Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

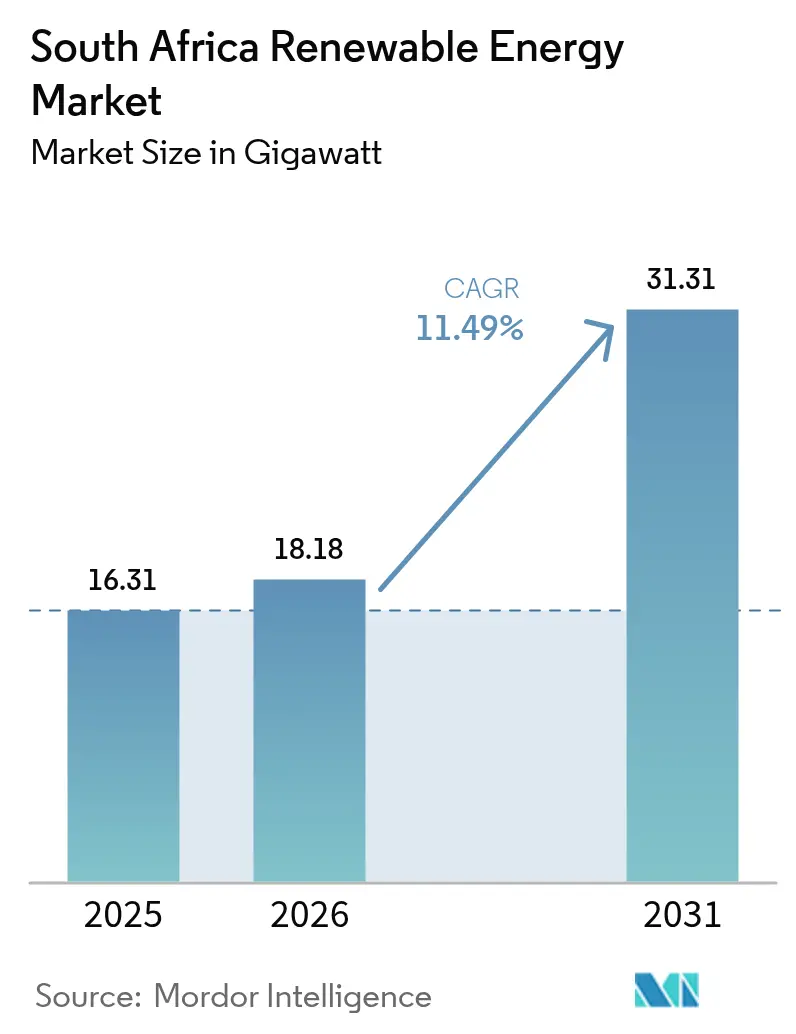

| Base Year Market Size (2025) | 16.31 gigawatt |

| Market Volume (2026) | 18.18 gigawatt |

| Market Volume (2031) | 31.31 gigawatt |

| Growth Rate (2026 - 2031) | 11.49% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Renewable Energy Market Analysis by Mordor Intelligence

South Africa Renewable Energy Market size in 2026 is estimated at 18.18 gigawatt, growing from 2025 value of 16.31 gigawatt with 2031 projections showing 31.31 gigawatt, growing at 11.49% CAGR over 2026-2031.

This trajectory reflects the country’s systematic shift from coal-reliant generation to a diversified mix, led by utility-scale solar photovoltaic (PV) and onshore wind projects. Tariffs for grid power have increased by 190% since 2014, making renewable contracts priced at R0.50-0.60 per kWh more attractive to mines, municipalities, and manufacturers. The Integrated Resource Plan (IRP) 2023 guides the addition of 3 to 5 GW of new clean capacity each year, while the removal of licensing caps for private plants under 100 MW in 2024 has unlocked a new class of distributed assets. Energy wheeling and day-ahead trading now provide fresh revenue channels, deepening competition and drawing foreign capital into the South African renewable energy market.

Key Report Takeaways

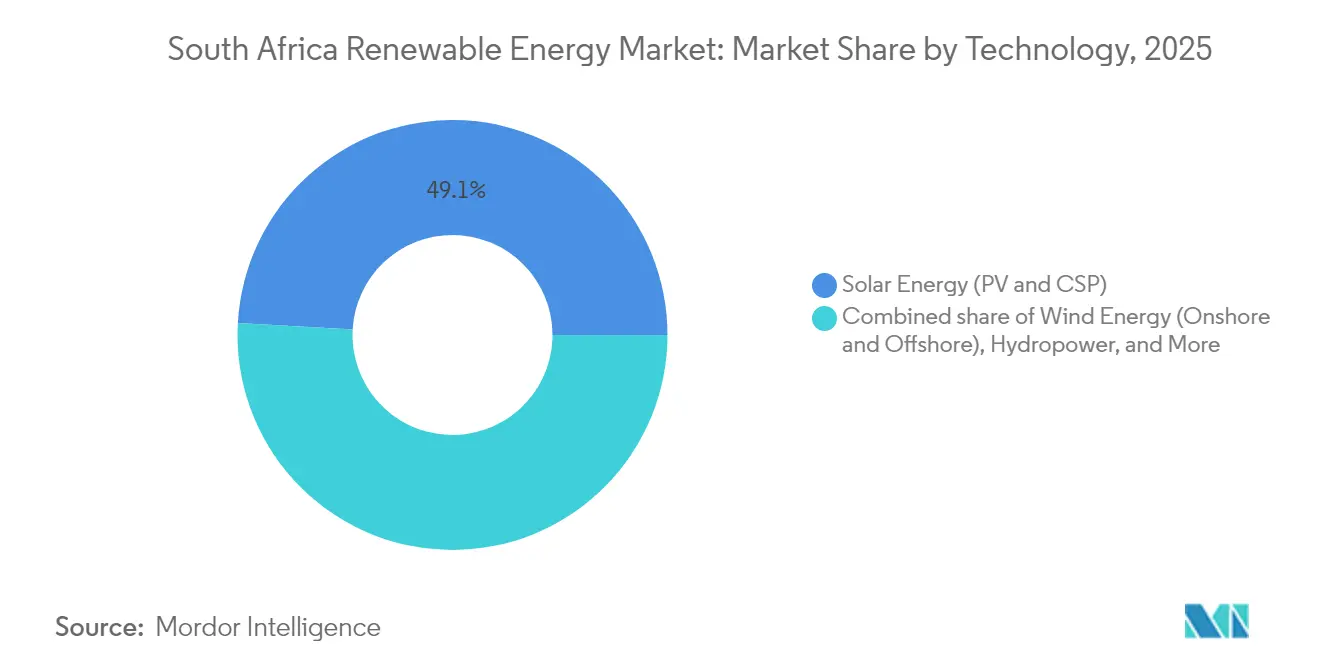

- By technology, solar PV retained the largest 49.12% share of the South Africa renewable energy market in 2025, whereas wind is on course for the fastest 17.83% CAGR to 2031.

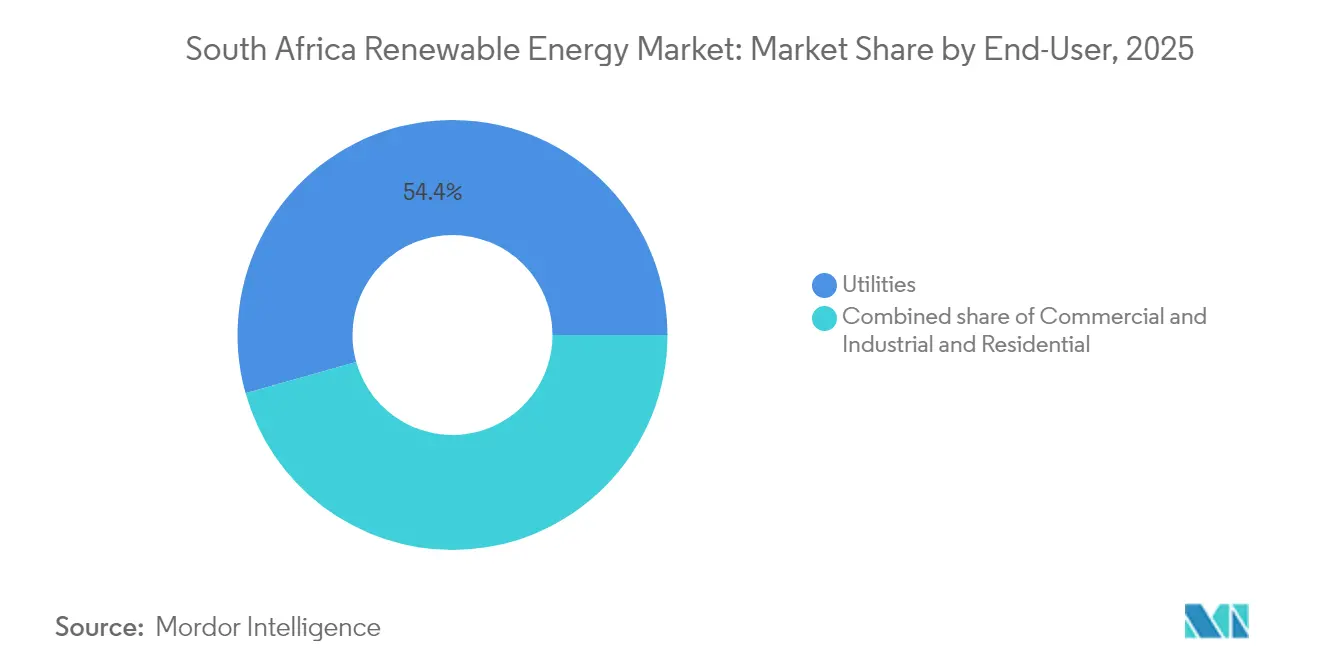

- By end-user, utilities controlled 54.37% of the South African renewable energy market size in 2025, and this segment is poised to grow the quickest at a 12.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating electricity tariffs accelerating C&I solar uptake | 2.8% | National, with early gains in Western Cape, Gauteng industrial corridors | Short term (≤ 2 years) |

| Government IRP target of 3–5 GW new renewables per year | 3.2% | National, concentrated in Northern Cape, Western Cape wind corridors | Medium term (2-4 years) |

| Rapid fall in solar-PV & battery storage LCOE | 2.1% | Global impact, amplified in high-irradiation regions (Northern Cape, Free State) | Long term (≥ 4 years) |

| Licensing-cap removal for <100 MW private projects | 1.9% | National, with spillover to industrial mining regions (Limpopo, North West) | Short term (≤ 2 years) |

| Emergence of energy-wheeling & day-ahead trading platforms | 1.4% | APAC core, spill-over to industrial hubs (Gauteng, KwaZulu-Natal) | Medium term (2-4 years) |

| Renewable-manufacturing master-plan & 10% import-tariff incentive | 1.1% | National, with manufacturing focus in Eastern Cape (Coega SEZ), Gauteng | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Electricity Tariffs Drive Commercial Solar Adoption

Average grid tariffs rose to R1.96 per kWh in 2024, while new utility-scale solar projects came in at nearly R0.55 per kWh, widening the savings gap. Registrations for private generation jumped from 7,454 MW in June 2024 to 9,662 MW in September 2024 as mining houses, led by Exxaro’s 68 MW Lephalale Solar project, opted for self-supply. Corporate power-purchase agreements now sidestep Eskom via trader portals, reinforcing the South Africa renewable energy market.[1]South African Photovoltaic Industry Association, “National Embedded Generation Statistics September 2024,” SAPVIA, sapvia.co.za

Government IRP Targets Accelerate Utility-Scale Deployment

The IRP 2023 sets a rolling commitment for 3 to 5 GW of annual renewable builds and 7,220 MW of gas-to-power for flexibility. National Energy Regulator of South Africa (NERSA) cleared 1.1 GW of projects in Q3 2024 alone, showing faster permitting under the Electricity Regulation Amendment Act. A 10% import-tariff incentive on locally produced components underpins domestic content goals and cements regional leadership, with South Africa forecast to account for 40% of Sub-Saharan Africa’s 90 GW renewable additions by 2030.[2]International Energy Agency, “Africa Energy Outlook 2024,” IEA, iea.org

Technology Cost Convergence Reshapes Project Economics

Ground-mounted solar now achieves €0.041–0.050 per kWh in top irradiation zones, matching onshore wind at €0.043 to 0.092 per kWh. Battery storage prices have decreased by 82% since 2013, propelling hybrids such as Scatec’s 540 MW Kenhardt PV plant, which includes a 225 MW/1,140 MWh battery. Stand-alone storage, such as Red Sands’ 153 MW/612 MWh unit, is increasingly offsetting diesel peakers, which averaged a 6.2% capacity factor in 2024.

Private Project Licensing Reforms Unlock Distributed Generation

Scrapping licenses for sub-100 MW plants reduces lead times to one year, spurring 500 MW of systems with a capacity of ≤ 1 MW in 2024. Mines in Limpopo and the North West gain immediate tariff relief, although 133 GW of queued projects still await grid allocation, spotlighting the need for accelerated transmission upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transmission-grid congestion in Northern Cape corridors | -1.8% | Northern Cape renewable energy development zones | Medium term (2-4 years) |

| High cost of capital & financing bottlenecks | -1.4% | National, particularly affecting smaller developers | Short term (≤ 2 years) |

| New 10% solar-panel import tariff raises near-term capex | -0.9% | National, with higher impact on utility-scale projects | Short term (≤ 2 years) |

| Rooftop-solar saturation dampening residential demand in 2024 | -0.6% | Urban centers (Cape Town, Johannesburg, Durban) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Transmission Grid Bottlenecks Constrain Northern Cape Development

Awarded wind volumes dipped when corridor capacity filled, leaving 133 GW in limbo. Kimberley-Upington’s 400 kV backbone was built for coal exports, not high-density renewables, so the Just Energy Transition Partnership’s USD 8.5 billion pledge focuses on new 765 kV lines. Slow disbursement delays unlock the Northern Cape’s top-tier solar and wind resources.

Financing Costs Impede Project Bankability

Weighted average cost of capital (WACC) for South African projects sits 300-500 basis points above global benchmarks. A USD 200 million European Investment Bank facility, in conjunction with the Development Bank of Southern Africa, offers relief, while JICA provides concessional loans; however, smaller developers lack comparable access. The Phase-Two carbon-tax escalation, set for January 2026, could improve margins, but policy uncertainty sustains investor risk premiums.[3]International Monetary Fund, “Financing Clean Energy in Emerging Markets,” IMF, imf.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Wind Acceleration Challenges Solar Dominance

Solar PV controlled 49.12% of the South Africa renewable energy market in 2025 and delivered 6 GW of registered capacity by September 2024. However, wind enjoys a 17.83% forecast CAGR thanks to 3,000+ full-load hours along coastal belts. For projects exceeding 100 MW, the technology share now stands at 54.4% solar and 45.6% wind, marking a rapid convergence. Concentrated solar power remains a niche market of approximately 500 MW, providing grid inertia, while hydro, bioenergy, and emerging ocean technologies offer limited incremental capacity. Strict IEC 61215 and IEC 61400 compliance underpins reliability, and turbine assembly at the Coega SEZ lends local depth.

Solar’s lower daytime capacity factor versus wind’s round-the-clock profile sparks hybrid proposals aimed at smoothing output and hitting dispatchable bids in future tenders. As battery prices fall, solar-plus-storage hybrids are expected to claim a growing slice of the South Africa renewable energy market for new utility awards.

By End-User: Utilities Drive Market Expansion

Utilities held 54.37% of the South Africa renewable energy market share in 2025 and are forecast to post the fastest 12.55% CAGR to 2031. Eskom improved energy availability to 60% in 2024, opening space for renewables to offset diesel peakers. Cities such as Cape Town and Johannesburg now procure directly, with Cape Town’s 200 MW tender serving as a model for peers.

Commercial and industrial (C&I) buyers follow, accounting for most of the 9,662 MW private-registration pipeline, led by mining majors that integrate PV behind the meter. Residential adoption nears saturation in high-income suburbs, though rural electrification keeps volume upside down alive. NERSA’s 2024 Amendment Act streamlines approvals, while SANS 10142-1 installation standards secure grid safety for distributed projects.

Geography Analysis

The Northern Cape hosts 65% of South Africa's utility solar and 45% of its wind capacity, thanks to over 2,000 kWh/m² of irradiation and robust Karoo winds. Transmission limits, however, place a ceiling on near-term additions until new 765 kV corridors arrive. The Western Cape ranks next, with 25% of the national wind stock and the only domestic turbine-assembly line at Coega in the Eastern Cape.

Eastern Cape and Free State contribute 20% combined through coastal wind farms and inland PV arrays. KwaZulu-Natal's grid constraints limit large-scale projects, but Durban's commercial and industrial (C&I) market drives the adoption of rooftop PV. Gauteng leads the way in distributed generation, boasting a registered capacity of 1,200 MW, despite weaker resources, as industrial users seek tariff relief. Limpopo and North West see traction in mining self-generation, while Mpumalanga's coal sector hinders the expansion of renewable build, leaving a structurally heterogeneous landscape for the South African renewable energy market.

Regulatory Landscape

South Africa's renewable build-out is guided by national planning and procurement instruments led by the Integrated Resource Plan 2025 (IRP 2025) and the REIPPPP, with private generation and trading rules continuing to expand. NERSA is still registering small-scale embedded generators under the Licensing Exemption and Registration Notice 4 of 2022, which supports a growing distributed-project pipeline following licensing reforms seen in the Electricity Regulation Amendment Act era.

Industrial policy is increasingly linked to power-market regulation through the South African Renewable Energy Masterplan (SAREM), which targets localization across renewable energy and storage value chains. Oversight and execution remain anchored in procurement and monitoring, with NERSA renewable monitoring reports tracking operational performance, and by June 2025 South Africa had 6,618 MW of grid-installed capacity from 94 REIPPPP and three risk-mitigation IPP plants. Government also signaled a continued procurement focus in the 2025/2026 financial year, including new rounds for REIPPPP, the Battery Energy Storage Programme, and gas-to-power, with the Department of Electricity and Energy issuing a reminder notice in March 2026 for prospective bidders for the Gas IPP Procurement Programme (GASIPPPP) Bid Window 1.

Competitive Landscape

International developers lead a moderately concentrated field. Scatec ASA operates the 540 MW Kenhardt solar-plus-storage flagship, while EDF Renewables controls a 1.2 GW pipeline across multiple provinces. Enel Green Power and Mainstream Renewable Power develop hybrid systems with advanced energy management. Local firms such as Mulilo and SolarAfrica gain ground through BBBEE partnerships and distributed solutions.

M&A activity accelerated: Aggreko acquired RenEnergy in July 2024 to expand its C&I reach, and Greenstreet acquired select Scatec assets for portfolio diversification. Swedfund and IFU placed USD 44 million into Sturdee Energy, underscoring investor appetite even amid grid bottlenecks. Competitive edges center on financing strength, hybrid design skills, and compliance with local-content thresholds that reach 45% in some bid windows.

White-space opportunities span rural mini-grids, green hydrogen exports, and heavy-industry heat electrification, but all hinge on incoming regulation. Combined, the top five developers controlled roughly 45% of installed capacity in 2024, supporting the moderate profile of the South Africa renewable energy market.

South Africa Renewable Energy Industry Leaders

-

Mainstream Renewable Power Ltd

-

EDF Renewables

-

Scatec ASA

-

Enel Green Power

-

ENGIE SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Wholesale-market reform and new utility-private partnership models are opening near-term whitespace for developers, traders, and balance-sheet investors that can structure bankable offtake and grid-access solutions. A phased implementation of a Market Code in 2026, alongside the Electricity Regulation Amendment Act pathway, supports wheeling and competitive contracting beyond the traditional utility procurement channel, reinforcing corporate offtake momentum already visible in the market.

Execution-led opportunities cluster around (i) grid-ready renewable projects able to clear licensing and connection milestones under REIPPPP Bid Window 7 activity, (ii) hybridization and flexibility assets aligned with procurement emphasis in the 2025/2026 financial year (Battery Energy Storage Programme and gas-to-power rounds), and (iii) local supply-chain buildout mapped to SAREM and domestic content goals. Evidence from 2026 includes financial close progress on Bid Window 7 solar, including Mulilo's 337 MW Middlepunt Solar PV project in Free State, alongside commissioning and energization of large wind capacity, such as EDF Power Solutions commissioning the 420 MW Koruson 1 cluster and Enel Green Power RSA bringing online the 330 MW Impofu wind cluster. Eskom's creation of Eskom Green, with an initial 2 GW pipeline and announced capital allocation, is also expanding the addressable deal flow for EPC, O&M, project finance, and corporate PPA structuring.

Recent Industry Developments

- July 2026: NERSA granted generation licences for four solar projects under REIPPPP Bid Window 7.3, totaling about 890 MW of contracted capacity (reported as over 1 GW installed capacity across the set). The approvals move shovel-ready utility-scale solar closer to construction starts and underscore the role of formal licensing decisions, including for developers such as Red Rocket SA and ENGIE.

- June 2026: The acquisition of Mainstream Renewable Power South Africa by A.P. Moller Capital was signed, bringing a portfolio that includes 148 MW of assets and an 11.6 GW development pipeline under a new owner. This reflects continued infrastructure investor interest in South African renewable platforms with corporate offtake-led pipelines.

- April 2026: EDF and Anglo American, through the Envusa Energy joint venture, powered up a 140 MW wind farm. The milestone adds operating capacity linked to private-sector partnership structures and supports the scaling of corporate renewable procurement models that depend on wheeling and long-term offtake agreements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the installed renewable power capacity operating in South Africa across grid connected and eligible behind the meter projects, expressed in gigawatts (GW). We treat the market as capacity additions and the resulting installed base, not electricity sales or equipment revenue.

Scope exclusions: We exclude fossil-based generation, pure transmission and distribution spending, and renewable energy certificate trading that is not tied to physical operating capacity.

Segmentation Overview

-

By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

-

By End-User

- Utilities

- Commercial and Industrial

- Residential

Data Sources, Market Sizing, and Validation

Desk Research

For the desk phase, we first anchored the capacity baseline using public power statistics and policy releases that describe what is commissioned, contracted, and still under procurement. Sources used for this step include official energy and electricity publications such as those from South Africa's Department of Mineral Resources and Energy, Eskom system updates, IRENA renewables statistics, IEA country dashboards, and the World Bank energy indicators.

To avoid overstating the market, the desk work was then cross-checked with project level signals from association pages, grid connection announcements, and credible press releases, followed by a scan of company filings and investor presentations for disclosed MW commissioning and pipeline timing. We also used a paid subscription for company financials and intelligence, and a patent database selectively to check supplier activity and technology direction. These desk sources are illustrative and not exhaustive, and we also used other public references to collect, verify, and clarify data points.

Primary Interviews and Surveys

Primary work was used to confirm what is actually reaching commercial operation and to sanity-check expected commissioning timelines, curtailment risk, and the split between utility and distributed build. We spoke with developers, EPC and O&M participants, financiers, and large power buyers, and then reconciled the inputs across South Africa to reflect differences by province and grid availability.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 17% | |

| Mid tier: 45% | Functional/Unit leaders: 25% | |

| Smaller Players: 21% | Managers: 58% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction of South Africa's renewable installed base using published commissioning, procurement awards, and grid connection status, which are then converted into an annual GW pathway. Once that path is built, selective bottom-up checks are applied using a sampled roll-up of project MW by technology and expected COD timing, and then totals are adjusted where the two views do not align.

The model is driven by a small set of repeatable inputs that we can validate in calls, such as awarded procurement volumes, observed commissioning cadence, capacity factors by technology, grid connection and curtailment indications, and the pace of private offtake (including corporate PPAs and wheeling enabled demand). When a project pipeline data point is incomplete, we fill the gap by assigning a probability-weighted COD based on permitting stage and typical build times in the country, and then we retest the output against expert feedback.

For forecasting, we primarily use scenario analysis so the outlook reflects policy and grid constraints, along with execution upside, and the scenario weights are reviewed with primary respondents. The final forecast remains capacity based, and year-to-year changes are explained through additions, retirements where applicable, and timing shifts rather than assumed revenue inflation.

Data Validation & Update Cycle

Validation is done through multiple checks so the final numbers do not depend on one source type. We compare model outputs against independent signals like national renewable statistics, utility system communications, and known procurement results, and then investigate spikes that do not match commissioning reality.

Before sign-off, the build and forecast assumptions are reviewed in steps by another analyst, and follow-up calls are triggered when the model shows large variance by technology or an unexpected step change in annual additions. The report is refreshed annually, with interim updates when major procurement rounds, regulation changes, or large project delays occur, and a final pre-delivery review is completed so the latest events are reflected.

Mordor Intelligence's South Africa Renewable Energy Market Sizing Compared With Other Published Estimates

Published estimates for South Africa renewables often do not line up because they are not always measuring the same thing, and the units can quietly switch between capacity, generation, and revenue. Differences also appear when one source counts announced pipelines as if they are operating assets, or when time windows for commissioning are assumed more aggressively.

The biggest gap driver is the unit of measurement, where Mordor Intelligence sizes the market as installed renewable capacity in gigawatts and ties year-by-year changes to commissioning and grid connection status, rather than translating capacity into implied dollar value using wholesale power prices or equipment spending assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.31 B (2025) | |

| Industry Publisher A | USD 100.27 B (2024) | Uses a revenue framing in USD and appears to bundle multiple value pools (technology sales, project spend, and or power value) across renewables, which does not map cleanly to installed capacity additions in a single year. |

| Sector Publisher B | USD 45.20 B (2025) | Limits scope mainly to solar and wind, and the value is sensitive to assumed equipment and project pricing, storage attachment, and how distributed systems are monetized, which can inflate or compress the total versus a capacity-only view. |

The spread in the table is mainly explained by what is being counted, and whether the total is built from GW of operating assets or from a value stack that depends on pricing and conversion assumptions. By keeping the market definition tied to measurable capacity signals and then stress-testing timing with field feedback, the final size stays easier to replicate and audit when new projects are awarded or delayed.

Key Questions Answered in the Report

What is the projected capacity of the South Africa renewable energy market in 2031?

The market is forecast to reach 31.31 GW by 2031, up from 18.18 GW in 2026.

Which segment holds the largest South Africa renewable energy market share?

Solar PV leads with 49.12% share in 2025, while wind is the fastest-growing technology segment.

How fast is the utilities segment growing?

Utilities are expected to expand at a 12.55% CAGR through 2031, the quickest among end-users.

Why are electricity tariffs driving renewable uptake?

Grid tariffs rose 190% since 2014, while new solar contracts price near a third of Eskom rates, spurring C&I uptake.

What are the main obstacles for new projects?

Transmission congestion in the Northern Cape and elevated financing costs remain the leading constraints on new capacity.

Page last updated on: