Electric Vehicle Battery Anode Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

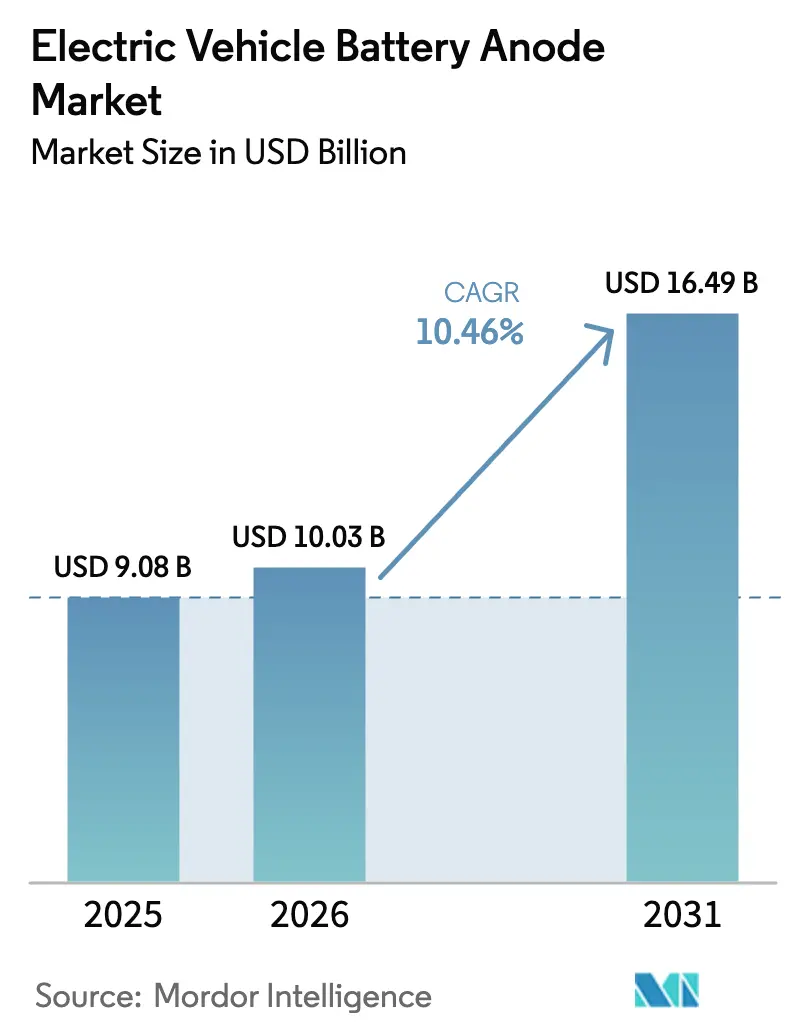

| Market Size (2026) | USD 10.03 Billion |

| Market Size (2031) | USD 16.49 Billion |

| Growth Rate (2026 - 2031) | 10.46% CAGR |

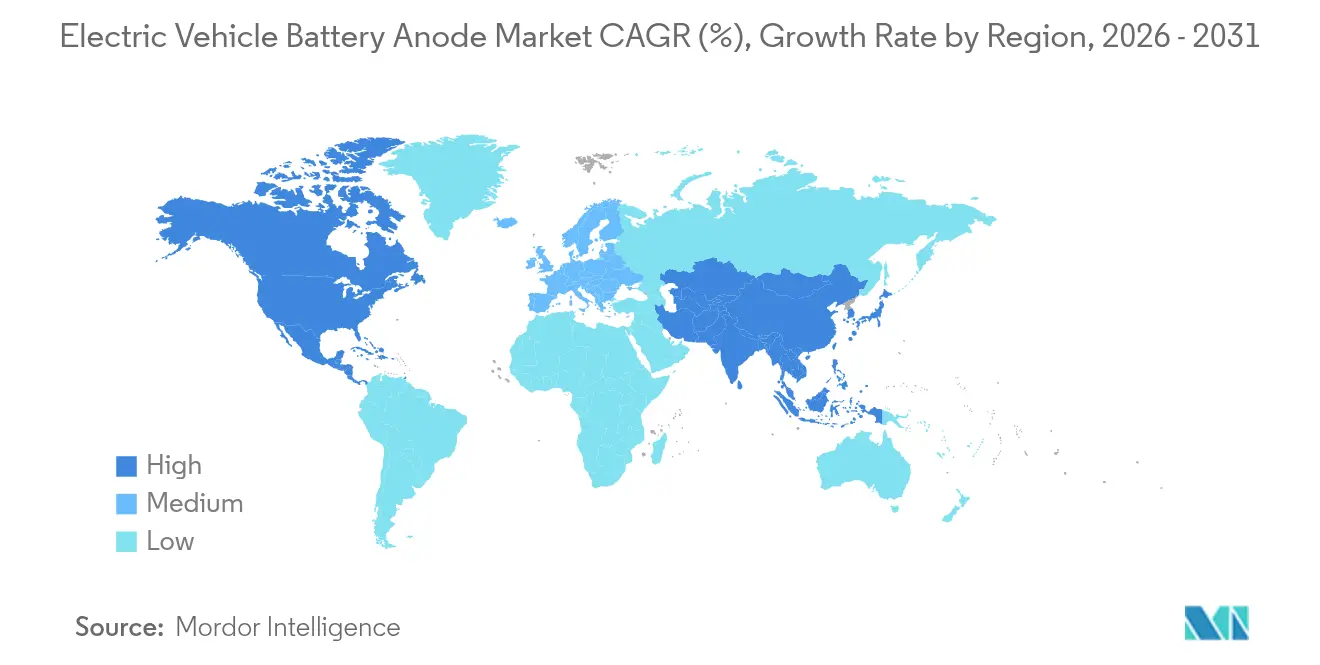

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Battery Anode Market Analysis by Mordor Intelligence

Electric Vehicle Battery Anode Market size in 2026 is estimated at USD 10.03 billion, growing from 2025 value of USD 9.08 billion with 2031 projections showing USD 16.49 billion, growing at 10.46% CAGR over 2026-2031.

High-silicon anodes, policy-driven local-content mandates, and recycling scale-ups provide momentum, while China-centric coating operations and silicon cycle-life hurdles temper the outlook. Cylindrical 4680-format cells expand their share because they lower pack assembly complexity, and Asia-Pacific remains the revenue anchor thanks to China’s spheronization capacity and South Korea’s synthetic-graphite build-out. North America and Europe accept higher costs to secure supply-chain sovereignty, and new mines in Mozambique, Australia, and Canada diversify feedstock. Moderate competitive concentration persists: the top five Chinese suppliers hold about 60% of global capacity, yet Western and Korean challengers scale quickly under the Inflation Reduction Act and Critical Raw Materials Act incentives.

Key Report Takeaways

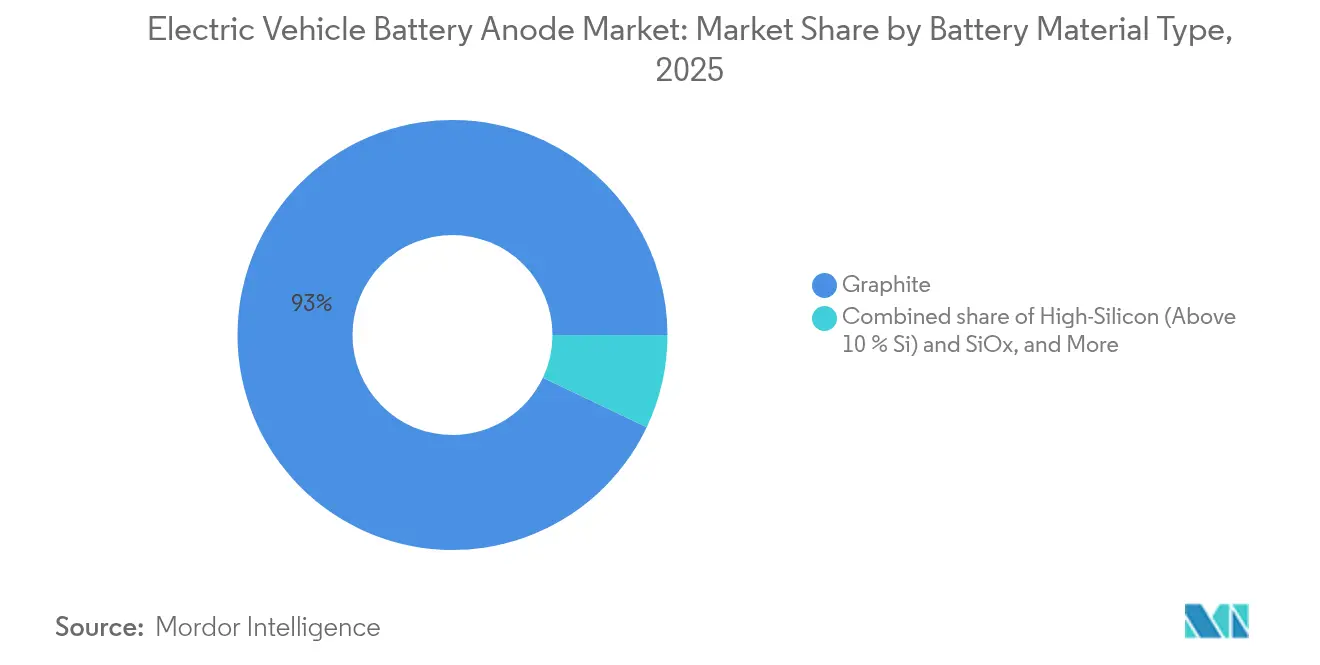

- By battery material type, graphite led with a 92.95% revenue share in 2025, while high-silicon formulations above 10% Si content are projected to grow at a 33.2% CAGR to 2031.

- By cell format, cylindrical cells captured 51.25% of demand in 2025 and are forecast to expand at a 11.75% CAGR through 2031.

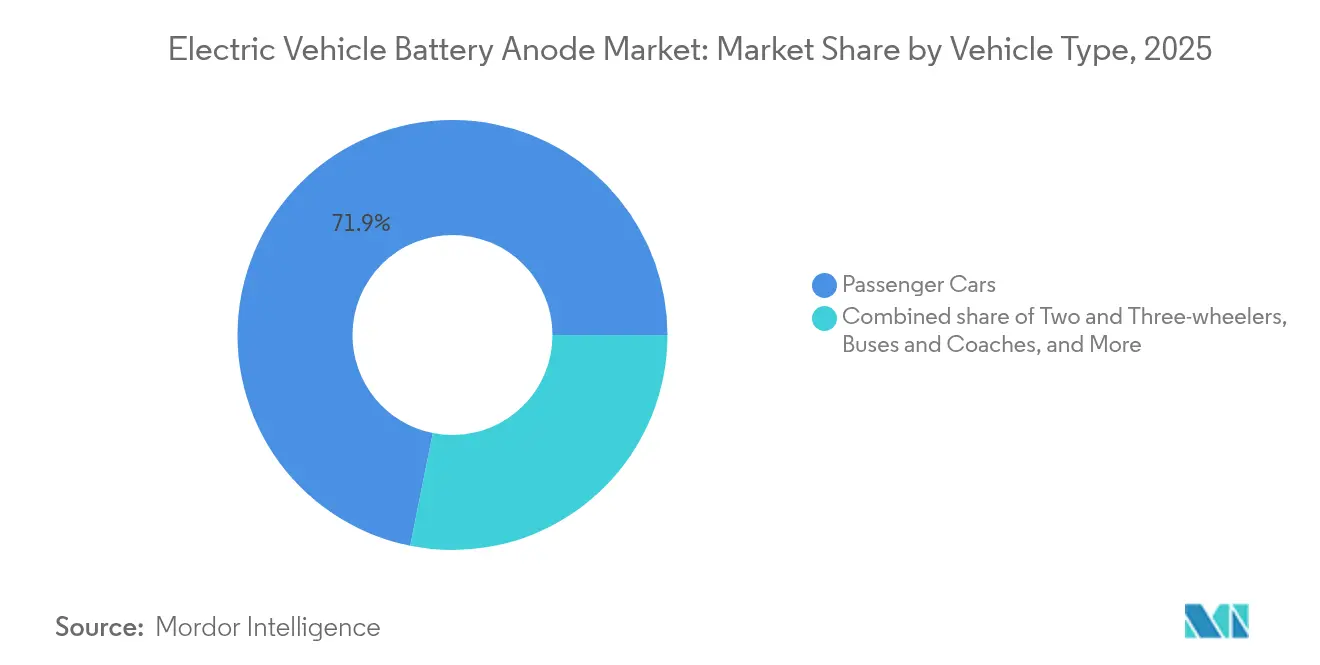

- By vehicle type, two- and three-wheelers represented the fastest-growing segment with a 29.1% CAGR outlook to 2031, although passenger cars retained a 71.85% volume share in 2025.

- By geography, Asia-Pacific held 63.10% of 2025 revenue, and is set to post an 11.65% CAGR, while North America is expected to grow at 12.98% as Section 45X credits catalyze domestic capacity.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicle Battery Anode Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV production volumes worldwide | 3.2% | Global, with Asia-Pacific contributing 65% of incremental volume, North America and Europe accounting for 28% | Medium term (2-4 years) |

| Government incentives & local-content rules for battery materials | 2.8% | North America & EU (IRA, CRMA), spill-over to India (PLI scheme), South Korea (K-Battery Strategy), Japan (Green Innovation Fund) | Long term (≥ 4 years) |

| Synthetic-graphite capacity build-out lowering cost curves | 1.1% | North America, Europe, South Korea—regions targeting cost parity with Chinese synthetic graphite by 2027-2028 | Medium term (2-4 years) |

| China's graphite export controls triggering supply-chain diversification | 1.9% | North America, EU, Japan, South Korea, Australia—markets pursuing non-Chinese feedstock and processing capacity | Short term (≤ 2 years) |

| OEM shift to high-Si composite anodes for 4680/"Gen 4" cylindrical cells | 1.5% | North America, EU, China (Tesla, BMW, Panasonic, CATL ecosystems), premium vehicle segments globally | Medium term (2-4 years) |

| Cell-format migration (prismatic to large-cylindrical) altering anode design specs | 0.8% | North America & EU primarily (Tesla 4680, BMW Neue Klasse), with gradual adoption in Asia-Pacific from 2027 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV Production Volumes Worldwide

Global light-duty EV output hit 14 million units in 2024, a 25% year-on-year rise that required roughly 420 GWh of batteries and 462,000 metric tons of anode material.[1]International Energy Agency, “Global EV Outlook 2024,” iea.org China produced 9.5 million passenger EVs, whereas Europe and North America combined for 3.2 million. Average pack capacities climbed from 60 kWh in 2020 to 80 kWh in 2024, lifting anode intensity per vehicle by 33%. Commercial-vehicle electrification amplifies demand: Daimler Truck and Volvo specify 540 kWh packs for Class 8 models, each containing 600 kg of anode material. Two-wheeler sales in Southeast Asia reached 20 million electric units in 2024 and already consume 80,000 t of graphite, a figure set to double by 2027.

Government Incentives & Local-Content Rules for Battery Materials

The Inflation Reduction Act requires that battery components originate from North America or FTA partners, prompting LG Energy Solution to invest USD 5.6 billion in a Michigan anode complex scheduled for 2026.[2]LG Energy Solution, “Michigan Investment,” lgensol.com Europe’s Critical Raw Materials Act targets 40% domestic processing by 2030; Syrah’s Louisiana synthetic-graphite plant advanced under a EUR 200 million EIB loan guarantee. South Korea’s K-Battery scheme allocates KRW 20.5 trillion to localize anodes, while India’s PLI program offers 20% capital subsidies, catalyzing Epsilon Advanced Materials’ 10,000 t Gujarat project.

China’s Graphite Export Controls Triggering Supply-Chain Diversification

Beijing’s December 2023 export-licensing rules cut non-Chinese spherical-graphite supply by 18% in 1H 2024, raising prices 12%. Syrah’s Balama mine, Novonix’s Tennessee line, and Daejoo’s Hungary plant collectively target 65,000 t of new annual capacity outside China by 2026. Canada’s Lac des Îles expansion and Australia’s developing assets aim to reduce China’s share of global feedstock to 60% by 2028.

OEM Shift to High-Si Composite Anodes for 4680 Cells

Tesla’s 4680 incorporates 5%–8% silicon, delivering 272 Wh/kg and a 16% range gain over 2170 cells. BMW’s Neue Klasse specifies 10% silicon and targets 1,000-cycle life starting in 2025.[3]BMW Group, “Neue Klasse Battery Cell,” bmwgroup.com Sila, Group14, and Panasonic lab results top 290 Wh/kg, yet blends keep silicon below 10% to retain 80% capacity after 1,000 cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicon's volumetric-expansion & cycle-life challenges | -1.4% | Global, acute in North America and EU where warranty standards exceed 1,500 cycles and premium-vehicle adoption drives silicon demand | Medium term (2-4 years) |

| ESG & carbon-footprint scrutiny on synthetic graphite | -0.7% | EU (CBAM enforcement from 2026), North America (corporate sustainability mandates), with secondary impact in Japan and South Korea | Medium term (2-4 years) |

| Impending recycling over-capacity curbing virgin-material demand | -0.6% | Europe (Northvolt Revolt, BASF black-mass refinery), North America (Li-Cycle, Redwood Materials), China (CATL, GEM Co.) | Long term (≥ 4 years) |

| Anode-coating stage still 97% China-centric; Heightened geopolitical risk | -1.2% | North America, EU, Japan—regions pursuing supply-chain sovereignty but facing 18-24 month lead times for coating-line commissioning | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Silicon’s Volumetric-Expansion & Cycle-Life Challenges

Pure silicon expands threefold during lithiation, fracturing the SEI and limiting first-generation composites to 500 cycles, well below automaker warranties of 1,500 cycles. Nano-structuring and carbon shells mitigate stress but raise material costs from USD 15/kg for graphite to USD 45/kg for silicon nanowires. Silicon blends of 5%–10% uplift energy density 8% yet delay the jump to 400 Wh/kg packs. Solid-state electrolytes could restrain swelling, but commercial volumes remain five to seven years away.

Anode-Coating Stage Still 97% China-Centric

Coating capacity clusters in Guangdong and Hunan, where BTR and Shanshan run lines that process 500,000 t/yr.[4]Bloomberg, “China’s EV Battery Dominance Is Built on Graphite Coating Plants,” bloomberg.com Western cell makers face 18- to 24-month equipment lead times, raising costs by USD 2/kg versus Chinese incumbents. New lines in Michigan, Okayama, and France together add 73,000 t/yr by 2026, still covering less than 10% of non-Chinese demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Material Type: Graphite Anchors, Silicon Surges

Graphite retained a 92.95% revenue share in 2025, while high-silicon anodes will grow at a 33.2% CAGR, the fastest of all materials. Natural graphite addresses cost-sensitive two-wheelers, whereas synthetic graphite commands a 30% premium in high-cycle applications. The electric vehicle battery anode market size for high-silicon formulations is forecast to reach USD 2.76 billion by 2031, equal to 16.74% of the segment revenue. Hard-carbon anodes for sodium-ion cells and lithium-titanate anodes for fast-charging fleets remain sub-3% niches but post 18%-22% CAGRs. Europe’s Carbon Border Adjustment Mechanism will penalize high-emission synthetic graphite, pushing suppliers toward renewable-powered furnaces.

Automakers split sourcing strategies: mass-market platforms pursue cost-optimized graphite, while premium models absorb silicon premiums for range advantages. Westwater’s Alabama mine and Epsilon’s Gujarat plant illustrate feedstock localization under U.S. and Indian policy umbrellas.

By Cell Format: Cylindrical Cells Consolidate Leadership

Cylindrical cells held 51.25% of anode demand in 2025 and are climbing at a 11.75% CAGR, reflecting Tesla’s, BMW’s, and Panasonic’s 46-series adoption. Prismatic cells account for 34.6% of volume, led by BYD’s blade architecture suited to compact sedans. Pouch cells form the balance, favored by Ultium and Hyundai for design flexibility. Electric vehicle battery anode market share for cylindrical cells is projected to hit 57.80% by 2031 as gigafactories scale 4680 lines in the United States and Europe. Cylindrical formats tolerate higher calendering pressure, raising volumetric density 6% without extra tooling.

Ongoing standardization reduces supplier risk: Panasonic, LG Energy Solution, Samsung SDI, and CATL all offer compatible cylindrical cells, enabling OEMs to dual-source. Prismatic suppliers remain closely linked to Chinese automakers, while pouch cells confront swelling challenges under 350 kW fast charging.

By Vehicle Type: Two-Wheelers Outpace Passenger Cars

Passenger cars commanded 71.85% of 2025 demand, but two- and three-wheelers are growing at 29.1% CAGR as India and Indonesia electrify 40 million annual scooter sales. The electric vehicle battery anode market size for two-wheelers is forecast to exceed USD 1.19 billion by 2031 on low-cost natural-graphite packs. Light commercial vehicles post a 13.7% CAGR, propelled by e-commerce delivery fleets, while medium and heavy trucks expand share as depot charging matures. Lithium-titanate’s 6-minute recharge meets bus and logistics duty cycles, keeping that chemistry’s niche alive.

Segment demand profiles diverge: passenger cars pay for silicon blends to maximize range, scooters chase USD 8/kg natural graphite, and commercial fleets weigh fast-charging gains against pack cost.

Geography Analysis

Asia-Pacific accounted for 63.10% of revenue in 2025 and is projected to grow at a 11.65% CAGR. China’s Hunan and Jiangxi provinces alone process 400,000 t/yr of natural graphite, while South Korea spends USD 15.4 billion to add synthetic capacity. Japan focuses on technology, with Mitsubishi Chemical’s 15,000 t line feeding Panasonic. India’s consumption triples to 45,000 t by 2030 as Tata Motors scales output. North America held 18.35% in 2025 and will post a 12.98% CAGR, driven by Section 45X’s USD 10/kg credits and feedstock from Canada’s Lac des Îles mine. The electric vehicle battery anode market size in North America is projected to reach USD 4.12 billion by 2031. Mexico remains an assembly hub, importing U.S. anodes to meet USMCA rules. Europe captured 15.25% in 2025 and grows at 12.55% as the Critical Raw Materials Act and CBAM add compliance costs to Asian imports. Syrah’s Louisiana plant and Northvolt’s recycling loop cover 88,000 t, still short of demand. South America and Africa export feedstock; Mozambique’s Balama mine alone fills 8% of global natural graphite trade.

Asia retains the largest share, yet China’s effective veto over coating capacity ensures global supply vulnerability until alternative lines are commission after 2027.

Mordor Intelligence provides coverage of the electric vehicle battery anode market across other key regional markets, including North America, South America, Europe, Middle East, and Africa, Europe, and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States, United Kingdom, Germany, India, and France incorporating local coverage and market participation, as required.

Competitive Landscape

Moderate concentration prevails: BTR, Shanshan, Putailai, Zeto, and Shinzoom together hold about 60% of capacity, with no single firm above 18%. Electric vehicle battery anode market entrants exploit policy tailwinds: Novonix targets 30,000 t/yr in Tennessee by 2026, while Syrah pursues 30,000 t/yr in Louisiana. Silicon specialists Sila, Amprius, and Nexeon court premium OEMs willing to pay 30% more for 20% range gains.

Vertical integration drives cost leadership. POSCO Future M combines precursor supply with coating to beat merchant costs by 15%. Panasonic and Samsung SDI enlarge patent portfolios around silicon prelithiation and graphene coatings. White-space lies in fast-charging anodes for logistics fleets and recycled graphite that can undercut virgin synthetic material by 20% once purity hits 95%.

The landscape will stay fragmented through 2027, then tighten as Western capacity scales under IRA and EU rules, while Chinese incumbents defend cost positions in natural graphite.

Electric Vehicle Battery Anode Industry Leaders

BTR New Material Group

Mitsubishi Chemical Group (incl. Kureha)

Shanshan Corporation

Shanghai Putailai New Energy (PTL)

LG Chem / LG Energy Solution

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: POSTECH and KIER produced hard-carbon–tin nano-composite anodes with 1.5× volumetric energy density over graphite while sustaining 1,500 cycles.

- February 2025: Resonac Corporation divested Resonac Packaging to Dai Nippon Printing to focus capital on anode material scale-up.

- May 2024: A team of Chinese scientists announced the development of a water-based battery with nearly double the energy density of conventional lithium batteries, potentially making aqueous batteries viable for electric vehicle applications.

- January 2024: The European Investment Bank (EIB) and GDI signed a quasi-equity loan agreement worth USD 22.15 million to advance GDI's next-generation silicon anode technology for electric vehicles, aiming to reduce reliance on graphite. This agreement is part of the InvestEU program, which seeks to stimulate over USD 412.05 billion in additional investment in new technologies by 2027.

Global Electric Vehicle Battery Anode Market Report Scope

An electric vehicle (EV) battery anode is one of the two main electrodes in a battery, the other being the cathode. In the context of electric vehicle (EV) batteries, typically lithium-ion batteries, the anode is commonly constructed using graphite.

The electric vehicle battery anode market is segmented by battery material type, cell format, vehicle type, and geography. By battery material type, the market is segmented into graphite, silicon-enhanced graphite (Up to 10 % Si), high-silicon (Above 10 % Si) and SiOx, lithium titanate (LTO), and other advanced (Hard-Carbon, CNT-Doped, Graphene). By cell format, the market is segmented into cylindrical, prismatic, and pouch. The market is segmented into passenger cars, light commercial vehicles, medium and heavy trucks, buses and coaches, two and three-wheelers, and off-highway and specialty EVs. The report also covers the market size and forecasts for the market across major regions. For each segment, the market size and forecasts are done based on value (USD).

| Graphite |

| Silicon-Enhanced Graphite (Up to 10 % Si) |

| High-Silicon (Above 10 % Si) and SiOx |

| Lithium Titanate (LTO) |

| Other Advanced (Hard-Carbon, CNT-Doped, Graphene) |

| Cylindrical |

| Prismatic |

| Pouch |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks |

| Buses and Coaches |

| Two and Three-wheelers |

| Off-Highway and Specialty EVs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Battery Material Type | Graphite | |

| Silicon-Enhanced Graphite (Up to 10 % Si) | ||

| High-Silicon (Above 10 % Si) and SiOx | ||

| Lithium Titanate (LTO) | ||

| Other Advanced (Hard-Carbon, CNT-Doped, Graphene) | ||

| By Cell Format | Cylindrical | |

| Prismatic | ||

| Pouch | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Trucks | ||

| Buses and Coaches | ||

| Two and Three-wheelers | ||

| Off-Highway and Specialty EVs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the electric vehicle battery anode market?

The electric vehicle battery anode market size reached USD 10.03 billion in 2026 and is forecast to climb to USD 16.49 billion by 2031.

Which anode material is growing the fastest?

High-silicon formulations with more than 10% Si content are expanding at a 33.2% CAGR to 2031, the quickest among all materials.

Why are cylindrical 4680 cells important for anode demand?

They increase energy density and simplify pack assembly, pushing cylindrical cells to a projected 57.80% share of anode demand by 2031.

How do China’s graphite export controls affect the supply chain?

The December 2023 licensing rules cut non-Chinese access by 18% in early 2024, raising prices and accelerating diversification into Mozambique, Canada, and the United States.

Which regions are investing most aggressively in local anode capacity?

North America leverages Section 45X tax credits, while Europe relies on the Critical Raw Materials Act and EIB financing to build synthetic-graphite and recycling plants.

What cycle-life issues limit high-silicon anodes?

Silicon expands up to 300% during lithiation, fracturing the SEI and restricting first-generation cells to 500 cycles, below automaker warranty thresholds of 1,500 cycles.

Page last updated on: