Cardiology Electrodes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

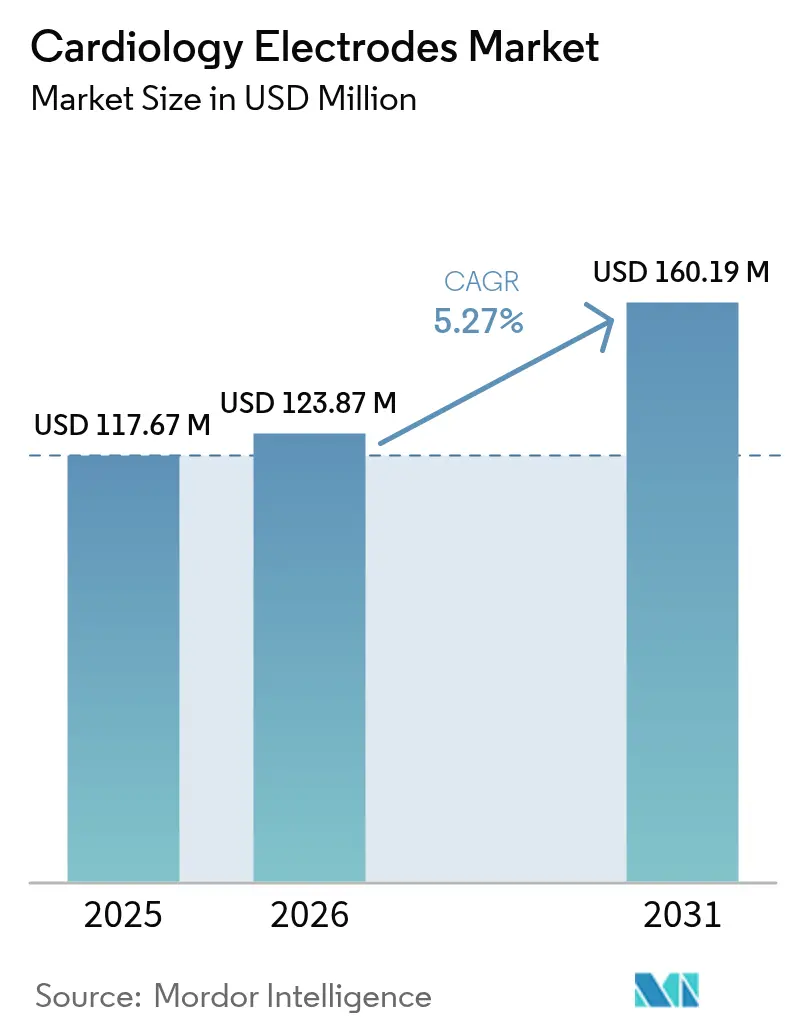

| Market Size (2026) | USD 123.87 Million |

| Market Size (2031) | USD 160.19 Million |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

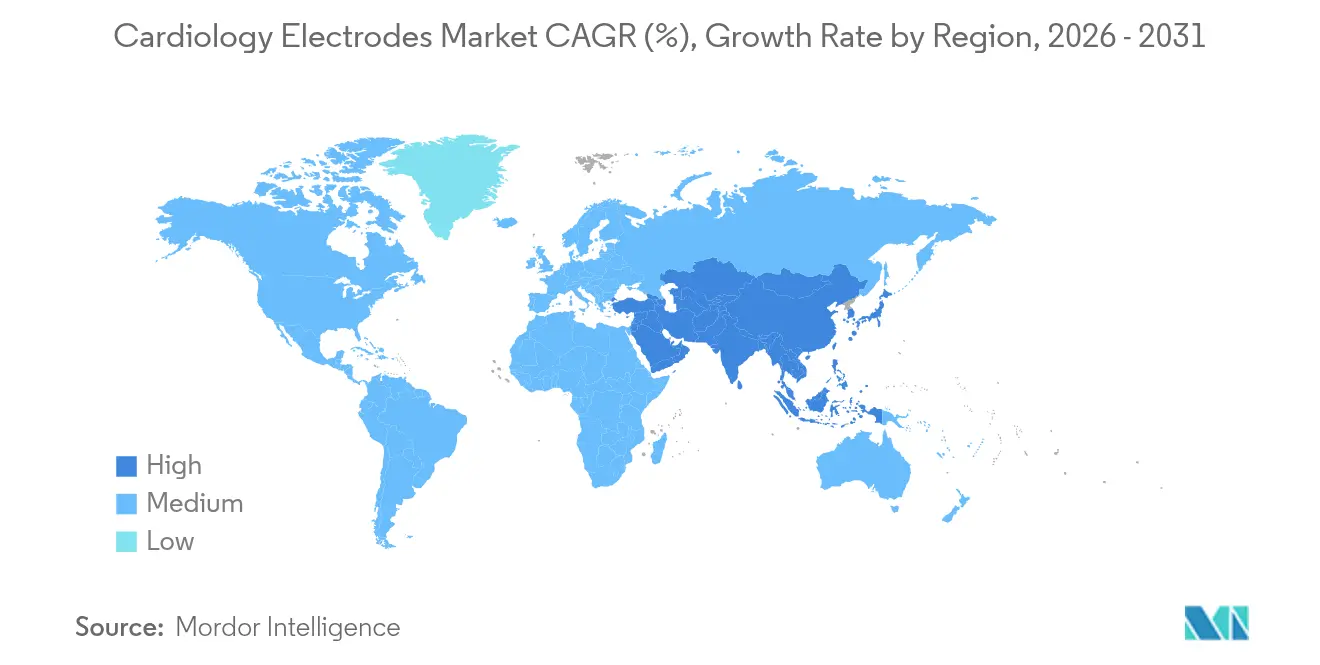

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiology Electrodes Market Analysis by Mordor Intelligence

Cardiology Electrodes market size in 2026 is estimated at USD 123.87 million, growing from 2025 value of USD 117.67 million with 2031 projections showing USD 160.19 million, growing at 5.27% CAGR over 2026-2031.

Robust demand stems from the convergence of telehealth adoption, artificial-intelligence-enabled diagnostics, and hospitals’ cost-containment mandates. Manufacturers focusing on disposable electrodes benefit as infection-control protocols tighten, while suppliers of dry polymer designs gain momentum thanks to rising patient comfort requirements. Reimbursement expansions for home cardiac monitoring further widen addressable patient pools, and printed electronics continue to cut production costs, allowing broader geographic reach. Competitive intensity remains moderate because established brands rely on regulatory expertise and materials science know-how to defend positions, yet price pressure from low-cost Asian producers pushes incumbents toward product differentiation.

Key Report Takeaways

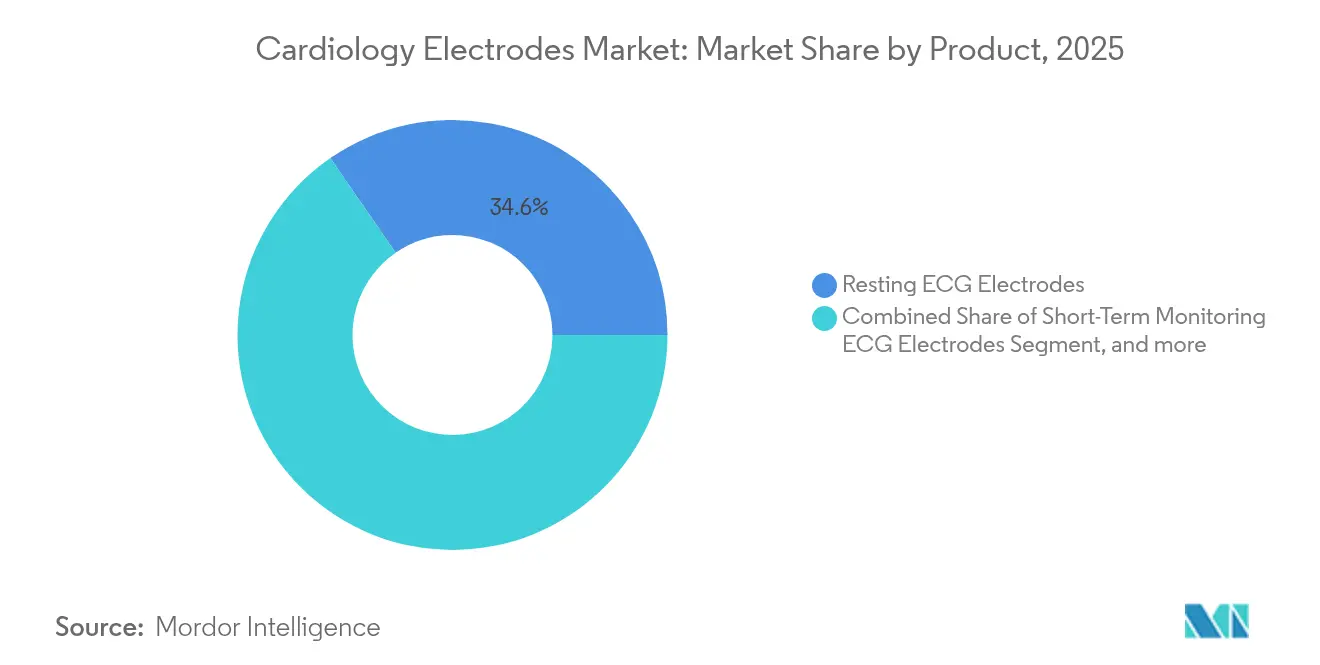

- By product, resting ECG electrodes led with 34.62% of cardiology electrodes market share in 2025, while long-term monitoring ECG electrodes are forecast to advance at an 11.02% CAGR through 2031.

- By usability, disposable medical electrodes captured 60.72% of the cardiology electrodes market size in 2025 and are projected to expand at a 12.35% CAGR to 2031.

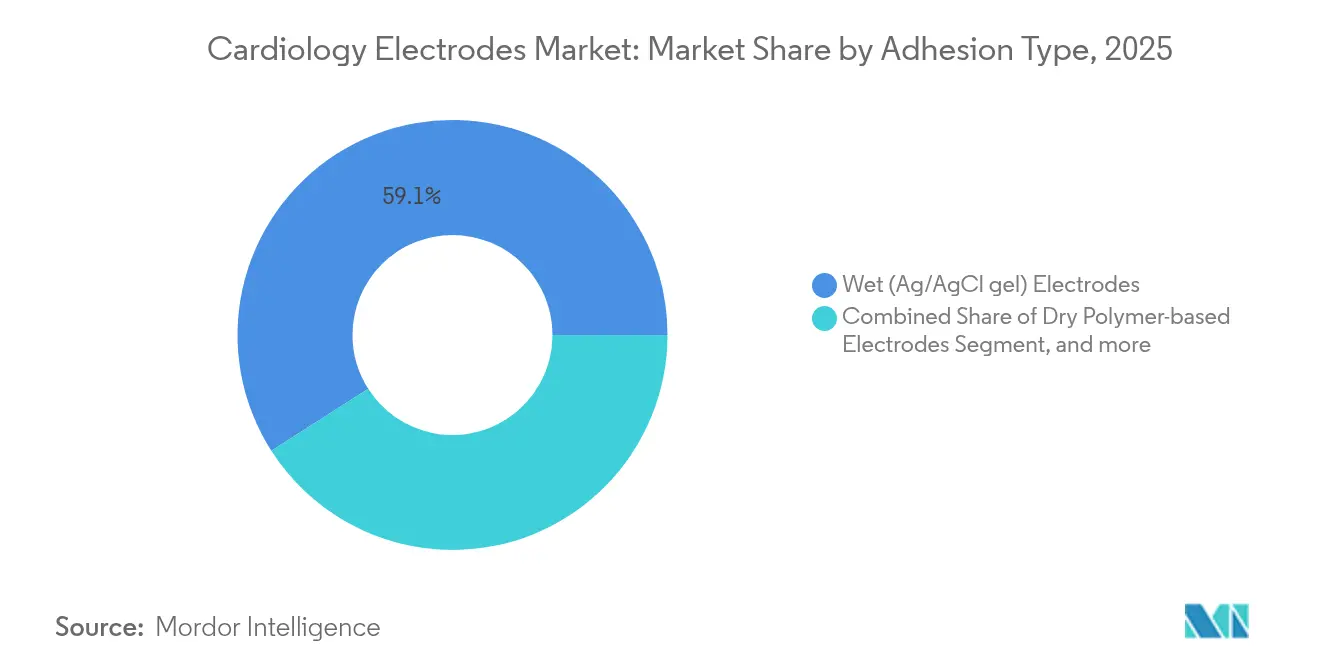

- By adhesion type, traditional wet Ag/AgCl gel electrodes held 59.05% revenue share in 2025; dry polymer-based electrodes are poised to post the highest CAGR at 12.95% between 2026 and 2031.

- By end user, hospitals and cardiac centers accounted for 40.74% share of the cardiology electrodes market size in 2025, while ambulatory surgical centers are expected to record a 14.21% CAGR through 2031.

- By geography, North America commanded 39.02% of global revenue in 2025; Asia-Pacific is projected to be the fastest-growing region with a 11.67% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiology Electrodes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of CVDs | +1.8% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Growing demand for single-use electrodes | +1.2% | Global, strong in APAC and North America | Medium term (2-4 years) |

| Home-based cardiac monitoring via telehealth | +0.9% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Printed and flexible-electronics cost cuts | +0.7% | APAC core, global spill-over | Medium term (2-4 years) |

| Miniaturised dry-contact micro-arrays | +0.5% | Global, led by North America and Europe | Long term (≥ 4 years) |

| AI and machine-learning cardiac diagnostics | +0.3% | North America and EU, early urban APAC adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of CVDs

Cardiovascular disease prevalence keeps electrode demand resilient. The American Heart Association projects hypertension rates to climb to 61.0% and diabetes to 26.8% by 2050, trends that elevate the need for long-term monitoring solutions.[1]American Heart Association, “Heart Disease and Stroke Statistics 2024 Update,” heart.org Productivity losses linked to cardiovascular conditions are also expected to swell, encouraging investment in early detection technologies that rely on high-performance ECG interfaces. Asia faces a sharper rise as lifestyle shifts interact with population aging, prompting global suppliers to localize production. Because cardiac monitoring is essential rather than discretionary, device orders remain stable even during economic slowdowns. Clinical guidelines that emphasize preventive cardiology reinforce continuous monitoring protocols, cementing electrodes as routine consumables.

Growing Demand for Single-Use Electrodes

Hospitals have institutionalized disposable electrodes after the COVID-19 pandemic highlighted infection-control gaps. Studies published in the British Journal of Nursing documented meaningful reductions in surgical-site infections when single-use ECG leads were employed.[2]British Journal of Nursing, “Single-Use ECG Leads Reduce Surgical Site Infections,” bjn.com Beyond infection mitigation, disposables cut sterilization labor and liability costs, often proving economical on a total-cost-of-ownership basis. Suppliers that can certify products in multiple jurisdictions enjoy scaling advantages, while newer biodegradable substrates such as nanocellulose ECG patches position vendors to satisfy sustainability mandates. The shift from reusable to disposable formats is most pronounced in North America and is rapidly taking hold in major Asian health-systems as capacity for high-volume manufacturing grows.

Home-Based Cardiac Monitoring Boom via Telehealth

Remote ECG monitoring soared during pandemic restrictions. A Journal of Arrhythmia study recorded patient satisfaction rates of 87% and trimmed average clinic time from 168.2 minutes to 13 minutes.[3]Journal of Arrhythmia, “Patient Satisfaction with Remote Monitoring During Pandemic,” j-arrhythmia.com This adoption sends electrode performance requirements in a new direction: patches must remain effective for several days, be simple for self-application, and avoid messy gels. Dry polymer and textile designs satisfy these needs, improving adherence and user comfort. Expanded reimbursement by Medicare and private insurers removes financial obstacles, and insurers are increasingly the core purchasing decision-makers. In parallel, digital health platforms integrate AI analytics that flag arrhythmias with sensitivities above 95%, boosting clinician trust in home data streams.

Printed & Flexible-Electronics Cost Reductions

Screen-printing and roll-to-roll processing have cut material and labor costs while maintaining signal integrity. Researchers demonstrated fully printed wet ECG electrodes with performance on par with conventional Ag/AgCl using significantly less silver. Flexographic lines also support mass-production volumes essential for emerging markets. APAC vendors, already advantaged by labor costs, capitalize on printed-electronics gains to undercut Western pricing without sacrificing quality. Integration of conductive polymers and nanofillers further refines impedance characteristics, letting manufacturers pitch value-based features such as lower motion artifacts. As cost hurdles fall, the cardiology electrodes market finds new customers in lower-tier hospitals and rural clinics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skin irritation and allergic dermatitis | -0.8% | Global, severe in sensitive populations | Medium term (2-4 years) |

| Price pressure from low-cost Asian OEMs | -0.6% | Global, most intense in cost-sensitive markets | Short term (≤ 2 years) |

| Environmental disposal rules on Ag/AgCl | -0.4% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Signal-quality drift in long-term wearables | -0.3% | Global, critical in ambulatory and home-care settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skin Irritation & Allergic-Contact Dermatitis

Case studies in the journal Contact Dermatitis highlight patients reacting to acrylic acid impurities and methacrylates in electrode hydrogels. Such reactions discourage extended monitoring, especially among older adults and neonates. Manufacturers respond by formulating hypoallergenic hydrogels, adopting textile substrates, or shifting toward dry micro-needle arrays. However, alternative designs may raise costs or complicate application, limiting rapid replacement of legacy products. Regulatory agencies now scrutinize labeling of potential allergens, increasing documentation burdens.

Price Pressure from Low-Cost Asian OEMs

Large-scale factories in China, Malaysia, and Vietnam leverage economies of scale and proximity to printed-electronics supply chains to offer electrodes at steep discounts. Hospital procurement teams facing budget caps often rank cost above brand loyalty, putting margin pressure on incumbents. Suppliers defend share through advanced material science, faster regulatory approvals, and integrated monitoring ecosystems that lock buyers into higher-level services. Over time, consolidation is likely, as smaller domestic players find it hard to meet quality and compliance thresholds while matching low prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Long-Term Monitoring Drives Innovation

Long-term monitoring ECG electrodes opened 2026 with a smaller base but are projected to post an 11.02% CAGR, well above the overall cardiology electrodes market. That trajectory reflects payer support for continuous surveillance programs intended to catch asymptomatic arrhythmias early. Premium revenues accrue to vendors offering breathable substrates and low-motion-artifact designs. Resting ECG electrodes still represent 34.62% of cardiology electrodes market share, owing to their ubiquity in emergency departments and routine checkups. Yet growth in that mature segment is modest because device replacement cycles are slow in developed nations.

Commercial deployment of multi-sensor Holter units illustrates the product transition. Recent studies in Sensors journal show that advanced Holters with Bluetooth Low Energy streamed high-resolution ECG and accelerometer data simultaneously, enhancing diagnostic yield. Motion-robust electrodes enable these devices to remain accurate during daily activities, unlocking higher reimbursements. Neonatal and pediatric electrodes form a niche requiring ultra-gentle adhesives and miniaturized snap connectors. Emerging biodegradable variants, currently in pilot trials, promise environmentally neutral disposal, a feature attracting European clinics prioritizing sustainability.

By Usability: Disposables Dominate Growth Trajectory

Disposable electrodes accounted for 60.72% of cardiology electrodes market size in 2025 and will outpace reusable formats through 2031. Infection-prevention protocols drive procurement, especially in operating rooms and high-turnover wards. Cost analysis that factors cleaning labor, autoclave energy, and risk of cross-contamination often favors single-use options even when unit prices are higher. DuPont’s Liveo Soft Skin Conductive Tape exemplifies innovation, keeping impedance stable for seven days without hydrogel slippage. Such endurance expands disposables into ambulatory monitoring use-cases once dominated by reusable pads.

Reusable electrodes hold certain cost advantages in long-stay facilities and home environments, where the same patient wears the device for months. Caregivers appreciate lower waste volumes and the option to swap cables instead of full assemblies. Nevertheless, reimbursement policies increasingly bundle electrode costs into episode-of-care payments, encouraging providers to offload sterilization chores onto vendors through disposables.

By Adhesion Type: Dry Technologies Challenge Traditional Dominance

Wet Ag/AgCl gel pads delivered 59.05% of global revenue in 2025 because clinicians trust decades of signal-quality evidence. Yet patient feedback often cites discomfort, skin maceration, and residue cleanup. Dry polymer electrodes log a 12.95% CAGR by mitigating these complaints. Comparative tests published on ScienceDirect demonstrated that embroidered textile patches achieved nearly identical QRS amplitude yet boosted comfort ratings [SCiencedirect.com]. When combined with flexible electronics, dry platforms tolerate sweat and movement, ideal for sports cardiology.

Hydrogel-less micro-needle electrodes enter the scene with unprecedented low contact impedance achieved without skin prep. Current production costs limit volume adoption, but roll-to-roll micro-molding lines promise scalability. Capacitive coupling designs, meanwhile, flirt with the prospect of measuring ECG through clothing, a future that could redefine electrode semantics entirely. For now, procurement teams weigh the trade-off between proven gel reliability and emerging dry comfort gains.

By End User: Ambulatory Centers Lead Growth Acceleration

Hospitals and cardiac centers comprised 40.74% of global revenue in 2025 because they remain the first point of advanced cardiac care. Their purchasing power secures bulk contracts and drives specification standards across a region. However, ambulatory surgical centers are set to grow at 14.21% CAGR as procedures migrate to outpatient settings for cost efficiency. These centers favor lightweight electrode kits that pair seamlessly with portable monitors, allowing quick patient turnover.

Home-care and remote-patient-monitoring providers represent the next frontier. Insurer reimbursement for RPM codes, alongside patient preference to avoid hospital visits, pushes volume to the consumer channel. Manufacturers respond with packaging tailored for self-application, complete with QR-code video instructions and recycling envelopes. Diagnostic laboratories hold modest but steady share, buying specialized electrodes for stress-test treadmills and imaging-triggered ECG gating.

Geography Analysis

North America owned 39.02% of global revenue in 2025 thanks to insurance coverage that funds remote monitoring, a stringent FDA framework assuring device efficacy, and early consumer adoption of smartwatch-linked ECG. Integrated delivery networks commonly bundle electrodes into value-based care contracts, locking vendors into multi-year supply deals. Collaborations such as the Medtronic and Philips partnership demonstrate how platform integration strengthens competitive moats.

Europe maintains steady expansion, sustained by aging demographics and stringent Medical Device Regulation that rewards companies with proven quality systems. Germany commands high per-capita expenditure on cardiac care, while France and Italy increasingly emphasize environmentally benign disposables. United Kingdom hospitals under the NHS favor single-use electrodes to streamline infection-control compliance.

Asia-Pacific is the fastest riser at a 11.67% CAGR. China’s hospital modernization and telehealth pilot reimbursement stimulate demand volumes unmatched elsewhere. Japan, already proficient in remote monitoring, adopts premium dry-contact solutions driven by patient comfort preferences. India’s burgeoning middle class fuels double-digit growth in urban private hospitals, although cost sensitivity remains paramount in public facilities. Regional production clusters in Guangdong and Penang supply both domestic and export markets, shrinking lead times.

Middle East and Africa along with South America are nascent but accelerating. Gulf Cooperation Council states allocate oil revenues toward cardiac centers outfitted with Western-brand electrodes, while Brazilian device regulators streamline approvals to reduce import costs. Vendors entering these zones often partner with local distributors to navigate diverse procurement policies.

Competitive Landscape

The cardiology electrodes market is moderately fragmented. Global leaders such as 3M Company, Cardinal Health, Koninklijke Philips, Ambu A/S, and Nihon Kohden command significant yet not dominant shares, each excelling in different subsegments. These incumbents invest heavily in R&D to differentiate through hydrogel chemistry, printed-electronics accuracy, and integrated data platforms. Regulatory acumen presents a key barrier; lengthy 510(k) pipelines deter smaller challengers.

Price competition intensifies for commodity resting ECG pads where Asian OEMs undercut Western brands. In response, incumbents pursue vertical integration, controlling silver-ink supply or adhesive formulation to lower costs without eroding quality. Several players focus on sustainability, developing biodegradable substrates to meet European waste directives.

Strategic collaboration characterizes the high-growth AI monitoring niche. Device makers sign exclusivity deals with software analytics startups to bundle electrodes with cloud interpretation services. Mergers and acquisitions also surface as firms seek scale economies amid cost pressures. Meanwhile, new entrants exploring capacitive and camera-based heart-rate sensors threaten long-term electrode demand but face hurdles in clinical validation.

Cardiology Electrodes Industry Leaders

Advin Health Care

CONMED

3M

Cardinal Health

Koninklijke Philips

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Medtronic announced a strategic partnership with Philips to expand access to patient monitoring technology, integrating Medtronic's next-generation technologies including Nellcor pulse oximetry and Microstream capnography into Philips' monitoring solutions to enhance comprehensive cardiac care delivery.

- June 2025: Anumana and InfoBionic.Ai announced collaboration to advance AI-powered remote cardiac telemetry technology, combining Anumana's FDA-cleared ECG-AI algorithms with InfoBionic.Ai's MoMe ARC platform for early detection of cardiac diseases including low ejection fraction.

- April 2025: HeartBeam and AccurKardia integrated advanced ECG analysis capabilities into their cardiac monitoring platform, enhancing diagnostic accuracy and enabling more timely clinical interventions through improved ECG data processing algorithms.

- April 2024: BIOTRONIK introduced the BIOMONITOR IV insertable cardiac monitor featuring artificial intelligence at EHRA Congress 2024, incorporating SmartECG technology that reduces false positive detections by 86% while maintaining 98% of clinically relevant episodes.

Global Cardiology Electrodes Market Report Scope

As per the report's scope, cardiac electrodes are small, plastic patches that stick to the skin and are placed at certain spots on the chest, arms, and legs. The electrodes are connected to an ECG machine by lead wires. The heart's electrical activity is then measured, interpreted, and printed out. The Cardiology Electrodes Market is Segmented by Product (Resting ECG Electrodes, Short-term Monitoring ECG Electrodes, Long-Term Monitoring ECG Electrodes, and Other Products), By Usability ( Disposable Medical Electrodes, Reusable Medical Electrodes), Adhesion Type (Wet Electrodes, Dry Electrodes, and Other Adhesion Types), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the abovementioned segments.

| Resting ECG Electrodes |

| Short-Term Monitoring ECG Electrodes |

| Long-Term Monitoring ECG Electrodes |

| Stress-Test / Exercise & Holter Electrodes |

| Neonatal & Pediatric ECG Electrodes |

| Other Products |

| Disposable Medical Electrodes |

| Reusable Medical Electrodes |

| Wet (Ag/AgCl gel) Electrodes |

| Dry Polymer-based Electrodes |

| Hydrogel-less Micro-needle Electrodes |

| Other Adhesion Types |

| Hospitals & Cardiac Centres |

| Ambulatory Surgical Centres |

| Home Care Settings |

| Diagnostic Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Resting ECG Electrodes | |

| Short-Term Monitoring ECG Electrodes | ||

| Long-Term Monitoring ECG Electrodes | ||

| Stress-Test / Exercise & Holter Electrodes | ||

| Neonatal & Pediatric ECG Electrodes | ||

| Other Products | ||

| By Usability | Disposable Medical Electrodes | |

| Reusable Medical Electrodes | ||

| By Adhesion Type | Wet (Ag/AgCl gel) Electrodes | |

| Dry Polymer-based Electrodes | ||

| Hydrogel-less Micro-needle Electrodes | ||

| Other Adhesion Types | ||

| By End User | Hospitals & Cardiac Centres | |

| Ambulatory Surgical Centres | ||

| Home Care Settings | ||

| Diagnostic Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the cardiology electrodes market in 2026?

The cardiology electrodes market size reached USD 123.87 million in 2026 and is forecast to grow steadily through 2031.

Which product segment is growing the fastest?

Long-term monitoring ECG electrodes are projected to expand at an 11.02% CAGR, the highest among product categories.

Why are disposable electrodes gaining share?

Hospitals prefer single-use electrodes to reduce infection risk and avoid sterilization costs, pushing disposables to 60.72% share in 2025.

Which region will see the highest growth to 2031?

Asia-Pacific is expected to record a 11.67% CAGR, propelled by healthcare infrastructure expansion and rising cardiovascular disease incidence.

How is AI affecting electrode demand?

AI-enabled cardiac diagnostics require reliable ECG inputs, driving demand for high-quality electrodes that can capture accurate signals even in home settings.

Who are the leading vendors?

Key players include 3M, Cardinal Health, Koninklijke Philips, Ambu A/S, and Nihon Kohden, each leveraging R&D and regulatory expertise to maintain competitiveness.

Page last updated on: