside concerns about synthetic additives and highly processed foods. Fermented foods naturally meet these expectations due to their reliance on simple ingredient lists and minimal processing, while also offering digestive and overall health benefits. According to the International Food Information Council (IFIC), 25% of U.S. consumers in 2024 expressed a preference for foods with limited or no artificial ingredients [2] Source: International Food Information Council, " 2024 IFIC Food & Health SURVEY", ific.org. This trend is encouraging manufacturers to reformulate products by removing unnecessary additives and emphasizing the natural benefits of fermentation. The growing preference for clean-label foods highlights fermented foods as a favored category, supporting continued market growth and innovation driven by ingredient transparency.

Emergence of precision fermentation

Precision fermentation is transforming the fermented foods and beverages market by enabling cost-efficient production and facilitating the development of high-value ingredients that are challenging or impractical to produce using conventional fermentation methods. Utilizing engineered microorganisms, this technology allows for the precise production of specific proteins, enzymes, flavors, and functional compounds with enhanced accuracy, consistency, and scalability. This enables manufacturers to achieve better process control while adhering to strict standards for product quality, safety, and nutritional integrity. Additionally, precision fermentation reduces dependence on traditional agricultural inputs and animal-based raw materials, thereby lowering resource consumption and minimizing environmental impact. This approach aligns with sustainability objectives and the increasing consumer demand for environmentally friendly and ethically produced food products. Advances in synthetic biology and bioprocessing further support scalable production without compromising performance or functionality. In June 2024, Danone formed a strategic partnership with Michelin and DMC Biotechnologies, investing over EUR 16 million to establish the Biotech Open Platform in France. This shared innovation infrastructure aims to provide food and biotechnology companies with access to specialized equipment, technical expertise, and collaborative research opportunities, accelerating the development and commercialization of precision fermentation solutions. As these technologies advance, precision fermentation is anticipated to play a critical role in addressing sustainability challenges and driving long-term innovation within the fermented foods and beverages market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High contamination and food-safety recall risk | -0.8% | Global, with stricter enforcement in developed markets | Short term (≤ 2 years) |

| Limited shelf-life requiring cold-chain logistics | -0.6% | Global, with higher impact in emerging markets with limited infrastructure | Medium term (2-4 years) |

| Variability in fermentation quality and microbial consistency | -0.4% | Global, with higher impact on artisanal and small-scale producers | Medium term (2-4 years) |

| Consumer aversion to sour or strong fermented flavors | -0.3% | Regional, particularly in markets new to fermented products | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High contamination and food-safety recall risk

The fermented foods and beverages market has encountered substantial operational challenges due to increasingly stringent regulatory frameworks across various regions. In the United States, the Food Safety and Inspection Service (FSIS) implemented updated testing protocols in January 2025 for non-Listeria monocytogenes Listeria species. These protocols require producers to undertake comprehensive remediation measures whenever contamination is identified. Additionally, the Food and Drug Administration (FDA) extended the public comment period in 2024 for its revised Hazard Analysis and Risk-Based Preventive Controls guidance, highlighting the ongoing evolution of food safety regulations. In Australia, the Queensland Government introduced a mandate requiring fermented foods to maintain pH levels at or below 4.6 to ensure microbial safety [3]Source: Queensland Government, "Fermented foods", gov.au. This measure was driven by previous contamination incidents, product recalls, and the resulting reputational damage. These stricter regulations have posed significant entry barriers, particularly for small-scale and artisanal producers, while also increasing operational and compliance costs for established manufacturers.

Limited shelf-life requiring cold-chain logistics

The reliance on cold-chain logistics poses a significant challenge in the fermented foods and beverages market. Products such as kefir, yogurt, and soft cheeses require precise temperature-controlled storage to maintain quality and safety, coupled with their inherently short shelf lives. Ensuring these conditions adds complexity and raises costs across the supply chain. Companies must invest substantially in refrigeration infrastructure, temperature-monitoring systems, and specialized transportation, which can considerably reduce profit margins. An example of these challenges is Wonder Veggies’ launch of probiotic fresh produce in June 2024. The company implemented a stringent cold-chain system to preserve probiotic viability in fresh vegetables, resulting in a 20% price premium to cover additional distribution costs. These operational demands are particularly challenging for small-scale producers and businesses in regions with inadequate logistics infrastructure. Regulatory requirements further compound the issue. For instance, the FDA’s 2022 Food Code supplement mandates strict temperature controls for fermented products to ensure probiotic activity and prevent spoilage. These cold-chain dependencies collectively create significant operational challenges, increasing production costs, limiting market flexibility, and acting as a barrier to entry for new players in the fermented foods and beverages market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beverages Accelerate Despite Food Dominance

In 2025, the fermented foods segment accounted for a dominant 65.31% market share, supported by their deep cultural significance, enhanced nutritional value, and alignment with the growing demand for plant-based and functional foods. Conversely, the fermented beverages market is experiencing rapid growth, with a CAGR of 7.42% forecasted through 2031, surpassing the growth rate of fermented foods. This growth is attributed to increasing consumer interest in functional beverages that prioritize lower sugar content, transparent ingredient lists, and health benefits such as digestive and immune system support.

Within the fermented foods category, traditional products like yogurt and cheese continue to lead the market, while alternative options such as tempeh, sauerkraut, and tofu are gaining traction as consumer preferences shift toward a broader range of culturally diverse products. The dairy subcategory shows strong performance, particularly in protein-enriched yogurt and dessert segments. The fermented beverages market is also expanding beyond traditional offerings, as demonstrated by Wonder Veggies' 2025 launch of probiotic fresh produce, introducing innovative product categories that combine fresh and fermented elements.

By Ingredient Source: Plant-based Transformation Accelerates

In 2025, dairy-based fermented products held a substantial 51.12% share of the fermented foods and beverages market. However, their dominance is increasingly challenged by the rising demand for plant-based alternatives. This shift is driven by growing concerns over sustainability, animal welfare, and allergen sensitivities. Plant-based fermented products represent the fastest-growing segment in the market, with a projected CAGR of 8.87% through 2031. These products appeal to vegans, lactose-intolerant individuals, and consumers seeking clean-label options, while also offering a reduced environmental footprint. Technological advancements, particularly in precision fermentation, are accelerating this transition. These innovations enable the production of animal-free products that closely mimic the taste, texture, and functionality of traditional dairy. For instance, in February 2024, Unilever launched Breyers ice cream made with Perfect Day's precision-fermented whey, delivering dairy-like creaminess without animal-derived ingredients.

Grain-based fermented products represent a promising yet underexplored subcategory, recognized for their nutritional benefits, versatility, and cultural significance worldwide. These products offer plant-based probiotic benefits while utilizing widely available and cost-effective staple ingredients. Fermented grains provide gut-friendly properties and are rich in fiber, B vitamins, and bioactive compounds. The category demonstrates significant growth potential, driven by innovations in grain fermentation techniques and increasing consumer demand for gluten-free, high-fiber, and ancient grain-based options. Additionally, this segment offers manufacturers opportunities for differentiation through the use of unconventional fermentation substrates.

By Distribution Channel: Digital Transformation Reshapes Retail

Supermarkets/hypermarkets accounted for a dominant market share of 56.21% in 2025, supported by their extensive private-label product offerings and well-established cold-chain distribution systems. Online retail distribution channels are expected to grow at a CAGR of 8.04% through 2031, driven by increasing consumer demand for convenient access to specialized fermented products. The adoption of direct-to-consumer distribution strategies continues to enhance market penetration, enabling fermented food manufacturers to build strategic consumer relationships while improving operational profit margins.

Convenience stores are addressing market demand by upgrading refrigeration infrastructure and expanding product lines, particularly in urban areas where there is significant demand for portable fermented beverages. Traditional retail outlets are responding to competition from digital channels by enhancing in-store experiences and utilizing data analytics to optimize product placement and promotional activities. This approach fosters a complementary relationship between physical and digital retail channels. Additionally, alternative distribution channels are experiencing growth as fermented products gain recognition for their functional health benefits.

Geography Analysis

The Asia-Pacific region held a dominant market position with a 33.53% market share in 2025, supported by a robust regional growth rate of 7.87% CAGR through 2031. This growth underscores the region's role as a leading consumer market and innovation hub for fermented products globally. The market leadership in this region is driven by the deep-rooted integration of fermentation practices within its cultural traditions, particularly in countries like Japan, China, and Indonesia. These nations leverage centuries-old fermentation methodologies, fostering greater consumer acceptance of new product innovations.

North America exhibits market maturity, characterized by ongoing corporate consolidation and a focus on premium products. The region benefits from a strong regulatory framework and consumer preferences for health-oriented spending, which support the introduction of premium fermented products. For instance, Coca-Cola launched Simply Pop in February 2025, a product with no added sugar and 6 grams of prebiotic fiber, reflecting the adaptation of traditional beverage companies to health-conscious consumer demands. Additionally, Canada and Mexico contribute to regional growth through retail expansion and heightened health awareness, while harmonized regulations facilitate cross-border product distribution.

Europe continues to hold a prominent position as a leader in plant-based fermented product innovation, driven by comprehensive sustainability initiatives that set global benchmarks for product development. The region's focus on plant-based fermentation technologies highlights advanced environmental awareness among consumers and is supported by robust regulatory frameworks promoting sustainable food production systems. Meanwhile, the Middle East and Africa exhibit significant growth potential. Although current market capacity remains limited, improvements in cold-chain infrastructure and rising health consciousness are creating favorable conditions for the accelerated adoption of fermented products in these regions.

Regulatory Landscape

Food safety and labeling compliance remain central for fermented dairy, fermented vegetables, and functional fermented beverages, with tighter requirements around contamination control and claim substantiation. In the United States, FSIS implemented updated testing protocols in January 2025 for non-Listeria monocytogenes Listeria species, raising remediation expectations when positives are detected. FDA has also continued work on preventive-controls guidance and food-program deliverables, which affect hazard analysis and process controls for fermented products sold through retail and foodservice.

Competitive Landscape

The market for fermented foods and beverages is characterized by a high degree of fragmentation, reflecting a competitive environment shared among well-established multinational corporations, emerging businesses, and regional players. Prominent companies such as Danone S.A., Nestlé S.A., PepsiCo, Inc., and Yakult Honsha Co., Ltd. have secured strong positions in the market by leveraging precision fermentation technology and extensive distribution networks. The market's structure supports a variety of strategic approaches, as demonstrated by PepsiCo's acquisition of the prebiotic soda brand Poppi for USD 1.95 billion in May 2025.

The competitive environment is shaped by the rapid pace of technological advancements and changing consumer preferences, compelling companies to strike a balance between innovation and the management of their existing product portfolios. Industry participants are heavily investing in research and development to improve their product offerings and sustain their competitive positions. Companies are also engaging in strategic collaborations, mergers, and acquisitions to enhance their market presence and expand their product lines. The industry is further defined by a growing emphasis on product differentiation, compliance with quality standards, and the adoption of sustainable production practices.

The personalized nutrition segment represents a significant area of growth, with companies channeling resources into advanced technological innovations. Businesses are focusing on developing AI-driven fermentation techniques and creating specialized probiotic formulations tailored to individual microbiome profiles. These advancements, combined with strategic investments in research and development, highlight the industry's dedication to innovation and consumer-focused solutions. Additionally, companies are implementing robust quality management systems and prioritizing sustainable production methods to maintain their competitive advantages in the global market.

Fermented Foods And Beverages Industry Leaders

-

Danone S.A.

-

Nestlé S.A.

-

PepsiCo, Inc.

-

Yakult Honsha Co. Ltd

-

Fonterra Co-operative Group Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Functional positioning and everyday consumption occasions create whitespace across both fermented foods and fermented beverages, especially where brands can pair gut-health credentials with mainstream taste and convenience. Demand signals in core categories support scale-up of fermented dairy and drinkable formats, including U.S. kefir value growth of 29.1% and volume growth of 26.1% in the year ending mid-2026, which reinforces opportunities in flavored, low-sugar, and protein-forward cultured dairy. At the same time, the move toward plant-based and lactose-free fermented products is showing up in concrete portfolio actions, including Yakult Europe’s April 2026 launch of a dairy-free soy-based probiotic drink, supporting broader development of non-dairy cultured beverages and spoonable alternatives.

Capacity additions and distribution build-outs also point to investable pathways to expand output and improve cold-chain reliability for short-shelf-life fermented products. In March 2026, Chobani announced a USD 567 million multi-phase expansion at its La Colombe facility in Norton Shores, Michigan, adding over 200,000 square feet of production space, illustrating how leading players are funding manufacturing scale for fermented and adjacent functional dairy offerings. In beverages, Suntory PepsiCo’s July 2026 opening of its largest Asian factory in Tay Ninh, Vietnam, including fully automated warehousing, highlights an emphasis on high-throughput production and logistics efficiency for health-oriented beverage portfolios. In Europe, Spraga’s March 2026 retail listings across multiple Polish chains (Kaufland, Zabka, Biedronka, and Dino) illustrate how expanded shelf access and local investments can accelerate trial for emerging fermented beverage brands.

Recent Industry Developments

- July 2026: Suntory PepsiCo opened its largest Asian factory in Tay Ninh, Vietnam, including fully automated warehousing. The expansion reinforces the focus on high-throughput production and logistics efficiency for health-oriented beverage portfolios in Southeast Asia.

- June 2026: Danone S.A. announced a definitive agreement to acquire MADE Group, an Australia-based health-focused nutrition company. The transaction widens Danone's Asia-Pacific footprint and adds a gut-health portfolio supported by MADE's distribution network.

- March 2026: Chobani announced a USD 567 million multi-phase expansion at its La Colombe facility in Norton Shores, Michigan, adding over 200,000 square feet of production space. The investment expands capacity to support fermented and adjacent functional dairy offerings for national retailer supply.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the sales value of fermented foods and fermented beverages that are made for human consumption and sold through retail and food service, where fermentation is a main processing step.

Scope exclusions: We exclude industrial fermentation inputs (such as starter cultures and enzymes), bio-ethanol fuel, distilled spirits, and products that are only fermented as a minor step or are effectively non-fermented due to full heat treatment.

Segmentation Overview

-

By Product Type

-

Fermented Foods

- Yogurt

- Cheese

- Tempeh

- Sauerkraut/Pickled Vegetables

- Tofu

- Other Fermented Food

-

Fermented Beverages

- Yogurt Drinks/Smoothies

- Probiotic Drink

- Kombucha

- Kefir

- Other Fermented Beverages

-

Fermented Foods

-

By Ingredient Source

- Dairy-based

- Plant-based

- Grain-based

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Other Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the structure of the market model and to build realistic starting ranges for consumption and pricing by major regions. We reviewed public sources such as FAOSTAT food supply and production series, USDA food availability and dairy statistics, UN Comtrade trade flows for fermented beverage and food categories, and government health and nutrition agencies that publish diet and category definitions. We also reviewed trade association websites and conference materials in areas like dairy, brewing, and functional beverages to clarify product mapping and common pack formats.

To keep the model practical, we cross-checked with company filings, investor presentations, and audited annual reports to understand category exposure and regional mix, then paired those findings with trusted press and retail news for pricing and launch signals. Where public information was thin, we used paid subscriptions for company financials and intelligence, news and financials, patent databases, and an import-export shipment-level database to sense-check trends at a high level without forcing the model to fit the data. The desk sources listed here are illustrative only, since many other public and paid references were also used to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with manufacturers, ingredient and culture suppliers, distributors, and category specialists across the main consuming regions, with selected food service contacts added to capture on-premise demand signals. These conversations were used to confirm what is counted as fermented at shelf level, validate typical pricing progression, and pressure-test assumptions on premiumization, refrigeration needs, and the split between alcoholic and non-alcoholic fermented drinks.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 16% | APAC: 49% |

| Mid tier: 45% | Functional/Unit leaders: 24% | EMEA: 30% |

| Smaller Players: 21% | Managers: 60% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach, where category consumption is reconstructed from food supply, beverage volumes, and trade balances, then converted into value using observed price ladders and mix shifts. We also used selective bottom-up approximations, such as sampling major brand revenues by fermented exposure and running channel checks on typical pack prices, which were used to validate totals and adjust for gaps.

Key inputs used in the model include per capita intake trends for fermented dairy and fermented vegetables, regional direction for beer and wine volume, the share shift toward functional fermented drinks (such as kombucha and probiotic dairy beverages), refrigeration and cold-chain penetration for short shelf life items, and average selling price movement by pack size and channel. When a sub-category had limited public visibility, the gap was handled through proxy indicators (for example, related dairy category volumes and import intensity) and then refined through primary feedback.

For forecasting, we relied on scenario analysis supported by exponential smoothing on the more stable food categories, then applied sensitivity-based adjustments for parts that are more cycle-linked, such as alcoholic fermented beverages. The final forecast path was only accepted after the assumptions on pricing, mix, and region growth were consistent with expert feedback and recent category signals.

Data Validation & Update Cycle

Validation was done by comparing the model outputs against independent signals, such as reported category growth in public company results, major trade flow movements, and region-level consumption direction that should logically align with the final totals. If a variance looked too large, we re-checked product mapping, currency timing, and the price assumptions first, then re-contacted selected interviewees when the inconsistency could not be explained.

Before sign-off, the work goes through multi-step analyst reviews, where calculations are traced back to the core inputs and checked for outliers across regions and categories. The report is refreshed annually, and interim updates are made when material events occur, such as major regulation shifts, tax changes impacting alcoholic beverages, or step-changes in input costs. Right before delivery, a fresh review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Fermented Foods Beverages Market Size Compared Against Other Published Estimates

Published market sizes for fermented foods and beverages can differ even when the topic sounds identical, because the scope rules and the conversion to value are not consistent across publishers. The biggest shifts usually come from what counts as fermented at shelf level, whether alcoholic fermented beverages are included, and how pricing is averaged across retail and food service.

Some estimates treat fermented beverages as a small add-on inside a fermented foods total, and a few also blur in adjacent categories that are only lightly fermented or fully heat-treated. In Mordor Intelligence, products are counted only when fermentation is a primary processing step and the item is sold as a consumer-ready fermented food or fermented drink, which keeps the value tied to a clearer demand pool and helps avoid inflating totals with industrial inputs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 298.90 B (2025) | |

| Industry Research Firm A | USD 302.28 B (2025) | The scope summary is broader on paper and does not clearly state exclusions for industrial fermentation inputs or fully heat-treated products, which can slightly lift the total. It also presents a higher long-range growth curve, suggesting more aggressive premiumization or mix assumptions for fermented beverages. |

| Industry Publisher B | USD 258.97 B (2025) | The framing is closer to fermented foods, and beverages appear as a segment without clear treatment of alcoholic fermented drinks, which can lower the starting value. Category mapping is also more process-driven, which can miss consumer-ready fermented items that are sold under broader shelf labels. |

The spread across the three figures is mostly explained by how tightly fermented products are defined and whether alcoholic fermented drinks are fully counted, partly counted, or left implicit. By keeping the inclusion rules explicit and then tying value to observable consumption and price signals, the final number stays easier to reconcile and replicate when assumptions are updated.

Key Questions Answered in the Report

What is the current value of the fermented foods and beverages market?

The fermented foods and beverages market is valued at USD 318.20 billion in 2026 and is projected to reach USD 434.60 billion by 2031 at a 6.43% CAGR.

Which region leads the market in both size and growth?

Asia-Pacific commands 33.53% of market value in 2025 and is forecast to grow at 7.87% CAGR to 2031, making it the largest and fastest-growing region.

What product segment is expanding the fastest?

Fermented beverages, led by kombucha and emerging prebiotic sodas, are growing at a 7.42% CAGR, outpacing fermented foods.

How are plant-based alternatives influencing market dynamics?

Plant-based fermented products are growing at 8.87% CAGR, driven by sustainability and allergen-free positioning, challenging dairy’s long-standing dominance.

Page last updated on: