Fabric Softeners And Conditioners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

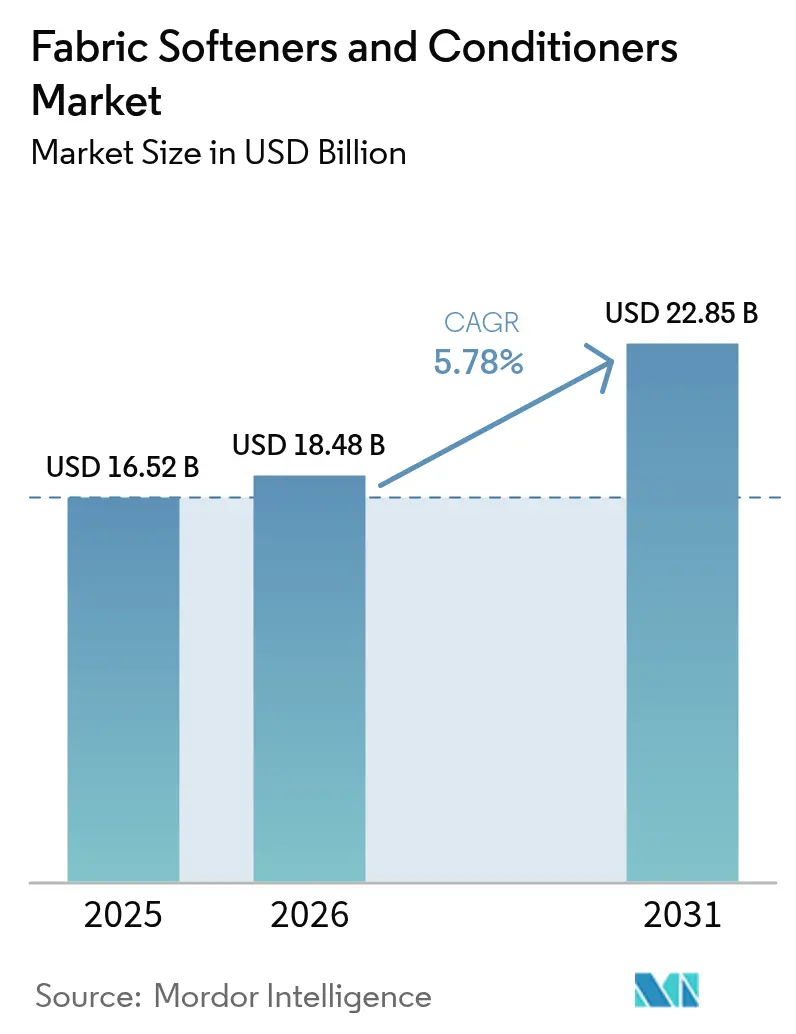

| Market Size (2026) | USD 18.48 Billion |

| Market Size (2031) | USD 22.85 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

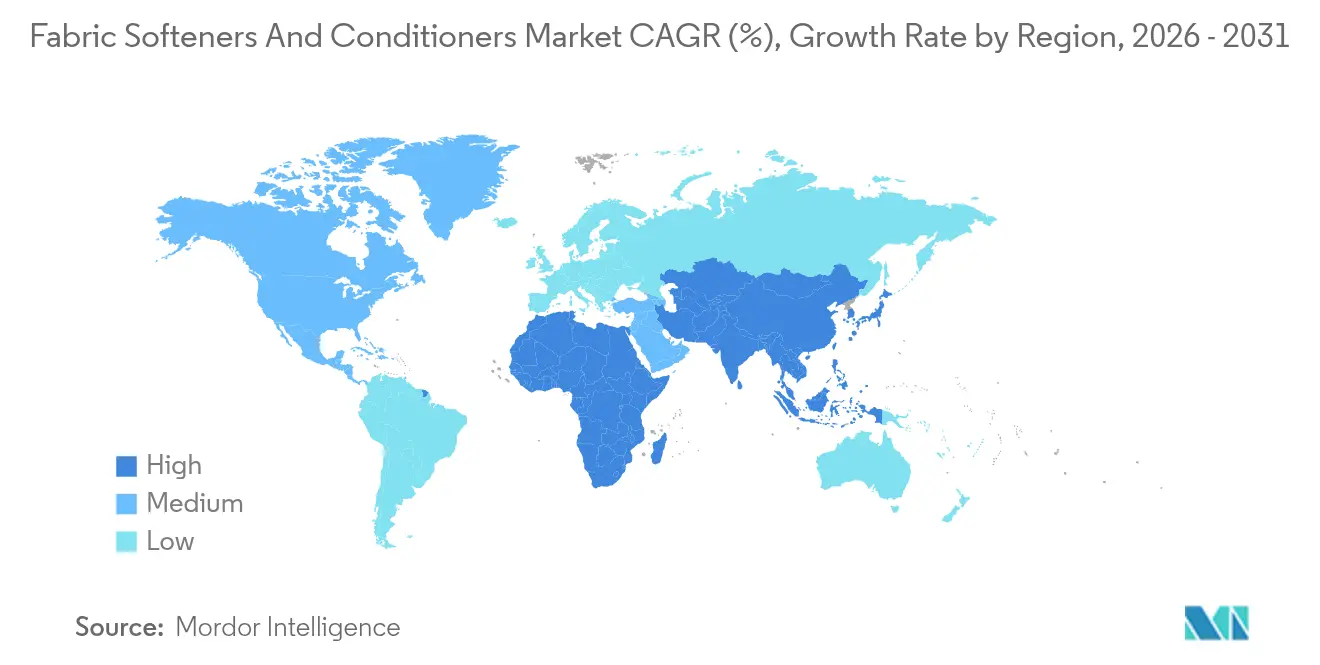

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fabric Softeners And Conditioners Market Analysis by Mordor Intelligence

The fabric softeners and conditioners market size is expected to increase from USD 16.52 billion in 2025 to USD 18.48 billion in 2026 and reach USD 22.85 billion by 2031, growing at a CAGR of 5.78% over 2026-2031. Concentrated liquids, bio-based quaternary ammonium compounds, and refillable packaging are reshaping category economics, reducing per-load material costs while letting brands charge premiums for eco-positioned formulas. Regulatory scrutiny of conventional cationic surfactants: California authorities report that 89.6% of conditioners still rely on quats with documented aquatic toxicity, forcing reformulation and splitting supply chains between sustainable palm-oil derivatives and petroleum-based alternatives. Europe’s upcoming digital product passports raise compliance costs, but also reward first movers able to verify biodegradability and traceability at the Stock-Keeping Unit level. Demand shifts toward devices that meter smaller doses—automatic dispensers embedded in washing machines now reach 60% penetration in Asia-Pacific urban sales—further cementing concentrated liquids as the standard.

Key Report Takeaways

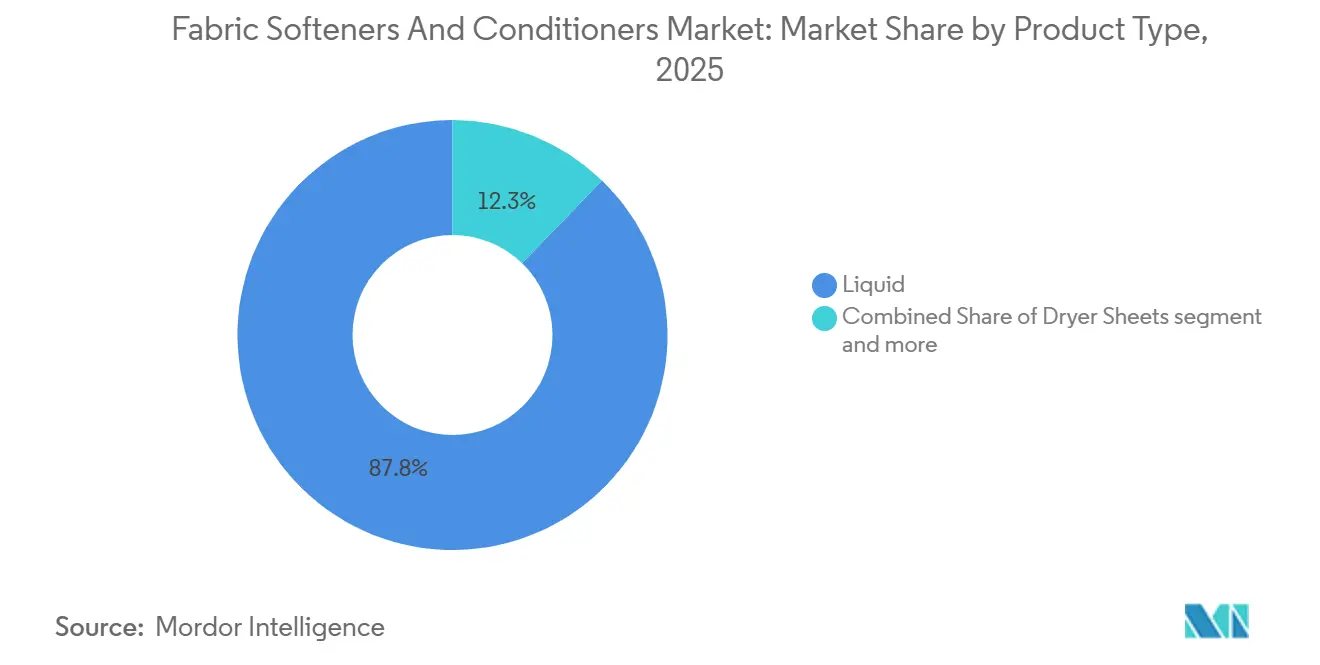

- By product type, liquid softeners accounted for 87.75% revenue share in 2025, while dryer sheets are forecast to expand at a 7.32% CAGR to 2031.

- By nature, conventional formulations held 80.65% of the fabric softeners and conditioners market share in 2025; organic variants are projected to grow at a 7.41% CAGR through 2031.

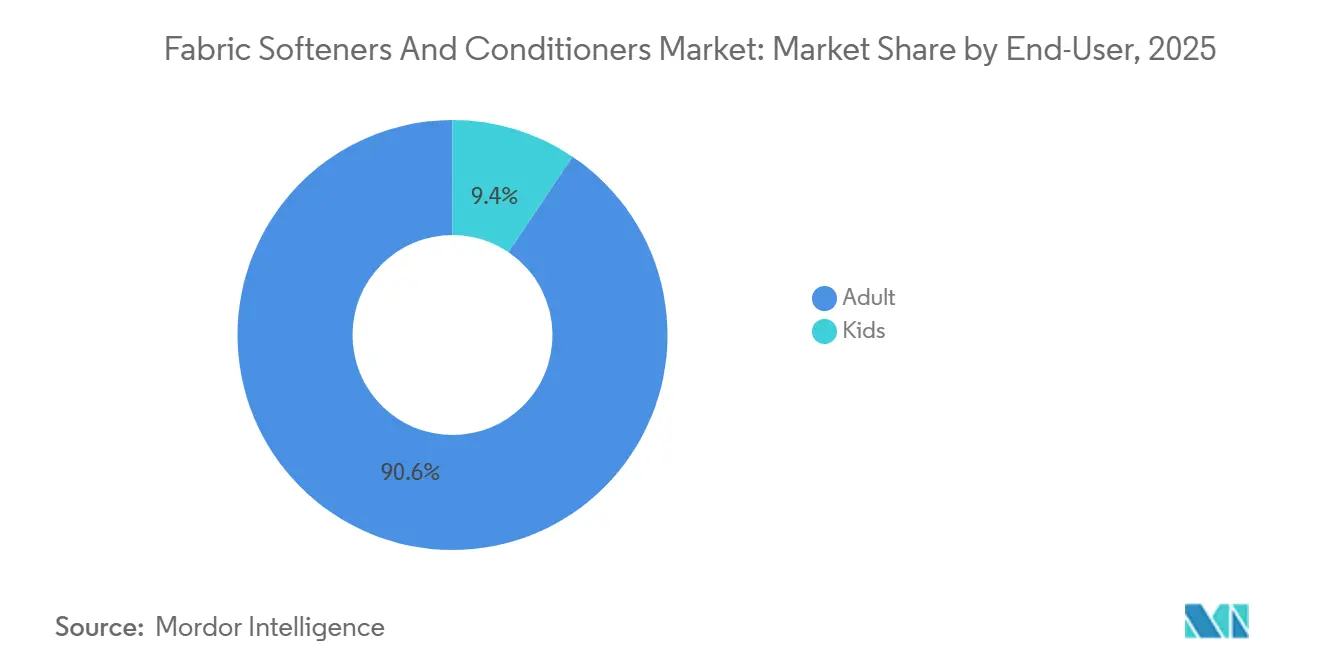

- By end user, adults dominated with 90.57% of 2025 sales, whereas the kids segment is advancing at a 6.31% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets captured 41.21% of value in 2025, but online retail is set to post a 7.38% CAGR up to 2031.

- By geography, North America led with 35.21% share in 2025; Asia-Pacific is on track for the fastest 7.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fabric Softeners And Conditioners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Awareness of Fabric Protection and Cleanliness | +1.2% | Global, with peak intensity in North America and Europe | Short term (≤ 2 years) |

| Advancements in Formula Development | +1.5% | North America, Europe, Asia-Pacific urban clusters | Medium term (2-4 years) |

| Boom in Green and Sustainable Solutions | +1.3% | Europe, North America, urban Asia-Pacific | Long term (≥ 4 years) |

| Expanding Adoption of Laundry Appliances | +1.4% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Customization and Premium Fragrances | +0.8% | North America, Middle East, Western Europe | Short term (≤ 2 years) |

| Promotional Campaigns and Influencer Partnerships | +0.6% | Global, with digital-first markets leading | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Awareness of Fabric Protection and Cleanliness Spurs Product Demand

Post-pandemic hygiene consciousness persists, with 80% of consumers washing laundry at least once weekly using quick cycles, according to A.I.S.E.'s 2025 pan-European study, yet this frequency strains textile fibers and accelerates wear. Fabric softeners mitigate mechanical abrasion by depositing cationic surfactants that lubricate fiber surfaces, extending garment lifespan by an estimated 15-20% in controlled wash tests. This value proposition resonates in inflationary environments where apparel replacement costs climb. The California DTSC's December 2024 background document noted that 89.6% of conditioners rely on quaternary ammonium compounds, underscoring the category's technical maturity but also spotlighting the regulatory scrutiny that will reshape formulation roadmaps. Brands emphasizing fabric-protection claims, such as Procter & Gamble's Downy Rinse & Refresh, launched in February 2024 with a 12-week freshness guarantee, capture incremental share by framing softeners as preventive maintenance rather than discretionary indulgence

Advancements in Formula Development Improve Efficacy and Appeal

Encapsulation technology, exemplified by Unilever's 2024 WIPO patent filing on microencapsulated fragrance-release systems, allows scent molecules to survive wash cycles and activate during wear through friction, delivering olfactory performance that justifies price premiums of 20-30% over commodity liquids. Henkel's European Patent Office grant (EP3976756B1) in 2024 for biodegradable ester-quat compositions demonstrates how green chemistry can match or exceed the softness imparted by traditional diester-dimethyl-ammonium chlorides while achieving >90% biodegradation within 28 days under OECD 301B protocols. Procter & Gamble's March 2024 U.S. patent (US11939554B2) on cationic-polymer-silicone blends enhances wrinkle reduction and static control, addressing the 43% of European consumers who expressed interest in app-connected laundry features that optimize dosing based on fabric type, according to the USPTO Patent Database[1]Source: United States Patent and Trademark Office, “US11939554B2,” uspto.gov. These innovations compress time-to-market for differentiated SKUs, enabling incumbents to defend shelf space against private-label encroachment.

Boom in Green and Sustainable Solutions Aligns with Eco-Trends

The European Commission's November 2025 Council position on the revised Detergents Regulation (COM(2023)217) mandates digital product passports, phosphorus limits, and enhanced biodegradability criteria, compelling manufacturers to reformulate or forfeit access to the EU's 450-million-consumer market, according to the European Commission[2]Source: European Commission, “Detergents Regulation – Environment,” europa.eu. Unilever's Comfort Botanicals, launched in May 2024 with 95% biodegradable ingredients and CrystalFresh technology, secured listings in 15 markets by meeting both EU Ecolabel and Safer Choice standards, a dual certification that only 12% of global softener SKUs achieved as of 2024. The Roundtable on Sustainable Palm Oil reported that 19% of global palm oil carried RSPO certification in 2023, with 4.6 million metric tons sold to buyers including Procter & Gamble, Henkel, and Colgate-Palmolive, yet demand for certified esterquats outstrips supply, creating procurement bottlenecks that elevate input costs by 8-12%. Blueland's July 2024 Series B raise of USD 20 million signals investor confidence in zero-plastic refill models, which eliminate single-use bottles and appeal to the 49% of European consumers prioritizing recyclable packaging

Expanding Adoption of Laundry Appliances Broadens Market Reach

Washing-machine penetration in urban China reached 95% in 2024, while urban India attained 45% and Indonesia 60%, according to national statistics bureaus, unlocking addressable populations that previously relied on hand-washing, according to the National Bureau of Statistics of China[3]Source: National Bureau of Statistics of China, “Statistical Communiqué 2024,” stats.gov.cn. Automatic dispensers in mid-tier and premium machines, now standard in 60% of units sold in Asia-Pacific, optimize softener dosing and reduce waste, lowering per-load costs and encouraging trial among price-sensitive cohorts. E-commerce platforms such as Alibaba and Amazon embed softener purchases into appliance bundles, with Unilever's 2024 partnership with Alibaba integrating Comfort SKUs into washing-machine starter kits shipped to 1.2 million Chinese households. Rural electrification programs in India and Indonesia, supported by World Bank infrastructure loans, extend grid access to 80 million additional households by 2026, creating a latent demand pool that will materialize as appliance financing becomes available.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ecological Issues and Backlash Raise Sustainability Concerns | -0.9% | Europe, North America, urban Asia-Pacific | Medium term (2-4 years) |

| Skin Allergies and Irritations Impact Sensitive Consumers | -0.7% | Global, with heightened scrutiny in North America and Europe | Short term (≤ 2 years) |

| Fake and Substandard Goods Undermine Market Confidence | -0.5% | Middle East, Latin America, Southeast Asia | Short term (≤ 2 years) |

| Disruptions in Supply Chains and Ingredient Costs Cause Volatility | -0.8% | Global, with acute pressure in Asia-Pacific and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ecological Issues and Backlash Raise Sustainability Concerns

Quaternary ammonium compounds, the cationic surfactants in 89.6% of fabric conditioners, exhibit aquatic toxicity at concentrations as low as 0.1 mg/L, according to California's Department of Toxic Substances Control December 2024 background document, prompting wastewater-treatment facilities in Germany and the Netherlands to flag effluent non-compliance. The European Commission's revised Detergents Regulation, negotiated by the Council in November 2025, imposes digital product passports that trace ingredient origins and biodegradability scores, raising compliance costs by an estimated 6-8% for mid-tier producers lacking vertical integration. Activist campaigns targeting microplastic shedding from synthetic textiles—exacerbated by softener residues that coat fibers—pressure retailers to delist non-certified SKUs; Henkel's shift to 50% recycled plastic in Snuggle bottles and Unilever's 95% biodegradable Comfort Botanicals formulation represent defensive pivots to preserve shelf access. Consumer willingness to pay for eco-certified products plateaus at 15-20% premiums, limiting margin recovery for reformulation investments.

Fake and Substandard Goods Undermine Market Confidence

Counterfeit fabric softeners, prevalent in Middle Eastern souks and Latin American open markets, contain substandard surfactants and undisclosed fillers that trigger allergic reactions and fabric damage, eroding trust in legitimate brands. Procter & Gamble's 2024 anti-counterfeiting initiative in Saudi Arabia and the United Arab Emirates deployed blockchain-enabled QR codes on Downy bottles, enabling consumers to verify authenticity, yet adoption remains below 30% due to low smartphone penetration in rural areas. Regulatory enforcement gaps in Nigeria, Egypt, and Morocco allow unbranded products to capture 15-20% of volume, undercutting premium-tier pricing by 40-50% and forcing multinationals to compete on cost rather than innovation. The World Health Organization's 2024 guidance on household-chemical safety standards, while non-binding, pressures governments to tighten import controls, yet implementation lags by 2-3 years in resource-constrained jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Concentration Drives Liquid Dominance

In 2025, liquid softeners dominated the market with an 87.75% share, thanks to their ease of dosing, compatibility with automatic dispensers, and flexible formulations. These formulations can accommodate enzymes, encapsulated fragrances, and biodegradable surfactants. In February 2025, Henkel launched its Snuggle formulas, now 16% more concentrated. These new formulas come in bottles made from 50% recycled plastic and are projected to save 9 million gallons of water annually. This move underscores how increased concentration can lead to reduced packaging waste and logistics costs, ultimately cutting per-unit carbon footprints by 25 to 30%. Dryer sheets, projected to grow at a 7.32% CAGR through 2031, have found favor among North American and European consumers. These consumers prioritize convenience and single-dose control. The compact nature of dryer sheets is ideal for urban apartments with limited storage, and their anti-static properties cater to the care of synthetic fabrics. Procter & Gamble's Bounce brand, revamped in 2024 with plant-based fibers, is strategically targeting the 40% of households that use concentrated detergents and are on the lookout for eco-friendly credentials.

Other formats, such as beads, crystals, and dissolvable pods, are carving out a niche. These early adopters are willing to pay a 30 to 40% premium for the novelty and precise dosing these formats offer. Unilever's Comfort Botanicals, introduced in May 2024, boasts 15 SKUs that span both liquids and in-wash boosters. Utilizing CrystalFresh technology, these products claim a competitive edge with their 12-week freshness promise, setting them apart from standard commodity liquids. While liquid formats enjoy the advantage of established supply chains and retailer familiarity, dryer sheets are gaining momentum in markets. Here, front-loading machines, which benefit from in-drum softening, have yet to reach a 50% penetration rate. Regulatory changes are also leaning in favor of liquid formats. The European Commission's Detergents Regulation revision in November 2025 introduced digital product passports. These passports trace ingredient origins, a requirement that liquid formulations, with their simpler supply chains, can more readily fulfill.

By Nature: Conventional Strength Meets Organic Momentum

In 2025, conventional formulations captured an 80.65% market share, supported by cost advantages as petroleum-basedbio-based quaternary ammonium compounds were 15 to 20 percent cheaper than their bio based esterquat counterparts and offered comparable performance in softness and static control. Organic softeners, projected to grow at a 7.41% CAGR through 2031, utilize ester quat chemistries that achieve over 90 percent biodegradation within 28 days, adhering to OECD 301B protocols. This compliance ensures they meet the stringent thresholds set by the EU Ecolabel and the EPA's Safer Choice. Henkel's 2024 patent grant (EP3976756B1) from the European Patent Office underscores the potential of biodegradable ester quat compositions. These compositions not only rival but can surpass the performance of traditional diester dimethyl ammonium chlorides, all while adhering to regulatory standards. Unilever's Comfort Botanicals, boasting 95 percent biodegradable ingredients, proudly holds dual certifications from the EU Ecolabel and Safer Choice. This achievement is noteworthy, as only 12 percent of global softener SKUs attained such recognition by 2024.

Retailer mandates are further propelling the shift towards organic products. By 2027, European supermarket chains are pushing for 30 percent of fabric care SKUs to flaunt third-party eco labels, thereby squeezing shelf space for conventional offerings. The Roundtable on Sustainable Palm Oil highlighted that in 2023, 19 percent of the global palm oil market bore RSPO certification. Notably, 4.6 million metric tons of this certified oil found its way to major buyers like Procter & Gamble and Henkel. However, a pronounced demand for certified esterquats, outpacing supply, has led to notable procurement challenges. While organic variants enjoy a 20 to 30 percent price premium, this pricing strategy curtails their reach among price-sensitive demographics in the Asia Pacific and Latin America. Here, conventional softeners still reign supreme, especially in rural areas and among lower-income urbanites. Blueland, with its innovative zero plastic refill tablets, has tapped into this market gap. Backed by a USD 20 million Series B funding in July 2024, Blueland marries organic formulations with eco-friendly packaging, resonating with the 49 percent of European consumers who prioritize recyclability.

By End-User: Adult Focus Expands to Specialized Kids Market

Adults accounted for 90.57% of end-use in 2025, driven by higher per-capita laundry volumes and willingness to pay for premium fragrances and performance attributes. The kids segment, growing at 6.31% CAGR through 2031, benefits from pediatric dermatology endorsements and hypoallergenic certifications that address the 18% prevalence of contact dermatitis among children exposed to quaternary ammonium compounds and synthetic fragrances. Procter & Gamble's Dreft brand, reformulated in 2024 to exclude high-concern surfactants and meet EPA Safer Choice DCC-13 benchmarks, targets new parents willing to pay 25-35% premiums for clinically validated gentleness. Unilever's Comfort Pure, launched in Asia-Pacific markets in 2024, leverages plant-derived surfactants and fragrance-free formulations to capture share among households with infants and toddlers.

Adult-segment growth hinges on premiumization; Henkel's Snuggle concentration increase in February 2025 allows consumers to adjust dosing for fabric weight, reducing waste and appealing to sustainability-conscious buyers. Customization extends to fragrance; Procter & Gamble's Downy Infusions line, relaunched in 2024 with botanically inspired scent profiles, targets the 32% of North American adults citing fragrance as the primary purchase driver. Kids-segment players face higher testing costs, clinical validation for hypoallergenic claims adds USD 150,000-USD 300,000 per SKU, and longer approval cycles. Retailer private-label entries in the kids tier remain limited, granting branded players pricing power and margin expansion opportunities.

By Distribution Channels: E-Commerce Disrupts Traditional Retail

Supermarkets and hypermarkets retained a 41.21% share in 2025, leveraging high foot traffic, promotional end-caps, and private-label penetration that reached 22% in European markets. Online retail channels, expanding at 7.38% CAGR through 2031, benefit from subscription models, direct-to-consumer brands, and algorithm-driven recommendations that personalize softener selection based on fabric type and washing-machine compatibility. Unilever's 2024 partnership with Alibaba integrated Comfort SKUs into washing-machine starter kits shipped to 1.2 million Chinese households, embedding brand trial into appliance purchases. Blueland's refillable tablet system, supported by USD 20 million in Series B funding raised in July 2024, bypasses traditional retail entirely, achieving customer-acquisition costs 40% below industry averages through user-generated content and influencer partnerships.

Convenience and grocery stores capture 18-20% of volume, serving top-up purchases and rural markets with limited hypermarket access. Other distribution channels, including direct sales, institutional buyers, and laundromat suppliers, account for the remainder, with laundromats in urban Asia-Pacific and Latin America adopting bulk-softener dispensers that reduce per-load costs by 30-40%. Amazon's Subscribe and Save program, offering 15% discounts on recurring softener deliveries, locks in consumers and compresses retail margins, forcing brick-and-mortar chains to match pricing or lose share. Digital-first brands exploit lower overhead, Blueland operates without physical stores, and invest savings into product innovation and sustainability certifications that command premiums in online marketplaces.

Geography Analysis

In 2025, North America commanded a 35.21% market share, supported by high per capita consumption, swift adoption of enzyme-enhanced softeners, and retailer mandates for Safer Choice certification. These mandates favor established players with compliant infrastructures. Procter & Gamble's Downy Infusions line, reintroduced in 2024 with botanically inspired scents, aims at the 32% of consumers who prioritize fragrance. Concurrently, Henkel's Snuggle, boosted by a 16% concentration increase in February 2025, not only cuts packaging waste but also resonates with eco-conscious buyers. Canada and Mexico together account for 12 to 15% of the region's volume. Notably, Mexico's urbanization and modernized retail landscape are propelling double-digit growth in organized trade channels. An August 2024 update from the U.S. Environmental Protection Agency on the Safer Choice Standard, introducing DCC 13 performance benchmarks and sidelining certain surfactants, imposes a 6 to 8% compliance cost hike on mid-tier producers, inadvertently consolidating market share among larger multinationals.

Asia-Pacific, charting a 7.29% CAGR through 2031, is witnessing a surge in washing machine penetration. Urban China hit 95% by 2024, urban India reached 45%, and urban Indonesia stands at 60%, according to national statistics. In a strategic move, Unilever teamed up with Alibaba in 2024, embedding Comfort SKUs into washing machine starter kits, effectively introducing the brand to 1.2 million Chinese households. Japan's premium segment, leveraging micro encapsulation technology for enduring fragrances, commands retail prices 30 to 40% above regional norms. In contrast, Southeast Asian nations like Thailand, Vietnam, and Indonesia lean towards value packs and sachet formats, easing entry for novices. Thanks to World Bank-backed rural electrification initiatives, 80 million more households in India and Indonesia will gain grid access by 2026, igniting latent demand for appliances as financing options emerge.

Europe, while grappling with mature market saturation and stringent regulations, stands at the forefront of sustainability. The European Commission's November 2025 stance on the revised Detergents Regulation (COM(2023)217) introduces mandates like digital product passports and stricter biodegradability criteria. These changes push manufacturers to either reformulate or lose access to a market of 450 million consumers. Unilever's Comfort Botanicals, debuting in May 2024 with 95% biodegradable components, clinched both the EU Ecolabel and Safer Choice certifications, a feat accomplished by a mere 12% of global softener SKUs. Germany, the UK, and France dominate, making up half of the region's volume, with private labels capturing 28% of discount chain sales. Insights from A.I.S.E.'s 2025 survey highlight that 49% of Europeans value recyclable packaging, 48% prioritize low temperature efficacy, and 62% regard official ecolabels as crucial, steering product development. South America witnesses urbanization surges in Brazil, Argentina, and Colombia, with organized retail penetration climbing from 55% in 2020 to a projected 68% by 2026. Meanwhile, the Middle East and Africa, buoyed by premium growth in Saudi Arabia and the UAE, grapple with a counterfeit challenge, seizing 15 to 20% of market volume. Yet, Procter & Gamble's 2024 blockchain-driven QR code initiative on Downy bottles seeks to mend trust and validate premium pricing.

Regulatory Landscape

Regulatory oversight is tightening around surfactant safety, biodegradability, and product transparency, which directly affects conventional cationic chemistries used across the category. In the European Union, Regulation (EU) 2026/405 on detergents and surfactants entered into force on March 22, 2026, expanding coverage to areas such as refill and online sales and strengthening digital labeling expectations, with full applicability scheduled for September 23, 2029. The EU direction reinforces the shift toward verifiable ingredient traceability and biodegradability data at the SKU level, consistent with the market emphasis on digital product passports.

In North America, the US Environmental Protection Agency continues to use TSCA tools, including Significant New Use Rules (SNURs), to control the introduction and change of use of chemical substances relevant to household and cleaning applications, which can include ingredients used in fabric softeners. Voluntary standards used by retailers and institutional buyers are also evolving: Green Seal issued clarifying revisions to its GS-48 Laundry Care Products standard on April 3, 2026, while ASTM updated its Standard Guide for Evaluating Fabric Softeners (ASTM D5237-14) on January 17, 2024, maintaining common performance-evaluation practices that underpin substantiation for softness, static control, and related claims.

Competitive Landscape

In the fabric softeners and conditioners market, a concentration score indicates a moderate level of consolidation. Here, multinational giants like Procter & Gamble, Unilever, Henkel, Kao, and Reckitt Benckiser share the stage with regional specialists and eco innovators such as Blueland and Koparo Clean. These established players utilize intellectual property to safeguard their premium offerings. For instance, Procter & Gamble's U.S. patent (US11939554B2), granted in March 2024, focuses on cationic polymer silicone blends that enhance wrinkle reduction and static control. Similarly, Henkel's 2024 European Patent Office grant (EP3976756B1) showcases biodegradable ester quat compositions, highlighting the potential of green chemistry to rival traditional methods while adhering to regulatory standards. Strategic moves underscore this concentration trend: Henkel's February 2025 launch of a denser Snuggle formula, which is 16% more concentrated, not only reduces packaging waste but also cuts logistics costs. Meanwhile, Unilever's GBP 9 million (USD 11.3 million) campaign for Comfort Botanicals, driven by influencer partnerships, garnered an impressive 450 million impressions.

There is a notable focus on hypoallergenic formulations for kids, an area where the costs of clinical validation deter private label competition, and innovative zero plastic refill systems. These refill systems resonate with 49% of European consumers, as highlighted by A.I.S.E.'s 2025 survey, who prioritize recyclable packaging. New entrants are leveraging direct-to-consumer strategies and subscription models, sidestepping the challenges of traditional shelf space negotiations. Blueland, fresh off a USD 20 million Series B funding round in July 2024, boasts customer acquisition costs that are 40% lower than the industry norm, thanks to its savvy use of user-generated content and algorithmic recommendations. Their innovative refillable tablet system not only eliminates single-use plastics but also commands a premium of 25 to 30%. Unilever is pushing the boundaries of technology; their 2024 WIPO patent on microencapsulated fragrance release systems ensures scent molecules endure wash cycles and activate during wear, allowing them to price their products at a 20 to 30% premium over standard commodity liquids.

Regional players like LG H&H in South Korea, Godrej Consumer Products in India, and Lion Corporation in Japan are fortifying their home markets with localized fragrances and value packs. However, they are grappling with margin pressures due to e-commerce platform promotions that squeeze pricing power. By 2025, private label products captured 22% of European supermarket sales and 18% in North American discount chains. This surge has compelled branded players to carve out distinctions through sustainability certifications and clinical claims, justifying their premium pricing.

Fabric Softeners And Conditioners Industry Leaders

The Procter and Gamble Company

Unilever PLC

Henkel AG & Co. KGaA

Church & Dwight Co., Inc.

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-led reformulation and digital compliance create openings for suppliers and brand owners that can document biodegradability, responsible sourcing, and safer chemistry while holding performance constant in concentrated liquids. The EU move to Regulation (EU) 2026/405, in force from March 2026 with a staged transition to September 2029 applicability, increases demand for digital-ready product data, traceability, and compliant labeling for both online and refill pathways. Portfolios already structured around recognized criteria, such as alignment with EU Ecolabel and EPA Safer Choice referenced in the category context, should be better positioned, and it also supports service demand around testing, certification, and data management for mid-tier and private-label manufacturers.

Product and business-model opportunities are also forming around water and waste reduction, where packaging-light formats and concentrated dosing fit appliance-driven metering and retailer sustainability requirements. Separately from formulation, academic work published in March 2026 on self-cleaning textile coatings (using polyelectrolyte multilayers) reported detergent-free laundering with large per-cycle reductions in resource use, pointing to a long-horizon route for innovation that could shift attention toward additive products that complement new fabric finishes rather than relying on high-deposition softening actives. In parallel, circularity programs in adjacent home-care materials, such as industrial-scale recycling collaborations for difficult plastics, reinforce momentum for refill and reduced-plastic packaging concepts already reflected in the category through refillable packaging and sheet-based conditioner formats.

Recent Industry Developments

- June 2026: Procter & Gamble introduced Downy Boutique Botanicals, expanding its fabric care lineup with in-wash scent bead boosters built around botanical-inspired fragrance profiles. The launch advances premiumization through fragrance-led differentiation and reinforces the role of adjunct products that complement concentrated liquid softeners in multi-step laundry routines.

- May 2026: Unilever completed its GBP 150 million investment at the Port Sunlight manufacturing hub in the United Kingdom, upgrading Home Care production lines for Persil, Comfort, and Surf and opening a new automated distribution center. The project increases manufacturing and logistics efficiency for laundry products, improving service levels and cost-to-serve for high-volume formats such as concentrated liquids.

- April 2026: Henkel relaunched its Purex laundry brand with reformulated concentrated liquid formulas and updated, nature-inspired fragrances. The refresh tracks the market shift toward concentrated formats and fragrance performance as a key purchase driver, while also creating room for claims tied to dosing efficiency and packaging reduction.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the retail and institutional sales value generated from fabric softeners and fabric conditioners used during laundry to improve feel, softness, scent, and static control across common fabric types.

Scope exclusions: We exclude laundry detergents, stain removers, bleach and bluing agents, dry-cleaning chemicals, and textile finishing chemicals used at the fiber or mill stage.

Segmentation Overview

- By Product Type

- Liquid

- Dryer Sheets

- Others

- By Nature

- Conventional

- Organic

- By End-User

- Adults

- Kids

- By Distribution Channels

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building a fact base on household care consumption and trade flows, because those signals help keep the size tied to real demand. We referred to public sources such as UN Comtrade for import and export patterns, the World Bank and OECD for macro and consumer indicators, and the US Bureau of Labor Statistics for inflation and category price movement. Standards and ingredient context were also checked through sources such as the US Environmental Protection Agency and the European Chemicals Agency, mainly to understand how product shifts can affect volumes and pricing.

To connect the market to supplier reality, we reviewed company annual reports, investor presentations, and product disclosures, followed by reported channel developments from large retailer websites and reputed press coverage. For structured cross-checks, we also used paid subscriptions that support company financials and news discovery, along with shipment-level import and export data where relevant for major producing and consuming countries. The sources listed above are illustrative, and many other public and paid references were used for data collection, validation, and clarifying open questions.

Primary Interviews and Surveys

Primary work was used to confirm what is actually selling by form and channel, and to pressure-test price ladders across economy to premium tiers. We spoke with a mix of manufacturers, distributors, category managers, and downstream buyers across APAC, EMEA, and the Americas so that regional mix, promotion intensity, and pack-size choices were reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | APAC: 47% |

| Mid tier: 53% | Functional/Unit leaders: 39% | EMEA: 29% |

| Smaller Players: 16% | Managers: 45% | Americas: 24% |

Market-Sizing & Forecasting

Our sizing uses a top-down approach where household counts, laundry frequency proxies, and per-wash or per-household usage assumptions are converted into a demand pool, which is then translated into value using country-level pricing and product mix. To keep it practical, results are corroborated with selective bottom-up approximations such as sampled brand and pack pricing across key channels, supplier revenue exposure checks, and distributor feedback on volume movement, which are then used to adjust totals where gaps show up.

Inputs in the model include urbanization and household formation, penetration of washing machines and dryers, average pack sizes and dosage guidance, promotion intensity that shifts effective pricing, and mix shifts between liquid formats and dryer sheets. In markets where organic or premium share is rising, the price curve is updated separately so the value growth is not overstated by volume alone. Forecasting relies mainly on scenario analysis supported by expert expectations for category penetration, price inflation, and channel expansion, followed by smoothing to avoid year-to-year jumps that do not match observed retail behavior. Where interview feedback indicates limited visibility on informal channels, we handle the gap by using conservative penetration and cross-checking with trade and price signals before finalizing the split.

Data Validation & Update Cycle

Validation is done through consistency checks across regions, segment shares, and implied per-capita consumption so the totals do not drift away from real-world usage patterns. If a country shows unusual value growth, the driver is traced back to one or two explainers such as inflation, pack-size changes, or a channel mix shift, and then the assumption is rechecked with follow-up calls.

Before sign-off, the model and assumptions go through a multi-step analyst review so calculation errors, unit mismatches, and currency timing issues are caught early. The study is refreshed annually, and interim updates are triggered when material events occur, such as sharp cost inflation, regulatory changes affecting formulations, or major channel disruptions. Right before delivery, a final pass is completed so clients receive an updated view aligned to the latest available public data and field inputs.

Mordor Intelligence's Fabric Softeners and Conditioners Market Size Compared With Other Published Estimates

Published market sizes for fabric softeners and conditioners can differ even when the topic label looks the same, because the underlying counting rules are not always aligned. The biggest drivers tend to be what formats are included, whether household-only demand is mixed with institutional volumes, how pricing is normalized across countries, and how frequently assumptions are refreshed.

Some published figures widen the scope into adjacent laundry care items or include broader fragrance and fabric-refresh categories in the same value pool. In Mordor Intelligence, the total is kept limited to fabric softeners and conditioners by form, and it is only counted when it is used as a distinct laundry add-on product sold through defined retail and distributor channels.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.48 B (2026) | |

| Global Consultancy A | USD 15.01 B (2024) | Uses an earlier base year and a different forecast window, and it also applies a broader product list in some sections (for example, adding dryer bars and similar variants), which can shift mix and pricing assumptions versus a form-led view. |

| Industry Publisher B | USD 12.44 B (2025) | Frames the market as fabric softeners and may treat conditioners and format overlap differently across end users, and its year and geography weighting can pull totals down when premium mix and channel pricing are not updated with the same cadence. |

The spread in the table mainly comes from timing, product inclusion choices, and how price progression is carried forward across countries. When scope is kept specific and variables like penetration, pack-size behavior, and effective pricing are checked with field feedback, the resulting market value becomes easier to trace and repeat year after year with the same steps and inputs.

Key Questions Answered in the Report

What is the projected value of the fabric softeners and conditioners market by 2031?

The market is forecast to reach USD 22.85 billion by 2031.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to post a 7.29% CAGR, the highest among all regions.

Which product format currently dominates sales?

Concentrated liquid softeners held 87.75% of 2025 revenue, far surpassing other formats.

Why are organic variants gaining ground?

Retailer eco-label mandates and consumer preference for biodegradable formulas are driving a 7.41% CAGR for organic softeners.

Page last updated on: