Anti-Slip Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

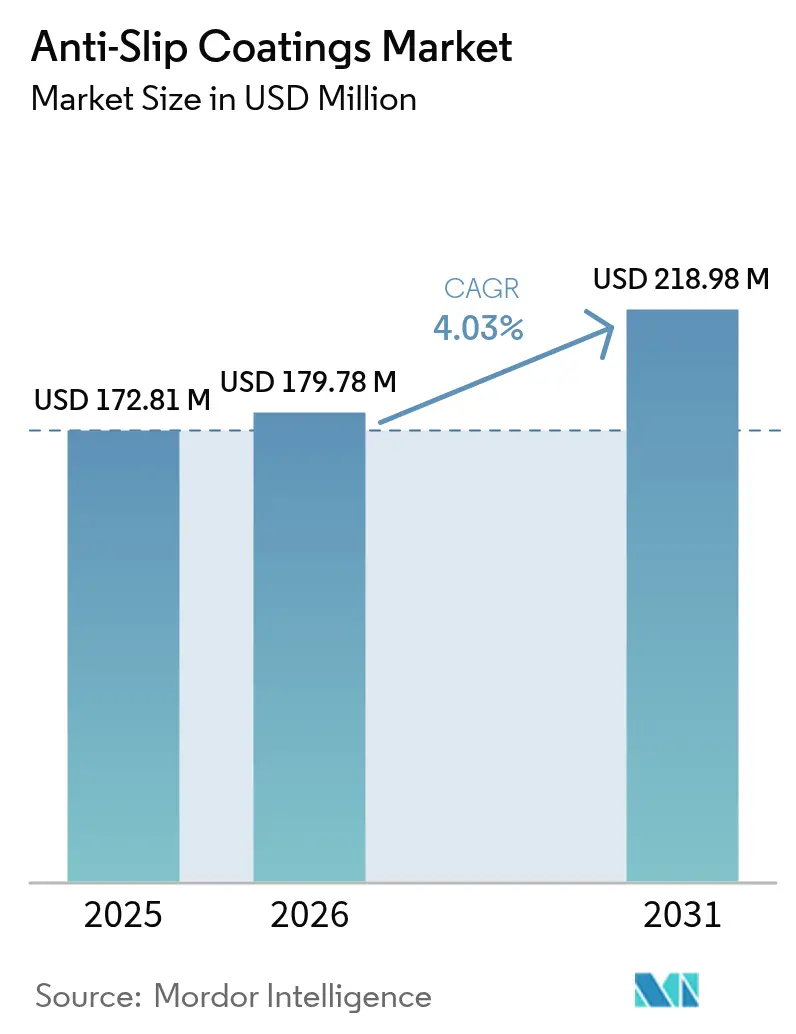

| Market Size (2026) | USD 179.78 Million |

| Market Size (2031) | USD 218.98 Million |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Slip Coatings Market Analysis by Mordor Intelligence

The anti-slip coatings market size was valued at USD 172.81 million in 2025 and estimated to grow from USD 179.78 million in 2026 to reach USD 218.98 million by 2031, at a CAGR of 4.03% during the forecast period (2026-2031). Mandatory safety regulations, higher liability premiums, and the spread of automated production lines underpin consistent spending on slip-resistant flooring across factories, hospitals, and public infrastructure. Demand is rising fastest where robotics, electrostatic-sensitive devices, and frequent chemical wash-downs intersect because traditional floor finishes cannot balance traction with electrostatic discharge control or chemical durability. Raw-material price swings and tighter solvent regulations add cost pressure, yet they also accelerate investment in low-VOC chemistries that improve worker safety and ease of installation. Suppliers that combine technical support with agile manufacturing are positioned to capture specification wins as project owners seek turnkey solutions rather than commodity coatings.

Key Report Takeaways

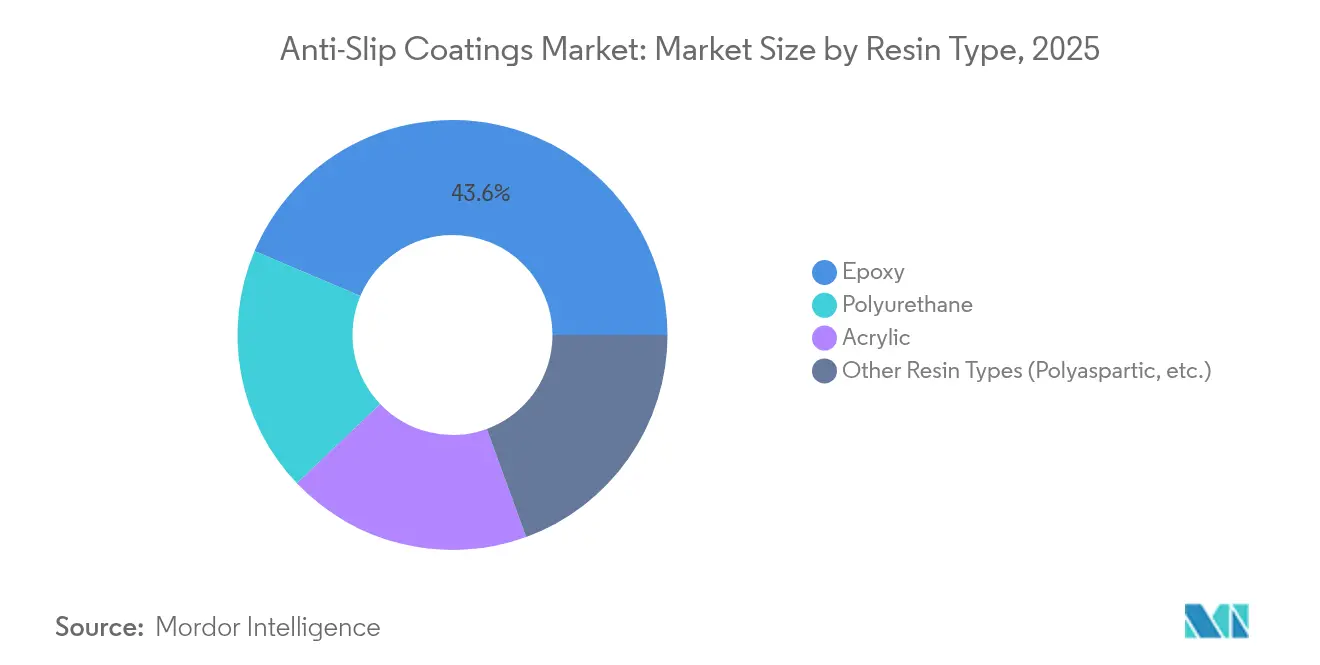

- By resin type, epoxy captured 43.62% of the anti-slip coatings market share in 2025, and other resin types will advance at a steady 4.74% CAGR through 2031.

- By technology, water-based systems held 58.77% of the anti-slip coatings market size in 2025 and are expanding at the fastest 4.61% CAGR to 2031.

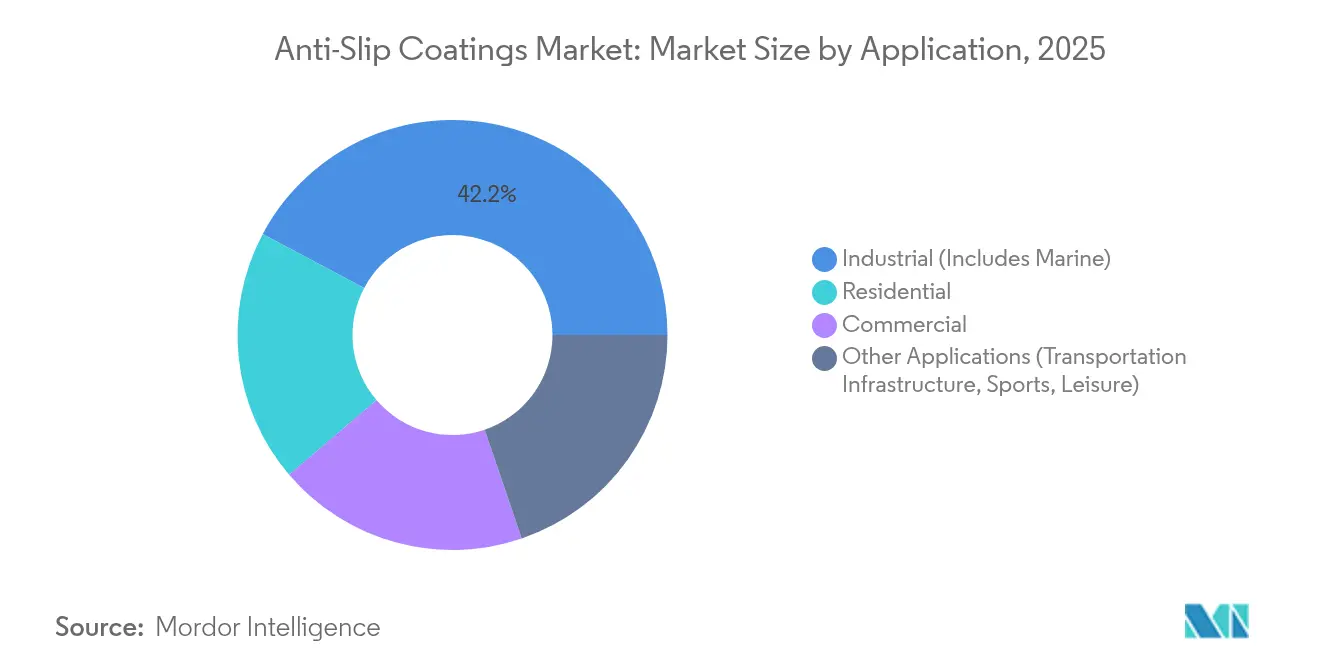

- By application, industrial led with 42.21% revenue share in 2025, while “other” applications are forecast to grow at the highest 4.83% CAGR through 2031.

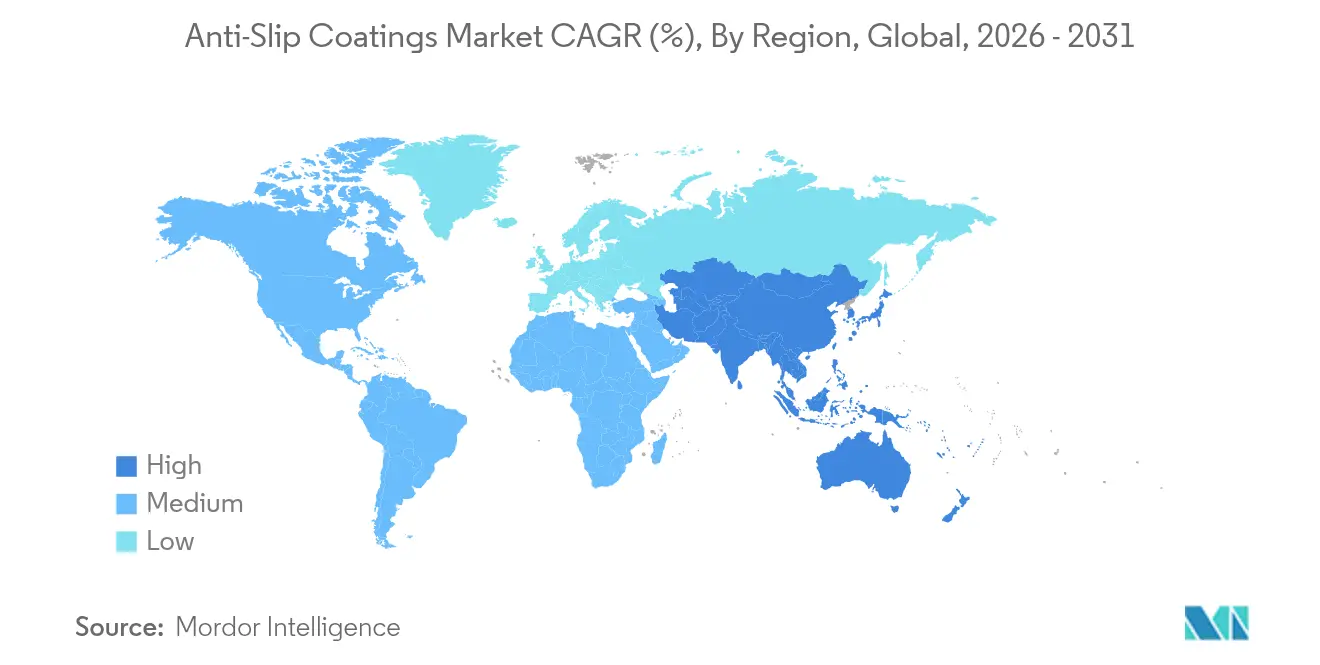

- By geography, Asia-Pacific commanded 44.35% of global revenue in 2025 and is set to grow at a 4.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-Slip Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Use Across Smart and Automated Manufacturing Floors | +0.80% | APAC core, spill-over to North America & EU | Medium term (2-4 years) |

| Stricter Workplace-Safety Codes and Insurance Mandates | +0.90% | Global, with early gains in North America & EU | Short term (≤ 2 years) |

| Rising Retro-Fit Demand from Aging Commercial Infrastructure | +0.60% | North America & EU primarily | Long term (≥ 4 years) |

| Construction Boom in Asia-Pacific and Middle-East | +1.10% | APAC core, MEA emerging markets | Medium term (2-4 years) |

| Anti-Slip Hybrid Coatings Gaining Healthcare Traction | +0.40% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Use Across Smart & Automated Manufacturing Floors

Automated factories now specify flooring that can tolerate continual robotic traffic, rolling loads, and aggressive sanitation while preserving stable friction values. Plant engineers have found that many legacy epoxy finishes interfere with electromagnetic sensors or degrade after repeated peroxide clean-downs, leading to unscheduled shutdowns. Hybrid polyaspartic systems that pair slip resistance with electrostatic discharge protection are gaining favor because they cure rapidly and support full production restart within hours. In Asia-Pacific’s electronics clusters, downtime costs have climbed sharply, making the incremental price of premium coatings less significant than the risk of line interruption. As a result, procurement teams increasingly reference preset “smart floor” performance templates that bundle anti-slip, ESD, and chemical-resistance metrics into a single specification.

Stricter Workplace-Safety Codes & Insurance Mandates

The Occupational Safety and Health Administration now issues penalties topping USD 15,000 per serious slip-and-fall breach, while insurers offer double-digit premium discounts to sites that install certified non-skid finishes. Settlement payouts of USD 50,000–100,000 per claim are common, so facility owners calculate that a USD 5–8 per ft² coating expense pays for itself after averting even one incident[1]United States Department of Labor, “Walking-Working Surfaces and Personal Protective Equipment,” osha.gov . Safety auditors also require documented coefficient-of-friction testing, pushing demand for products that ship with certification packages. These compliance dynamics quickly convert optional upgrades into mandatory capital items, especially in retail chains and logistics centers that face heavy foot traffic.

Rising Retro-fit Demand from Aging Commercial Infrastructure

More than 2 billion ft² of retail and office space built before 2010 in North America and Europe now falls short of new slip-resistance codes, creating a sizable retrofit backlog. Contractors must often diamond-grind weathered substrates, apply moisture-tolerant primers, and complete night-shift installations to avoid tenant disruption, all of which add premium labor mark-ups. However, property managers accept higher project costs when weighed against liability exposure and insurance prerequisites. Coating vendors answer this niche with accelerated-cure systems that attain full hardness overnight, shortening re-opening windows for revenue-critical sites.

Construction Boom in Asia-Pacific and Middle-East

Regional governments are channeling more than USD 1.7 trillion into airports, hospitals, and smart factories through 2030, and most projects now reference international traction norms such as ANSI A326.3 in their tender packages. Developers prefer high-solids or water-based formulations that reduce onsite VOC exposure and shorten schedule floats. Gulf Cooperation Council projects additionally demand resistance to thermal shock and sand abrasion, steering specifications toward polyurethane and hybrid chemistries known for toughness at temperature extremes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environment Regulations | -0.70% | Global, stricter in EU & North America | Short term (≤ 2 years) |

| Raw-Material (Epoxy, PU) Price Volatility | -0.50% | Global supply chain impact | Medium term (2-4 years) |

| Competition from Embedded Textured Flooring and Tapes | -0.30% | Primarily cost-sensitive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environment Regulations

The Environmental Protection Agency plans to restrict N-Methyl-2-pyrrolidone and several PFAS surfactants, compelling formulators to re-engineer legacy lines at a cost uptick of 15-25%[2]United States Environmental Protection Agency, “Proposed Rule: N-Methyl-2-pyrrolidone Industrial Surface Coatings,” epa.gov . Water-based options solve VOC hurdles but sometimes need extra build coats, which lengthen installation schedules and raise labor invoices. Firms with deep R&D pipelines can absorb these transitions, whereas small regional suppliers may exit the market or become acquisition targets.

Raw-Material (Epoxy, PU) Price Volatility

Anti-dumping duties on Asian epoxy imports raised North American resin input costs by more than 30% year-over-year in 2024[3]United States International Trade Commission, “Epoxy Resins From China and South Korea,” usitc.gov. Polyurethane feedstocks faced parallel swings after weather-related outages in the United States. To mitigate risk, large manufacturers lock multi-year supply pacts or internalize resin production, leaving small competitors exposed to spot-market spikes. Contractors increasingly request alternative quotes that standardize on polyaspartic or hybrid chemistries to hedge against single-resin dependence, opening the door for niche suppliers with flexible portfolios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance Faces Specialty Challenge

Epoxy finishes generated 43.62% of the anti-slip coatings market size for resin systems. They retain appeal because they bond tenaciously to concrete, endure chemicals, and accept varied aggregate blends that raise friction under wet oils. Yet, growth momentum is shifting toward other resin categories that deliver rapid return-to-service, lower temperature cure, or UV reliability that basic epoxies cannot match. Polyaspartic blends cure within two hours, letting automotive plants resume fork-truck routes before the next shift, while hybrid urethane-acrylic systems stretch enough to bridge micro-cracks in suspended slabs.

From 2026 to 2031, other resin types are projected to advance at a 4.74% CAGR, the highest among resin families. Hospitals and data centers prefer them because they emit ultra-low odor and release workers faster. Suppliers now bundle nonslip silica into pre-weighted cartridges, simplifying field ratios and reducing installer error. As specification writers value performance over commodity cost, niche resin innovators secure reference listings that were once the exclusive domain of epoxy giants, reshaping the competitive narrative inside the anti-slip coatings market.

By Technology: Water-Based Systems Lead Environmental Transition

Water-borne products represented 58.77% of anti-slip coatings market size by technology. Regulatory VOC caps, fire-safety rules in tunnels, and odor constraints in occupied buildings drive broad acceptance. New binder chemistries have closed historical gaps in hardness and chemical tolerance, and applicators appreciate equipment clean-up with plain water, which cuts solvent disposal fees. Several metros in the European Union now mandate water-borne or 100% solids solutions in public tenders, effectively standardizing demand.

Solvent-rich lines persist in ship decks and workshops that need extreme chemical resistance or sub-zero cure. Even so, most suppliers now promote hybrid technology that combines water carriers with reactive emulsions, delivering slip ratings equal to solvent counterparts. As green building labels gain traction, contractors who specialize in water-borne installs win premium bids, reinforcing the shift toward eco-aligned products inside the anti-slip coatings market.

By Application: Industrial Leadership Meets Diversification

Industrial facilities translate to 42.21% of current anti-slip coatings market share by end use. Petrochemical units, assembly plants, and marine docks rely on high-build aggregates that tolerate caustic spills and rolling loads. Yet the fastest expansion lies within transportation infrastructure, leisure complexes, and sports, which post a 4.83% CAGR. Airport owners specify nonslip polyurethane layers for jet-blast zones, and sports-venue operators install cushioned acrylic textures that reduce athlete fatigue while preventing skids.

Commercial office fit-outs also embedded micro-textured clear coats onto polished concrete lobbies to maintain aesthetics without compromising coefficient of friction. Residential uptake remains modest but grows as homeowners apply rough-profile epoxies around pools and garage entries. This diffusion underscores an evolving perception that slip-resistance is a lifestyle necessity rather than an industrial afterthought, broadening the total addressable anti-slip coatings market.

Geography Analysis

Asia-Pacific generated the largest regional revenue, leveraging a 44.35% share in 2025 and advancing at a 4.82% CAGR through 2031. Mass rail, semiconductor fab, and megahospital projects in China and India specify premium non-skid surfaces that integrate with automated guided vehicles. The Association of Southeast Asian Nations is standardizing safety codes in line with ISO friction norms, lifting baseline requirements, and pushing municipal tenders toward branded products.

North America trails in absolute size but benefits from extensive retrofit cycles across logistics warehouses, supermarkets, and healthcare campuses. Stringent OSHA enforcement and mid-western winter hazards keep demand resilient even during construction slowdowns. End users often bundle slip resistance with antimicrobial ratings, favoring hybrid chemistries that answer both criteria.

Europe maintains mature adoption levels driven by insurer stipulations, yet growth stems from heritage building upgrades where contractors seek breathable water-borne solutions that protect historic substrates. Middle Eastern and African markets remain smaller but display outsized growth rates as stadiums, metros, and tourism assets emerge. Specifications here emphasize UV durability and thermal shock resistance, giving polyurethane hybrids an edge.

Regulatory Landscape

Anti-slip coatings sit across chemical-management rules and performance verification requirements. In the United States, VOC compliance is anchored in EPA rules under 40 CFR Part 59, which shapes formulation choices toward water-based and high-solids systems. OSHA enforcement and documentation requirements also push facility owners to specify coatings supported with test data and certification packages for slip resistance. Anti-dumping duties affecting epoxy resin imports added to compliance economics as well, lifting North American resin input costs by more than 30% year-over-year in 2024 and influencing product selection and sourcing strategies for contractors and formulators.

Across Europe and parts of Asia, market access depends heavily on product stewardship and standardized test methods. EU REACH and CLP drive substance restrictions and labeling, accelerating reformulation away from tightly regulated solvents and surfactants, while performance testing is increasingly referenced to harmonized methods such as DIN EN 16165:2021 for slip resistance. In Asia-Pacific, national standards including China GB/T 9263-2020, along with tender specifications that cite international traction norms (for example ANSI A326.3 in large infrastructure projects), raise the baseline for documented friction performance and favor suppliers that can provide consistent testing protocols across regions.

Value Chain Analysis

The value chain begins with upstream suppliers of base resins (epoxy, polyurethane, acrylic, and specialty hybrids) and functional additives that create texture and traction, including silica, ceramic or mineral aggregates, and polymer-bead or microsphere systems. Formulators then blend binders, fillers, anti-slip media, and curing packages into site-applied coatings, with growing emphasis on low-VOC water-based technologies and rapid-cure hybrids to reduce downtime for industrial and public facilities. Compliance is built in early, because product design and QA are often mapped to the test methods referenced by end markets, including DIN EN 16165 (Europe) and GB/T 9263-2020 (China), alongside sector-specific requirements such as MIL-PRF-24667D and EN 4508:2006 for defense and aerospace use cases.

Midstream distribution typically runs through direct-to-project sales for industrial and infrastructure accounts, and through coating distributors or specialty flooring installers for commercial and residential work. Applicators and contractors capture value through surface preparation, aggregate broadcast rates, and curing conditions, which determine whether a coating meets coefficient-of-friction targets. This raises demand for supplier technical service, on-site testing support, and packaged systems rather than commodity products. Downstream buyers include factories, hospitals, logistics centers, marine and transportation assets, and retrofit-heavy commercial buildings, where procurement increasingly bundles slip resistance with chemical durability, ESD control, and certification documentation within a single flooring specification.

Competitive Landscape

The anti-slip coatings market is moderately fragmented, yet tier-one multinationals still set performance benchmarks. AkzoNobel continues to widen its Interpon powder line with water-based binders that meet EU green mandates. PPG Industries divested its silicas unit to sharpen focus on high-value coatings and is funneling proceeds into low-friction additive research. Sherwin-Williams recently launched soft-feel comfort floors that marry aesthetics with traction, reinforcing its position in healthcare and education niches.

Regional producers in Southeast Asia and Eastern Europe capture municipal work through localized service and flexible batch sizes, but many rely on imported resins, leaving them vulnerable to currency swings. Raw-material shocks have triggered strategic alliances where independents form purchasing pools to secure epoxy contracts. Meanwhile, merger interest is rising as private equity targets specialty formulators that own patented aggregate blends or antimicrobial IP, signaling an approaching consolidation phase inside the anti-slip coatings industry.

Customers increasingly compare suppliers based on digital specification tools, COF certification packages, and total installed warranty support rather than unit price. Firms able to validate on-site friction via smartphone-linked sensors or provide turnkey resurfacing services lock in repeat revenue. This service-oriented competition raises entry barriers for small-scale players and encourages product differentiation anchored in data transparency.

Anti-Slip Coatings Industry Leaders

3M

Akzo Nobel N.V.

PPG Industries Inc.

Sika AG

The Sherwin-Williams Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear gap is emerging between heavy-duty broadcast epoxy floor systems and lighter, maintenance-oriented sealers for residential and light-commercial surfaces, where owners want slip resistance without disruptive resurfacing. This shows up in 2026 product activity focused on ready-to-use, water-based, anti-slip sealers and color coats that simplify application on concrete, pavers, and exterior walkways, widening the addressable market for contractors and DIY channels. At the same time, healthcare, electronics, and automated manufacturing sites are specifying multi-attribute floors that combine traction with fast return-to-service and chemical wash-down resistance, and in some cases ESD performance, which creates room for hybrid chemistries and system suppliers that can support validation using standardized friction documentation.

Opportunities also extend to additive and testing support as regulators and specifiers move toward performance-based verification. Broader use of standardized methods such as ANSI A326.3 and DIN EN 16165 increases the value of coatings shipped with friction-testing documentation and clear installation protocols, particularly for public infrastructure and institutional buildings. On the innovation side, published research in 2026 introduced the TexCoMP framework for optimizing texture-coating-material performance on walkways, supporting more data-driven design of anti-slip surfaces and giving formulators a structured pathway to reduce trial-and-error while meeting wet-traction thresholds with lower-VOC systems.

Recent Industry Developments

- June 2026: A peer-reviewed study in PLOS One published the TexCoMP (Texture-Coating-Material-Performance) framework to model and optimize anti-slip performance of coated walkway surfaces across environmental and material variables. The work supports more predictive formulation and texture-design approaches, which can shorten development cycles and improve confidence in meeting wet-traction targets across varied substrates.

- April 2025: DYCO, a division of ICP Group, launched DYCO Court & Floor, a 100% acrylic anti-slip coating for commercial and residential recreational surfaces. The launch broadened options for medium-texture, skid-resistant finishes on asphalt and concrete, reinforcing demand for acrylic systems in high-traffic leisure and light-commercial applications.

- May 2024: The market saw increased specification pull-through for documented slip-resistance testing aligned to newer methods such as DIN EN 16165:2021 in Europe, influencing how contractors package testing and compliance documentation for public-facing projects. This shift elevated the role of certification packages and standardized on-site verification as differentiators alongside resin chemistry and installation speed.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the sales value of anti-slip coating materials that are applied as a film on a surface to improve traction and reduce slip risk in day to day use. It includes products sold for industrial, commercial, and residential surfaces where slip resistance is a key performance need.

Scope exclusions: Excludes anti-slip tapes and mats, separately sold aggregate additives, and non-coating mechanical texturing solutions.

Segmentation Overview

- By Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Other Resin Types (Polyaspartic, etc.)

- By Technology

- Water-based

- Solvent-based

- By Application

- Residential

- Commercial

- Industrial (Includes Marine)

- Other Applications (Transportation Infrastructure, Sports, Leisure)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of APAC

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the first demand map and to keep the market model anchored to indicators that can be checked year after year. We refer to public sources such as the US Bureau of Labor Statistics (workplace injury and safety indicators), OSHA and similar national safety regulators (slip resistance guidance and compliance themes), Eurostat and UN Comtrade (construction and industrial activity proxies, plus trade signals for coating materials), and industry standards bodies such as ASTM and ISO (test methods and coefficient of friction terminology).

On top of that, we review company filings, investor presentations, product technical data sheets, and reputable press to understand where coating systems are being specified and how performance claims are positioned. Select paid subscriptions are used to speed up company financials and intelligence checks, patent trend scans, and shipment-level import and export review where it is relevant to coating raw materials. The sources listed here are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what is actually being purchased and applied, and then stress testing the assumptions used in the model. We spoke with a mix of coating formulators, applicators, distributors, and safety and facility stakeholders across major end-use settings, and respondent input was balanced across APAC, EMEA, and the Americas so that one geography did not overly shape the final numbers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | APAC: 38% |

| Mid tier: 45% | Functional/Unit leaders: 28% | EMEA: 35% |

| Smaller Players: 22% | Managers: 56% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where surface protection coatings demand is reconstructed using construction and industrial activity indicators, and then filtered through the likely adoption of slip-resistant systems in floors, decks, ramps, and similar substrates. Once the demand pool is formed, we apply splits by resin family and end-use context using interview feedback and visible specification patterns, and the main clause is reached only after those layers are reconciled into a single value.

For checks, bottom-up approximations are run on a selective basis using a sampled set of product price points and typical consumption per square foot for common floor and deck applications, which is then multiplied by plausible project volumes derived from sector activity. Key inputs used in the model include industrial and commercial flooring activity, workplace safety focus indicators, resurfacing and maintenance cycles for high traffic areas, resin and additive price direction, and the mix shift between water-based and solvent-based systems as compliance expectations evolve.

Forecasts are built using scenario analysis supported by short-run trend fitting (exponential smoothing) on the leading indicators above, and then adjusted based on what primary respondents expect for specification intensity and pricing over the next few years. Where bottom-up checks have gaps, such as limited visibility on small local applicator volumes, the missing share is handled through penetration ranges that are reviewed with channel participants and then applied consistently across regions.

Data Validation & Update Cycle

Validation is done by triangulating the model output against independent signals, and then following up on any large variances until the story is coherent. We run anomaly checks on year over year movement, resin mix changes, and implied average selling prices, and any outliers are reviewed by a second analyst before sign-off.

The report is refreshed annually, and interim updates are triggered when material events occur, such as sharp raw material price changes or regulation shifts that alter specification behavior. Before delivery, a fresh review pass is completed so the numbers reflect the latest public releases and recent expert feedback.

Mordor Intelligence's Anti Slip Coatings Market Size Versus Other Published Estimates

Published market sizes for anti-slip coatings often vary because each publisher draws the market line differently and does not always align on the same base year or pricing assumptions. Differences also show up when one estimate leans more on construction cycles, while another leans more on safety compliance narratives without quantifying conversion into coating demand.

Anti-slip tapes and mats sit outside Mordor Intelligence's scope, which is one practical reason our value can differ from estimates that bundle adjacent traction products into a single safety surface total. The spread also comes from how fast price is assumed to rise for epoxy and polyurethane systems, whether marine and industrial flooring are counted with the same intensity across regions, and how frequently currency conversions and indicator series are refreshed.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 179.78 M (2026) | |

| Global Consultancy A | USD 158.72 M (2024) | Uses an earlier base year and a faster growth curve, and the scope description is broader around end uses, which can shift the implied demand pool and price mix versus a coatings-only definition. |

| Industry Publisher B | USD 169.00 M (2025) | Includes a wider application framing (such as flooring and marine stated together) and applies higher long-range growth, which can lift totals if penetration and ASP progression are not constrained by near-term activity indicators. |

Taken together, the table shows that year selection and what gets counted as an anti-slip solution explain most of the distance between figures. By keeping the variables tied to observable coating demand drivers and by rechecking assumptions with channel participants, our estimate stays easier to trace back to clear steps that can be repeated in later updates.

Key Questions Answered in the Report

What is the current size of the anti-slip coatings market?

The anti-slip coatings market stands at USD 179.78 million in 2026 and is on track to reach USD 218.98 million by 2031, reflecting a 4.03% CAGR.

Which region contributes most to global sales?

Asia-Pacific leads with 44.35% of worldwide demand in 2025 and is expanding at a 4.82% CAGR through 2031.

Why are water-based anti-slip products growing so quickly?

Water-based systems already account for 58.77% of the anti-slip coatings market size because they satisfy tightening VOC rules, lower fire risk, and simplify cleanup without sacrificing performance.

Which resin type is dominant today?

Epoxy formulations hold 43.62% of 2025 revenue thanks to their chemical resistance and adhesion, although faster-curing polyaspartic resins are escalating at 4.74% CAGR.

How do safety regulations affect purchasing decisions?

OSHA fines, insurance incentives, and stricter building codes have turned slip-resistant flooring from a discretionary upgrade into a compliance essential, boosting demand across industrial, commercial, and public sectors.

What is driving retrofit demand in developed markets?

Buildings erected before 2010 often fail new slip standards, creating a retrofit pool of more than 2 billion ft² in North America and Europe where owners seek fast-curing, low-odor solutions to minimize downtime.

Page last updated on: