Fabry Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

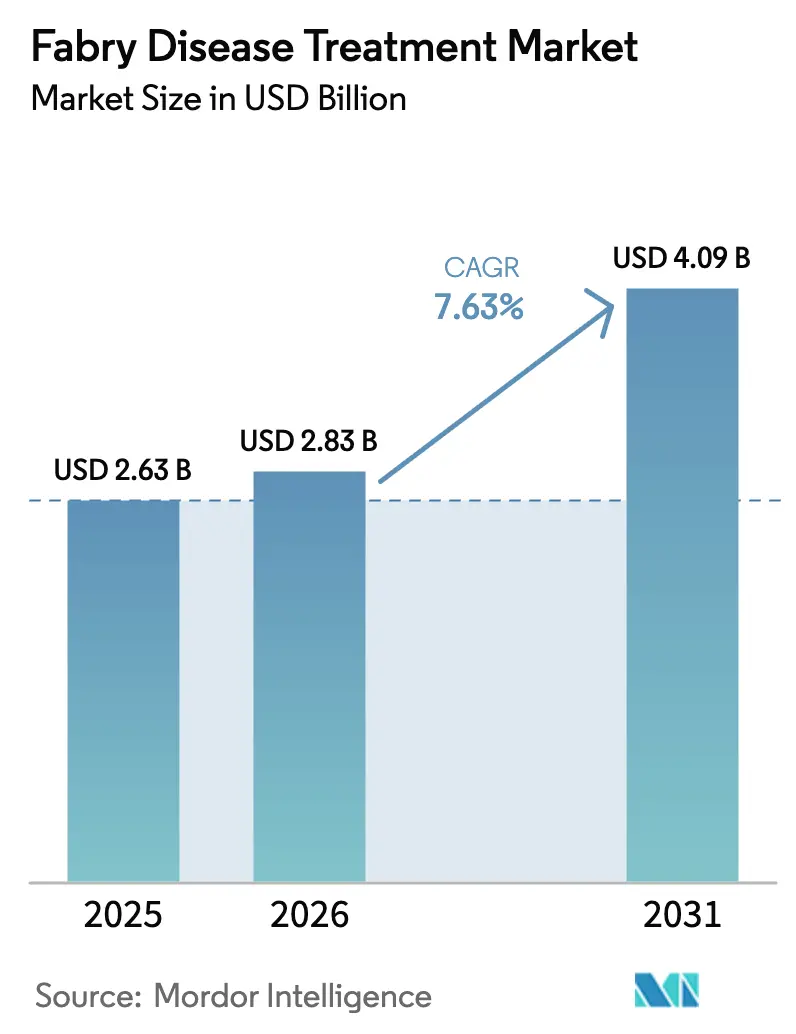

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 4.09 Billion |

| Growth Rate (2026 - 2031) | 7.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fabry Disease Treatment Market Analysis by Mordor Intelligence

The fabry disease treatment market size is expected to grow from USD 2.63 billion in 2025 to USD 2.83 billion in 2026 and is forecast to reach USD 4.09 billion by 2031 at 7.63% CAGR over 2026-2031. The Fabry disease treatment market is progressing from conventional bi-weekly enzyme replacement infusions toward once-only gene therapies and oral substrate reduction regimens. Growing clinical recognition of late-onset variants, broadened newborn screening, and favorable orphan-drug regulations are expanding the Fabry disease treatment market addressable population. Continued investment in home-infusion services and telemedicine reduces administration burdens and supports adherence. Manufacturing innovations and biosimilar pressure are simultaneously lowering entry barriers, amplifying competitive intensity in the Fabry disease treatment market[1]Matthias Lenders, Eva-Renee Menke, and Eva Brand, “Progress and Challenges in the Treatment of Fabry Disease,” BioDrugs, springer.com.

Key Report Takeaways

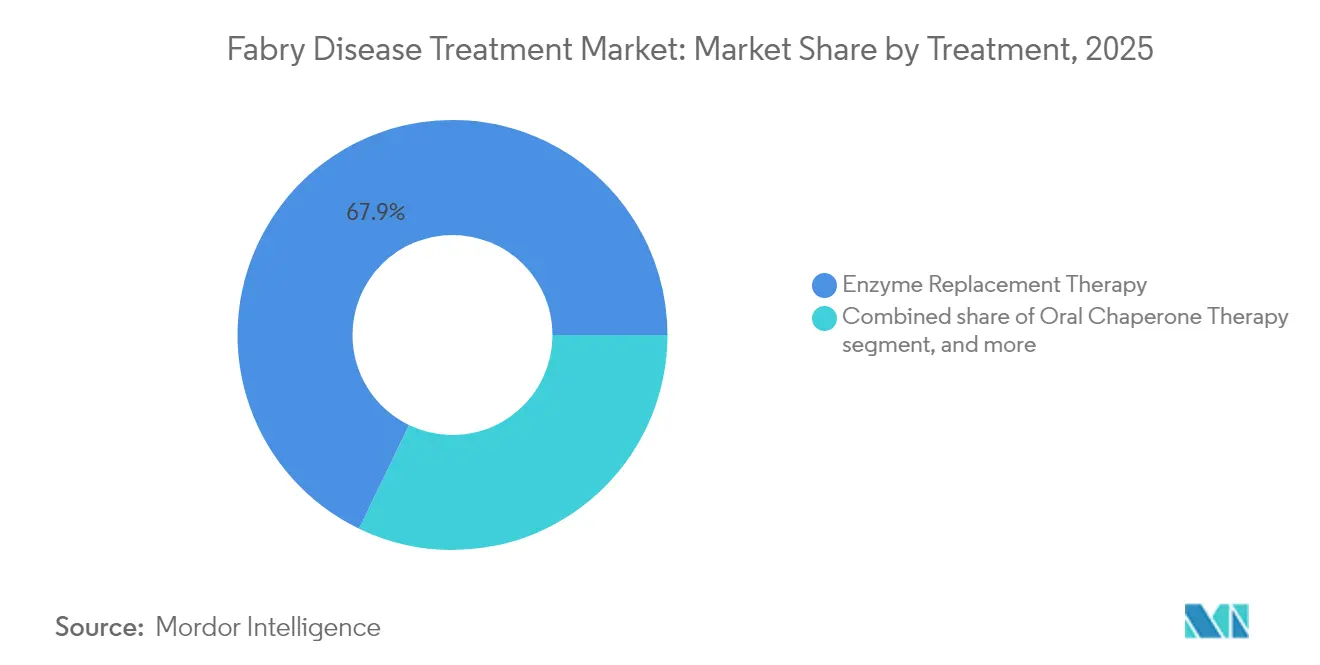

- By treatment, enzyme replacement therapy held 67.85% of the Fabry disease treatment market share in 2025 while gene therapy is projected to advance at a 9.18% CAGR through 2031.

- By route of administration, intravenous delivery commanded 72.60% of the Fabry disease treatment market size in 2025, whereas subcutaneous delivery is expected to expand at a 9.21% CAGR to 2031.

- By distribution channel, hospital pharmacies accounted for 55.70% of the Fabry disease treatment market size in 2025 and specialty pharmacies post the highest projected CAGR of 10.05% during 2026-2031.

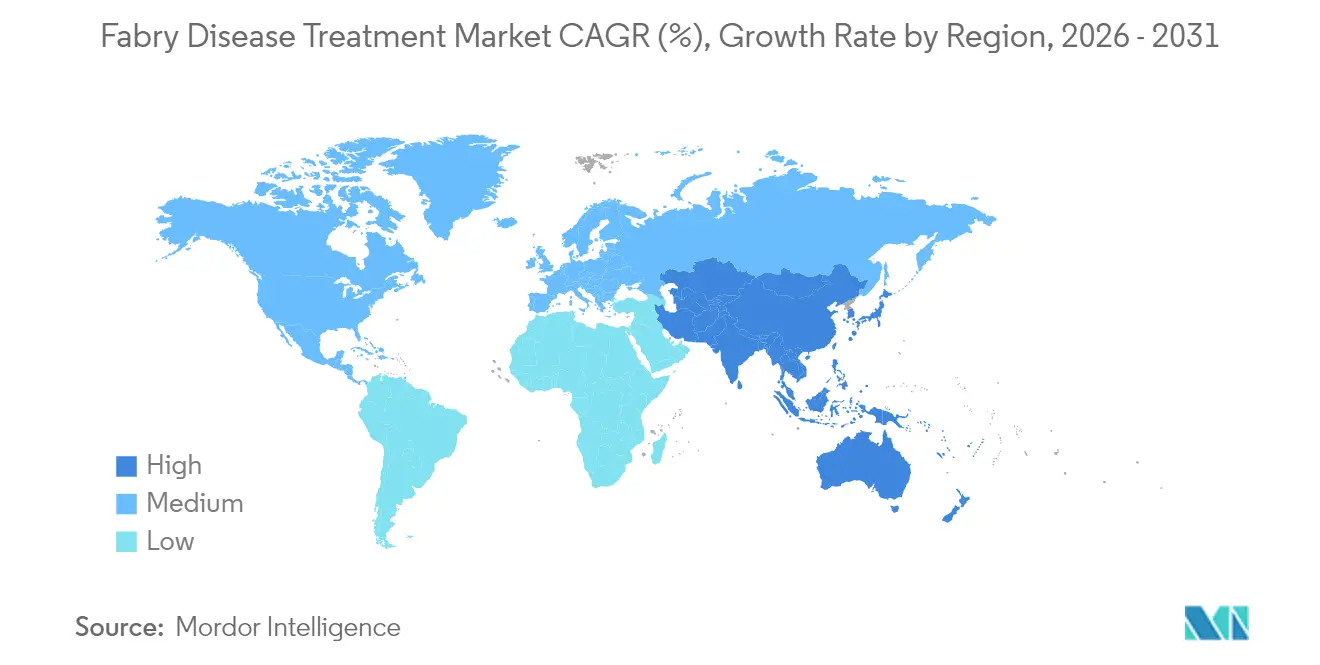

- By geography, North America led with 42.85% revenue share of the Fabry disease treatment market in 2025; Asia-Pacific is forecast to post the fastest 8.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fabry Disease Treatment Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of Fabry disease | +1.5% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Advancements in gene- and mRNA-based therapies | +1.2% | North America & EU leading, APAC following | Long term (≥4 years) |

| Favorable orphan-drug incentives and fast-track designations | +0.8% | Global, highest impact in US & EU | Short term (≤2 years) |

| Increasing global healthcare expenditure on rare diseases | +1.0% | Global, with regional variations | Medium term (2-4 years) |

| Strategic collaborations and licensing agreements | +0.9% | Primarily developed markets worldwide | Medium term (2-4 years) |

| Expansion of telemedicine and home-infusion services | +0.6% | North America & Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Fabry Disease

Re-evaluation of screening programs indicates Fabry disease affects nearly 1 in 10,000 individuals, a four-fold increase on earlier estimates. Late-onset forms account for most symptomatic cases and often escape detection until organ damage progresses, which creates a significant latent pool of untreated adults[2]James Cook et al., “Estimating the Prevalence of Late-Onset Fabry Disease in the US in 2024,” medRxiv, medrxiv.org. Broader renal and cardiology screening plus newborn testing in several countries funnels higher numbers of presymptomatic carriers into specialty clinics. This expanding patient funnel underpins sustained demand in the Fabry disease treatment market.

Advances in Gene and mRNA Therapies

Multiple AAV-based vectors now show persistent α-galactosidase A expression for at least two years, minimizing immunogenicity and infusion burden. FDA agreement on an accelerated approval path for Sangamo’s ST-920 underscores rising regulatory confidence in biomarker-driven endpoints. uniQure’s AMT-191 and Exegenesis Bio’s EXG110 hold orphan designations and early safety data support single-dose curative potential. Each milestone heightens investor interest and propels the Fabry disease treatment market toward transformative modalities.

Favorable Orphan-Drug Incentives and Fast-Track Designations

Seven-year exclusivity, tax credits, and priority review vouchers shorten time-to-market and protect pricing flexibility. The Inflation Reduction Act’s orphan exemption preserves revenue potential by shielding rare-disease therapies from mandatory Medicare negotiations. Collectively these policy levers de-risk pipeline investment and accelerate availability of novel agents in the Fabry disease treatment market.

Increasing Global Healthcare Expenditure on Rare Diseases

Orphan drugs are projected to represent 20% of total prescription outlays by 2026. Average annual therapy cost for a rare-disease patient has risen to USD 147,000, with Fabry drugs exceeding USD 400,000 per year in some markets. China’s Hainan Province recorded an 88.99% annual growth in rare-disease spend between 2019-2023, illustrating escalating resource commitments that underpin the Fabry disease treatment market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs and payer budget constraints | -0.7% | Global, most severe in emerging markets | Medium term (2-4 years) |

| Limited diagnostic infrastructure in emerging markets | -0.5% | APAC, MEA, Latin America | Long term (≥4 years) |

| Manufacturing capacity constraints for advanced therapies | -0.4% | Global, heightened in regions with limited biomanufacturing | Short term (≤2 years) |

| Stringent reimbursement criteria and access barriers | -0.6% | Global, pronounced in cost-constrained health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Payer Budget Constraints

Elfabrio’s annual price surpasses USD 430,000, placing Fabry therapy among the costliest prescriptions worldwide. Insurers often restrict reimbursement until organ pathology is documented, delaying initiation and potentially worsening prognosis[3]Morgan Loh and Julia Settler, “Clinical Overview: Elfabrio for Fabry Disease in Adults,” Pharmacy Times, pharmacytimes.com. Variable public financing leaves emerging-market patients exposed to catastrophic out-of-pocket fees, muting penetration rates in the Fabry disease treatment market despite rising clinical need.

Limited Diagnostic Infrastructure in Emerging Markets

Sophisticated enzymatic assays and gene sequencing remain scarce outside major urban centers. Misdiagnosis is common because neuropathic pain, proteinuria, and hypertrophic cardiomyopathy mimic more prevalent disorders. Absence of newborn screening in many low- and middle-income nations delays identification for years, shrinking the treated cohort and restraining Fabry disease treatment market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment: Gene Therapy Drives Innovation Despite ERT Dominance

Enzyme replacement therapy generated 67.85% of Fabry disease treatment market revenue in 2025 and continues to anchor clinical practice due to decades of safety data. However, gene therapy is forecast to post a 9.18% CAGR, reflecting patient demand for single-dose, potentially curative solutions. Oral chaperone migalastat addresses amenable mutations, and substrate reduction agent venglustat is in Phase III for neuropathic pain management. The diversified pipeline signals that the Fabry disease treatment market will transition toward modality pluralism rather than a single therapeutic hegemon.

Gene therapy sponsors improve vector tropism and dosing efficiency, reducing manufacturing cost and immunogenic risk. Pegunigalsidase alfa’s monthly infusion option demonstrates legacy ERT innovation while biosimilar entries loom as patents expire. Collectively, these shifts promise a more competitive and patient-centric Fabry disease treatment market over the next decade.

By Route of Administration: Subcutaneous Delivery Gains Momentum

Intravenous infusions accounted for 72.60% of the Fabry disease treatment market size in 2025 given that all approved ERTs require vein access. Patients increasingly favor subcutaneous formulations under development that permit self-administration at home, driving a 9.21% CAGR for this route. Oral migalastat offers unmatched convenience for mutation-amenable patients but serves a narrow niche. Gene therapy could ultimately bypass chronic administration entirely, redefining expectations within the Fabry disease treatment market.

Home-infusion services now cover most urban areas in North America and Europe, cutting administration costs and hospital time. Subcutaneous development programs aim to replicate efficacy while shrinking infusion duration, an advance particularly valuable in regions with sparse infusion centers. These delivery innovations reinforce adherence and expand reach, bolstering long-term growth of the Fabry disease treatment market.

By Distribution Channel: Specialty Pharmacies Capitalize on Complexity

Hospital pharmacies captured 55.70% share of the Fabry disease treatment market in 2025 driven by in-hospital infusion dominance. Specialty pharmacies are projected to deliver a 10.05% CAGR by supplying complex dispensing, nursing coordination, and insurance navigation that high-touch rare diseases demand. Retail chains remain minor participants because of cold-chain requirements and payer mandates, though they distribute oral agents. The widening role of specialty pharmacies improves logistic resilience and patient experience, supporting wider adoption across the Fabry disease treatment market.

Payers increasingly channel high-cost biologics through limited distribution networks that couple dispensing with adherence programs and outcome reporting. This model aligns stakeholder incentives by improving real-world effectiveness and justifying budget impact, reinforcing specialty pharmacy ascendance. Hospital pharmacies retain relevance for initiation and high-risk monitoring, yet even these functions are migrating to ambulatory or home settings as the Fabry disease treatment market seeks efficiency.

Geography Analysis

North America led with 42.85% Fabry disease treatment market revenue in 2025 underpinned by broad newborn screening, specialist centers, and comprehensive reimbursement. The FDA routinely applies priority and breakthrough designations, enabling swift adoption of novel modalities. Despite payer scrutiny, commercial plans typically cover enzyme replacement and migalastat, while multiple gene therapy trials recruit aggressively across the United States and Canada.

Europe ranks second, benefiting from cross-border regulatory harmonization via the EMA and robust academic registries tracking long-term outcomes. National health technology assessments can delay uptake but ultimately assure broad coverage. Recent Scottish approval for pegunigalsidase alfa highlights continued regional expansion of the Fabry disease treatment market. EU research consortia and patient groups provide an integrated ecosystem that supports evidence generation and guideline refinement.

Asia-Pacific is the fastest growing zone at an 8.28% CAGR. Japan’s conditional early-access framework and South Korea’s national insurance adoption of ERT illustrate mature system capacity. China’s rare-disease catalog, expanded reimbursement, and domestic biotech investment collectively accelerate penetration. Rising clinical trial activity and infrastructure upgrades in India and Southeast Asia suggest further upside for the Fabry disease treatment market over the horizon.

Competitive Landscape

The fabry disease treatment market remains moderately concentrated yet increasingly contested. Sanofi, Takeda, and Chiesi defend entrenched ERT franchises while scaling manufacturing to counter biosimilar threats. Amicus Therapeutics leverages oral migalastat differentiation and recorded USD 528.3 million revenue in 2024, implying 33% annual growth and confirming strong physician adoption.

Gene therapy challengers pursue curative positioning. Sangamo’s ST-920 secured an FDA alignment for accelerated approval based on eGFR slope, aiming to launch by 2027. uniQure’s AMT-191 and Exegenesis EXG110 add competitive diversity, enhancing patient choice and price discipline. Pegylated PRX-102 from Protalix and Chiesi demonstrates incremental innovation within ERT class, extending infusion intervals to four weeks and offering improved pharmacokinetics.

Supply chain reliability and patient-support programs emerge as decisive differentiators. Past shortages of Fabrazyme triggered legal scrutiny and underscore the premium on robust manufacturing and logistics. Specialty pharmacies and home-infusion providers integrate digital adherence tools and nurse coaching, creating service layers that competitors must match as the Fabry disease treatment market evolves.

Fabry Disease Treatment Industry Leaders

Sanofi (Genzyme Corporation)

Takeda Pharmaceutical Company Limited

Amicus Therapeutics, Inc

ISU ABXIS

JCR Pharmaceuticals Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Amicus Therapeutics posted record USD 528.3 million revenue for 2024, a 33% YoY increase, and raised 2028 revenue guidance above USD 1 billion.

- January 2025: Sangamo Therapeutics secured FDA agreement that one-year eGFR slope will support accelerated approval of ST-920, with BLA filing expected H2 2026.

- December 2024: Exegenesis Bio gained FDA orphan-drug status for EXG110 and initiated China Phase I trials, with US enrollment planned.

- September 2024: Chiesi launched a grant initiative to fund lysosomal storage disorder research, including Fabry projects.

- July 2024: Scottish Medicines Consortium approved Chiesi’s pegunigalsidase alfa, broadening UK access.

- December 2024: AdventHealth opened recruitment for Phase III PERIDOT study of venglustat tablets in Fabry neuropathic pain.

Global Fabry Disease Treatment Market Report Scope

As per the scope of the report, Fabry disease is defined as a rare genetic condition that is marked by the deficiency of an enzyme called alpha-galactosidase A. The lower levels or absence of alpha-galactosidase A causes the accumulation of globotriaosylceramide (GL-3) in the affected tissues of the central nervous system, heart, kidneys, and skin. The Fabry disease treatment market is segmented by treatment (enzyme replacement therapy, oral chaperone therapy, and other treatments), route of administration (oral route and intravenous route), distribution channel (hospital pharmacies, retail pharmacies, and online pharmacies), and geography (North America, Europe, Asia-Pacific and Rest of the World). The report offers the value (in USD) for the above segments.

| Enzyme Replacement Therapy |

| Oral Chaperone Therapy |

| Gene Therapy |

| Substrate Reduction Therapy |

| Other Treatments |

| Intravenous |

| Oral |

| Subcutaneous |

| Hospital Pharmacies |

| Retail Pharmacies |

| Specialty Pharmacies |

| Online Pharmacies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | GCC | |

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Treatment | Enzyme Replacement Therapy | ||

| Oral Chaperone Therapy | |||

| Gene Therapy | |||

| Substrate Reduction Therapy | |||

| Other Treatments | |||

| By Route of Administration | Intravenous | ||

| Oral | |||

| Subcutaneous | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Specialty Pharmacies | |||

| Online Pharmacies | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | GCC | ||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current Fabry disease treatment market size and projected growth?

The market is valued at USD 2.83 billion in 2026 and is expected to reach USD 4.09 billion by 2031, delivering a 7.63% CAGR.

Which therapy type dominates the Fabry disease treatment market?

Enzyme replacement therapy leads with 67.85% revenue share in 2025, although gene therapy shows the fastest 9.18% CAGR outlook.

Which region grows fastest in the Fabry disease treatment market?

Asia-Pacific posts the highest 8.28% CAGR through 2031 due to rising diagnosis rates, expanding reimbursement, and local clinical trial activity.

How are high treatment costs influencing market access?

Annual therapy prices above USD 400,000 drive stringent reimbursement criteria, particularly in emerging markets, tempering uptake despite clinical benefits.

What role do specialty pharmacies play in this market?

Specialty pharmacies offer tailored patient support and complex reimbursement services, fueling a 10.05% CAGR and increasing their share of drug dispensing.

Page last updated on: