Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

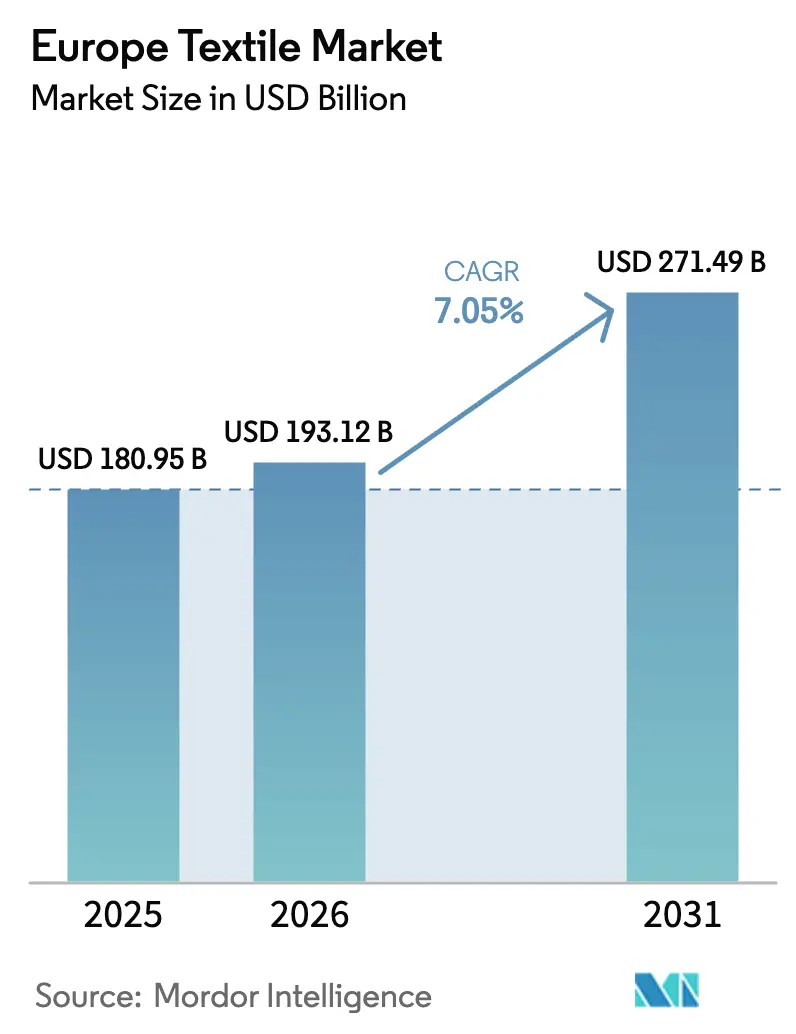

| Base Year Market Size (2025) | USD 180.95 Billion |

| Market Size (2026) | USD 193.12 Billion |

| Market Size (2031) | USD 271.49 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

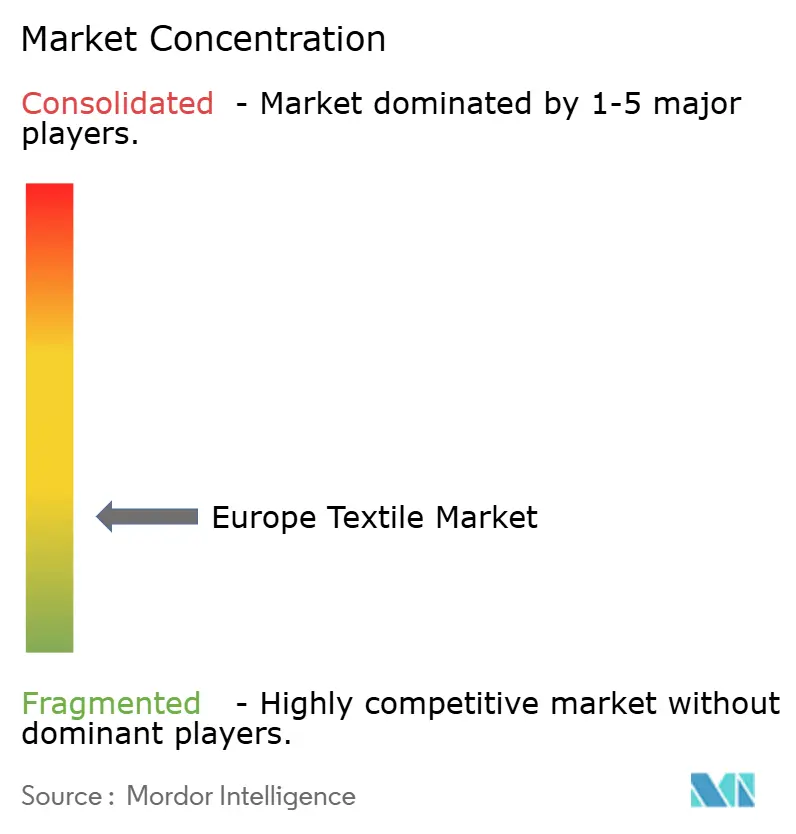

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Textile Market Analysis by Mordor Intelligence

The Europe Textile Market size is projected to expand from USD 180.95 billion in 2025 and USD 193.12 billion in 2026 to USD 271.49 billion by 2031, registering a CAGR of 7.05% between 2026 to 2031.

Circular-economy legislation, quicker fashion cycles, and surging demand for technical fabrics are the pivotal forces shaping the European textile market. Mandatory separate textile-waste collection across the EU-27, together with the phased launch of the Digital Product Passport, is channeling capital toward recycling plants and traceability tools. E-commerce platforms have cut design-to-shelf lead times to under four weeks, prompting mills to adopt digital knitting, automated dye kitchens, and near-infrared sorting. Investment is also shifting to high-margin applications such as flame-retardant fabrics for electric-vehicle battery enclosures and geotextiles for rail and road upgrades. At the same time, demand for locally cultivated flax, hemp, and wool is rising as brands highlight reduced transport footprints and “made-in-Europe” fiber stories.

Key Report Takeaways

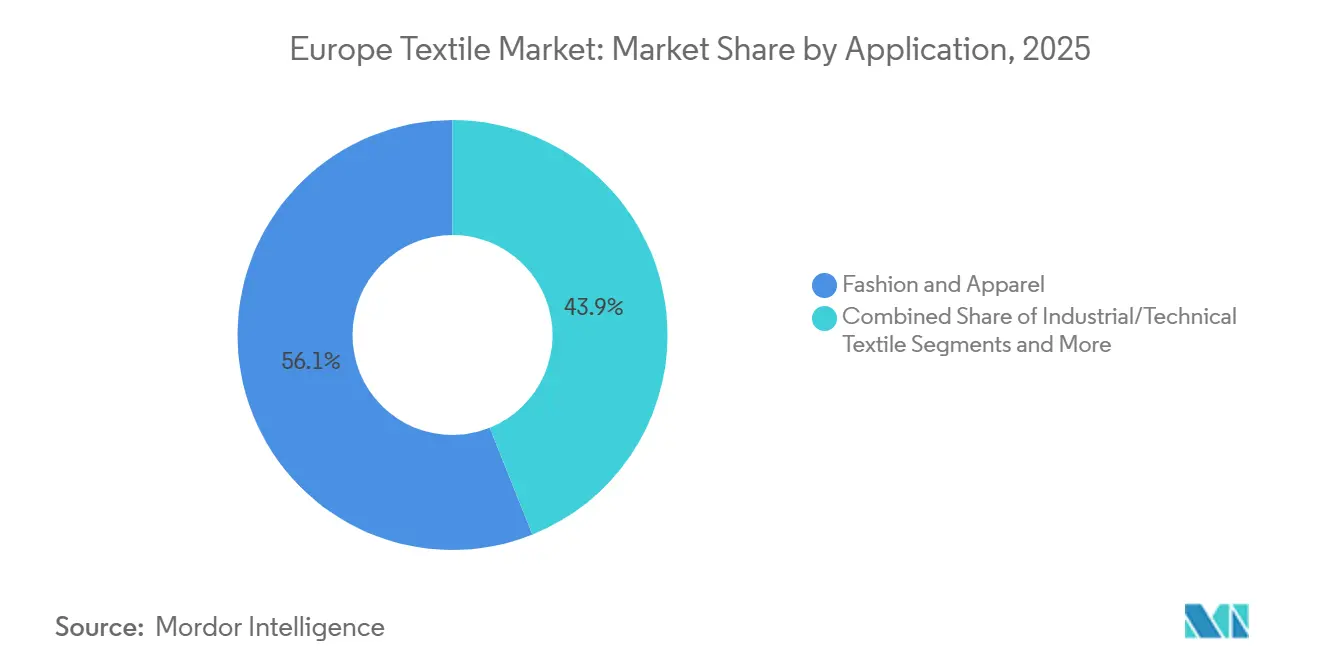

- By application, fashion and apparel held 56.06% of the European textile market share in 2025, while industrial and technical textiles are forecast to expand at a 6.15% CAGR through 2031.

- By raw material, synthetic fibers accounted for 53.96% of the European textile market size in 2025, with polyester alone projected to register a 6.56% CAGR between 2026 and 2031.

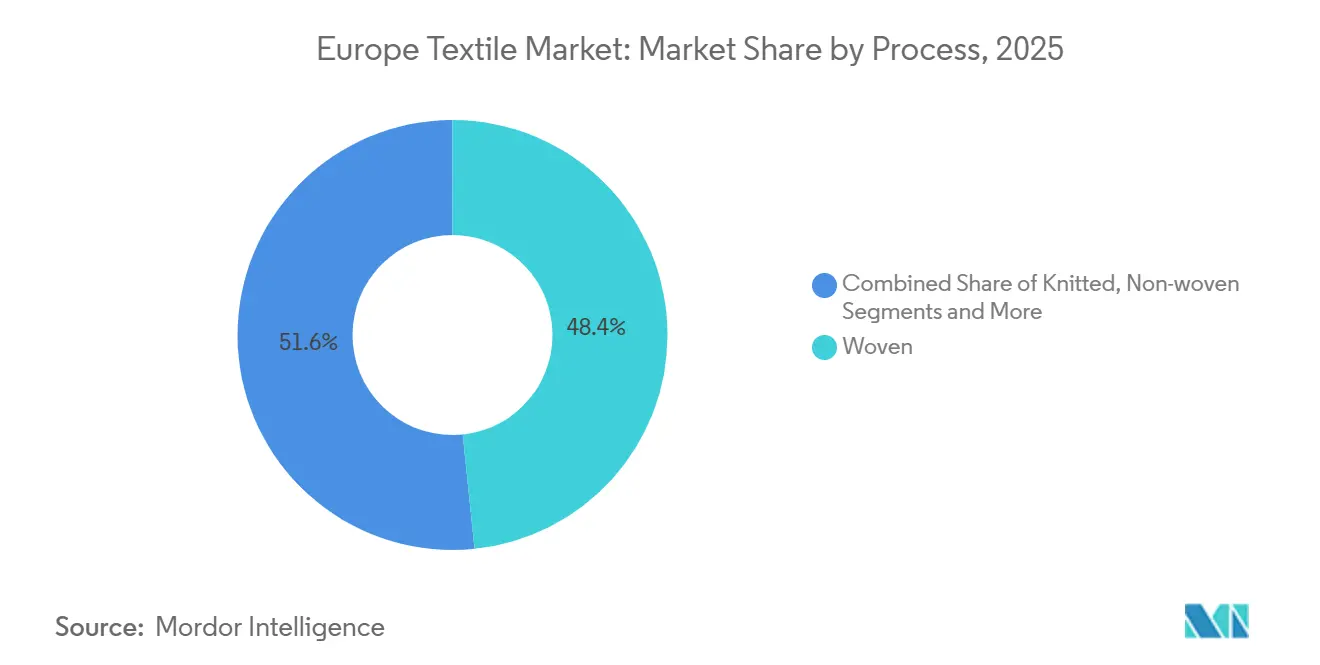

- By process, woven fabrics contributed 48.36% revenue in 2025, whereas non-woven technologies are anticipated to post a 6.05% CAGR to 2031.

- By geography, Germany captured 25.45% of the European textile market share in 2025, and Spain is set to record the fastest growth at 5.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Textile Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Separate Collection of Textile Waste Across EU-27 from 2025 | +1.5% | EU-27 | Medium term (2–4 years) |

| Growth of High-Performance Technical Textiles for Mobility and Infrastructure | +1.3% | Germany, France, Nordics | Long term (≥ 4 years) |

| Rapid Changes in Fashion Cycles and Rise of Fast Fashion | +1.2% | Spain, Italy, Portugal | Short term (≤ 2 years) |

| EU Digital Product Passport Enabling Data-Rich Circular Business Models | +1.0% | EU-27 | Medium term (2–4 years) |

| E-Commerce and Social-Commerce Platforms Shortening Design-to-Shelf Lead Times | +0.9% | Germany, France, UK | Short term (≤ 2 years) |

| Demand Surge for Europe-Grown Flax, Hemp, and Wool as Low-Carbon Local Fibers | +0.8% | France, Belgium, Netherlands | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Mandatory Separate Collection of Textile Waste Across EU-27 from 2025

From January 2025, all municipalities were required to install dedicated textile-collection points, redirecting roughly 5 million tonnes of garments per year into European sorting hubs[1]European Commission, “Waste Framework Directive,” environment.ec.europa.eu. Early movers such as France and the Netherlands achieved collection rates above 60% by pairing curbside bins with social-enterprise partners. The regulation exposed a shortfall: Europe had fewer than 50 automated sorting lines in mid-2025, so investors committed USD 870 million to new plants in Poland, Spain, and Portugal. Producers now face eco-modulation fees, pushing them to design mono-material garments with detachable trims. Over the medium term, the collection mandate is expected to lift recycled-fiber availability and underpin circular supply contracts.

Growth of High-Performance Technical Textiles for Mobility and Infrastructure

Electric-vehicle makers increased technical-textile content to more than 12 kg per car in 2025, replacing steel in battery enclosures with carbon-fiber composites for weight savings. EU states earmarked USD 130 billion for rail and highway upgrades, lifting demand for geotextiles that stabilize soil and reduce asphalt thickness. Hospitals mandated washable barrier fabrics that meet ISO 16604, driving purchases of flame-retardant and antimicrobial materials. Patent filings for hybrid spacer-composite architectures rose 18% in 2024, signaling fresh R&D spend[2]European Patent Office, “Patent Statistics 2024,” epo.org. The long-term driver pulls investment toward ultra-high-molecular-weight polyethylene and aramid filaments that earn margins three to five times those of commodity polyester.

Rapid Changes in Fashion Cycles and Rise of Fast Fashion

Ultra-fast fashion platforms now post new styles every 48 hours, forcing European mills to switch from six-month production runs to micro-batches of 500–1,000 meters. Digital printing, automated cutting, and in-house dyeing allow vertically integrated groups to meet next-day orders, while contract weavers risk cancellation if they miss narrow delivery windows. Between 2023 and 2025, European apparel brands raised SKU counts by 35%, yet overall unit sales stayed flat, showing a pivot to variety over volume. A consumer backlash is emerging at the premium end, where “slow fashion” labels that offer repair services and fiber disclosure are gaining traction. The driver raises velocity expectations but also enlarges niches for traceable, durable fabrics.

EU Digital Product Passport Enabling Data-Rich Circular Business Models

The Ecodesign for Sustainable Products Regulation introduces a phased Digital Product Passport, requiring every textile to carry embedded traceability data by 2030[3]European Commission, "Ecodesign for Sustainable Products Regulation," commission.europa.eu. Pilot projects already link QR codes to supply-chain records, enabling resale marketplaces, rental platforms, and repair networks to verify fiber content and care history. Early adopters gain brand trust and premium pricing, while laggards risk exclusion from regulated markets. The passport also underpins producer-responsibility fees, rewarding mono-material construction that simplifies end-of-life recycling. Over the medium term, data-rich garments are expected to unlock secondary revenue streams and tighten material loops.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile energy and raw-material prices squeezing low-margin producers | -0.8% | EU-27 | Short term (≤ 2 years) |

| High capex requirement for state-of-the-art recycling and sorting capacity | -0.6% | Western Europe | Medium term (2–4 years) |

| Skilled-labor shortages in dyeing, finishing, and advanced weaving | -0.5% | Germany, Italy, France | Long term (≥ 4 years) |

| Fragmented SME base complicating compliance with new EU due-diligence rules | -0.4% | Italy, Spain, Portugal | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatile Energy and Raw-Material Prices Squeezing Low-Margin Producers

Natural-gas costs peaked at USD 130 per MWh in early 2024 before sliding to USD 43 in late 2025, unsettling dyehouses where energy can reach 70% of operating costs. Crude swings of USD 10 per barrel drove 8% moves in polymer prices, while cotton futures oscillated between USD 75 and USD 95 per pound. SMEs without hedging tools saw margins evaporate, prompting asset sales in Poland and Romania. Cost-plus contracts that share risk remain rare outside deep partnerships. Price instability, therefore, threatens capacity and fuels consolidation.

High Capex Requirement for State-of-the-Art Recycling and Sorting Capacity

A 20,000-tonne fiber-to-fiber plant demands up to USD 87 million, including near-infrared sorting and chemical-depolymerization reactors. Banks insist on offtake deals and government co-investment, slowing project finance. Public grants worth USD 1.3 billion have been pledged but move slowly through permitting channels. SME operators cannot absorb USD 5 million AI-sorting lines, widening the technology gap. The funding hurdle will constrain recycled-fiber supply until at least 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Industrial Textiles Outpace Fashion’s Volume Base

In 2025, the fashion and apparel segment represented a significant majority of the overall Europe textile market, accounting for 56.06% of the total market size. The fastest-growing technical segment is forecast to clock a 6.15% CAGR through 2031, buoyed by electric-vehicle interiors, medical barrier fabrics, and geotextile reinforcement. German automakers used more than 12 kg of technical textiles per vehicle in 2025, up from 9 kg in 2020, to lighten battery platforms. Hospitals mandated ISO 16604-compliant drapes, expanding medical-textile contracts. Protective workwear profits from stricter flame-retardant rules, and sportswear integrates conductive yarns that capture biometric data, backed by 18% growth in smart-textile patents in 2024.

Premium fashion labels pivot to direct-to-consumer sites and store events, yet mid-market apparel grapples with ultra-fast competitors that post styles every two days. This bifurcation encourages mills to balance staple apparel orders with high-margin technical contracts. Regional production also realigns: Italy continues to anchor luxury shirting, while Germany and France lead technical-fabric R&D for automotive and aerospace partners. Over the forecast horizon, the Europe textile market will rely on industrial demand to offset slower apparel volumes.

By Raw Material: Polyester Leads Synthetic Resurgence

Synthetic fibers dominated with 53.96% of the Europe textile market share in 2025, and polyester alone is predicted to post a 6.56% CAGR to 2031. Glycolysis and methanolysis plants backed by Lenzing and Indorama plan to add 200,000 tonnes of recycled-polyester output by 2028, elevating circular content without sacrificing yarn strength. Nylon and acrylic hold niche positions in airbags and outdoor upholstery. Natural fibers remain stable in volume but shift toward certified premium grades; European mills pay 15–25% premiums for organic cotton to satisfy brand pledges. Locally grown flax and hemp supply chain security and lower emissions, aligning with the EU Green Deal. Specialty fibers such as aramid and ultra-high-molecular-weight polyethylene deliver margins up to five times higher than commodity polyester, attracting R&D and venture funding.

Pre-consumer cutting waste and post-consumer garments represent a small but fast-rising recycled-fiber pool. The EU waste-collection mandate could channel 5 million tonnes yearly into sorting hubs, yet blend complexity means only 20% can be recycled at scale today. Chemical-recycling investments aim to lift that rate over the decade, supporting recycled-content targets embedded in brand scorecards.

By Process: Non-Woven Innovation Challenges Woven Maturity

Woven fabrics still generated 48.36% of process-based revenue in 2025, but non-woven technologies are forecast to accelerate at a 6.05% CAGR between 2026 and 2031. Spunbond and meltblown lines added since 2024 serve HVAC filters and EN 14683 medical-barrier fabrics, riding sustained public-health awareness. Hydroentangled webs enjoy demand in household wipes for softness and absorbency, while needle-punched mats secure automotive carpeting contracts. Woven mills face Asian price pressure, pushing them to differentiate through jacquard designs and traceable yarns.

Digital warp-knit machines, capable of mass customization with near-zero waste, support on-demand fashion factories in Portugal and Spain. Three-dimensional weaving for spacer fabrics grew on the back of German and Swiss equipment breakthroughs that cut labor costs by 40%. Wet-laid non-wovens cater to battery separators and high-performance filters, commanding high unit value despite modest tonnage. Automation, robotic material handling, and AI vision inspection raise capex but reduce variable costs, advantaging vertically integrated groups.

Geography Analysis

Germany captured 25.45% of the Europe textile market size in 2025, driven by automotive and industrial-textile clusters in Baden-Württemberg and North Rhine-Westphalia. Close links to OEMs speed sample approval for seat covers, airbags, and battery housing fabrics. Federal apprenticeship programs combine craft skills with digital process control to ease labor shortages. Energy-efficiency grants help mills cut gas consumption in dyehouses.

Spain is the fastest-growing market with a 5.8% CAGR expected through 2031. Government incentives encourage the reshoring of cut-and-sew from North Africa, while EU recovery funds subsidize machinery upgrades. Proximity to Morocco and Tunisia allows flexible sourcing, and Spanish e-commerce brands rely on local mills to replenish micro-collections within days. Textile clusters in Catalonia and Valencia also pilot near-infrared sorting lines for post-consumer waste.

Italy retains a commanding position in luxury and technical fabrics. Lombardy mills supply premium shirting and merino knits, whereas Veneto focuses on carbon-fiber prepregs for aerospace. Patent filings surpassed 200 in 2024, the highest in Europe. France combines heritage fashion with non-woven innovation and dominates flax cultivation, exporting to mills across Belgium and the Netherlands. BENELUX countries excel in spunbond and circular-business pilots, while Nordic firms trial wood-based fibers. Central and Eastern European nations offer low-cost weaving capacity but face skilled-labor constraints and energy volatility.

Competitive Landscape

Competition remains fragmented; the ten largest producers hold under 30% combined share, giving the European textile market a low concentration profile. Commodity segments, basic apparel fabrics, and standard non-wovens battle shrinking margins due to Asian imports and energy swings. High-performance technical textiles and luxury fabrics, however, command premiums owing to proprietary know-how and brand partnerships.

Strategic moves center on vertical integration and circular scale-ups. Lenzing’s 2025 buyout of a chemical-recycling startup secures mono-ethylene glycol feedstock for lyocell lines. Indorama Ventures acquired a Spanish depolymerization plant capable of turning 30,000 tonnes of polyester waste into virgin-grade pellets, locking in recycled content for European yarns. Freudenberg teamed with a German OEM to co-develop aramid non-woven battery enclosures, targeting a 25% weight cut over steel.

Disruptors attack niches. Enzymatic-recycling startups promise lower-temperature depolymerization. Digital-knitting platforms accept orders as small as 100 meters, reducing inventory risk for fashion labels. Swiss research tie-ups produce conductive yarns that embed biometric sensors into garments, opening medical and sportswear channels. Compliance readiness is also a competitive lever: mills that implement Digital Product Passport data layers and AI-sorting ahead of 2025 waste rules will win supply contracts, while laggards risk disqualification.

Europe Textile Industry Leaders

-

Lenzing AG

-

Freudenberg Performance Materials

-

Indorama Ventures (M&G Fibras Europe)

-

Albini Group

-

Marzotto Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Lenzing allocated USD 163 million to add 50,000 tonnes of Tencel lyocell capacity in Austria, integrating 99% solvent recovery.

- December 2025: Freudenberg partnered with a German automaker on aramid-reinforced non-wovens for electric-vehicle battery enclosures.

- November 2025: Indorama Ventures bought a Spanish chemical-recycling plant that transforms 30,000 tonnes of polyester waste into virgin-equivalent pellets.

- October 2025: Albini Group launched a blockchain traceability platform aligned with the Digital Product Passport.

- September 2025: Marzotto upgraded wool-spinning in Italy with automation that cuts energy use by 30%.

Europe Textile Market Report Scope

The textile market encompasses the entire process from development and production to processing, manufacturing, and distribution of textile and fabric materials. It involves designing and producing yarn, clothing, and garments. Raw materials, including those derived from chemical sources, can be natural and synthetic.

The European textile market is segmented into application type, material type, process type, and region. By application type, the market is segmented into clothing, industrial/technical applications, and household applications. By material type, the market is segmented into cotton, jute, silk, synthetics, and wool. By process type, the market is segmented into woven and non-woven. By region, the market is segmented into Germany, France, Italy, Spain, the United Kingdom, and the rest of Europe. The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Application

| Fashion & Apparel |

| Industrial/Technical Textiles |

| Household & Home Textiles |

| Medical & Healthcare Textiles |

| Automotive & Transport Textiles |

| Others (Protective, Sports Textiles, etc.) |

By Raw Material

| Natural Fibers | Cotton |

| Wool | |

| Silk | |

| Synthetic Fibers | Polyester |

| Nylon | |

| Rayon / Viscose | |

| Acrylic | |

| Polypropylene | |

| Recycled Fibers | |

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) |

By Process / Technology

| Woven | |

| Knitted | |

| Non-woven | Spunlaid (Spunbond / Melt-blown) |

| Dry-laid Hydro-entangled | |

| Wet-Laid | |

| Needle-punched | |

| 3-D Weaving & Spacer Fabrics |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Application | Fashion & Apparel | |

| Industrial/Technical Textiles | ||

| Household & Home Textiles | ||

| Medical & Healthcare Textiles | ||

| Automotive & Transport Textiles | ||

| Others (Protective, Sports Textiles, etc.) | ||

| By Raw Material | Natural Fibers | Cotton |

| Wool | ||

| Silk | ||

| Synthetic Fibers | Polyester | |

| Nylon | ||

| Rayon / Viscose | ||

| Acrylic | ||

| Polypropylene | ||

| Recycled Fibers | ||

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) | ||

| By Process / Technology | Woven | |

| Knitted | ||

| Non-woven | Spunlaid (Spunbond / Melt-blown) | |

| Dry-laid Hydro-entangled | ||

| Wet-Laid | ||

| Needle-punched | ||

| 3-D Weaving & Spacer Fabrics | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How big is the Europe textile market in 2026?

The Europe textile market size reached USD 193.12 billion in 2026.

What is the expected CAGR for European textiles to 2031?

The overall market is forecast to grow at a 7.05% CAGR between 2026 and 2031.

Which segment is growing fastest within European textiles?

Industrial and technical textiles are projected to rise at a 6.15% CAGR, outpacing apparel.

Which raw material leads in market share?

Synthetic fibers dominate with 53.96% share, led by polyester.

Which EU country is the largest contributor by revenue?

Germany contributed 25.45% of regional revenue in 2025 thanks to its automotive cluster.

What regulatory change most affects circularity goals?

The mandatory separate collection of textile waste across the EU-27 starting in January 2025 drives investment in recycling infrastructure.

Page last updated on: