Continuing Medical Education Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

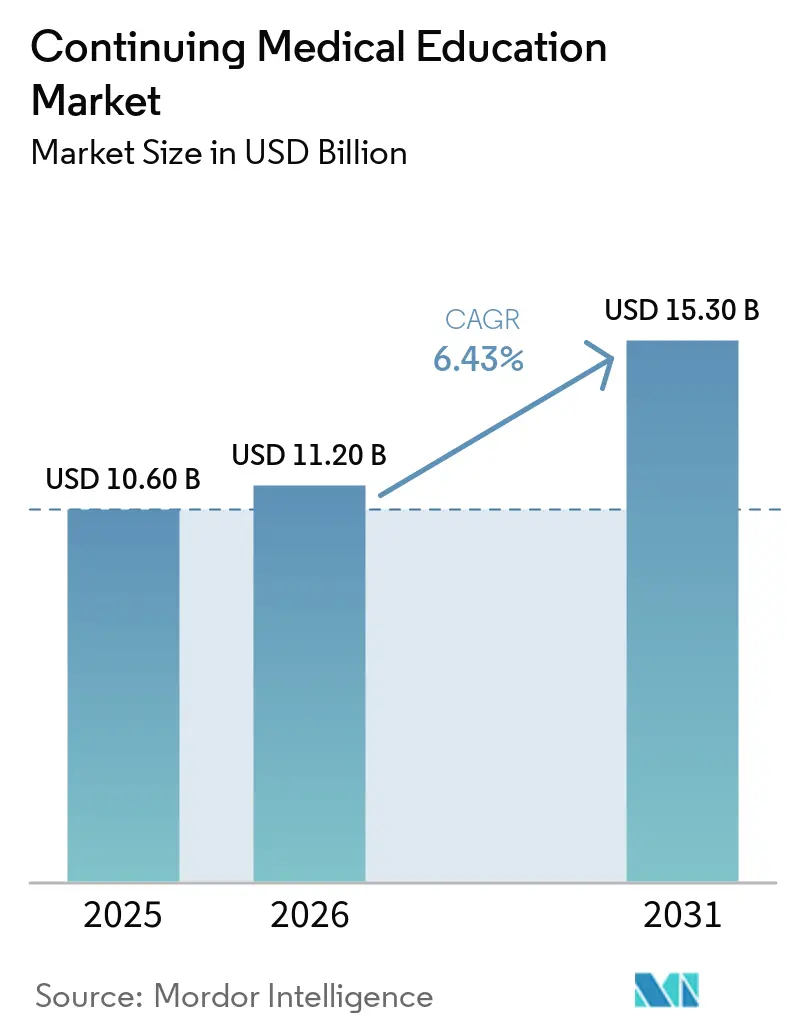

| Market Size (2026) | USD 11.20 Billion |

| Market Size (2031) | USD 15.30 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Continuing Medical Education Market Analysis by Mordor Intelligence

The Continuing Medical Education Market size is projected to be USD 10.60 billion in 2025, USD 11.20 billion in 2026, and reach USD 15.30 billion by 2031, growing at a CAGR of 6.43% from 2026 to 2031.

Sustained regulatory pressure to earn credits for license renewal, the normalization of digital delivery infrastructure installed during the pandemic, and rapid adoption of interprofessional team-based learning continue to enlarge addressable demand for the continuing medical education market. Technology-driven formats that deliver credits inside the electronic health record (EHR) are converting administrative screen time into accredited learning, while renewed interest in on-site conferences signals a post-pandemic appetite for networking and hands-on skills.

Provider consolidation remains moderate, as the ten largest players capture only a notable portion of accredited revenue, leaving substantial whitespace for specialty societies, academic centers, and digital platforms to segment the continuing medical education market through content depth, modality innovation, and geographic focus.

Key Report Takeaways

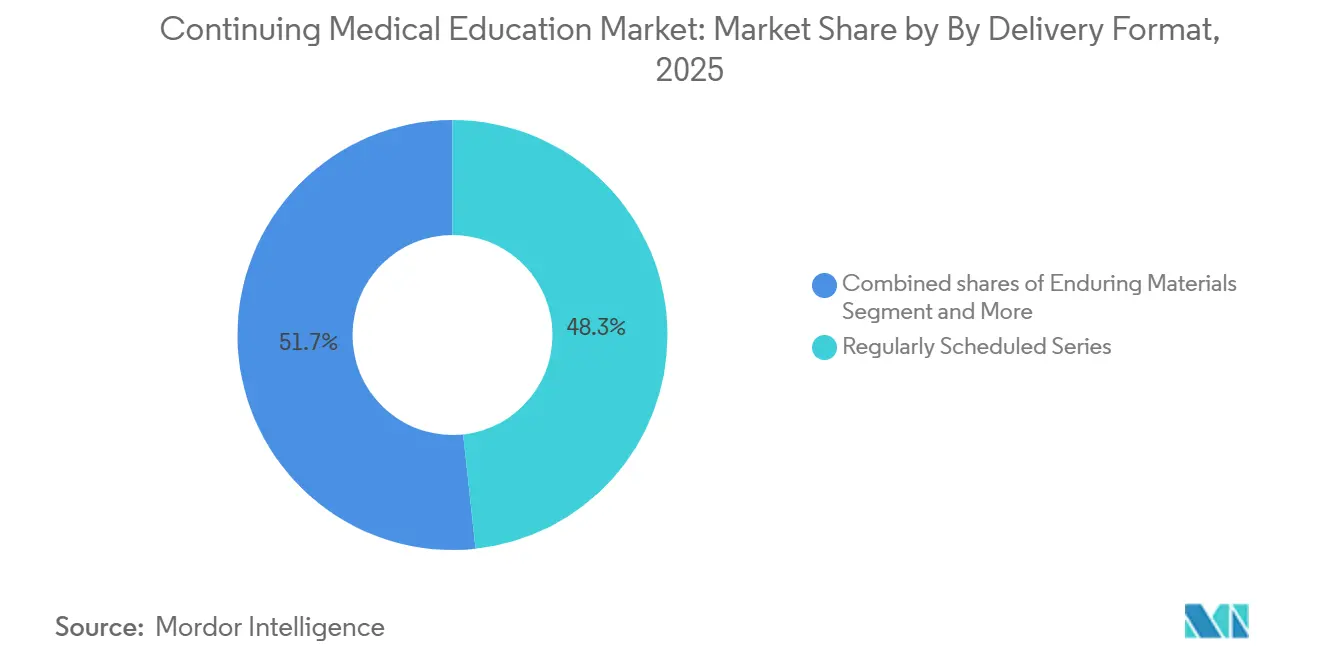

- By delivery format, regularly scheduled series led with 48.30% of continuing medical education market share in 2025, while live in-person courses are forecast to grow at the quickest 6.95% CAGR through 2031.

- By provider type, hospitals and integrated health systems held 45.36% continuing medical education market share in 2025, whereas government and non-profit agencies post the strongest 6.86% CAGR outlook to 2031.

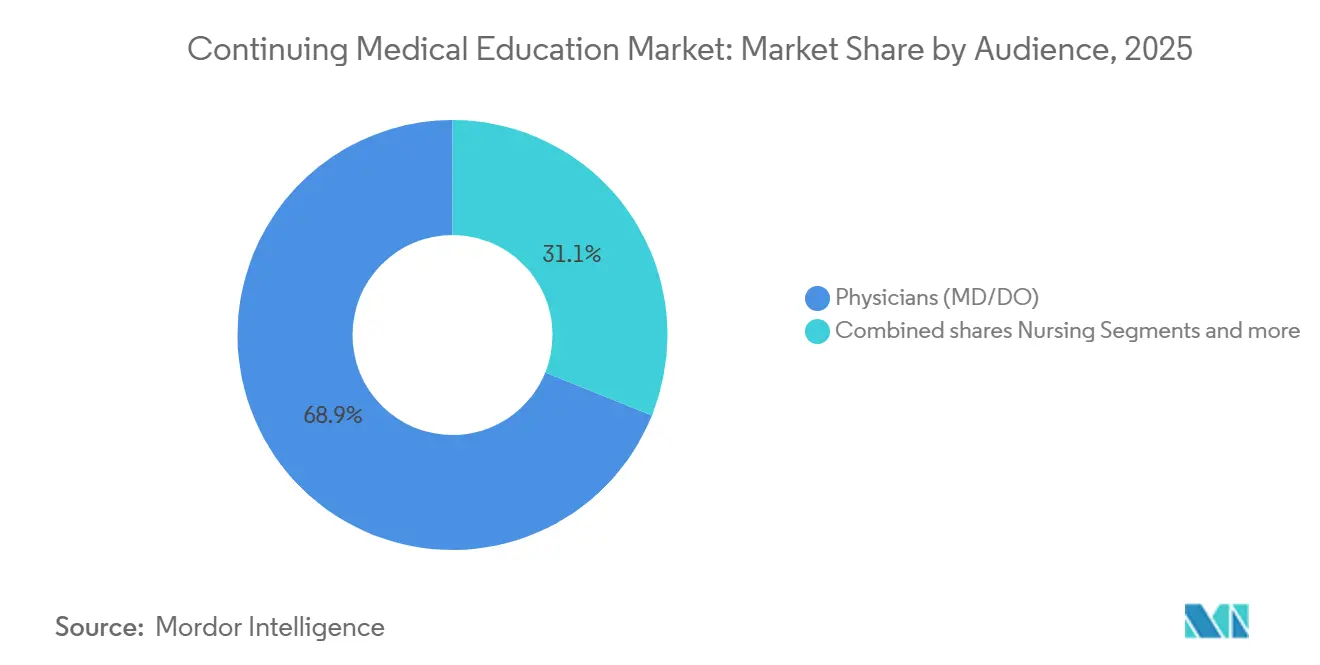

- By audience, physicians accounted for 68.90% of the continuing medical education market size in 2025 and are expected to maintain a solid 6.78% CAGR as boards tighten recertification cycles.

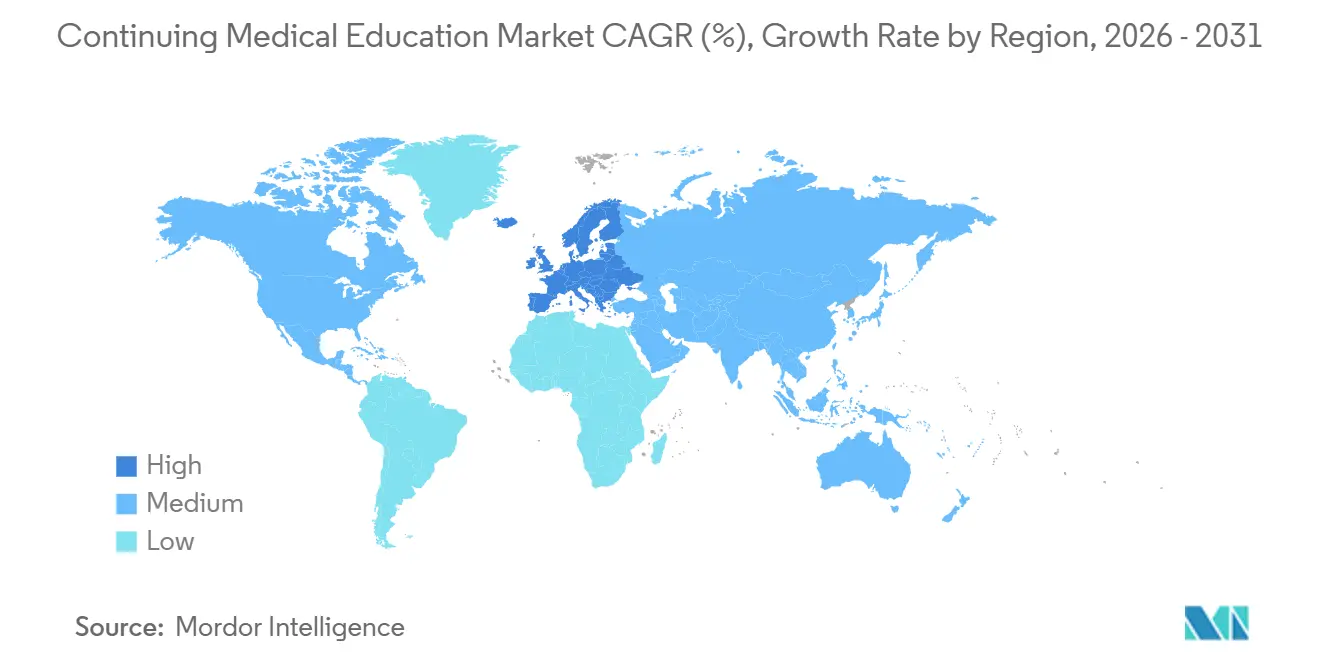

- By geography, North America dominated with 55.61% revenue share in 2025, yet Europe is expanding fastest at 6.84% CAGR due to cross-border credit portability.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Continuing Medical Education Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory licensure/recertification CPD/CME requirements across major markets | +1.8% | Global, with strongest enforcement in North America, Europe, China, India | Long term (≥ 4 years) |

| Persistent shift to online enduring and virtual live CME (sustained post-pandemic) | +1.2% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Interprofessional continuing education (IPCE) scaling with team-based care | +0.9% | North America, Europe, Australia | Medium term (2-4 years) |

| Rebound and growth in commercial support and exhibit/advertising spend | +0.7% | North America, Europe | Short term (≤ 2 years) |

| AMA–UEMS mutual credit recognition enabling cross-border credit portability | +0.5% | North America and Europe | Long term (≥ 4 years) |

| Point-of-care and EHR-integrated microlearning CME acceptance expanding | +1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory Licensure and Recertification Requirements Tightening Globally

National and sub-national regulators are shortening renewal cycles and lifting credit minimums, effectively transforming CME from optional development into a licensure price of entry. China now obliges clinicians to log 25 credits annually, and India requires 30 credits every five years, both tracked in centralized registers that remove work-around loopholes [1]National Medical Commission India, “CME Enforcement in the National Medical Register,” NMC.ORG.IN. In the United States, 46 state medical boards link license renewal directly to CME hour completion, creating inelastic demand even as 48.2% of physicians report burnout.

Platforms that embed credits into everyday workflows such as Elsevier’s ClinicalKey AI, which grants 0.5 credits per clinical query benefit because they convert routine search behavior into compliant education. The upshot is a competition shift from price to convenience, rewarding providers that shrink friction through microlearning, podcasts, and mobile push alerts.

Interprofessional Continuing Education Scaling with Team-Based Care Models

Joint Accreditation counted 123,175 interprofessional activities in 2024, up from 113,000 a year earlier, signaling a shift among providers toward sessions that credit physicians, nurses, pharmacists, and allied staff simultaneously [2]Joint Accreditation for Interprofessional Continuing Education, “2024 Annual Report,” JOINTACCREDITATION.ORG. Health systems value these programs for improving collaboration; research links IPCE participation to 25% higher staff retention and 12% fewer safety incidents.

Applications for joint accreditation have grown significantly since 2019, reflecting a culture shift from siloed learning to shared competency frameworks. The February 2026 IPEC Symposium promoted outcome-based team assessment models, underscoring that credit volume alone is no longer sufficient.

Point-of-Care and EHR-Integrated Microlearning Expanding Acceptance

Physicians spend 15.6 weekly hours on EHR tasks, so inserting CME into that workflow solves the time-scarcity paradox. Wolters Kluwer’s alliance with Microsoft pipes UpToDate into ambient documentation tools, awarding credits as evidence summaries are viewed. Elsevier’s DrFirst tie-in applies a similar mechanic at the prescribing screen. Completion rates for five-minute micro-modules exceed 75%, far above the 40-50% typical for hour-long webinars, proving that format convenience, not content depth, now drives engagement across the continuing medical education market.

Live In-Person Courses Rebounding Despite Digital Convenience

Live congresses and workshops are projected to grow, outpacing all other formats, as clinicians seek networking and hands-on practice after years of virtual saturation. A 2024 Postgraduate Institute for Medicine survey ranked in-person meetings as the top preference, and 91% of Mayo Clinic conferees indicated they would return to the format. Exhibits and advertising revenue eclipsed USD 725 million in 2024, showing that sponsors still value physical floor space to reach targeted specialists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict independence standards limiting sponsor influence and proximity to promotion | -0.8% | North America, Europe | Medium term (2-4 years) |

| Fragmented global accreditation and CPD rules hindering portability and scale | -0.6% | Global, particularly Europe, Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Privacy regulations constraining outcomes data and closed-loop impact measurement | -0.4% | Europe (GDPR), North America (HIPAA), Asia-Pacific | Medium term (2-4 years) |

| Clinician time pressure and burnout limiting discretionary CME engagement | -1.0% | Global, most acute in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict Independence Standards Limiting Sponsor Influence and Commercial Support

ACCME rules effective 2022 curb sponsor participation in content design, triggering a 5% slide in commercial grants to roughly USD 700 million during 2024[3]Accreditation Council for Continuing Medical Education, “Standards for Integrity and Independence,” ACCME.ORG. Pharma and device firms redirected budgets toward non-accredited channels and congress exhibits, fragmenting provider revenue streams. Compliance overhead rose 15-20% as accredited firms expanded conflict-resolution and outcomes-analytics capacity, squeezing smaller medical-education companies that lack scale advantages

Clinician Time Pressure and Burnout Limiting Discretionary Engagement

Clinician schedules continue to tighten as administrative demands mount. Medscape’s 2025 National Physician Burnout & Suicide Report showed that 46% of physicians felt burned out; 68% said the strain undermined patient relationships, and 56% linked it to lower care quality. A 2024 American Medical Association survey reported similar pressure, with 48.2% of respondents experiencing burnout and 1 in 5 planning to exit practice within two years, signaling a clash between compulsory CME credits and dwindling discretionary time. Physicians already allocate 15.6 hours each week to EHR and other paperwork, and 52% cite lack of time as the main barrier to CME engagement, even when those credits are necessary for license renewal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Format: Live Courses Regain Momentum Amid Screen Fatigue

Regularly scheduled series held 48.30% of continuing medical education market share in 2025, reflecting their baked-in presence during hospital rounds and morbidity conferences. Nevertheless, live meetings are forecast to clock the segment’s fastest 6.95% CAGR, illustrating pent-up demand for tactile learning and real-time networking. That surge lifts the continuing medical education market size for live formats alongside premium fees as high as USD 2,000 per registration.

The growth does not eliminate digital demand; enduring online modules, podcasts, and internet-live webinars remain critical for clinicians in rural or resource-constrained settings. Yet they confront commoditization as free open-access content multiplies. Meanwhile, point-of-care CME embedded in EHR queries and microlearning platforms like Praktiki outflank both legacy digital and conference models by converting idle minutes into credit-earning moments.

By Provider Type: Government and Non-Profit Agencies Accelerate

Hospitals and health systems commanded 45.36% continuing medical education market share in 2025 because they can tie grand rounds and quality-improvement CME directly to employment contracts and value-based reimbursement metrics. However, government and non-profit bodies are set to outpace all rivals with a 6.86% CAGR to 2031, buoyed by federal grants for rural clinician upskilling and pandemic-preparedness curricula.

This trajectory raises the continuing medical education market size for grant-funded content libraries and creates partnership openings for commercial platforms that can supply scalable technology. Independent medical-education companies dependent on commercial support must diversify into learner-paid or institutional-subscription models to hedge sponsor-funding volatility post-standards tightening

By Audience/Profession: Physicians Remain Core, IPCE Gains Traction

Physicians contributed 68.90% of continuing medical education market size in 2025 and are projected to maintain a healthy 6.78% CAGR, protected by state boards that mandate 20-50 hours biennially. Yet the interprofessional education wave is pulling nurses, pharmacists, and allied staff into shared sessions, prompting providers to re-engineer curricula around team communication and safety culture.

The shift encourages bundled subscription offers covering multiple licenses inside one health-system contract. Over time this could dilute physician percentage share even as absolute credit volume rises, an inflection likely to reshape pricing, accreditation logistics, and marketing language across the continuing medical education industry.

Geography Analysis

North America accounted for 55.61% of continuing medical education market share in 2025 due to stringent state licensure rules in the United States and biennial CPD mandates in Canadian provinces. Digital mainstays such as Medscape, UpToDate, and ClinicalKey dominate online delivery, while specialty societies monopolize large-scale meetings. Mexico added incremental growth by enacting mandatory CME for public-sector physicians in 2024.

Europe is on track to post the highest 6.84% CAGR through 2031, a pace grounded in the AMA-UEMS reciprocity accord that cuts duplication for physicians practicing trans-Atlantically. Application volume at the European Accreditation Council for CME reached 2,735 in 2024, confirming appetite for cross-border activities. Fragmented national CPD schemes still inflate localization costs, yet the agreement’s signaling effect may spur similar deals in Asia-Pacific and Latin America.

Asia-Pacific ranks third by revenue. China mandates 25 credits per year and India enforces 30 every five years, tracked through centralized registries that tighten compliance. Japan, South Korea, and Australia run specialty-specific programs, while private platforms translate content to local practice contexts. The Middle East, Africa, and South America remain nascent but benefit from workforce-expansion policies in Saudi Arabia, the UAE, Brazil, and South Africa, collectively lifting baseline demand even where accreditation infrastructure lags.

Competitive Landscape

The continuing medical education market remains moderately fragmented; the top ten providers pool significant share of accredited revenue. Medscape, Wolters Kluwer, and Elsevier anchor global digital reach, each serving tens of millions of learners through freemium portals underwritten by advertising, sponsorship, and subscription tiers.

Workflow integration is one strategic front. Elsevier’s ClinicalKey AI dispenses credits for decision-support searches, embedding education at the prescribing step. Wolters Kluwer’s September 2024 pact with Microsoft implants UpToDate inside Dragon Copilot, positioning point-of-care learning as ambient documentation.

Format innovation is the second battlefront. The December 2025 launch of VirtualiSurg-Dräger SimLabsXR proves that VR simulation is transitioning from experimental to mainstream for high-stakes procedural skills. Simultaneously, audio companions such as Wolters Kluwer’s AudioDigest and newly acquired Learner’s Digest fill commute windows with passive CME, expanding recurring-revenue portfolios.

Continuing Medical Education Industry Leaders

Medscape Education

Wolters Kluwer

Elsevier

PlatformQ Health

Cleveland Clinic Center for Continuing Education

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Interprofessional Education Collaborative hosted a symposium that advanced competency-based IPCE metrics adopted by 1,200+ attendees.

- December 2025: VirtualiSurg and Dräger debuted SimLabsXR, a VR platform for ICU training, with plans to secure ACCME and ANCC accreditation during 2026.

- March 2025: AdventHealth completed the $260 million acquisition of the ShorePoint Health System expanding its clinical and educational reach.

Global Continuing Medical Education Market Report Scope

As per the scope of the report, Continuing Medical Education (CME) is a structured approach to lifelong learning designed to help healthcare professionals maintain competence and keep pace with rapid advancements in medical science, technology, and treatment protocols. As the third and longest phase of medical education—following undergraduate and graduate training, CME serves as a critical mechanism for bridging the gap between new research evidence and actual clinical practice.

The continuing medical education market is segmented by delivery format, provider type, audience/profession, and geography. By delivery format, the market is segmented into live courses, internet live, enduring materials, regularly scheduled series, point-of-care/EHR-integrated CME, performance/quality improvement, microlearning/nano-CME, and simulation/VR/AR-based activities.

By provider type, the market is segmented into publishing/education companies & digital platforms, physician membership organizations/specialty societies, schools of medicine/academic centers, hospitals & health systems, accredited independent medical education companies (MECCs), and government/non-profit agencies & foundations. By audience/profession, the market is segmented into physicians, nurses, pharmacists, physician associates/assistants, dentists, allied health/behavioral health, and interprofessional teams (IPCE).

By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Live Courses |

| Internet Live |

| Enduring Materials |

| Regularly Scheduled Series |

| Point-of-Care/EHR-integrated CME |

| Performance/Quality Improvement |

| Microlearning/Nano-CME |

| Simulation/VR/AR-based activities |

| Publishing/Education Companies & Digital Platforms |

| Physician Membership Organizations/Specialty Societies |

| Schools of Medicine/Academic Centers |

| Hospitals & Health Systems |

| Accredited Independent Medical Education Companies (MECCs) |

| Government/Non-profit Agencies & Foundations |

| Physicians (MD/DO) |

| Nursing (RNs, NPs) |

| Pharmacy (Pharmacists, Technicians) |

| Physician Associates/Assistants (PAs) |

| Dentistry (Dentists, Allied Dental Staff) |

| Allied Health/Behavioral Health (e.g., PT/OT, Social Work, Psych) |

| Interprofessional Teams (IPCE) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Delivery Format | Live Courses | |

| Internet Live | ||

| Enduring Materials | ||

| Regularly Scheduled Series | ||

| Point-of-Care/EHR-integrated CME | ||

| Performance/Quality Improvement | ||

| Microlearning/Nano-CME | ||

| Simulation/VR/AR-based activities | ||

| By Provider Type | Publishing/Education Companies & Digital Platforms | |

| Physician Membership Organizations/Specialty Societies | ||

| Schools of Medicine/Academic Centers | ||

| Hospitals & Health Systems | ||

| Accredited Independent Medical Education Companies (MECCs) | ||

| Government/Non-profit Agencies & Foundations | ||

| By Audience/Profession | Physicians (MD/DO) | |

| Nursing (RNs, NPs) | ||

| Pharmacy (Pharmacists, Technicians) | ||

| Physician Associates/Assistants (PAs) | ||

| Dentistry (Dentists, Allied Dental Staff) | ||

| Allied Health/Behavioral Health (e.g., PT/OT, Social Work, Psych) | ||

| Interprofessional Teams (IPCE) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the continuing medical education market?

The continuing medical education market size reached USD 11.2 billion in 2026 and is forecast to climb to USD 15.3 billion by 2031 at a 6.43% CAGR, underpinned by mandatory credit rules and widespread digital learning adoption.

Which delivery format is expanding fastest?

Live in-person courses, congresses, symposia, and workshops, are projected to grow at 6.95% CAGR through 2031, outpacing digital-only modules thanks to networking and hands-on skill demand.

What are the chief growth drivers?

Mandatory licensure quotas add 1.8 percentage points to growth, workflow-integrated microlearning contributes 1.1 points, and interprofessional education adds 0.9 points to the continuing medical education market CAGR.

Why does physician burnout restrain growth?

Burnout affects 46% of physicians, and 52% cite lack of time for CME, subtracting 1.0 percentage point from the market CAGR despite credit mandates.

Page last updated on: