Executive Search Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

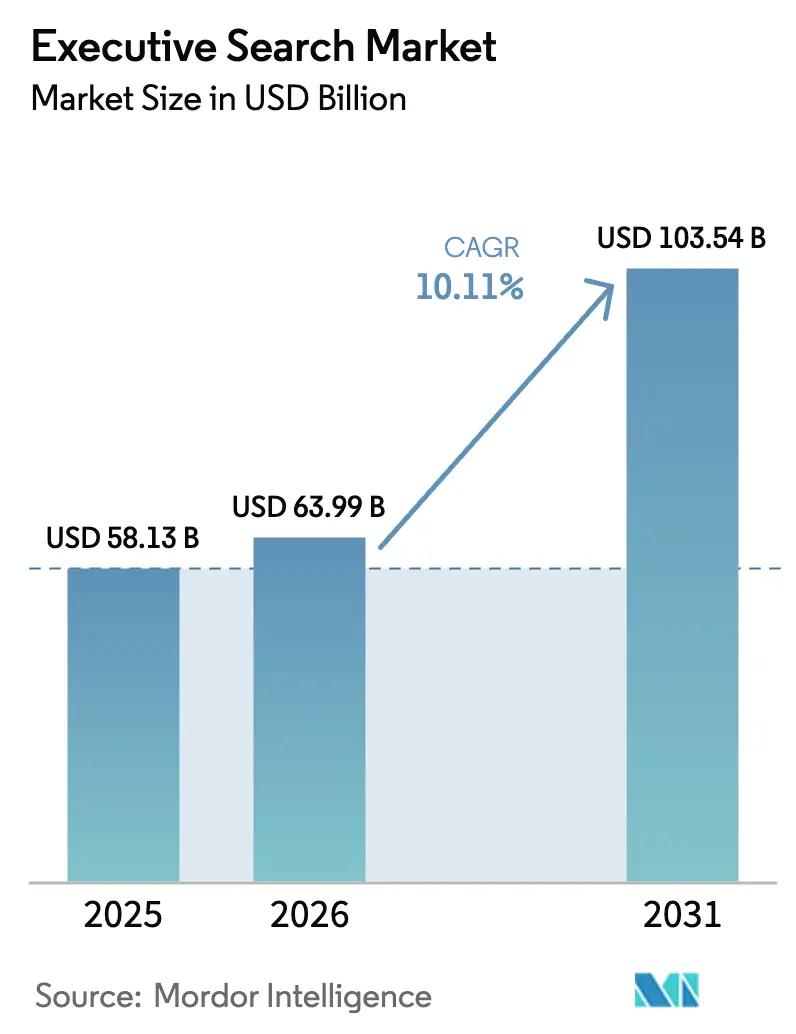

| Market Size (2026) | USD 63.99 Billion |

| Market Size (2031) | USD 103.54 Billion |

| Growth Rate (2026 - 2031) | 10.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Executive Search Market Analysis by Mordor Intelligence

The executive search market size in 2026 is estimated at USD 63.99 billion, growing from 2025 value of USD 58.13 billion with 2031 projections showing USD 103.54 billion, growing at 10.11% CAGR over 2026-2031. Robust demand for leadership talent in digital transformation, ESG compliance, and corporate governance sustains double-digit growth even as in-house talent teams expand. Specialized C-suite roles such as Chief AI and Chief Sustainability Officers shorten executive tenures and intensify search cycles, while interim leadership assignments complement permanent placements to create new revenue streams for providers. Global private equity dry powder and heightened succession activity in family-owned enterprises add structural drivers that counterbalance pricing pressure from internal recruiting functions. Regulatory frameworks around data localization and sustainability reporting reinforce barriers to entry and favor search firms with sophisticated compliance infrastructure, thereby enabling premium fee structures.

Key Report Takeawyas

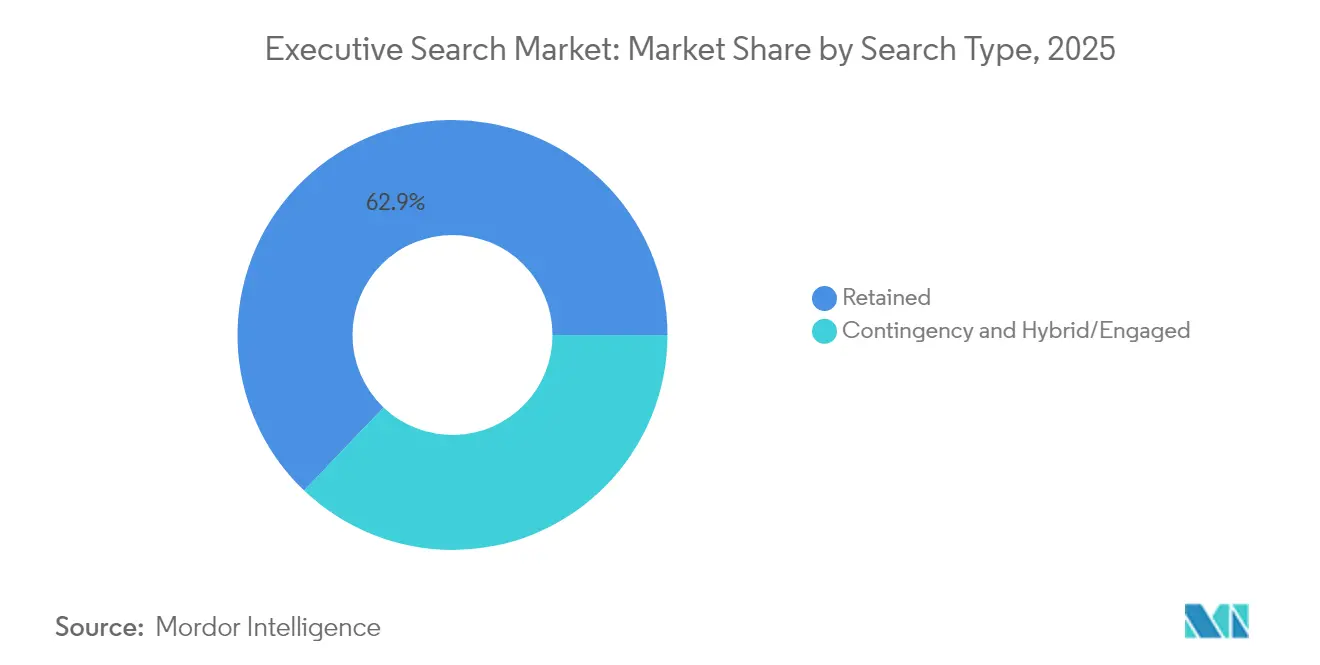

- By search type, the retained model held 62.88% of executive search market share in 2025 and hybrid approaches posted the highest projected CAGR at 11.72% through 2031.

- By function level, C-suite appointments accounted for 50.64% of the executive search market size in 2025 while Chief Digital and AI roles are advancing at an 11.03% CAGR to 2031.

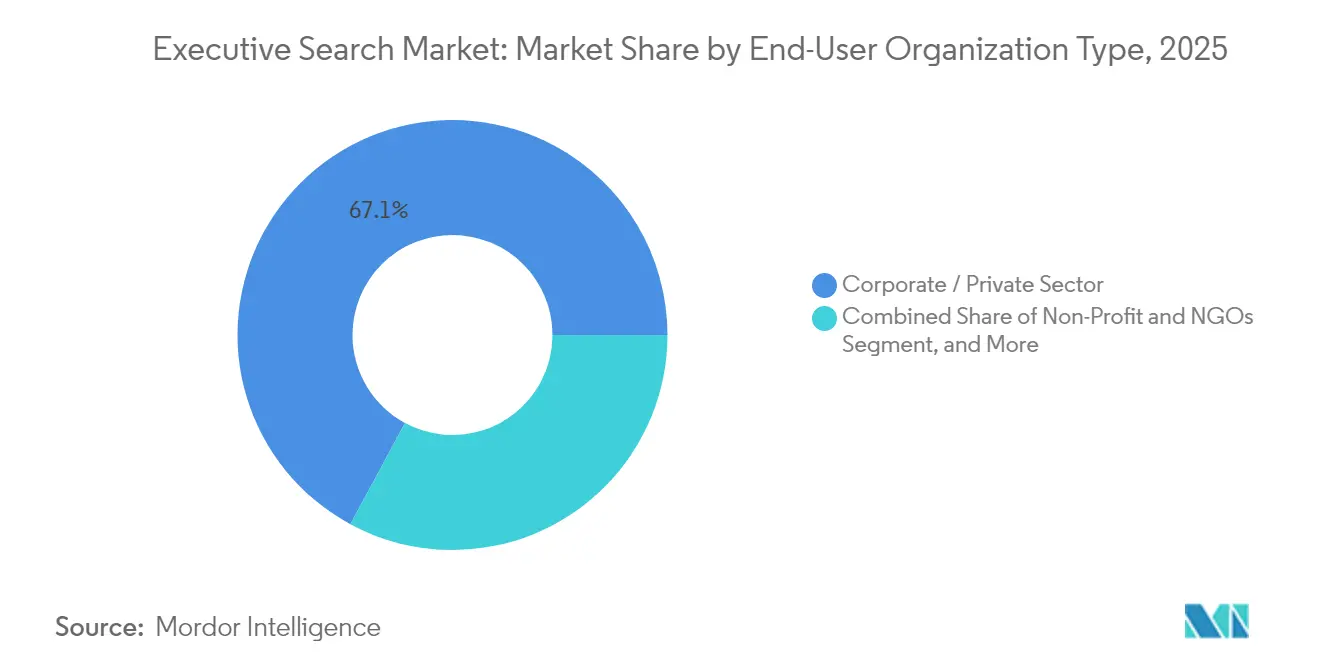

- By end-user organization type, corporate and private sector clients captured 67.12% revenue share in 2025 whereas private equity and venture-backed entities are expanding at an 11.28% CAGR through 2031.

- By industry vertical, technology and digital services commanded 27.45% of the executive search market size in 2025 and life sciences and healthcare is projected to grow at a double-digit CAGR of 10.44% through 2031.

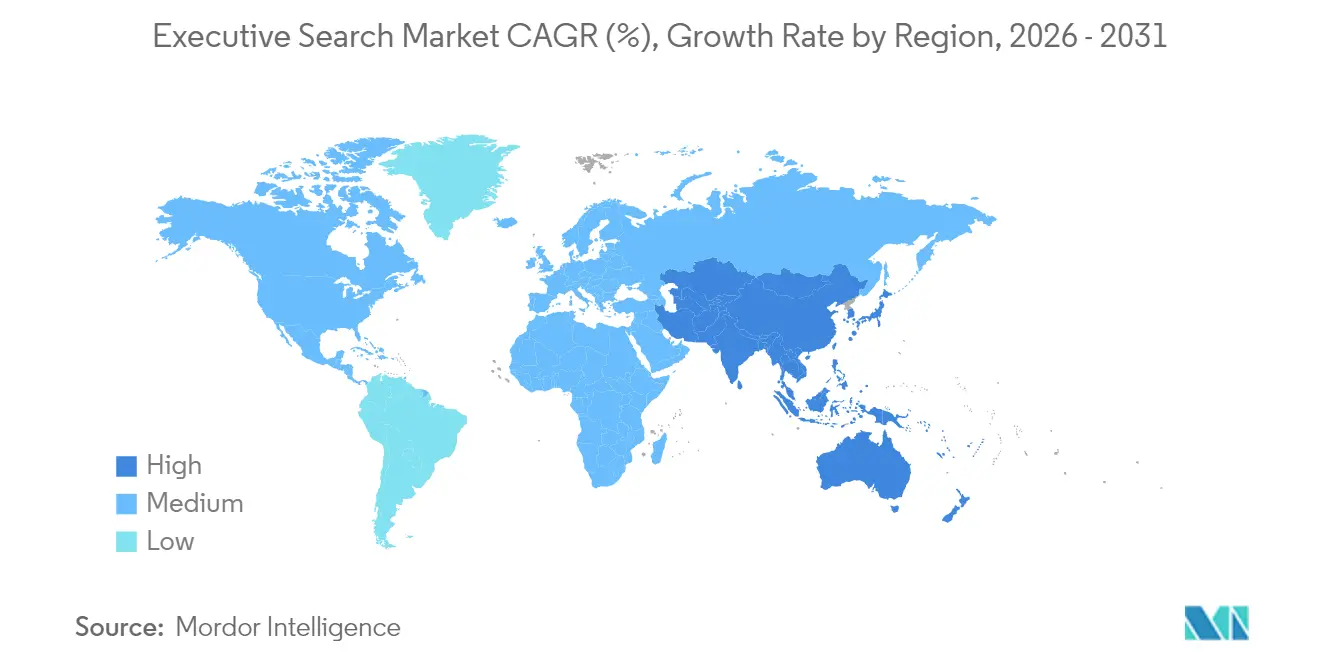

- By geography, North America led with 38.20% executive search market share in 2025 and Asia Pacific is forecast to record the fastest 10.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Executive Search Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emerging-market demand for leadership talent | +2.8% | Asia Pacific, Latin America, Middle East and Africa | Medium term (2-4 years) |

| Next-gen roles such as Chief AI and Sustainability | +3.1% | Global with focus on North America and Europe | Short term (≤2 years) |

| Digital-transformation-driven C-suite churn | +2.4% | Global | Short term (≤2 years) |

| Fractional leadership and interim CEO model | +1.6% | North America and Europe | Medium term (2-4 years) |

| ESG-mandated board searches | +1.9% | Europe, North America with APAC spillover | Long term (≥4 years) |

| Professionalization of family businesses | +1.4% | Asia Pacific, Latin America, Middle East and Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing demand for leadership talent in emerging and frontier markets

Companies in Asia Pacific, Latin America, and the Middle East and Africa accelerate professionalization as they scale beyond founder leadership and invite multinational competition. Family-owned enterprises that generate more in revenue seek external executives to manage succession complexity and globalize operations. The executive search market benefits because established firms offer local compliance expertise in regions where data privacy laws are tightening. Private equity inflows into fast-growing economies intensify the need for seasoned operators able to enact value-creation plans before exit events. Talent scarcity across frontier geographies allows retained search models to maintain premium fee structures and extended engagement timelines. Providers that combine on-the-ground networks with cross-border assessment methodologies enjoy sustainable competitive advantages.

Rise of specialized, next-gen executive roles (Chief AI, Chief Sustainability)

Artificial intelligence job titles tripled between 2022 - 2024 as organizations recognized AI governance as a C-suite imperative. Nearly half of large enterprises intend to appoint a Chief AI Officer within 12 months to mitigate algorithmic risk and unlock productivity gains. Parallel momentum surrounds Chief Sustainability Officers as ESG reporting deadlines approach, illustrated by Heidrick & Struggles expanding its Climate and Sustainability Practice in late 2024.[1]Heidrick & Struggles, “2024 Global Data, Analytics, and AI Executive Survey,” heidrick.com Scarce candidate supply elongates search cycles and supports average fee structures of 33% on first-year cash compensation for specialized mandates. Retained search firms strengthen pricing power because contingency or DIY platforms cannot replicate their curated shortlists for niche roles.

Digital-transformation-driven C-suite churn

CEO turnover reached a decades-high level in 2025 as boards replaced traditional leaders with technology-native executives who can steer innovation roadmaps. CFO churn in industrial firms mirrored the trend, with average tenure falling to 4.8 years.[2]Russell Reynolds Associates, “The Global Industrial CFO Turnover Report,” russellreynolds.com Heightened rotation boosts placement volume across the executive search market and feeds cross-functional mandates spanning digital, finance, and operations. Competition escalates because multiple enterprises pursue similar digital skill sets, compressing candidate pools. Search firms counter by integrating psychometric and AI-based assessment tools to match leadership style with transformation culture. Longer retainer periods and re-placement guarantees emerge as standard contractual terms amid volatile leadership tenures.

Fractional leadership and interim CEO model adoption

Companies unable to justify full-time C-suite packages embrace fractional executives for mission-critical projects such as market entry or restructuring. Interim CEO demand spiked 220% year-over-year in 2023, signaling board preference for flexibility during macro uncertainty. Executive search providers diversify into interim placement services that combine rapid deployment with short engagement horizons, creating annuity-like revenue when assignments roll into permanent placements. Private equity firms employ fractional leaders across portfolio companies to spread expertise and reduce compensation overhead. While engagement fees are lower than permanent searches, higher transaction volume and shorter cycle times offset revenue dilution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pricing pressure from in-house TA and RPO teams | -1.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Diversity metric compliance increasing search cycle time | -0.9% | North America and Europe, with spillover to APAC | Medium term (2-4 years) |

| AI-enabled DIY talent platforms reducing external spend | -1.2% | Global, with early adoption in North America | Medium term (2-4 years) |

| Cross-border data-privacy regulations limiting candidate pools | -0.7% | Global, with highest impact in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pricing pressure from in-house TA and RPO teams

Enterprises investing in internal recruiting report 30% to 35% cost savings when shifting mandates away from external firms. Recruitment Process Outsourcing providers expand up-market, competing for director-level and even selective C-suite searches at lower margins. Advanced internal teams leverage LinkedIn Recruiter, automated outreach, and employer branding to approach passive executives directly. Yet the executive search market retains an advantage for high-stakes placements because mis-hires at senior levels can cost USD 17,000 to USD 240,000 in downstream productivity losses. Search firms emphasize risk-mitigation and cultural alignment to justify retainers and defend pricing.

AI-enabled DIY talent platforms reducing external spend

Ninety-seven percent of large organizations now experiment with AI-based sourcing, and 58% of recruitment agencies deploy AI for screening. Time-to-fill reductions of up to 60% tempt finance leaders to divert budget from external search. In response, firms like Spencer Stuart embed proprietary algorithms through partnerships such as its 2025 alliance with Qlu to enhance discovery and assessment.[3]Spencer Stuart, “Partnership with Qlu,” spencerstuart.com Human-centered evaluation of leadership nuance and board dynamics remains a differentiator that pure-play platforms cannot replicate, particularly for confidential or succession-critical roles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Search Type: Retained Model Dominance Amid Hybrid Innovation

Retained engagements accounted for 62.88% of executive search market share in 2025, underlining persistent client preference for exclusivity when stakes are highest. The executive search market size attributed to retained searches reflected USD 36.55 billion, and hybrid models are projected to expand at 11.72% CAGR through 2031 as companies demand outcome-based pricing flexibility.

Hybrid contracts marry AI-powered candidate mapping with milestone-driven fees, reducing upfront commitment while preserving search rigor. Private equity clients favor hybrid structures to stretch budget across multiple portfolio companies, and technology improvements around remote interviewing reduce logistical costs. Contingency search remains relevant for director-level appointments but faces commoditization as internal sourcing capabilities mature.

By Function Level: C-Suite Leadership Amid AI Role Emergence

C-suite mandates comprised 50.64% of overall placements in 2025, signaling the segment’s importance to the executive search market size. Within this cadre, Chief Digital and Chief AI Officer searches are projected to grow at an 11.03% CAGR, outpacing traditional CEO and CFO roles.

Organizations prioritize technology literacy in top leadership, with 82% integrating AI responsibilities into business strategy by 2024. The surge elevates fee potential because candidate pools remain shallow. EVP and VP searches hold steady as firms build succession benches, whereas middle-management layers continue to thin under delayering strategies, pushing more responsibility to director roles.

By End-User Organization Type: Corporate Sector Stability with PE Growth

Corporate and private enterprises generated 67.12% of 2025 revenue, providing recurring engagements for leadership renewal. Private equity and venture capital clients, though a smaller base, exhibit the fastest expansion at 11.28% CAGR through 2031 as they deploy record capital and refine value-creation playbooks.

General partners favor retained or hybrid search to secure seasoned operators capable of rapid EBITDA improvement ahead of exit events. Government and NGO demand grows modestly, constrained by procurement rigor and pay compression, yet ESG overlap drives occasional crossover for sustainability experts.

By Industry Vertical: Technology Leadership with Healthcare Acceleration

Technology and digital services contributed 27.45% to the executive search market size in 2025 and will maintain a double-digit 10.44% CAGR to 2031 as cloud computing, cybersecurity, and AI adoption refresh leadership rosters continuously.

Life sciences and healthcare ascend on the back of demographic aging, regulatory scrutiny, and innovation in biopharma. Financial services stay resilient, balancing digital disruption with compliance oversight. Industrial sectors gain momentum from reshoring and sustainability mandates that demand supply-chain transformation expertise, expanding the talent pool requirements that search consultants must navigate.

Geography Analysis

North America captured 38.20% executive search market share in 2025, buoyed by a concentration of Fortune 500 headquarters, robust private equity ecosystems, and active M&A pipelines. Short CEO tenures and venture capital-backed unicorn proliferation in technology corridors like Silicon Valley and Austin sustain premium search activity. Boards intensify governance scrutiny, elevating demand for directors versed in cybersecurity and ESG oversight, further anchoring retained search engagement.

Asia Pacific is projected to record a 10.71% CAGR through 2031, reflecting economic growth, capital market maturation, and succession planning in family-owned conglomerates. It is expected that family businesses to comprise a signficiant rate of large enterprises by 2025, signaling amplified leadership professionalization requirements. Governments encourage foreign direct investment in technology, healthcare, and renewable energy, which in turn necessitates localized executive talent capable of navigating regulatory and cultural complexity.

Europe maintains steady expansion underpinned by ESG regulation. The Corporate Sustainability Reporting Directive drives board refreshment cycles for sustainability expertise, while GDPR enforcement imposes stringent data-handling protocols that elevate compliance costs for smaller challengers. Continued post-Brexit corporate restructuring in financial services sustains cross-border leadership searches centered on Paris, Frankfurt, and Amsterdam hubs. Emerging regions in South America and the Middle East and Africa register rising mandates tied to infrastructure development and digital economy investments, though geopolitical volatility tempers overall contribution.

Competitive Landscape

Global leaders such as Korn Ferry, Heidrick & Struggles, and Russell Reynolds Associates leverage scale advantages in proprietary databases, psychometric tools, and multi-service advisory to defend premium fees. Korn Ferry posted USD 668.7 million professional fee revenue in Q3 FY 2025, with executive search comprising USD 204.6 million, underscoring demand resilience. Heidrick & Struggles documented USD 283.6 million in Q1 2025 revenue, reflecting diversification across consulting and on-demand talent.

Mid-tier consolidation accelerates, evidenced by ZRG’s acquisition of Bravanti and Creative Artists Agency’s purchase of Hanold Associates in 2024. Such moves expand sector coverage and provide scale for technology investments. Boutique firms remain competitive through deep domain expertise and high-touch service; for instance, Wilkinson Partners’ carve-out into A&M STAR enables Alvarez & Marsal to enter executive search focused on financial officers. Digital capability is the central battleground, with Spencer Stuart’s partnership with Qlu and Adecco Group’s Salesforce-powered subsidiary highlighting a hybrid human-AI future.

Regulatory compliance under GDPR and proliferating data-localization laws creates a moat for incumbents that have already embedded robust governance frameworks. Market differentiation increasingly hinges on advisory breadth, including leadership development, board effectiveness, and interim management, which allow firms to cross-sell beyond initial search mandates and lock in client relationships over multi-year horizons.

Executive Search Industry Leaders

Korn Ferry International

Heidrick & Struggles International, Inc.

Russell Reynolds Associates, Inc.

Egon Zehnder International AG

Spencer Stuart Associates, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Korn Ferry announced Q3 FY 2025 fee revenue of USD 668.7 million, including USD 204.6 million in executive search, reflecting 3% year-over-year growth.

- January 2025: TalentoHC acquired The PeterSan Group to broaden executive search capability and geographic reach.

- December 2024: Heidrick & Struggles added four senior hires to its Climate and Sustainability Practice to meet ESG leadership demand.

- October 2024: Creative Artists Agency purchased Hanold Associates, bringing entertainment sector expertise into executive search engagements.

Global Executive Search Market Report Scope

The executive search market focuses on recruiting senior-level professionals and leaders, such as CEOs, CFOs, and other C-suite executives, for critical organizational roles. Unlike general recruitment, it involves a tailored, strategic process to identify top-tier talent with the required expertise and cultural fit. Executive search firms often specialize in leadership placements across various industries, leveraging global networks and industry insights to deliver high-quality candidates.

The Executive Search Market is segmented by search type (retained, contingency, hybrid), function (C-suite, director level and above, specialized functional roles), end user (corporate sector, non-profit organization, government and public sector, other end users), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). the market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Retained |

| Contingency |

| Hybrid / Engaged |

| C-Suite (CEO, CFO, etc.) |

| EVP / SVP / VP |

| Director Level and Above |

| Niche / Emerging Roles (Chief AI, CISO, etc.) |

| Corporate / Private Sector |

| Government and Public-Sector Bodies |

| Non-Profit and NGOs |

| Private-Equity / Venture-Backed Firms |

| Technology and Digital Services |

| Life Sciences and Healthcare |

| Financial Services |

| Industrial and Manufacturing |

| Consumer and Retail |

| Other Industry Verticals |

| North America |

| South America |

| Europe |

| Asia Pacific |

| Middle East and Africa |

| By Search Type | Retained |

| Contingency | |

| Hybrid / Engaged | |

| By Function Level | C-Suite (CEO, CFO, etc.) |

| EVP / SVP / VP | |

| Director Level and Above | |

| Niche / Emerging Roles (Chief AI, CISO, etc.) | |

| By End-User Organization Type | Corporate / Private Sector |

| Government and Public-Sector Bodies | |

| Non-Profit and NGOs | |

| Private-Equity / Venture-Backed Firms | |

| By Industry Vertical | Technology and Digital Services |

| Life Sciences and Healthcare | |

| Financial Services | |

| Industrial and Manufacturing | |

| Consumer and Retail | |

| Other Industry Verticals | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

How large is the executive search market in 2026?

The executive search market size is USD 63.99 billion in 2026.

What is the forecast CAGR for executive search through 2031?

The market is projected to grow at a 10.11% CAGR through 2031.

Which search model has the largest share today?

Retained search commands 62.88% executive search market share in 2025.

Which region is expanding the fastest for executive search providers?

Asia Pacific is forecast to grow at a 10.71% CAGR between 2026 and 2031.

Why are Chief AI Officer roles boosting search activity?

The rise of AI governance creates specialized C-suite positions with limited talent supply, driving high-fee retained searches.

How are private equity firms influencing demand?

Private equity and venture-backed companies are increasing searches at an 11.28% CAGR as they upgrade leadership to accelerate portfolio value creation.

Page last updated on: